SuperATR 7-Step Profit - Strategy [presentTrading] Long time no see!

█ Introduction and How It Is Different

The SuperATR 7-Step Profit Strategy is a multi-layered trading approach that integrates adaptive Average True Range (ATR) calculations with momentum-based trend detection. What sets this strategy apart is its sophisticated 7-step take-profit mechanism, which combines four ATR-based exit levels and three fixed percentage levels. This hybrid approach allows traders to dynamically adjust to market volatility while systematically capturing profits in both long and short market positions.

Traditional trading strategies often rely on static indicators or single-layered exit strategies, which may not adapt well to changing market conditions. The SuperATR 7-Step Profit Strategy addresses this limitation by:

- Using Adaptive ATR: Enhances the standard ATR by making it responsive to current market momentum.

- Incorporating Momentum-Based Trend Detection: Identifies stronger trends with higher probability of continuation.

- Employing a Multi-Step Take-Profit System: Allows for gradual profit-taking at predetermined levels, optimizing returns while minimizing risk.

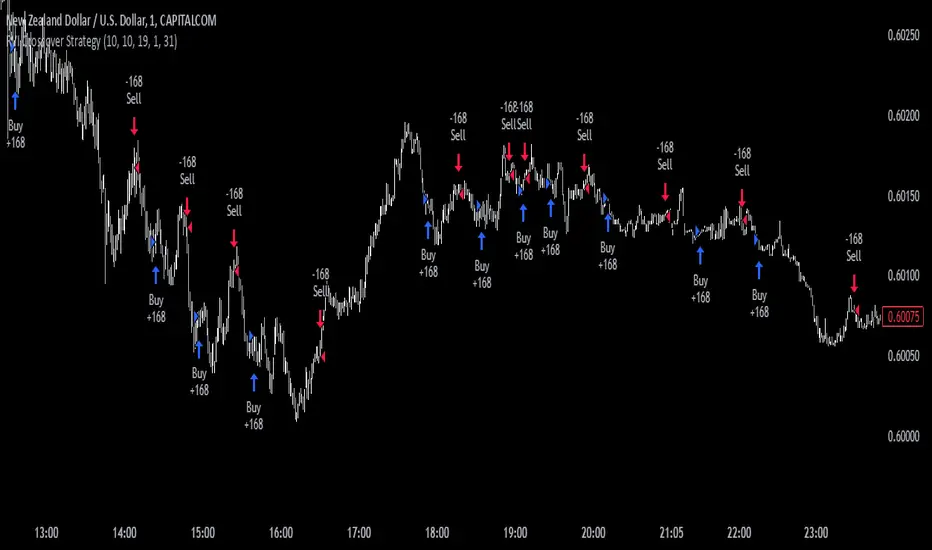

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy revolves around detecting strong market trends and capitalizing on them using an adaptive ATR and momentum indicators. Below is a detailed breakdown of each component of the strategy.

🔶 1. True Range Calculation with Enhanced Volatility Detection

The True Range (TR) measures market volatility by considering the most significant price movements. The enhanced TR is calculated as:

TR = Max

Where:

High and Low are the current bar's high and low prices.

Previous Close is the closing price of the previous bar.

Abs denotes the absolute value.

Max selects the maximum value among the three calculations.

🔶 2. Momentum Factor Calculation

To make the ATR adaptive, the strategy incorporates a Momentum Factor (MF), which adjusts the ATR based on recent price movements.

Momentum = Close - Close

Stdev_Close = Standard Deviation of Close over n periods

Normalized_Momentum = Momentum / Stdev_Close (if Stdev_Close ≠ 0)

Momentum_Factor = Abs(Normalized_Momentum)

Where:

Close is the current closing price.

n is the momentum_period, a user-defined input (default is 7).

Standard Deviation measures the dispersion of closing prices over n periods.

Abs ensures the momentum factor is always positive.

🔶 3. Adaptive ATR Calculation

The Adaptive ATR (AATR) adjusts the traditional ATR based on the Momentum Factor, making it more responsive during volatile periods and smoother during consolidation.

Short_ATR = SMA(True Range, short_period)

Long_ATR = SMA(True Range, long_period)

Adaptive_ATR = /

Where:

SMA is the Simple Moving Average.

short_period and long_period are user-defined inputs (defaults are 3 and 7, respectively).

🔶 4. Trend Strength Calculation

The strategy quantifies the strength of the trend to filter out weak signals.

