Adaptive CE-VWAP Breakout Framework [KedArc Quant]Description

A structured framework that unites three complementary systems into one charting engine:

Chandelier Exit (CE) – ATR-based trailing logic that defines trend direction, stop placement, and risk/reward overlays.

Swing-Anchored VWAP (SWAV) – a dynamically anchored VWAP that re-starts from each confirmed swing and adapts its smoothness to volatility.

Pivot S/R with Volume Breaks – confirmed horizontal levels with alerts when broken on expanding volume.

This script builds a single workflow for bias → trigger → managementwithout mixing unrelated indicators. Each module is internally linked rather than layered cosmetically, making it a true analytical framework—not.

Acknowledgment

Special thanks to Dynamic Swing Anchored VWAP by Zeiierman, whose swing-anchoring concept inspired a part of the SWAV module’s implementation and adaptation logic.

Support and Resistance Levels with Breaks by LuxAlgo for S/R breakout logic.

How this helps traders

Trend clarity – CE color-codes direction and provides evolving stops.

Context value – SWAV traces adaptive mean paths so traders see where price is heavy or light.

Action filter – Pivot+volume logic highlights true structural breaks, filtering false moves.

Discipline tool – Optional R:R boxes visualize risk and target zones to enforce planning.

Entry / Exit guidelines (for study purposes only)

Bias Use CE direction: green = long bias red = short bias

Entry

1. Breakout method– Trade in CE direction when a pivot level breaks on valid volume.

2. VWAP confirmation– Prefer breaks occurring around the nearest SWAV path (fair-value cross or re-test).

Exit

Stop = CE line / recent swing HL / ATR × (multiplier)

Target = R-multiple × risk (default 2 R)

Optional live update keeps SL/TP aligned with current CE state.

Core formula concepts

ATR Stop: Stop = High/Low – ATR × multiplier

VWAP calc: Σ(price × vol) / Σ(vol) anchored at swing pivot, adapted by APT (Adaptive Price Tracking) ratio ∝ ATR volatility.

Volume oscillator: 100 × (EMA₅ – EMA₁₀)/EMA₁₀; valid break when threshold %.

Input configuration (high-level)

Master Controls

Show CE / SWAV modules Theme & Fill opacity

CE Section

ATR period & multiplier Use Close for extremums

Show buy/sell labels Await bar confirmation

Risk-Reward overlay: R-multiple, Stop basis (CE/Swing/ATR×), Live update toggle

SWAV Section

Swing period Adaptive Price Tracking length Volatility bias (ATR-based adaptation) Line width

Pivot & Volume Breaks

Left/Right bar windows Volume threshold % Show Break labels and alerts

Best timeframes

Intraday: 5 m – 30 m for breakout confirmation

Swing: 1 h – 4 h for trend context

Settings scale with instrument volatility—adjust ATR period and volume threshold to match liquidity.

Glossary

ATR: Average True Range (volatility metric)

CE: Chandelier Exit (trailing stop/trend filter)

SWAV: Swing-Anchored VWAP (anchored mean price path)

Pivot H/L: Confirmed local extrema using left/right bar windows

R-multiple: Profit target as a multiple of initial risk

FAQ

Q: Does it repaint? A: No—pivots wait for confirmation and VWAP updates forward-only.

Q: Can modules be disabled? A: Yes—each section has its own toggle.

Q: Can it trade automatically? A: This is an indicator/study, not an auto-strategy.

Q: Is this financial advice? A: No—educational use only.

Disclaimer

This script is for educational and analytical purposes only.

It is not financial advice. Trading involves risk of loss. Past performance does not guarantee future results. Always apply sound risk management.

Vwaps

ZenAlgo - BoxerThis indicator plots multi-period Volume-Weighted Average Price (VWAP) ranges and deviation bands across several timeframes — specifically weekly, monthly, quarterly, semi-annual, and yearly. It is designed to visualize how price evolves relative to statistically weighted value areas within each period, based on both traded price and volume distribution.

Each timeframe layer is drawn independently, using its own cumulative VWAP and standard deviation calculation, and displayed as horizontal ranges aligned precisely with calendar periods. This structure allows the chart to show where price currently trades relative to past value zones and how each higher-timeframe VWAP acts as a dynamic reference for mean reversion or continuation.

Calculation Logic

1. Source and Base Inputs

The indicator uses the average of high, low, and close as its price source.

Stocks reset daily at session open.

2. VWAP and Deviation Computation

For each active timeframe, it accumulates the product of price and volume and divides it by cumulative volume, forming a continuously updated VWAP within that period.

The dispersion of price around VWAP is measured through a volume-weighted variance, converted to standard deviation.

These values form symmetrical bands around the VWAP (±1σ, ±2σ, etc.), describing the statistically typical price spread.

3. Range Drawing and Persistence

When a new period begins (e.g., a new week or month), the script finalizes the previous VWAP and deviation values, fixes them to time coordinates representing the full duration of that completed period, and draws corresponding lines or boxes across the entire range.

The user can control how many historical periods remain visible, ensuring performance and clarity even on high-frequency charts.

Each band can be toggled independently (for example ±1, ±2, ±3 deviations), and colors are adjustable per timeframe.

4. Adaptive Time Anchors

The start of each timeframe is aligned with calendar boundaries.

For stocks, the start time aligns with 9:30 New York time to coincide with market open for NYSE.

Each new anchor triggers a reset of cumulative data and creation of a new VWAP range.

5. Visualization Structure

The weekly layer is drawn first and can optionally display live VWAP bands extending backward for a user-defined number of weeks.

Monthly, quarterly, semi-annual, and yearly layers use the same computation principle but with independent accumulation windows.

The central VWAP line is dashed, while outer deviation levels are drawn as dotted or solid lines depending on their multiplier.

Boxes are rendered for key deviation intervals (e.g., ±2σ) to highlight broader value zones.

Interpretation

The VWAP represents the mean price weighted by traded volume for the given period.

Deviation bands describe statistically typical distance from that mean; outer bands mark less frequent extremes.

When price remains within ±1σ or ±2σ, it suggests balance around fair value.

Repeated touches or breaks beyond outer deviations indicate expansion or compression of volatility relative to prior periods.

Overlaps of VWAPs from multiple timeframes reveal multi-period confluence zones, useful for observing where long-term and short-term value agree or diverge.

Recommended Timeframes by Range Type

Weekly Range

Recommended timeframe: 30m to 12h

Suggested options: 30m, 1h, 2h, 3h, 4h, 6h, 8h, 12h

Using lower timeframes (like 5m) is technically possible, but higher ones provide smoother visualization and better readability.

Monthly Range

Recommended timeframe: 1h to 1D

Suggested options: 1h, 2h, 3h, 4h, 6h, 8h, 12h, 1D

Lower timeframes such as 30m may not display the full monthly range due to TradingView’s bar limits, so use higher TFs for complete coverage.

Quarterly Range

Recommended timeframe: 4h to 1W

Suggested options: 4h, 6h, 8h, 12h, 1D, 1W

Quarterly ranges benefit from higher timeframes to ensure that enough historical data is visible without exceeding chart limits.

Semi-Annual Range

Recommended timeframe: 12h to 1M

Suggested options: 12h, 1D, 1W, 1M

Lower timeframes would require too many bars to load a full six-month range; higher TFs offer a clearer overview.

Yearly Range

Recommended timeframe: 1D to 1M or higher

Suggested options: 1D, 1W, 1M

Yearly ranges often cannot display correctly on low timeframes (e.g. 1h) because of TradingView’s maximum bar limits — for instance, five years of 1h data exceeds 40,000 bars. Use higher TFs for accurate rendering.

Added Value Compared to Common Free VWAP Indicators

Incorporates five independent timeframes simultaneously (week, month, quarter, half-year, year) with exact calendar anchoring and timezone handling.

Calculates volume-weighted deviation for each layer, maintaining consistent statistical scale across assets.

Provides historical box persistence , allowing comparison of completed VWAP structures instead of only current running lines.

Enables selective visibility, bandwidth control, and precise visual differentiation through adjustable colors and line weights.

Limitations and Notes

The indicator does not generate trading signals. It is purely analytical and descriptive.

On very low timeframes or illiquid assets, deviation values may fluctuate if volume data is inconsistent.

Historical boxes are approximate in length for months with fewer than 31 days; this simplification has negligible effect on interpretation.

