VWAP SESSION BUY SELL STRATEGY (INDICATOR) (PDK1977)VWAP SESSION BUY SELL STRATEGY (INDICATOR) (PDK1977)

This indicator combines the proven UT Bot breakout engine but with VWAP directional filtering and ATR-based take profit levels.

It delivers clean, high-probability trend entries and automatic volatility-calibrated exits.

How it works:

Buy only when price is above VWAP

Sell only when price is below VWAP

UT Bot confirms momentum with ATR-based trailing logic

ATR Take Profit gives consistent exits based on volatility

Bars turn green/red only while in a trade, back to normal after TP

Best For:

Intraday and swing trading

Indices, FX, crypto, and high-volume stocks but also for Forex with right TF and settings

Traders who want clean signals and minimal noise

2. Trade Checklist:

Use this before every entry. Quick, simple, reliable.

BUY Checklist:

Price confirmed above VWAP

Label prints BUY

Enter on Buy label (on bar close)

→ Hold until ATR TP hits

SELL Checklist:

Price below VWAP

Label prints SELL

Enter on Sell label

→ Hold until ATR TP hits

Avoid Entries When:

Price is chopping tightly around VWAP

Major news events are about to release

Volume is extremely low

ATR is shrinking rapidly (market compression)

3. Risk-Management Guide

This is tailored to how your system actually behaves.

1. Use ATR TP as Primary Exit:

The system automatically calculates a TP based on volatility:

High volatility → larger TP

Low volatility → smaller TP

This keeps trades consistent and avoids lingering too long.

2. Stop-Loss Recommendation

This strategy is designed for TP-only exits, but if you want a SL:

Recommended Stop-Loss:

Use ATR’s opposite trail, OR

Use 1 × ATR behind your entry candle

This matches the system's internal logic.

3. Position Sizing

Since this system enters during momentum expansions, use:

1–2% max risk per trade

Reduce risk during high-impact news sessions

4. Understand VWAP Environment

Different VWAP conditions require different expectations:

Strong Trend (price far from VWAP)

Higher TP probability

Fewer whipsaws

Excellent continuation setups

Chop Zone (price flips above/below VWAP)

Do NOT trade

Signals lose edge

Wait for a clean break + UT confirmation

5. Choose Correct VWAP Reset for your trading and session

This dramatically improves results.

Market Recommended VWAP Reset

US Stocks New York Session

Indices Daily

Forex London or New York

Crypto Daily or None

4. Final Tips for Best Performance

✔ Enter only in the direction of VWAP

✔ Don’t chase signals far away from entry candle

✔ Avoid trading right into major support/resistance

✔ ATR TP will handle exits mostly

Disclaimer

This script is provided for educational and informational purposes only.

It does not constitute financial advice, investment advice, trading advice, or any form of recommendation to buy or sell any financial instrument. The auto take no responsibility for loss or error in the script.

Average True Range (ATR)

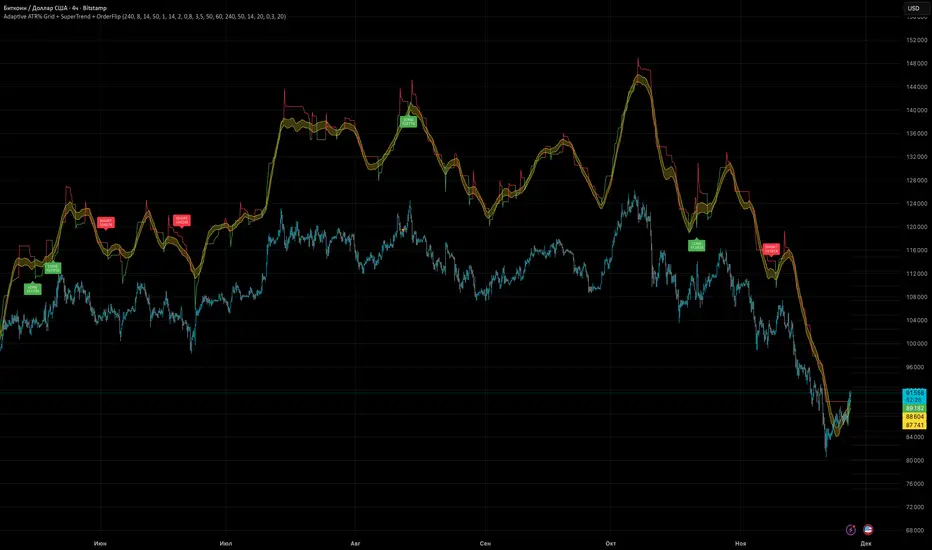

Adaptive ATR% Grid + SuperTrend + OrderFlipDescription:

This indicator combines multiple technical analysis tools to identify key price levels and trading signals:

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OrderFlip – identifies price reversal points relative to a moving average with ATR-based sensitivity, optionally filtered by OBV and DMI.

MTF Confirmation – multi-timeframe trend verification using EMA to reduce false signals.

Signal Labels – "LONG" and "SHORT" labels appear on the chart with an offset from the price for better visibility.

JSON Alerts – ready-to-use format for automated alerts, including price, SuperTrend direction, Fair Zone, and ATR%.

Features:

Fully compatible with Pine Script v6

Lines and signals are fixed on the chart, do not shift with new bars

Configurable grid, ATR, SuperTrend, and filter parameters

Works with MTF analysis and classic indicators (OBV/DMI)

Usage:

Best used with additional indicators and risk management strategies. ATR% Grid is ideal for both positional trading and intraday setups.

перевод на русский

Описание:

Этот индикатор объединяет несколько методов технического анализа для выявления ключевых уровней цены и сигналов на покупку/продажу:

Сетка ATR% (ATR% Grid) – автоматическое построение уровней поддержки и сопротивления на основе текущей цены и волатильности (ATR). Позволяет видеть потенциальные цели и зоны входа/выхода.

