Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

Forecasting

Timeframe StrategyThis is a multi-timeframe trading strategy inspired by Ross Cameron's style, optimized for scalping and trend-following across various timeframes (1m, 5m, 15m, 1h, and 1D). The strategy integrates a comprehensive set of technical indicators, dynamic risk management, and visual tools.

Core Features

Dynamic Take Profit, Stop Loss & Trailing Stop

> Separate settings per timeframe for:

-TP% (Take Profit)

-SL% (Stop Loss)

-Trailing Stop %

-Cooldown bars

> Configurable via UI inputs.

>Smart Entry Conditions

Bullish entry: EMA9 crossover EMA20 and EMA50 > EMA200

Bearish entry: EMA9 crossunder EMA20 and EMA50 < EMA200

>Additional confirmation filters:

-Volume Filter (enabled/disabled via UI)

-Time Filter (e.g., only between 15:00–20:00 UTC)

-Spike Filter: rejects high-volatility candles

-RSI Filter: above/below 50 for trend confirmation

-ADX Filter (only applied on 1m, e.g., ADX > 15)

-Micro-Volatility Filter: minimum range percentage (1m only)

-Trend Filter (1m only): price must be above/below EMA200

>Trailing Stop Logic

-Configurable for each timeframe.

- Optional via toggle (use_trailing).

>Trade Cooldown Logic

-Prevents consecutive trades within X bars, configurable per timeframe.

>Technical Indicators Used

-EMA 9 / 20 / 50 / 200

-VWAP

-RSI (14)

-ATR (14) for volatility-based spike filtering

-Custom-calculated ADX (14) (manually implemented)

>Visual Elements

🔼/🔽 Entry signals (long/short) plotted on the chart.

📉 Table in bottom-left:

Displays current values of EMA/VWAP/volume/ATR/ADX.

> Optional "Tab info" panel in top-right (toggleable):

-Timeframe & strategy settings

-Live status of filters (volume, time, cooldown, spike, RSI, ADX, range, trend)

-Uses emoji (✅ / ❌) for quick diagnostics.

>User Customization

-Inputs per timeframe for all key parameters.

-Toggle switches for:

-Trailing stop

-Volume filter

-Info table visibility

This strategy is designed for active traders seeking a balance between momentum entry, risk control, and adaptability across timeframes. It's ideal for backtesting quick reversals or breakout setups in fast markets, especially at lower timeframes like 1m or 5m.

30-70 RSI Strategy with Colored BarThis script colors price bars based on Relative Strength Index (RSI) levels, giving traders a quick and visual way to assess overbought or oversold market conditions directly on the chart.

📈 Key Features:

✅ RSI-Based Bar Coloring:

Green bars when RSI is above the upper threshold (default 70) – suggests bullish momentum.

Red bars when RSI is below the lower threshold (default 30) – indicates bearish pressure.

Bars remain uncolored when RSI is between thresholds – a neutral zone.

🔧 Customizable RSI Settings:

Adjustable RSI length (default: 14 periods)

Adjustable overbought/oversold levels (default: 70/30)

🧠 Helps traders:

Quickly spot potential reversals or trend continuations

Visually align price action with momentum

🛠️ Usage:

Ideal for trend-following, reversal, and momentum strategies.

Works across any timeframe (1m, 5m, 1h, daily, etc.).

Sharpe Ratio Forced Selling StrategyThis study introduces the “Sharpe Ratio Forced Selling Strategy”, a quantitative trading model that dynamically manages positions based on the rolling Sharpe Ratio of an asset’s excess returns relative to the risk-free rate. The Sharpe Ratio, first introduced by Sharpe (1966), remains a cornerstone in risk-adjusted performance measurement, capturing the trade-off between return and volatility. In this strategy, entries are triggered when the Sharpe Ratio falls below a specified low threshold (indicating excessive pessimism), and exits occur either when the Sharpe Ratio surpasses a high threshold (indicating optimism or mean reversion) or when a maximum holding period is reached.

The underlying economic intuition stems from institutional behavior. Institutional investors, such as pension funds and mutual funds, are often subject to risk management mandates and performance benchmarking, requiring them to reduce exposure to assets that exhibit deteriorating risk-adjusted returns over rolling periods (Greenwood and Scharfstein, 2013). When risk-adjusted performance improves, institutions may rebalance or liquidate positions to meet regulatory requirements or internal mandates, a behavior that can be proxied effectively through a rising Sharpe Ratio.

By systematically monitoring the Sharpe Ratio, the strategy anticipates when “forced selling” pressure is likely to abate, allowing for opportunistic entries into assets priced below fundamental value. Exits are equally mechanized, either triggered by Sharpe Ratio improvements or by a strict time-based constraint, acknowledging that institutional rebalancing and window-dressing activities are often time-bound (Coval and Stafford, 2007).

The Sharpe Ratio is particularly suitable for this framework due to its ability to standardize excess returns per unit of risk, ensuring comparability across timeframes and asset classes (Sharpe, 1994). Furthermore, adjusting returns by a dynamically updating short-term risk-free rate (e.g., US 3-Month T-Bills from FRED) ensures that macroeconomic conditions, such as shifting interest rates, are accurately incorporated into the risk assessment.

While the Sharpe Ratio is an efficient and widely recognized measure, the strategy could be enhanced by incorporating alternative or complementary risk metrics:

• Sortino Ratio: Unlike the Sharpe Ratio, the Sortino Ratio penalizes only downside volatility (Sortino and van der Meer, 1991). This would refine entries and exits to distinguish between “good” and “bad” volatility.

• Maximum Drawdown Constraints: Integrating a moving window maximum drawdown filter could prevent entries during persistent downtrends not captured by volatility alone.

• Conditional Value at Risk (CVaR): A measure of expected shortfall beyond the Value at Risk, CVaR could further constrain entry conditions by accounting for tail risk in extreme environments (Rockafellar and Uryasev, 2000).

• Dynamic Thresholds: Instead of static Sharpe thresholds, one could implement dynamic bands based on the historical distribution of the Sharpe Ratio, adjusting for volatility clustering effects (Cont, 2001).

Each of these risk parameters could be incorporated into the current script as additional input controls, further tailoring the model to different market regimes or investor risk appetites.