High visual density may occur when enabling many deviations or timeframes at once; users should limit visible history for performance.

Best Usage Practices

Apply on intraday charts (5–240 min) to study how price interacts with weekly or higher-timeframe VWAP zones.

Observe convergence of VWAPs from multiple periods to locate significant equilibrium levels.

Use outer deviations to frame potential exhaustion or re-entry zones rather than directional predictions.

Combine with independent volume- or structure-based analysis for context.

Vwap Daily By SamsungTitle

Daily VWAP with Historical Lookback (Logic Fix)

Description

This script calculates and plots the daily Volume-Weighted Average Price (VWAP), an essential tool for intraday traders.

What makes this indicator special is its robust plotting logic. Unlike many simple VWAP scripts that struggle to show data for previous days, this version includes a crucial fix that allows you to reliably display historical VWAP lines for as many days back as you need. This allows for more comprehensive backtesting and analysis of how price has interacted with the VWAP on previous trading days.

This is an indispensable tool for traders who use VWAP as a dynamic level of support/resistance, a benchmark for trade execution quality, or a gauge of the day's trend.

Key Features

Historical VWAP Display: Easily plot VWAP for multiple past days on your chart. Simply set the number of lookback days in the settings.

Accurate Daily Calculation: The VWAP calculation correctly resets at the beginning of each new trading session (00:00 server time).

Fully Customizable: You have full control over the appearance of the VWAP line, including its color, width, and style (Solid or Stepped).

Robust Plotting Engine: This script solves the common Pine Script issue where conditionally plotted historical lines fail to render. It works reliably on all intraday timeframes.

Built-in Debug Mode: For advanced users or those curious about the inner workings, a comprehensive debug mode can be enabled to display raw VWAP values, cumulative volume, and timeframe warnings.

How to Use

Add the "Daily VWAP with Historical Lookback" indicator to your chart.

IMPORTANT: Make sure you are on an intraday timeframe (e.g., 1H, 30M, 15M, 5M, 1M). This indicator is designed for intraday analysis and will display a warning if used on a daily or higher timeframe.

Open the indicator's settings.

In the "VWAP Settings" tab, adjust the "Lookback Days to Display" to set how many previous days of VWAP you want to see. (e.g., 0 for today only, 1 for today and yesterday, 10 for the last 10 days).

Customize the line's appearance in the "Line Style" tab.

The "Logic Fix" Explained (For Developers)

A common challenge in Pine Script is conditionally plotting data for historical bars. Many scripts attempt this by dynamically changing the plot color to na (transparent) for bars that shouldn't be displayed. This method is often unreliable and can result in the entire plot failing to render.

This script employs a more robust and standard approach: manipulating the data series itself.

The Problem: plot(vwap, color = shouldPlot ? color.red : na) can be buggy.

The Solution: plot(shouldPlot ? vwap : na, color = color.red) is reliable.

Instead of changing the color, we create a new data series (plotVwap). This series contains the vwapValue only on the bars that meet our date criteria. On all other bars, its value is na (Not a Number). The plot() function is designed to handle na values by simply "lifting the pen," creating a clean break in the line. This ensures that the VWAP is drawn only for the selected days, with 100% reliability across all historical data.

Settings Explained

Lookback Days to Display: Sets the number of past days (from the last visible bar) for which to display the VWAP.

Line Color, Width, and Style: Standard cosmetic settings for the VWAP line.

Enable Debug Mode (Master Switch): Toggles all debugging features on or off. It is enabled by default to help new users.

Display Debug: Cumulative Volume: When enabled, it shows the daily cumulative volume in a gray area on a separate pane.

Display Debug: Raw VWAP Value: When enabled, it plots the raw, unfiltered VWAP calculation for all days on the chart, helping to verify the core logic.

This script is provided for educational and informational purposes. Trading involves significant risk. Always conduct your own research and analysis before making any trading decisions.

If you find this script useful, a 'Like' is always appreciated! Happy trading

Multi-Anchor VWAP Deviation Dashboard Overview

Multi-Anchor VWAP Deviation Dashboard (Optimized Global) is an overlay indicator that computes up to five user-defined Anchored Volume Weighted Average Prices (AVWAPs) from custom timestamps, plotting their lines and displaying real-time percentage deviations from the current close. It enables precise analysis of price positioning relative to key events (e.g., earnings, news) or periods (e.g., weekly opens), with a compact dashboard for quick scans. Optimized for performance, it uses manual iterative calculations to handle dynamic anchor changes without repainting.

Core Mechanics

The indicator focuses on efficient AVWAP computation and deviation tracking:

Anchor Configuration: Five independent anchors, each with a name, UTC timestamp (e.g., "01 Oct 2025 00:00" for monthly open), show toggle, and color. Timestamps define the calculation start—e.g., AVWAP1 from "20 Oct 2025" onward.

AVWAP Calculation: For each enabled anchor, it identifies the first bar at/after the timestamp as the reset point, then iteratively accumulates (price * volume) / total volume from there. Uses HLC3 source (customizable); handles input changes by resetting sums on new anchors.

Deviation Metric: For each AVWAP, computes % deviation = ((close - AVWAP) / AVWAP) * 100—positive = above (potential resistance), negative = below (support).

Visuals: Plots lines (linewidth 1–2, user colors); dashboard (2 columns, 6 rows) shows names (anchor-colored if enabled) and deviations (green >0%, red <0%, gray N/A), positioned user-selectable with text sizing. Updates on last bar for efficiency.

This setup scales deviations across volatilities, aiding multi-period bias assessment.

Why This Adds Value & Originality

Standard VWAPs limit to session anchors (daily/weekly); deviation tools often lack multiples. This isn't a simple mashup: Manual iterative AVWAP (no built-in ta.vwap reliance) ensures dynamic resets on timestamp tweaks—e.g., shift "Event" to FOMC date without recalc lag. The 5-anchor flexibility (arbitrary UTC times) + centralized dashboard (colored deviations at a glance) creates a "global timeline scanner" unique to event-driven trading, unlike rigid multi-VWAP scripts. It streamlines what requires 5 separate indicators, with % normalization for cross-asset comparison (e.g., SPY vs. BTC).

How to Use

Setup: Overlay on chart. Configure anchors (e.g., Anchor1: "Weekly Open" at next Monday 00:00 UTC; enable/show 2–3 for focus). Set source (HLC3 default), position (Top Right), text size (Small).

Interpret Dashboard:

Left Column: Anchor names (e.g., "Monthly Open" in orange).

Right Column: Deviations (e.g., "+1.25%" green = above, bullish exhaustion?).

Scan for confluence (e.g., all >+2% = overbought).

Trading:

Lines: Price near AVWAP = mean reversion; breaks = momentum.

Example: -0.8% below "Event" anchor post-earnings → potential bounce buy.

Use on 1H–D; adjust timestamps via calendar.

Tips: Enable 1–3 anchors to avoid clutter; test on historical events.

Limitations & Disclaimer

AVWAPs reset on anchor bars, potentially lagging mid-period; deviations are % only (add ATR for absolute). Table updates on close (no intrabar). Timestamps must be UTC/future-proof. No alerts/exits—integrate manually. Not advice; backtest deviations on your assets. Past ≠ future. Comments for ideas.

The VWAP OracleOverview

The VWAP Oracle is a sophisticated overlay indicator that elevates VWAP (Volume Weighted Average Price) from a simple benchmark to an intelligent oracle for intraday and swing decisions. It offers flexible anchoring (rolling MVWAP, weekly, monthly, yearly) with session options, augmented by heuristic "AI/ML" elements for trend forecasting, dynamic S/R identification, and mean-reversion pullback strategies. A comprehensive dashboard delivers at-a-glance intel on trends, roles, touch history, and trade stats, complemented by visual zones, entry shapes, and alerts. Tailored for active traders in equities, forex, or futures, this iteration refines state handling and role logic for seamless execution on Pine v6.

Core Mechanics

Built around robust VWAP computations with layered analytics:

VWAP Framework: Primary line via user-selected type—Rolling (volume-weighted over lookback bars for agility), or Anchored (resets on week/month/year changes). HLC3 source standard; regular or 24h sessions. Toggles for secondary lines (e.g., weekly in orange for context).