SuperTrend – классический трендовый индикатор с адаптивным множителем ATR, который корректируется на основе средней волатильности.

OrderFlip – определение моментов разворота цены относительно скользящей средней с учетом ATR, с возможностью фильтрации по OBV и DMI.

MTF-подтверждение – проверка направления тренда на нескольких таймфреймах с помощью EMA, чтобы снизить ложные сигналы.

Сигнальные метки – на графике появляются "LONG" и "SHORT" с отступом от цены для наглядности.

JSON Alerts – готовый формат для автоматических уведомлений, включающий цену, направление SuperTrend, Fair Zone и ATR%.

Особенности:

Поддержка Pine Script v6

Линии и сигналы закреплены на графике, не двигаются при обновлении свечей

Настраиваемые параметры сетки, ATR, SuperTrend и фильтров

Совместимость с MTF-анализом и классическими индикаторами OBV/DMI

Рекомендации:

Используйте в сочетании с другими индикаторами и стратегиями управления риском. Сетка ATR% отлично подходит для позиционной торговли и интрадей.

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

[CT] ATR Chart Levels From Open ATR Chart Levels From Open is a volatility mapping tool that projects ATR based price levels directly from a user defined center price, most commonly the current session open, and displays them as clean horizontal levels across your chart. The script pulls an Average True Range from a higher timeframe, by default the daily, using a user selectable moving average type such as SMA, EMA, WMA, RMA or VWMA. That ATR value is then used as the unit of measure for all projected levels. You can choose the ATR length and timeframe so the bands can represent anything from a fast intraday volatility regime to a smoother multi week average range.

The core of the tool is the center line, which is treated as zero ATR. By default this center is the current session open, but you can instead anchor it to the previous close, previous open, previous high or low, or several blended prices such as HLC3, HL2, HLCC4 and OHLC4, including options that use the minimum or maximum of the previous close and current open. From this center, the indicator builds a symmetric grid of ATR based levels above and below the zero line. The grid size input controls the spacing in ATR units, for example a value of 0.25 produces levels at plus or minus 25, 50, 75, 100 percent of ATR and so on, while the number of grids each side determines how far out the bands extend. You can restrict levels to only the upper side, only the lower side, or draw both, which is useful when you want to focus on upside targets or downside expansion separately.

The levels themselves are drawn as horizontal lines on the main price chart, with configurable line style and width. Color handling is flexible. You can assign separate colors to the upper and lower levels, keep the center line in a neutral color, and choose how the colors are applied. The “Cool Towards Center” and “Cool Towards Outermost” modes apply smooth gradients that either intensify toward the middle or toward the outer bands, giving an immediate visual sense of how extended price is relative to its average range. Alternatively, the “Candle’s Close” mode dynamically colors levels based on whether the current close is above or below a given band, which can help highlight zones that are acting as resistance or support in real time.

Each level is optionally labeled at its right endpoint so you always know exactly what you are looking at. The center line label shows “Daily Open”, or more generally the chosen center, along with the exact price. All other bands show the percentage of ATR and the corresponding price, for example “+25% ATR 25999.90”. The label offset input lets you push those tags a user defined number of bars to the right of the current price action so the chart remains clean while still keeping the information visible. As new bars print, both the lines and their labels automatically extend and slide to maintain that fixed offset into the future.

To give additional context about current volatility, the script includes an optional table in the upper right corner of the chart. This table shows the latest single period ATR value on the chosen higher timeframe alongside the smoothed ATR used for the bands, clearly labeled with the timeframe and ATR length. When enabled, a highlight color marks the table cells whenever the most recent ATR reading exceeds the average, making it easy to see when the market is operating in an elevated volatility environment compared to its recent history.

In practical trading terms, ATR Chart Levels From Open turns the abstract concept of “average daily range” into specific, actionable intraday structure. The bands can be used to frame opening range breakouts, define realistic intraday profit targets, establish volatility aware stop placement, or identify areas where price has moved an unusually high percentage of its average range and may be vulnerable to mean reversion or responsive flow. Because the ATR is computed on a higher timeframe yet projected on whatever chart you are trading, you can sit on a one minute or five minute chart and still see the full higher timeframe volatility envelope anchored from your chosen center price for the session.

15m ORB Breakout NAS100 (5m Mgmt) v6 - OptimizedOpening Range Breakout Strategy

Buy and sell signals are given upon break of market session opening range. Best utilized for 30 minute NY opening range, managed on 5 min timeframe on NAS100. Tweak the settings for higher win rate on backtesting dashboard before implementing strategy.

Position Size Calculator - R & ATR v1# Position Size Calculator - R & ATR

Professional position sizing tool for crypto traders using risk management principles and ATR-based stop loss placement.

## Features

✅ **Automatic ATR Calculation** - Uses ATR(14) by default, customizable period

✅ **Risk Management** - Calculate position size based on portfolio % risk

✅ **Tranche Support** - Split positions into multiple entries

✅ **Visual Stop Loss** - Red line showing stop loss placement on chart

✅ **Real-time Results** - Table displays all calculations instantly

✅ **Clean Interface** - Professional table with all key metrics

## How It Works

The indicator calculates optimal position size using this formula:

1. **Risk Amount** = Portfolio Size × (Risk % / 100)

2. **Stop Distance** = ATR × Multiplier

3. **Stop Loss Price** = Entry Price - Stop Distance

4. **Position Size** = Risk Amount / Stop Distance

5. **Tranche Size** = Position Size / Number of Tranches

## Settings

**Portfolio & Risk**

- Portfolio Size (USD): Your total trading capital

- Risk per Trade (R in %): Percentage of portfolio to risk per trade

- Number of Tranches: Split position into multiple entries

**ATR Settings**

- ATR Length: Period for ATR calculation (default: 14)

- ATR Multiplier: Multiply ATR for stop loss distance (0.5x, 1x, 1.5x, etc.)