References

• Cont, R. (2001) ‘Empirical properties of asset returns: stylized facts and statistical issues’, Quantitative Finance, 1(2), pp. 223-236.

• Coval, J.D. and Stafford, E. (2007) ‘Asset Fire Sales (and Purchases) in Equity Markets’, Journal of Financial Economics, 86(2), pp. 479-512.

• Greenwood, R. and Scharfstein, D. (2013) ‘The Growth of Finance’, Journal of Economic Perspectives, 27(2), pp. 3-28.

• Rockafellar, R.T. and Uryasev, S. (2000) ‘Optimization of Conditional Value-at-Risk’, Journal of Risk, 2(3), pp. 21-41.

• Sharpe, W.F. (1966) ‘Mutual Fund Performance’, Journal of Business, 39(1), pp. 119-138.

• Sharpe, W.F. (1994) ‘The Sharpe Ratio’, Journal of Portfolio Management, 21(1), pp. 49-58.

• Sortino, F.A. and van der Meer, R. (1991) ‘Downside Risk’, Journal of Portfolio Management, 17(4), pp. 27-31.

Dkoderweb repainting issue fix strategyHarmonic Pattern Recognition Trading Strategy

This TradingView strategy called "Dkoderweb repainting issue fix strategy" is designed to identify and trade harmonic price patterns with optimized entry and exit points using Fibonacci levels. The strategy implements various popular harmonic patterns including Bat, Butterfly, Gartley, Crab, Shark, ABCD, and their anti-patterns.

Key Features

Pattern Recognition: Identifies 17+ harmonic price patterns including standard and anti-patterns

Fibonacci-Based Entries and Exits: Uses customizable Fibonacci levels for precision entries, take profits, and stop losses

Alternative Timeframe Analysis: Option to use higher timeframes for pattern identification

Heiken Ashi Support: Optional use of Heiken Ashi candles instead of regular candlesticks

Visual Indicators:

Pattern visualization with ZigZag indicator

Buy/sell signal markers

Color-coded background to highlight active trade zones

Customizable Fibonacci level display

How It Works

The strategy uses a ZigZag-based pattern identification system to detect pivot points

When a valid harmonic pattern forms, the strategy calculates the optimal entry window using the specified Fibonacci level (default 0.382)

Entries trigger when price returns to the entry window after pattern completion

Take profit and stop loss levels are automatically set based on customizable Fibonacci ratios

Visual alerts notify you of entries and exits

The strategy tracks active trades and displays them with background color highlights

Customizable Settings

Trade size

Entry window Fibonacci level (default 0.382)

Take profit Fibonacci level (default 0.618)

Stop loss Fibonacci level (default -0.618)

Alert messages for entries and exits

Display options for specific Fibonacci levels

Alternative timeframe selection

This strategy is designed to fix repainting issues that are common in harmonic pattern strategies, ensuring more reliable signals and backtesting results.

IU Bigger than range strategyDESCRIPTION

IU Bigger Than Range Strategy is designed to capture breakout opportunities by identifying candles that are significantly larger than the previous range. It dynamically calculates the high and low of the last N candles and enters trades when the current candle's range exceeds the previous range. The strategy includes multiple stop-loss methods (Previous High/Low, ATR, Swing High/Low) and automatically manages take-profit and stop-loss levels based on user-defined risk-to-reward ratios. This versatile strategy is optimized for higher timeframes and assets like BTC but can be fine-tuned for different instruments and intervals.

USER INPUTS:

Look back Length: Number of candles to calculate the high-low range. Default is 22.

Risk to Reward: Sets the target reward relative to the stop-loss distance. Default is 3.

Stop Loss Method: Choose between:(Default is "Previous High/Low")

- Previous High/Low

- ATR (Average True Range)

- Swing High/Low

ATR Length: Defines the length for ATR calculation (only applicable when ATR is selected as the stop-loss method) (Default is 14).

ATR Factor: Multiplier applied to the ATR to determine stop-loss distance(Default is 2).

Swing High/Low Length: Specifies the length for identifying swing points (only applicable when Swing High/Low is selected as the stop-loss method).(Default is 2)

LONG CONDITION:

The current candle’s range (absolute difference between open and close) is greater than the previous range.

The closing price is higher than the opening price (bullish candle).

SHORT CONDITIONS:

The current candle’s range exceeds the previous range.

The closing price is lower than the opening price (bearish candle).

LONG EXIT:

Stop-loss:

- Previous Low

- ATR-based trailing stop

- Recent Swing Low

Take-profit:

- Defined by the Risk-to-Reward ratio (default 3x the stop-loss distance).

SHORT EXIT:

Stop-loss:

- Previous High

- ATR-based trailing stop

- Recent Swing High

Take-profit:

- Defined by the Risk-to-Reward ratio (default 3x the stop-loss distance).

ALERTS:

Long Entry Triggered

Short Entry Triggered

WHY IT IS UNIQUE:

This strategy dynamically adapts to different market conditions by identifying candles that exceed the previous range, ensuring that it only enters trades during strong breakout scenarios.

Multiple stop-loss methods provide flexibility for different trading styles and risk profiles.

The visual representation of stop-loss and take-profit levels with color-coded plots improves trade monitoring and decision-making.

HOW USERS CAN BENEFIT FROM IT:

Ideal for breakout traders looking to capitalize on momentum-driven price moves.

Provides flexibility to customize stop-loss methods and fine-tune risk management parameters.

Helps minimize drawdowns with a strong risk-to-reward framework while maximizing profit potential.

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

Simple APF Strategy Backtesting [The Quant Science]Simple backtesting strategy for the quantitative indicator Autocorrelation Price Forecasting. This is a Buy & Sell strategy that operates exclusively with long orders. It opens long positions and generates profit based on the future price forecast provided by the indicator. It's particularly suitable for trend-following trading strategies or directional markets with an established trend.

Main functions

1. Cycle Detection: Utilize autocorrelation to identify repetitive market behaviors and cycles.

2. Forecasting for Backtesting: Simulate trades and assess the profitability of various strategies based on future price predictions.

Logic

The strategy works as follow:

Entry Condition: Go long if the hypothetical gain exceeds the threshold gain (configurable by user interface).

Position Management: Sets a take-profit level based on the future price.

Position Sizing: Automatically calculates the order size as a percentage of the equity.