Heuristic Enhancements: ATR safeguards (min tick fallback) normalize zones (± sensitivity * ATR for touches) and distances (e.g., 3x for setups). Linear regression over lookback derives slope (ATR-scaled for cross-asset comparability), flagging strong trends (> threshold) with rising/falling confirmation and volume >20-bar SMA.

Role & Proximity Engine: Scans enabled VWAPs globally—assigns nearest as support (price above, higher value prioritized) or resistance (below, lower prioritized), e.g., "Weekly" if closest. Tracks main VWAP touches for strength tiers (Weak <3, Moderate 3-4, Strong 5-7, Proven ≥8).

Pullback Strategy: In validated trends (slope + price move + volume), distant deviations (> ATR multiple) trigger "awaiting" state. Confirms entries on fresh touches with directional candles (close > open for longs), setting ATR-based stops (1x offset from VWAP) and targets (2x extension). Manages to hit (success tally) or breach (reset); daily/anchor resets clear stats.

Outputs: Trend-colored VWAP (blue/red in strong regimes, gray in range), role-tinted zones (green/red fill), triangles for entries, labels for outcomes.

Why This Mashup Adds Value & Originality

Traditional VWAPs are passive lines; multi-anchor plots add clutter without synthesis. Here, the fusion of anchored/rolling VWAPs with regression-normalized "AI" slope (volatility-adjusted for invariance) and touch-based strength scoring forms a predictive layer—e.g., "Proven" supports from 8+ interactions signal higher-probability bounces than raw levels. Stateful pullback logic (distant setup → touch entry → managed exit) with explicit breach cancels differentiates it from basic deviation oscillators, while the 11-row dashboard (trend icons, nearest roles, live success %) consolidates what would take multiple indicators. Global role reassignment (no function var limits) ensures accuracy, creating a unified "oracle" for confluence without redundancy—ideal for evolving static VWAP into adaptive decision support.

How to Use

Configuration: Overlay on chart. VWAP: Pick Rolling for scalps (252-bar default); enable weeklies for bias. AI: ATR 14, sensitivity 0.5 (tighter for precision). Trade: 3x min distance setups, 2x/1x target/stop. Visuals: Dashboard top-right, zones on, signals toggled.

Dashboard Readout (semi-opaque black, size-adjustable):

Header/Type: "The VWAP Oracle" + active (e.g., "Rolling (MVWAP)").

Trend: 🔵/🔴 Strong or ⚪ Range—align trades accordingly.

Nearest S/R: "Main" support (green) for bounces; "Monthly" resistance (red) for fades.

Strength/Role: "Strong (5 touches)"; "Support" for current main bias.

Position: "🔄 Pullback Setup" flags opportunity; "⏳ Awaiting" pre-entry.

Success/Setup: "80% (4/5)"; 🟢 Long Active if running; volume "✅ Strong" validates.

Execution: Strong bull + distant alert → Long on green triangle touch → Trail to target label (✓) or stop (✗). Use zones for invalidation; alerts cover setups/hits. Suits 15m-4H on majors like NAS100.

Pro Tips: Backtest resets (daily intraday); tweak slope threshold (1.5) for noise.

Limitations & Disclaimer

Touches and entries confirm on close, introducing minor lag; rolling VWAP smooths but may trail sharp moves. Slope can oscillate in transitions—add manual filters. Stats reset periodically (e.g., daily), so sample sizes vary; "success" is backward-looking. No auto-sizing—cap risk at 1% equity. v6-optimized, but verify on live data. Not advice; simulate trades, as history ≠ future. Feedback welcome in comments.

Pivot Regime Anchored VWAP [CHE] Pivot Regime Anchored VWAP — Detects body-based pivot regimes to classify swing highs and lows, anchoring volume-weighted average price lines directly at higher highs and lower lows for adaptive reference levels.

Summary

This indicator identifies shifts between top and bottom regimes through breakouts in candle body highs and lows, labeling swing points as higher highs, lower highs, lower lows, or higher lows. It then draws anchored volume-weighted average price lines starting from the most recent higher high and lower low, providing dynamic support and resistance that evolve with volume flow. These anchored lines differ from standard volume-weighted averages by resetting only at confirmed swing extremes, reducing noise in ranging markets while highlighting momentum shifts in trends.

Motivation: Why this design?

Traders often struggle with static reference lines that fail to adapt to changing market structures, leading to false breaks in volatile conditions or missed continuations in trends. By anchoring volume-weighted average price calculations to body pivot regimes—specifically at higher highs for resistance and lower lows for support—this design creates reference levels tied directly to price structure extremes. This approach addresses the problem of generic moving averages lagging behind swing confirmations, offering a more context-aware tool for intraday or swing trading.

What’s different vs. standard approaches?

- Baseline reference: Traditional volume-weighted average price indicators compute a running total from session start or fixed periods, often ignoring price structure.

- Architecture differences:

- Regime detection via body breakout logic switches between high and low focus dynamically.

- Anchoring limited to confirmed higher highs and lower lows, with historical recalculation for accurate line drawing.

- Polyline rendering rebuilds only on the last bar to manage performance.

- Practical effect: Charts show fewer, more meaningful lines that start at swing points, making it easier to spot confluences with structure breaks rather than cluttered overlays from continuous calculations.

How it works (technical)

The indicator first calculates the maximum and minimum of each candle's open and close to define body highs and lows. It then scans a lookback window for the highest body high and lowest body low. A top regime triggers when the body high from the lookback period exceeds the window's highest, and a bottom regime when the body low falls below the window's lowest. These regime shifts confirm pivots only when crossing from one state to the other.

For top pivots, it compares the new body high against the previous swing high: if greater, it marks a higher high and anchors a new line; otherwise, a lower high. The same logic applies inversely for bottom pivots. Anchored lines use cumulative price-volume products and volumes from the anchor bar onward, subtracting prior cumulatives to isolate the segment. On pivot confirmation, it loops backward from the current bar to the anchor, computing and storing points for the line. New points append as bars advance, ensuring the line reflects ongoing volume weighting.

Initialization uses persistent variables to track the last swing values and anchor bars, starting with neutral states. Data flows from regime detection to pivot classification, then to anchoring and point accumulation, with lines rendered globally on the final bar.

Parameter Guide

Pivot Length — Controls the lookback window for detecting body breakouts, influencing pivot frequency and sensitivity to recent action. Shorter values catch more pivots in choppy conditions; longer smooths for major swings. Default: 30 (bars). Trade-offs/Tips: Min 1; for intraday, try 10–20 to reduce lag but watch for noise; on daily, 50+ for stability.

Show Pivot Labels — Toggles display of text markers at swing points, aiding quick identification of higher highs, lower highs, lower lows, or higher lows. Default: true. Trade-offs/Tips: Disable in multi-indicator setups to declutter; useful for backtesting structure.

HH Color — Sets the line and label color for higher high anchored lines, distinguishing resistance levels. Default: Red (solid). Trade-offs/Tips: Choose contrasting hues for dark/light themes; pair with opacity for fills if added later.

LL Color — Sets the line and label color for lower low anchored lines, distinguishing support levels. Default: Lime (solid). Trade-offs/Tips: As above; green shades work well for bullish contexts without overpowering candles.

Reading & Interpretation

Higher high labels and red lines indicate potential resistance zones where volume weighting begins at a new swing top, suggesting sellers may defend prior highs. Lower low labels and lime lines mark support from a fresh swing bottom, with the line's slope reflecting buyer commitment via volume. Lower highs or higher lows appear as labels without new anchors, signaling possible range-bound action. Line proximity to price shows overextension; crosses may hint at regime shifts, but confirm with volume spikes.

Practical Workflows & Combinations

- Trend following: Enter longs above a rising lower low anchored line after higher low confirmation; filter with rising higher highs for uptrends. Use line breaks as trailing stops.

- Exits/Stops: In downtrends, exit shorts below a higher high line; set aggressive stops above it for scalps, conservative below for swings. Pair with momentum oscillators for divergence.

- Multi-asset/Multi-TF: Defaults suit forex/stocks on 1H–4H; on crypto 15M, shorten length to 15. Scale colors for dark themes; combine with higher timeframe anchors for confluence.