**Display**

- Show Stop Loss Line: Toggle red stop loss line on chart

- Show Calculation Table: Toggle results table

## Results Displayed

- Risk Amount (1R): Dollar amount risked on trade

- Stop Distance: Distance from entry to stop loss

- Stop Loss: Exact stop loss price

- Risk per Coin: Amount risked per unit

- Position Size (coins): Number of coins to buy

Orbital Barycenter Matrix @darshaksscThe Orbital Barycenter Matrix is a visual, informational-only tool that models how price behaves around a dynamically calculated barycenter —a type of moving equilibrium derived entirely from historical price data.

Instead of focusing on signals, this indicator focuses on market structure symmetry, distance, compression, expansion, and volatility-adjusted movement.

This script does not predict future price and does not provide buy/sell signals .

All values and visuals come solely from confirmed historical data , in full compliance with TradingView policy.

📘 How the Indicator Works

1. Dynamic Barycenter (Core Mean Line)

The barycenter is calculated from a smoothed blend of historical price components.

It represents the center of mass around which price tends to oscillate.

This is not a forecast line—only a representation of historical average behavior.

2. Orbital Rings (Distance Zones)

Around the barycenter, the indicator draws several “orbital rings.”

Each ring shows a volatility-scaled distance from the barycenter using ATR-based calculations.

These rings help visualize:

How far price has drifted from its historical center

Whether price is moving in an inner, mid, or outer region

How volatility influences the spacing of the rings

Rings do not imply future targets and are informational only.

3. Orbital Extension Range

Beyond the outermost ring, a wider band (extension range) shows a high-volatility reference distance.

It represents extended displacement relative to past price behavior—not a projected target.

4. Orbit Trail (Motion Trace)

The Orbit Trail plots small circles behind price, helping visualize how price has moved through the orbital regions over time.

Colors adjust with “pressure” (distance from center), making compression and expansion easy to observe.

5. Satellite Nodes (Swing Markers)

Confirmed swing highs and lows (using fixed pivots) are marked as small dots.

Their color reflects the orbital zone they formed in, giving context to how significant or extended each pivot was.

These swing markers do not repaint because they use confirmed pivots.

6. Pressure & Distance Calculations

The indicator converts price displacement away from the barycenter into a pressure metric, scaled between 0%–100%.

Higher pressure means price is further from its historical center relative to volatility.

The dashboard displays:

Zone classification

ATR-based distance

Pressure level

A small intensity gauge

All are informational readings—no direction or forecast.

📊 Key Features

✔ Dynamic barycenter core

✔ Up to four orbital rings

✔ Informational orbital extension band

✔ Visual orbit trail showing recent movement

✔ Non-repainting satellite swing nodes

✔ Distance & pressure analytics

✔ Fully adjustable HUD

✔ Always-visible floating dashboard (screen-anchored)

✔ Zero repainting on confirmed elements

✔ 100% sourced from historical data only

✔ Policy-safe: no predictions, no signals, no targets

🎯 What to Look For

1. How close price is to the barycenter

This can reveal whether price is in:

The inner region

The mid zone

The outer region

The extended field

2. Pressure level

Shows how “stretched” price is relative to its past behavior.

3. Satellite nodes

Indicate where confirmed pivots formed and in which orbital band.

4. Ring interactions

Observe how price moves between rings—inside, outside, or oscillating around them.

5. Color changes in the orbit trail

These show changes in market compression/expansion.

🧭 How to Read the Indicator

Inner Orbit

Price close to its historical equilibrium.

Mid Orbit

Moderate displacement from typical range.

Outer Orbit

Historically extended movement.

Beyond Extension Field

Price has moved further than usual relative to historical volatility.

These are descriptive conditions only , not trade recommendations.

🛠 How to Apply It on the Chart

Use the barycenter to understand where price has historically balanced.

Observe how volatility changes the spacing between rings.

Use pressure readings to identify when price is compressed, neutral, or extended.

Use swing nodes to contextualize historical pivot formation.

Watch how price interacts with rings to better understand rhythm, velocity, and structural behavior.

This tool is meant to enhance visual understanding—not to generate trade entries or exits.

⚠️ Important Disclosure

This indicator is strictly informational.

It does not predict or project future price movement.

It does not provide buy/sell/long/short signals.

All lines, zones, and values are derived solely from past market data.

Any interpretation is at the user’s discretion.

FBB Buy/Sell ProDisclaimer : This script is for educational purposes only and does not constitute financial advice. Use at your own risk.

FBB Buy/Sell Pro is a volatility based reversal tool that builds a dynamic channel around a volume weighted moving average and highlights potential turning points at the extremes. The indicator paints a smooth "funnel" of bands around price and generates Buy/Sell labels when candles reject the outer zones, helping you spot exhaustion and mean reversion opportunities in trending or ranging markets.

Signals are based on price interaction with the outer bands combined with candle direction, optionally filtered by RSI to reduce noise. When enabled, the built in TP/SL module projects an ATR based stop and target using a configurable risk to reward ratio and clearly draws entry, risk and reward zones directly on the chart.

For tracking performance, FBB Pro includes an on chart statistics table that simulates trades using your own base capital, leverage and fee settings. It displays net profit, number of trades and win rate so you can quickly evaluate how the logic behaves on different symbols and timeframes.

Key features

Dynamic FBB volatility channel around VWMA with smooth gradient visualization

Clear reversal Buy/Sell labels at outer band reactions with optional RSI filter

Automatic TP/SL projection based on ATR and custom risk to reward

Realistic stats module with leverage and fee simulation shown in a compact table

Works on most markets and timeframes. It is recommended to combine FBB Buy/Sell Pro with your own higher timeframe context and risk management.

