The Strat: 3-2D Setup Label + Entry, Target & AlertsThis is an indicator that identifies the 3-2D setup based on TheStrat & will alert you if you have this on the chart. Once the 3-2D setup happens this will give you the entry, target and price labels. You can change the font size, label colors and add optional alerts.

Indikatoren und Strategien

Trend Stress Quant [MarkitTick]💡This indicator combines a liquidity-based stress model with a dynamic linear regression channel to identify potential market exhaustion points and assess trend quality. By merging volume impact analysis with statistical deviation, this tool aims to highlight moments where price action may be overextended relative to the underlying liquidity conditions.

● Originality and Utility

Standard volatility indicators often rely solely on price range (like Bollinger Bands). This script introduces a Stress Engine that normalizes the relationship between Price Range (True Range) and Volume. This helps distinguish between healthy price movements and liquidity-stress events (illiquidity). Furthermore, instead of using a fixed-length channel, this tool offers a Dynamic Mode that anchors the regression channel to recent pivot points, ensuring the statistical analysis aligns with the current market structure rather than an arbitrary timeframe.

● Methodology

The script operates on two distinct mathematical models:

• Illiquidity Stress Engine

The core formula calculates a raw illiquidity metric based on the log-normal distribution of the ratio between True Range and Volume. A Z-Score (standard score) is then derived from this data over a specific lookback period. High Z-Scores indicate that price is moving disproportionately fast relative to the available volume, often a signature of panic selling or euphoric buying (exhaustion).

• Linear Regression Channel

The script calculates an Ordinary Least Squares (OLS) regression line (the line of best fit) to determine the mean price trend.

Standard Deviation Bands are plotted parallel to this mean.

Pearson Correlation Coefficient (R) is calculated to quantify the strength of the linear trend. Values closer to 1 or -1 indicate a strong trend, while values near 0 indicate a chaotic or ranging market.

📑 How to Use

Traders can utilize the visual outputs for mean reversion or trend continuation context:

• Exhaustion Signals (SE / BE Labels)

SE (Seller Exhaustion): Appears when the market is in a downtrend, but the Stress Engine detects a statistical anomaly (High Z-Score) on a down candle. This suggests panic selling may be peaking.

BE (Buyer Exhaustion): Appears when the market is in an uptrend, but the Stress Engine detects high stress on an up candle, suggesting a potential blow-off top.

• Regression Channel

The dashed middle line represents the fair value (mean) of the current trend.

The outer bands represent statistical extremes. Price interacting with the outer bands (default 2 Standard Deviations) while coincident with an Exhaustion Signal provides a high-confluence area of interest.

• Metrics Dashboard

A dashboard displays the current Trend Regime, Exhaustion Status, and Channel Width (volatility percentage).

● Settings

• Exhaustion Model

Trend Filter Length: Sets the baseline EMA to determine if the market is bullish or bearish.

Stress Threshold (Sigma): The Z-Score required to trigger an exhaustion signal (default is 2.0).

• Channel Configuration

Dynamic Pivot Mode: If enabled, automatically calculates the channel length based on recent pivots. If disabled, uses the Fixed Length.

Standard Deviations: Controls the width of the inner and outer channel bands.

📖This guide explains how to interpret and utilize signals for trading:

The script is designed primarily for Mean Reversion and Exhaustion trading strategies.

● The Core Strategy: Volatility Exhaustion

The script uses a "Stress Engine" to identify when price movement is statistically overextended relative to the available liquidity (Volume).

• Setup A: The "Seller Exhaustion" (Bullish Bounce)

Look for this setup during a downtrend to catch a temporary bottom or a reversal.

Trend Condition: The dashboard shows Bearish (Price is below the trend filter).

Trigger: The label SE (Seller Exhaustion) appears below a candle.

Why? This indicates that selling pressure was intense but likely panic-driven (High Z-Score/Stress) and may be drying up.

Confluence: Ideally, this signal appears when the price is touching or piercing the Lower Channel Band (dotted or solid lines).

Action: Traders often use this as a signal to close Short positions or enter a speculative Long (counter-trend) targeting the middle line.

• Setup B: The "Buyer Exhaustion" (Bearish Pullback)

Look for this setup during an uptrend to catch a local top.

Trend Condition: The dashboard shows Bullish .

Trigger: The label BE (Buyer Exhaustion) appears above a candle.

Why? This indicates euphoric buying on low liquidity or extreme volatility that is statistically unsustainable.

Confluence: Look for price rejection at the Upper Channel Band.

Action: Traders often use this to close Long positions or enter a Short targeting the mean.

● The Filter: Trend & Correlation

The script includes a Linear Regression Channel that quantifies the quality of the trend.

• Channel Slope

If the channel is angling steeply up or down, the trend is strong.

• Pearson R (Correlation)

The script calculates the Pearson R coefficient.

Weak Correlation: If the channel turns Gray/Neutral (or the fill becomes weak), it means the correlation is below the threshold (default 0.5).

Trading Rule: Avoid trading exhaustion signals when the channel is Gray/Neutral, as the market is likely chopping sideways with no clear direction.

● Risk Management & Targets

• Stop Loss

Since this is a volatility tool, a common technique is to place stops just outside the Outer Deviation Band (the widest line). If price expands beyond the outer band with no exhaustion signal, the trend may be entering a "runaway" phase.

• Take Profit

Target 1: The Middle Regression Line (The dashed center line). Prices tend to revert to this mean after an exhaustion event.

Target 2: The opposite channel band (e.g., if you bought at the bottom, hold until the top).

● Summary of Dashboard Metrics

The table on your chart provides a quick snapshot:

Trend Regime: Tells you if you should fundamentally look for Shorts (Bearish) or Longs (Bullish).

Seller/Buyer Status: Alerts you if the current bar is EXHAUSTED or Normal .

Channel Width %: Indicates volatility. If the width is very low (percentage is small), a breakout might be imminent (squeezing). If high, be careful of chop.

⚙️ Indicator settings

• Signal Parameters

Exhaustion & Stress Model: Controls signal sensitivity.