No Stop-Loss: this strategy doesn't includes any stop loss.

Example Use Case

A trader analyzes a dayli period using 7 historical bars for autocorrelation.

Sets a threshold gain of 20 points using a 5% of the equity for each trade.

Evaluates the effectiveness of a long-only strategy in this period to assess its profitability and risk-adjusted performance.

User Interface

Length: Set the length of the data used in the autocorrelation price forecasting model.

Thresold Gain: Minimum value to be considered for opening trades based on future price forecast.

Order Size: percentage size of the equity used for each single trade.

Strategy Limit

This strategy does not use a stop loss. If the price continues to drop and the future price forecast is incorrect, the trader may incur a loss or have their capital locked in the losing trade.

Disclaimer!

This is a simple template. Use the code as a starting point rather than a finished solution. The script does not include important parameters, so use it solely for educational purposes or as a boilerplate.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Divergence IQ [TradingIQ]Hello Traders!

Introducing "Divergence IQ"

Divergence IQ lets traders identify divergences between price action and almost ANY TradingView technical indicator. This tool is designed to help you spot potential trend reversals and continuation patterns with a range of configurable features.

Features

Divergence Detection

Detects both regular and hidden divergences for bullish and bearish setups by comparing price movements with changes in the indicator.

Offers two detection methods: one based on classic pivot point analysis and another that provides immediate divergence signals.

Option to use closing prices for divergence detection, allowing you to choose the data that best fits your strategy.

Normalization Options:

Includes multiple normalization techniques such as robust scaling, rolling Z-score, rolling min-max, or no normalization at all.

Adjustable normalization window lets you customize the indicator to suit various market conditions.

Option to display the normalized indicator on the chart for clearer visual comparison.

Allows traders to take indicators that aren't oscillators, and convert them into an oscillator - allowing for better divergence detection.

Simulated Trade Management:

Integrates simulated trade entries and exits based on divergence signals to demonstrate potential trading outcomes.

Customizable exit strategies with options for ATR-based or percentage-based stop loss and profit target settings.

Automatically calculates key trade metrics such as profit percentage, win rate, profit factor, and total trade count.

Visual Enhancements and On-Chart Displays:

Color-coded signals differentiate between bullish, bearish, hidden bullish, and hidden bearish divergence setups.

On-chart labels, lines, and gradient flow visualizations clearly mark divergence signals, entry points, and exit levels.

Configurable settings let you choose whether to display divergence signals on the price chart or in a separate pane.

Performance Metrics Table:

A performance table dynamically displays important statistics like profit, win rate, profit factor, and number of trades.

This feature offers an at-a-glance assessment of how the divergence-based strategy is performing.

The image above shows Divergence IQ successfully identifying and trading a bullish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a bearish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a hidden bullish divergence between an indicator and price action!

The image above shows Divergence IQ successfully identifying and trading a hidden bearish divergence between an indicator and price action!

The performance table is designed to provide a clear summary of simulated trade results based on divergence setups. You can easily review key metrics to assess the strategy’s effectiveness over different time periods.

Customization and Adaptability

Divergence IQ offers a wide range of configurable settings to tailor the indicator to your personal trading approach. You can adjust the lookback and lookahead periods for pivot detection, select your preferred method for normalization, and modify trade exit parameters to manage risk according to your strategy. The tool’s clear visual elements and comprehensive performance metrics make it a useful addition to your technical analysis toolbox.

The image above shows Divergence IQ identifying divergences between price action and OBV with no normalization technique applied.

While traders can look for divergences between OBV and price, OBV doesn't naturally behave like an oscillator, with no definable upper and lower threshold, OBV can infinitely increase or decrease.

With Divergence IQ's ability to normalize any indicator, traders can normalize non-oscillator technical indicators such as OBV, CVD, MACD, or even a moving average.

In the image above, the "Robust Scaling" normalization technique is selected. Consequently, the output of OBV has changed and is now behaving similar to an oscillator-like technical indicator. This makes spotting divergences between the indicator and price easier and more appropriate.

The three normalization techniques included will change the indicator's final output to be more compatible with divergence detection.

This feature can be used with almost any technical indicator.

Stop Type

Traders can select between ATR based profit targets and stop losses, or percentage based profit targets and stop losses.

The image above shows options for the feature.

Divergence Detection Method

A natural pitfall of divergence trading is that it generally takes several bars to "confirm" a divergence. This makes trading the divergence complicated, because the entry at time of the divergence might look great; however, the divergence wasn't actually signaled until several bars later.

To circumvent this issue, Divergence IQ offers two divergence detection mechanisms.

Pivot Detection

Pivot detection mode is the same as almost every divergence indicator on TradingView. The Pivots High Low indicator is used to detect market/indicator highs and lows and, consequently, divergences.

This method generally finds the "best looking" divergences, but will always take additional time to confirm the divergence.

Immediate Detection

Immediate detection mode attempts to reduce lag between the divergence and its confirmation to as little as possible while avoiding repainting.

Immediate detection mode still uses the Pivots Detection model to find the first high/low of a divergence. However, the most recent high/low does not utilize the Pivot Detection model, and instead immediately looks for a divergence between price and an indicator.

Immediate Detection Mode will always signal a divergence one bar after it's occurred, and traders can set alerts in this mode to be alerted as soon as the divergence occurs.

TradingView Backtester Integration

Divergence IQ is fully compatible with the TradingView backtester!

Divergence IQ isn’t designed to be a “profitable strategy” for users to trade. Instead, the intention of including the backtester is to let users backtest divergence-based trading strategies between the asset on their chart and almost any technical indicator, and to see if divergences have any predictive utility in that market.

So while the backtester is available in Divergence IQ, it’s for users to personally figure out if they should consider a divergence an actionable insight, and not a solicitation that Divergence IQ is a profitable trading strategy. Divergence IQ should be thought of as a Divergence backtesting toolkit, not a full-feature trading strategy.

Strategy Properties Used For Backtest

Initial Capital: $1000 - a realistic amount of starting capital that will resonate with many traders

Amount Per Trade: 5% of equity - a realistic amount of capital to invest relative to portfolio size

Commission: 0.02% - a conservative amount of commission to pay for trade that is standard in crypto trading, and very high for other markets.

Slippage: 1 tick - appropriate for liquid markets, but must be increased in markets with low activity.