Dynamic Fair-Value Ribbon Pro @darshakssc1. What This Indicator Is (In Simple Terms)

The Dynamic Fair-Value Ribbon Pro is a visual tool that helps you see how price behaves around a statistically derived “fair-value zone”:

A colored ribbon/cloud marks a central “fair” area.

Areas above the ribbon are labeled as “Unfair High Zone”.

Areas below the ribbon are labeled as “Unfair Low Zone”.

A small state panel tells you where price currently sits relative to this ribbon.

All calculations are based only on historical price, volume, and volatility.

It does not predict future price, does not give buy/sell signals, and is not financial advice.

2. Adding the Indicator

Open a chart on TradingView.

Click on Indicators .

Search for “Dynamic Fair-Value Ribbon Pro” .

Click to add it to your chart.

You will see:

A cloud/ribbon around price.

Colored bars when price is outside the ribbon.

A panel in the top right describing the current state.

3. Core Concept: Fair vs Unfair Zones (Analytical Only)

The indicator tries to answer a descriptive question:

“Where is price trading relative to a historically derived central area?”

It does this by:

Calculating a central value (“fair mid”).

Building a band around that mid.

Coloring the chart depending on whether price is inside or outside that band.

It is not claiming that:

Price “must” return to the band.

Price is “overvalued” or “undervalued”.

Any state is good or bad.

It is simply a visual classification tool .

4. Engine Modes — How the Ribbon Is Calculated

Under “Fair-Value Engine” you can choose:

4.1 Mode 1: Range

Looks back over a chosen number of bars (default: 100).

Finds the highest high and lowest low in that window.

Defines a central “slice” of that range as the fair-value ribbon :

Range Mode: Lower Percent → bottom boundary of the slice (e.g., 30%).

Range Mode: Upper Percent → top boundary of the slice (e.g., 70%).

Effect:

The ribbon represents a middle portion of the historical range .

Above the ribbon = “Unfair High Zone” (analytical label only).

Below the ribbon = “Unfair Low Zone”.

This is purely statistical — it does not mean price is wrong or will revert.

4.2 Mode 2: VWAP + Stdev

In this mode, the central value is based on VWAP :

VWAP (Volume-Weighted Average Price) is used as the midline.

A standard deviation envelope is built around VWAP:

VWAP Mode: Stdev Multiplier controls how wide that envelope is.

Effect:

The ribbon shows where price is trading relative to a volume-weighted average .

Again, areas above and below are just described as “unfair” zones in a visual, analytical sense , not a predictive one.

5. ATR Adaptive Width — Making the Ribbon React to Volatility

Under “ATR Adaptive Width” :

Use ATR Adaptive Width:

On: the band width scales with volatility.

Off: band width stays fixed based on Range or VWAP settings.

ATR Length: how many bars to use for ATR.

Reference ATR (% of price): a reference level for normal volatility.

Min Width Scale / Max Width Scale: clamps the scaling so that the band doesn’t get too narrow or too wide.

What this does (analytically):

When volatility (ATR) is higher than the reference, the band can become wider .

When volatility is lower , the band can become narrower .

This is a mathematical rescaling only and does not imply any optimal levels or performance.

6. Visual Elements — What You See on the Chart

6.1 Fair-Value Ribbon (Cloud)

The cloud between Fair Ribbon Low and Fair Ribbon High is the fair zone .

Color can be changed via “Fair Ribbon Color” .

6.2 Midline

If “Show Center Line” is enabled:

A line runs through the middle of the ribbon.

In Range mode, this is the average of the upper and lower band.

In VWAP mode, it’s essentially the VWAP-based mid.

This line is for visual reference only and makes no claims about support, resistance, or reversion.

6.3 Bar Colors

Unfair High Zone: bars are colored with Unfair High Bar Color.

Unfair Low Zone: bars are colored with Unfair Low Bar Color.

Inside the ribbon:

If “Fade Bars Inside Fair Zone” is ON, bars may be more faded/neutral.

These colors are simply classification highlights ; they do not tell you what to do.

6.4 State Panel (Top Right)

If “Show State Panel” is enabled, you’ll see a small box that displays:

Current engine:

Range or VWAP+Stdev.

Current price state:

Inside Ribbon (Fair Zone)

Above Ribbon (Unfair High Zone)

Below Ribbon (Unfair Low Zone)

This is a quick summary of where price sits relative to the computed ribbon.

7. Typical Ways to Use It (Informational Only)

The indicator can help you visually:

See when price is spending time inside a historically defined central zone.

Notice when price is frequently trading outside that zone.

Compare different timeframes (e.g., 5m vs 1h vs 4h) to see how the fair zone shifts.

Experiment with:

Range length (shorter vs longer lookback).

VWAP vs Range mode.

ATR adaptation on/off.

Important:

Any interpretation of these visuals is entirely up to the user.

The script does not tell you to buy, sell, hold, or do anything specific.

8. Limitations and Important Notes

All calculations use past data only (price, volume, volatility).

The ribbon does not guarantee:

that price will revert,

that zones will hold,

or that any outcome will occur.

There are no built-in signals such as “long/short” or automatic entries/exits.

The script is best used as a supporting, visual layer alongside other tools or methods you choose.

9. Disclaimer

This indicator is:

Strictly informational and educational.

Not a trading system or strategy.

Not financial advice or a recommendation.

Not guaranteed to be accurate, complete, or suitable for any specific purpose.

Users should always perform their own research and due diligence.

Past behavior of any visual pattern or zone does not guarantee future behavior.

Average True Range % infoATR% is a modified version of the classic Average True Range indicator that displays price volatility as a percentage of the instrument's value, rather than in absolute values. This allows you to easily compare the volatility of different assets (e.g., Bitcoin vs Tesla stock) regardless of their price.