Trend Filter: Decides if the market is Bullish or Bearish.

Stress Threshold (Sigma): Higher values (e.g., 2.5) make the script stricter, showing fewer but potentially stronger signals.

• Channel Configuration

Dynamic Pivot Mode: If ON, the channel length auto-adjusts to recent market pivots. If OFF, it uses the Fixed Length you set.

Channel Bands: Adjusts the channel width.

Outer Deviation: The boundary for "extreme" moves. Price hitting this often signals a reversal.

• Quality Filter

Filter Weak Correlations: If enabled, the channel turns gray during choppy/sideways markets to warn you not to trust trend signals.

• Visuals

Display Options: Toggles the "Stats" dashboard and adjusts volatility coloring.

● Disclaimer

All provided scripts and indicators are strictly for educational exploration and must not be interpreted as financial advice or a recommendation to execute trades. I expressly disclaim all liability for any financial losses or damages that may result, directly or indirectly, from the reliance on or application of these tools. Market participation carries inherent risk where past performance never guarantees future returns, leaving all investment decisions and due diligence solely at your own discretion.

Dragon Flow Arrows (LITE)🚀 DRAGON FLOW ARROWS | Smart Trend Engine + Clean Reversal Arrows

A lightweight but highly-optimized trend system designed for clean charts, powerful visual signals, and no-noise directional flow. Built for traders who want simplicity, clarity, and professional-level momentum-filtered signals without over-complication.

🔥 Dragon Channel (Clean 3-Line Ribbon)

A smooth adaptive channel formed from ATR + EMA, giving you structural trend zones without clutter.

✅ Dragon Flow Gradient

A horizontal, color-shifted flow:

🟢 Bull flow → green glow

🔴 Bear flow → red glow

Automatic blend based on trend direction

Smooth visual transitions (no vertical stripes)

✅ Momentum-Filtered Arrows

BUY/SELL arrows only print when:

Price breaks outside the Dragon Channel

Momentum confirms (RSI + MACD filters)

Trend flips → one clean arrow per direction

✅ Smart Header Panel

At the top of your chart:

📌 Trend: Uptrend / Downtrend / Neutral

⚡ Impulse Strength: Weak / Normal / Strong

📊 How to Use

Entry:

- BUY Setup

Price moving above baseline

Dragon Flow turns bullish (cyan side)

Arrow appears below channel

- SELL Setup

Price breaks below baseline

Dragon Flow turns bearish (magenta side)

Arrow pops above channel

Exit / Filter:

Opposite arrow

Flow color shift

Trend panel flips

Works on Forex, Crypto, Stocks, Indices — all timeframes (just adjust the channel length).

Happy trading!

Trinity Multi-Timeframe CCITrinity Multi-Timeframe CCI Indicator

This Pine Script indicator is a powerful **multi-timeframe Commodity Channel Index (MTF CCI)** tool that displays three CCI lines on a single pane:

- **Current timeframe** (whatever chart you're viewing, e.g., 1h, 15m, etc.)

- **4-hour timeframe**

- **Daily timeframe**

All three use the same CCI length (default 20, adjustable) and are fully customizable—you can enable/disable each line, change its timeframe, color, and thickness. Horizontal levels at 0 (dashed white by default), +100 (red), and -100 (green) are also included and fully editable.

### Core Functionality & Visual Signals

The standout feature is the **dynamic coloring of the current timeframe CCI line**:

- **Green**: Strong **bullish alignment**. This occurs when **all three CCIs are above the zero line** AND the current timeframe CCI is the **highest** of the three (leading the move upward with higher-timeframe confirmation).

- **Red**: Strong **bearish alignment**. This occurs when **all three CCIs are below the zero line** AND the current timeframe CCI is the **lowest** of the three (leading the move downward with higher-timeframe confirmation).

- **Yellow**: Neutral or no clear alignment (default state when the above conditions aren't met).

An optional light background shading (green or red) highlights when the indicator is in a bullish or bearish state.

Small triangle markers appear on the pane when a new bullish or bearish alignment forms, and built-in alerts notify you of new signals or when a signal ends. These are editable to enable or disable.

### How Traders Can Use It

This indicator helps identify **high-probability trend continuations or reversals** by combining momentum (CCI) across multiple timeframes with alignment confirmation:

- **Trend-following entries**: A green current line (especially with a fresh alert) suggests strong upward momentum backed by higher timeframes—ideal for long entries or adding to positions in an uptrend.

- **Bearish entries/short setups**: A red current line signals strong downward momentum confirmed across timeframes—good for short entries or exiting longs.

- **Confluence filter**: Use it as a filter for other strategies. Only take trades in the direction of the alignment (e.g., only long if current line is green).

- **Early warning of weakness**: When the current line turns yellow after being green/red, it often signals the trend is losing multi-timeframe support—useful for tightening stops or taking partial profits.

In essence, it visually answers the question: “Is the short-term momentum not only strong, but also aligned with and leading the medium- and long-term momentum?” When the answer is yes (green or red), it highlights moments of **multi-timeframe confluence**—some of the most reliable setups in technical trading.

The alerts make it practical for active traders: you get notified the moment a strong aligned signal appears, without needing to watch the chart constantly.

It's clean, highly customizable, and focuses on one clear concept—**multi-timeframe CCI leadership**—making it excellent for trend, swing, and even intraday traders looking for higher-timeframe confirmation.

Gaps IdentifierThis indicator identifies up and down Gaps using previous period's close price to the next period's open price. Potentially useful for Gap rebound strategies.

(Will identify gaps 4%–11% by default; can change in settings)

Gemini Smart SMA Pro + Wyckoff V2 (Enhanced Cloud)The Smart SMA Pro + Wyckoff V2 is an advanced trend-following and market-cycle indicator built for traders who utilize Wyckoff Theory and Volume Spread Analysis (VSA). It is specifically designed to identify the transition from "Cause" (Squeeze/Accumulation) to "Effect" (Expansion/Markup).

