Vega Convexity Engine [PRO]ENGINEERED ASYMMETRY.

This is the flagship Stage 2 Specialist Model of the Vega Crypto Strategies ecosystem.

While the free "Regime Filter" tells you when to trade (filtering out chop), the Convexity Engine tells you how to trade. It activates only when the Regime Filter confirms an Impulse, classifying the specific vector of the market move to maximize risk-adjusted returns.

PRO FEATURES

This script visualizes the output of our Hierarchical Machine Learning Engine:

🚀 Directional Classification:

It does not just say "Buy." It classifies volatility into 4 distinct probability classes:

- EXPLOSION: High-confidence, high-velocity upside (Fat-Tail).

- RALLY: Standard trend continuation.

- PULLBACK: Short-term correction opportunity.

- CRASH: High-confidence downside (Long Squeeze Detection).

🛡️ Dynamic Risk Engine (Intraday Stops):

The "+" markers on your chart represent the Vega Institutional Stop Loss . These levels dynamically adjust based on Average True Range (ATR) and Volatility Z-Scores.

Strategy: If price breaches the "+" marker, the hypothesis is invalidated. Exit immediately.

📊 Institutional HUD:

A professional heads-up display showing the current Regime, Vector, and Risk Deployment status in real-time.

THE PHILOSOPHY

"Convexity" means limited downside with unlimited upside. By combining the Regime Filter (sitting in cash during noise) with Dynamic Stops (cutting losers fast), this engine is designed to capture the "fat tails" of the crypto market distribution.

🔒 HOW TO GET ACCESS

This is an Invite-Only script. It is strictly for members of Vega Crypto Strategies .

To unlock access, please visit the link in the Author Profile below or check our signature. Once subscribed via Whop, your TradingView username will be automatically authorized instantly.

Disclaimer: This tool is for educational purposes only. Past performance is not indicative of future results. Trading cryptocurrencies involves significant risk.

Machinelearning

JINN: A Multi-Paradigm Quantitative Trading and Execution EngineI. Core Philosophy: A Substitute for Static Analysis

JINN (Joint Investment Neural and Network) represents a paradigm shift from static indicators to a living, adaptive analytical ecosystem. Traditional tools provide a fixed snapshot of the market. JINN operates on a fundamentally different premise: it treats the market as a dynamic, regime-driven system. It processes market data through a hierarchical suite of advanced, interacting models, arbitrates their outputs through a rules-based engine, and adapts its own logic in real-time.

It is designed as a complete framework for traders who think in terms of statistical edge, market regimes, probabilistic outcomes, and adaptive risk management.

II. The JINN Branded Architecture: Your Command and Control Centre

JINN’s power emerges from the synergy of its proprietary, branded architectural components. You do not simply "use" JINN; you command its engines.

1. JINN Signal Arbitration (JSA) Engine

The heart of JINN. The JSA is your configurable arbitration desk for weighing evidence from all internal models. As the Head Strategist, you define the entire arbitration philosophy:

• Priority and Weighting : Define a "chain of command". Specify which model's opinion must be considered first and assign custom weights to their outputs, directly controlling the hierarchy of your analytical flow.

• Arbitration Modes :

First Wins: For high-conviction, rapid signal deployment based on your most trusted leading model.

Highest Score: A "best evidence" approach that runs a full analysis and selects the signal with the highest weighted probabilistic backing.

Consensus: An ultra-conservative, "all-clear" mode that requires a unanimous pass from all active models, ensuring maximum confluence.

2. JINN Threshold Fusion (JTF) Engine

Static entry thresholds can be limiting in a dynamic market. The JTF engine replaces them with a robust, adaptive "breathing" channel.

• Kalman Filter Core : A noise-reducing, parametric filter that provides a smooth, responsive centre for the entry bands.

• Exponentially Weighted Quantile (EWQ) : A non-parametric, robust measure of the signal's recent distribution, resistant to outliers.

• Dynamic Fusion : The JTF engine intelligently fuses these two methodologies. In stable conditions, it can blend them; in volatile conditions, it can be configured to use the "Minimum Width" of the two, ensuring your entry criteria are always the most statistically relevant.

3. JINN Pattern Veto (JPV) with Dynamic Time Warping

The definitive filter for behavioural edge and pattern recognition. The JPV moves beyond value-based analysis to analyse the shape of market dynamics.

• Dynamic Time Warping (DTW) : A powerful algorithm from computer science that compares the similarity of time series.

• Pattern Veto : Define a "toxic" price action template—a pattern that has historically preceded failed signals. If the JPV detects this pattern, it will veto an otherwise valid trade, providing a sophisticated layer of qualitative, shape-based filtering.

4. JINN Flow VWAP

This is not a standard VWAP. The JINN Flow VWAP is an institutionally-aware variant that analyses volume dynamics to create a "liquidity pressure" band. It helps visualise and gate trades based on the probable activity of larger market participants, offering a nuanced view of where significant flow is occurring.

III. The Advanced Model Suite: Your Pre-Built Quantitative Toolkit

JINN provides you with a turnkey suite of institutional-grade models, saving you thousands of hours of research and development.

1. Auto-Tuning Hyperparameters Engine (Online Meta-Learning)

Markets evolve. A static strategy is an incomplete strategy. JINN’s Auto-Tuning engine is a meta-learning layer inspired by the Hedge (EWA) algorithm, designed to combat alpha decay.

• Portfolio of Experts : It treats a curated set of internal strategic presets as a portfolio of "experts".

• Adaptive Weighting : It runs an online learning algorithm that continuously measures the risk-adjusted performance of each expert (using a sophisticated reward function blending Expected Value and Brier Score).

• Dynamic Adaptation : The engine dynamically allocates more influence to the expert strategy that is performing best in the current market regime, allowing JINN’s core logic to adapt without manual intervention.

2. Lorentzian Classification and PCA-Lite EigenTrend

• Lorentzian Engine : A powerful probabilistic classifier that generates a continuous probability (0-1) of market state. Its adaptive, volatility-scaled distribution is specifically designed to handle the "fat tails" and non-Gaussian nature of financial returns.

• PCA-Lite EigenTrend : A Principal Component Analysis engine. It reduces the complex, multi-dimensional data from the Technical and Order-Flow ensembles into a single, maximally descriptive "EigenTrend". This factor represents the dominant, underlying character of the market, providing a pure, decorrelated input for the Lorentzian engine and other modules.

3. Adaptive Markov Chain Model

A forward-looking, state-based model that calculates the probability of the market transitioning between Uptrend, Downtrend, and Sideways states. Our implementation is academically robust, using an EMA-based adaptive transition matrix and Laplace Smoothing to ensure stability and prevent model failure in sparse data environments.

IV. The Execution Layer: JINN Execution Latch Options

A good signal is worthless without intelligent execution. The JINN Execution Latch is a suite of micro-rules and safety mechanisms that govern the "last mile" of a trade, ensuring signals are executed only under optimal, low-risk conditions. This is your final pre-flight check.

• Execution Latch and Dynamic Cool-Down : A core safety feature that enforces a dynamic cool-down period after each trade to prevent over-trading in choppy, whipsaw markets. The latch duration intelligently adapts, using shorter periods in low-volatility and longer periods in high-volatility environments.

• Volatility-Scaled Real-Time Threshold : A sophisticated gate for real-time entries. It dynamically raises the entry threshold during sudden spikes in volatility, effectively filtering out noise and preventing entries based on erratic, unsustainable price jerks.

• Noise Debounce : In market conditions identified as "noisy" by the Shannon Entropy module, this feature requires a real-time signal to persist for an extra tick before it is considered valid. This is a simple but powerful heuristic to filter out fleeting, insignificant price flickers.

• Liquidity Pressure Confirmation : An institutional-grade check. This gate requires a minimum threshold of "Liquidity Pressure" (a measure of volume-driven momentum) to be present before validating a real-time signal, ensuring you are entering with market participation on your side.

• Time-of-Day (ToD) Weighting : A practical filter that recognises not all hours of the trading day are equal. It can be configured to automatically raise entry thresholds during historically low-volume, low-liquidity sessions (e.g., lunch hours), reducing the risk of entering trades on "fake" moves.

• Adaptive Expectancy Gate : A self-regulating feedback mechanism. This gate monitors the strategy's recent, realised performance (its Expected Value). If the rolling expectancy drops below a user-defined threshold, the system automatically tightens its entry criteria, becoming more selective until performance recovers.

