inwCoin HMA AlertSimple alert to go along with the inwCoin HMA Strategy

Please not that the alerts are persistent 2.70% , if you already enter the position,

just ignore the rest of the same alert until the opposite alert show up

( long then short / or short then long , if change, just close and enter opposite position )

You can set the alert and let it tell you to iOS app via TradingView app ( yey! )

Please note that, if you don't have bot to track your trailing start/stop. you have to enter the TP/SL manually ( also tracking the position )

So... be careful to follow this alert. just try it with small amount of money first.

and make sure to set stop loss every time because OKEX is a portfolio killer if you don't have any stop loss.

** if you cannot trailing stop bot, just uncheck the "Aggressive Strategy" in both strategy and alert to reduce alert to minimum level.

In den Scripts nach "bot" suchen

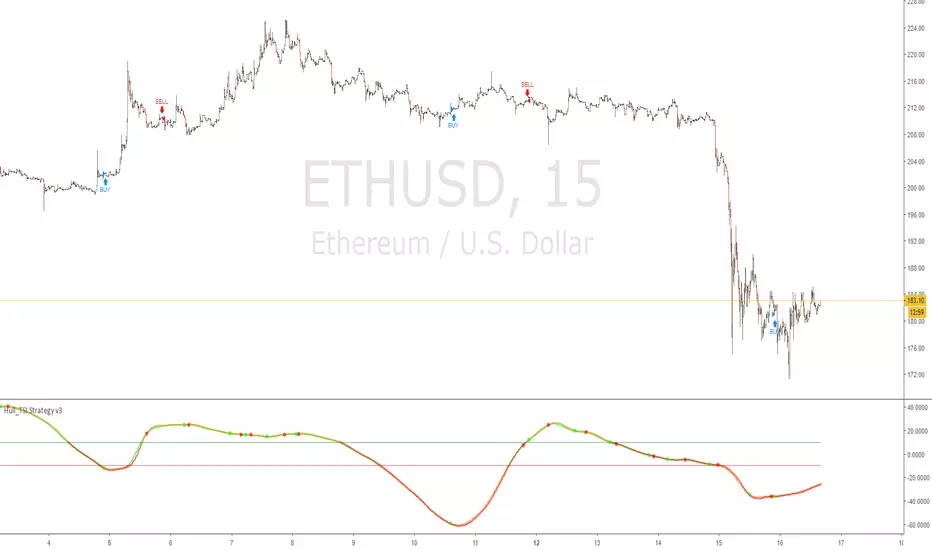

Hull_TSI Strategy v3True Strength Index, but Exponential Moving Average taken out and replaced with Hull Moving Average

this version uses 3 Hull MA's as well as the TSI value crossovers above or below the upper/lower lines

This version is the closest to the API bot featured at gekkoplus.com

Hull_TSI bot is competing in the competition

" Gekko Plus is hosting a strategy contest. Submit the best performing Gekko strategy and win 0.1 BTC! "

15 Nov 2018: Strategy contest start

10 Dec 2018: Strategy contest end

12 Dec 2018: Contest evaluation, announcement of winners!

Most Profitable HelloEpicWorld v2.0[Eric] This is the most profitable un-repaint fully support auto trading Algo on earth.

Usage:

Buy and Sell && Stop Loss

1. When it shows buy, you can buy it immediately or wait for a small dump to buy it, stop loss at the red cross below.(Both buy and stop signal support alert autoview bots auto trading)

2. When it shows sell, you can sell it immediately or wait for a small pump to sell it, stop loss at the green cross above.(Both buy and stop signal support alert autoview bots auto trading)

Background Color:

It can be turn on and off in the settings. When it is green, you have a 78% probability to get a win trade on buying the pullback. And a 73% probability to get a win trade on selling the pullback when it's red. So, even missed the buy and sell signal, you can still open a trade in the middle, but I don't recommend this kind of trades, it's no good for Risk/Reward ratio. The best ratio is when the signal show up. Background color is more suitable using to hold your trades after entering.

Forex:

Bitcoin:

Altcoin:

MarketSpeed:

RSIC:

3 HULLs & ICHIMOKU divided by PRICEBasically just another form of moving average, for quick swings, built for testing/use with API cryptobots, simple switch from buy to sell.

Hull MA(2 candles back) times 3 plus Ichimoku divided by price(1 candle back) = value1

Hull MA(3 candles back) times 3 plus Ichimoku divided by price(1 candle back) = value2

if value1>value2 then buy else sell

calculates price from 1 candle back, and calculates signal from 2nd and 3rd candle prices, so no repainting? so best on low timeframes.

for when use in bot, would not need 1 candle lag. Lag is for TV chartists to not have to suffer repainting.

Bots do not repaint. they are not "painting" anything, they simply open or close orders, which cannot be "repainted"

but here on TV chart, when you refresh the browser page, the script recalculates, and signals may be repainted.

hopefully this will not repaint. please test. thankyou

MACs EasyMoney - LongTermSignalsIntroducing " MACs EasyMoney - LongTermSignals " Indicator. Specially designed for weekly and 1 Month duration charts . Picks the calls perfectly :)

Latest other updates:

BOT Trading Integration is completed for the following indicators,

1) MACs EasyMoney - Swing Trade Signals

2) MACs EasyMoney - Scalp Trade Signals

Strategy Test Report for the BOT script shows the following results,

* Profitable Percent = 99.42%

* Profitable Factor = 93.76

Thanks,

Mac.

Pharoceus PT-V2 CryptoScalper RSI+BB+SRSI+Stochastic IndicatorThis is the updated Version of the ProfitTrailerV2 RSI+BB+StochRSI+Stochastic Oscillator Signal+Alerts

Description

This is an all-in-one indicator with alerts that most people call signals and it's designed for Cryptocurrency leverage trading. This indicator features, the most popularly used indicators in technical analysis and are the basic technical analysis indicators any successful trader should master before going into more advance technical analysis tools. The Pharoceus ProfitTrailerV2 CryptoScalper RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts features the Bollinger Bands, Relative Strength Index, Stochastic RSI and Stochastic Oscillator, and it was designed for use with Pharoceus ProfitTrailerV2 CryptoScalper and can also be used with all other trading bots or on its own as a powerful market leveraging and trading indicator using alerts.

The ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts can be customized to any trader specific trading patterns and offers the ability to choose a combination of indicators from the featured ones to use. With the Buy and Sell Signal feature, trading on any cryptocurrency exchange can be automated and with the alerts feature, the Pharoceus ProfitTrailerV2 CryptoScalper RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts will automated buying and selling signals for any crypto trading bot but I'll always recommend using for making buys only when using with any bot. This indicator/script can be used with any base pair; BTC, ETH, and USD or USDT.

As mentioned above, all four indicators can be combined to find a very safe and secure buy and profitable sell signals, which maximizes your profit margins and overall earnings over time. Also, 2 or 3 could be combined as well, depending on the traders knowledge on how to use each indicator independently to find its best settings. My recommendation would be to test all independently and or together with very little capital to find what works best for you. I recommend this because the cryptocurrency market in a very volatile market and unpredictable, some combination of indicators would work for some certain coin pairs and not all, while others would work better with a different setting and a particular coin pair.

As with all script use at your own risk and only trade what you can afford to lose, while this indicator isn't designed to lose you money and I will not be held liable for any losses due to misuse. I am also not a financial advisor and the ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts will be made available soon as it's still undergoing rigorous testing and it's in no way and manner affiliated with any group of individuals or bot.

Trade Smart and with only what you can afford. Donations are also welcome to encourage my work, This is a totally free to use script to help traders, small time or big time that works towards making the indicator sharing world accessible to all who will not definitely be ripped-off and support a community of sharing.

discord.gg

BTC: 199qMzu4gvr3bUXWEpLG5uS6TEKKvw5pbe

ETH: 0xf8339952a224a228f2f8c58a5666a8ffleddebfb

BCH: qqmmds8u3f8m6ek387jtefg07525dvaxzqrshd86gz

Ichimoku Cloud Strategy for CryptoVersion 1.0

This strategy uses the Ichimoku Cloud indicators and is based on a bot i developed. The bot has more entry/exit rules which will hopefully be added in the near future.

Still a profitable strategy even in it's simplest form.

Do not run this strategy on a timeframe < 1h, best timeframe will be 4h

Happy Trading!!