Once more, the backtester is meant for traders to personally figure out if divergences are actionable trading signals on the market they wish to trade with the indicator they wish to use.

And that's all!

If you have any cool features you think can benefit Divergence IQ - please feel free to share them!

Thank you so much TradingView community!

Ultimate T3 Fibonacci for BTC Scalping. Look at backtest report!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto trading! This strategy is for BITCOIN on the 30 minute chart since I designed it to be a scalping strategy. I calculated for trading fees, and use a small amount of capital in the backtest report. But feel free to modify the capital and how much per order to see how it changes the results:)

It is called the "Ultimate T3 Fibonacci Indicator by NHBprod" that computes and displays two T3-based moving averages derived from price data. The t3_function calculates the Tilson T3 indicator by applying a series of exponential moving averages to a combined price metric and then blending these results with specific coefficients derived from an input factor.

The script accepts several user inputs that toggle the use of the T3 filter, select the buy signal method, and set parameters like lengths and volume factors for two variations of the T3 calculation. Two T3 lines, T3 and T32, are computed with different parameters, and their colors change dynamically (green/red for T3 and blue/purple for T32) based on whether the lines are trending upward or downward. Depending on the selected signal method, the script generates buy signals either when T32 crosses over T3 or when the closing price is above T3, and similarly, sell signals are generated on the respective conditions for crossing under or closing below. Finally, the indicator plots the T3 lines on the chart, adds visual buy/sell markers, and sets alert conditions to notify users when the respective trading signals occur.

The user has the ability to tune the parameters using TP/SL, date timerames for analyses, and the actual parameters of the T3 function including the buy/sell signal! Lastly, the user has the option of trading this long, short, or both!

Let me know your thoughts and check out the backtest report!

GOLD Volume-Based Entry StrategyShort Description:

This script identifies potential long entries by detecting two consecutive bars with above-average volume and bullish price action. When these conditions are met, a trade is entered, and an optional profit target is set based on user input. This strategy can help highlight momentum-driven breakouts or trend continuations triggered by a surge in buying volume.

How It Works

Volume Moving Average

A simple moving average of volume (vol_ma) is calculated over a user-defined period (default: 20 bars). This helps us distinguish when volume is above or below recent averages.

Consecutive Green Volume Bars

First bar: Must be bullish (close > open) and have volume above the volume MA.

Second bar: Must also be bullish, with volume above the volume MA and higher than the first bar’s volume.

When these two bars appear in sequence, we interpret it as strong buying pressure that could drive price higher.

Entry & Profit Target

Upon detecting these two consecutive bullish bars, the script places a long entry.

A profit target is set at current price plus a user-defined fixed amount (default: 5 USD).

You can adjust this target, or you can add a stop-loss in the script to manage risk further.

Visual Cues

Buy Signal Marker appears on the chart when the second bar confirms the signal.

Green Volume Columns highlight the bars that fulfill the criteria, providing a quick visual confirmation of high-volume bullish bars.

Works fine on 1M-2M-5M-15M-30M. Do not use it on higher TF. Due the lack of historical data on lower TF, the backtest result is limited.

John Bob-Trading-BotDeveloped by Ayebale John Bob with the help of his bestie, this innovative strategy combines advanced Smart Money Concepts with practical risk management tools to help traders identify and capitalize on key market moves.

Key Features:

Smart Money Concepts & Fair Value Gaps (FVG):

The strategy monitors price action for fair value gaps, which are visualized as extremely faint horizontal lines on the chart. These FVGs signal potential areas where institutional traders might have entered or exited positions.

Dynamic Entry Signals:

Buy signals are triggered when the price crosses above the 50-bar lowest low or when a bullish FVG is detected. Conversely, sell signals are generated when the price falls below the 50-bar highest high or a bearish FVG is identified. Each signal is visually marked on the chart with clear buy (green) and sell (red) labels.

Multi-Level Order Execution:

Once an entry signal occurs, the strategy places five separate orders, each with its own take-profit (TP) level. The TP levels are calculated dynamically using the Average True Range (ATR) and a set of predefined multipliers. This allows traders to scale out of positions as the market moves favorably.

Dynamic Risk Management:

A stop-loss is automatically set at a distance determined by the ATR, ensuring that risk is managed in accordance with current market volatility.

Real-Time Trade Information Table:

In the bottom-right corner of the chart, a trade information table displays essential details about the current trade:

Side: Displays "BUY NOW" (with a dark green background) for long entries or "SELL NOW" (with a dark red background) for short entries.

Entry Price & Stop-Loss: Shows the entry price (highlighted in green) and the corresponding stop-loss level (highlighted in red).

Take-Profit Levels: Lists the five TP levels, each of which turns green once the market price reaches that target.

Timer: A live timer in minutes counts from the moment the current trade trigger started, helping traders track the duration of their active trades.

Visual Progress Bar:

A histogram-style progress bar is plotted on the chart, visually representing the percentage gain (or loss) relative to the entry price.

This strategy was meticulously designed to incorporate both technical analysis and smart risk management, offering a robust trading solution that adapts to changing market conditions. Whether you're a seasoned trader or just starting out, the AyebaleJohnBob Trading Bot equips you with the tools and visual cues needed to make well-informed trading decisions. Enjoy a seamless blend of strategy and style—crafted with passion by Ayebale John Bob and his bestie!

Ultimate Stochastics Strategy by NHBprod Use to Day Trade BTCHey All!

Here's a new script I worked on that's super simple but at the same time useful. Check out the backtest results. The backtest results include slippage and fees/commission, and is still quite profitable. Obviously the profitability magnitude depends on how much capital you begin with, and how much the user utilizes per order, but in any event it seems to be profitable according to backtests.

This is different because it allows you full functionality over the stochastics calculations which is designed for random datasets. This script allows you to:

Designate ANY period of time to analyze and study

Choose between Long trading, short trading, and Long & Short trading

It allows you to enter trades based on the stochastics calculations

It allows you to EXIT trades using the stochastics calculations or take profit, or stop loss, Or any combination of those, which is nice because then the user can see how one variable effects the overall performance.

As for the actual stochastics formula, you get control, and get to SEE the plot lines for slow K, slow D, and fast K, which is usually not considered.