• Bar-Close Quantile Confirmation : A final layer of confirmation for bar-close signals. It requires the signal's final score to be in the top percentile (e.g., 85th percentile) of all signal scores over a lookback period, ensuring only the highest conviction signals are taken.

V. The Contextual and Ensemble Frameworks

1. Multi-Factor Ensembles and Bayesian Fusion

JINN is built on the principle of diversification. Its signals are derived from two comprehensive, fully customizable ensembles:

• Technical Ensemble : A weighted combination of over a dozen technical features, from cyclical analysis (MAMA, Hilbert Transforms) and momentum (Fisher Transform) to trend efficiency (KAMA, Fractal Efficiency Ratio).

• Order-Flow Ensemble : A deep dive into market microstructure, incorporating Volume Delta, Absorption, Imbalance, and Delta Divergence to decode institutional footprints.

• Bayesian Fusion : Move beyond simple AND/OR logic. JINN’s Bayesian engine allows you to probabilistically combine evidence from trend and order-flow filters, weighing each according to its perceived reliability to derive a final posterior probability.

2. Context-Aware Framework and Entropy Engine

JINN understands that a successful strategy requires not just a good entry, but an intelligent exit and a dynamic approach to risk.

• Shannon Entropy Filter : A direct application of information theory. JINN quantifies market randomness and allows you to set a precise entropy ceiling to automatically halt trading in unpredictable, high-entropy conditions.

• Adaptive Exits and Regime Awareness : The script uses its entropy-derived regime awareness to dynamically scale your Take Profit and Trailing Stop parameters . It can be configured to automatically take smaller profits in choppy markets and let winners run in strong trends, hard-coding adaptive risk management into your system.

VI. The Dashboard: Your Mission Control

JINN features a dynamic, dual-mode dashboard that provides a comprehensive, real-time overview of the entire system's state.

Mode 1: Signal Gate Metrics Dashboard

This dashboard is your pre-flight checklist. It displays the real-time Pass/Fail/Off status of every single gating and filtering component within JINN, including:

• Core Ensembles : Technical and Order-Flow Ensemble status.

• Trend Filters : VWAP, VWMA, ADX, ATR Slope, and Linear Regression Angle gates.

• Advanced Models : Dual-Lorentzian Consensus, Markov Probability, and JPV Veto status.

• Regime and Safety : Shannon Entropy, Execution Latch, and Expectancy Gate status.

• Final Confirmation : A master "All Hard Filters" status, giving you an at-a-glance confirmation of system readiness.

Mode 2: Quantitative Metrics Dashboard

This dashboard provides a high-level, institutional-style data readout of the current market state, as seen through JINN's analytical lens. It includes over 60 key metrics for both Signal Gate and Quantitative Metrics, such as:

• Ensemble and Confidence Scores : The raw numerical output of the Technical, Order-Flow, and Lorentzian models.

• Volatility and Volume Analysis : Realised Volatility (%), Relative Volume, Volume Sigma Score, and ATR Z-Score.

• Momentum and Market Position : ADX, RSI Z-Score, VWAP Distance (%), and Distance from 252-Bar High/Low.

• Regime Metrics : The numerical value of the Shannon Entropy score and the Model Confidence score.

VII. The User as the Head Strategist

With over 178 meticulously designed user inputs, JINN is the ultimate "glass box" engine. The internal code is proprietary, but the control surface is transparent and grants you architectural-level command.

• Prototype Sophisticated Strategies : Test complex, multi-model theses at your own pace that would otherwise take weeks of coding. Want to test a strategy that uses a Lorentzian classifier driven by the EigenTrend, arbitrated by JSA in "highest score" mode, and filtered by a strict Markov trend gate? These can be configured and unified.

• Tune the Engine to Any Market : The inputs provide the control surface to optimise JINN's behaviour for specific assets and timeframes, from crypto scalping to swing trading indices.

• Build Trust Through Configuration : The granular controls allow you to align the script's behaviour precisely with your own market view, building trust in your own deployment of the tool.

JINN is a commitment. It is a tool for the serious analyst who seeks to move from discretionary trading to a systematic, quantitative, and adaptive approach. If this aligns with your philosophy, we invite you to apply for access.

Disclaimer

This script is for informational and educational purposes only. It does not constitute financial, investment, or trading advice, nor is it a recommendation to buy or sell any asset.

All trading and investment decisions are the sole responsibility of the user. It is strongly recommended to thoroughly test any strategy on a paper trading account for at least one week before risking real capital.

Trading financial markets involves a high risk of loss, and you may lose more than your initial investment. Past performance is not indicative of future results. The developer is not responsible for any losses incurred from the use of this script.

RSI Forecast Colorful [DiFlip]RSI Forecast Colorful

Introducing one of the most complete RSI indicators available — a highly customizable analytical tool that integrates advanced prediction capabilities. RSI Forecast Colorful is an evolution of the classic RSI, designed to anticipate potential future RSI movements using linear regression. Instead of simply reacting to historical data, this indicator provides a statistical projection of the RSI’s future behavior, offering a forward-looking view of market conditions.

⯁ Real-Time RSI Forecasting

For the first time, a public RSI indicator integrates linear regression (least squares method) to forecast the RSI’s future behavior. This innovative approach allows traders to anticipate market movements based on historical trends. By applying Linear Regression to the RSI, the indicator displays a projected trendline n periods ahead, helping traders make more informed buy or sell decisions.

⯁ Highly Customizable

The indicator is fully adaptable to any trading style. Dozens of parameters can be optimized to match your system. All 28 long and short entry conditions are selectable and configurable, allowing the construction of quantitative, statistical, and automated trading models. Full control over signals ensures precise alignment with your strategy.

⯁ Innovative and Science-Based

This is the first public RSI indicator to apply least-squares predictive modeling to RSI calculations. Technically, it incorporates machine-learning logic into a classic indicator. Using Linear Regression embeds strong statistical foundations into RSI forecasting, making this tool especially valuable for traders seeking quantitative and analytical advantages.

⯁ Scientific Foundation: Linear Regression

Linear regression is a fundamental statistical method that models the relationship between a dependent variable y and one or more independent variables x. The general formula for simple linear regression is:

y = β₀ + β₁x + ε

where:

y = predicted variable (e.g., future RSI value)

x = explanatory variable (e.g., bar index or time)

β₀ = intercept (value of y when x = 0)

β₁ = slope (rate of change of y relative to x)

ε = random error term

The goal is to estimate β₀ and β₁ by minimizing the sum of squared errors. This is achieved using the least squares method, ensuring the best linear fit to historical data. Once the coefficients are calculated, the model extends the regression line forward, generating the RSI projection based on recent trends.

⯁ Least Squares Estimation

To minimize the error between predicted and observed values, we use the formulas:

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Σ denotes summation; x̄ and ȳ are the means of x and y; and i ranges from 1 to n (number of observations). These equations produce the best linear unbiased estimator under the Gauss–Markov assumptions — constant variance (homoscedasticity) and a linear relationship between variables.

⯁ Linear Regression in Machine Learning

Linear regression is a foundational component of supervised learning. Its simplicity and precision in numerical prediction make it essential in AI, predictive algorithms, and time-series forecasting. Applying regression to RSI is akin to embedding artificial intelligence inside a classic indicator, adding a new analytical dimension.

⯁ Visual Interpretation

Imagine a time series of RSI values like this:

Time →

RSI →

The regression line smooths these historical values and projects itself n periods forward, creating a predictive trajectory. This projected RSI line can cross the actual RSI, generating sophisticated entry and exit signals. In summary, the RSI Forecast Colorful indicator provides both the current RSI and the forecasted RSI, allowing comparison between past and future trend behavior.

⯁ Summary of Scientific Concepts Used

Linear Regression: Models relationships between variables using a straight line.

Least Squares: Minimizes squared prediction errors for optimal fit.

Time-Series Forecasting: Predicts future values from historical patterns.

Supervised Learning: Predictive modeling based on known output values.

Statistical Smoothing: Reduces noise to highlight underlying trends.

⯁ Why This Indicator Is Revolutionary

Scientifically grounded: Built on statistical and mathematical theory.

First of its kind: The first public RSI with least-squares predictive modeling.

Intelligent: Incorporates machine-learning logic into RSI interpretation.