Behavior, Constraints & Performance

Closed-bar logic ensures pivots confirm after the lookback period, with no repainting on historical bars—live bars may adjust until regime shift. No higher timeframe calls, so minimal repaint risk beyond standard delays. Resources include a 2000-bar history limit, label/polyline caps at 200/50, and loops for historical point filling (up to current bar count from anchor, typically under 500 iterations). Known limits: In extreme gaps or low-volume periods, anchors may skew; lines absent until first pivots.

Sensible Defaults & Quick Tuning

Start with the 30-bar length for balanced pivot detection across most assets. For too-frequent pivots in ranges, increase to 50 for fewer signals. If lines lag in trends, reduce to 20 and enable labels for visual cues. In low-volatility assets, widen color contrasts; test on 100-bar history to verify stability.

What this indicator is—and isn’t

This is a structure-aware visualization layer for anchoring volume-weighted references at swing extremes, enhancing manual analysis of regimes and levels. It is not a standalone signal generator or predictive model—always integrate with broader context like order flow or news. Use alongside risk management and position sizing, not as isolated buy/sell triggers.

Many thanks to LuxAlgo for the original script "McDonald's Pattern ". The implementation for body pivots instead of wicks uses a = max(open, close), b = min(open, close) and then highest(a, length) / lowest(b, length). This filters noise from the wicks and detects breakouts over/under bodies. Unusual and targeted, super innovative.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

VWAP Entry Assistant (v1.0)Description:

Anchored VWAP with a lightweight assistant for VWAP reversion trades.

It shows the distance to VWAP, an estimated hit probability for the current bar, the expected number of bars to reach VWAP, and a recommended entry price.

If the chance of touching VWAP is low, the script suggests an adjusted limit using a fraction of ATR.

The VWAP line is white by default, and a compact summary table appears at the bottom-left.

Educational tool. Not financial advice. Not affiliated with TradingView or any exchange. Always backtest before use.

Dual Session VWAPSeparate VWAP with 1 standard deviation band for the regular session as well as electronic session

VWAP + Multi-Condition RSI Signals + FibonacciPlatform / System

Platform: TradingView

Language: Pine Script® v6

Purpose: This script is an overlay indicator for technical analysis on charts. It combines multiple tools: VWAP, RSI signals, and Fibonacci levels.

1️⃣ VWAP (Volume Weighted Average Price)

What it does:

Plots the VWAP line on the chart, which is a weighted average price based on volume.

Can be anchored to different periods: Session, Week, Month, Quarter, Year, Decade, Century, or corporate events like Earnings, Dividends, Splits.

Optionally plots bands above and below VWAP based on standard deviation or a percentage.

Supports up to 3 bands with customizable multipliers.

Will not display if the timeframe is daily or higher and the hideonDWM option is enabled.

Visual on chart: A main VWAP line with optional shaded bands.

2️⃣ RSI (Relative Strength Index) Signals

What it does:

Calculates RSI with a configurable period.

Identifies overbought and oversold zones using user-defined levels.

Generates buy/sell signals based on:

RSI crossing above oversold → Buy

RSI crossing below overbought → Sell

Detects strong signals using divergences:

Bullish divergence: Price makes lower low, RSI makes higher low → Strong Buy

Bearish divergence: Price makes higher high, RSI makes lower high → Strong Sell

Optional momentum signals when RSI crosses 50 after recent overbought/oversold conditions.

Visual on chart:

Triangles for buy/sell

Different color triangles/circles for strong and momentum signals

Background shading in RSI overbought/oversold zones

Alerts: The script can trigger alerts when any of these signals occur.

3️⃣ Fibonacci Levels

What it does:

Calculates Fibonacci retracement and extension levels based on the highest high and lowest low over a configurable lookback period.

Plots standard Fibonacci levels: 0.146, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0

Plots extension levels: 1.272, 1.618, 2.0, 2.618

Helps identify potential support/resistance zones.

Visual on chart: Horizontal lines at each Fibonacci level, shaded with different transparencies.

Summary

This script is essentially a multi-tool trading indicator that combines:

VWAP with dynamic bands for trend analysis and price positioning

RSI signals with divergences for entry/exit points

Fibonacci retracement and extension levels for support/resistance

It is interactive and visual, providing both chart overlays and alert functionality for active trading strategies.

This code is provided for training and educational purposes only. It is not financial advice and should not be used for live trading without proper testing and professional guidance.

Ghost Signal — MTF EMA/VWAP Confluence SystemGhost Signal — MTF EMA/VWAP Confluence System

Purpose

Ghost Signal is an intraday trend-entry tool that tries to do one thing well: only fire when multiple, independent edges agree. It looks for pullbacks to the EMA-20 or clean trend-continuations, then gates those raw triggers behind VWAP/Anchored-VWAP alignment, higher-timeframe structure, momentum, spacing (anti-chop), volume and ATR context. The goal is fewer, higher-quality entries that avoid “death-by-a-thousand scalps” in chop.

What it plots

EMA 20/50/200 for trend structure and spacing (no-braid filter).

VWAP (session) and optional Anchored VWAP (Daily/Weekly/Monthly).

ENTRY labels when all filters pass.

A compact status table: HTF score (M/W/D/4H/15/5), VWAP/AVWAP arrows, EMA regime, slopes %, ATR%, spacing %, and distance from EMA-50.

How signals are built

Raw triggers (on chart TF or a lower “signal TF” for intrabar precision):

PB20: trend pullback that crosses back through EMA-20.

TC: trend-continuation when price holds the side of EMA-20 with limited gap.

Confluence filters (must pass):

EMA regime & slopes: 20>50>200 for longs (reverse for shorts) with minimum slope on EMA-20/50.

VWAP/AVWAP alignment: price must be above both for longs / below for shorts, with a configurable margin.

HTF structure score: combines M/W/D/4H/15/5 states and penalizes corrections.

Anti-chop spacing: minimum separation between 20↔50 and 50↔200.

Context: volume ≥ SMA×mult, ATR% ≥ floor, max distance from EMA-50 to avoid late chases.

Optional breakout: close > prior high (long) / < prior low (short).

Time lockouts: exclude known messy windows (open/close, FX rollover, etc.).

Adaptive slope (optional): slopes auto-tighten/loosen with market heat (ATR% & relative volume).

How to use

Works on 1–5m best; designed for futures, stocks, FX, and crypto.

Use the status table to confirm context (HTF score, VWAP arrows, slopes/ATR/spacing).

Pair with your own risk model; common templates: stop ≈ 1.5–2× ATR, TP ≈ 1.2–1.8R or an ATR trail.

Turn the Signal TF to “1” on 3m/5m charts if you want intrabar PB20 detection.

Why it helps

Ghost Signal tries to stack institutional anchors (VWAP/AVWAP), higher-timeframe bias, and momentum/structure so you participate in moves with real sponsorship—and sit out the braid.

Notes & limits

No indicator removes risk. Expect fewer signals on range days, slippage around news, and thinner markets to require stricter volume/spacing. Past results don’t guarantee future returns.

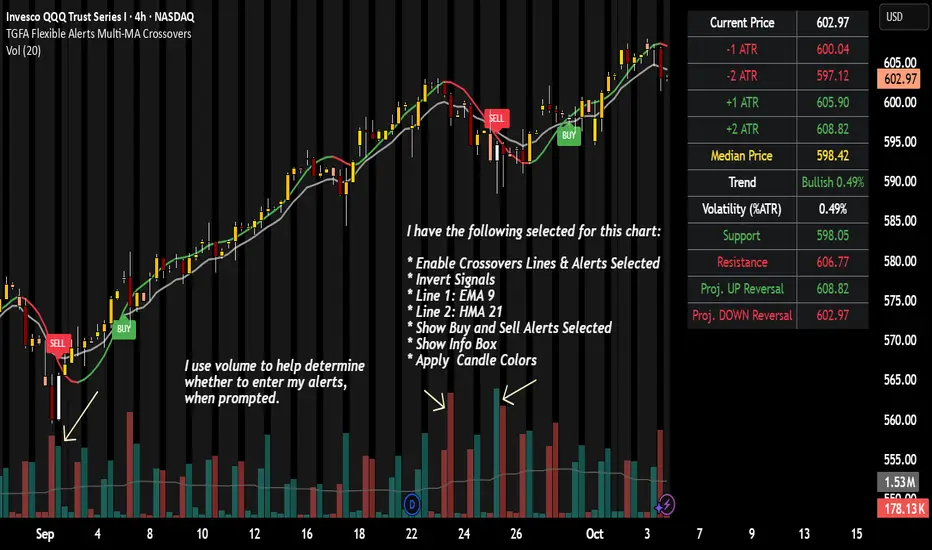

TGFA Flexible Alerts Multi-MA CrossoversTGFA Flexible Alerts, Multi-MA Crossovers

Description

Flexible MA crossovers with BUY/SELL alerts, customizable candle colors, and an info box for ATR/volatility insights. Supports EMA/SMA/HMA/VWAP on any chart.