Main Features

1. ATR% Chart

The red line shows the average volatility from the last N candles (default 14), expressed as a percentage. For example:

ATR% = 2.5% means that the average daily move is approximately 2.5% of the asset's value

Higher values = greater volatility (higher profit potential, but also greater risk)

Lower values = lower volatility (calmer market)

2. Volatility Trend Analysis

The indicator automatically detects whether volatility is rising, falling, or stable:

Up arrow (↑) - volatility is rising (price becomes more "nervous")

Down arrow (↓) - volatility is falling (market is calming down)

Horizontal arrow (⮆) - volatility is stable (within ±3% of the moving average)

3. Information Table

In the upper right corner of the chart you will see Current ATR% value and Trend arrow with color coding:

- Green = rising volatility

- Red = falling volatility

- Gray = stable volatility

Parameters to Configure

Indicator Length (default: 14) - How many candles back to include in calculations:

Lower values (5-10): more sensitive to sudden changes, reacts faster

Higher values (20-30): more smoothed, shows long-term volatility picture

Trend Length (default: 10) - Period to analyze whether volatility is rising/falling:

Lower values: faster trend change signals

Higher values: more reliable, but slower signals

Sample Interpretations

ATR% Volatility Asset Type/Situation

< 1% Very low Stable blue-chip stocks, calm market

1-3% Low-medium Typical stocks, normal conditions

3-5% Medium-high Volatile stocks, cryptocurrencies at rest

5-10% High Cryptocurrencies, penny stocks

> 10% Extremely high Market panic, crash, pump & dump

SMC Trend Filter Strategy (EMA50/EMA200 + FVG)Overview

This strategy implements a multi-timeframe Smart Money Concept (SMC) trading system designed for intraday and swing trading.

It combines a Daily trend filter, Break of Structure (BOS) detection, Order Block (OB) zones, Fair Value Gap (FVG) confirmation, and an ATR-based trailing stop system to achieve structured and rule-based entries.

The strategy is fully automated for backtesting and allows users to evaluate SMC concepts without repainting or discretionary interpretation.

- Core Components

1. Higher-Timeframe Trend Filter (Daily EMA50/EMA200)

The strategy retrieves D1 data and determines market direction using EMA50 and EMA200:

Uptrend → EMA50 > EMA200

Downtrend → EMA50 < EMA200

Trades are only taken in the direction of the Daily trend to avoid counter-trend setups.

2. Market Structure & Break of Structure (BOS)

The strategy identifies swing highs/lows and detects when price breaks beyond them:

Bullish BOS: price closes above previous swing high

Bearish BOS: price closes below previous swing low

This forms the foundation of SMC market structure recognition.

3. Order Block Zone (OB)

Upon detecting a BOS, the strategy marks the previous candle as a potential Order Block:

For bullish BOS → OB = previous candle’s high/low

For bearish BOS → OB = previous candle’s high/low

The OB zone is visualized using a semi-transparent box extended forward

ATR multiple from High & LowA simple numerical indicator measuring ATR multiple from recent 252 days high and low.

ATR multiples from high (and low) are used as a base in many systematic trading and trend following systems. As an example many systems buy after a 2.5–4 ATR multiple pullback in a strong stock if the regime allows it. This would then be paired with an entry tactic, for example buy as it recaptures the a pivot within the upper range, a MA or breaks out again after this mid term pullback/shakeout.

This indicator uses a function which captures the recent high and low no matter if we have 252 bars or not, which is not how standard high/low works in Tradingview. This means it also works with recent IPO:s.

I prefer to overlay the indicator in one of the lower panes, for example the volume pane and then right click on the indicator and select Pin to scale > No scale (fullscreen).

Aquas TrendIt’s a trend-following crossover system with:

A local fast/slow EMA cross for timing entries

A higher-timeframe EMA filter to only trade in the dominant trend

An ATR-based volatility filter so it only trades when the market is moving

ATR-based stop loss and take profit with fixed RR

It tries to catch swings in the direction of the larger trend and ignore chop.

Reward-Risk Visual Zones (RRZ)Reward–Risk Visual Zones (RRZ) – Structure-Driven Risk Mapping Engine

Most indicators tell you when to trade.

RRZ is designed to answer a different question:

“Is this setup worth the risk before I take the trade?”

RRZ is not a mashup of unrelated indicators.

It is a 3-stage risk engine that builds a complete trade “story” around each swing:

1. Market structure pivot → defines the trade idea

2. ATR volatility unit → defines the risk size

3. Projected reward → compares reward vs that risk and filters bad setups

The output is a visual trade map : entry, target, stop, and R:R, printed directly on chart at each qualified swing.

1. Market Structure Layer – Where trades are anchored

RRZ doesn’t fire signals from MA/RSI crossovers.

It begins with s wing structure :

• Uses ta.pivotlow() and ta.pivothigh() with user-controlled left/right sensitivity:

• Pivot Sensitivity (L) controls how wide a swing must be to qualify as a structural pivot.

• Pivot Confirmation (R) controls how fast/slow a pivot is confirmed (1 = almost real-time, larger values = safer but later).

• A confirmed swing low becomes the candidate anchor for a long R:R zone.

• A confirmed swing high becomes the candidate anchor for a short R:R zone.

Each pivot is stored with its exact price and bar index , so the rest of the logic is always anchored to a real swing instead of a random candle.

2. Volatility Layer – Turning ATR into a “risk unit”

Once a pivot is confirmed, RRZ measures local volatility using ATR:

• ATR length is configurable via ATR Length.

• ATR is not used as a trailing stop or overlay.

In RRZ it plays one specific role:

“One ATR = one unit of structural risk from this swing.”

From that:

Long scenario:

• Entry = pivot low

• Stop = Entry − 1 × ATR

Short scenario:

• Entry = pivot high

• Stop = Entry + 1 × ATR

This standardizes risk across different volatility regimes:

a 2R move in a quiet market and a 2R move in a volatile market are both “2 × ATR” from the structure.