Forward-looking: Generates predictive, not just reactive, signals.

Customizable: Exceptionally flexible for any strategic framework.

⯁ Conclusion

By combining RSI and linear regression, the RSI Forecast Colorful allows traders to predict market momentum rather than simply follow it. It's not just another indicator: it's a scientific advancement in technical analysis technology. Offering 28 configurable entry conditions and advanced signals, this open-source indicator paves the way for innovative quantitative systems.

⯁ Example of simple linear regression with one independent variable

This example demonstrates how a basic linear regression works when there is only one independent variable influencing the dependent variable. This type of model is used to identify a direct relationship between two variables.

⯁ In linear regression, observations (red) are considered the result of random deviations (green) from an underlying relationship (blue) between a dependent variable (y) and an independent variable (x)

This concept illustrates that sampled data points rarely align perfectly with the true trend line. Instead, each observed point represents the combination of the true underlying relationship and a random error component.

⯁ Visualizing heteroscedasticity in a scatterplot with 100 random fitted values using Matlab

Heteroscedasticity occurs when the variance of the errors is not constant across the range of fitted values. This visualization highlights how the spread of data can change unpredictably, which is an important factor in evaluating the validity of regression models.

⯁ The datasets in Anscombe’s quartet were designed to have nearly the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but look very different when plotted

This classic example shows that summary statistics alone can be misleading. Even with identical numerical metrics, the datasets display completely different patterns, emphasizing the importance of visual inspection when interpreting a model.

⯁ Result of fitting a set of data points with a quadratic function

This example illustrates how a second-degree polynomial model can better fit certain datasets that do not follow a linear trend. The resulting curve reflects the true shape of the data more accurately than a straight line.

⯁ What Is RSI?

The RSI (Relative Strength Index) is a technical indicator developed by J. Welles Wilder. It measures the velocity and magnitude of recent price movements to identify overbought and oversold conditions. The RSI ranges from 0 to 100 and is commonly used to identify potential reversals and evaluate trend strength.

⯁ How RSI Works

RSI is calculated from average gains and losses over a set period (commonly 14 bars) and plotted on a 0–100 scale. It consists of three key zones:

Overbought: RSI above 70 may signal an overbought market.

Oversold: RSI below 30 may signal an oversold market.

Neutral Zone: RSI between 30 and 70, indicating no extreme condition.

These zones help identify potential price reversals and confirm trend strength.

⯁ Entry Conditions

All conditions below are fully customizable and allow detailed control over entry signal creation.

📈 BUY

🧲 Signal Validity: Signal remains valid for X bars.

🧲 Signal Logic: Configurable using AND or OR.

🧲 RSI > Upper

🧲 RSI < Upper

🧲 RSI > Lower

🧲 RSI < Lower

🧲 RSI > Middle

🧲 RSI < Middle

🧲 RSI > MA

🧲 RSI < MA

🧲 MA > Upper

🧲 MA < Upper

🧲 MA > Lower

🧲 MA < Lower

🧲 RSI (Crossover) Upper

🧲 RSI (Crossunder) Upper

🧲 RSI (Crossover) Lower

🧲 RSI (Crossunder) Lower

🧲 RSI (Crossover) Middle

🧲 RSI (Crossunder) Middle

🧲 RSI (Crossover) MA

🧲 RSI (Crossunder) MA

🧲 MA (Crossover)Upper

🧲 MA (Crossunder)Upper

🧲 MA (Crossover) Lower

🧲 MA (Crossunder) Lower

🧲 RSI Bullish Divergence

🧲 RSI Bearish Divergence

🔮 RSI (Crossover) Forecast MA

🔮 RSI (Crossunder) Forecast MA

📉 SELL

🧲 Signal Validity: Signal remains valid for X bars.

🧲 Signal Logic: Configurable using AND or OR.

🧲 RSI > Upper

🧲 RSI < Upper

🧲 RSI > Lower

🧲 RSI < Lower

🧲 RSI > Middle

🧲 RSI < Middle

🧲 RSI > MA

🧲 RSI < MA

🧲 MA > Upper

🧲 MA < Upper

🧲 MA > Lower

🧲 MA < Lower

🧲 RSI (Crossover) Upper

🧲 RSI (Crossunder) Upper

🧲 RSI (Crossover) Lower

🧲 RSI (Crossunder) Lower

🧲 RSI (Crossover) Middle

🧲 RSI (Crossunder) Middle

🧲 RSI (Crossover) MA

🧲 RSI (Crossunder) MA

🧲 MA (Crossover)Upper

🧲 MA (Crossunder)Upper

🧲 MA (Crossover) Lower

🧲 MA (Crossunder) Lower

🧲 RSI Bullish Divergence

🧲 RSI Bearish Divergence

🔮 RSI (Crossover) Forecast MA

🔮 RSI (Crossunder) Forecast MA

🤖 Automation

All BUY and SELL conditions can be automated using TradingView alerts. Every configurable condition can trigger alerts suitable for fully automated or semi-automated strategies.

⯁ Unique Features

Linear Regression Forecast

Signal Validity: Keep signals active for X bars

Signal Logic: AND/OR configuration

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Chart Labels: BUY/SELL markers above price

Automation & Alerts: BUY/SELL

Background Colors: bgcolor

Fill Colors: fill

Linear Regression Forecast

Signal Validity: Keep signals active for X bars

Signal Logic: AND/OR configuration

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Chart Labels: BUY/SELL markers above price

Automation & Alerts: BUY/SELL

Background Colors: bgcolor

Fill Colors: fill

SNP420/INDI/support_resist_future_levelFunctionality – short description

The indicator automatically detects the latest pivot highs/lows and builds the current resistance and support levels from them. New levels start as candidate levels (dotted lines).

Using an ATR-based tolerance, it counts how many times price precisely tests and rejects the level (touch + reversal).

Once the minimum number of touches is reached, the level is marked as validated (solid line). The indicator also detects breakouts of S/R, colors breakout candles, projects a target level after the breakout, and highlights retests of the broken levels with boxes.

autor: SNP_420

project: FNXS

ps: Piece a love

Lorentzian Length Adaptive Moving Average [LLAMA] Adaptation of "Machine Learning: Lorentzian Classification" by

Gradient color by base on work by

LLAMA: A regime-aware adaptive moving average that bends with the market.

Start with a problem traders know:

Traditional moving averages are either too slow (EMA200) or too fast (EMA9)

Adaptive MAs exist, but they often hug price too tightly or smooth too much, failing to balance bias and tactics

LLAMA uses a Lorentzian distance function to adapt its length dynamically. Instead of a fixed smoothing window, it stretches or contracts depending on market conditions. This distortion reduces lag while still providing a clear bias line.

The indicator looks back at recent bars and measures how similar they are using a Lorentzian distance (a log‑scaled absolute difference). It keeps track of the “nearest neighbors” — bars that most resemble the current regime. Each neighbor carries a label (long, short, neutral) based on simple price comparisons. By averaging these labels, LLAMA predicts whether the market is leaning bullish or bearish. That prediction is then mapped into a dynamic length between and .

Bullish bias -> length stretches toward max (smoother, more stable).

Bearish bias -> length contracts toward min (snappier, more reactive).

During breakouts, LLAMA tightens and comes into contact with bars, giving actionable signals. During chop, it stretches to avoid false triggers. It covers both ends of the spectrum (bias and tactics) in one line, something static MA's can't do.

Think of LLAMA as a lens that bends with the market:

Wide lens (max length) for big picture bias.

Narrow lens (min length) for tactical precision.

The "Lorentzian Loop" is the math that decides when to widen or narrow.

Screener (SSA) [AlgoAlpha]🟠 OVERVIEW

This script is a multi-symbol screener that serves as a dashboard companion to the "Smart Signals Assistant (SSA)" indicator. Its purpose is to monitor the entire suite of SSA components—from the core signals to all confluence tools—across a customizable watchlist of up to 18 assets. By displaying the real-time status of each indicator in a single table, it allows traders to get a bird's-eye view of the market, quickly identify assets with strong trend confluence, and filter for high-probability setups without needing to switch charts.

The screener is designed to mirror the modularity of the main SSA indicator, allowing you to enable or disable components in the table to match your preferred trading dashboard.