If you find this strategy useful, please consider a donation to:

BTC: 1PGuWcQwb4WZyFYX4ehyqcJWcbX42jW7Y6

ETH: 0x912aD30Ff9A49c69D51ECeE5A65A7E7d5321ED0C

ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+AlertsThis is an all-in-one indicator with alerts that most people call signals and it's designed for Cryptocurrency leverage trading. This indicator features, the most popularly used indicators in technical analysis and are the basic technical analysis indicators any successful trader should master before going into more advanced technical analysis tool. The ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts features the Bollinger Bands, Relative Strength Index, Stochastic RSI and Stochastic Oscillator, and it was designed for use with ProfitTrailer V2 and can also be used with all other trading bots or on its own as a powerful market leveraging and trading indicator using alerts.

The ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts can be customized to any trader specific trading patterns and offers the ability to choose a combination of indicators from the featured ones to use. With the Buy and Sell Signal feature, trading on any cryptocurrency exchange can be automated and with the alerts feature, the ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts will automated buying and selling signals for any crypto trading bot but I'll always recommend using for making buys only when using with any bot. This indicator/script can be used with any base pair; BTC, ETH, and USD or USDT.

As mentioned above, all four indicators can be combined to find a very safe and secure buy and profitable sell signals, which maximizes your profit margins and overall earnings over time. Also, 2 or 3 could be combined as well, depending on the traders knowledge on how to use each indicator independently to find its best settings. My recommendation would be to test all independently and or together with very little capital to find what works best for you. I recommend this because the cryptocurrency market in a very volatile market and unpredictable, some combination of indicators would work for some certain coin pairs and not all, while others would work better with a different setting and a particular coin pair.

As with all script use at your own risk and only trade what you can afford to lose, while this indicator isn't designed to lose you money and I will not be held liable for any losses due to misuse. I am also not a financial advisor and the ProfitTrailerV2 RSI+BB+SRSI+Stochastic Oscillator Signal+Alerts will be made available soon as it's still undergoing rigorous testing.

CMYK RMI TRIPLE Automated strategy▼ This is the strategy version of the script.

◊ Introduction

This script makes use of three RMI 's, that indicate Overbought/Oversold on different timescales that correspond with Frequency’s that move the market.

◊ Origin

The Relative Momentum Index was developed by Roger Altman and was introduced in his article in the February, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

While RSI counts up and down ticks from close to close, the Relative Momentum Index counts up and down ticks from the close relative to a close x number of days ago.

This results in an RSI that is smoother, and has another setting for fine tuning results.

This bot originated out of Project XIAM , an investigative script that outlined my approach towards Automated Trading Strategies.

Are you interested in writing bots yourself ? check out the beta version of this script.

It has many bugs, but also most of the Skeleton.

◊ Usage

This script is intended for Automated Trading with AUTOVIEW or TVAUTOTRADER , on the 1 minute chart.

◊ Features Summary

Overlay Mode

Indicator Mode

Three RMI's

Trend adjustment

Pyramiding

Ignore first entries

Take Profit

Stop Loss

Interval between Entries

Multiring Fix

Alert signal Seperation

◊ Community

Wanna try this script out ? need help resolving a problem ?

CMYK :: discord.gg

AUTOVIEW :: discordapp.com

TRADINGVIEW UNOFFICIAL :: discord.gg

◊ Setting up Autoview Alerts

Use the study version of this script, To set up The Alerts Autoview Picks up on.

The Signals to work with are :

Open 1 Long

Use this to open one Long Position.

With quantity being : /

Once per bar

Being larger than 0

Comment example : e=exchange b=long q=amount t=market

Open 1 Short

Use this to open one Short Position.

With quantity being : /

Once per bar

Being larger than 0

Comment example : e=exchange b=short q=amount t=market

Close1 Position

Use this to Close The amount of one Open Position.

With quantity* being : /

Once per bar

Being larger than 0

Comment example : e=exchange c=position q=amount t=market

*Beware when using a percental % quantity, instead of an absolute quantity.

Percental Quantities are based on the , Not

And will change in absolute value relative to the amount of open trades.

Close All positions

Use this to Close All Open Positions.

With quantity being :

Once per bar

Being larger than 0

Comment example : e=exchange c=position t=market

For the specific Syntax used in the comment of the alert, visit Autoview .

◊ Setting up TVAutotrader

Use the strategy version of this script, And load it into TVAT .

◊ Backtesting

Use the strategy version of this script for backtesting.

◊ Contact

Wanna try this script out ? need help resolving a problem ?

CMYK :: discord.gg

PT Magic Triggers So its me again. I have decided to create Trend Trigger Script for PT Magic addon for a trading bot Profit Trailer. If you do not own this bot and Addon the following explanation will not help you.

For each Trend you define number of minutes and it then calculates the percentage change between the close price now and X candles before.

Same calculation is for all 6 Triggers i beleive that is all you need :)

Hope it helps you all.

LTC: LYHj4WDN7BPu5294cSpqK3SgWSWdDX56Qt

BTC: 1NPVzeDSsenaCS9QdPro877hkMk93nRLcD

MACD, backtest 2015+ only, cut in half and doubledThis is only a slight modification to the existing "MACD Strategy" strategy plugin!

found the default MACD strategy to be lacking, although impressive for its simplicity. I added "year>2014" to the IF buy/sell conditions so it will only backtest from 2015 and beyond ** .

I also had a problem with the standard MACD trading late, per se. To that end I modified the inputs for fast/slow/signal to double. Example: my defaults are 10, 21, 10 so I put 20, 42, 20 in. This has the effect of making a 30min interval the same as 1 hour at 10,21,10. So if you want to backtest at 4hr, you would set your time interval to 2hr on the main chart. This is a handy way to make shorter time periods more useful even regardless of strategy/testing, since you can view 15min with alot less noise but a better response.

Used on BTCCNY OKcoin, with the chart set at 45 min (so really 90min in the strategy) this gave me a percent profitable of 42% and a profit factor of 1.998 on 189 trades.

Personally, I like to set the length/signals to 30,63,30. Meaning you need to triple the time, it allows for much better use of shorter time periods and the backtests are remarkably profitable. (i.e. 15min chart view = 45min on script, 30min= 1.5hr on script)

** If you want more specific time periods you need to try plugging in different bar values: replace "year" with "n" and "2014" with "5500". The bars are based on unix time I believe so you will need to play around with the number for n, with n being the numbers of bars.

Trend Targets Oscillator- Webhooks v1.8.3Trend Targets Oscillator - Webhooks v1.8.3

Overview

This technical indicator combines a momentum-based oscillator with statistical analysis of historical price behavior to generate trading signals and calculate position management levels. The indicator analyzes past price patterns to establish data-driven thresholds for entries, exits, and stop placement.

Key Components:

• Weighted momentum oscillator with trend-following characteristics

• Statistical percentile analysis for take profit level calculation

• Dynamic stop loss placement based on price structure and volatility

• Adaptive ranges (ATR-based) for dynamic support/resistance visualization

• Real-time performance tracking and historical signal analysis

Critical Disclaimer: This indicator performs technical analysis on historical data. Past patterns, statistics, and performance do not predict, indicate, or guarantee future results. All trading carries substantial risk of loss. This tool does not provide investment advice or trading recommendations.

Important Note: Calculations use standard OHLC data; results may differ on non-standard chart types (Heikin Ashi, Renko, Kagi, Point & Figure, Range).

Technical Methodology

1. Momentum Oscillator

Core Approach: The oscillator employs a weighted Relative Strength Index (RSI) methodology combined with Quantitative Qualitative Estimation (QQE) trailing stop concepts. This creates a momentum indicator that adapts to trending conditions while maintaining sensitivity to reversals.

How It Functions:

• Calculates directional price momentum using weighted price changes

• Applies directional bias to amplify movements aligned with the prevailing trend direction

• Uses a dynamic trailing stop mechanism adapted from QQE methodology to identify potential trend reversals

• Applies exponential moving average smoothing to reduce market noise

• Operates within configurable overbought/oversold threshold zones (default: 70/30)

Signal Generation Process:

• BUY signals occur when the oscillator line crosses above its trailing stop level

• SELL signals occur when the oscillator line crosses below its trailing stop level

• All signals confirm only at bar close, eliminating mid-bar fluctuations and repainting

Technical Parameters (All Configurable):

• RSI Length (default: 100 bars) - Controls the period for momentum calculation

• Stop Multiplier (default: 2.5) - Adjusts the sensitivity of the trailing stop mechanism

• Smoothing Length (default: 6 bars) - Reduces noise through exponential smoothing

• Directional Weight (default: 6.4) - Amplifies trend-aligned price movements

• Overbought/Oversold Levels (default: 70/30) - Defines momentum extreme zones

What This Component Does: This component identifies potential trend changes through momentum analysis, generates entry signals based on the interaction between an oscillator and a trailing stop, filters those signals using overbought and oversold zones, and confirms all signals at bar close to help prevent repainting.