By analyzing the volatility spread between two customizable Moving Averages and validating movements with relative volume, this tool helps traders stay out of sideways markets and enter only when high-conviction momentum is present.

Key Features

Wyckoff Phase Detection: Automatically detects Squeeze (Accumulation/Distribution) and Expansion (Markup/Markdown) phases.

Intelligent Dynamic Cloud: The cloud between the MAs changes its transparency dynamically based on the Volume Ratio and trend slope. Darker colors indicate high-volume trend confirmation.

Dual-Layered SOS/SOW Signals: * SOS (Sign of Strength): A Yellow Dot appears on a bullish squeeze breakout. A Yellow Arrow is added only if the move is validated by High Relative Volume.

SOW (Sign of Weakness): An Orange Dot appears on a bearish breakout, with an Orange Arrow appearing only if supported by high volume.

Live Multi-Data Dashboard: A real-time table displaying the status of Fast/Slow MAs, the current market cycle stage, and the Volume Ratio.

Professional Alerts: Built-in alerts for Sign of Strength (SOS) and Sign of Weakness (SOW) breakouts.

How to Trade with it

Grey Cloud (Squeeze): Market is building a "Cause." Avoid trading and prepare for a breakout.

Yellow Dot + Arrow: This is a Confirmed SOS. It indicates institutional participation and a high probability of a new Markup phase.

Buy/Sell Labels: Standard trend entries based on price crossing the Signal Line (Fast MA). Use these to join an already established trend.

Dashboard Monitoring: Check the "Vol. Ratio" to see if the current move has enough strength to sustain the expansion.

How this Indicator was Created

This project is the result of a cutting-edge collaborative development process between a human trader and Gemini (Google’s AI).

Logic Synthesis: We combined traditional technical analysis with AI-optimized algorithms to calculate the Volatility Ratio, ensuring the "Squeeze" detection is more accurate than standard Bollinger-based tools.

Conditional Visuals: The logic was refined through multiple iterations to create a "Smart Visual" system. For instance, the Volume-Validated Arrow was an architectural decision to separate minor breakouts from high-conviction institutional moves.

Code Optimization: The entire script was written in Pine Script® V6, ensuring maximum performance, low latency on charts, and a clean, responsive Dashboard interface using advanced table objects.

----------------------------------------------------------------------------------------------------------------------------------------------------

The Partnership: This indicator represents the perfect synergy between human market intuition and AI’s computational precision, resulting in a tool that is both mathematically sound and visually intuitive for professional use.

Advanced Multi-Level S/R ZonesAdvanced Multi-Level S/R Zones: The Comprehensive Guide

1. Introduction: The Evolution of Support & Resistance:

Support and Resistance (S/R) is the backbone of technical analysis. However, traditional methods of drawing these levels are often plagued by subjectivity. Two traders looking at the same chart will often draw two different lines. Furthermore, standard indicators often treat every price point equally, ignoring the critical context of Volume and Time.

The Advanced Multi-Level S/R Zones script represents a paradigm shift. It moves away from subjective line drawing and toward Quantitative Zoning. By utilizing statistical measures of variability (Standard Deviation, MAD, IQR) combined with Volume-Weighting and Time-Decay algorithms, this tool identifies where price is mathematically most likely to react. It treats S/R not as thin lines, but as dynamic zones of probability.

2. Core Logic and Mathematical Foundation:

To understand how to use this tool optimally, one must understand the "engine" under the hood. The script operates on four distinct pillars of logic:

A. Session-Based Data Collection:

The script does not look at every single tick. Instead, it aggregates data into "Sessions" (daily bars by default logic). It extracts the High, Low, and Total Volume for every session within the user-defined lookback period. This filters out intraday noise and focuses on the macro structure of the market.

B. Adaptive Statistical Variability:

Most Bollinger Band-style indicators use Standard Deviation (StdDev) to measure width. However, StdDev is heavily influenced by outliers (extreme wicks). This script offers a sophisticated Adaptive Method-Skewness Detection: The script calculates the skewness of the price distribution. Adaptive Selection: If the data is highly skewed (lots of outliers, typical in Crypto), it switches to MAD (Median Absolute Deviation). MAD is robust and ignores outliers. If the data is moderately skewed, it uses IQR (Interquartile Range). If the data is normal (Gaussian), it uses StdDev.

Benefit: This ensures the zone widths are accurate regardless of whether you are trading a stable Forex pair or a volatile Altcoin.

C. The Weighting Engine (Volume + Time)

Not all price history is equal. This script assigns a "Weight Score" to every session based on two factors:

Volume Weighting: Sessions with massive volume (institutional activity) are given higher importance. A high formed on low volume is less significant than a high formed on peak volume.

Time Decay: Recent price action is more relevant than price action from 50 bars ago. The script applies a decay factor (default 0.85). This means a session from yesterday has 100% impact, while a session from 10 days ago has significantly less influence on the zone calculation.

D. Clustering Algorithm

Once the data is weighted, the script runs a clustering algorithm. It looks for price levels where multiple session Highs (for Resistance) or Lows (for Support) congregate.

It requires a minimum number of points to form a zone (User Input: minPoints).

It merges nearby levels based on the Cluster Separation Factor.

This results in "Primary," "Secondary," and "Tertiary" zones based on the strength and quantity of data points in that cluster.

3. Detailed Features and Inputs Breakdown:

Group 1: Main Settings

Lookback Sessions (Default: 10): Defines how far back the script looks for pivots. A higher number (e.g., 50) creates long-term structural zones. A lower number (e.g., 5) creates short-term scalping zones.

Variability Method (Adaptive): As described above, leave this on "Adaptive" for the best results across different assets.

Zone Width Multiplier (Default: 0.75): Controls the vertical thickness of the zones. Increase this to 1.0 or 1.5 for highly volatile assets to ensure you catch the wicks.

Minimum Points per Zone: The strictness filter. If set to 3, a price level must be hit 3 times within the lookback to generate a zone. Higher numbers = fewer, but stronger zones.

