Bullish/Bearish Divergence DetectorUsuable on all time-frames

Indicates multiple divergences (up to 3) with the same start point/date of the divergence

Forecasting

20 Day Range High/Low (Turtle Soup)This indicator identifies the Highest High and Lowest Low of the last 20 periods (customizable) and projects horizontal support/resistance lines to the right.

Unlike standard Donchian Channels or other High/Low indicators that clutter the chart with historical "steps" or extend lines infinitely to the left, this script focuses on chart cleanliness.

Key Features:

Pivot-Point Start: The lines do not span the whole chart. They start exactly at the candle where the High or Low occurred.

Right Extension: Lines extend only to the future, providing a clear visual for potential breakouts or support levels.

No Historical Clutter: It does not draw the past movement of the High/Low, keeping your chart clean for price action analysis.

Dynamic: As new Highs or Lows are made, the lines instantly update to the new positions.

How to Use:

Trend Identification: Use the High line as a resistance/breakout level (similar to Turtle Trading strategies).

Stop Loss Placement: The Low line of the last 20 days often acts as a trailing stop location for long-term trends.

Timeframes: While designed for the classic "20-Day" lookback on the Daily chart, this script works on any timeframe (e.g., finding the 20-hour range on a 1H chart).

Settings:

Length: Default is 20 bars. You can change this in the settings to any lookback period you prefer (e.g., 50, 100).

Mean Reversion Signals (v6.4) – VWAP ±SD use with "support and resistence levels with breaks {lux algo} " at 5m tf for better results

HK Premarket RangeIndicates Highs and lows in the premarket for Hong Kong futures. Could be used for Chinese futures too.

Smart RSI Money Flow - Core Bands V1.01SMART RSI – Money Flow Bands (Technical Overview)

1. Background: RSI and Its Behavior on Lower Timeframes

The Relative Strength Index (RSI) originally is a momentum oscillator calculated from average gains and losses over a selected period. In its standard form, RSI is derived solely from price changes; it does not incorporate volume data or order-flow information in its formula.

Because RSI is price-based, its interpretation depends strongly on the timeframe:

• On higher timeframes, each bar aggregates more trading activity, and RSI tends to behave more smoothly.

• On lower timeframes (1-hour down to intraday scalping intervals), price fluctuations are quicker, and RSI becomes more sensitive to short-term noise.

This does not imply that RSI becomes invalid, but that its signals on fast charts can be more reactive and may benefit from additional context such as volume behavior or structural information.

2. Purpose of This Indicator

This indicator extends the classical RSI by adding information that RSI does not include:

• Mapping RSI values into price-based bands instead of the 0–100 oscillator space.

• Retrieving lower timeframe volume data and separating it into buy and sell components.

• Comparing the slope (angle) of price movement with the slope of buy and sell volume.

The goal is to provide a structural interpretation of where price sits relative to RSI conditions and how volume is behaving on a lower timeframe.

3. Technical Differences Compared to Classical RSI

A) Classical RSI

• Input: price only (usually close).

• Output: normalized oscillator between 0 and 100.

• Does not incorporate intra-bar volume distribution.

• Does not separate buy/sell volume.

B) SMART RSI – Money Flow Bands

1) RSI-to-Price Mapping

Converts RSI values into upper/lower price bands using recent price extremes.

2) Lower Timeframe Volume Decomposition

Retrieves LTF data and splits each bar’s volume into buy (close>open) and sell (close

Candlestick toolkit (Candle Over Candle)Candlestick pattern toolkit focused on reading price action via candle anatomy, body dynamics, and a specific 2-bar continuation/reversal pattern.

This indicator highlights:

Long upper and lower wicks (“topping” and “bottoming” tails) that can signal exhaustion or potential reversal.

Large bullish bodies relative to Average True Range (ATR), showing strong momentum.

Sequences of large green candles.

Runs of green candles with strictly increasing or strictly decreasing body size, to visualize acceleration vs. momentum fade.

A two-candle pattern:

“Candle over Candle” (CoC) for long bias: two bullish bars where the first has a small upper wick and the second has a modest lower wick (a brief dip then push higher).

Optional mirrored “Candle under Candle” (CuC) for short bias.

The script labels:

Topping/Bottoming tails (TT/BT).

Large-green sequences and increasing/decreasing bodies (N×LG, ↑B, ↓B).

CoC/CuC pattern bars as “PRE” and the actual breakout bars as “GO”.

While a pattern is “live,” a reference line marks the trigger level (pattern high for longs, pattern low for shorts).