Overview

TGFA Flexible Alerts is a versatile Pine Script indicator for traders seeking customizable moving average (MA) crossovers, visual signals, and quick-reference metrics. It overlays crossover lines (e.g., fast EMA over slow SMA), generates BUY/SELL labels and alerts, colors candles based on themes, and includes an optional info box with ATR bands, support/resistance, and trend projections. Built for any symbol and timeframe (optimized for 1H intraday), it auto-detects Heikin Ashi charts and handles mixed MA types like responsive HMA with lagging EMAs. All logic uses built-in TA functions for reliability—no repainting on confirmed bars.

Key Features

MA Crossover Engine: Configurable lines (EMA, SMA, HMA, VWAP) with dynamic colors (HMA tints green/red based on slope). Enable/disable via inputs.

Invert Signals Toggle: Flips BUY/SELL logic for mixed MA setups (e.g., HMA as fast line over EMA).

Reasoning: Traditional crossovers assume a fast line (low lag) crossing above a slow line (high lag) for buys. HMA's hull design makes it ultra-responsive, so it may "lead" too aggressively—causing premature signals. Inverting aligns it with user intuition (e.g., HMA dipping below then recovering signals strength), reducing false positives in trending markets. Test on your pairs!

Visual Alerts: BUY/SELL labels at crossover price (with optional price display and offset adjustment).

Single MA Overlays: Independent plots for EMA/SMA/HMA/VWAP (length 0 to hide).

Info Box: Real-time table with current price, ±1/2 ATR bands, median price (over lookback), trend (SMA50 slope), volatility % (ATR normalized), support/resistance (recent highs/lows), and reversal projections (tied to SMA50 pivot for up/down bias).

Candle Coloring: 20+ themes (dark/light canvases) for bull/bear/reversal/low-volume bars—e.g., Emerald Blaze greens uptrends, dims on low vol. Toggle off for no changes.

Chart Source Flexibility: Auto-switches to Heikin Ashi if detected; manual override for Regular/HA.

Alerts fire on crossovers/crossunders (custom messages with ticker/interval). Open-source for forking.

How to Use

Add to Chart: Search in TradingView's public library, apply to any symbol (e.g., stocks, forex). Best on 1H for intraday, but works on daily/weekly too.

Setup Crossovers: Choose Line 1/2 types/lengths (e.g., HMA 9 over SMA 20). Enable "Invert Signals" if using HMA—prevents lag mismatches in volatile assets.

Alerts & Labels: Toggle labels for visuals; set TradingView alerts on "Buy"/"Sell" conditions. Use offset for crowded charts.

Info Box Insights: Enable for quick scans—e.g., enter long near support if trend is bullish and price > median. Adjust ATR length (default 14) for sensitivity.

Candle Themes: Pick a scheme (e.g., Neon Pulse for dark mode); it overrides bar colors without altering data.

Customization Tip: For HMA-heavy setups, invert + short lengths (5-9) catch turns early; pair with volume filter in alerts.

Limitations & Disclaimers - Designed for overlay on price charts; may overlap in tight ranges—adjust transparency via styles.

HMA can repaint intra-bar; signals confirm on close. Not back tested for all assets—validate with strategy tester.

Info box projections use SMA(50) as a trend pivot (same for up/down as reference); customize via code for advanced calcs. Candle colors are cosmetic only.

This is an analysis tool, not advice. Trading involves risk; combine with fundamentals/news. Past performance isn't indicative of future results. No liability for losses.

I'm still a newbie, so feedback encouraged!

Thank you!!

ThisGirl

VWAP Multi Sessions + EMA + TEMA + PivotThis indicator combines several technical tools in one, designed for both intraday and swing traders to provide a complete view of market dynamics.

- VWAP Multi Sessions: calculates and plots five independent VWAPs, each based on a specific time range. This allows you to better identify value zones and price evolution during different phases of the trading day.

- Moving Averages (EMA): three strategic EMAs (55, 144, and 233 periods) are included to track the broader trend and highlight potential crossovers.

- TEMA (Triple Exponential Moving Average): two TEMAs (144 and 233 periods) offer a more responsive alternative to EMAs, reducing lag while filtering out some market noise.

- Daily Levels: the previous day’s open, close, high, and low are plotted as key support and resistance references.

- Pivot Point (P): also included is the classic daily pivot from the previous session, calculated as (High + Low + Close) / 3, which acts as a central level around which price often gravitates.

In summary, this indicator combines:

- intraday value references (session VWAPs),

- trend indicators (EMA and TEMA),

- and daily reference points (OHLC and Pivot).

It is particularly suited for intraday, scalping, and swing trading strategies, helping traders anticipate potential reaction zones in the market more effectively.

VWAP Daily/Weekly/Monthly - Automatic AnchoredExplanation:

This script plots Volume-Weighted Average Price (VWAP) lines that are automatically anchored to the beginning of key timeframes — daily, weekly, and monthly. VWAP is a widely used trading indicator that shows the average price of an asset weighted by trading volume, making it useful for identifying fair value and institutional trading levels.

The “automatic anchored” feature means that you don’t have to manually select starting points. Instead, the script automatically resets the VWAP at the start of each day, week, or month, depending on the chosen setting. This ensures the VWAP always reflects the true average price for that period, providing traders with a consistent reference for support, resistance, and trend direction across multiple timeframes.

Notice:

On the chart, you may notice visible “jumps” in the VWAP lines. These are intentional. Each jump marks the reset point at the start of a new day, week, or month, depending on the selected setting. This design keeps the VWAP history from the previous period intact, allowing you to clearly see how price interacted with VWAP in past sessions.

By keeping these historical resets, you can easily compare short-term (daily) VWAP behavior against longer-term levels like weekly and monthly VWAP. This provides valuable context, helping you spot when price respects or diverges from fair value across different timeframes.

In short:

Daily VWAP resets at the start of each trading day.

Weekly VWAP resets at the beginning of each trading week.

Monthly VWAP resets at the start of each month.

This makes it easy to analyze how price interacts with VWAP levels across different time horizons without manual adjustments.

Foresight Cone (HoltxF1xVWAP) [KedArc Quant]Description:

This is a time-series forecasting indicator that estimates the next bar (F1) and projects a path a few bars ahead. It also draws a confidence cone based on how accurate the recent forecasts have been. You can optionally color the projection only when price agrees with VWAP.

Why it’s different

* One clear model: Everything comes from Holt’s trend-aware forecasting method—no mix of unrelated indicators.

* Transparent visuals: You see the next-bar estimate (F1), the forward projection, and a cone that widens or narrows based on recent forecast error.

* Context, not signals: The VWAP option only changes colors. It doesn’t add trade rules.

* No look-ahead: Accuracy is measured using the forecast made on the previous bar versus the current bar.

Inputs (what they mean)

* Source: Price series to forecast (default: Close).

* Preset: Quick profiles for fast, smooth, or momentum markets (see below).

* Alpha (Level): How fast the model reacts to new prices. Higher = faster, twitchier.

* Beta (Trend): How fast the model updates the slope. Higher = faster pivots, more flips in chop.

* Horizon: How many bars ahead to project. Bigger = wider cone.

* Residual Window: How many bars to judge recent accuracy. Bigger = steadier cone.

* Confidence Z: How wide the cone should be (typical setting ≈ “95% style” width).

* Show Bands / Draw Forward Path: Turn the cone and forward lines on/off.

* Color only when aligned with VWAP: Highlights projections only when price agrees with the trend side of VWAP.

* Colors / Show Panel: Styling plus a small panel with RMSE, MAPE, and trend slope.

Presets (when to pick which)

* Scalp / Fast (1-min): Very responsive; best for quick moves. More twitch in chop.

* Smooth Intraday (1–5 min): Calmer and steadier; a good default most days.

* Momentum / Breakout: Quicker slope tracking during strong pushes; may over-react in ranges.