Price_Change = Close - Close

ATR_Multiple = Price_Change / Adaptive_ATR (if Adaptive_ATR ≠ 0)

Trend_Strength = SMA(ATR_Multiple, n)

🔶 5. Trend Signal Determination

If (Short_MA > Long_MA) AND (Trend_Strength > Trend_Strength_Threshold):

Trend_Signal = 1 (Strong Uptrend)

Elif (Short_MA < Long_MA) AND (Trend_Strength < -Trend_Strength_Threshold):

Trend_Signal = -1 (Strong Downtrend)

Else:

Trend_Signal = 0 (No Clear Trend)

🔶 6. Trend Confirmation with Price Action

Adaptive_ATR_SMA = SMA(Adaptive_ATR, atr_sma_period)

If (Trend_Signal == 1) AND (Close > Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Elif (Trend_Signal == -1) AND (Close < Short_MA) AND (Adaptive_ATR > Adaptive_ATR_SMA):

Trend_Confirmed = True

Else:

Trend_Confirmed = False

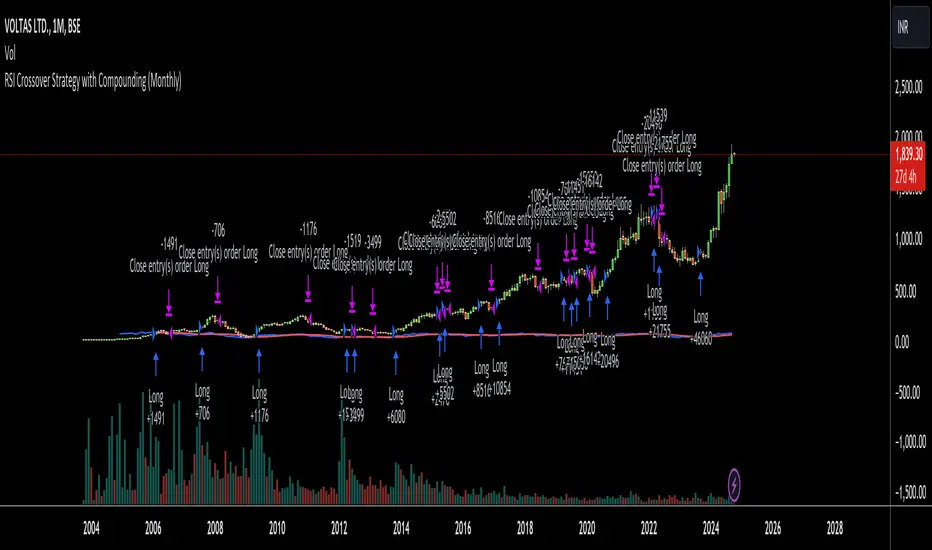

Local Performance

🔶 7. Multi-Step Take-Profit Mechanism

The strategy employs a 7-step take-profit system

█ Trade Direction

The SuperATR 7-Step Profit Strategy is designed to work in both long and short market conditions. By identifying strong uptrends and downtrends, it allows traders to capitalize on price movements in either direction.

Long Trades: Initiated when the market shows strong upward momentum and the trend is confirmed.

Short Trades: Initiated when the market exhibits strong downward momentum and the trend is confirmed.

█ Usage

To implement the SuperATR 7-Step Profit Strategy:

1. Configure the Strategy Parameters:

- Adjust the short_period, long_period, and momentum_period to match the desired sensitivity.

- Set the trend_strength_threshold to control how strong a trend must be before acting.

2. Set Up the Multi-Step Take-Profit Levels:

- Define ATR multipliers and fixed percentage levels according to risk tolerance and profit goals.

- Specify the percentage of the position to close at each level.

3. Apply the Strategy to a Chart:

- Use the strategy on instruments and timeframes where it has been tested and optimized.

- Monitor the positions and adjust parameters as needed based on performance.

4. Backtest and Optimize:

- Utilize TradingView's backtesting features to evaluate historical performance.

- Adjust the default settings to optimize for different market conditions.

█ Default Settings

Understanding default settings is crucial for optimal performance.

Short Period (3): Affects the responsiveness of the short-term MA.

Effect: Lower values increase sensitivity but may produce more false signals.

Long Period (7): Determines the trend baseline.

Effect: Higher values reduce noise but may delay signals.

Momentum Period (7): Influences adaptive ATR and trend strength.

Effect: Shorter periods react quicker to price changes.

Trend Strength Threshold (0.5): Filters out weaker trends.

Effect: Higher thresholds yield fewer but stronger signals.

ATR Multipliers: Set distances for ATR-based exits.

Effect: Larger multipliers aim for bigger moves but may reduce hit rate.

Fixed TP Levels (%): Control profit-taking on smaller moves.

Effect: Adjusting these levels affects how quickly profits are realized.

Exit Percentages: Determine how much of the position is closed at each TP level.

Effect: Higher percentages reduce exposure faster, affecting risk and reward.

Adjusting these variables allows you to tailor the strategy to different market conditions and personal risk preferences.

By integrating adaptive indicators and a multi-tiered exit strategy, the SuperATR 7-Step Profit Strategy offers a versatile tool for traders seeking to navigate varying market conditions effectively. Understanding and adjusting the key parameters enables traders to harness the full potential of this strategy.

Pine Script® Strategie