The Abramelin Protocol [MPL]"Any sufficiently advanced technology is indistinguishable from magic." — Arthur C. Clarke

🌑 SYSTEM OVERVIEW

The Abramelin Protocol is not a standard technical indicator; it is a "Technomantic" trading algorithm engineered to bridge the gap between 15th-century esoteric mathematics and modern high-frequency markets.

This script is the flagship implementation of the MPL (Magic Programming Language) project—an open-source experimental framework designed to compile metaphysical intent into executable Python and Pine Script algorithms.

Unlike traditional indicators that rely on arbitrary constants (like the 14-period RSI or 200 SMA), this protocol calculates its parameters using "Dynamic Entity Gematria." We utilize a custom Python backend to analyze the ASCII vibrational frequencies of specific metaphysical archetypes, reducing them via Tesla's 3-6-9 harmonic principles to derive market-responsive periods.

🧬 WHAT IS ?

MPL (Magic Programming Language) is a domain-specific language and research initiative created to explore Technomancy—the art of treating code as a spellbook and the market as a chaotic entity to be tamed.

By integrating the logic of ancient Grimoires (such as The Book of Abramelin) with modern Data Science, MPL aims to discover hidden correlations in price action that standard tools overlook.

🔗 CONNECT WITH THE PROJECT:

If you are a developer, a trader, or a seeker of hidden knowledge, examine the source code and join the order:

• 📂 Official Project Site: hakanovski.github.io

• 🐍 MPL Source Code (GitHub): github.com

• 👨💻 Developer Profile (LinkedIn): www.linkedin.com

🔢 THE ALGORITHM: 452 - 204 - 50

The inputs for this script are mathematically derived signatures of the intelligence governing the system:

1. THE PAIMON TREND (Gravity)

• Origin: Derived from the ASCII summation of the archetype PAIMON (King of Secret Knowledge).

• Function: This 452-period Baseline acts as the market's "Event Horizon." It represents the deep, structural direction of the asset.

• Price > Line: Bullish Domain.

• Price < Line: Bearish Void.

2. THE ASTAROTH SIGNAL (Trigger)

• Origin: Derived from the ASCII summation of ASTAROTH (Knower of Past & Future), reduced by Tesla’s 3rd Harmonic.

• Function: This is the active trigger line. It replaces standard moving averages with a precise, gematria-aligned trajectory.

3. THE VOLATILITY MATRIX (Scalp)

• Origin: Based on the 9th Harmonic reduction.

• Function: Creates a "Cloud" around the signal line to visualize market noise.

🛡️ THE MILON GATE (Matrix Filter)

Unique to this script is the "MILON Gate" toggle found in the settings.

• ☑️ Active (Default): The algorithm applies the logic of the MILON Magic Square. Signals are ONLY generated if Volume and Volatility align with the geometric structure of the move. This filters out ~80% of false signals (noise).

• ⬜ Inactive: The algorithm operates in "Raw Mode," showing every mathematical crossover without the volume filter.

⚠️ OPERATIONAL USAGE

• Timeframe: Optimized for 4H (The Builder) and Daily (The Architect) charts.

• Strategy: Use the Black/Grey Line (452) as your directional bias. Take entries only when the "EXECUTE" (Long) or "PURGE" (Short) sigils appear.

Use this tool wisely. Risk responsibly. Let the harmonics guide your entries.

— Hakan Yorganci

Technomancer & Full Stack Developer

Volatilityindex

IV vs Realised Volatility (VIX/HV Comparator)VIX / HV Comparator – Implied vs Realised Volatility

This indicator compares Implied Volatility (IV) from a volatility index (VIX, India VIX, etc.) with the Realised / Historical Volatility (HV) of the current chart symbol.

It helps you see whether options are pricing volatility as rich or cheap relative to what the underlying is actually doing.

What it does

Pulls IV from any user-selected vol index symbol (e.g. CBOE:VIX for SPX, NSEINDIA:INDIAVIX for Nifty).

Calculates realised volatility from the chart’s price data using returns over a user-defined lookback.

Annualises HV so IV and HV are displayed on the same percentage scale, on any timeframe (intraday or higher).

Optionally shows an IV/HV ratio in a separate pane to highlight when options are rich or cheap relative to realised volatility.

How to read it

Main panel:

Orange line – Implied Volatility (IV) from your chosen vol index.

Aqua line – Realised / Historical Volatility (HV) of the current chart symbol.

Fill between lines:

Green shading -> IV > HV -> options are priced richer than what the underlying is currently realising.

Red shading -> HV > IV -> realised vol is higher than the options market is implying.

Sub-panel (optional):

IV / HV ratio

- Above 1 -> IV > HV (vol rich).

- Below 1 -> IV < HV (vol cheap).

- Horizontal guides (for example 1.2 / 0.8) help frame “significantly rich/cheap” zones.

A small label on the latest bar displays the current IV, HV and their difference in vol points.

Inputs (key ones)

IV Index Symbol – choose the volatility index that corresponds to your underlying (VIX, India VIX, etc.).

Realised Vol Lookback – number of bars used to compute HV (for example 20).

Trading Days per Year and Active Hours per Day – used for annualising HV so it stays consistent across timeframes.

IV Scale Factor – adjust if your IV index is quoted in decimals (0.15) instead of points (15).

Practical uses

Context for options trades – Quickly see if current IV is high or low relative to realised volatility when deciding on strategies (premium selling vs buying, spreads, hedges).

Vol regime analysis – Track shifts where HV starts to rise above IV (real stress building) or IV spikes far above HV (fear premium / insurance bid).

Cross-timeframe checks – Use on intraday charts for short-term trading context, or on daily/weekly charts for bigger picture vol regimes.

This tool is not a stand-alone signal generator. It is meant to be a volatility dashboard you combine with your usual price action, trend, and options strategy rules to understand how the options market is pricing risk vs what the underlying is actually delivering.

Phenom(指標版:EMA 交叉訊號 v8.8 + 結構與風險)標題 (Title): Phenom Intelligence: Trend & Risk Structure System (v8.8)

內文 (Description):

Introduction Phenom Intelligence v8.8 is a comprehensive trading system designed to capture trends while strictly managing risk. It integrates Dynamic EMA Structures, Momentum Filters, and Risk Boundaries (ATR & Pivots) into one chart, providing a complete decision-making framework.

Key Features

Dynamic EMA Ribbon: Automatically adjusts EMA lengths based on the selected mode (Swing, Scalping, Trend-Following, or Long-Term Investment).

ATR Risk Channel: Visualizes volatility risk. A close below the lower ATR band signals a potential structure break and suggests defensive measures.

Pivot Points (Auto-Structure): Automatically plots Pivot (P), Resistance (R1), and Support (S1) levels to identify optimal take-profit and stop-loss zones.

Golden Confluence Signals: High-quality buy/sell signals are triggered only when Trend, Momentum (MACD), RSI, and Multi-Timeframe (MTF) conditions align.

Disclaimer This script is "Invite-Only" and intended for educational purposes. It does not constitute financial advice.