* Custom: Set your own values if you know exactly what you want.

What is F1 here?

F1 is the model’s next-bar fair value. Crosses of price versus F1 can hint at short-term momentum shifts or mean-reversion, especially when viewed with VWAP or the cone.

How this helps

* Gives a baseline path of where price may drift and a cone that shows normal wiggle room.

* Helps you tell routine noise (inside cone) from information (edges or breaks outside the cone).

* Keeps you aware of short-term bias via the trend slope and F1.

How to use (step by step)

1. Add to chart → choose a Preset (start with Smooth Intraday).

2. Set Horizon around 8–15 bars for intraday.

3. (Optional) Turn on VWAP alignment to color only when price agrees with the trend side of VWAP.

4. Watch where price sits relative to the cone and F1:

* Inside = normal noise.

* At edges = stretched.

* Outside = possible regime change.

5. Check the panel: if RMSE/MAPE spike, expect a wider cone; consider a smoother preset or a higher timeframe.

6. Tweak Alpha/Beta only if needed: faster for momentum, slower for chop.

7. Combine with your own plan for entries, exits, and risk.

Accuracy Panel — what it tells you

Preset & Horizon: Shows which preset you’re using and how many bars ahead the projection goes. Longer horizons mean more uncertainty.

RMSE (error in price units): A “typical miss” measured in the chart’s currency (e.g., ₹).

Lower = tighter fit and a usually narrower cone. Rising = conditions getting noisier; the cone will widen.

MAPE (error in %): The same idea as RMSE but in percent.

Good for comparing different symbols or timeframes. Sudden spikes often hint at a regime change.

Slope T: The model’s short-term trend reading.

Positive = gentle up-bias; negative = gentle down-bias; near zero = mostly flat/drifty.

How to read it at a glance

Calm & directional: RMSE/MAPE steady or falling + Slope T positive (or negative) → trends tend to respect the cone’s mid/upper (or mid/lower) area.

Choppy/uncertain: RMSE/MAPE climbing or jumping → expect more whipsaw; rely more on the cone edges and higher-TF context.

Flat tape: Slope T near zero → mean-revert behavior is common; treat cone edges as stretch zones rather than breakout zones.

Warm-up & tweaks

Warm-up: Right after adding the indicator, the panel may be blank for a short time while it gathers enough bars.

Too twitchy? Switch to Smooth Intraday or increase the Residual Window.

Too slow? Use Scalp/Fast or Momentum/Breakout to react quicker.

Timeframe tips

* 1–3 min: Scalp/Fast or Momentum/Breakout; horizon \~8–12.

* 5–15 min: Smooth Intraday; horizon \~12–15.

* 30–60 min+: Consider a larger residual window for a steadier cone.

FAQ

Q: Is this a strategy or an indicator?

A: It’s an indicator only. It does not place orders, TP/SL, or run backtests.

Q: Does it repaint?

A: The next-bar estimate (F1) and the cone are calculated using only information available at that time. The forward path is a projection drawn on the last bar and will naturally update as new bars arrive. Historical bars aren’t revised with future data.

Q: What is F1?

A: F1 is the indicator’s best guess for the next bar.

Price crossing above/below F1 can hint at short-term momentum shifts or mean-reversion.

Q: What do “Alpha” and “Beta” do?

A: Alpha controls how fast the indicator reacts to new prices

(higher = faster, twitchier). Beta controls how fast the slope updates (higher = quicker pivots, more flips in chop).

Q: Why does the cone width change?

A: It reflects recent forecast accuracy. When the market gets noisy, the cone widens. When the tape is calm, it narrows.

Q: What does the Accuracy Panel tell me?

A:

* Preset & Horizon you’re using.

* RMSE: typical forecast miss in price units.

* MAPE: typical forecast miss in percent.

* Slope T: short-term trend reading (up, down, or flat).

If RMSE/MAPE rise, expect a wider cone and more whipsaw.

Q: The panel shows “…” or looks empty. Why?

A: It needs a short warm-up to gather enough bars. This is normal after you add the indicator or change settings/timeframes.

Q: Which timeframe is best?

A:

* 1–3 min: Scalp/Fast or Momentum/Breakout, horizon \~8–12.

* 5–15 min: Smooth Intraday, horizon \~12–15.

Higher timeframes work too; consider a larger residual window for steadier cones.

Q: Which preset should I start with?

A: Start with Smooth Intraday. If the market is trending hard, try Momentum/Breakout.

For very quick tapes, use Scalp/Fast. Switch back if things get choppy.

Q: What does the VWAP option do?

A: It only changes colors (highlights when price agrees with the trend side of VWAP).

It does not add or remove signals.

Q: Are there alerts?

A: Yes—alerts for price crossing F1 (up/down). Use “Once per bar close” to reduce noise on fast charts.

Q: Can I use this on stocks, futures, crypto, or FX?

A: Yes. It works on any symbol/timeframe. You may want to adjust Horizon and the Residual Window based on volatility.

Q: Can I use it with Heikin Ashi or other non-standard bars?

A: You can, but remember you’re forecasting the synthetic series of those bars. For pure price behavior, use regular candles.

Q: The cone feels too wide/too narrow. What do I change?

A:

* Too wide: lower Alpha/Beta a bit or increase the Residual Window.

* Too narrow (misses moves): raise Alpha/Beta slightly or try Momentum/Breakout.

Q: Why do results change when I switch timeframe or symbol?

A: Different noise levels and trends. The accuracy stats reset per chart, so the cone adapts to each context.

Q: Any limits or gotchas?

A: Extremely large Horizon may hit TradingView’s line-object limits; reduce Horizon or turn

off extra visuals if needed. Big gaps or news spikes will widen errors—expect the cone to react.

Q: Can this predict exact future prices?

A: No. It provides a baseline path and context. Always combine with your own rules and risk management.

Glossary

* TS (Time Series): Data over time (prices).

* Holt’s Method: A forecasting approach that tracks a current level and a trend to predict the next bars.

* F1: The indicator’s best guess for the next bar.

* F(h): The projected value h bars ahead.

* VWAP: Volume-Weighted Average Price—used here for optional color alignment.

* RMSE: Typical forecast miss in price units (how far off, on average).

* MAPE: Typical forecast miss in percent (scale-free, easy to compare).

Notes & limitations

* The panel needs a short warm-up; stats may be blank at first.

* The cone reflects recent conditions; sudden volatility changes will widen it.

* This is a tool for context. It does not place trades and does not promise results.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

VWAP + Range Breakout (Pre-Signal for Manual Entry)WHAT IT DOES

This tool highlights potential breakout opportunities when price sweeps the previous day’s high or low and aligns with VWAP and short-term range levels. It provides both pre-signals (early warnings) and confirmed signals (breakout closed) so traders can prepare before momentum accelerates.

Works on all timeframes and across markets (indices, forex, crypto). Especially useful during active London and New York sessions.

---

KEY FEATURES

Daily sweep logic: previous day high/low as liquidity reference

VWAP with cumulative calculation

Adjustable range breakout levels

Optional SMA trend filter

Session filter (London / NY trading hours)

Pre-Signal markers (early alert before breakout)

Confirmed LONG/SHORT signals after breakout close

Alerts for Pre-Long, Pre-Short, and Confirmed entries

---

HOW TO USE

1. Wait for price to sweep the previous day high/low.

2. Look for alignment with VWAP and the defined range breakout levels.

3. Use trend/session filters for higher accuracy.

4. Combine with your own risk management rules.

---

SETTINGS TIPS

Adjust range lookback for different timeframes (shorter for fast intraday, longer for higher timeframes).

Enable/disable session filters depending on your market.

Use SMA trend filter to stay aligned with higher-timeframe bias.

---

WHO IT’S FOR

Scalpers, intraday, and swing traders who want early signals when liquidity is taken and price is preparing for a breakout.

---

NOTES

For educational purposes only. No financial advice.

This script is open-source; redistribution follows TradingView rules.

Smart Money LITE — Daily Sweep → HQ Signals (VWAP • FVG • CHoCH) 🔗 PRO VERSION (VWAP + FVG + CHoCH — full confirmations, all timeframes):

chartedgepro.gumroad.com/l/rmnbhw

Daily liquidity sweep → confluence signals with VWAP, FVG & CHoCH. Works on all timeframes & markets (Indices, Forex, Crypto).