3. Reward Projection Layer – Evaluating if the trade is worth it

RRZ then estimates how far price can realistically travel away from the pivot, given recent behaviour:

For longs (from swing low):

• Projects reward using the highest high in a rolling lookahead window (e.g., last 20 bars).

• Reward = HighestHigh – PivotLow

• Risk = ATR

• R:R = Reward / ATR

For shorts (from swing high):

• Projects reward using the lowest low in the window.

• Reward = PivotHigh – LowestLow

• Risk = ATR

• R:R = Reward / ATR

The user can set a minimum R:R filter via Min R:R Threshold.

• If R:R ≥ threshold → zone is tagged as “ GOOD R:R ” and highlighted in green (long) or red (short).

• If R:R < threshold → optionally still shown as “ LOW R:R ” in orange (so you can visually see “tempting but not worth it” trades).

This transforms a raw pivot + ATR into a quantified decision:

“From this swing, volatility says my stop is 1× ATR. Do I even have 2× ATR of room in my favour?”

4. Execution Map – How components work together on chart

Instead of just printing numbers, RRZ builds a full execution template for every qualifying swing:

• Entry line at the pivot price

• Target line at the reward projection price

• Stop line at pivot ± ATR

• A structured label including:

• LONG / SHORT direction

• “GOOD R:R” or “LOW R:R”

• Numerical R:R (e.g., 2.3 : 1)

• Entry, Target, Stop, current Close

A Cooldown Bars parameter prevents overlapping spam:

• After an R:R zone is created (long or short), the script waits X bars before considering another zone in the same direction.

• This keeps charts readable and focuses attention on the most recent high-quality swings.

RRZ also includes line style controls (solid/dashed/dotted) and separate colours for entry, target, and stop, so traders can quickly read the chart even without opening settings.

5. How to Use RRZ in a Trading Plan

RRZ is not a magic “buy/sell” button.

It is designed to sit on top of your existing strategy as a risk filter.

Typical workflows:

SMC / price-action traders:

• Use your own logic for BOS/CHoCH, order blocks, or liquidity sweeps.

• Use RRZ only where structure aligns and the zone shows GOOD R:R ≥ 2.0.

• Avoid setups where RRZ marks LOW R:R even if the pattern looks good.

System traders / swing traders:

• Use RRZ to standardize risk across assets and timeframes.

• Filter out trades where potential reward does not justify the stop, based on current ATR.

Beginners:

• Learn to stop taking trades where the target is too close and the stop is too wide.

• Visually understand how structural swings and volatility interact.

RRZ works across Forex, Crypto, Indices, and Stocks on intraday and higher timeframes.

Once a pivot is confirmed and a zone is plotted, its lines and labels do not repaint.

⸻

6. Why this invite-only script is more than a basic mashup

RRZ does use classic building blocks (pivots, ATR), but the value is in the way they are stitched into a single risk framework:

• It doesn’t run multiple separate indicators on chart.

Everything is computed inside one engine with a single purpose: structure-based R:R evaluation.

• ATR is not just “slapped on” as a stop line; it is treated as the core risk unit in the R:R calculation pipeline.

• Every zone is a coherent trade idea: from swing, to risk unit, to projected reward, to filtered label, to execution lines.

• The script is designed specifically to help traders do the one thing that almost no free indicator prioritizes:

“Say NO to low R:R trades automatically.”

This is what distinguishes RRZ from generic ATR-stop scripts or simple pivot overlays.

⸻

Important

• No performance promises.

• No marketing claims (“guaranteed”, “high win rate”, etc.).

• Purely a risk mapping & visualization tool.

MTRA Pro+ ScreenerMTRA Pro+ Screener an analysis tool that provides traders with critical market structure information on up to 10 instruments simultaneously. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single dashboard.

## Key Features

- Customizable display with adjustable positioning, colors, and sizing

**Momentum & Trend Tracking**

- Real-time momentum direction via 5-period SMA slope analysis

- Short-term trend direction using 10-period SMA slope analysis

- Color-coded visual representation for quick interpretation

**Range Relationship Analysis**

- Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

- Three-period historical view of recent price action patterns

- Immediate identification of breakout and consolidation scenarios

**ATR-Based Volatility Analysis**

- Real-time ATR percentage calculations showing current range vs. average

- Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

- Identification of potential exhaustion zones for risk management

**Intraday ATR Levels**

- Dynamic support/resistance levels based on current timeframe ATR

- Real-time upper and lower boundaries for precise entries/exits

- Customizable line styles integrated with price scale

## Practical Applications

- **Context Assessment**: Quickly gauge market conditions across multiple intraday timeframes

- **Exhaustion Detection**: Identify overextended moves when ATR exceeds 100%

- **Confluence Analysis**: Spot potential setups when timeframes align

- **Risk Management**: Some traders will use ATR levels for dynamic stops and position sizing

- **Breakout Confirmation**: Distinguish false breakouts from genuine momentum shifts

## Configuration Options

- Full dashboard positioning and color customization

- Individual timeframe toggles

- Adjustable ATR periods and sensitivity thresholds

- Multiple line styles for level visualization

MTRA Intraday Pro+MTRA Pro Intraday is a multi-timeframe analysis tool that provides traders with critical market structure information across five intraday timeframes: 5m, 15m, 30m, 1h, and 4h. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single dashboard.

