RSI Multi-Timeframe Dashboard by giua64)### Summary

This is an advanced dashboard that provides a comprehensive overview of market strength and momentum, based on the Relative Strength Index (RSI) analyzed across 6 different timeframes simultaneously (from 5 minutes to the daily chart).

The purpose of this script is to offer traders an immediate and easy-to-read summary of market conditions, helping to identify the prevailing trend direction, overbought/oversold levels, and potential reversals through divergence detection. All of this is available in a single panel, eliminating the need to switch timeframes on your main chart.

### Key Features

* **Multi-Timeframe Analysis:** Simultaneously monitors the 5m, 15m, 30m, 1H, 4H, and Daily timeframes.

* **Scoring System:** Each timeframe is assigned a score based on multiple RSI conditions (e.g., above/below 50, overbought/oversold status, direction) to quantify bullish or bearish strength.

* **Aggregated Signal:** The dashboard calculates a total percentage score and provides a clear summary signal: **LONG**, **SHORT**, or **WAIT**.

* **Divergence Detection:** Automatically identifies Bullish and Bearish divergences between price and RSI for each timeframe.

* **Non-Repainting Option:** In the settings, you can choose to base calculations on the close of the previous candle (`Use RSI on Closed Candle`). This ensures that past signals (like status and score) do not change, providing more reliable data for analysis.

* **Fully Customizable:** Users can modify the RSI period, overbought/oversold thresholds, divergence detection settings, and the appearance of the table.

### How to Read the Dashboard

The table consists of 6 columns, each providing specific information:

* **% (Total Score):**

* **Header:** Shows the overall strength as a percentage. A positive value indicates bullish momentum, while a negative value indicates bearish momentum. The background color changes based on intensity.

* **Rows:** Displays the numerical score for the individual timeframe.

* **RSI:**

* **Header:** The background color indicates the average of all RSI values. Green if the average is > 50, Red if < 50.

* **Rows:** Shows the real-time RSI value for that timeframe.

* **Signal (Status):**

* **Header:** This is the final operational signal. It turns **🟢 LONG** when bullish strength is high, **🔴 SHORT** when bearish strength is high, and **⚪ WAIT** in neutral conditions.

* **Rows:** Describes the RSI status for that timeframe (e.g., Bullish, Bearish, Overbought, Oversold).

* **Dir (Direction):**

* **Header:** Displays an arrow representing the majority direction across all timeframes.

* **Rows:** Shows the instantaneous direction of the RSI (↗️ for rising, ↘️ for falling).

* **Diverg (Divergence):**

* Indicates if a bullish (`🟢 Bull`) or bearish (`🔴 Bear`) divergence has been detected on that timeframe.

* **TF (Timeframe):**

* Indicates the reference timeframe for that row.

### Advantages and Practical Use

This tool was created to solve a common problem: the need to analyze multiple charts to understand the bigger picture. With this dashboard, you can:

1. **Confirm a Trend:** A predominance of green and a "LONG" signal provides strong confirmation of bullish sentiment.

2. **Identify Weakness:** Red signals on higher timeframes can warn of an impending loss of momentum.

3. **Spot Turning Points:** A divergence on a major timeframe can signal an excellent reversal opportunity.

### Originality and Acknowledgements

This script is an original work, written from scratch by giua64. The idea was to create a comprehensive and visually intuitive tool for RSI analysis.

Any feedback, comments, or suggestions to improve the script are welcome!

**Disclaimer:** This is a technical analysis tool and should not be considered financial advice. Always do your own research and backtest any tool before using it in a live trading environment.

Script open-source

In pieno spirito TradingView, il creatore di questo script lo ha reso open-source, in modo che i trader possano esaminarlo e verificarne la funzionalità. Complimenti all'autore! Sebbene sia possibile utilizzarlo gratuitamente, ricorda che la ripubblicazione del codice è soggetta al nostro Regolamento.

giua64

borsamercati.it – Educational tools by giua64

Anche su:

Declinazione di responsabilità

Le informazioni ed i contenuti pubblicati non costituiscono in alcun modo una sollecitazione ad investire o ad operare nei mercati finanziari. Non sono inoltre fornite o supportate da TradingView. Maggiori dettagli nelle Condizioni d'uso.