Group 2: Weighting

Volume-Weighted Zones: Crucial for identifying "Smart Money" levels. Keep this TRUE.

Time Decay: Ensures the zones update dynamically. If price moves away from a level for a long time, the zone will fade in significance.

ATR-Normalized Zone Width: This is a dynamic volatility filter. If TRUE, the zone width expands and contracts based on the Average True Range. This is vital for maintaining accuracy during market breakouts or crashes.

Group 3: Zone Strength & Scoring

The script calculates a "Score" (0-100%) for every zone based on:

-Point Count: More hits = higher score.

-Touches: How many times price wicked into the zone recently.

-Intact Status: Has the zone been broken?

-Weight: Volume/Time weight of the constituent points.

-Track Zone Touches: Looks back n bars to see how often price respected this level.

-Touch Threshold: The sensitivity for counting a "touch."

Group 4: Visuals & Display

Extend Bars: How far to the right the boxes are drawn.

Show Labels: Displays the Score, Tier (Primary/Secondary), and Status (Retesting).

Detect Pivot Zones (Overlap): This is a killer feature. It detects where a Support Zone overlaps with a Resistance Zone.

Significance: These are "Flip Zones" (Old Resistance becomes New Support). They are colored differently (Orange by default) and represent high-probability entry areas.

Group 5: Signals & Alerts

Entry Signals: Plots Buy/Sell labels when price rejects a zone.

Detect Break & Retest: specifically looks for the "Break -> Pullback -> Bounce" pattern, labeled as "RETEST BUY/SELL".

Proximity Alert: Triggers when price gets within x% of a zone.

4. Understanding the Visuals (Interpreting the Chart)

When you load the script, you will see several visual elements. Here is how to read them:

The Boxes (Zones)

Red Shades: Resistance Zones.

Dark Red (Solid Border): Primary Resistance. The strongest wall.

Lighter Red (Dashed Border): Secondary/Tertiary. Weaker, but still relevant.

Green Shades: Support Zones.

Dark Green (Solid Border): Primary Support. The strongest floor.

Orange Boxes: Pivot Zones. These are areas where price has historically reacted as both support and resistance. These are the "Line in the Sand" for trend direction.

The Labels & Emojis

The script assigns emojis to zone strength:

🔥 (Fire): Score > 80%. A massive level. Expect a strong reaction.

⭐ (Star): Score > 60%. A solid structural level.

✓ (Check): Score > 40%. A standard level.

"⟳ RETESTING": Appears when a zone was broken, and price is currently pulling back to test it from the other side.

The Dashboard (Top Right)

A statistics table provides a "Head-Up Display" for the asset:

High/Low σ (Sigma): The variability of the highs and lows. If High σ is much larger than Low σ, it implies the tops are erratic (wicks) while bottoms are clean (flat).

Method: Shows which statistical method the Adaptive engine selected (e.g., "MAD (auto)").

ATR: Current volatility value used for normalization.

5. Strategies for Optimum Output

To get the most out of this script, you should not just blindly follow the lines. Use these specific strategies:

Strategy A: The "Zone Fade" (Range Trading)

This works best in sideways markets.

Identify a Primary Support (Green) and Primary Resistance (Red).

Wait for price to enter the zone.

Look for the "SUPPORT BOUNCE" or "RESISTANCE REJECTION" signal label.

Entry: Enter against the zone (Buy at support, Sell at resistance).

Stop Loss: Place just outside the zone width. Because the zones are calculated using volatility stats, a break of the zone usually means the trade is invalid.

Strategy B: The "Pivot Flip" (Trend Following)

This is the highest probability setup in trending markets.

Look for an Orange Pivot Zone.

Wait for price to break through a Resistance Zone cleanly.

Wait for the price to return to that zone (which may now turn Orange or act as Support).

Look for the "RETEST BUY" label.

Logic: Old resistance becoming new support is a classic sign of trend continuation. The script automates the detection of this exact geometric phenomenon.

Strategy C: The Volatility Squeeze

Look at the Dashboard. Compare High σ and Low σ.

If the values are dropping rapidly or becoming very small, the zones will contract (become narrow).

Narrow zones indicate a "Squeeze" or compression in price.

Prepare for a violent breakout. Do not fade (trade against) narrow zones; look to trade the breakout.

6. Optimization & Customization Guide

Different markets require different settings. Here is how to tune the script:

For Crypto & Volatile Stocks (Tesla, Nvidia)

Method: Set to Adaptive (Mandatory, as these assets have "Fat Tails").

Multiplier: Increase to 1.0 - 1.25. Crypto wicks are deep; you need wider zones to avoid getting stopped out prematurely.

Lookback: 20-30 sessions. Crypto has a long memory; short lookbacks generate too much noise.

For Forex (EURUSD, GBPJPY)

Method: You can force StdDev or IQR. Forex is more mean-reverting and Gaussian.

Multiplier: Decrease to 0.5 - 0.75. Forex levels are often very precise to the pip.

Volume Weighting: You may turn this OFF for Forex if your broker's volume data is unreliable (since Forex has no centralized volume), though tick volume often works fine.

For Scalping (1m - 15m Timeframes)

Lookback: Decrease to 5-10. You only care about the immediate session history.

Decay Factor: Decrease to 0.5. You want the script to forget about yesterday's price action very quickly.

Touch Lookback: Decrease to 20 bars.

For Swing Trading (4H - Daily Timeframes)

Lookback: Increase to 50.

Decay Factor: Increase to 0.95. Structural levels from weeks ago are still highly relevant.

Min Points: Increase to 3 or 4. Only show levels that have been tested multiple times.

7. Advantages Over Standard Tools:

Feature Standard S/R Indicator, Advanced Multi-Level S/R Calculation, Uses simple Pivots or Fractals, Uses Statistical Distributions (MAD/IQR). Zone Width Arbitrary or Fixed Adaptive based on Volatility & ATR.

Context Ignores Volume Volume Weighted (Smart Money tracking).

Time Relevance Old levels = New levels Time Decay (Recency bias applied).

Overlaps Usually ignores overlaps Detects Pivot Zones (Res/Sup Flip).