What This Component Does Not Do: This component does not predict future price direction or guarantee signal accuracy or profitability, it cannot eliminate false signals entirely, and it will not perform equally well across all market conditions.

2. Statistical Take Profit Calculation

Methodology: Rather than using fixed risk-reward ratios, this indicator analyzes the Maximum Favorable Excursion (MFE) from historical signals to establish statistically-derived take profit levels using percentile (quantile) analysis.

Maximum Favorable Excursion (MFE) Concept: MFE measures how far price moved in the favorable direction after each historical signal before either reversing or hitting the stop loss. This creates a dataset of historical "best case" price movements for each direction.

Statistical Process:

• Maintains separate historical datasets for LONG signals and SHORT signals (markets behave differently in uptrends vs downtrends)

• Tracks MFE data from the last N signals (configurable, default: 20 signals per direction)

• Calculates percentiles (quantiles) from this historical MFE dataset

• Uses these percentiles to determine take profit distance from entry

Three Statistical Thresholds:

TP1:

• Default: 66th percentile of historical MFE data

• Meaning: Based on historical analysis, approximately 66% of similar past signals moved at least this far in the favorable direction

• Note: This is a statistical observation of past behavior, not a prediction that 66% of future signals will reach this level

TP2:

• Default: 50th percentile (median) of historical MFE data

• Meaning: Represents the middle point of historical favorable price movements

• Note: Past median values do not indicate future median performance

TP3:

• Default: 30th percentile of historical MFE data

• Meaning: Based on historical analysis, approximately 30% of similar past signals moved at least this far

Important Technical Notes:

• Percentile thresholds are fully configurable in settings (you can adjust 66/50/30 to any values)

• Requires minimum historical data (20+ signals per direction) for statistical relevance

• Falls back to configurable risk-reward ratio (default 1.5R) when insufficient historical data exists

• Recalculates dynamically as new signals complete and add to the historical dataset

• "R" represents Risk units (distance from entry to stop loss)

What This Component Does: This component analyzes historical price behavior patterns and calculates statistical percentiles from past favorable movements to establish take-profit levels based on observed historical data. It adapts to the specific instrument and timeframe being analyzed, and it separates its analysis for long versus short signals.

What This Component Does Not Do: This component does not predict where future price will reach or guarantee any specific hit rate or success percentage, and it cannot ensure profits on any individual trade. It also does not account for changing market conditions or regime shifts, and it does not replace the need for proper risk management and position sizing.

3. Dynamic Stop Loss Placement

Methodology: Stop loss calculation combines Donchian Channel logic with Average True Range (ATR) volatility adjustment to create stops that respect recent price structure while accounting for normal market fluctuations.

How It Functions:

Donchian Channel Component:

• Identifies the highest high and lowest low over a specified lookback period (default: 20 bars)

• For LONG signals: Uses the lowest low as the base for stop placement

• For SHORT signals: Uses the highest high as the base for stop placement

• This respects recent price structure and support/resistance levels

ATR Volatility Buffer:

• Calculates the Average True Range over 14 periods to measure current volatility

• Adds a configurable buffer (default: 1.0 × ATR) beyond the Donchian extreme

• For LONG signals: Stop = Donchian Low - (ATR × Buffer Multiplier)

• For SHORT signals: Stop = Donchian High + (ATR × Buffer Multiplier)

• This prevents premature stop-outs from normal price volatility

Technical Parameters (All Configurable):

• Donchian Length (default: 20 bars) - Period for identifying recent price extremes

• SL Buffer Multiplier (default: 1.0 × ATR) - Distance beyond Donchian extreme (0.0 to 5.0)

What This Component Does: This component places stops based on recent price structure using Donchian extremes, adjusts them to reflect current volatility via an ATR-based offset, and adapts dynamically as conditions change. It includes a configurable buffer to suit different trading styles and is designed to respect key technical support and resistance levels.

What This Component Does Not Do: This component does not guarantee that a stop loss will not be hit, nor can it prevent slippage, gaps, or other execution-related risks. It does not ensure a favorable risk-reward outcome on every trade, does not account for fundamental events or news releases, and it does not replace the need for proper position sizing and overall capital management.

4. Adaptive Ranges (ATR-Based)

Methodology: The indicator includes an optional overlay that displays adaptive support and resistance zones based on Average True Range (ATR) volatility measurements. These ranges adjust dynamically as price moves beyond volatility thresholds.

How It Functions:

• Calculates an adaptive moving average that shifts when price moves beyond ATR-based thresholds

• Displays five levels: Upper Resistance 2 (R2), Upper Resistance 1 (R1), Middle (AVG), Lower Support 1 (S1), Lower Support 2 (S2)

• Zones are created using ATR multiples above and below the adaptive average

• When price breaches the outer boundaries significantly, the entire range structure recalculates and repositions

Technical Parameters (All Configurable):

• Length (default: 50 bars) - Period for ATR calculation

• Factor (default: 6.0) - Multiplier for ATR to set zone width

• Source (default: close) - Price data used for calculations

• Show (default: ON) - Toggle visibility

Purpose and Use:

• Provides context for potential reversal or consolidation areas

• Can complement the statistical TP levels by showing additional resistance/support

• Helps visualize market volatility expansion and contraction

• Creates dynamic zones that adapt to changing volatility conditions

What This Component Does: This component displays volatility-adjusted support and resistance zones, adapt dynamically to price movement and changing volatility, providing visual context for potential reversal areas. The segments update when price moves beyond defined threshold boundaries.

What This Component Does Not Do: This component does not predict future support or resistance levels, does not guarantee that reversals will occur at zone boundaries, or replace traditional support and resistance analysis. It also does not account for fundamental catalysts or news-driven events that can override technical behavior.

Visual Components and Displays

Oscillator Panel (Lower Pane)

The oscillator displays in a separate pane below the price chart with the following elements:

• Main Oscillator Line (teal/green): Shows current momentum state

• Trailing Stop Line (purple): Dynamic support/resistance level that triggers signals

• Overbought/Oversold Zones: Horizontal threshold lines (default 70/30)

• Historical Signal Markers: BUY (green triangles up) and SELL (red triangles down) where signals occurred

Reading the Display:

- When oscillator crosses above trailing stop = BUY signal generated

- When oscillator crosses below trailing stop = SELL signal generated

- Oscillator in upper zone (>70) = momentum in overbought territory

- Oscillator in lower zone (<30) = momentum in oversold territory

On-Chart Overlays (Price Chart)

For each historical signal, the indicator displays visual overlays on the main price chart:

Entry Line (Yellow):

- Horizontal line showing the price level where the signal was generated

- Helps identify the actual entry point

Stop Loss Line (Red):

- Horizontal line showing the calculated stop loss level

- Based on Donchian + ATR methodology described above

Three Take Profit Zones (Green for LONG / Red for SHORT):

- TP1 Zone: Lightest shade - conservative percentile target

- TP2 Zone: Medium shade - moderate percentile target

- TP3 Zone: Darkest shade - aggressive percentile target

- Zones displayed as shaded rectangular areas extending forward from signal

Visual historical overlays: This provides visual feedback on historical signal performance and helps assess whether the statistical methodology is appropriate for the current instrument and timeframe.

These visual overlays allow you to see: These visual overlays allow you to see where historical signals occurred and at what price, where stops were placed according to the methodology, and where statistical take-profit levels were calculated. They also show which targets were reached versus not reached, how price behaved relative to the statistical projections, and the adaptive support/resistance context that frames overall market structure.

Statistics Table (Real-Time Analysis)

The indicator displays a comprehensive statistics table (typically in the upper-right corner) showing performance metrics for historical signals.

Table Header: "Historical stats (not predictive) under current settings"

Performance Metrics (Separate rows for BUY and SELL): For the Last N Signals (default: last 20 BUY and last 20 SELL separately):

Column Headers:

• Signal: Direction (BUY or SELL)

• Win: Count of signals where at least one take profit was reached before stop loss

• Loss: Count of signals where stop loss was hit before any take profit was reached

• TP1 Hit: Percentage of signals that reached the first take profit level

• Δ1%: Average percentage distance from entry to TP1, calculated only for signals that actually reached TP1

• TP2 Hit: Percentage of signals that reached the second take profit level

• Δ2%: Average percentage distance from entry to TP2, calculated only for signals that actually reached TP2

• TP3 Hit: Percentage of signals that reached the third take profit level

• Δ3%: Average percentage distance from entry to TP3, calculated only for signals that actually reached TP3

Understanding the Distance Metrics:

The "Dist%" columns show the average percentage gain (from entry price to TP level) for only those trades that successfully reached that specific TP level. This helps you understand the typical profit magnitude when that target is hit.