系統簡介 Phenom Intelligence v8.8 是一套專為捕捉波段趨勢與風險控管而設計的綜合交易系統。整合了「趨勢結構」、「動能濾網」與「風險邊界」,協助交易者在進場前具備完整的決策依據。

核心功能

智能趨勢均線 (Dynamic EMA): 內建四種戰略模式,系統會根據選定的模式自動調整均線週期。

ATR 動態風險通道: 以均線為軸心繪製波動率通道。當價格跌破下通道時,視為結構破壞警訊,提供客觀的離場參考。

結構支撐壓力 (Pivots): 自動計算關鍵結構點位。R1 (阻力) 可作為獲利調節目標,S1 (支撐) 作為防守區。

黃金共振訊號: 當 EMA 趨勢、MACD 動能、RSI 強度與多週期狀態完全共振時,才會觸發特定訊號,過濾雜訊。

免責聲明 本指標僅供技術分析參考與教育用途,不代表任何形式的投資建議。

FX OSINT - Institutional Midnight Intelligence For ForexFX OSINT — Institutional Midnight Intelligence For Forex

See Your FX Charts Like an Intelligence Briefing, Not a Guess

If you’ve ever stared at EURUSD or GBPJPY and thought:

Where is the real liquidity?

Is this move sponsored by smart money or just noise?

Am I buying into premium or discount?

…then FX OSINT is designed for you.

FX OSINT (Forex Open Source Intelligence) treats the FX market the way an analyst treats an investigation:

Collect open‑source signals from price, time, and volatility.

Map out liquidity, structure, and sessions in a repeatable way.

Present them in a clean, non‑cluttered dashboard so you can read context quickly.

No rainbow spaghetti. No 12 indicators stacked on top of each other. Just structured information, midnight visuals, and a clear read on what the market is doing right now.

Why FX OSINT Exists

Many FX traders run into the same problems:

Overloaded charts – multiple indicators fighting for space, none talking to each other.

Signals with no context – arrows that ignore structure, sessions, and liquidity.

Tools not tuned for FX – generic indicators that don’t care what pair you are on.

FX OSINT brings this together into one FX‑focused framework that:

Understands structure : BOS/CHOCH, swings, and trend across multiple timeframes.

Respects liquidity : sweeps, order blocks, and FVGs with controlled visibility.

Reads volatility & ADR : how far today’s range has developed.

Knows the clock : London, New York, and key killzones.

Scores confluence : a 0–100 engine that summarizes how much is lining up.

FX OSINT is built for traders who want structured, institutional‑style logic with a disciplined, midnight‑themed UI —not flashing buy/sell buttons.

1. Midnight Dashboard — Top‑Right Intelligence Panel

This panel acts as your compact “situation room”:

CONFLUENCE — 0–100 score blending trend alignment, volatility regime, sessions, liquidity events, order blocks, FVGs, and ADR context.

REGIME — Low / Building / Normal / Expansion / Extreme, driven by ATR relationships, so you know if you’re in chop, trend, or expansion.

HTF / MTF / LTF TREND — Higher‑, medium‑, and current‑timeframe bias in one place, so you see if you are trading with or against the larger flow.

ADR USED — How much of today’s typical range has already been consumed in percentage terms.

PIP VALUE — Approximate pip size per pair, including JPY‑style pairs.

Everything is bold, legible, and color‑coded, but the layout stays minimal so you can:

Look once → understand the context.

2. Structure, BOS, CHOCH — Smart‑Money‑Style Skeleton

FX OSINT tracks swing highs and lows, then shows how structure evolves:

Trend logic based on evolving swings, not just a moving average cross.

BOS (Break of Structure) when price expands in the direction of trend.

CHOCH (Change of Character) when behavior flips and the market structure changes.

Labels are selective, not spammy . You don’t get a tag on every minor wiggle—only when structure meaningfully shifts, so it’s easier to answer:

"Are we continuing the current leg, or did something actually change here?"

3. Liquidity Sweeps, Order Blocks & FVGs — The OSINT Layer

FX OSINT treats liquidity as a key information layer:

Liquidity sweeps — Detects when price spikes through recent highs/lows and then snaps back, flagging potential stop runs.

Order blocks — The last opposite candle before a displacement move, drawn as controlled boxes with limited lifespan to avoid clutter.

Fair Value Gaps (FVGs) — Three‑candle imbalances rendered as precise zones with a cap on how many can exist at once.

Under the hood, boxes are managed so your chart does not become a wall of old zones:

// Draw Order Blocks with overlap prevention

if isBullishOB and showOrderBlocks

if array.size(obBoxes) >= maxBoxes

oldBox = array.shift(obBoxes)

box.delete(oldBox)

newBox = box.new(bar_index , low , bar_index + obvLength, high ,

border_color = bullColor, bgcolor = bullColorTransp,

border_width = 2, extend = extend.none)

array.push(obBoxes, newBox)

Box limits keep the number of zones under control.

Borders and transparency are tuned so you still see price clearly.

You end up with a curated liquidity map , rather than a chart buried under every level price has ever touched.

4. Volatility, ADR & Sessions — Time and Range Intelligence

FX OSINT runs a Volatility Regime Analyzer and an ADR engine in the background:

Volatility regime — Five states (Low → Extreme) derived from fast vs. slow ATR.

ADR bands — Daily high/mid/low projected from the current daily open.

ADR used % — How far today’s move has traveled relative to its typical range.

On the time side:

Asia, London, New York sessions are softly highlighted with a single active background to avoid overlapping colors.

Killzones (e.g., London and New York opens) can be emphasized when you want to focus on where significant moves often begin.

Together, this helps you answer:

"What time is it in the trading day?"

"How stretched are we?"

"Is expansion just starting, or are we late to the move?"

5. ICT‑Style Add‑Ons — BOS/CHOCH, Premium/Discount, and Confluence

For modern FX / ICT‑inspired workflows, FX OSINT includes:

BOS / CHOCH labels — Clear structural shifts based on swings.

Premium / Discount zones — 25%, 50%, 75% levels of the daily range, so you know if you are buying discount in an uptrend or selling premium in a downtrend.

Confluence score — A single number summarizing how many conditions line up in the current context.

Instead of replacing your plan, FX OSINT compresses your checklist into the chart:

Structure

Liquidity

Session / Time

Volatility / ADR

Higher‑timeframe alignment

When these agree, the dashboard reflects it. When they don’t, it stays neutral and lets you see the conflict.

How To Use FX OSINT

FX OSINT is not a signal bot. It is an information engine that organizes context so you can apply your own plan.

A typical workflow might look like:

Start on higher timeframes (e.g., H4/D1) to form directional bias from structure, volatility regime, and ADR context.

Move to intraday timeframes (e.g., M15/H1) around your chosen sessions (London and/or New York).

Look for confluence :

HTF / MTF / LTF trends aligned.

Price in discount for longs or premium for shorts.

Recent liquidity sweep into a meaningful OB or FVG.

Confluence score at or above a level you consider significant.

Then refine entries using BOS/CHOCH on lower timeframes according to your own risk and execution rules.

FX OSINT aims to make sure you do not enter a trade without seeing:

Where you are in the day (ADR and sessions).

Where you are in the volatility cycle (regime).

Who currently appears in control (structure and trend).

Which liquidity was just targeted (sweeps and zones).

Design Choices and Scope

FX OSINT was designed around a few clear constraints:

FX‑focused — Logic and filters tuned for FX majors, minors, exotics, and metals. It is intended for FX markets, not for every possible asset class.

Open‑source — The full Pine Script code is available so you can read it, learn from it, and adapt it to your own workflow if needed.

Clear themes — Two main visual styles (e.g., dark institutional “midnight” and a lighter accent variant) with a focus on readability, not visual noise.

Chart‑friendly — Panels use fixed areas, session highlights avoid overlapping, and boxes are capped/pruned so the chart remains usable.

FX OSINT is for only Forex pairs, not anything else!

Hope you enjoyed and remember your Open Source Intelligence Matters 😉!