WHAT IT DOES

Smart Money LITE+ highlights high-quality LONG/SHORT signals only after daily liquidity is swept (previous day high/low) with confluence from VWAP, FVG and structure (BOS/CHoCH).

Works on all timeframes and across markets: indices, forex, crypto.

KEY FEATURES (Lite)

• Daily sweep logic (PDH/PDL) + previous day zones

• VWAP + deviation bands (optional) and proximity filter

• 3-bar FVG boxes (visual) with adjustable extension

• ATR/volatility filter, optional HTF trend filter

• Anti-spam cooldown, clean LONG/SHORT labels

• Alerts: HQ LONG / HQ SHORT

HOW TO USE

1. Wait for price to sweep PDH/PDL → indicator opens “signal window”.

2. Look for confluence: VWAP touch/proximity + CHoCH or BOS in direction.

3. Enter with proper risk management (stop beyond swing/zone, partials).

SETTINGS TIPS

• Enable “Require VWAP Confluence?” for strictest setups.

• Use “HTF Trend Filter?” to align with higher-timeframe EMA trend.

• Adjust “After sweep (bars)” to define signal validity window.

• FVGs are visual in Lite — advanced filtering and confirmation are in Pro.

WHO IT'S FOR

Scalpers, intraday, and swing traders looking for objective, visual signals based on liquidity sweeps and VWAP/FVG confluence.

PRO VERSION (full confirmations)

Adds advanced FVG/iFVG logic, more confluence filters, dynamic risk tools and extended alert packages — optimized for all timeframes.

👉 chartedgepro.gumroad.com/l/rmnbhw

NOTES

• For educational purposes only. No financial advice.

• “Lite” is open-source; redistribution of code follows TradingView rules.

Dynamic EMA x VWAP AlertsDynamic EMA × VWAP Alerts generates buy and sell signals only when an EMA crossover happens in a meaningful VWAP (or standard deviation band) context. By combining classic EMA logic with flexible VWAP anchors (Daily, Weekly, Rolling) and optional advanced filters (ATR, Relative Volume, Deviation, Distance, Time Windows) to trim noise further, the script creates location-aware, filterable alerts rather than “everywhere” crosses. The value for trading and originality here lies in the integration of one or multiple anchors, band gating, combinator logic, and advanced regime filters. It’s designed for use across multiple instruments and timeframes, where EMA/VWAP context is relevant. It can run quietly in the background while you focus on price action and your own S/R levels.

What it does (quick take)

Detects EMA crossovers (double or optional triple) and evaluates them in VWAP context.

Plots Buy/Sell markers only when all chosen conditions are met.

Clean UX: keep all or parts of the engine visible or hide everything and let alerts run based on the silent engine behind your own S/R levels in an uncluttered, practical chart, as illustrated below.

Engine illustration: All selected engines visible

Practical use case: Same snapshot sequence as above but all selected engines invisible

Swing examples (beyond intraday)

Signals-only (clean value view):

Signals + your own S/R lines:

EMA selection (choose your playbook)

Defaults: Fast 9, Medium 21 (common intraday combo).

Modes: Double Cross — Fast vs Medium.

Triple Cross (optional) — adds a Slow EMA trend filter (enable Slow > 0).

Ranges: you can set each EMA 0–200 (0 = hidden/off)

Visuals are optional; you can display or hide each EMA line

EMA cross footprints (optional): Helps you assess trend continuation or change.

Use your own strategy: switch to 9/50, 20/50, 50/200, or whatever EMA set you trust for your instrument/timeframe.

VWAP Selection (the context engine)

Daily VWAP – resets each chart day (00:00–23:59). Typical fit: scalpers and fast intraday decision points.

Weekly VWAP – resets at the start of the calendar week. Typical fit: intraday with higher-timeframe context (aligns day trades with weekly bias).

Rolling VWAP – an adjustable VWMA-based rolling anchor (not session-reset), used as a flexible context reference Typical fit: multi-day swings when you want a flexible anchor that adapts across sessions.

Standard deviation bands (σ ±1/±2/±3) available for each anchor and help you express the “how far from fair value” idea.

Why VWAP matters: it’s a running, volume-weighted anchor where strong moves relative to VWAP and its bands help frame mean-reversion vs. trend-continuation risk. Evaluating crosses relative to VWAP/±σ reduces “everywhere” noise and helps frame potential setups.

How alerts are decided

An alert triggers only when:

Your selected EMA crossover occurs, and

Your chosen VWAP gate(s) and any filters pass. (Computed on bar close to avoid mid-bar noise)

Signals and alerts do not repaint; alerts evaluate and fire once per bar close.

Alert gates (Single / AND / OR)

Select one VWAP source or combine two (e.g., Daily + Weekly) with Single, AND, or OR logic.

Choose gate levels from VWAP or standard deviation bands (±σ). Typical long logic: price at/under VWAP or −σ. Typical short logic: price at/over VWAP or +σ.

Practical recipes:

Trend-follow: Daily AND Weekly at/above VWAP → confirms strength on two anchors.

Mean-reversion probe: Daily OR Rolling at −1σ → allows earlier fades with flexibility.

Advanced filtering: Suitable for advanced/Quant traders

During the research and development of this indicator, the EMA/VWAP cross logic was tested on historical S&P500 Futures data to explore patterns on multiple timeframes. These selected filtering indicators below showed correlation between certain market conditions and chosen indicator thresholds, helping reduce noise and lower-quality alerts. Results were research-oriented and are not predictive of future performance.

Therefore, I have built these indicator filters that run silently in the background. They let you trim noise by requiring alerts to appear only in market regimes you define. Each one constrains alert conditions; using them together helps tailor alerts to your strategy—but overly strict settings may filter out most or all alerts.

Relative Volume (RVOL): compares current volume to a baseline; ensures alerts arrive with participation instead of thin tape.

Deviation Threshold (%): controls how close the cross must be to the VWAP/σ level; tight = anchored signals, loose = more activity.

ATR Gate (+ Relative regime): keeps alerts inside a volatility regime; avoids both dead tape and chaotic spikes.

Distance Guard: requires price to be at least X ticks/% away from VWAP; useful to avoid premature signals near fair value.

Note: It’s not recommended to activate all of them at once or change the values aggressively. Unless you’ve done deeper backtesting or machine learning calibration, you can easily filter out everything. Use small thresholds at first, then adjust to your instrument once you see how each filter changes alert frequency and quality. Advanced/quant users can fine-tune freely.

Case example:

Unfiltered: Timeframe 15 min, EMA Selection 9/21, VWAP gates Rolling (250 bars) OR Weekly

Filtered: Same setup as above + activated filters:

RVOL: 100 bars, Min. RVOL 0.4

Deviation threshold (%): 0.3

ATR Length: 14

Min ATR (%): 0.05

Relative regime: Base length 2000, Min Ratio 0.85, Max Ratio 2

Under the hood

This indicator leans on TradingView built-ins (e.g., EMA, VWMA, ATR, alertcondition) to maximize speed, stability, and compatibility while we implement the custom logic (VWAP anchors, band gating, combinator gates, advanced filters, time windows). Built-ins were easy to work with and reduced edge-case bugs and kept the visuals responsive, while the design gives fine-tuning and clean visuals—so both discretionary traders and quant-minded users can shape the alerts to their strategy and workflow.

Disclaimer

The tools, scripts, and indicators presented here are provided for educational and informational purposes only. They are not financial advice and should not be interpreted as investment recommendations, trading signals, or a solicitation to buy or sell any financial instrument.

All forms of trading and investing involve risk. The past performance of any security, strategy, or market condition does not guarantee future outcomes. Users are solely responsible for their own trading and investment decisions, including evaluating their financial situation, objectives, and risk tolerance.

By using this indicator, you acknowledge that you do so at your own risk. The author accepts no liability for any direct or indirect loss or damage—including, without limitation, loss of profits—that may arise from the use of, or reliance upon, this tool.

Multi-Exchange VWAP Aggregator (Crypto)Description:

This advanced VWAP indicator aggregates volume data from up to 9 cryptocurrency exchanges simultaneously, providing a more accurate volume-weighted average price than single-exchange VWAP calculations.