Footer Message (Historical Performance Evaluation): The table displays one of three messages based on historical loss percentage:

✅ "Historical performance threshold met. Based on past data under current settings. Not a recommendation."

- Displayed when both LONG and SHORT directions show less than 40% losses on past historical data on this specific instrument and timeframe

- indicates the loss-rate is below the configured threshold (40% losses) for both directions over the last N historical observations (descriptive only).

🛑 "Historical performance below threshold. Based on past data under current settings. Not a recommendation."

- Displayed when both LONG and SHORT directions show more than 40% losses on past historical data on this specific instrument and timeframe

- indicates the loss-rate is above the configured threshold (40% losses) for both directions over the last N historical observations (descriptive only).

⚠️ "Historical performance: Mixed / higher risk. Based on past data under current settings. Not a recommendation."

- Displayed when one direction is <40% loss and one is >40% loss on past historical data on this specific instrument and timeframe

- indicates a mixed result: one direction is above and the other is below the threshold over the last N historical observations (descriptive only).

These statistics and messages are descriptive of past historical performance for the specific instrument and timeframe being analyzed, and they are provided purely as informational tools to help you understand how the indicator behaved historically. They are based solely on historical data analysis and can change over time as new signals complete and the underlying dataset updates.

These statistics and messages are not predictions of future performance, trading recommendations or advice, or guarantees of profitability. They do not indicate that past results will repeat, and they should not be interpreted as suggestions to enter trades or to avoid them.

The footer message helps you understand whether the current settings and statistical thresholds have shown historically favorable or unfavorable results on this particular market. However, past favorable statistics do not ensure future favorable results, and past unfavorable statistics do not ensure future unfavorable results.

Configuration Options

All parameters are fully adjustable in the indicator settings. Default values are provided as starting points and may require optimization for different instruments and timeframes.

Oscillator Parameters

• RSI Length (default: 100)

Controls the period used for momentum calculation. Higher values = smoother, slower momentum readings. Lower values = more responsive, potentially noisier readings.

• Stop Multiplier / QQE Factor (default: 2.5)

Controls sensitivity of the trailing stop mechanism. Higher values = wider trailing stop, fewer signals, more trend-following. Lower values = tighter trailing stop, more signals, more sensitive to reversals.

• Smoothing Length (default: 6)

EMA smoothing applied to reduce noise. Higher values = smoother oscillator line. Lower values = more responsive to price changes.

• Directional Weight (default: 6.4)

Amplification factor for trend-aligned movements. Higher values = stronger bias toward current trend direction. Lower values = more balanced, less trend-biased.

• Source (default: close)

Price data used for calculations (close, open, high, low, hl2, hlc3, ohlc4).

Threshold Parameters

• Overbought Level (default: 70)

Oscillator level considered overbought. Range: 0-100. Used for signal filtering and visual reference.

• Oversold Level (default: 30)

Oscillator level considered oversold. Range: 0-100. Used for signal filtering and visual reference.

Statistical Analysis Parameters (Historical Percentile Targets)

• Lookback N Trades (default: 20)

Number of historical signals to include in statistical analysis. Analyzed separately for LONG and SHORT. Higher values = more stable statistics, slower adaptation. Lower values = more adaptive, potentially less stable statistics. Minimum: 5 signals.

• TP1 Target Percentile (default: 66)

Percentile of historical MFE data used for first take profit. Range: 1-99. 66 means ~66% of historical signals reached at least this distance. Higher percentile = more conservative target (closer to entry). Lower percentile = more aggressive target (farther from entry).

• TP2 Target Percentile (default: 50)

Percentile of historical MFE data used for second take profit. 50 = median of historical favorable movements. Adjust based on desired risk-reward profile.

• TP3 Target Percentile (default: 30)

Percentile of historical MFE data used for third take profit. 30 means ~30% of historical signals reached at least this distance. More aggressive, historically reached less frequently.

• Fallback TP (default: 1.50 R)

Risk-reward ratio used when insufficient historical data exists. "R" = Risk units (distance from entry to stop loss). 1.50 R = take profit placed at 1.5× the distance to stop loss. Used until enough signals accumulate for statistical calculation.

Note on Percentile Configuration:

You can customize these percentiles to match your trading style:

- Conservative approach: Use higher percentiles (e.g., 80/60/40) for closer, more frequently reached targets

- Aggressive approach: Use lower percentiles (e.g., 50/30/15) for extended targets with lower historical hit rates

- Balanced approach: Default values (66/50/30) provide middle ground

Stop Loss Parameters

• Donchian Length (default: 20)

Lookback period for identifying recent price extremes. Higher values = stops based on longer-term structure. Lower values = stops based on shorter-term swings.

• SL Buffer (× ATR) (default: 1.00)

Multiplier for ATR-based volatility buffer. Range: 0.0-5.0. 1.0 = stop placed one ATR beyond Donchian extreme. Higher values = wider stops, less risk of premature stop-out. Lower values = tighter stops, higher risk of normal volatility hitting stop.

Adaptive Ranges (ATR-Based) Parameters

• Length (default: 50)

Period for ATR calculation used in adaptive range zones. Higher values = zones based on longer-term volatility. Lower values = zones more responsive to recent volatility changes.

• Factor (default: 6.0)

Multiplier applied to ATR for determining zone width. Higher values = wider zones, farther from average. Lower values = tighter zones, closer to average.

• Source (default: close)

Price data used for adaptive average calculation.

• Show (default: ON)

Toggle visibility of adaptive range overlays on chart. Turn OFF for cleaner chart if you only want oscillator signals.

Visual Display Parameters

• Show Historical B/S Markers (Pane) (default: ON): Displays BUY/SELL triangles in oscillator panel.

• Show B/S on Price Chart (default: ON): Displays BUY/SELL markers on main price chart.

• Show History TP/SL Overlays (default: ON): Displays entry lines, stop lines, and TP zones on price chart. Turn OFF for cleaner chart if you only want the oscillator signals.

• History Segment Length (Bars) (default: 20): How many bars forward the TP/SL overlays extend from signal. Range: 5-200 bars. Does not affect calculations, only visual display duration.

Initial Setup and Learning Period

1. Adding Indicator to Chart

The indicator can be applied to any instrument and timeframe. Default settings are provided as a starting point.

2. Data Collection Period

The statistical analysis requires historical signals to function. Typically 20+ bars provide initial data, while 50-100+ bars may produce more robust statistics. The table displays "Not enough data yet to evaluate" until sufficient signals exist.

3. Observing Initial Performance

Signals develop over time. The calculated TP levels appear relative to actual price movement. Historical statistics show which direction (LONG vs SHORT) has performed differently. The statistics table displays historical behavior patterns.

4. Statistical Data Accumulation

The indicator accumulates historical data over time. Some traders choose to observe performance in paper trading or demo environments before live use. Understanding the methodology involves reviewing how calculations work on historical data.

Webhook Integration and Alerts

The indicator includes alert functionality for integration with automated trading systems and notification services.

Alert Characteristics:

• Alerts trigger only when signals confirm at bar close (no mid-bar alerts)

• Respects the historical performance evaluation footer status

• Includes symbol, timeframe, and direction information in alert message

• Provides JSON-formatted data for easy parsing by automated systems

• Separate alert events for: Entry, TP1, TP2, TP3, Stop Loss, Early Close (Win/Loss)

Alert Events Available:

- Entry: When a new signal is generated

- TP1/TP2/TP3: When each take profit level is reached

- SL: When stop loss is hit

- Early Close Win: When position closes early in profit (without hitting TP or SL)

- Early Close Loss: When position closes early at a loss (without hitting TP or SL)

JSON Data Structure:

Each alert contains structured data including:

• Event type (Entry, TP1, TP2, TP3, SL, etc.)