🟠 CONCEPTS

The screener is built directly on the analytical framework of the Smart Signals Assistant, applying its complex, proprietary algorithms to each symbol in your watchlist and summarizing the results. The combination of these different analytical concepts is what gives the screener its utility, as it helps traders find opportunities where multiple, distinct strategies align.

Each column in the table represents a core trading concept:

Smart Signals: This is the primary signal engine, designed to identify potential entry points. It operates in different modes to capture both long-term swings and faster scalping opportunities.

Fair Value Trail (FVT): This component provides a dynamic, volatility-adjusted baseline for the trend. It acts as a form of dynamic support or resistance, helping to confirm the validity of a trend shown by the Smart Signals.

Trend Spine: This tool is designed to identify the underlying "backbone" of the market's trend. It filters out short-term price noise to provide a more stable, clear indication of the dominant market direction.

Trend Bias: This measures the strength and conviction behind a trend. It helps distinguish between a strong, accelerating move and a weak, decelerating one, adding a layer of momentum analysis.

Firmament Clouds: These are volatility-based bands that create dynamic overbought and oversold zones. They help identify when price is potentially overextended and due for a pullback or consolidation.

Trend-Range Classifier (TRC): A machine-learning model that analyzes market characteristics to classify the current environment as either "Trending" or "Ranging." This is crucial for helping traders apply the right strategy for the current conditions.

🟠 FEATURES

This screener organizes the complex data from the SSA indicator into a simple, color-coded table. Here is a breakdown of each column and its possible values:

Asset: Displays the ticker symbol for the asset being analyzed.

Smart Signals: Shows the latest signal from the core engine.

▲: A standard bullish signal has been detected.

▼: A standard bearish signal has been detected.

▲+: A strong bullish signal with higher conviction has been detected.

▼+: A strong bearish signal with higher conviction has been detected.

Fair Value Trail: Indicates the trend direction based on the volatility trail.

▲: The FVT is in a bullish trend (acting as dynamic support).

▼: The FVT is in a bearish trend (acting as dynamic resistance).

Trend Spine: Shows the direction of the core underlying trend.

▲: The underlying trend backbone is bullish.

▼: The underlying trend backbone is bearish.

Trend Bias: Measures the current momentum strength.

Strong▲: Strong and accelerating bullish momentum.

Weak▲: Bullish momentum exists but is weakening.

Strong▼: Strong and accelerating bearish momentum.

Weak▼: Bearish momentum exists but is weakening.

Firmament Clouds: Identifies overbought/oversold conditions relative to volatility.

Very Overbought / Overbought: Price is significantly extended above its recent range.

Very Oversold / Oversold: Price is significantly extended below its recent range.

Neutral: Price is trading within its normal volatility range.

Trend-Range Classifier: Displays the market state as determined by the ML model.

Trend: The market is in a trending environment, suitable for trend-following strategies.

Range: The market is in a ranging or consolidating environment, suitable for mean-reversion strategies.

Exit Signal Count: Tracks the number of take-profit signals that have occurred since the last primary Smart Signal.

0, 1, 2, 3...: A numerical count of exit signals. A higher number suggests a trend may be maturing or exhausting.

🟠 USAGE

The main purpose of the screener is to quickly identify assets where multiple components of the SSA system are in alignment, indicating a high-confluence trading opportunity.

1. Setup and Configuration:

Add the screener to your chart.

Go into the settings and populate the "Watchlist" group with the symbols you wish to monitor.

Ensure the settings for the components (Time Horizon, Signal Mode, etc.) are synchronized with the settings on your main SSA indicator for consistency.

2. Interpreting the Columns for Trading Decisions:

Start with the Big Picture (TRC): First, look at the "Trend-Range Classifier" column. If it shows "Trend," you should be looking for trend-following setups. If it shows "Range," you might avoid taking strong trend signals.

Establish Directional Bias (Spine & Bias): For trend-following, look for assets where the "Trend Spine" and "Trend Bias" agree. A "▲" in the Spine column combined with a "Strong▲" in the Bias column indicates a healthy and robust uptrend.

Time Your Entry (Smart Signals): Once you have an asset with a clear bias, watch the "Smart Signals" column for a fresh signal that aligns with that bias. A "▲+" signal appearing in an asset with a strong bullish bias across other columns is a high-confluence entry point.

Add Context (FVT & Clouds): Use the "Fair Value Trail" and "Firmament Clouds" to refine your entry. A buy signal is generally stronger if the FVT is also bullish ("▲") and the price is not in a "Very Overbought" state according to the clouds.

Manage the Trade (Exit Count): After entering a trade, keep an eye on the "Exit Signal Count." As the number increases, it serves as a warning that the trend is becoming extended and it might be time to take partial profits or tighten your stop-loss.

Bezahltes Script

Machine Learning Moving Average [BackQuant]Machine Learning Moving Average

A powerful tool combining clustering, pseudo-machine learning, and adaptive prediction, enabling traders to understand and react to price behavior across multiple market regimes (Bullish, Neutral, Bearish). This script uses a dynamic clustering approach based on percentile thresholds and calculates an adaptive moving average, ideal for forecasting price movements with enhanced confidence levels.

What is Percentile Clustering?

Percentile clustering is a method that sorts and categorizes data into distinct groups based on its statistical distribution. In this script, the clustering process relies on the percentile values of a composite feature (based on technical indicators like RSI, CCI, ATR, etc.). By identifying key thresholds (lower and upper percentiles), the script assigns each data point (price movement) to a cluster (Bullish, Neutral, or Bearish), based on its proximity to these thresholds.

This approach mimics aspects of machine learning, where we “train” the model on past price behavior to predict future movements. The key difference is that this is not true machine learning; rather, it uses data-driven statistical techniques to "cluster" the market into patterns.

Why Percentile Clustering is Useful

Clustering price data into meaningful patterns (Bullish, Neutral, Bearish) helps traders visualize how price behavior can be grouped over time.

By leveraging past price behavior and technical indicators, percentile clustering adapts dynamically to evolving market conditions.

It helps you understand whether price behavior today aligns with past bullish or bearish trends, improving market context.

Clusters can be used to predict upcoming market conditions by identifying regimes with high confidence, improving entry/exit timing.

What This Script Does

Clustering Based on Percentiles : The script uses historical price data and various technical features to compute a "composite feature" for each bar. This feature is then sorted and clustered based on predefined percentile thresholds (e.g., 10th percentile for lower, 90th percentile for upper).

Cluster-Based Prediction : Once clustered, the script uses a weighted average, cluster momentum, or regime transition model to predict future price behavior over a specified number of bars.

Dynamic Moving Average : The script calculates a machine-learning-inspired moving average (MLMA) based on the current cluster, adjusting its behavior according to the cluster regime (Bullish, Neutral, Bearish).

Adaptive Confidence Levels : Confidence in the predicted return is calculated based on the distance between the current value and the other clusters. The further it is from the next closest cluster, the higher the confidence.

Visual Cluster Mapping : The script visually highlights different clusters on the chart with distinct colors for Bullish, Neutral, and Bearish regimes, and plots the MLMA line.

Prediction Output : It projects the predicted price based on the selected method and shows both predicted price and confidence percentage for each prediction horizon.

Trend Identification : Using the clustering output, the script colors the bars based on the current cluster to reflect whether the market is trending Bullish (green), Bearish (red), or is Neutral (gray).

How Traders Use It

Predicting Price Movements : The script provides traders with an idea of where prices might go based on past market behavior. Traders can use this forecast for short-term and long-term predictions, guiding their trades.

Clustering for Regime Analysis : Traders can identify whether the market is in a Bullish, Neutral, or Bearish regime, using that information to adjust trading strategies.

Adaptive Moving Average for Trend Following : The adaptive moving average can be used as a trend-following indicator, helping traders stay in the market when it’s aligned with the current trend (Bullish or Bearish).

Entry/Exit Strategy : By understanding the current cluster and its associated trend, traders can time entries and exits with higher precision, taking advantage of favorable conditions when the confidence in the predicted price is high.

Confidence for Risk Management : The confidence level associated with the predicted returns allows traders to manage risk better. Higher confidence levels indicate stronger market conditions, which can lead to higher position sizes.

Pseudo Machine Learning Aspect

While the script does not use conventional machine learning models (e.g., neural networks or decision trees), it mimics certain aspects of machine learning in its approach. By using clustering and the dynamic adjustment of a moving average, the model learns from historical data to adjust predictions for future price behavior. The "learning" comes from how the script uses past price data (and technical indicators) to create patterns (clusters) and predict future market movements based on those patterns.