***Dashboard Timeframes that are low than chart timeframes can be inaccurate - Because of this always focus attention on the details on higher timeframes for accurate data****

## Key Features

**Multi-Timeframe Analysis**

- Simultaneous analysis across 5m, 15m, 30m, 1h, and 4h timeframes

- Customizable display with adjustable positioning, colors, and sizing

**Momentum & Trend Tracking**

- Real-time momentum direction via 5-period SMA slope analysis

- Short-term trend direction using 10-period SMA slope analysis

- Color-coded visual representation for quick interpretation

**Range Relationship Analysis**

- Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

- Three-period historical view of recent price action patterns

- Immediate identification of breakout and consolidation scenarios

**ATR-Based Volatility Analysis**

- Real-time ATR percentage calculations showing current range vs. average

- Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

- Identification of potential exhaustion zones for risk management

**Intraday ATR Levels**

- Dynamic support/resistance levels based on current timeframe ATR

- Real-time upper and lower boundaries for precise entries/exits

- Customizable line styles integrated with price scale

## Practical Applications

- **Context Assessment**: Quickly gauge market conditions across multiple intraday timeframes

- **Exhaustion Detection**: Identify overextended moves when ATR exceeds 100%

- **Confluence Analysis**: Spot high-probability setups when timeframes align

- **Risk Management**: Use ATR levels for dynamic stops and position sizing

- **Breakout Confirmation**: Distinguish false breakouts from genuine momentum shifts

## Configuration Options

- Full dashboard positioning and color customization

- Individual timeframe toggles

- Adjustable ATR periods and sensitivity thresholds

- Multiple line styles for level visualization

## Who Benefits

- **Scalpers**: 5m/15m alignment for quick entries

- **Day Traders**: Multi-timeframe confluence for swing entries within the day

- **Intraday Swing Traders**: 1h/4h context for position holds

MTRA Pro Intraday transforms complex multi-timeframe analysis into clear, actionable market structure data without switching charts. This tool enhances decision-making by providing objective context across all relevant intraday timeframes in one view.

Pele CandlesPele Candles Indicator

Named after Pele, the Hawaiian goddess of volcanoes, this indicator identifies "explosive" candles with unusually large ranges that exceed a customizable ATR (Average True Range) threshold. These volcanic-like price movements often signal significant market activity where liquidity may have been swept from one side.

Pele candles appear as colored bars (blue for bullish, purple for bearish) when candle ranges surpass the ATR multiplier. While a single Pele candle doesn't guarantee direction, consecutive Pele candles in opposite directions can indicate potential trend reversals - much like volcanic eruptions that reshape the landscape.

The indicator helps traders spot moments of intense market activity and potential turning points, but should be used alongside other analysis tools for confirmation.

Features:

Customizable ATR period and multiplier

Visual highlighting of explosive price moves

Alert notifications for significant candles

No repainting - signals appear in real-time

******Make sure you go to visual order settings and bring to front******

Pua CandlesPua Candles Indicator

Named after "Pua," the Hawaiian word for flower, this indicator identifies small, delicate price movements that often precede significant market expansion. Like tiny flowers that can bloom into something magnificent, Pua candles represent seemingly insignificant moments that frequently mark exhaustion areas in the market.

Pua candles are both inside bars (contained within the previous bar's range) and small relative to the ATR threshold. These quiet, compressed price actions often signal consolidation before major moves. When price eventually expands beyond these delicate formations, it can lead to substantial directional movement.

The indicator highlights bullish Pua candles in teal and bearish ones in pink, making these critical junctures easy to spot. Pay special attention to follow-through action after Pua candles - they often mark the calm before the storm.

Features:

Identifies inside bars with small ATR-relative ranges

Customizable ATR period and smallness threshold

Visual highlighting with Hawaiian-inspired colors

Alert notifications for Pua formations and follow-through

No repainting - confirmed signals only

Perfect for spotting potential breakout setups and market turning points.

******Make sure you go to visual order settings and bring to front******

MTRA Pro+Momentum - Trend - Range - ATR Dashboard!

MTRA Pro+ is a comprehensive multi-timeframe analysis tool designed to provide traders with critical market structure information across six different timeframes. This indicator consolidates momentum direction, trend analysis, range relationships, and volatility metrics into a single, customizable dashboard.

Core Features:

Multi-Timeframe Dashboard

Simultaneous analysis across Daily, 24H, Weekly, Monthly, Quarterly, and Yearly timeframes

Customizable display options to focus on relevant timeframes for your trading style

Professional dashboard with adjustable positioning, colors, and sizing

Momentum & Trend Analysis

Real-time momentum direction based on 5-period SMA slope analysis

Short-term trend direction using 10-period SMA slope analysis

Configurable sensitivity settings to filter out market noise

Color-coded visual representation for quick interpretation

Range Relationship Analysis

Current bar analysis relative to previous period (Inside, Outside, 2Up, 2Dn)

Three-period historical view showing recent price action patterns

Immediate identification of breakout and consolidation scenarios

Context for potential continuation or reversal setups

ATR-Based Volatility Analysis

Real-time ATR percentage calculations showing current range relative to average

Visual distinction between normal (<100% ATR) and extended (>100% ATR) conditions

Identification of potential exhaustion zones when price extends beyond typical volatility

Context for position sizing and risk management decisions

Daily ATR Level Visualization

Dynamic support and resistance levels based on current daily ATR

Real-time upper and lower boundaries for intraday trading

Customizable line styles and positioning options

Price scale integration for easy reference

Comprehensive Alert System

Momentum direction changes across all timeframes

Trend direction changes for longer-term position management

Range relationship status changes for breakout/breakdown alerts

ATR percentage threshold crossings for volatility-based signals

Practical Applications:

Market Context Assessment Quickly assess whether the market is trending, consolidating, or experiencing unusual volatility across multiple timeframes. This context helps inform position sizing, entry timing, and exit strategies.

Exhaustion Detection When ATR percentages exceed 100%, price may be overextended relative to typical volatility, potentially signaling pullback opportunities or areas to reduce position size.

Confluence Analysis Identify high-probability setups when multiple timeframes align in momentum and trend direction, or spot potential reversal zones when shorter timeframes diverge from longer-term trends.

Risk Management Enhancement Use ATR-based levels for dynamic stop placement and the dashboard's range analysis to understand current market structure before entering positions.

Breakout Confirmation Range relationship analysis helps distinguish between false breakouts and genuine momentum shifts by providing context about recent price action patterns.