• Direction (long/short)

• Symbol and timeframe

• Price levels (entry, stop, take profits)

• Timestamps (entry time, event time)

• Duration (milliseconds and minutes from entry to event)

Compatible With:

• Third-party webhook automation platforms and tools that support TradingView webhooks

• Custom trading bot implementations via webhook endpoints

• Notification systems that can receive TradingView alerts

• Any service supporting webhook integration through TradingView's alert system

The author and indicator provider assume no responsibility for losses incurred through automated trading, alert-based systems, webhook implementations, or any third-party integrations. Users are solely responsible for their trading decisions, automation setup, risk management, and system monitoring.

What This Indicator Is and Is Not

What This Indicator Is:

This indicator is a technical analysis tool that combines momentum oscillation with statistical analysis, using a signal-generation methodology built on weighted RSI and QQE concepts. It calculates take-profit levels through historical percentile analysis, places stop losses based on both price structure and volatility, and displays adaptive support/resistance zones derived from ATR. In addition, it tracks and presents historical signal performance and serves as an educational resource for understanding statistical approaches to trading. For accurate results, it requires standard OHLC chart data.

What This Indicator Is Not:

This indicator is not a prediction system or “fortune-telling” tool, nor is it a guaranteed profit generator or a “holy grail” trading system. It does not provide investment advice or financial recommendations, and it is not a substitute for proper education and solid risk management. It may not be suitable for every trader, market, chart type, or market condition, and it is not a replacement for human judgment and decision-making. It also cannot eliminate the possibility of losses, drawdowns, or periods of underperformance, and it is not designed for or tested on non-standard chart types—so results may differ when used outside standard charts.

Who This Indicator Is Designed For

May Be Suitable For:

This indicator may be suitable for traders who prefer systematic, rules-based approaches and want to incorporate statistical analysis into their trading, especially if they’re looking for a methodology that adapts to historical price behavior. It’s best for users who are comfortable with technical analysis concepts, can manage risk and position sizing properly, and are willing to invest time in testing and optimization. It also fits those who understand that past results don’t guarantee future performance and who use standard OHLC charts for their analysis.

May Not Be Suitable For:

This indicator may not be suitable for absolute beginners with no trading experience, or for traders looking for guaranteed profits and “get rich quick” systems. It’s also not ideal for those who are uncomfortable with technical analysis or statistical concepts, who cannot tolerate losses or drawdown periods, or who are unwilling to spend time learning, testing, and refining the methodology. Additionally, it may not fit users seeking a fully automated “set and forget” solution, traders who don’t follow proper risk management principles, or those who primarily work with non-standard chart types.

Important Limitations and Considerations

Technical Limitations:

This indicator has several technical limitations: it requires sufficient historical data for its statistical calculations to work properly, and its performance can vary significantly across different instruments and timeframes. It may perform poorly in ranging, choppy, or low-liquidity markets, and the statistical percentiles it uses are derived from past data that may not reflect future behavior. Depending on market conditions, signals can cluster or become sparse, and no technical system performs equally well across all regimes. Results may also differ on non-standard chart types (such as Heikin Ashi, Renko, Kagi, Point & Figure, or Range charts), and while the adaptive ranges adjust to volatility, they cannot predict regime changes.

Market Limitations:

This indicator has market-related limitations because it cannot account for fundamental events, news, or black swan scenarios, and it does not incorporate market sentiment, positioning, or order flow. Historical statistical patterns can break down during regime shifts, and as market structure evolves, past behaviors may not persist. External drivers such as geopolitical developments or policy changes are also outside its scope, and risks from gaps as well as weekend or overnight moves are not explicitly factored into its calculations.

Execution Limitations:

This indicator has execution limitations because it does not account for slippage, spread, or execution delays, and it cannot guarantee fills at the calculated levels. It also does not explicitly factor in gap risk or overnight holding risk, and it assumes there is sufficient liquidity to execute orders as intended. In addition, it cannot account for exchange outages or other technical failures, and webhook or alert delivery can fail due to connectivity problems or third-party system issues.

User Limitations:

This indicator also has user-related limitations: it requires the discipline to follow signals consistently rather than overriding them emotionally, along with proper position sizing and risk management. Users need the psychological resilience to handle losing streaks and the time to monitor performance and evaluate results on an ongoing basis, especially if using alerts or automation. It also assumes sufficient capital and emotional reserves to withstand drawdowns, as well as a clear understanding of the constraints of standard OHLC charts.

Risk Warnings and Disclaimers

Please Read This Section Carefully

General Trading Risks: Trading and investing involve substantial risk of loss, and you can lose some or even all of your invested capital. Past performance does not indicate, predict, or guarantee future results, and no trading system, indicator, or methodology can eliminate risk. Markets are inherently unpredictable and uncertain, so outcomes can vary widely even when using a consistent approach.

Specific Risks Related to This Indicator: Its historical statistics and percentile calculations are inherently backward-looking, not forward-looking, and past favorable results do not ensure future favorable results. Market conditions can change, historical patterns may stop working or fail to repeat, and statistical analysis cannot predict future price movements. As a result, the indicator can generate losing signals and experience unprofitable periods, with no guarantee of any particular win rate, profit level, or overall performance. Metrics such as “Dist%” reflect historical averages and should not be interpreted as future profit guarantees, while adaptive ranges reflect historical volatility behavior not future support or resistance. Results may also differ significantly when used on non-standard chart types.

What This Indicator Does Not Guarantee: This indicator does not guarantee profitable trades or positive returns, any specific win percentage, success rate, or profit distance, or protection from losses and drawdowns. It also cannot guarantee that historical statistics will persist into the future, that it will be suitable for your specific financial situation, or that it will match your risk tolerance or trading goals. In addition, it does not guarantee reliable operation when used with automated trading systems, nor does it guarantee consistent results across different chart types.

Regulatory Disclaimer:

This indicator is a technical analysis tool for educational and informational purposes only. It does not constitute: Investment advice or recommendations, Financial planning or wealth management services, A solicitation to buy or sell any securities or instruments, A guarantee or warranty of any kind regarding performance, Professional advice tailored to your specific situation

Legal Liability:

By using this indicator, users acknowledge and agree that they are solely responsible for all trading decisions and outcomes, and that the author and indicator provider assume no liability for any losses or damages. Users confirm that they have read and understood all stated risks and disclaimers, agree not to hold the author or provider responsible for any results, and recognize that trading can result in the total loss of capital. They also understand the limitations related to chart types and the indicator’s calculation methods, which may affect how results are produced and interpreted.

Geographic Restrictions:

This indicator may not be suitable or legal in all jurisdictions. It is your responsibility to ensure compliance with local laws and regulations regarding trading and financial markets.

Final Statement

This indicator represents a systematic approach to technical analysis that combines momentum oscillation with statistical analysis of historical price behavior and adaptive volatility-based ranges. It is designed to provide a structured framework for visualizing historical market conditions and statistical behavior under the selected settings.

Access and Support Information

This is an invite-only indicator. For access requests, detailed documentation, setup guides, and ongoing support, please refer to the author's signature field displayed below this publication.

Thank you for taking the time to read this complete description. Understanding the methodology, limitations, and proper usage is essential for anyone considering using this indicator.

Trade safely and responsibly.

SN Trader📌 SN Trader – ATR Trailing Stop with EMA Confirmation (Scalping Strategy)

SN Trader is a precision-built ATR-based trailing stop strategy enhanced with EMA 9 & EMA 26 trend confirmation, designed for high-probability intraday and scalping trades, especially effective on XAUUSD (Gold) and other volatile instruments.

This script is a strategy (not just an indicator), meaning it supports backtesting, performance analysis, alerts, and automated trading via webhooks.

🔍 Core Concept

The strategy combines three powerful components:

ATR Trailing Stop (UT Bot logic)

Dynamically adapts to volatility

Acts as both trend filter and dynamic support/resistance

EMA 9 & EMA 26 Trend Confirmation

Filters out low-quality signals

Ensures trades align with short-term momentum

Crossover-Based Entry & Exit Logic

Prevents over-trading

Keeps entries clean and disciplined

This fusion makes SN Trader suitable for manual traders, systematic traders, and algo traders.