-officialjackofalltrades

ARCH ProxyARCH Proxy (ARCH) - Volatility Assessment Indicator

The ARCH Proxy indicator (short title: ARCH) is a dynamic, multi-factor volatility assessment tool designed to help traders quickly gauge the current energy and risk level of the market. It plots a real-time measure of price fluctuation against its long-term historical average and adaptive High/Low Volatility thresholds. This provides a clear, objective framework for distinguishing between periods of market compression (low-energy consolidation) and expansion (high-risk volatility), optimizing strategy selection and risk management.

Simplified Trading Guide

The ARCH indicator offers a clear, objective signal framework to guide your trading decisions based on market energy :

Spotting High-Risk Expansion (Climax):

Signal: The main ARCH Proxy line moves sharply above the High Volatility Threshold (typically a red line).

Action: This signals the market is in a period of intense, climactic price action. This is often a time to avoid new entries, reduce exposure, or look for potential trend exhaustion and reversals due to the high risk of a sudden correction.

Identifying Low-Energy Compression (Setup):

Signal: The main ARCH Proxy line trends consistently below the Low Volatility Threshold (typically a green line).

Action: This indicates a market consolidation phase. This "low-energy" compression frequently precedes a strong breakout (expansion). Traders should prepare for an entry in the direction of the dominant trend, anticipating a coming surge in momentum.

Normal Trading Conditions:

Signal: The ARCH Proxy line is fluctuating between the High and Low Volatility thresholds.

Action: The market is in a normal state. Use this time to follow the dominant trend with standard risk parameters.

Strategy: HMA 50 + Supertrend SniperHMA 50 + Supertrend Confluence Strategy (Trend Following with Noise Filtering)

Description:

Introduction and Concept This strategy is designed to solve a common problem in trend-following trading: Lag vs. False Signals. Standard Moving Averages often lag too much, while price action indicators can generate false signals during choppy markets. This script combines the speed of the Hull Moving Average (HMA) with the volatility-based filtering of the Supertrend indicator to create a robust "Confluence System."

The primary goal of this script is not just to overlay two indicators, but to enforce a strict rule where a trade is only taken when Momentum (HMA) and Volatility Direction (Supertrend) are in perfect agreement.

Why this combination? (The Logic Behind the Mashup)

Hull Moving Average (HMA 50): We use the HMA because it significantly reduces lag compared to SMA or EMA by using weighted calculations. It acts as our primary Trend Direction detector. However, HMA can be too sensitive and "whipsaw" during sideways markets.

Supertrend (ATR-based): We use the Supertrend (Factor 3.0, Period 10) as our Volatility Filter. It uses Average True Range (ATR) to determine the significant trend boundary.

How it Works (Methodology) The strategy uses a boolean logic system to filter out low-quality trades:

Bullish Confluence: The HMA must be rising (Slope > 0) AND the Close Price must be above the Supertrend line (Uptrend).

Bearish Confluence: The HMA must be falling (Slope < 0) AND the Close Price must be below the Supertrend line (Downtrend).

The "Choppy Zone" (Noise Filter): This is a unique feature of this script. If the HMA indicates one direction (e.g., Rising) but the Supertrend indicates the opposite (e.g., Downtrend), the market is considered "Choppy" or indecisive. In this state, the script paints the candles or HMA line Gray and exits all positions (optional setting) to preserve capital.

Visual Guide & Signals To make the script easy to interpret for traders who do not read Pine Script, I have implemented specific visual cues:

Green Cross (+): Indicates a LONG entry signal. Both HMA and Supertrend align bullishly.

Red Cross (X): Indicates a SHORT entry signal. Both HMA and Supertrend align bearishly.

Thick Line (HMA): The main line changes color based on the trend.

Green: Bullish Confluence.

Red: Bearish Confluence.

Gray: Divergence/Choppy (No Trade Zone).

Thin Step Line: This is the Supertrend line, serving as your dynamic Trailing Stop Loss.

Strategy Settings

HMA Length: Default is 50 (Mid-term trend).

ATR Factor/Period: Default is 3.0/10 (Standard for trend catching).

Exit on Choppy: A toggle switch allowing users to decide whether to hold through noise or exit immediately when indicators disagree.

Risk Warning This strategy performs best in trending markets (Forex, Crypto, Indices). Like all trend-following systems, it may experience drawdown during prolonged accumulation/distribution phases. Please backtest with your specific asset before using it with real capital.

Market Echo Screener [BigBeluga]

The Market Echo Screener is a structured multi-asset dashboard capable of tracking up to 15 symbols simultaneously .

Designed to condense complex market data into an actionable format. Each column represents a specialized calculation, giving traders insight into signals, phases, retests, and volatility — all updated in real time.

For each symbol, it displays a full set of analytics: trend signals, take profit progression, wave structure, equilibrium pulls, volatility-adjusted flows, smart band retests, volatility regimes, and live price context — all condensed into one unified table.

Instead of flipping through multiple charts, traders get an instant overview of market dynamics across an entire watchlist, making it easier to spot alignment and high-probability opportunities.

⬤ Trend Signals

This column is powered by a low-pass digital trend filter that smooths short-term fluctuations and isolates directional momentum.

It produces Buy and Sell signals when price crosses adaptive thresholds relative to the smoothed baseline. Stronger “+” signals appear when slope acceleration or momentum divergence confirms additional conviction.

• Uses recursive filtering to eliminate noise.

• Signal strength is determined by the magnitude of deviation from the baseline.

• Tracks how many bars back the signal occurred, using a bar-counting algorithm.

• Combines both normal and power signals to reflect phases of market conviction.

⬤ TPs (Take Profits)

The take profit ladder is generated through an adaptive volatility-projection model .

When a signal fires, projected levels are based on volatility-weighted extensions. Each level (TP1–TP6) represents an incrementally wider confidence band, dynamically recalculated with every new bar.

• Uses volatility-normalized ranges for TP distances.

• Level activation is sequential, progressing as price reaches thresholds.

• Reset occurs when opposite signals are detected.

• Higher TPs imply extended momentum runs, while early TP triggers highlight conservative exits.

⬤ ActionWave

The ActionWave column applies a dual-smoothing algorithm combining custom MA stacks and polynomial regression to capture the underlying wave structure.

It identifies macro phases (Bullish ∆ / Bearish ∇) and flags retests when price folds back into the average after expansion.

• Wave slope is calculated using gradient differentials.

• Retests are confirmed within a bar-window threshold (e.g., 20–25 bars).

• Distinguishes continuation from exhaustion by analyzing whether slope remains positive/negative.

• Provides a clean map of trend rhythm without intrabar noise.

⬤ Magnet

The Magnet measure calculates a dynamic equilibrium band around price.

By averaging the midpoints of recent high–low ranges and weighting them by volatility, it defines a “fair zone” where price tends to trend and mean-revert.

• Bullish/Bearish status is derived from price position relative to the equilibrium mean.

• Retests occur when price leaves the zone and then re-enters within a tolerance band.

• Incorporates a mean-reversion index to highlight strength of pull.

• Acts as a gravitational anchor, showing when price is likely to snap back.

⬤ FlowTrend

FlowTrend is calculated using volatility and noise adjusted envelope bands .

It determines the active market flow by testing whether price consistently holds above or below the smoothed envelope. Retests are logged when price touches the envelope and respects trend direction.

• Bands expand/contract based on ATR and rolling variance.

• Flow state = Bullish if closing above upper envelope, Bearish if below.

• Retests validated only if trend slope and band alignment remain intact.

• Helps identify continuation setups by filtering false flips.