Inputs let you:

Tune wick and body percentage thresholds for tail detection.

Adjust ATR length and the multiplier that defines a “large” body.

Change how many candles are required for large-green sequences and body size trends.

Configure the two-candle pattern (maximum wick sizes, whether a small dip is required, confirmation within N bars).

Choose confirmation mode: close-through the trigger or intrabar wick break.

Enable or disable the short (CuC) side.

Control visual features (tail markers, sequence markers, pattern labels, and background shading on pattern bars).

Typical use:

Apply on intraday or swing timeframes.

Use tails and body behavior to read strength/weakness and potential exhaustion.

Treat CoC/CuC PRE labels as pattern formation, and GO labels as potential trade triggers above/below the pattern.

Combine with your own filters (trend, volume, higher-timeframe levels) rather than using it as a standalone signal generator.

Ross Cameron 5 Pillars FilterFirst, I am not Ross Cameron. This indicator is based on his five pillars of stock selection.

ROSS CAMERON 5 PILLARS MOMENTUM FILTER

🎯 OVERVIEW

This indicator automatically checks if the current symbol meets Ross Cameron's famous "5 Pillars" stock selection criteria from Warrior Trading - a proven methodology for identifying high-probability momentum day trading setups.

📊 ROSS CAMERON'S 5 PILLARS

1️⃣ RELATIVE VOLUME ≥5x (Automated ✅)

• Compares current volume to 30-day average

• Minimum 5x confirms institutional/retail interest

• High RVol = high liquidity and momentum potential

2️⃣ DAILY % CHANGE ≥10% (Automated ✅)

• Stock must already be showing momentum

• Default threshold: 10% up from previous close

• Confirms demand is already present

3️⃣ NEWS CATALYST (Manual Check ⚠️)

• Breaking news justifies the price movement

• Look for: earnings, FDA approvals, partnerships, contracts

• 🔥 icon flags stocks with ≥15% momentum (likely news-driven)

4️⃣ PRICE RANGE $1-$20 (Automated ✅)

• Sweet spot for retail trader momentum

• Highly volatile small-cap stocks

• Accessible price range for position building

5️⃣ FLOAT <10 MILLION SHARES (Automated ✅)

• Low float creates supply/demand imbalances

• Enables explosive 50-100%+ intraday moves

• Automatically checked when data available

• Shows actual float with ✅/❌ indicator

🚀 KEY FEATURES

✅ GREEN BACKGROUND HIGHLIGHT

• Visual alert when ALL automated criteria are met

• Instantly identify potential setups while scanning watchlist

📋 DETAILED BREAKDOWN TABLE

• Shows pass/fail status for each pillar

• Displays actual values (RVol, %, Float, etc.)

• Color-coded for quick interpretation

🔥 STRONG MOMENTUM INDICATOR

• Highlights stocks ≥15% (likely have news catalyst)

• Helps prioritize which stocks to research first

🔔 BUILT-IN ALERTS

• "Ross Cameron Criteria Met" - All automated criteria pass

• "Strong Momentum Alert" - Stock showing explosive movement

⚙️ FULLY CUSTOMIZABLE

• Adjust all thresholds to your trading style

• Configurable table position and display

• Toggle volume spike filter on/off

💡 HOW TO USE

BEST WORKFLOW:

1. Build a watchlist of small-cap stocks using TradingView's Stock Screener

2. Add this indicator to your charts

3. Flip through your watchlist - look for GREEN BACKGROUNDS

4. Check the table for detailed breakdown of each pillar

5. VERIFY NEWS CATALYST (required for Pillar 3)

6. If float shows N/A, verify manually on Finviz

7. Execute your trading plan with proper risk management

OPTIMAL TIMING:

• Pre-Market (8:00-9:30 AM ET) - Identify gap-up candidates

• Morning Session (9:30 AM-12:00 PM ET) - Prime momentum window

• Avoid lunch hour (12:00-2:00 PM ET) - Low volume, choppy

ALERT SETUP:

1. Click "Create Alert" on your chart

2. Select "Ross Cameron Criteria Met" condition

3. Get notified when new setups appear real-time

⚙️ CUSTOMIZABLE SETTINGS

PILLAR 1 - RELATIVE VOLUME:

• Min RVol: 5.0x (Ross's minimum, increase for more selective)

• RVol Period: 30 days (industry standard)

PILLAR 2 - MOMENTUM:

• Min Daily %: 10% (increase to 15% for stronger setups)

PILLAR 3 - CATALYST:

• Strong Momentum %: 15% (threshold for 🔥 indicator)

PILLAR 4 - PRICE RANGE:

• Min Price: $1.00 (adjust based on account size)

• Max Price: $20.00 (Ross's sweet spot)

PILLAR 5 - FLOAT:

• Max Float: 10M shares (ultra-aggressive traders use 5M)

ADDITIONAL FILTERS:

• Volume Spike: 2x (Warrior Trading standard)

• Confirms intraday momentum continuation

📈 INTERPRETATION GUIDE

✅ GREEN BACKGROUND = GO!