Scoring None 0-100% Strength Score per zone.

8. Conclusion:

The Advanced Multi-Level S/R Zones script is not just a drawing tool; it is a statistical analysis engine. By accounting for the skewness of data, the volume behind the moves, and the decay of time, it provides a strictly objective roadmap of the market structure.

For the optimum output, combine the Pivot Zone identification with the Retest Signals. This aligns you with the underlying flow of order blocks and prevents trading against the statistical probabilities of the market.

The Strat Candle Labels & Color Inc F2D F2UThis script uses TheStrat candle numbers 1, 2D, 2U, 3 and places the text below or above. I have also now added the Failed 2D/2U labels. You can also change the text size. This also allows you to change the colors of the candles with two options for the 1 & 3 so you can color them in the direction they are going. For example a 1 that is green can be green and a 1 that is red can be red.

Multi-Timeframe Market Structure [MattyBTradez]Provides a Bullish or Bearish analysis based on market structure for the 1M, 5M, 15M, 30M, 1H, 4H, and 1D timeframes.

Early Trend Warning Using MTF AnalysisAs an active trader and software professional, I build my own indicators. I built this one today which I want to share with fellow traders.

If you are a trend trader then HTF/MTF analysis is very critical. It is virtually impossible to constantly track multiple tickers all the time. One should not take a buy trade when MTF is bearish and vice versa. This indicator solves this problem.

The EMA Trend Warning indicator helps traders detect potential trend changes early by analyzing price interactions with multi-timeframe Exponential Moving Averages (EMAs) and their momentum. It sends instant alerts when price crosses above or below EMAs with supporting momentum, making it easier to capture bullish or bearish moves.

The EMA Trend Warning indicator detects potential trend changes by monitoring price against 14-period EMAs on multiple timeframes: 15-minute, 30-minute, and 1-hour charts. It sends alerts when the price crosses above or below the EMA with supporting momentum, helping traders identify early bullish or bearish signals.

How It Works:

1. Calculates 14-period EMA on 15m, 30m, and 1H charts.

2. Computes EMA slopes to determine momentum direction.

3. BUY alert triggers when price crosses above the 15m EMA and at least one EMA slope is upward.

4. SELL alert triggers when price crosses below the 15m EMA and at least one EMA slope is downward.

5. Alerts fire once per bar and track previous state to avoid repeated notifications.

Features:

1. Multi-timeframe EMA monitoring.

2. Momentum confirmation with EMA slopes.

3. Instant BUY/SELL alerts.

4. Tracks previous trend state to prevent alert spam.

Benefits:

1. Detects trend changes early for better entry timing.

2. Confirms trend across multiple timeframes.

3. Saves time with automated alerts.

4. Helps traders align trades with market momentum.

Please consider this indicator as EARLY WARNING ONLY. Take trade based on multiple confluences post receiving any warning. I have tested it on BTCUSD since yesterday, multiple warning alerts were 100% perfect.

SMC Post-Analysis Lab [PhenLabs]📊 SMC Post-Analysis Lab

Version: PineScript™ v6

📌 Description

The SMC Post-Analysis Lab is a dedicated hindsight analysis tool built for traders who want to understand what really happened during any historical trading period. Unlike forward-looking indicators, this tool lets you scroll back through time and instantly receive algorithmic classification of market states using Smart Money Concepts methodology.

Whether you’re reviewing a losing trade, studying a successful session, or building your pattern recognition skills, this indicator provides immediate context. The expansion-aware algorithm processes price action within your selected window and outputs clear, actionable classifications ranging from Parabolic Expansion to Consolidation Inducements.

Stop relying on subjective post-trade analysis. Let the algorithm objectively tell you whether institutional players were accumulating, distributing, or running inducements during your trades.

🚀 Points of Innovation

First indicator specifically designed for SMC-based post-trade review rather than live signal generation

Dual-mode analysis system allowing both dynamic scrollback and precise date selection

Expansion-aware classification algorithm that weighs range position against net displacement

Real-time efficiency metrics calculating directional quality of price movement

Integrated visual FVG detection within the analysis window only

Interactive table with clickable date range adjustment via chart interface

🔧 Core Components

Pivot Detection Engine: Uses configurable pivot length to identify significant swing highs and lows for structure break detection

Window Calculator: Determines active analysis zone based on either bar offset or timestamp boundaries

Data Aggregator: Tracks window open, high, low, close and counts bullish/bearish structure break events

State Classification Algorithm: Applies hierarchical logic to determine market state from six possible classifications

Visual Renderer: Draws structure breaks, FVG boxes, and window highlighting within the active zone

🔥 Key Features

Sliding Window Mode: Use the Scroll Back slider to dynamically move your analysis zone backwards through history bar-by-bar

Date Range Mode: Select specific start and end timestamps for precise session or trade review

Six Market State Classifications: Parabolic Expansion (Bull/Bear), Bullish/Bearish Order Flow, Accumulation/Distribution Reversal, and Consolidation/Inducement

Range Position Percentile: See exactly where price closed relative to the window’s high-low range as a percentage

Bull/Bear Event Counter: Quantified count of structure breaks in each direction during the analysis period

Efficiency Calculation: Net move divided by total range reveals trending quality versus chop

🎨 Visualization

Blue Window Highlight: Active analysis zone is clearly marked with blue background shading on the chart

Structure Break Lines: Dashed lines appear at each bullish or bearish structure break within the window

FVG Boxes: Fair Value Gaps automatically render as semi-transparent boxes in bullish or bearish colors

Dashboard Table: Top-right positioned table displays State, Analysis description, and Metrics in real-time

Color-Coded States: Each classification uses distinct coloring for immediate visual recognition

Interactive Tip Row: Optional help text guides users on clicking the table to adjust date range

📖 Usage Guidelines

General Configuration

Analysis Mode: Default is Sliding Window. Choose Date Range for specific timestamp analysis.

Sliding Window Settings

Scroll Back (Bars): Default 0. Increase to move window backwards into history.