📈 Trading Logic (How It Works)

✅ BUY (Long Entry)

A BUY trade is triggered only when:

Price crosses above the ATR trailing stop (UT Buy signal)

EMA 9 crosses above EMA 26

Price is trading above the ATR trailing stop

❌ SELL (Short Entry)

A SELL trade is triggered only when:

Price crosses below the ATR trailing stop (UT Sell signal)

EMA 9 crosses below EMA 26

Price is trading below the ATR trailing stop

🔁 Exit Rules

Long trades close automatically when a Sell signal appears

Short trades close automatically when a Buy signal appears

No repainting logic is used

⚙️ Inputs & Customization

ATR Settings

Key Value – Controls signal sensitivity

Lower value = more trades (aggressive)

Higher value = fewer trades (conservative)

ATR Period – Volatility calculation window

Candle Source

Option to calculate signals using:

Regular candles

Heikin Ashi candles (for smoother trends)

EMA Settings

Default:

EMA Fast: 9

EMA Slow: 26

Can be adjusted to suit different markets or timeframes

🕒 Recommended Usage

Parameter Recommendation

Timeframe 5-Minute (Scalping)

Markets XAUUSD, Indices, Crypto, Forex

Sessions London & New York

Market Type Trending / Volatile

⚠️ Avoid ranging or extremely low-volatility conditions for best results.

📊 Visual Elements

EMA 9 – Green line

EMA 26 – Red line

ATR Trailing Stop – Blue line

BUY / SELL labels on chart

Clean, minimal overlay for fast decision-making

🔔 Alerts & Automation

Because this script is a strategy, it supports:

TradingView Strategy Order Fill Alerts

Webhook alerts for:

MT4 / MT5 bridges

Crypto exchanges

Custom algo execution systems

This makes SN Trader suitable for fully automated trading workflows.

🛑 Risk Disclaimer

This strategy does not include fixed stop-loss or take-profit by default.

Users are strongly encouraged to:

Apply broker-level SL/TP

Avoid high-impact news events

Forward-test before live deployment

Trading involves risk. Past performance does not guarantee future results.

👤 Access & Distribution

This script may be shared as:

Invite-only

Protected source

Redistribution, resale, or modification without permission is prohibited.

⭐ Final Notes

SN Trader is built for traders who value:

Discipline over noise

Confirmation over impulse

Structure over randomness

Whether used for manual scalping, strategy testing, or algo execution, this script provides a robust and professional trading framework.

TREND PULL BACK BUY SELL//@version=5

indicator("Clean Signal Bot 24/7 ($250 SL)", overlay=true)

// ===== SETTINGS =====

riskDollars = 250.0

pointValue = syminfo.pointvalue

// ===== INDICATORS =====

fastEMA = ta.ema(close, 9)

slowEMA = ta.ema(close, 21)

rsi = ta.rsi(close, 14)

// ===== TREND =====

bullTrend = fastEMA > slowEMA

bearTrend = fastEMA < slowEMA

// ===== PULLBACK =====

pullbackLong = close < fastEMA and close > slowEMA

pullbackShort = close > fastEMA and close < slowEMA

// ===== CANDLE CONFIRM =====

bullCandle = close > open

bearCandle = close < open

// ===== ENTRY SIGNALS =====

buySignal = bullTrend and pullbackLong and bullCandle and rsi > 50

sellSignal = bearTrend and pullbackShort and bearCandle and rsi < 50

// ===== TRADE STATE =====

var bool inLong = false

var bool inShort = false

var float entry = na

var float stop = na

riskPoints = riskDollars / pointValue

// ===== ENTER =====

if buySignal

inLong := true

inShort := false

entry := close

stop := entry - riskPoints

if sellSignal

inShort := true

inLong := false

entry := close

stop := entry + riskPoints

// ===== EXIT =====

exitLong = inLong and (close <= stop or bearTrend)

exitShort = inShort and (close >= stop or bullTrend)

if exitLong

inLong := false

if exitShort

inShort := false

// ===== CANDLE HIGHLIGHT =====

barcolor(

buySignal ? color.lime :

sellSignal ? color.red :

exitLong or exitShort ? color.yellow :

na)

// ===== LABELS =====

if buySignal

label.new(bar_index, low, "BUY", style=label.style_label_up, color=color.lime, textcolor=color.black)

if sellSignal

label.new(bar_index, high, "SELL", style=label.style_label_down, color=color.red, textcolor=color.white)

if exitLong or exitShort

label.new(bar_index, close, "EXIT", style=label.style_label_left, color=color.yellow, textcolor=color.black)

// ===== ALERTS =====

alertcondition(buySignal, "BUY ENTRY", "BUY SIGNAL")

alertcondition(sellSignal, "SELL ENTRY", "SELL SIGNAL")

alertcondition(exitLong or exitShort, "EXIT TRADE", "EXIT SIGNAL")

Quarterlytheory Candles [Fractal Edition Pro+] by aamirlangQuarterlytheory Candles - by aamirlang

Overview

Quarterlytheory Candles is a comprehensive multi-timeframe Smart Money Concepts (SMC) indicator designed for precision trading based on quarterly theory, institutional order flow, and advanced market structure analysis. This indicator combines Higher Timeframe (HTF) candle visualization, liquidity sweeps, market structure shifts, Fair Value Gaps (FVGs), and Smart Money Tool (SMT) divergences to provide traders with institutional-level insights.

Core Features

1. HTF Candles with Quarter-Based System

Adaptive Timeframe Selection: Automatically calculates optimal Higher Timeframe based on your chart timeframe

1m chart → 23m HTF (Q1-Q4 quarters)

5m chart → 90m HTF (Q1-Q4 quarters)

15m/60m chart → 360m/6H HTF (Asia/London/NY AM/NY PM sessions)

Daily chart → Weekly/Monthly HTF

Weekly chart → Monthly/Quarterly HTF

Visual HTF Candle Display:

Shows up to 50 HTF candles with customizable offset

Bullish/Bearish body and wick coloring

Real-time candle formation with live updates

Quarter labels (Q1, Q2, Q3, Q4) or session names (Asia, London, NY AM, NY PM)

Countdown timer showing time remaining in current HTF period

HTF Open Line: Displays the opening price of each HTF candle with customizable style

HTF Fair Value Gaps: Identifies imbalances (BISI/SIBI) on HTF candles

2. C2 Setup Detection

The cornerstone of this indicator - identifies high-probability reversal setups:

C2 Buy Signal: Occurs when HTF candle sweeps previous HTF low and closes back above it

C2 Sell Signal: Occurs when HTF candle sweeps previous HTF high and closes back below it

C2 Confirmation System:

CISD Pattern (Change In State of Delivery): Validates sweep with price reclaiming CISD level

Multi-Period Validation: Confirms setups within 2 HTF periods

C3 Box: Shows HTF open to previous HTF EQ (50% level)

C4 Setup: Secondary setup when C3 EQ is favorable relative to HTF open

Standard Deviation Levels: Automatically calculates extension targets (-1, -2, -2.5, -4, -4.5)

Visual Elements:

C2/C4 labels with transparent backgrounds

T-Spot boxes highlighting setup zones (bullish=green, bearish=red)

CISD confirmation lines

Setup invalidation tracking (XC2/XC4 labels when stop hit)

3. Current Range Tool (CRT)

Displays three critical levels from the most recently closed HTF candle:

HTF High (red dotted line)

HTF EQ/Midpoint (gray dotted line)

HTF Low (green dotted line)

These levels serve as key support/resistance and targets for current HTF period.

4. Market Structure Shifts (MSS)

Automatically detects bullish and bearish market structure breaks

Uses fractal-based swing detection (customizable period: 1-15)

Color-coded MSS lines (blue=bullish, red=bearish)

Labels mark precise MSS points

5. Fair Value Gaps (FVG)

Bullish FVGs (BISI - Buy Side Imbalance Sell Side Inefficiency): Blue zones

Bearish FVGs (SIBI - Sell Side Imbalance Buy Side Inefficiency): Red zones

Mitigation Tracking: Changes to gray when price taps the zone

Automatically manages up to 50 FVGs (configurable)

6. Confirmed HTF Swing Levels

Draws horizontal lines at confirmed swing highs/lows

Confirmation Logic: HTF candle sweeps a level AND next candle closes with rejection

Lines extend for customizable overshoot bars

Useful for identifying swept liquidity levels

7. LTF Sweep Detection

Identifies when HTF candles sweep previous HTF candle highs/lows

Draws sweep lines on main chart at swept levels

Helps visualize liquidity grabs in real-time

8. Trading Sessions & Killzones -

Highlights key institutional trading sessions:

Asia Session (18:00-00:00 NY time) - Gray

London Session (00:00-06:00 NY time) - Red

NY AM Session (06:00-12:00 NY time) - Green

NY PM Session (12:00-18:00 NY time) - Blue

Session Features:

Customizable box colors and transparency

Session high/low pivot lines

Pivot labels with optional price display

Session open lines ("True Day/Asia/London/NY Open")

Days of week labels (MON, TUE, WED, etc.)