• All automated criteria are met

• Check news catalyst before trading

• Verify setup on chart (not overextended)

• Follow your risk management plan

❌ NO GREEN BACKGROUND = WAIT

• At least one criterion failed

• Check table to see which pillar(s) failed

• May become valid later if momentum increases

🔥 FLAME ICON = HIGH PRIORITY

• Stock showing very strong momentum (≥15%)

• Likely has significant news catalyst

• Research news IMMEDIATELY

• Often the best setups of the day

⚠️ N/A FOR FLOAT = MANUAL CHECK

• TradingView doesn't have float data for this symbol

• Verify on Finviz.com or similar

• If float >10M, setup is invalid per Ross's criteria

📚 RECOMMENDED STRATEGIES

GAP AND GO:

• Stock gaps up 10%+ on news

• Enters above gap high with volume

• Targets: 20-50% gains

VWAP BOUNCE:

• Pullback to VWAP support

• Enters on bounce with volume confirmation

• Tight stop below VWAP

HIGH OF DAY BREAKOUT:

• New HOD with volume surge

• Momentum continuation play

• Trail stop as it runs

ABCD PATTERN:

• Classic reversal pattern

• Enters on D-point breakout

• Target: A-B distance from C

⚠️ RISK WARNINGS

• DAY TRADING IS HIGHLY RISKY - Most day traders lose money

• This indicator finds setups - YOUR EXECUTION determines success

• Always use proper risk management (1-2% risk per trade)

• Never trade without stop losses

• Paper trade extensively before using real money

• Past performance does not guarantee future results

🔧 TECHNICAL DETAILS

• Pine Script v6

• Works on any timeframe (calculates daily metrics automatically)

• Compatible with TradingView Free, Pro, Premium

• No repainting - all calculations based on confirmed data

• Efficient code - minimal lag

📊 DATA SOURCES

• Relative Volume: Calculated from 30-day volume average

• Daily %: Previous day's close vs current price

• Float: TradingView's shares_outstanding_float data

• Volume Spike: 20-period volume moving average

🎯 WHO THIS IS FOR

IDEAL FOR:

✅ Day traders focused on momentum strategies

✅ Traders who follow Ross Cameron/Warrior Trading methodology

✅ Small-cap stock traders ($1-$20 range)

✅ Scalpers and swing traders seeking high-volatility setups

NOT IDEAL FOR:

❌ Long-term investors

❌ Large-cap stock traders

❌ Options-only traders

❌ Traders who don't monitor news catalysts

💬 USAGE TIPS

1. COMBINE WITH OTHER TOOLS

• Use alongside your charting/technical analysis

• Verify pattern setups (bull flags, ABCD, etc.)

• Check Level 2 / Time & Sales for confirmation

2. MAINTAIN A WATCHLIST

• Update daily with fresh small-cap movers

• Use Finviz Gap Scanner as starting point

• Focus on sectors with momentum

3. RISK MANAGEMENT IS KEY

• Never risk more than 1-2% per trade

• Use 2:1 minimum profit/loss ratio

• Cut losses quickly, let winners run

• Position size based on volatility (ATR)

4. TRACK YOUR RESULTS

• Keep a trading journal

• Note which setups work best for you

• Refine criteria based on your data

• Continuous improvement mindset

📝 DISCLAIMER

This indicator is for EDUCATIONAL PURPOSES ONLY. It is not investment advice, a recommendation to buy/sell securities, or a guarantee of profits. Trading involves substantial risk of loss. Always:

• Conduct your own research and due diligence

• Consult with a licensed financial advisor

• Never risk money you cannot afford to lose

• Understand that most day traders lose money

• Practice in a simulator before trading real money

The creator of this indicator is not affiliated with Ross Cameron or Warrior Trading. This is an independent implementation of publicly available trading methodology.

📈 SUPPORT & FEEDBACK

If you find this indicator helpful, please:

• Give it a thumbs up 👍

• Leave a comment with your experience

• Share with other momentum traders

• Follow for updates and new indicators

For questions or suggestions, leave a comment below!