You also get the chance to modify the smoothing method, which has not been done with regular stochastics indicators. You get to choose the standard simple moving average (SMA) method, but I also allow you to choose other MA's such as the HMA and WMA.

Lastly, the user gets the option of using a custom trade extender, which essentially allows a buy or sell signal to exist for X amount of candles after the initial signal. For example, you can use "max bars since signal" to 1, and this will allow the indicator to produce an extra sequential buy signal when a buy signal is generated. This can be useful because it is possible that you use a small take profit (TP) and quickly exit a profitable trade. With the max bars since signal variable, you're able to reenter on the next candle and allow for another opportunity.

Let me know if you have any questions! Please take a look at the performance report and let me know your thoughts! :)

Gold Pro StrategyHere’s the strategy description in a chat format:

---

**Gold (XAU/USD) Trend-Following Strategy**

This **trend-following strategy** is designed for trading gold (XAU/USD) by combining moving averages, MACD momentum indicators, and RSI filters to capture sustained trends while managing volatility risks. The strategy uses volatility-adjusted stops to protect gains and prevent overexposure during erratic price movements. The aim is to take advantage of trending markets by confirming momentum and ensuring entries are not made at extreme levels.

---

**Key Components**

1. **Trend Identification**

- **50 vs 200 EMA Crossover**

- **Bullish Trend:** 50 EMA crosses above 200 EMA, and the price closes above the 200 EMA

- **Bearish Trend:** 50 EMA crosses below 200 EMA, and the price closes below the 200 EMA

2. **Momentum Confirmation**

- **MACD (12,26,9)**

- **Buy Signal:** MACD line crosses above the signal line

- **Sell Signal:** MACD line crosses below the signal line

- **RSI (14 Period)**

- **Bullish Zone:** RSI between 50-70 to avoid overbought conditions

- **Bearish Zone:** RSI between 30-50 to avoid oversold conditions

3. **Entry Criteria**

- **Long Entry:** Bullish trend, MACD bullish crossover, and RSI between 50-70

- **Short Entry:** Bearish trend, MACD bearish crossover, and RSI between 30-50

4. **Exit & Risk Management**

- **ATR Trailing Stops (14 Period):**

- Initial Stop: 3x ATR from entry price

- Trailing Stop: Adjusts to lock in profits as price moves favorably

- **Position Sizing:** 100% of equity per trade (high-risk strategy)

---

**Key Logic Flow**

1. **Trend Filter:** Use the 50/200 EMA relationship to define the market's direction

2. **Momentum Confirmation:** Confirm trend momentum with MACD crossovers

3. **RSI Validation:** Ensure RSI is within non-extreme ranges before entering trades

4. **Volatility-Based Risk Management:** Use ATR stops to manage market volatility

---

**Visual Cues**

- **Blue Line:** 50 EMA

- **Red Line:** 200 EMA

- **Green Triangles:** Long entry signals

- **Red Triangles:** Short entry signals

---

**Strengths**

- **Clear Trend Focus:** Avoids counter-trend trades

- **RSI Filter:** Prevents entering overbought or oversold conditions

- **ATR Stops:** Adapts to gold’s inherent volatility

- **Simple Rules:** Easy to follow with minimal inputs

---

**Weaknesses & Risks**

- **Infrequent Signals:** 50/200 EMA crossovers are rare

- **Potential Missed Opportunities:** Strict RSI criteria may miss some valid trends

- **Aggressive Position Sizing:** 100% equity allocation can lead to large drawdowns

- **No Profit Targets:** Relies on trailing stops rather than defined exit targets

---

**Performance Profile**

| Metric | Expected Range |

|----------------------|---------------------|

| Annual Trades | 4-8 |

| Win Rate | 55-65% |

| Max Drawdown | 25-35% |

| Profit Factor | 1.8-2.5 |

---

**Optimization Recommendations**

1. **Increase Trade Frequency**

Adjust the EMAs to shorter periods:

- `emaFastLen = input.int(30, "Fast EMA")`

- `emaSlowLen = input.int(150, "Slow EMA")`

2. **Relax RSI Filters**

Adjust the RSI range to:

- `rsiBullish = rsi > 45 and rsi < 75`

- `rsiBearish = rsi < 55 and rsi > 25`

3. **Add Profit Targets**

Introduce a profit target at 1.5% above entry:

```pine

strategy.exit("Long Exit", "Long",

stop=longStopPrice,

profit=close*1.015, // 1.5% target

trail_offset=trailOffset)

```

4. **Reduce Position Sizing**

Risk a smaller percentage per trade:

- `default_qty_value=25`

---

**Best Use Case**

This strategy excels in **strong trending markets** such as gold rallies during economic or geopolitical crises. However, during sideways or choppy market conditions, the strategy might require manual intervention to avoid false signals. Additionally, integrating fundamental analysis—like monitoring USD weakness or geopolitical risks—can enhance its effectiveness.

---

This strategy offers a balanced approach for trading gold, combining trend-following principles with risk management tailored to the volatility of the market.

IU Range Trading StrategyIU Range Trading Strategy

The IU Range Trading Strategy is designed to identify range-bound markets and take trades based on defined price ranges. This strategy uses a combination of price ranges and ATR (Average True Range) to filter entry conditions and incorporates a trailing stop-loss mechanism for better trade management.

User Inputs:

- Range Length: Defines the number of bars to calculate the highest and lowest price range (default: 10).

- ATR Length: Sets the length of the ATR calculation (default: 14).

- ATR Stop-Loss Factor: Determines the multiplier for the ATR-based stop-loss (default: 2.00).

Entry Conditions:

1. A range is identified when the difference between the highest and lowest prices over the selected range is less than or equal to 1.75 times the ATR.

2. Once a valid range is formed:

- A long trade is triggered at the range high.

- A short trade is triggered at the range low.

Exit Conditions:

1. Trailing Stop-Loss:

- The stop-loss adjusts dynamically using ATR targets.

- The strategy locks in profits as the trade moves in your favor.

2. The stop-loss and take-profit levels are visually plotted for transparency and easier decision-making.

Features:

- Automated box creation to visualize the trading range.

- Supports one position at a time, canceling opposite-side entries.

- ATR-based trailing stop-loss for effective risk management.

- Clear visual representation of stop-loss and take-profit levels with colored bands.

This strategy works best in markets with defined ranges and can help traders identify breakout opportunities when the price exits the range.