Why This Is Important for Traders

Understanding market regimes helps to adjust trading strategies in a way that adapts to current market conditions.

Forecasting price behavior provides an additional edge, enabling traders to time entries and exits based on predicted price movements.

By leveraging the clustering technique, traders can separate noise from signal, improving the reliability of trading signals.

The combination of clustering and predictive modeling in one tool reduces the complexity for traders, allowing them to focus on actionable insights rather than manual analysis.

How to Interpret the Output

Bullish (Green) Zone : When the price behavior clusters into the Bullish zone, expect upward price movement. The MLMA line will help confirm if the trend remains upward.

Bearish (Red) Zone : When the price behavior clusters into the Bearish zone, expect downward price movement. The MLMA line will assist in tracking any downward trends.

Neutral (Gray) Zone : A neutral market condition signals indecision or range-bound behavior. The MLMA line can help track any potential breakouts or trend reversals.

Predicted Price : The projected price is shown on the chart, based on the cluster's predicted behavior. This provides a useful reference for where the price might move in the near future.

Prediction Confidence : The confidence percentage helps you gauge the reliability of the predicted price. A higher percentage indicates stronger market confidence in the forecasted move.

Tips for Use

Combining with Other Indicators : Use the output of this indicator in combination with your existing strategy (e.g., RSI, MACD, or moving averages) to enhance signal accuracy.

Position Sizing with Confidence : Increase position size when the prediction confidence is high, and decrease size when it’s low, based on the confidence interval.

Regime-Based Strategy : Consider developing a multi-strategy approach where you use this tool for Bullish or Bearish regimes and a separate strategy for Neutral markets.

Optimization : Adjust the lookback period and percentile settings to optimize the clustering algorithm based on your asset’s characteristics.

Conclusion

The Machine Learning Moving Average offers a novel approach to price prediction by leveraging percentile clustering and a dynamically adapting moving average. While not a traditional machine learning model, this tool mimics the adaptive behavior of machine learning by adjusting to evolving market conditions, helping traders predict price movements and identify trends with improved confidence and accuracy.

AI Money FlowAI Money Flow is a revolutionary trading indicator that combines cutting-edge artificial intelligence technologies with traditional Smart Money concepts. This indicator provides comprehensive market analysis with emphasis on signal accuracy and reliability.

Key Features:

Volume Profile with Smart Money Analysis - Displays real money flow instead of just volume, identifying key support and resistance levels based on actual trader activity.

Volatility-Based Support & Resistance - Intelligent support and resistance levels that dynamically adapt to market volatility in real-time for maximum accuracy.

Order Flow Analysis - Advanced detection of buying and selling pressure that reveals the true intentions of large market players.

Machine Learning Optimization - Futuristic AI technology that automatically learns and optimizes settings for each specific asset and timeframe.

Risk Management - Advanced volatility and price spike detection for better risk management and capital protection.

Real-time Dashboard - Modern dashboard with color-coded signals provides instant overview of market conditions and trends.

Accuracy: 88-93%

Machine Learning Price Predictor: Ridge AR [Bitwardex]🔹Machine Learning Price Predictor: Ridge AR is a research-oriented indicator demonstrating the use of Regularized AutoRegression (Ridge AR) for short-term price forecasting.

The model combines autoregressive structure with Ridge regularization , providing stability under noisy or volatile market conditions.

The latest version introduces Bull and Bear signals , visually representing the current momentum phase and model direction directly on the chart.

Unlike traditional linear regression, Ridge AR minimizes overfitting, stabilizes coefficient dynamics, and enhances predictive consistency in correlated datasets.

The script plots:

Fit Line — in-sample fitted data;

Forecast Line — out-of-sample projection;

Trend Segments — color-coded bullish/bearish sections;

Bull/Bear Labels 🐂🐻 — dynamic visual signals showing directional bias.

Designed for researchers, students, and developers, this tool helps explore regularized time-series forecasting in Pine Script™.

🧩 Ridge AR Settings

Training Window — number of bars used for model training;

Forecast Horizon — forecast length (bars ahead);

AR Order — number of lags used as features;

Ridge Strength (λ) — regularization coefficient;

Damping Factor — exponential trend decay rate;

Trend Length — period for trend/volatility estimation;

Momentum Weight — strength of the recent move;

Mean Reversion — pullback intensity toward the mean.

🧮 Data Processing

Prefilter:

None — raw close price;

EMA — exponential smoothing;

SuperSmoother — Ehlers filter for noise reduction.

EMA Length, SuperSmoother Length — smoothing parameters.

🖥️ Display Settings

Update Mode:

Lock — static model;

Update Once Reached — rebuild after forecast horizon;

Continuous — update every bar.

Forecast Color — projection line color;

Bullish/Bearish Colors — colors for trend segments.

🐂🐻 Bull/Bear Signal System

The Bull/Bear Signal System adds directional visual cues to highlight local momentum shifts and model-based trend confirmation.

Bull (🐂) — appears when upward momentum is confirmed (momentum > 0) .

Displayed below the bar, colored with Bullish Color.

Bear (🐻) — appears when downward momentum is dominant (momentum < 0) .

Displayed above the bar, colored with Bearish Color.

Signals are generated during model recalculations or when the directional bias changes in Continuous mode.

These visual markers are analytical aids , not trading triggers.

🧠 Core Algorithmic Components

Regularized AutoRegression (Ridge AR):

Solves: (X′X+λI)−1X′y

to derive stable regression coefficients.

Matrix and Pseudoinverse Operations — implemented natively in Pine Script™.

Prefiltering (EMA / Ehlers SuperSmoother) — stabilizes noisy data.

Forecast Dynamics — integrates damping, momentum, and mean reversion.

Trend Visualization — color-coded bullish/bearish line segments.

Bull/Bear Signal Engine — visualizes real-time impulse direction.

📊 Applications

Academic and educational purposes;

Demonstration of Ridge Regression and AR models;

Analysis of bull/bear market phase transitions;

Visualization of time-series dependencies.

⚠️ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading or investment advice.

The author assumes no liability for financial losses resulting from its use.

Use responsibly and at your own risk.

PAS/ML Hybrid Score System Metrics & SignalsThis tool provides trade signal visualization and live performance metrics for the PAS+ML Hybrid framework. It builds on the core " Price Action Strength/Machine Learning Hybrid Score System " indicator and displays actionable entries, exits, and historical trade statistics directly on the chart.

Signals:

Plots entry (▲) and exit (▼) arrows based on the Hybrid PAS+ML crossover logic, with an optional long-term trend filter for confirmation. Entry arrows occur at candle following the signal (i.e. the next open); exit arrows occur on the same candle, at the close. Metrics are calculated using these prices.

Performance Metrics:

Displays a live table of cumulative results including total trades, win rate, average realized profit, average maximum profit, and profit after X bars. Results can be viewed in percent or pips.

Customization:

Adjustable parameters for lookback lengths, smoothing, ML weighting, trend filter type (SMA/EMA), and FX pip display options.

Integration:

Designed to be used together with the ""Price Action Strength/Machine Learning Hybrid Score System" indicator, which provides the underlying hybrid score and volatility context. Use this metrics version for trade execution analysis and performance tracking.

Use Case:

Ideal for traders who want to quantify the historical and ongoing effectiveness of PAS+ML hybrid signals. Can assist in refining thresholds, holding periods, and risk-reward calibration.

Price Action Strength/Machine Learning Hybrid Score SystemThis indicator combines Price Action Strength (PAS) with a Machine Learning (ML) derived signal to form a dynamic hybrid momentum model. It helps visualize underlying trend quality and predictive strength, and includes optional Bollinger Bands for volatility context.

PAS (Price Action Strength):

Measures directional momentum using the slope of a linear regression and candle body bias. The slope can be normalized by ATR or price and is smoothed using EMAs for stability.

ML Score:

Computes a predictive signal using multiple technical features (such as distance from recent highs/lows, EMA change, SMA slope, and MACD histogram). The result is z-scored and smoothed via WMA for noise reduction.

Hybrid Score:

Dynamically weights PAS and ML signals. PAS dominates when ML confidence is low; ML influence increases as predictive strength rises. Produces a smooth, normalized hybrid curve oscillating around zero.