Daily/Weekly/Monthly open lines and high/low pivots

9. Smart Money Tool (SMT) Divergences

Compares your chart with two other symbols to identify divergences:

Symbol 1 (default: TVC:DXY - US Dollar Index)

Symbol 2 (default: OANDA:GBPUSD)

10. Information Tables

Two customizable watermark tables:

Info Table: Shows ticker, LTF, HTF, countdown timer, and bias

Personal Table: Customizable inspirational message

How to Use This Indicator

Getting Started

Add to Chart: Apply indicator to your preferred timeframe (works best on 1m, 5m, 15m, 60m, Daily)

Review HTF Candles: Check the HTF candles displayed on the right side with quarter/session labels

Monitor CRT Levels: Watch the dotted High/EQ/Low lines from previous closed HTF candle

Wait for C2 Setup: Look for C2 labels appearing after HTF sweep + CISD confirmation

Trading the C2 Setup

For Long Positions (C2 Buy):

Wait for HTF candle to sweep previous HTF low (price goes below previous HTF low)

HTF candle closes back above the swept low (rejection)

CISD confirmation: Price reclaims the CISD level (blue line)

C2 label appears at the swept low

T-Spot (green box) shows optimal entry zone between HTF open and previous HTF EQ

Standard Deviation levels provide targets (-1, -2, -2.5, -4, -4.5 from CISD swing)

Stop Loss: Above C2 label level (swept low)

Invalidation: If stop hit, label changes to XC2 in red

For Short Positions (C2 Sell):

Wait for HTF candle to sweep previous HTF high (price goes above previous HTF high)

HTF candle closes back below the swept high (rejection)

CISD confirmation: Price breaks below the CISD level (blue line)

C2 label appears at the swept high

T-Spot (red box) shows optimal entry zone between HTF open and previous HTF EQ

Standard Deviation levels provide targets (-1, -2, -2.5, -4, -4.5 from CISD swing)

Stop Loss: Below C2 label level (swept high)

Invalidation: If stop hit, label changes to XC2 in red

Advanced Techniques

Using Bias Filter:

Auto: Allows both long and short setups

Bullish: Only shows long setups (filters out shorts)

Bearish: Only shows short setups (filters out longs)

Combining with Sessions:

Trade C2 setups that occur during high-volume sessions (London/NY AM)

Use session highs/lows as additional confluence

Avoid setups during low-volume periods (late NY PM/early Asia)

FVG Confluence:

Look for C2 setups that align with unfilled FVGs

Target FVGs as potential reversal zones

Use mitigated FVGs as trailing stop areas

MSS Confirmation:

Stronger setups occur after MSS in the C2 direction

Wait for bullish MSS before taking C2 long setups

Wait for bearish MSS before taking C2 short setups

SMT Divergence:

Use SMT divergences as additional confirmation

If DXY shows divergence at your C2 level = higher probability setup

Helps filter false setups and identify institutional manipulation

Risk Management

Maximum 2 HTF periods: C2 setups invalidate if stop not hit within 2 HTF candles

C4 Secondary Setup: If C3 EQ is favorable, you may get a C4 continuation setup

Std Dev Targets: Scale out at -1, -2, -2.5 levels; let runner go to -4/-4.5

Monitor CRT Levels: Previous HTF high/low often act as magnets for price

⚙️ Customization Options

HTF Candles Settings

Toggle HTF Candles display on/off

Fractal mode (uses fractal-based HTF calculation)

Number of candles to display (1-50)

Offset positioning

HTF labels with custom size and color

Body, border, and wick colors for bull/bear candles

FVG zones on HTF candles

HTF Open line style, color, width

Watermark tables (position, text customization)

General Settings

T-Spot box toggle and colors

Bias filter (Auto/Bullish/Bearish)

Market Structure markers (HH/HL/LH/LL)

Vertical lines for HTF candle open/close

CRT lines (High/Low/EQ) with color and width customization

MSS detection toggle with bull/bear colors

Fractal period (1-15)

FVG detection with bull/bear colors, mitigated color

Maximum FVGs to track (1-50)

StdDs toggle with custom levels input

Sessions and Pivots Settings

Timeframe limit (prevents display on higher TFs)

Toggle each session individually (Asia/London/NY AM/NY PM/Extra)

Custom session times and colors

Box transparency control

Session labels toggle

Session high/low pivot lines

Pivot label price display

Alert on broken pivots

D/W/M open lines

D/W/M high/low lines

Days of week labels

True session opens (custom session times for precise opens)

Line styles and widths

SMT Settings

Symbol 1 and Symbol 2 selection

Invert symbol options (for inverse correlations)

Historical data toggle

Alerts

C2 Setup Alerts (long and short)

Sweep Alerts (optional)

MSS Alerts (optional)

FVG Alerts (optional)

Broken Pivot Alerts (optional)

Label System

C2: Confirmed setup label

C4: Secondary setup label

XC2: Invalidated C2 (red if hit on HTF 1, orange if HTF 2)

XC4: Invalidated C4 (red)

MSS: Market structure shift

Q1, Q2, Q3, Q4: Quarter labels for sub-session HTF

Asia, London, NY AM, NY PM: Session labels for 6H HTF

MON, TUE, WED, etc.: Day of week labels

HH, HL, LH, LL: Market structure markers

Std Dev Labels: -1, -2, -2.5, -4, -4.5

Best Practices

For Day Traders (1m, 5m charts)

Use fractal mode for cleaner HTF calculation

Focus on London and NY AM sessions for volume

Trade C2 setups aligned with session bias

Use -1 and -2 Std Dev levels as initial targets

Monitor SMT divergences for confirmation

For Swing Traders (15m, 60m, Daily charts)

Use standard HTF mode for accurate session mapping

Focus on C2 setups at major session opens (Daily, Weekly)

Target -4 and -4.5 Std Dev levels

Use Weekly/Monthly pivots for additional confluence

Allow 2 full HTF periods for setup to play out

For All Traders

Journal your C2 setups: Track success rate, best sessions, best Std Dev targets

Use bias filter strategically: If trending strongly, filter counter-trend setups

Combine with price action: C2 is a framework, not a mechanical system

Respect CRT levels: Previous HTF high/EQ/low are magnets

Don't force trades: Quality > quantity with C2 setups

Backtest on your instrument: Every market has nuances

🔔 Alert Configuration

This indicator supports TradingView alerts:

Click "Create Alert" on TradingView

Select "Quarterlytheory Candles" as condition

Choose alert type:

"Long Trade Alert!" - Fires when C2 Buy confirmed

"Short Trade Alert!" - Fires when C2 Sell confirmed

Set "Once Per Bar Close" frequency

Customize alert actions (notification, email, webhook, sound)

Pro Tip: Use webhook alerts to connect to Discord, Telegram, or trading bots for automated notifications.

⚠️ DISCLAIMER

FOR EDUCATIONAL PURPOSES ONLY

This indicator is provided as an educational tool for learning about Smart Money Concepts, quarterly theory, and institutional order flow analysis. It is NOT financial advice.

Important Notices:

Trading involves substantial risk of loss and is not suitable for everyone

Past performance does not guarantee future results

No indicator can predict market movements with certainty

The developer (aamirlang) is not a registered financial advisor

Always use proper risk management and position sizing

Never risk more than you can afford to lose

This indicator does not guarantee profitable trades

Users are solely responsible for their trading decisions

Test thoroughly on paper/demo accounts before risking real capital

Market conditions change; what works today may not work tomorrow

Technical Disclaimer:

This indicator may repaint on unconfirmed bars (use confirmed signals only)

Higher timeframe calculations may vary slightly from standard TradingView HTF functions

Performance may vary across different instruments and market conditions

Ensure adequate chart history is loaded for accurate calculations

By using this indicator, you acknowledge:

You understand the risks of trading

You have tested this indicator thoroughly

You take full responsibility for all trading decisions

You will not hold the developer liable for any losses

🙏 CREDITS & ACKNOWLEDGMENTS

This indicator builds upon the excellent work of several open-source contributors and combines concepts from various trading methodologies. Full credit and gratitude to:

Core Concepts & Methodology

@traderdaye: I have used the Quarterly theory concepts and True opens of Daye.