Bitcoin 1H-15M Breakout StrategyKey Features

1H and 15M Timeframes:

The script uses the 1-hour timeframe for the range and 15-minute timeframe for breakout conditions.

request.security is used to fetch the higher timeframe data.

Risk Management:

Variables entry_price, sl_price, and tp_price are declared explicitly as float with na initialization to handle dynamic assignment.

Stop-loss and take-profit levels are calculated based on the specified Risk-Reward Ratio (RRR) and buffer (in pips).

Trade Logic:

Long trade triggered when the 15-minute candle closes above the 1-hour high.

Short trade triggered when the 15-minute candle closes below the 1-hour low.

Visualization:

The range_high and range_low (previous 1-hour high and low) are plotted on the chart using dashed lines.

Debugging:

Enabling the show_debug input displays labels showing stop-loss and take-profit values for easier troubleshooting.

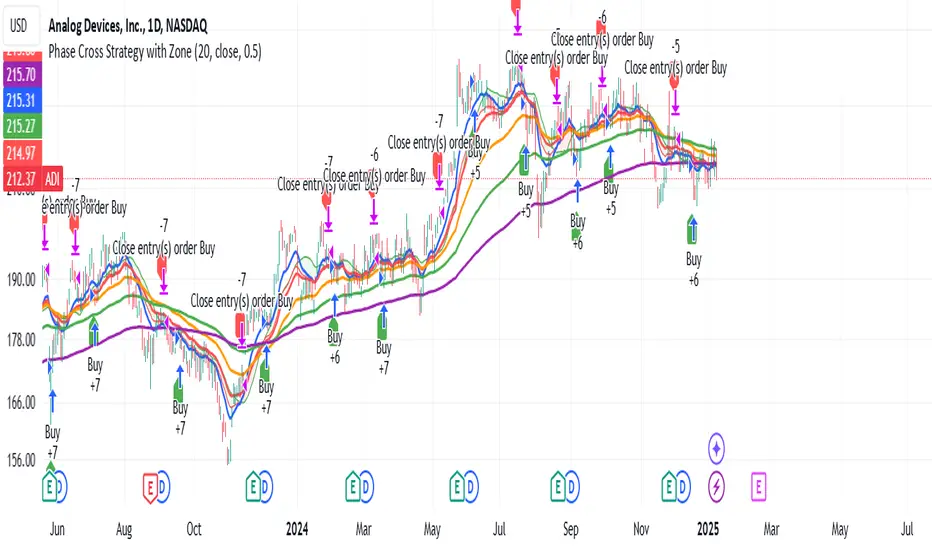

Phase Cross Strategy with Zone### Introduction to the Strategy

Welcome to the **Phase Cross Strategy with Zone and EMA Analysis**. This strategy is designed to help traders identify potential buy and sell opportunities based on the crossover of smoothed oscillators (referred to as "phases") and exponential moving averages (EMAs). By combining these two methods, the strategy offers a versatile tool for both trend-following and short-term trading setups.

### Key Features

1. **Phase Cross Signals**:

- The strategy uses two smoothed oscillators:

- **Leading Phase**: A simple moving average (SMA) with an upward offset.

- **Lagging Phase**: An exponential moving average (EMA) with a downward offset.

- Buy and sell signals are generated when these phases cross over or under each other, visually represented on the chart with green (buy) and red (sell) labels.

2. **Phase Zone Visualization**:

- The area between the two phases is filled with a green or red zone, indicating bullish or bearish conditions:

- Green zone: Leading phase is above the lagging phase (potential uptrend).

- Red zone: Leading phase is below the lagging phase (potential downtrend).

3. **EMA Analysis**:

- Includes five commonly used EMAs (13, 26, 50, 100, and 200) for additional trend analysis.

- Crossovers of the EMA 13 and EMA 26 act as secondary buy/sell signals to confirm or enhance the phase-based signals.

4. **Customizable Parameters**:

- You can adjust the smoothing length, source (price data), and offset to fine-tune the strategy for your preferred trading style.

### What to Pay Attention To

1. **Phases and Zones**:

- Use the green/red phase zone as an overall trend guide.

- Avoid taking trades when the phases are too close or choppy, as it may indicate a ranging market.

2. **EMA Trends**:

- Align your trades with the longer-term trend shown by the EMAs. For example:

- In an uptrend (price above EMA 50 or EMA 200), prioritize buy signals.

- In a downtrend (price below EMA 50 or EMA 200), prioritize sell signals.

3. **Signal Confirmation**:

- Consider combining phase cross signals with EMA crossovers for higher-confidence trades.

- Look for confluence between the phase signals and EMA trends.

4. **Risk Management**:

- Always set stop-loss and take-profit levels to manage risk.

- Use the phase and EMA zones to estimate potential support/resistance areas for exits.

5. **Whipsaws and False Signals**:

- Be cautious in low-volatility or sideways markets, as the strategy may generate false signals.

- Use additional indicators or filters to avoid entering trades during unclear market conditions.

### How to Use

1. Add the strategy to your chart in TradingView.

2. Adjust the input settings (e.g., smoothing length, offsets) to suit your trading preferences.

3. Enable the strategy tester to evaluate its performance on historical data.

4. Combine the signals with your own analysis and risk management plan for best results.

This strategy is a versatile tool, but like any trading method, it requires proper understanding and discretion. Always backtest thoroughly and trade with discipline. Let me know if you need further assistance or adjustments to the strategy!