Bollinger Bands (optional):

Can be plotted on the ML smooth line, PAS normalized line, or Hybrid Score (selectable). Configurable length and multiplier to visualize volatility and overbought/oversold zones.

Visualization:

- PAS (blue), ML (orange), and Hybrid (aqua) plotted together.

- Background shading indicates bullish (green) or bearish (red) hybrid momentum.

- Optional Bollinger Bands for visual reference.

Inputs:

- PAS length, smoothing, and signal EMA

- ATR normalization toggle

- ML toggle, smoothing, and weighting scale

- Bollinger Bands toggle, source, length, and multiplier

Usage:

- Hybrid Score above zero suggests bullish momentum

- Hybrid Score below zero suggests bearish momentum

- Bollinger Band extremes can highlight potential turning points

- Better results on higher timeframes (i.e. 1H+)

Companion Indicator:

This indicator pairs with "PAS/ML Hybrid Score System Metrics & Signals " , a separate tool that displays trade signals and performance metrics directly on the price chart. Use both together for a full analytical workflow.

Adaptive Machine Learning Trading System [PhenLabs]📊Adaptive ML Trading System

Version: PineScript™v6

📌Description

The Adaptive ML Trading System is a sophisticated machine learning indicator that combines ensemble modeling with advanced technical analysis. This system uses XGBoost, Random Forest, and Neural Network algorithms to generate high-confidence trading signals while incorporating robust risk management features. Traders benefit from objective, data-driven decision-making that adapts to changing market conditions.

🚀Points of Innovation

• Machine Learning Ensemble - Three integrated models (XGBoost, Random Forest, Neural Network)

• Confidence-Based Trading - Only executes trades when ML confidence exceeds threshold

• Dynamic Risk Management - ATR-based stop loss and max drawdown protection

• Adaptive Position Sizing - Volatility-adjusted position sizing with confidence weighting

• Real-Time Performance Metrics - Live tracking of win rate, Sharpe ratio, and performance

• Multi-Timeframe Feature Analysis - Adaptive lookback periods for different market regimes

🔧Core Components

• ML Ensemble Engine - Weighted combination of XGBoost, Random Forest, and Neural Network outputs

• Feature Normalization System - Advanced preprocessing with custom tanh/sigmoid activation

• Risk Management Module - Dynamic position sizing and drawdown protection

• Performance Dashboard - Real-time metrics and risk status monitoring

• Alert System - Comprehensive alert conditions for entries, exits, and risk events

🔥Key Features

• High-confidence ML signals with customizable confidence thresholds

• Multiple trading modes (Conservative, Balanced, Aggressive) for different risk profiles

• Integrated stop loss and risk management with ATR-based calculations

• Real-time performance metrics including win rate and Sharpe ratio

• Comprehensive alert system with entry, exit, and risk management notifications

• Visual confidence bands and threshold indicators for easy signal interpretation

🎨Visualization

• ML Signal Line - Primary signal output ranging from -1 to +1

• Confidence Bands - Visual representation of model confidence levels

• Threshold Lines - Customizable buy/sell threshold levels

• Position Histogram - Current market position visualization

• Performance Tables - Real-time metrics display in customizable positions

📖Usage Guidelines

Model Configuration

• Confidence Threshold: Default 0.55, Range 0.5-0.95 - Minimum confidence for signals

• Model Sensitivity: Default 0.9, Range 0.1-2.0 - Adjusts signal sensitivity

• Ensemble Mode: Conservative/Balanced/Aggressive - Trading style preference

• Signal Threshold: Default 0.55, Range 0.3-0.9 - ML signal threshold for entries

Risk Management

• Position Size %: Default 10%, Range 1-50% - Portfolio percentage per trade

• Max Drawdown %: Default 15%, Range 5-30% - Maximum allowed drawdown

• Stop Loss ATR: Default 2.0, Range 0.5-5.0 - Stop loss in ATR multiples

• Dynamic Sizing: Default true - Volatility-based position adjustment

Display Settings

• Show Signals: Default true - Display entry/exit signals

• Show Threshold Signals: Default true - Display ±0.6 threshold crosses

• Show Confidence Bands: Default true - Display ML confidence levels

• Performance Dashboard: Default true - Show metrics table

✅Best Use Cases

• Swing trading with 1-5 day holding periods

• Trend-following strategies in established trends

• Volatility breakout trading during high-confidence periods

• Risk-adjusted position sizing for portfolio management

• Multi-timeframe confirmation for existing strategies

⚠️Limitations

• Requires sufficient historical data for accurate ML predictions

• May experience low confidence periods in choppy markets

• Performance varies across different asset classes and timeframes

• Not suitable for very short-term scalping strategies

• Requires understanding of basic risk management principles

💡What Makes This Unique

• True machine learning ensemble with multiple model types

• Confidence-based trading rather than simple signal generation

• Integrated risk management with dynamic position sizing

• Real-time performance tracking and metrics

• Adaptive parameters that adjust to market conditions

🔬How It Works

Feature Calculation: Computes 20+ technical features from price/volume data

Feature Normalization: Applies custom normalization for ML compatibility

Ensemble Prediction: Combines XGBoost, Random Forest, and Neural Network outputs

Signal Generation: Produces confidence-weighted trading signals

Risk Management: Applies position sizing and stop loss rules

Execution: Generates alerts and visual signals based on thresholds

💡Note:

This indicator works best on daily and 4-hour timeframes for most assets. Ensure you understand the risk management settings before live trading. The system includes automatic risk-off modes that halt trading during excessive drawdown periods.

Institutional Levels (CNN) - [PhenLabs]📊Institutional Levels (Convolutional Neural Network-inspired)

Version : PineScript™v6

📌Description

The CNN-IL Institutional Levels indicator represents a breakthrough in automated zone detection technology, combining convolutional neural network principles with advanced statistical modeling. This sophisticated tool identifies high-probability institutional trading zones by analyzing pivot patterns, volume dynamics, and price behavior using machine learning algorithms.

The indicator employs a proprietary 9-factor logistic regression model that calculates real-time reaction probabilities for each detected zone. By incorporating CNN-inspired filtering techniques and dynamic zone management, it provides traders with unprecedented accuracy in identifying where institutional money is likely to react to price action.

🚀Points of Innovation

● CNN-Inspired Pivot Analysis - Advanced binning system using convolutional neural network principles for superior pattern recognition

● Real-Time Probability Engine - Live reaction probability calculations using 9-factor logistic regression model

● Dynamic Zone Intelligence - Automatic zone merging using Intersection over Union (IoU) algorithms

● Volume-Weighted Scoring - Time-of-day volume Z-score analysis for enhanced zone strength assessment

● Adaptive Decay System - Intelligent zone lifecycle management based on touch frequency and recency

● Multi-Filter Architecture - Optional gradient, smoothing, and Difference of Gaussians (DoG) convolution filters

🔧Core Components

● Pivot Detection Engine - Advanced pivot identification with configurable left/right bars and ATR-normalized strength calculations

● Neural Network Binning - Price level clustering using CNN-inspired algorithms with ATR-based bin sizing

● Logistic Regression Model - 9-factor probability calculation including distance, width, volume, VWAP deviation, and trend analysis

● Zone Management System - Intelligent creation, merging, and decay algorithms for optimal zone lifecycle control

● Visualization Layer - Dynamic line drawing with opacity-based scoring and optional zone fills

🔥Key Features

● High-Probability Zone Detection - Automatically identifies institutional levels with reaction probabilities above configurable thresholds

● Real-Time Probability Scoring - Live calculation of zone reaction likelihood using advanced statistical modeling

● Session-Aware Analysis - Optional filtering to specific trading sessions for enhanced accuracy during active market hours

● Customizable Parameters - Full control over lookback periods, zone sensitivity, merge thresholds, and probability models

● Performance Optimized - Efficient processing with controlled update frequencies and pivot processing limits

● Non-Repainting Mode - Strict mode available for backtesting accuracy and live trading reliability

🎨Visualization

● Dynamic Zone Lines - Color-coded support and resistance levels with opacity reflecting zone strength and confidence scores

● Probability Labels - Real-time display of reaction probabilities, touch counts, and historical hit rates for active zones

● Zone Fills - Optional semi-transparent zone highlighting for enhanced visual clarity and immediate pattern recognition

● Adaptive Styling - Automatic color and opacity adjustments based on zone scoring and statistical significance