Window Width (Bars): Default 100. Range 20-50 for scalping, 100+ for swing analysis.

Date Range Settings

Start Date: Select the beginning timestamp for your analysis period.

End Date: Select the ending timestamp for your analysis period.

Visual Settings

Show Help Tip: Default true. Toggle to hide instructional row in dashboard.

Bullish Color: Default teal. Customize for bullish elements.

Bearish Color: Default red. Customize for bearish elements.

SMC Parameters

Pivot Length: Default 5. Lower values (3-5) catch minor breaks. Higher values (10+) focus on major swings.

✅ Best Use Cases

Post-trade review to understand why entries succeeded or failed

Session analysis to identify institutional activity patterns

Trade journaling with objective algorithmic classifications

Pattern recognition training through historical scrollback

Identifying whether stop hunts were inducements or legitimate breaks

Comparing your real-time read versus what the algorithm detected

⚠️ Limitations

Designed for historical analysis only, not live trade signals

Classification accuracy depends on appropriate pivot length for the timeframe

FVG detection uses simple gap logic without mitigation tracking

State classification is based on window data only, not broader context

Requires manual scrolling or date input to review different periods

💡 What Makes This Unique

Purpose-Built for Review: Unlike most indicators focused on live signals, this is designed specifically for post-trade analysis

Expansion-Aware Logic: Algorithm weighs both position in range AND directional efficiency for accurate state detection

Interactive Date Control: Click the dashboard table to reveal draggable anchors for window adjustment directly on chart

🔬 How It Works

1. Window Definition:

User selects either Sliding Window or Date Range mode

System calculates which bars fall within the active analysis zone

Active zone receives blue background highlighting

2. Data Collection:

Algorithm captures window open, running high, running low, and current close

Structure breaks are detected when price crosses above last pivot high or below last pivot low

Bullish and bearish events are counted separately

3. State Classification:

Range Position calculates where close sits as percentage of high-low range

Efficiency calculates net move divided by total range

Hierarchical logic applies priority rules from Parabolic states down to Consolidation

4. Output Rendering:

Dashboard table updates with State title, Analysis description, and Metrics

Visual elements render within window only to keep chart clean

Colors reflect bullish, bearish, or neutral classification

💡 Note:

This indicator is intended for educational and review purposes. Use it to develop your understanding of Smart Money Concepts by analyzing what institutional order flow looked like during historical periods. Combine insights with your own analysis methodology for best results.

rosh Swift ALGO-X based on ema for xauusd scalping use with original settings, assured 100 pips per day

CCI Standard DeviationCCI Standard Deviation – Asymmetric Volatility-Adjusted Trend Filter (CCI SD)

The Commodity Channel Index (CCI), created by Donald Lambert in 1980, measures how far the typical price deviates from its statistical average to identify cyclical momentum and trend strength.

The standard formula is:

CCI = (Typical Price − SMA(Typical Price, n)) / (0.015 × Mean Deviation)

where Typical Price = (High + Low + Close)/3.

CCI is unbounded and centered around zero: sustained readings above zero indicate bullish momentum, below zero bearish. Classic interpretations often use zero-line crosses or fixed levels (±100, ±200, ±250), but these can be unreliable when CCI volatility changes across market regimes.

This indicator was developed to create a more disciplined trend-following tool that aligns with my core risk principle: “always protect to the downside.”

Starting from the standard CCI zero-line concept for trend direction, I experimented with standard deviation bands to make the oscillator volatility-adjusted. I then applied deliberate asymmetry: requiring the lower 1σ envelope (CCI − stdev) to cross above a positive threshold for bullish confirmation (high-probability entry only in robust trends), while exiting immediately on any raw CCI weakness below a negative threshold (quick downside protection). User inputs for both thresholds were added to allow fine-tuning and adaptability across different assets and timeframes.

An optional DEMA-smoothed version of the lower envelope provides additional clarity when desired.

Extreme zones

raw CCI ±240 and lower envelope > 200 or < –200 - are highlighted with background shading to flag rare acceleration or capitulation phases.

How it works

Standard CCI calculated on typical price (default length 38).

Rolling standard deviation of the CCI itself (default length 13) measures the oscillator’s recent volatility.

Lower envelope = CCI − stdev (dn).

Optional DEMA smoothing (default length 12) can be toggled.

Trend logic:

Bullish regime only when lower envelope

→ Long Threshold (default +10)

→ statistical proof of strength

Bearish/neutral immediately when raw CCI

→ Short Threshold (default –25)

→ fast downside protection

Origin and development

The indicator emerged from wanting a cleaner, more reliable CCI for trend direction. After testing volatility-adjusted versions, the asymmetric design proved superior:

it enters only high-conviction uptrends and exits rapidly on weakness, significantly reducing whipsaws while preserving trend capture.

Parameters were optimized through extensive backtests on major assets (BTC, ETH, SOL and many more Cryptos; Magnificent 7 stocks, QQQ, SPX, gold).

The defaults were selected for the best average Sortino ratio and lowest maximum drawdown across this broad universe, ensuring robustness and avoiding single-asset overfitting.

How to use it

Green triangle below bar

→ lower envelope crosses above Long Threshold

→ high-conviction bullish trend confirmed

→ enter or add to longs

Magenta triangle above bar

→ CCI crosses below Short Threshold

→ exit longs or go cash/short

While lower envelope remains above Long Threshold

→ hold bullish positions

Extreme background shading (dn >200 or CCI ±240)

→ rare high-attention zones (potential acceleration or exhaustion)

Recommended defaults

CCI length: 38

SD length: 13

Long threshold: +10

Short threshold: –25

Optional MA length: 12 (DEMA of lower envelope)

All visual elements (bar coloring, signals, background, smoothed line) are toggleable for personal preference.

This indicator is designed as a trend-strength and risk-management filter and is not intended as a standalone trading system.

Disclaimer:

This is not financial advice. Backtests are based on past results and are not indicative of future performance.