Key Features:

Multi-Exchange Aggregation - Combines volume from Binance, Coinbase, Bybit, Bitfinex, Bitstamp, Deribit, OKEx, Phemex, and FTX

Flexible Currency Pairs - Supports both spot (USD, USDT, EUR, USDC, BUSD, DAI) and perpetual futures contracts

Standard Deviation Bands - Includes customizable 1σ, 2σ, and 3σ bands for identifying overbought/oversold levels

Multiple Reset Periods - Daily, Weekly, Monthly, or Session-based VWAP calculations

Volume Calculation Options - Choose between SUM, AVG, MEDIAN, or VARIANCE for volume aggregation

Why Use This?

Traditional VWAP indicators only use volume from a single exchange, which can be misleading in fragmented crypto markets. This indicator provides a comprehensive market-wide VWAP by aggregating volume across major exchanges, giving you a more reliable benchmark for entries, exits, and institutional price levels.

Perfect for traders who want to see where the real volume-weighted price sits across the entire crypto market, not just one exchange.

VWAP Trend Strategy (Intraday) [KedarArc Quant]Description:

An intraday strategy that anchors to VWAP and only trades when a local EMA trend gate and a volume participation gate are both open. It offers two entry templates—Cross and Cross-and-Retest—with an optional Momentum Exception for impulsive moves. Exits combine a TrendBreak (structure flips) with an ATR emergency stop (risk cap).

Updates will be published under this script.

Why this merits a new script

This is not a simple “VWAP + EMA + ATR” overlay. The components are sequenced as gates and branches that *change the trade set* in ways a visual mashup cannot:

1. Trend Gate first (EMA fast vs. slow on the entry timeframe)

Counter-trend VWAP crosses are suppressed. Many VWAP scripts fire on every cross; here, no entry logic even evaluates unless the trend gate is open.

2. Participation Gate second (Volume SMA × multiplier)

This gate filters thin liquidity moves around VWAP. Without it, the same visuals would produce materially more false triggers.

3. Branching entries with structure awareness

* Cross: Immediate VWAP cross in the trend direction.

* Cross-and-Retest: Requires a revisit to VWAP vicinity within a lookback window (recent low near VWAP for longs; recent high for shorts). This explicitly removes first-touch fakeouts that a plain cross takes.

* Momentum Exception (optional): A quantified body% + volume condition can bypass the retest when flow is impulsive—intentional risk-timing, not “just another indicator.”

4. Dual exits that reference both anchor and structure

* TrendBreak: Close only when price loses VWAP and EMA alignment flips.

* ATR stop: Placed at entry to cap tail risk.

These exits complement the entry structure rather than being generic stop/target add-ons.

What it does

* Trades the session’s fair value anchor (VWAP), but only with local-trend agreement (EMA fast vs. slow) and sufficient participation (volume filter).

* Lets you pick Cross or Cross-and-Retest entries; optionally allow a fast Momentum Exception when candles expand with volume.

* Manages positions with a structure exit (TrendBreak) and an emergency ATR stop from entry.

How it works (concepts & calculations)

* VWAP (session anchor):

Standard VWAP of the active session; entries reference the cross and the retest proximity to VWAP.

* Trend gate:

Long context only if `EMA(fast) > EMA(slow)`; short only if `EMA(fast) < EMA(slow)`.

A *gate*, not a trigger—entries aren’t considered unless this is true.

* Participation (volume) gate:

Require `volume > SMA(volume, volLen) × volMult`.

Screens out low-participation wiggles around VWAP.

Entries:

* Cross: Price crosses VWAP in the trend direction while volume gate is open.

* Cross-and-Retest: After crossing, price revisits VWAP vicinity within `lookback` (recent *low near VWAP* for longs; recent *high near VWAP* for shorts).

* Momentum Exception (optional): If body% (|close−open| / range) and volume exceed thresholds, enter without waiting for the retest.

Exits:

* TrendBreak (structure):

* Longs close when `price < VWAP` and `EMA(fast) < EMA(slow)` (mirror for shorts).

* ATR stop (risk):

* From entry: `stop = entry ± ATR(atrLen) × atrMult`.

How to use it ?

1. Select market & timeframe: Intraday on liquid symbols (equities, futures, crypto).

2. Pick entry mode:

* Start with Cross-and-Retest for fewer, more selective signals.

* Enable Momentum Exception if strong moves leave without retesting.

3. Tune guards:

* Raise `volMult` to ignore thin periods; lower it for more activity.

* Adjust `lookback` if retests come late/early on your symbol.

4. Risk:

* `atrLen` and `atrMult` set the emergency stop distance.

5. Read results per session: Optional panel (if enabled) summarizes Net-R, Win%, and PF for today’s session to evaluate

behavior regime by regime.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Monthly VWAPDescription

This indicator identifies potential mean reversion opportunities by tracking price deviations from monthly VWAP with dynamic volatility-adjusted thresholds.

Core Logic:

The indicator monitors when price moves significantly away from monthly VWAP and looks for potential reversal opportunities. It uses ATR-based dynamic thresholds that adapt to current market volatility, combined with volume confirmation to filter out weak signals.

Key Features:

Adaptive Thresholds: ATR-based bands that adjust to market volatility

Volume Confirmation: Requires average volume spike to validate signals

Monthly Reset: VWAP anchors reset each month for fresh reference levels

Visual Clarity: Color-coded deviation line with background highlights for active signals

Info Panel: Shows days from anchor and current price context vs fair value

Signal Generation:

Buy Signal: Price below monthly VWAP by threshold amount with elevated volume

Sell Signal: Price above monthly VWAP by threshold amount with elevated volume

Neutral: Price within threshold range or insufficient volume

Best Used For:

Mean reversion strategies in ranging markets

Identifying potential oversold/overbought conditions

Understanding price position relative to monthly fair value

DVWAP Spread -WinCAlgoDynamic VWAP Spread Oscillator

This indicator transforms the relationship between two adaptive VWAP curves into an oscillator format, making trend analysis more precise and intuitive.

What it shows:

Spread Value: The difference between Fast VWAP and Smoothed VWAP

Dynamic Coloring: Intensity increases as the spread moves away from zero

Zero Line: The neutral point where both VWAP curves converge

How to interpret:

Above Zero (Green): Fast VWAP > Smoothed VWAP → Bullish bias

Below Zero (Red): Fast VWAP < Smoothed VWAP → Bearish bias

Distance from Zero: Shows the strength of the current trend

Zero Crossovers: Potential trend change signals

📌 Usage Ideas:

Trend Filter: Take long trades only when oscillator is positive, shorts when negative

Momentum Gauge: Larger spread values indicate stronger trend momentum

Divergence Analysis: Look for divergences between price and oscillator for reversal signals

Overbought/Oversold: Extreme values may indicate potential mean reversion opportunities

Zero Line Bounces: Use zero line as dynamic support/resistance for entries

Parameters:

Period: Controls the lookback period for adaptive calculations

Adjustment Step: Fine-tunes the adaptive smoothing sensitivity

Fast Response: Adjusts how quickly the fast VWAP responds to price changes

Source: Price input for VWAP calculation (default: HLC3)

Dynamic VWAP -WinCAlgoDynamic VWAP Curve

This indicator applies an adaptive smoothing method to VWAP (Volume Weighted Average Price) to create two dynamic curves:

Fast VWAP (reacts quickly to price changes)

Smoothed VWAP (slower, adaptive baseline)

How to interpret:

When Fast VWAP > Smoothed VWAP, trend bias is bullish.

When Fast VWAP < Smoothed VWAP, trend bias is bearish.

The shaded area between the two lines works like a dynamic support/resistance zone.

📌 Usage ideas:

As a trend filter: take long trades only when Fast > Smoothed.

As a crossover signal: buy/sell when the two lines cross.

As support/resistance: price moving too far from the band can signal mean-reversion opportunities.

VWMA MACD Amanita Buy/Sell Signals VWMA MACD Amanita Buy/Sell Signals – Volume-Weighted Momentum Indicator

A twist on the classic MACD: this indicator uses Volume Weighted Moving Averages (VWMA) instead of EMAs, giving more weight to price moves backed by higher volume.

Features:

VWMA-based MACD line & signal line

Histogram highlights bullish/bearish momentum

Color-coded for easy visualization

Quick Guide:

MACD above Signal → bullish

MACD below Signal → bearish

Rising histogram → strengthening trend

Falling histogram → weakening trend

Perfect for traders who want momentum confirmed by volume.