📖Usage Guidelines

● Lookback Bars - Default 500, Range 100-1000, Controls the historical data window for pivot analysis and zone calculation

● Pivot Left/Right - Default 3, Range 1-10, Defines the pivot detection sensitivity and confirmation requirements

● Bin Size ATR units - Default 0.25, Range 0.1-2.0, Controls price level clustering granularity for zone creation

● Base Zone Half-Width ATR units - Default 0.25, Range 0.1-1.0, Sets the minimum zone width in ATR units for institutional level boundaries

● Zone Merge IoU Threshold - Default 0.5, Range 0.1-0.9, Intersection over Union threshold for automatic zone merging algorithms

● Max Active Zones - Default 5, Range 3-20, Maximum number of zones displayed simultaneously to prevent chart clutter

● Probability Threshold for Labels - Default 0.6, Range 0.3-0.9, Minimum reaction probability required for zone label display and alerts

● Distance Weight w1 - Controls influence of price distance from zone center on reaction probability

● Width Weight w2 - Adjusts impact of zone width on probability calculations

● Volume Weight w3 - Modifies volume Z-score influence on zone strength assessment

● VWAP Weight w4 - Controls VWAP deviation impact on institutional level significance

● Touch Count Weight w5 - Adjusts influence of historical zone interactions on probability scoring

● Hit Rate Weight w6 - Controls prior success rate impact on future reaction likelihood predictions

● Wick Penetration Weight w7 - Modifies wick penetration analysis influence on probability calculations

● Trend Weight w8 - Adjusts trend context impact using ADX analysis for directional bias assessment

✅Best Use Cases

● Swing Trading Entries - Enter positions at high-probability institutional zones with 60%+ reaction scores

● Scalping Opportunities - Quick entries and exits around frequently tested institutional levels

● Risk Management - Use zones as dynamic stop-loss and take-profit levels based on institutional behavior

● Market Structure Analysis - Identify key institutional levels that define current market structure and sentiment

● Confluence Trading - Combine with other technical indicators for high-probability trade setups

● Session-Based Strategies - Focus analysis during high-volume sessions for maximum effectiveness

⚠️Limitations

● Historical Pattern Dependency - Algorithm effectiveness relies on historical patterns that may not repeat in changing market conditions

● Computational Intensity - Complex calculations may impact chart performance on lower-end devices or with multiple indicators

● Probability Estimates - Reaction probabilities are statistical estimates and do not guarantee actual market outcomes

● Session Sensitivity - Performance may vary significantly between different market sessions and volatility regimes

● Parameter Sensitivity - Results can be highly dependent on input parameters requiring optimization for different instruments

💡What Makes This Unique

● CNN Architecture - First indicator to apply convolutional neural network principles to institutional-level detection

● Real-Time ML Scoring - Live machine learning probability calculations for each zone interaction

● Advanced Zone Management - Sophisticated algorithms for zone lifecycle management and automatic optimization

● Statistical Rigor - Comprehensive 9-factor logistic regression model with extensive backtesting validation

● Performance Optimization - Efficient processing algorithms designed for real-time trading applications

🔬How It Works

● Multi-timeframe pivot identification - Uses configurable sensitivity parameters for advanced pivot detection

● ATR-normalized strength calculations - Standardizes pivot significance across different volatility regimes

● Volume Z-score integration - Enhanced pivot weighting based on time-of-day volume patterns

● Price level clustering - Neural network binning algorithms with ATR-based sizing for zone creation

● Recency decay applications - Weights recent pivots more heavily than historical data for relevance

● Statistical filtering - Eliminates low-significance price levels and reduces market noise

● Dynamic zone generation - Creates zones from statistically significant pivot clusters with minimum support thresholds

● IoU-based merging algorithms - Combines overlapping zones while maintaining accuracy using Intersection over Union

● Adaptive decay systems - Automatic removal of outdated or low-performing zones for optimal performance

● 9-factor logistic regression - Incorporates distance, width, volume, VWAP, touch history, and trend analysis

● Real-time scoring updates - Zone interaction calculations with configurable threshold filtering

● Optional CNN filters - Gradient detection, smoothing, and Difference of Gaussians processing for enhanced accuracy

💡Note

This indicator represents advanced quantitative analysis and should be used by traders familiar with statistical modeling concepts. The probability scores are mathematical estimates based on historical patterns and should be combined with proper risk management and additional technical analysis for optimal trading decisions.

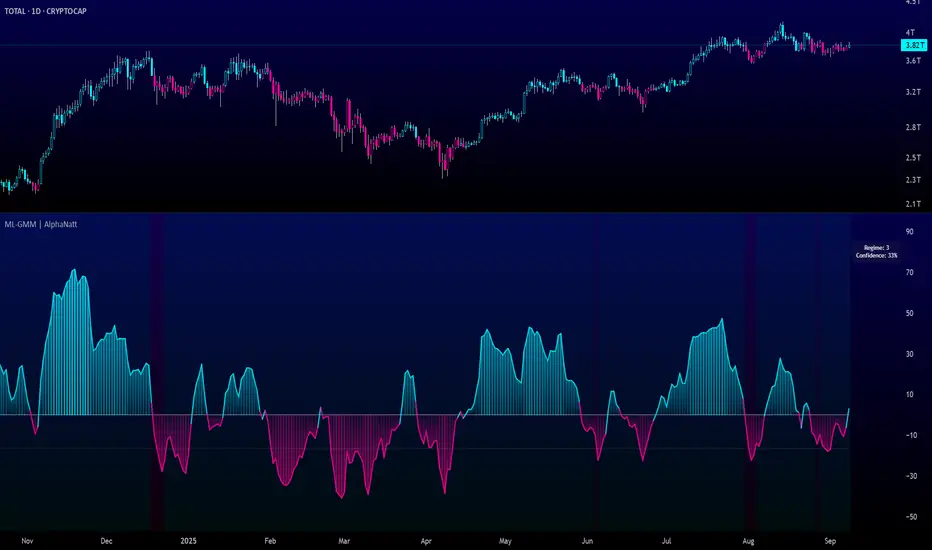

Machine Learning Gaussian Mixture Model | AlphaNattMachine Learning Gaussian Mixture Model | AlphaNatt

A revolutionary oscillator that uses Gaussian Mixture Models (GMM) with unsupervised machine learning to identify market regimes and automatically adapt momentum calculations - bringing statistical pattern recognition techniques to trading.

"Markets don't follow a single distribution - they're a mixture of different regimes. This oscillator identifies which regime we're in and adapts accordingly."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🤖 THE MACHINE LEARNING

Gaussian Mixture Models (GMM):

Unlike K-means clustering which assigns hard boundaries, GMM uses probabilistic clustering :

Models data as coming from multiple Gaussian distributions

Each market regime is a different Gaussian component

Provides probability of belonging to each regime

More sophisticated than simple clustering

Expectation-Maximization Algorithm:

The indicator continuously learns and adapts using the E-M algorithm:

E-step: Calculate probability of current market belonging to each regime

M-step: Update regime parameters based on new data

Continuous learning without repainting

Adapts to changing market conditions

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 THREE MARKET REGIMES

The GMM identifies three distinct market states:

Regime 1 - Low Volatility:

Quiet, ranging markets

Uses RSI-based momentum calculation

Reduces false signals in choppy conditions

Background: Pink tint

Regime 2 - Normal Market:

Standard trending conditions

Uses Rate of Change momentum

Balanced sensitivity

Background: Gray tint

Regime 3 - High Volatility:

Strong trends or volatility events

Uses Z-score based momentum

Captures extreme moves

Background: Cyan tint

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 KEY INNOVATIONS

1. Probabilistic Regime Detection:

Instead of binary regime assignment, provides probabilities:

30% Regime 1, 60% Regime 2, 10% Regime 3

Smooth transitions between regimes

No sudden indicator jumps

2. Weighted Momentum Calculation:

Combines three different momentum formulas

Weights based on regime probabilities

Automatically adapts to market conditions

3. Confidence Indicator:

Shows how certain the model is (white line)

High confidence = strong regime identification

Low confidence = transitional market state

Line transparency changes with confidence

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ PARAMETER OPTIMIZATION

Training Period (50-500):

50-100: Quick adaptation to recent conditions

100: Balanced (default)

200-500: Stable regime identification

Number of Components (2-5):

2: Simple bull/bear regimes

3: Low/Normal/High volatility (default)