⬤ Smart Bands

Smart Bands employ an adaptive trailing stop framework that shifts with volatility and momentum.

Price interaction with these bands is tracked for bullish (∆) or bearish (∇) retests, highlighting whether the current move has revalidated at its volatility boundary.

• Bands derived from trailing volatility-adjusted stops.

• Upward retest fires when price tests support bands during uptrend.

• Downward retest occurs when resistance bands are tapped in downtrend.

• Provides structured “confirmation points” that validate signals.

⬤ Volatility

Volatility is measured via a hybrid standard deviation logic .

First, the standard deviation of closing prices over 10 bars is scaled by a factor, then normalized against its own 20-bar rolling standard deviation. The result is converted into a 0–100 index, producing three regimes:

❄️ Calm (<50): low dispersion, mean-reversion conditions dominate.

⚠️ Elevated (50–70): directional expansion likely, watch for breakout tension.

💥 Explosive (>70): strong dispersion, trend-following setups favored.

• Uses layered smoothing to dampen noise.

• Normalization ensures comparability across different assets.

• Acts as a meta-filter for selecting strategy type (range vs. momentum).

⬤ Price

The price column displays the latest close rounded to the nearest tick size.

It is color-coded by candle bias: green for bullish closes, red for bearish closes.

• Tick normalization ensures clean display across assets with different decimal precision.

• Color-coding gives instant sentiment context.

• Serves as the anchor reference for all other metrics in the row.

The Market Echo Screener is not a simple signal table — it’s a layered analytics framework.

Each column is driven by technical calculations: smoothing filters, volatility projections, equilibrium models, and adaptive band logic. Together, they create a unified lens on multiple assets, allowing traders to rapidly identify alignment, filter out noise, and focus on the clearest opportunities.

Contango/Backwardation Monitor

This is an indicator to display the spread difference between two products. I designed it around VX1! and VX2! but any other two products can be chosen. It is a simple subtraction of VX2-VX1. I will go through the options first and what they do followed by what contango/backwardation is in my own words. You will need the data package for VX futures for the default version to work.

INPUTS

-Apply Smoothing: choose to apply smoothing or not.

-Smoothing Method: choose between SMA,EMA,WMA, etc.

-Line Width: Width of line if line is chosen style(can be changed in style section)

-Threshold 1-5: This is the level at which the line will change colors(defaults are for VX)

-Color 1-5: The color the line will change to when crossing threshold.

Towards Backwardation: Background color change when line is slanted down

Towards Contango: Background color change when line is slanted up

Bars to Confirm Trend: This is my method to cut down on background color changes. It is how many bars consecutive going back needed to change color.

STYLE

-All colors and whatnot can be changed here(threshold colors can be changed here or on the input page).

T1 Line-T5 line: These are simple horizontal lines that can be used to denote threshold areas or whatever you want.

Contango/Backwardation-These terms are used mostly with futures to define the calendar spread between two contracts. Contango is when that spread is is getting longer and backwardation is when that spread is closing. In terms of VIX futures, Contango would imply that volatility is stabilizing and the S and P will likely gain. Backwardation, woudl eb the opposite.

The most simple way to read this indicator with default settings- If the line is up, red, and the background is red, then you can assume S and P prices are going down. And if the opposite is true, then prices are likely going up.

Please feel free to ask any questions and I will do my best to answer them.

RSI(Min-Max)RSI (Min-Max) is an enhanced version of Welles Wilder's Relative Strength Index, designed to offer greater analytical precision and dynamic insight into the behavior of the RSI within each candlestick.In addition to displaying the traditional RSI value, this script calculates the possible extreme values — the minimum and maximum RSI — based on the low and high prices of the current candle. This allows you to estimate how the RSI would react if the price moved to the extremes of the bar, providing a predictive and refined reading of momentum.

Volatility Cone Forecaster Lite [PhenLabs]📊 Volatility Cone Forecaster

Version: PineScript™v6

📌Description

The Volatility Cone Forecaster (VCF) is an advanced indicator designed to provide traders with a forward-looking perspective on market volatility. Instead of merely measuring past price fluctuations, the VCF analyzes historical volatility data to project a statistical “cone” that outlines a probable range for future price movements. Its core purpose is to contextualize the current market environment, helping traders to anticipate potential shifts from low to high volatility periods (and vice versa). By identifying whether volatility is expanding or contracting relative to historical norms, it solves the critical problem of preparing for significant market moves before they happen, offering a clear statistical edge in strategy development.

This indicator moves beyond lagging measures by employing percentile analysis to rank the current volatility state. This allows traders to understand not just what volatility is, but how significant it is compared to the recent past. The VCF is built for discretionary traders, system developers, and options strategists who need a sophisticated understanding of market dynamics to manage risk and identify high-probability opportunities.

🚀Points of Innovation

Forward-Looking Volatility Projection: Unlike standard indicators that only show historical data, the VCF projects a statistical cone of future volatility.

Percentile-Based Regime Analysis: Ranks current volatility against historical data (e.g., 90th, 75th percentiles) to provide objective context.

Automated Regime Detection: Automatically identifies and labels the market as being in a ‘High’, ‘Low’, or ‘Normal’ volatility regime.

Expansion & Contraction Signals: Clearly indicates whether volatility is currently increasing or decreasing, signaling shifts in market energy.

Integrated ATR Comparison: Plots an ATR-equivalent volatility measure to offer a familiar point of reference against the statistical model.

Dynamic Visual Modeling: The cone visualization directly on the price chart provides an intuitive guide for future expected price ranges.

🔧Core Components

Realized Volatility Engine: Calculates historical volatility using log returns over multiple user-defined lookback periods (short, medium, long) for a comprehensive view.

Percentile Analysis Module: A custom function calculates the 10th, 25th, 50th, 75th, and 90th percentiles of volatility over a long-term lookback (e.g., 252 days).

Forward Projection Calculator: Uses the calculated volatility percentiles to mathematically derive and draw the upper and lower bounds of the future volatility cone.

Volatility Regime Classifier: A logic-based system that compares current volatility to the historical percentile bands to classify the market state.

🔥Key Features

Customizable Lookback Periods: Adjust short, medium, and long-term lookbacks to fine-tune the indicator’s sensitivity to different market cycles.

Configurable Forward Projection: Set the number of days for the forward cone projection to align with your specific trading horizon.

Interactive Display Options: Toggle visibility for percentile labels, ATR levels, and regime coloring to customize the chart display.

Data-Rich Information Table: A clean, on-screen table displays all key metrics, including current volatility, percentile rank, regime, and trend.

Built-in Alert Conditions: Set alerts for critical events like volatility crossing the 90th percentile, dropping below the 10th, or switching between expansion and contraction.

🎨Visualization

Volatility Cone: Shaded bands projected onto the future price axis, representing the probable price range at different statistical confidence levels (e.g., 75th-90th percentile).

Color-Coded Volatility Line: The primary volatility plot dynamically changes color (e.g., red for high, green for low) to reflect the current volatility regime, providing instant context.

Historical Percentile Bands: Horizontal lines plotted across the indicator pane mark the key percentile levels, showing how current volatility compares to the past.

On-Chart Labels: Clear labels automatically display the current volatility reading, its percentile rank, the detected regime, and trend (Expanding/Contracting).

📖Usage Guidelines

Setting Categories

Short-term Lookback: Default: 10, Range: 5-50. Controls the most sensitive volatility calculation.

Medium-term Lookback: Default: 21, Range: 10-100. The primary input for the current volatility reading.

Long-term Lookback: Default: 63, Range: 30-252. Provides a baseline for long-term market character.