High/Low ARDR-ADR-WDRR-DDR V1Tracks the high and Low in 4 different tIme Frames

ARDR-ADR-WDRR-DDR

-You can set your own time frames

-Display lines or boxes

-Each line can have its own label

-Set own colors and linestyles

-Each box can also have their own lines at 75%, 50% and 25% of the box if that's needed

-Toggle wich session to display

-Toggle to auto extend untill Extended time

-Toggle to live update lines/boxes during live priceaction or to display the lines / boxes after the End Time

DDR lines have no history, so after 15:55 the DDR lines disappear and gets drawn again the next day starting at 04:00.

Happy Trading!!

ChromaFlows Momentum Index | LUPENIndicator Guide: ChromaFlows Momentum Index

Overview

The ChromaFlows Momentum Index is a next-generation momentum oscillator designed to filter out market noise and visualize pure trend strength. Unlike traditional indicators that often give conflicting signals, ChromaFlows uses a Consensus Algorithm. It simultaneously analyzes three distinct engines—RSI, Fast Stochastic, and Slow Stochastic—and only lights up when they all agree on the market direction.

The result is a fluid, glowing "Wave" that provides an immediate visual read on market sentiment:

Green Glow: Strong Bullish Consensus (Safe to buy/hold).

Red Glow: Strong Bearish Consensus (Safe to sell/short).

Gray/Neutral: Indecision or Choppy Market (Stay out or tread carefully).

Key Visual Components

1. The Gradient Wave (Main Oscillator)

This is the heartbeat of the indicator. It is usually based on the Slow Stochastic (customizable in settings) but its color is determined by the Consensus Logic.

How to read it: The higher the wave, the more overbought; the lower, the more oversold. However, pay attention to the Glow Intensity. A bright, solid color indicates all underlying indicators are aligned.

2. The SMI Line (Gold Line)

Overlaid on the wave is the SMI (Stochastic Momentum Index) Blau line. This acts as a fast-moving "Signal Line".

Usage: Watch for how this line interacts with the main wave. It leads price action and often signals reversals before they happen.

3. Signal Arrows (Triangles on the Wave)

▲ Cyan Triangle: SMI Crossover UP. This occurs when the Main Wave crosses above the SMI Signal line. This is a potential Long Entry.

▼ Magenta Triangle: SMI Crossover DOWN. This occurs when the Main Wave crosses below the SMI Signal line. This is a potential Short Entry.

4. Hull Trend Markers (Circles/Shapes at Edges)

Located at the very top and bottom of the indicator panel are the Hull Moving Average (HMA) filters.

Bottom Blue/Green Marker: The longer-term Hull Trend is UP.

Top Orange/Red Marker: The longer-term Hull Trend is DOWN.

How to Trade Strategy

✅ The "Flow" Setup (High Probability)

This strategy focuses on taking trades with the momentum consensus.

Wait for the Glow: Look for the Wave to turn Neon Green (Bullish) or Neon Red (Bearish). This confirms momentum is present.

Check the Filter: Ensure the Hull Trend Marker (at the top/bottom) matches the wave color (e.g., Blue marker + Green Wave).

The Trigger: Enter when a Triangle Signal Arrow appears in the direction of the color.

Example: Wave is Green + Cyan Triangle appears = STRONG BUY.

⚠️ The "Reversal" Setup (Aggressive)

Divergence: Price makes a new high, but the ChromaFlows Wave makes a lower high.

Color Shift: The wave changes from Green to Gray (Neutral), indicating momentum is dying.

The Trigger: Wait for a Magenta Triangle (Cross Down) to confirm the reversal.

⛔ The "No-Trade" Zone

When the Wave is Gray and hovering near the zero line, the markets are ranging or the indicators are conflicting. It is statistically safer to stand aside until the "ChromaFlow" (Green or Red color) returns.

Settings Configuration

Wave Source: Choose which oscillator drives the main wave (Default: Stochastic_2).

Consensus Sensitivity: Adjust the periods of the RSI and Stochastics to make the "Glow" appear faster (more signals) or slower (more filtering).

Visuals: All colors are fully customizable via Hex codes to match your chart theme.

Body Close Continuity & failure Backtesting @MaxMaseratiThis indicator, is a highly advanced institutional-grade tool designed to track the "lifespan" of a trend based on Body Close (BC) sequences.

Unlike basic indicators that just show direction, this script analyzes the structural integrity of a trend by monitoring how many candles continue the move before a "Touch" (retest) or a "Break" (failure) occurs.

The Continuity & Failure Stats indicator tracks sequences of Bullish Body Closes (BuBC) and Bearish Body Closes (BeBC). It measures three critical phases: Building (pure momentum), Touching (price retesting the low/high of the sequence), and Resumption (price continuing the trend after a retest). It provides a statistical distribution of how long these "buildings" typically last before failing, allowing traders to know exactly when a trend is overextended.

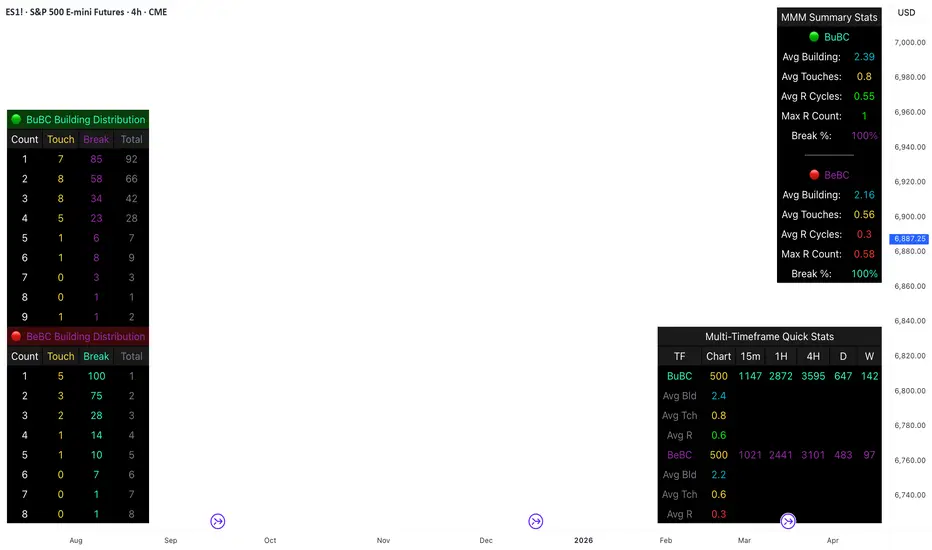

This comprehensive analysis blends the statistical breakdown of the Continuity & Failure Stats indicator to provide a deep understanding of the structural momentum for the S&P 500 E-mini (ES1!) on a 4-hour timeframe.