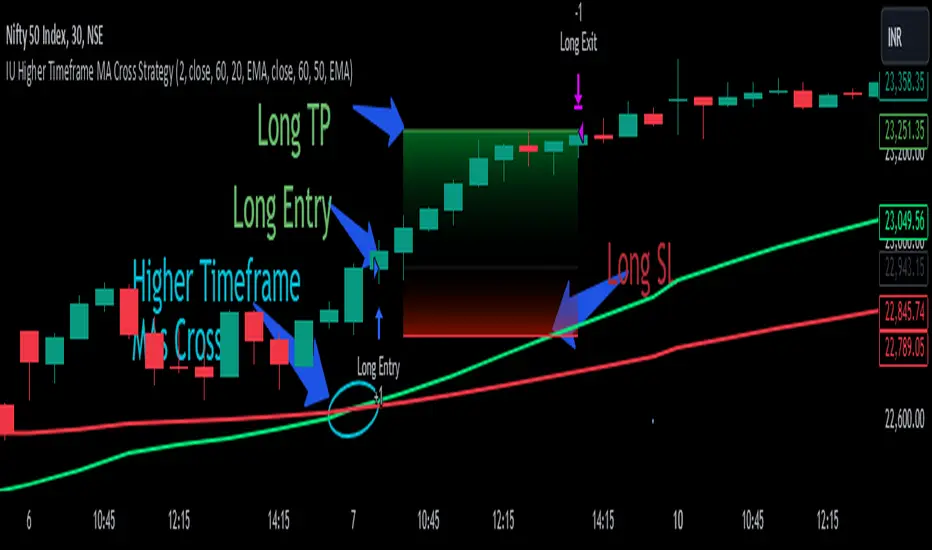

IU Higher Timeframe MA Cross StrategyIU Higher Timeframe MA Cross Strategy

The IU Higher Timeframe MA Cross Strategy is a versatile trading tool designed to identify trend by utilizing two customizable moving averages (MAs) across different timeframes and types. This strategy includes detailed entry and exit rules with fully configurable inputs, offering flexibility to suit various trading styles.

Key Features:

- Two moving averages (MA1 and MA2) with customizable types, lengths, sources, and timeframes.

- Both long and short trade setups based on MA crossovers.

- Integrated risk management with adjustable stop-loss and take-profit levels based on a user-defined risk-to-reward (RTR) ratio.

- Clear visualization of MAs, entry points, stop-loss, and take-profit zones.

Inputs:

1. Risk-to-Reward Ratio (RTR):

- Defines the take-profit level in relation to the stop-loss distance. Default is 2.

2. MA1 Settings:

- Source: Select the data source for calculating MA1 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA1 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA1 calculation. Default is 20.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA1 to merge gaps. Default is true.

3. MA2 Settings:

- Source: Select the data source for calculating MA2 (e.g., close, open, high, low). Default is close.

- Timeframe: Specify the timeframe for MA2 calculation. Default is 60 (60-minute chart).

- Length: Set the lookback period for MA2 calculation. Default is 50.

- Type: Choose the type of moving average (options: SMA, EMA, SMMA, WMA, VWMA). Default is EMA.

- Smooth: Option to enable or disable smoothing of MA2 to merge gaps. Default is true.

Entry Rules:

- Long Entry:

- Triggered when MA1 crosses above MA2 (crossover).

- Entry is confirmed only when the bar is closed and no existing position is active.

- Short Entry:

- Triggered when MA1 crosses below MA2 (crossunder).

- Entry is confirmed only when the bar is closed and no existing position is active.

Exit Rules:

- Stop-Loss:

- For long positions: Set at the low of the bar preceding the entry.

- For short positions: Set at the high of the bar preceding the entry.

- Take-Profit:

- For long positions: Calculated as (Entry Price - Stop-Loss) * RTR + Entry Price.

- For short positions: Calculated as Entry Price - (Stop-Loss - Entry Price) * RTR.

Visualization:

- Plots MA1 and MA2 on the chart with distinct colors for easy identification.

- Highlights stop-loss and take-profit levels using shaded zones for clear visual representation.

- Displays the entry level for active positions.

This strategy provides a robust framework for traders to identify and act on trend reversals while maintaining strict risk management. The flexibility of its inputs allows for seamless customization to adapt to various market conditions and trading preferences.

IU 4 Bar UP StrategyIU 4 Bar UP Strategy

The IU 4 Bar UP Strategy is a trend-following strategy designed to identify and execute long trades during strong bullish momentum, combined with confirmation from the SuperTrend indicator. This strategy is suitable for traders aiming to capitalize on sustained upward market movements.

Features :

1. SuperTrend Confirmation: Incorporates the SuperTrend indicator as a dynamic support/resistance line to filter trades in the direction of the trend.

2. 4 Consecutive Bullish Bars: Detects a series of 4 bullish candles as a signal for strong upward momentum, ensuring robust trade setups.

3. Dynamic Alerts: Sends alerts for trade entries and exits to keep traders informed.

4. Visual Enhancements:

- Plots the SuperTrend indicator on the chart.

- Changes the background color while a trade is active for easy visualization.

Inputs :

- SuperTrend ATR Period: The period used to calculate the Average True Range (ATR) for the SuperTrend indicator.

- SuperTrend ATR Factor: The multiplier for the ATR in the SuperTrend calculation.

Entry Conditions :

A long entry is triggered when:

1. The last 4 consecutive candles are bullish (closing prices are higher than opening prices).

2. The current price is above the SuperTrend line.

3. The strategy is not already in a position.

4. The bar is confirmed (not a partially formed bar).

When all these conditions are met, the strategy enters a long position and provides an alert:

"Long Entry triggered"

Exit Conditions :

The strategy exits the long position when:

1. The closing price drops below the SuperTrend line.

2. An alert is generated: "Close the long Trade"

Visualization :

- The SuperTrend line is plotted, dynamically colored:

- Green when the trend is bullish.

- Red when the trend is bearish.

- The background color turns semi-transparent green while a trade is active, indicating a long position.

Do use proper risk management while using this strategy.

IU open equal to high/low strategyIU open equal to high/low strategy:

The "IU Open Equal to High/Low Strategy" is designed to identify and trade specific market conditions where the day's first price action shows a strong directional bias. This strategy automatically enters trades based on the relationship between the market's open price and its first high or low of the day.

Entry Conditions:

1. Long Entry: A long position is initiated when the first open price of the session equals the day's first low. This signals a potential upward move.

2. Short Entry: A short position is initiated when the first open price of the session equals the day's first high. This signals a potential downward move.

Exit Conditions:

1. Stop Loss (SL): For both long and short trades, the stop loss is calculated based on the low or high of the candle where the position was entered.

2. Take Profit (TP): The take profit is set using a Risk-to-Reward (RTR) ratio, which is customizable by the user. The TP is calculated relative to the entry price and the distance between the entry and the stop loss.

Additional Features:

- Plots are used to visualize the entry price, stop loss, and take profit levels directly on the chart, providing clear and actionable insights.

- Labels are displayed to indicate the occurrence of the "Open == Low" or "Open == High" conditions for easier identification of potential trade setups.