Percentile Lookback Period: Default: 252, Range: 100-1000. Defines the period for historical ranking; 252 represents one trading year.

Forward Projection Days: Default: 21, Range: 5-63. Determines how many bars into the future the cone is projected.

✅Best Use Cases

Breakout Trading: Identify periods of deep consolidation when volatility falls to low percentile ranks (e.g., below 25th) and begins to expand, signaling a potential breakout.

Mean Reversion Strategies: Target trades when volatility reaches extreme high percentile ranks (e.g., above 90th), as these periods are often unsustainable and lead to contraction.

Options Strategy: Use the cone’s projected upper and lower bounds to help select strike prices for strategies like iron condors or straddles.

Risk Management: Widen stop-losses and reduce position sizes when the indicator signals a transition into a ‘High’ volatility regime.

⚠️Limitations

Probabilistic, Not Predictive: The cone represents a statistical probability, not a guarantee of future price action. Extreme, unpredictable news events can drive prices outside the cone.

Lagging by Nature: All calculations are based on historical price data, meaning the indicator will always react to, not pre-empt, market changes.

Non-Directional: The indicator forecasts the *magnitude* of future moves, not the *direction*. It should be paired with a directional analysis tool.

💡What Makes This Unique

Forward Projection: Its primary distinction is projecting a data-driven, statistical forecast of future volatility, which standard oscillators do not do.

Contextual Analysis: It doesn’t just provide a number; it tells you what that number means through percentile ranking and automated regime classification.

🔬How It Works

1. Data Calculation:

The indicator first calculates the logarithmic returns of the asset’s price. It then computes the annualized standard deviation of these returns over short, medium, and long-term lookback periods to generate realized volatility readings.

2. Percentile Ranking:

Using a 252-day lookback, it analyzes the history of the medium-term volatility and determines the values that correspond to the 10th, 25th, 50th, 75th, and 90th percentiles. This builds a statistical map of the asset’s volatility behavior.

3. Cone Projection:

Finally, it takes these historical percentile values and projects them forward in time, calculating the potential upper and lower price bounds based on what would happen if volatility were to run at those levels over the next 21 days.

💡Note:

The Volatility Cone Forecaster is most effective on daily and weekly charts where statistical volatility models are more reliable. For lower timeframes, consider shortening the lookback periods. Always use this indicator as part of a comprehensive trading plan that includes other forms of analysis.

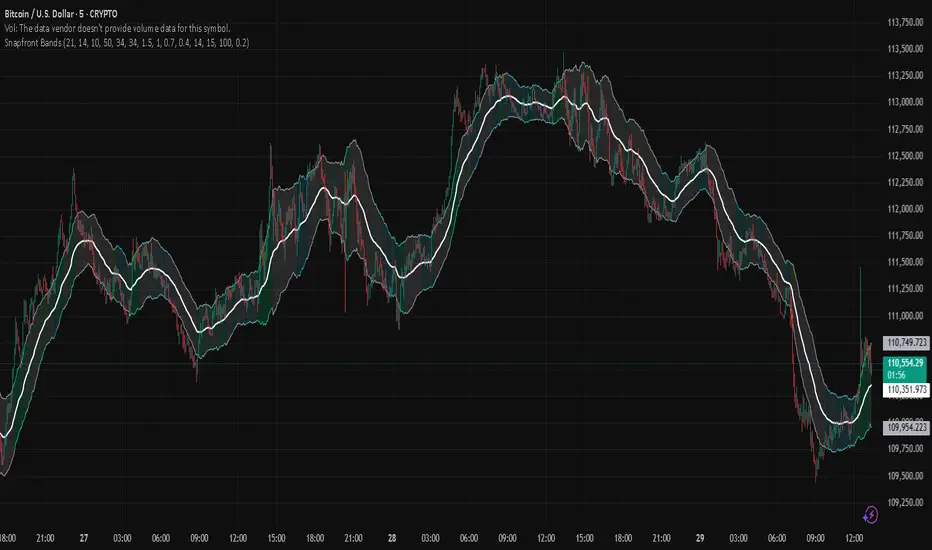

Snapfront WCTφ Coherence BandsSnapfront Coherence Bands — WCTφ (v6)

The Snapfront Coherence Bands (SCB) extend classic ATR-style bands with a coherence-driven engine. Instead of simple volatility envelopes, SCB adapt dynamically to market entropy, trend stability, and regime detection.

Core Features:

📊 WCTφ (Weighted Coherence Tracking) to measure entropy & disorder

🔍 Adaptive band width scaling with chaos factor (ATR × coherence)

🎯 Regime coloring:

Trend (lime)

Breakout (aqua)

Mean reversion (yellow)

Exhaustion (orange)

⚡ Squeeze detector with percentile-based compression zones

🟢/🔴 Entry/exit arrows on crossovers (optional)

Use Cases:

Spot high-clarity trend moves vs. noisy ranges

Anticipate volatility squeezes & breakout setups

Filter trades by regime classification

Visualize price stability with adaptive banding

⚠️ Invite-Only Access:

Available exclusively via SnapfrontTech. Subscription required.

Relative Volatility Mass [SciQua]The ⚖️ Relative Volatility Mass (RVM) is a volatility-based tool inspired by the Relative Volatility Index (RVI) .

While the RVI measures the ratio of upward to downward volatility over a period, RVM takes a different approach:

It sums the standard deviation of price changes over a rolling window, separating upward volatility from downward volatility .

The result is a measure of the total “volatility mass” over a user-defined period, rather than an average or normalized ratio.

This makes RVM particularly useful for identifying sustained high-volatility conditions without being diluted by averaging.

────────────────────────────────────────────────────────────

╭────────────╮

How It Works

╰────────────╯

1. Standard Deviation Calculation

• Computes the standard deviation of the chosen `Source` over a `Standard Deviation Length` (`stdDevLen`).

2. Directional Separation

• Volatility on up bars (`chg > 0`) is treated as upward volatility .

• Volatility on down bars (`chg < 0`) is treated as downward volatility .

3. Rolling Sum

• Over a `Sum Length` (`sumLen`), the upward and downward volatilities are summed separately using `math.sum()`.

4. Relative Volatility Mass

• The two sums are added together to get the total volatility mass for the rolling window.

Formula:

RVM = Σ(σ up) + Σ(σ down)

where σ is the standard deviation over `stdDevLen`.

╭────────────╮

Key Features

╰────────────╯

Directional Volatility Tracking – Differentiates between volatility during price advances vs. declines.

Rolling Volatility Mass – Shows the total standard deviation accumulation over a given period.

Optional Smoothing – Multiple MA types, including SMA, EMA, SMMA (RMA), WMA, VWMA.

Bollinger Band Overlay – Available when SMA is selected, with adjustable standard deviation multiplier.

Configurable Source – Apply RVM to `close`, `open`, `hl2`, or any custom source.

╭─────╮

Usage

╰─────╯

Trend Confirmation: High RVM values can confirm strong trending conditions.

Breakout Detection: Spikes in RVM often precede or accompany price breakouts.

Volatility Cycle Analysis: Compare periods of contraction and expansion.

RVM is not bounded like the RVI, so absolute values depend on market volatility and chosen parameters.

Consider normalizing or using smoothing for easier visual comparison.

╭────────────────╮

Example Settings

╰────────────────╯

Short-term volatility detection: `stdDevLen = 5`, `sumLen = 10`

Medium-term trend volatility: `stdDevLen = 14`, `sumLen = 20`

Enable `SMA + Bollinger Bands` to visualize when volatility is unusually high or low relative to recent history.