Configuration Options:

Visual Customization

Full dashboard positioning control (9 positions available)

Customizable colors for all elements

Adjustable text size and border styling

Toggle individual timeframes on/off

Technical Parameters

Adjustable ATR periods for each timeframe

Configurable momentum sensitivity thresholds

ATR level display options with margin controls

Multiple line style choices for level visualization

Who Benefits from MTRA Pro+:

Swing Traders: Multi-timeframe trend and momentum alignment for position entries

Day Traders: Real-time ATR levels and range analysis for intraday decision-making

Position Traders: Longer timeframe context for strategic position management

Risk Managers: Volatility-based metrics for dynamic position sizing

Important Notes:

This indicator provides market structure analysis and context - it does not generate specific buy/sell signals. Success depends on combining this information with your trading methodology, proper risk management, and market experience. The tool is designed to enhance decision-making by providing objective market structure data across multiple timeframes.

MTRA Pro+ transforms complex multi-timeframe analysis into an accessible, visual format that helps traders stay informed about market conditions without the need to manually switch between charts and timeframes.

Tripwire Pro+Tripwire – Trail-Based Trend Direction Indicator

OVERVIEW

Tripwire is a powerful, volatility-adaptive trailing indicator designed to keep traders on the right side of momentum while offering signals and alerts based on the users settings and filters.

CONCEPT & INSPIRATION

This indicator is directly inspired from the Zombie9Trail by Frosty (creator of the Zombie Pack and TickHunter for NinjaTrader).

When all filters are turned off, Tripwire replicates the core behavior of Zombie9Trail — delivering the same razor-sharp trailing logic.

Most of Frosty's testing has been done from the 1 minute time frame, while I have personally found for my style of trading the 5 minute time frame works better for me.

WHAT THIS VERSION ADDS — TradingView Enhancements

• Optional multi-layer trend filters (21, 34, 170 EMA) to separate high-probability pullbacks from actual trend changes

• Clean Buy/Sell/Pullback signal labels with alert conditions

• Real-time dashboard showing current trail value, trend state, and filter status

• Fully customizable ATR length, multiplier, source, and visual styling

• All values exported as plots — perfect for CSV download and strategy development

HOW TO USE

Filters ON (recommended for trend-following) → Take signals in the direction of the higher-timeframe trend. Great for staying in strong moves and avoiding fake outs.

Filters OFF (pure Zombie9Trail mode) → Possibly catch early reversals and ride new trends

CREDIT & RESPECT

Core trailing methodology and original genius: Frosty — creator of Zombie9Trail / Zombie Pack / TickHunter (NinjaTrader).

This TradingView adaptation was built in direct homage to his NinjaTrader work and with his encouragement. Everything beyond the base trailing logic (filters, dashboard, alerts, exportable plots, visual polish) is original.

DISCLAIMER

For educational and informational purposes only. Not financial advice. Past performance is no guarantee of future results. Test thoroughly.

WeeklyDealingRange Pro+ (Fib Edition)Weekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Fibonacci Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Optional function based alerts

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments

Session Ranges Pro+Session Range Zones – Professional Edition

OVERVIEW

Professional visualization of the classic opening-range / Initial Balance concept across Asian, London, and Regular (US) sessions.

Displays the high/low of the user-defined opening window as thick, hierarchical filled zones with optional Fibonacci and standard-deviation extensions plus full alerting.

CONCEPT BACKGROUND

Using the high and low of the first 30–60 minutes of a session as key support/resistance is public-domain knowledge that has been standard in institutional trading for decades (Initial Balance, Opening Range, Session Range, etc.).

On TradingView the same principle was popularized under the name “Defining / DealingRange / DR/IDR” by TheMas7er and others.

IMPLEMENTATION & VALUE ADDED

This indicator follows the established, public-domain range-calculation methodology but has been completely rewritten with the following original enhancements:

• Clean, filled High / Mid / Low zones for instant visual hierarchy

• Intuitive Asian / London / Regular session labelling and fully custom timing

• Comprehensive dynamic & static Fibonacci and 50%/100% standard-deviation extensions

• Alert conditions on every zone, midline, opening level, and extension line

• Modern, modular code architecture using arrays and custom drawing functions

• No repainting, lightweight performance on any intraday timeframe

HOW TO USE

Apply to 1–15 min charts. Select desired sessions and formation period (30 or 60 min typical).

Shaded zones serve as primary support/resistance; extensions provide measured-move targets.

CREDIT & TRANSPARENCY

Core methodology: public domain (Initial Balance / Opening Range / Session Range).

Early TradingView popularization of the DR/IDR naming and feature set: TheMas7er **(with thanks to community contributors like bmsitiaan and trading-guide for refinements)**.

**Utilizes PineCoders' VisibleChart library for optimized chart rendering.**

This script uses the same foundational principle and logical input options but is an independent implementation. All visual presentation, zone system, multi-session handling, extension systems, alerting framework, and underlying code structure are original.

DISCLAIMER

For educational and informational purposes only. Not financial advice. Past performance is no guarantee of future results. Test thoroughly on your instruments and timeframes.

PonoTrading WDRWeekly Dealing Range Indicator

Overview

The Weekly Dealing Range indicator identifies range + volatility based pivot levels that form at the close of the first trading session and extend for the entire week. This tool provides key reference points for both trending and range-bound market conditions.

What It Provides

Range High & Low: Weekly session extremes

Median Level: Mid-point of the weekly range

Weekly Open: First session opening price

Standard Deviation Extensions: Calculated levels above the high and below the low

Practical Application

These levels serve as:

Reversal zones for mean reversion setups

Support/resistance reference points

Target levels for existing positions

Framework for building trade ideas around high-probability pivot areas

Key Features

Traditional price crosses level alerts

Automatically updates each week

Clean, uncluttered chart display

Works across all timeframes

Suitable for all markets and instruments