1. Extensive Table Breakdown

A. Building Distribution (Left Table): The Fatigue Gauge

This table acts as a histogram of momentum, tracking the "Building Count"—the number of consecutive candles closing in a trend without price returning to its origin.

Count Column: Represents the streak length (e.g., 1, 2, or 3 candles).

Touch Column: Shows how many times a streak was interrupted by a retest ("touch") but remained structurally intact.

Break Column: Counts total structural failures where price closed beyond the sequence's anchor.

Data Insight: For BuBC, 92 sequences reached Count 1, but only 28 remained by Count 4. This reveals a steep momentum decay after the 3rd candle, establishing a "Statistical Wall" where only 2 sequences in history reached a count of 9.

B. MMM Summary Stats (Top Right): The Mathematical DNA

This table provides the "Expected Value" and behavior of a trend over the lookback period.

Avg Building (2.39 for BuBC): On average, a bullish move lasts ~2.4 candles of pure momentum before a retest or reversal occurs.

Avg Touches (0.8): This low number indicates "clean" trends that rarely wobble back to retest levels multiple times before reaching a conclusion.

Avg R Cycles (0.55): This suggests that once a bullish trend is interrupted, it only successfully resumes its momentum about half the time.

Max R Count (1): Typically, once a trend is "touched," it only manages one more push before failing.

C. Multi-Timeframe (MTF) Quick Stats (Bottom Right): Trend Weight

This compares the 4H chart against other layers of the market to identify "global" alignment.

Sample Comparison: There are 3,594 tracked BuBC sequences on the 4H compared to only 142 on the Weekly chart.

Fractal Law: The Avg Building (2.4) is consistent across several timeframes, implying that the "Rule of Three" (momentum fading after 3 candles) is a fractal characteristic of this asset.

2. Table Comparison: Synthesizing the Data

To trade effectively, you must compare Distribution (timing) against Summary Stats (averages):

Continuity vs. Failure: The Summary Stats show an average building of 2.39. When checking the Distribution table at Count 2, the "Break" count (58) is already high relative to the "Total". This confirms that the risk of failure increases exponentially the moment you exceed the average.

Momentum vs. Mean Reversion: Distribution tells you when a trend is "tired". If the 4H is at a "Building Count 4" (statistically overextended) while the Weekly chart is at "Building Count 1" (fresh momentum), you may choose to prioritize the higher timeframe's strength despite the local overextension.

3. Strategic Summary & Application

This indicator proves that market momentum follows a predictable "Building" cycle rather than an infinite streak.

The "Rule of Three" for ES1! 4H:

The Entry Zone (Momentum Start): The most profitable entries occur at Building Count 1. Statistically, you have a high probability of reaching a count of 2 or 3.

The Exit Zone (Momentum Limit): Take profits or tighten stops at Count 3. The data shows the sample size drops by nearly 50% between Count 3 and Count 4.

The "Touch" Rule (Retest Reliability): If price returns to the sequence low (a "Touch"), do not expect a massive continuation. The Max R Count of 1 tells us that resumptions are usually short-lived.

Danger Zone: Entering at Building Count 4 or higher is statistically dangerous, as the "Break" probability significantly outweighs the "Touch" or continuation probability.

Price Range CHoCH Alert🎯 Smart Money Concept (SMC) indicator that monitors a specific price level and alerts only when price touches that level AND

subsequently creates a Change of Character (CHoCH).

Key Features:

• Set a custom price level to monitor

• Detects CHoCH/BOS based on pivot highs/lows

• Alerts ONLY when: Price touches level → CHoCH occurs

• Visual confirmation with level line and status table

• Configurable tolerance for precise level targeting

• Works for both bullish and bearish scenarios

Perfect for:

✓ Institutional level trading

✓ Key support/resistance breakouts

✓ Liquidity grab confirmations

✓ Structure break validation

Simply set your target price level and let the indicator watch for the perfect SMC setup!

Price Prediction Forecast ModelPrice Prediction Forecast Model

This indicator projects future price ranges based on recent market volatility.

It does not predict exact prices — instead, it shows where price is statistically likely to move over the next X bars.

How It Works

Price moves up and down by different amounts each bar. This indicator measures how large those moves have been recently (volatility) using the standard deviation of log returns.

That volatility is then:

Projected forward in time

Scaled as time increases (uncertainty grows)

Converted into future price ranges

The further into the future you project, the wider the expected range becomes.

Volatility Bands (Standard Deviation–Based)

The indicator plots up to three projected volatility bands using standard deviation multipliers:

SD1 (1.0×) → Typical expected price movement

SD2 (1.25×) → Elevated volatility range

SD3 (1.5×) → High-volatility / stress range

These bands are based on standard deviation of volatility, not fixed probability guarantees.

Optional Drift

An optional drift term can be enabled to introduce a long-term directional bias (up or down).

This is useful for markets with persistent trends.

TSF - Rel Vol & Stop calcSimple swing data table showing:

1. Avg 20D dollar vol

2. Live dollar vol

3. Live % relative vol compared to avg 20d daily vol

4.Percent to LOD current price with color codes

5. Avg 20d ATR%

LJ Parsons Adjustable expanding MRT FibBased on premium/discount/fair-value levels the indicator will expand with the market by settable dates.

The levels are not fib based as such but are resonant levels within an multiplicative /12 log scale using the LJ Parsons Market resonance hypothesis.