╭───────────────────╮

Notes & Limitations

╰───────────────────╯

Not a directional signal by itself — use alongside price structure, volume, or other indicators.

Higher `sumLen` will smooth short-term fluctuations but reduce responsiveness.

Because it sums, not averages, values will scale with both volatility and chosen window size.

╭───────╮

Credits

╰───────╯

Based on the Relative Volatility Index concept by Donald Dorsey (1993).

TradingView

SciQua - Joshua Danford

Fear Volatility Gate [by Oberlunar]The Fear Volatility Gate by Oberlunar is a filter designed to enhance operational prudence by leveraging volatility-based risk indices. Its architecture is grounded in the empirical observation that sudden shifts in implied volatility often precede instability across financial markets. By dynamically interpreting signals from globally recognized "fear indices", such as the VIX, the indicator aims to identify periods of elevated systemic uncertainty and, accordingly, restrict or flag potential trade entries.

The rationale behind the Fear Volatility Gate is rooted in the understanding that implied volatility represents a forward-looking estimate of market risk. When volatility indices rise sharply, it reflects increased demand for options and a broader perception of uncertainty. In such contexts, price movements can become less predictable, more erratic, and often decoupled from technical structures. Rather than relying on price alone, this filter provides an external perspective—derived from derivative markets—on whether current conditions justify caution.

The indicator operates in two primary modes: single-source and composite . In the single-source configuration, a user-defined volatility index is monitored individually. In composite mode, the filter can synthesize input from multiple indices simultaneously, offering a more comprehensive macro-risk assessment. The filtering logic is adaptable, allowing signals to be combined using inclusive (ANY), strict (ALL), or majority consensus logic. This allows the trader to tailor sensitivity based on the operational context or asset class.

The indices available for selection cover a broad spectrum of market sectors. In the equity domain, the filter supports the CBOE Volatility Index ( CBOE:VIX VIX) for the S&P 500, the Nasdaq-100 Volatility Index ( CBOE:VXN VXN), the Russell 2000 Volatility Index ( CBOEFTSE:RVX RVX), and the Dow Jones Volatility Index ( CBOE:VXD VXD). For commodities, it integrates the Crude Oil Volatility Index ( CBOE:OVX ), the Gold Volatility Index ( CBOE:GVZ ), and the Silver Volatility Index ( CBOE:VXSLV ). From the fixed income perspective, it includes the ICE Bank of America MOVE Index ( OKX:MOVEUSD ), the Volatility Index for the TLT ETF ( CBOE:VXTLT VXTLT), and the 5-Year Treasury Yield Index ( CBOE:FVX.P FVX). Within the cryptocurrency space, it incorporates the Bitcoin Volmex Implied Volatility Index ( VOLMEX:BVIV BVIV), the Ethereum Volmex Implied Volatility Index ( VOLMEX:EVIV EVIV), the Deribit Bitcoin Volatility Index ( DERIBIT:DVOL DVOL), and the Deribit Ethereum Volatility Index ( DERIBIT:ETHDVOL ETHDVOL). Additionally, the user may define a custom instrument for specialized tracking.

To determine whether market conditions are considered high-risk, the indicator supports three modes of evaluation.

The moving average cross mode compares a fast Hull Moving Average to a slower one, triggering a signal when short-term volatility exceeds long-term expectations.

The Z-score mode standardizes current volatility relative to historical mean and standard deviation, identifying significant deviations that may indicate abnormal market stress.

The percentile mode ranks the current value against a historical distribution, providing a relative perspective particularly useful when dealing with non-normal or skewed distributions.

When at least one selected index meets the condition defined by the chosen mode, and if the filtering logic confirms it, the indicator can mark the trading environment as “blocked”. This status is visually highlighted through background color changes and symbolic markers on the chart. An optional tabular interface provides detailed diagnostics, including raw values, fast-slow MA comparison, Z-scores, percentile levels, and binary risk status for each active index.

The Fear Volatility Gate is not a predictive tool in itself but rather a dynamic constraint layer that reinforces discipline under conditions of macro instability. It is particularly valuable when trading systems are exposed to highly leveraged or short-duration strategies, where market noise and sentiment can temporarily override structural price behavior. By synchronizing trading signals with volatility regimes, the filter promotes a more cautious, informed approach to decision-making.

This approach does not assume that all volatility spikes are harmful or that market corrections are imminent. Rather, it acknowledges that periods of elevated implied volatility statistically coincide with increased execution risk, slippage, and spread widening, all of which may erode the profitability of even the most technically accurate setups.

Therefore, the Fear Volatility Gate acts as a protective mechanism.

Oberlunar 👁️⭐

Signalgo XSignalgo X

Signalgo X is a sophisticated indicator crafted for traders who demand a disciplined, multi-layered approach to market analysis and trade management. This overview will help you understand its capabilities, logic, and how it can elevate your trading.

Core Concept

Signalgo X is built to:

Scan multiple timeframes simultaneously for price, volume, and volatility patterns.

Filter out unreliable signals during periods of market hype or manipulation.

Automate trade management with dynamic take-profit (TP), stop-loss (SL), and trailing logic.

Deliver actionable, visual signals and alerts for timely, confident decisions.

Inputs & Controls

Preset System Parameters:

News Sensitivity: Determines how responsive the indicator is to price moves.

Hype Filter Strength: Sets how aggressively the system avoids volatile, manipulated, or news-driven periods.

User-Configurable:

Show TP/SL Logic: Turn on/off the display of take-profit and stop-loss levels directly on your chart.

How Signalgo X Works

1. Multi-Timeframe Market Analysis

Signalgo X continuously monitors:

Closing price

Trading volume

Volatility (ATR)

across six distinct timeframes, from 1 hour to 3 months. This layered approach ensures that signals are validated by both short-term momentum and long-term trends.

2. Price, Volume, and Volatility Synthesis

Price Change: The system tracks percentage changes over each timeframe to gauge momentum.

Volume Ratio: By comparing current volume to a moving average, it detects unusual spikes that may signal institutional activity or manipulation.

Volatility: Measures the intensity of price movements relative to average ranges, helping to identify breakout or exhaustion scenarios.

3. Proprietary Anti-Hype Filter

A unique scoring mechanism evaluates:

Volume spikes without corresponding price action

Sudden jumps in volatility

Conflicting signals across timeframes

Social hype proxies (e.g., sharp moves on low volume)

If the market is deemed “hyped,” all trading signals are suppressed and a clear warning is shown, keeping you out of unpredictable conditions.

4. Signal Classification & Mapping

Significant Moves: Only price actions that exceed a sensitivity threshold and are confirmed by volume/volatility are considered.

Bullish/Bearish Signals: Generated for each timeframe.

Signal Strength: Categorized as regular, or strong based on multi-timeframe agreement.

Entry & Exit Strategy

Entry Logic

Long (Buy) Entry: Triggered when bullish signals are detected (of any strength) and no hype is present.

Short (Sell) Entry: Triggered when bearish signals are detected and no hype is present.

Exit & Trade Management

Stop Loss (SL): Placed at a calculated distance from entry, adapting to recent volatility.

Take Profits (TP1, TP2, TP3): Three profit targets, each at a greater reward multiple.

Trailing Stop: After the first take-profit is hit, the stop-loss moves to breakeven and a trailing stop is activated to protect further gains.

Event Tracking: The indicator visually marks when each TP or SL is hit, providing real-time feedback.

Chart Plots: All relevant SL, TP, and trailing stop levels are clearly marked for both long and short trades.

Labels: Entry, exit, and signal strength events are color-coded and visually prominent.