---

🏆 HAPPY TRADING! Remember: The indicator finds opportunities, but YOUR discipline, risk management, and execution determine your success.

#DayTrading #Momentum #RossCameron #WarriorTrading #SmallCaps #GapAndGo #Scalping #StockScreener

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.

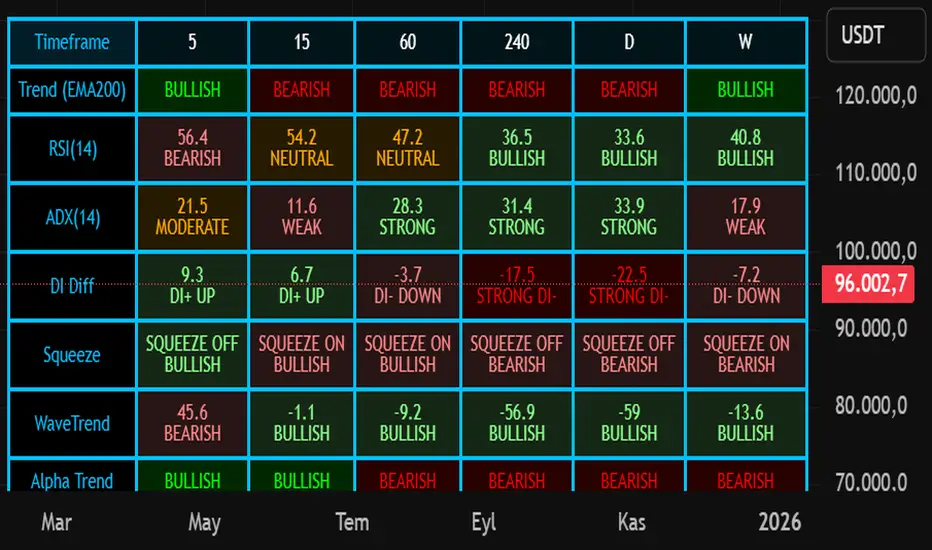

Nuh's Multi-Timeframe DashboardAll 10 indicators (EMA, RSI, ADX, RI, Squeezee, WaveTrend, Alpha Trend, SuperTrend, Stoch RSI, Vix Fix) across 7 time frames (5m, 15m, 1h, 2h, 4h, 1D, 1W) consolidated into a single table.

orb cody hoskinscody orb designed a 15 min range orb indicator for people to use dur8ng market open in asian and new york

Liquidity Hunter + ShortLiquidity Hunter + Short

Version with Short Trade Signals by Cihan Culha

This indicator is based on the original Liquidity Hunter by ChartPrime (MPL 2.0 license).

It detects potential Long and Short liquidity hunts by analyzing candle body, wick percentages, ATR bands, and slope direction.

Features:

Long signals (original) based on lower wick, body %, slope, and ATR bands

Short signals (added) based on upper wick, body %, negative slope, and ATR bands

Target (TP), Stop Loss (SL), CHOCH, and BOS levels plotted dynamically

Visual boxes highlight potential liquidity zones

Risk/Reward (RR) configurable via input

Usage Notes:

This modified version adds Short trade signals while preserving the original Long logic

Original author ChartPrime is credited; modifications by Cihan Culha

Adjust Body %, Wick %, and RR multiplier to suit your trading timeframe and style

For educational purposes; always use proper risk management

Bar RangeI use this to complement the daily ATR bars. It is interesting to see how much the stock has actually moved vs the ATR movement.

Target Reach & Trend ProjectionTarget Reach & Trend Projection

Overview: The Target Reach & Trend Projection indicator helps traders estimate how long (in candles) it might take for the price to reach a chosen target level, while also providing insight into the current and higher-timeframe trend directions.

Key Features

1. Target Projection: Set your custom Target Price manually.

The indicator calculates the expected number of candles needed to reach that price, based on recent price velocity.

Displays an estimated date and time for when the price could reach your target.

2. Trend Detection (Local): Detects the current market direction using one of two methods:

Linear Trend: Measures direct slope between candles.

Smoothed Trend: Uses a moving average slope for cleaner, less noisy trend estimation.

3. Higher-Timeframe Confirmation: Confirms whether the higher timeframe (e.g., 4H, 1D) trend agrees with the local trend.

Displays “✅ Aligned” when both are in sync and “⚠️ Diverging” when not.