4-5: More granular regime detection

Learning Rate (0.1-1.0):

0.1-0.3: Slow, stable learning

0.3: Balanced (default)

0.5-1.0: Fast adaptation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING STRATEGIES

Visual Signals:

Cyan gradient: Bullish momentum

Magenta gradient: Bearish momentum

Background color: Current regime

Confidence line: Model certainty

1. Regime-Based Trading:

Regime 1 (pink): Expect mean reversion

Regime 2 (gray): Standard trend following

Regime 3 (cyan): Strong momentum trades

2. Confidence-Filtered Signals:

Only trade when confidence > 70%

High confidence = clearer market state

Avoid transitions (low confidence)

3. Adaptive Position Sizing:

Regime 1: Smaller positions (choppy)

Regime 2: Normal positions

Regime 3: Larger positions (trending)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🚀 ADVANTAGES OVER OTHER ML INDICATORS

vs K-Means Clustering:

Soft clustering (probabilities) vs hard boundaries

Captures uncertainty and transitions

More mathematically robust

vs KNN (K-Nearest Neighbors):

Unsupervised learning (no historical labels needed)

Continuous adaptation

Lower computational complexity

vs Neural Networks:

Interpretable (know what each regime means)

No overfitting issues

Works with limited data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📈 PERFORMANCE CHARACTERISTICS

Best Market Conditions:

Markets with clear regime shifts

Volatile to trending transitions

Multi-timeframe analysis

Cryptocurrency markets (high regime variation)

Key Strengths:

Automatically adapts to market changes

No manual parameter adjustment needed

Smooth transitions between regimes

Probabilistic confidence measure

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🔬 TECHNICAL BACKGROUND

Gaussian Mixture Models are used extensively in:

Speech recognition (Google Assistant)

Computer vision (facial recognition)

Astronomy (galaxy classification)

Genomics (gene expression analysis)

Finance (risk modeling at investment banks)

The E-M algorithm was developed at Stanford in 1977 and is one of the most important algorithms in unsupervised machine learning.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💡 PRO TIPS

Watch regime transitions: Best opportunities often occur when regimes change

Combine with volume: High volume + regime change = strong signal

Use confidence filter: Avoid low confidence periods

Multi-timeframe: Compare regimes across timeframes

Adjust position size: Scale based on identified regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚠️ IMPORTANT NOTES

Machine learning adapts but doesn't predict the future

Best used with other confirmation indicators

Allow time for model to learn (100+ bars)

Not financial advice - educational purposes

Backtest thoroughly on your instruments

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🏆 CONCLUSION

The GMM Momentum Oscillator brings institutional-grade machine learning to retail trading. By identifying market regimes probabilistically and adapting momentum calculations accordingly, it provides:

Automatic adaptation to market conditions

Clear regime identification with confidence levels

Smooth, professional signal generation

True unsupervised machine learning

This isn't just another indicator with "ML" in the name - it's a genuine implementation of Gaussian Mixture Models with the Expectation-Maximization algorithm, the same technology used in:

Google's speech recognition

Tesla's computer vision

NASA's data analysis

Wall Street risk models

"Let the machine learn the market regimes. Trade with statistical confidence."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Machine Learning Trading Systems

Version: 1.0

Algorithm: Gaussian Mixture Model with E-M

Classification: Unsupervised Learning Oscillator

Not financial advice. Always DYOR.

AI-Weighted RSI (Zeiierman)█ Overview

AI-Weighted RSI (Zeiierman) is an adaptive oscillator that enhances classic RSI by applying a correlation-weighted prediction layer. Instead of looking only at RSI values directly, this indicator continuously evaluates how other price- and volume-based features (returns, volatility, volume shifts) correlate with RSI, and then weights them accordingly to project the next RSI state.

The result is a smoother, forward-looking RSI framework that adapts to market conditions in real time.

By leveraging feature correlation instead of static formulas, AI-Weighted RSI behaves like a lightweight learning model, adjusting its emphasis depending on which features are most aligned with RSI behavior during the current regime.

█ How It Works

⚪ Feature Extraction

Each bar, the script computes features: log returns, RSI itself, ATR% (volatility), volume, and volume log-change.

⚪ Correlation Screening

Over a rolling learning window, it measures the correlation of each feature against RSI. The strongest relationships are ranked and selected.

⚪ Adaptive Weighting

Features are standardized (z-scored), then combined using their signed correlations as weights, building a rolling, adaptive prediction of RSI.

⚪ Prediction to RSI Weight

The predicted RSI is mapped back into a “weight” scale (±2 by default). Above 0 = bullish bias, below 0 = bearish bias, with color-graded fills to visualize overbought/oversold pressure.

⚪ Signal Line

A smoothing option (signal length) overlays a moving average of the AI-Weighted RSI for clearer trend confirmation.

█ Why AI-Weighted RSI

⚪ Adaptive to Market Regime

Because the model re-evaluates correlations continuously, it naturally shifts which features dominate, sometimes volatility explains RSI best, sometimes volume, sometimes returns.

⚪ Forward-Looking Bias

Instead of simply reflecting RSI, the model provides a projection, helping anticipate shifts in momentum before RSI itself flips.

█ How to Use

⚪ Directional Bias

Read the RSI relative to 0. Above = bullish momentum bias, below = bearish.

⚪ Overbought / Oversold Zones

Shaded fills beyond +0.5 or -0.5 highlight extremes where RSI pressure often exhausts.

⚪ Divergences

When price makes new highs/lows but AI-Weighted RSI fails to confirm, it often signals weakening momentum.

█ Settings

RSI Length: Lookback for the core RSI calculation.

Signal Length: Smoothing applied to the AI-Weighted RSI output.

Learning Window: Bars used for correlation learning and z-scoring.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Machine Learning-Inspired Supply & Demand Zones [AlgoPoint]This indicator is a Smart Supply & Demand Zone tool, developed with principles inspired by Machine Learning (ML). It intelligently filters out market noise, allowing you to focus only on the most significant zones where institutional order flow is likely present.

💡 How It Works: Why Is This Indicator "Smart"?

Unlike traditional indicators that only measure simple price movements, this script uses an algorithm that asks the same critical questions an experienced market analyst would to qualify a zone:

- 1. Price Imbalance: How fast and aggressively did the price leave the zone? Our algorithm measures the body size of the "departure candle" relative to the current market volatility (ATR). A zone is only considered if it was formed by an explosive move that is statistically significant, indicating a major imbalance between buyers and sellers.

- 2. Volume Confirmation: Did the "smart money" participate in this move? The script checks if the volume on the departure candle was significantly higher than the recent average volume. A spike in volume confirms that the move was backed by institutional interest, adding strength and validity to the zone.

- 3. Valid Pivot Structure: Did the zone originate from a meaningful swing high or low? The algorithm first identifies a valid pivot structure, ensuring that zones are not drawn from insignificant or random price fluctuations.

Only when a potential zone passes these three critical tests—our "quality filter"—is it drawn on your chart.

🚀 Features & How to Use

Using the indicator is straightforward. You will see two primary types of boxes on your chart:

* 🟥 Red Box (Supply Zone): An area of potential resistance where selling pressure is likely to be strong. Look for potential shorting opportunities as the price approaches this zone.

* 🟩 Green Box (Demand Zone): An area of potential support where buying pressure is likely to be strong. Look for potential long opportunities as the price pulls back into this zone.

Dynamic Zone Management

This indicator is not static; it lives and breathes with the market:

- Fresh Zone: A newly formed zone appears in its full, vibrant color. These are the highest-probability zones as they have not yet been re-tested.

- Broken / Flipped Zone: You have full control over what happens when a zone is broken! In the settings, you can choose:

- Delete Zone: The zone will be removed completely when the price closes through it.

- Show as Broken (Flip): When broken, the zone will turn gray, stop extending, and remain on your chart. This is extremely useful for identifying Support/Resistance Flips, where a broken demand zone becomes new resistance, or a broken supply zone becomes new support.

⚙️ Settings & Customization

Fine-tune the indicator to match your personal trading style via the settings menu:

- Breakout Behavior: The most powerful feature. Choose between Delete Zone and Show as Broken (Flip) to customize your chart.

- Zone Finding Logic: Control the indicator's sensitivity.

- Selective: Requires both strong imbalance and high volume. Finds fewer, but higher-quality, zones.