Alerts: Built-in alert conditions allow you to set up TradingView notifications for strong/regular buy/sell signals and hype warnings.

Trading Strategy Application

Multi-Timeframe Confirmation: Only strong signals confirmed by several timeframes are acted upon, reducing false positives.

Volume & Volatility Awareness: The indicator avoids low-quality, “fakeout” signals by requiring confirmation from both price and volume/volatility.

Hype Avoidance: Keeps you out of the market during news-driven or manipulated periods, helping to protect your capital.

Automated Discipline: The TP/SL logic enforces a rules-based exit strategy, helping you lock in profits and limit losses without emotional interference.

Who Should Use Signalgo X?

Signalgo X is ideal for traders who want:

Systematic, high-confidence signals

Automated and disciplined trade management

Protection against unpredictable market events

Clear, actionable visuals and alerts

VIX-Price Covariance MonitorThe VIX-Price Covariance Monitor is a statistical tool that measures the evolving relationship between a security's price and volatility indices such as the VIX (or VVIX).

It can give indication of potential market reversal, as typically, volatility and the VIX increase before markets turn red,

This indicator calculates the Pearson correlation coefficient using the formula:

ρ(X,Y) = cov(X,Y) / (σₓ × σᵧ)

Where:

ρ is the correlation coefficient

cov(X,Y) is the covariance between price and the volatility index

σₓ and σᵧ are the standard deviations of price and the volatility index

Enjoy!

Features

Dual Correlation Periods: Analyze both short-term and long-term correlation trends simultaneously

Adaptive Color Coding: Correlation strength is visually represented through color intensity

Market Condition Assessment: Automatic interpretation of correlation values into actionable market insights

Leading/Lagging Analysis: Optional time-shift analysis to detect predictive relationships

Detailed Information Panel: Real-time statistics including current correlation values, historical averages, and trading implications

Interpretation

Positive Correlation (Red): Typically bearish for price, as rising VIX correlates with falling markets. This is what traders should be looking for.

Negative Correlation (Green): Typically bullish for price, as falling VIX correlates with rising markets

How to use it

Apply the indicator to any chart to see its correlation with the default VIX index

Adjust the correlation length to match your trading timeframe (shorter for day trading, longer for swing trading)

Enable the secondary correlation period to compare different timeframes simultaneously

For advanced analysis, enable the Leading/Lagging feature to detect if VIX changes precede or follow price movements

Use the information panel to quickly assess the current market condition and potential trading implications

EWMA Volatility EstimatorThis script calculates EWMA Volatility (Exponentially Weighted Moving Average Volatility).

Commonly used model in financial risk management.

It estimates recent price volatility by applying more weight to the most recent returns, capturing volatility clustering while remaining responsive to fast market shifts.

The method uses a decay factor (λ) of 0.94, the standard value used in models like RiskMetrics, and converts the variance estimate into annualized volatility in percentage terms.

This is not a forecasting tool. It’s an estimator that reflects the magnitude of recent price moves in a statistically robust way.

It can be helpful for:

Understanding regime shifts in market behavior

Designing position sizing rules based on recent volatility

Filtering entries during high or low volatility phases

How It Works

Computes log returns of the closing price.

Squares the returns to get a proxy for variance.

Applies an exponential moving average to the squared returns using an equivalent EMA period based on λ = 0.94.

Converts the result to volatility by taking the square root and scaling to a percentage.

Key Characteristics

Backward-looking estimator

Reacts faster than standard rolling-window volatility

Smooths noise while still being sensitive to recent spikes

This script is educational and informational. It is not financial advice or a guarantee of performance. Always test any tool as part of a broader strategy before using it in live markets.

Jesus Vix Spike ComboThis script will:

Show you vix spikes with your 4 different settings.

Draw a white line at the start of each vix.

Draw a dotted green line for 3 spikes in 6 minutes.

Draw a dotted pink line for 3 spikes in 16 minutes.

Draw a green line extending right if it takes out a past low in the last 200 bars plus a spike.

It will also:

Place a white dot on the 5th candle if the price rises past the vix starting point,

a white omega sign on the 6th candle if price rises past the vix starting point,

and a large white dot on the 7th candle past the vix starting point if the price is higher.

It will also:

Show higher time frame EMAs and other emas.

Has some alerts added also.

I have only been using this on the 1 minute chart with $OANDA:SPX500USD.

Ill write about the strategy I use for this soon. But basically you wait for a drop and for some prominent lows to be taken out, then a vix, then your white dot, omega then the large white dot to enter, expect a 100% expansion from the vix low. More aggressive entry's would be the first white dot or 3 green candles in a row. Backtest to see.

Thanks for checking it out. Let me know if it can be better.

The original script is from Xxattaxx and Christ Moody I believe, thank you for sharing all your hard work.

Swing-Based Volatility IndexSwing-Based Volatility Index

This indicator helps traders quickly determine whether the market has moved enough over the past few hours to justify scalping.

It measures the percentage price swing (high to low) over a configurable time window (e.g., last 4–8 hours) and compares it to a minimum threshold (e.g., 1%).

✅ If the percent move exceeds the threshold → Market is volatile enough to scalp (green background).

🚫 If it's below the threshold → Market is too quiet (red background).

Features:

Adjustable lookback period in hours

Custom threshold for volatility sensitivity

Automatically adapts to the current chart timeframe

This tool is ideal for scalpers and short-term traders who want to avoid entering trades in low-volatility environments.

DAILY ATR LEVELS AND EXPECTED MOVE LEVELSThis Pine Script code is designed to visualize ATR (Average True Range) levels and expected move levels on a chart. It provides useful inputs for customizing how these levels are displayed, such as line width, style, and color. The script is divided into several sections, each focused on a different feature:

1. User Inputs for Customization:

- Line Width and Style: Users can customize the line width, style (solid, dotted, or dashed), and color for various levels.

- Offset for Line Placement: The rightOffset input controls how far in the future the lines extend (measured in minutes).

- Show Labels: Labels can be toggled on/off for ATR levels and expected move lines, with customizable text colors.

2. ATR Levels and ATR Settings:

- The ATR length (atrLength) and the multiplier (atrMultiplier) control the calculation of ATR levels.

- The script plots ATR levels based on the daily open price, including key levels like ATR +25%, ATR +50%, etc., for both positive and negative movements.

- Line Drawing: The script dynamically creates lines for each ATR level, and the lines are customized according to the user's inputs. For each level, the line.new function is used to plot a line from the start of the day (daily open) to a point offset in the future.

- Labels: Labels are added near each ATR level to make them more identifiable, such as "ATR +25%" or "Daily Open."

3. Expected Move Calculation and Logic:

- The script calculates the expected move for the next trading session based on the previous close price and the volatility derived from the VIX (Volatility Index).

- The expected move is calculated as a percentage of the previous close and is added and subtracted from the previous close price to generate upper and lower levels.

- Volatility Adjustment: The VIX value is adjusted by the square root of 252 (the number of average trading days in a year) to calculate the daily volatility.

- Upper and Lower Lines: Lines are drawn for the expected move's upper and lower bounds, showing the potential price movement based on volatility.

4. Customizable Expected Move Lines:

- Line Style and Color: The upper and lower expected move lines can be customized in terms of width, style, and color, as specified by the user.

- Labels for Expected Move Levels: Labels are added for the upper and lower expected move lines, such as "Expected Move Upper" and "Expected Move Lower."

5. Logic for Drawing Lines:

- The script continuously evaluates whether the levels should be displayed based on the user's preferences.