@TTrades_edu: The foundational C2/C3/C4 setup structure and CISD pattern detection methodology that forms the core of this indicator

ICT (Inner Circle Trader): Smart Money Concepts framework, killzones, liquidity concepts, and FVG theory

Open Source Code Components

1. Smart Money Tool (SMT) Divergence Detection

Original Author: Algoryze

Component: SMT divergence calculation and visualization system

Contribution: Multi-symbol comparison logic, fractal-based swing detection for divergences

License: Open source (TradingView Public Library)

2. Killzones and Pivot System

Original Author: Tradeforopp

Component: Trading session boxes, pivot high/low detection, D/W/M separators and opens

Contribution: Session time management, pivot line extensions, timezone handling

License: Open source (TradingView Public Library)

Modifications & Enhancements by aamirlang

Integrated all components into unified quarterly theory framework

Developed adaptive HTF calculation system with quarter-based labeling

Created C2/C3/C4 setup detection logic with CISD confirmation

Implemented Standard Deviation target system

Built HTF candle visualization engine with custom quarter formatting

Added Current Range Tool (CRT) for previous HTF levels

Developed setup invalidation tracking system

Created custom watermark and information tables

Implemented confirmed swing detection and LTF sweep visualization

Added comprehensive alert system

Optimized performance and visual clarity

Enhanced customization options throughout

Community & Inspiration

TradingView Community: For feedback, testing, and continuous improvement suggestions

SMC Trading Community: For sharing knowledge on institutional order flow

Pine Script™ Documentation: For technical reference and best practices

Special Thanks

To all traders who have shared their experiences with quarterly theory

To the open-source trading community for fostering collaboration

To early testers who provided valuable feedback

📝 Version Information

Current Version: Fractal Edition Pro+

Indicator Name: Quarterlytheory Candles by aamirlang

Pine Script™ Version: 5

Last Updated: 2026

Compatibility: TradingView Free, Pro, Pro+, Premium plans

📧 Contact & Support

For questions, suggestions, or to report issues:

Before reaching out:

Read this description thoroughly

Check indicator settings and tooltips

Test on demo account first

Review TradingView's Pine Script™ documentation

🔄 Future Development

Potential enhancements under consideration:

Multi-timeframe dashboard view

Custom alert message templates

Volume profile integration

Enhanced session statistics table

Liquidity heatmap visualization

Trade journal integration

C2 Setup analysis and statistics

Auto Bias detection and implementation

Auto SSMT and SMT

PSP Detection

Feature requests are welcome via TradingView comments section.

📜 License

This indicator combines original code by aamirlang with modified open-source components from Algoryze (SMT) and Tradeforopp (Killzones/Pivots).

This indicator is shared for educational purposes. Redistribution or resale of this indicator or its components without proper attribution is prohibited.

SPY Quant ML + Session Filter Strategy [CocoChoco]S&P 500 Quant: Machine Learning & Mean Reversion (Session-Filtered)

Overview

This is a professional-grade quantitative strategy designed specifically for the S&P 500. It combines classical statistical mean reversion (Z-Score) with a modern Machine Learning filter and rigorous institutional-grade risk management.

The strategy is optimized for traders who prioritize high win rates and capital preservation, specifically avoiding the "gap risk" associated with holding positions overnight.

Core Methodology

1. Statistical Entry (The Z-Score Engine)

The strategy identifies "oversold" conditions in a bullish context. It calculates the Z-Score of the price relative to its 20-period Mean (SMA). By default, it looks for a -1.2 Standard Deviation extension, signaling a high-probability "dip" ripe for a snap-back to the mean.

2. Trend & ML Filters

To avoid "catching a falling knife," the strategy uses two layers of confirmation:

Trend Filter: Only takes Long positions when the price is above the 200-period SMA, ensuring we only buy dips in a confirmed uptrend.

ML Correlation Filter: A Machine Learning-inspired module that analyzes the correlation between RSI and Volatility (ATR). It only permits entries when market internal dynamics suggest a reversal is technically "healthy."

3. Institutional Risk Management

This script is built for "safety-first" automation:

Hard Stop Loss: Fixed at 1.5% to protect against sudden market shocks.

Active Trailing: A dual-trigger trailing stop. It activates once the price touches the 20 SMA (The Mean) OR once a trade reaches a 0.50% profit threshold. This ensures near-winners are protected and large runners are captured.

Intraday Circuit Breaker: Includes a Max Daily Drawdown (2%) limit. If hit, the script automatically closes losing positions and halts trading for the day, while allowing winning positions to continue.

Key Features

Session-Specific: Tailored for the US Trading Session (UTC/NY times).

Zero Overnight Risk: Automatically flattens all positions before the market close (16:00 NY Time).

Holiday Intelligence: Hard-coded logic for US Market Holidays and Early Closes (2026–2028), ensuring the bot doesn't get stuck in illiquid holiday markets.

Hourly Entry Cap: Limits entries to one per hour to prevent over-concentration during a single price leg.

How to Use

Timeframe: I suggest you use it on the 5-minute or 1-hour timeframe for optimal results.

Instrument: Designed for the S&P 500, but highly effective on SPY, IVV, and ES (Futures).

Pyramiding: Designed to handle up to 3 concurrent positions, allowing the strategy to scale into a move as the Z-Score deepens.

Automation Ready

This script is fully compatible with webhook-based automation tools. All signals (Entry, SL, Trail, Market Close, and Daily Limit) are clearly labeled in the Alert comments for seamless execution. I haven't tasted it though. This is not financial advice. Please perform your own tests and manage your risk.

Disclaimer

Past performance does not guarantee future results. This script is a tool for quantitative analysis and should be used as part of a broader diversified trading plan.

AngleAura UTAngleAura UT is an advanced trading indicator built on top of the classic UT Bot concept, enhanced with modern risk‑management logic, next‑candle execution, and a clean visual interface.

The script uses a modified algorithm based on:

- ATR‑adjusted trailing levels

- EMA crossover logic

- Dynamic trend switching

This helps identify trend reversals with minimal noise.

BTC - Sentiment (Posts weighted) LSMABTC - Sentiment (Posts Weighted) LSMA | RM

Concept

In the current 2026 market regime, Bitcoin has transitioned into a mature institutional asset. However, retail "Social Liquidity" remains the primary driver of local volatility and blow-off tops. This script serves as a deterministic proxy for crowd conviction, utilizing the LUNARCRUSH:BTC_SENTIMENT feed to identify when social hype has decoupled from fundamental value.

Data Source: LunarCrush Integration

This model utilizes the native LunarCrush data prefix. Unlike simple "mention counts," the BTC_SENTIMENT metric is a percentage-based value (0-100%) representing the "Sentiment of positive posts weighted by interactions."

• Interactions vs. Volume: By weighting sentiment by interactions (likes, shares, comments), the data filters out bot-driven "spam" and focuses on what real participants are actually engaging with.

• Meaning of the Value: 100% indicates that every single interaction-weighted post is positive; 0% indicates total negativity. Historically, BTC sentiment rarely drops below 60% or stays above 90% for long, creating a predictable mean-reverting corridor.

Technical Architecture

• The LSMA Denoising Engine Raw social data is inherently "jittery." To extract a tradable signal, we apply a Least Squares Moving Average (LSMA) with a 28-day lookback.

• Mathematical Advantage: Unlike a Simple Moving Average (SMA), the LSMA calculates a linear regression line for each period to find the "best fit." This allows the indicator to track the velocity of sentiment shifts with significantly less lag, which is critical for identifying "Social Exhaustion" before a price reversal occurs.

• The Social Heat Index (SHI) Calculation: To align this data with the broader Rob Maths ecosystem, we normalize the LSMA output into a standardized 0–10 score using a Linear Feature Scaling (Min-Max) formula: SHI = ((Current LSMA - 65) / 25) * 10 ; This formula treats 65% as the "Floor" (Apathy) and 90% as the "Ceiling" (Hysteria). This 0–10 scale allows for immediate comparison against other institutional risk metrics.

Regime Audits & Usage

• Accumulation (Blue Zone / <72.5%): Social Despair. Retail interest is at a mathematical minimum. Historically, these periods of "Social Apathy" coincide with major local bottoms as institutional "Smart Money" absorbs the lack of retail demand.

• Neutral Zone (Grey): Sustainable growth. Sentiment is within the normal distribution.

• Distribution (Red Zone / >82.5%): Overheated. The crowd is in a state of maximum FOMO. When the SHI exceeds 8.5/10, the risk of a "Liquidity Flush" increases significantly.

Visual Scaling

To ensure the curve is readable, the indicator pane is hard-locked to a 65–90 scale. This prevents the "flat line" effect often seen in 0-100 oscillators and highlights the subtle divergences that occur at cycle peaks.

Disclaimer