4. On-Chart Information: A dynamic label near the target price line shows:

Target level

Trend method used

Estimated candles to target

Current trend direction

Estimated time of arrival (ETA)

Higher-timeframe trend confirmation

5. Visual Feedback: Background color changes lightly to reflect trend direction (green for bullish, red for bearish).

6. Alerts: Optional alerts for when:

The target price is reached.

Both local and higher-timeframe trends align bullishly or bearishly.

How It Works

The script measures the average price velocity (slope) over a chosen lookback period.

It then divides the distance between the current price and the target by that slope to estimate how many candles it might take to get there.

It projects the estimated time of arrival based on your chart’s current timeframe.

The script also checks a higher timeframe trend (using a moving average) for multi-timeframe confirmation.

🧭 Use Cases

Estimating the time horizon for swing trades or targets.

Confirming momentum direction before entering or exiting positions.

Aligning intraday setups with higher-timeframe trends.

⚠️ Notes

Estimates assume current trend velocity continues — it does not predict future volatility or reversals.

Works best on time-based charts with clear directional movement (e.g., 1H, 4H, 1D).

Swing Trade BUY/SELL + SCORING +COLOUR FIXBUY/SELL labels now appear with a score (1–3) next to them.

Color coding visually distinguishes signal strength:

BUY → 1 yellow, 2 light green, 3 dark green

SELL → 1 orange, 2 red, 3 burgundy

This allows you to instantly see the signal strength both numerically and visually.

💰 Akıllı Para Akışı v7 – Full Detay + Güç Kutusu + Etiketler✅ Everything Included:

✔ Money Flow

✔ RSI (Relative Strength Index)

✔ Momentum Filter

✔ Price Change Analysis

✔ Smart Money Zone Detection

✔ Strength Score (0–100)

✔ Dual Power Box (Inflow/Outflow Strength)

✔ Full-Detail BUY/SELL Labels

✔ Alert System (BUY & SELL)

✔ Optimized for Bottom Panel Display

TTS Calculator Forex calculator - Input account size, risk size and stop loss size, to get your lot size.

Monthly, Weekly Open + Daily Pivot (Broken Lines, fixed)monthly open line weekly open and daily pivot

This TradingView indicator plots three key reference levels on your chart:

Monthly Open Line – shows the current month’s opening price.

Weekly Open Line – shows the current week’s opening price.

Daily Pivot Line – shows the pivot level based on the previous day’s high, low, and close.

Each line resets at the start of its new period (month, week, or day), so the lines are broken, not continuous.

You can fully customize visibility, color, and thickness for each line.

It helps traders quickly see market bias and important support/resistance levels for better intraday or swing trading decisions.

Squeeze Momentum Early In and Out CandlesJohn Carter presented some candles called "Early In and Out Candles". Although I couldn't imitate the exact candles and warnings I create better indications and bars in my opinion.

When the Candles are above Donchian MA then we have a bullish Momentum.

When the Candles are bellow Donchian MA then we have bearish momentum.

This indicator works best to get an WARNING to enter and close EARLY positions.

Bullish:

When the candles are Light Blue then we have early warning to enter.

When the candles are Dark Blue then we have early warning to close the position.

Bearish:

When the candles are Red then we have early warning to enter.

When the candles are Yellow then we have early warning to close the position.

IMPORTANT NOTES:

Always combine it with the Squeeze Pro indicator.

Suggested Donchian MA: 5 (You can adjust it).

Don't let candles only to be your closing indication once again there are EARLY WARNINGS therefore can move your stop loses to maximize your profits when you are exiting.

I tested my self and I found that is the best strategy when we get Dark Blue candle in the Bullish move I move my stop loss little bit bellow the candle.

Therefore here we go we have early warnings for In and Out.

Thank you and Good Luck.

Average Dollar Volume by Mashrab

Standard Mode: By default, it shows a 20-period SMA of the Dollar Volume. This is great for swing trading to see if money flow is increasing over days.

Day Trading Mode: Go to the indicator settings (User Input) and check "Reset Average Daily".

The line will now represent the Cumulative Average for today only.

Example: If it's 10:00 AM, the line shows the average dollar volume per bar since the market opened at 9:30 AM. This helps you spot if the current 5-minute bar is truly igniting compared to the rest of the morning.

How to Use for Day Trading

Add the script to your 1-minute chart.

Ensure "Reset Average Daily" is checked in the settings (I made it default to true for you).

Look at the Table in the top right:

Avg Dollar Vol: This tells you the average money flowing into the stock per minute today.

1% Threshold: This gives you the exact number your friend likely uses to gauge "minimum viable liquidity" or specific risk calculations.