- If showATRLevels or showLineEM is enabled, the script will draw the respective lines and labels on the chart.

- It uses line.new to draw the lines and label.new to position the labels at the correct levels on the chart.

6. Handling Time and Line Deletion:

- The script handles the dynamic nature of the chart by deleting previous lines (using line.delete) to avoid cluttering the chart with outdated lines.

- The time for the lines is set dynamically using the startTime and endTime variables, ensuring that lines are drawn within the correct timeframe.

Summary of Key Features:

- ATR Levels: Plots key levels of ATR, such as daily open, ATR +25%, ATR -25%, etc., with customizable colors and line styles.

- Expected Move Levels: Calculates and plots the upper and lower bounds of the expected move based on the VIX and previous close price.

- Customization Options: Users can control the appearance (line width, style, color) and whether to show labels for the ATR and expected move levels.

- Dynamic Updates: The lines and labels update dynamically throughout the trading day, adjusting based on market conditions.

Overall, this script is designed to help traders visualize volatility and potential price movement on a daily chart by providing ATR-based levels and expected move projections. It offers a high degree of customization to suit different charting preferences.

Titan Wings 3 (by Oberlunar)Titan Wings 3: Volatility and Trend Dynamics Tool

Description:

Titan Wings 3 is a comprehensive indicator designed to help traders navigate complex market conditions by integrating volatility analysis, advanced moving averages, and dynamic signal generation. This script is not a simple combination of public domain tools; it is a carefully engineered system that merges statistical insights with market structure analysis to deliver actionable signals.

Core Functionality:

The indicator uses log returns to calculate volatility, which is then conditioned by price behavior relative to multiple moving averages. Volatility bands are dynamically adjusted based on percentile ranks, standard deviations, and ATR values to provide traders with precise zones of market activity. These bands are visualized on the chart, highlighting areas of potential breakout or reversal.

Titan Wings 3 features three types of moving averages—Exponential (EMA), Simple (SMA), and Hull (HMA)—giving users flexibility to align the tool with their trading strategies. The script evaluates price action relative to these averages, identifying critical zones where market sentiment shifts.

In addition to trend-following metrics, the script dynamically generates labels to signal key trading opportunities. These signals are derived from normalized distance calculations between the price and selected moving averages, combined with a proprietary methodology for filtering noise and amplifying significant trends.

Why Titan Wings 3 Stands Out:

Originality: Titan Wings 3 is not a generic mashup of indicators. Its unique normalization technique for distance metrics, percentile-based volatility thresholds, and the use of Hull Moving Averages make it a sophisticated tool for identifying high-probability trades.

Actionable Insights: The script provides real-time labels and visual cues for both long and short opportunities, allowing traders to act decisively during key moments of price action.

Adaptability: The customizable parameters for moving average types, percentile thresholds, and volatility multipliers ensure that the tool can adapt to various market conditions and trading styles.

How It Works:

Volatility Bands: Percentile-based calculations and ATR/standard deviation multipliers are used to create adaptive upper and lower bands, highlighting areas of market expansion and contraction.

Dynamic Labels: Signals are generated based on normalized metrics that measure the price's relationship to key moving averages, providing a reliable framework for trend identification.

Visual Overlays: The script fills specific price zones with color-coded areas to indicate bullish or bearish conditions, enhancing the clarity of market structure.

How to Use It:

Adjust the moving average type and parameters to align with your trading style.

Use the volatility bands to identify breakouts or reversals.

Follow the real-time labels to confirm potential trade entries.

Pay attention to the visual overlays to quickly assess market sentiment.

Conditional Volatility Explosion/ContractionThis indicator identifies zones of potential volatility expansion by analyzing the contraction and expansion of volatility bands, which are conditioned by the relationship of the price to moving averages

Volatility Squeeze: When the bands contract, it indicates a potential buildup in market tension, often preceding a significant price movement.

Volatility Expansion: When the bands expand, it signals the release of built-up tension, often resulting in increased volatility.

Trend Confirmation: The bands are active only when the price aligns with the moving average condition, helping to filter out less relevant signals during non-trending markets.

Upper Band: Displays as a red band when the volatility condition is met.

Represents the upper boundary of potential price action during high volatility.

Lower Band: Displays as a green band when the volatility condition is met.

Represents the lower boundary of potential price action during high volatility.

Fill Areas: The areas between the EMA and the bands are filled with transparent colors:

Red for the upper fill.

Green for the lower fill.

These highlights help visualize zones of potential volatility explosion.

VolbandsThe Volbands indicator dynamically plots upper and lower volatility bands based on implied daily moves derived from volatility indices. This tool provides a visual forecast of the next trading day's price range, helping traders anticipate potential price movement boundaries.

Key Features:

1. Auto-Detect Volatility Index: Volbands automatically detects the appropriate volatility index based on the current symbol. For example, it uses the VIX for S&P 500, VXN for Nasdaq 100, and custom indexes like VXAPL for Apple. Users can also manually select a specific volatility index if preferred.

2. Projected Bands:

- The indicator plots the projected upper and lower bands for the next trading day using the implied move from the volatility index.

- Displays today’s projected bands as a reference and overlays next day’s bands with a slight offset, visually indicating the anticipated range.

3. Dynamic Updates: The indicator updates automatically as new bars are added, ensuring that users have up-to-date projections based on the latest volatility data.

4. Highlighting Extreme Price Action: Candles that close outside of the projected bands are colored in yellow, highlighting moments of higher-than-expected volatility.

5. Informative Table: A customizable table displays relevant information, including:

- The selected or auto-detected volatility index

- Implied daily move percentage

- Projected upper and lower levels

Potential Applications:

- Risk Management: The Volbands indicator can help traders set more informed stop-loss and take-profit levels based on volatility-driven price projections.

- Identifying Overbought/Oversold Conditions: Price movement outside the projected bands may indicate overbought or oversold conditions, potentially signaling trade opportunities.

-Enhancing Entry and Exit Points: The projected bands act as soft support and resistance levels, assisting traders in timing entries and exits in anticipation of volatility-driven price reactions.

Future Enhancements:

Potential improvements to expand functionality could include:

- Additional Volatility Indices: Expanding coverage to include more assets and volatility indices.

- Alerts: Setting alerts for when prices breach the projected bands, enabling traders to react quickly to unexpected price movements.

- Customization of Bands: Adding options for users to adjust the implied move percentage, creating customized bands that reflect individual trading strategies.

This indicator combines implied volatility with price action, offering valuable insights to traders on expected price ranges and volatility.

MMRI Chart (Primary)The **Mannarino Market Risk Indicator (MMRI)** is a financial risk measurement tool created by financial strategist Gregory Mannarino. It’s designed to assess the risk level in the stock market and economy based on current bond market conditions and the strength of the U.S. dollar. The MMRI considers factors like the U.S. 10-Year Treasury Yield and the Dollar Index (DXY), which indicate investor confidence in government debt and the dollar's purchasing power, respectively.

The formula for MMRI uses the 10-Year Treasury Yield multiplied by the Dollar Index, divided by a constant (1.61) to normalize the risk measure. A higher MMRI score suggests increased market risk, while a lower score indicates more stability. Mannarino has set certain thresholds to interpret the MMRI score:

- **Below 100**: Low risk.

- **100–200**: Moderate risk.

- **200–300**: High risk.

- **Above 300**: Extreme risk, indicating market instability and potential downturns.

This tool aims to provide insight into economic conditions that may affect asset classes like stocks, bonds, and precious metals. Mannarino often updates MMRI scores and risk analyses in his public market updates.