- A dynamic fill highlights the areas between the entry price and the stop loss or take profit, offering a clear visual representation of the trade's risk and reward zones.

This strategy is designed for traders looking to capitalize on directional momentum at the start of the trading session. It is customizable, allowing users to set their desired Risk-to-Reward ratio and tailor the strategy to fit their trading style.

IU Opening range Breakout StrategyIU Opening Range Breakout Strategy

This Pine Script strategy is designed to capitalize on the breakout of the opening range, which is a popular trading approach. The strategy identifies the high and low prices of the opening session and takes trades based on price crossing these levels, with built-in risk management and trade limits for intraday trading.

Key Features:

1. Risk Management:

- Risk-to-Reward Ratio (RTR):

Set a customizable risk-to-reward ratio to calculate target prices based on stop-loss levels.

Default: 2:1

- Max Trades in a Day:

Specify the maximum number of trades allowed per day to avoid overtrading.

Default: 2 trades in a day.

- End-of-Day Close:

Automatically closes all open positions at a user-defined session end time to ensure no overnight exposure.

Default: 3:15 PM

2. Opening Range Identification

- Opening Range High and Low:

The script detects the high and low of the first trading session using Pine Script's session functions.

These levels are plotted as visual guides on the chart:

- High: Lime-colored circles.

- Low: Red-colored circles.

3. Trade Entry Logic

- Long Entry:

A long trade is triggered when the price closes above the opening range high.

- Entry condition: Crossover of the price above the opening range high.

-Short Entry:

A short trade is triggered when the price closes below the opening range low.

- Entry condition: Crossunder of the price below the opening range low.

Both entries are conditional on the absence of an existing position.

4. Stop Loss and Take Profit

- Long Position:

- Stop Loss: Previous candle's low.

- Take Profit: Calculated based on the RTR.

- **Short Position:**

- **Stop Loss:** Previous candle's high.

- **Take Profit:** Calculated based on the RTR.

The strategy plots these levels for visual reference:

- Stop Loss: Red dashed lines.

- Take Profit: Green dashed lines.

5. Visual Enhancements

-Trade Level Highlighting:

The script dynamically shades the areas between the entry price and SL/TP levels:

- Red shading for the stop-loss region.

- Green shading for the take-profit region.

- Entry Price Line:

A silver-colored line marks the average entry price for active trades.

How to Use:

1.Input Configuration:

Adjust the Risk-to-Reward ratio, max trades per day, and session end time to suit your trading preferences.

2.Visual Cues:

Use the opening range high/low lines and shading to identify potential breakout opportunities.

3.Execution:

The strategy will automatically enter and exit trades based on the conditions. Review the plotted SL and TP levels to monitor the risk-reward setup.

Important Notes:

- This strategy is designed for intraday trading and works best in markets with high volatility during the opening session.

- Backtest the strategy on your preferred market and timeframe to ensure compatibility.

- Proper risk management and position sizing are essential when using this strategy in live markets.

CCI Threshold StrategyThe CCI Threshold Strategy is a trading approach that utilizes the Commodity Channel Index (CCI) as a momentum indicator to identify potential buy and sell signals in financial markets. The CCI is particularly effective in detecting overbought and oversold conditions, providing traders with insights into possible price reversals. This strategy is designed for use in various financial instruments, including stocks, commodities, and forex, and aims to capitalize on price movements driven by market sentiment.

Commodity Channel Index (CCI)

The CCI was developed by Donald Lambert in the 1980s and is primarily used to measure the deviation of a security's price from its average price over a specified period.

The formula for CCI is as follows:

CCI=(TypicalPrice−SMA)×0.015MeanDeviation

CCI=MeanDeviation(TypicalPrice−SMA)×0.015

where:

Typical Price = (High + Low + Close) / 3

SMA = Simple Moving Average of the Typical Price

Mean Deviation = Average of the absolute deviations from the SMA

The CCI oscillates around a zero line, with values above +100 indicating overbought conditions and values below -100 indicating oversold conditions (Lambert, 1980).

Strategy Logic

The CCI Threshold Strategy operates on the following principles:

Input Parameters:

Lookback Period: The number of periods used to calculate the CCI. A common choice is 9, as it balances responsiveness and noise.

Buy Threshold: Typically set at -90, indicating a potential oversold condition where a price reversal is likely.

Stop Loss and Take Profit: The strategy allows for risk management through customizable stop loss and take profit points.

Entry Conditions:

A long position is initiated when the CCI falls below the buy threshold of -90, indicating potential oversold levels. This condition suggests that the asset may be undervalued and due for a price increase.

Exit Conditions:

The long position is closed when the closing price exceeds the highest price of the previous day, indicating a bullish reversal. Additionally, if the stop loss or take profit thresholds are hit, the position will be exited accordingly.

Risk Management:

The strategy incorporates optional stop loss and take profit mechanisms, which can be toggled on or off based on trader preference. This allows for flexibility in risk management, aligning with individual risk tolerances and trading styles.

Benefits of the CCI Threshold Strategy

Flexibility: The CCI Threshold Strategy can be applied across different asset classes, making it versatile for various market conditions.

Objective Signals: The use of quantitative thresholds for entry and exit reduces emotional bias in trading decisions (Tversky & Kahneman, 1974).

Enhanced Risk Management: By allowing traders to set stop loss and take profit levels, the strategy aids in preserving capital and managing risk effectively.

Limitations

Market Noise: The CCI can produce false signals, especially in highly volatile markets, leading to potential losses (Bollinger, 2001).

Lagging Indicator: As a lagging indicator, the CCI may not always capture rapid market movements, resulting in missed opportunities (Pring, 2002).

Conclusion

The CCI Threshold Strategy offers a systematic approach to trading based on well-established momentum principles. By focusing on overbought and oversold conditions, traders can make informed decisions while managing risk effectively. As with any trading strategy, it is crucial to backtest the approach and adapt it to individual trading styles and market conditions.

References

Bollinger, J. (2001). Bollinger on Bollinger Bands. New York: McGraw-Hill.

Lambert, D. (1980). Commodity Channel Index. Technical Analysis of Stocks & Commodities, 2, 3-5.

Pring, M. J. (2002). Technical Analysis Explained. New York: McGraw-Hill.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124-1131.