Rohstoffe

CHN BUY SELL with EMA 200Overview

This indicator combines RSI 7 momentum signals with EMA 200 trend filtering to generate high-probability BUY and SELL entry points. It uses colored candles to highlight key market conditions and displays clear trading signals with built-in cooldown periods to prevent signal spam.

Key Features

Colored Candles: Visual momentum indicators based on RSI 7 levels

Trend Filtering: EMA 200 confirms overall market direction

Signal Cooldown: Prevents over-trading with adjustable waiting periods

Clean Interface: Simple BUY/SELL labels without clutter

How It Works

Candle Coloring System

Yellow Candles: Appear when RSI 7 ≥ 70 (overbought momentum)

Purple Candles: Appear when RSI 7 ≤ 30 (oversold momentum)

Normal Candles: All other market conditions

Trading Signals

BUY Signal: Triggered when closing price > EMA 200 AND yellow candle appears

SELL Signal: Triggered when closing price < EMA 200 AND purple candle appears

Signal Cooldown

After a BUY or SELL signal appears, the same signal type is suppressed for a specified number of candles (default: 5) to prevent excessive signals in ranging markets.

Settings

RSI 7 Length: Period for RSI calculation (default: 7)

RSI 7 Overbought: Threshold for yellow candles (default: 70)

RSI 7 Oversold: Threshold for purple candles (default: 30)

EMA Length: Period for trend filter (default: 200)

Signal Cooldown: Candles to wait between same signal type (default: 5)

How to Use

Apply the indicator to your chart

Look for yellow or purple colored candles

For LONG entries: Wait for yellow candle above EMA 200, then enter BUY when signal appears

For SHORT entries: Wait for purple candle below EMA 200, then enter SELL when signal appears

Use appropriate risk management and position sizing

Best Practices

Works best on timeframes M15 and higher

Suitable for Forex, Gold, Crypto, and Stock markets

Consider market volatility when setting stop-loss and take-profit levels

Use in conjunction with proper risk management strategies

Technical Details

Overlay: True (plots directly on price chart)

Calculation: Based on RSI momentum and EMA trend analysis

Signal Logic: Combines momentum exhaustion with trend direction

Visual Feedback: Colored candles provide immediate market condition awareness

Adaptive Multi-TF Indicator Table with Presets giua64📌 Script Name:

Adaptive Multi-Timeframe Indicator Table with Presets — giua64

📄 Description:

This script displays an adaptive multi-timeframe dashboard that summarizes the signals of three key technical indicators:

Moving Averages (MAs), Relative Strength Index (RSI), and MACD.

It provides a fast and visually intuitive overview of market conditions across five timeframes (5m, 15m, 30m, 1h, 4h), helping traders quickly identify potential directional biases (e.g., bullish, bearish, or neutral) based on either predefined presets or fully manual settings.

🧰 Preset Configurations:

You can choose between four trading styles, each with optimized indicator parameters:

Scalping

• MAs: 5 / 10 (Fast), 20 / 50 (Slow)

• RSI: 7 periods | Overbought: 70 | Oversold: 30

• MACD: 5 / 13 | Signal: 3

Intraday

• MAs: 9 / 21 (Fast), 50 / 100 (Slow)

• RSI: 14 periods | Overbought: 60 | Oversold: 40

• MACD: 12 / 26 | Signal: 9

Swing

• MAs: 10 / 20 (Fast), 50 / 200 (Slow)

• RSI: 14 periods | Overbought: 65 | Oversold: 35

• MACD: 12 / 26 | Signal: 9

Manual

• Full custom control over all indicator settings.

🛠️ All settings can be customized manually from the options panel, including the exact MA periods, RSI thresholds, and MACD structure.

🧠 How It Works:

For each timeframe, the script evaluates:

MA crossover status (two levels):

The first symbol refers to the crossover of the fast MAs

The second symbol refers to the crossover of the slow MAs

🟢 = Bullish crossover

🔴 = Bearish crossover

➖ = Flat or no clear signal

RSI Direction:

↑ = RSI above upper threshold (potential overbought)

↓ = RSI below lower threshold (potential oversold)

→ = RSI in neutral range

MACD Line vs Signal Line:

↑ = MACD line is above signal line (bullish)

↓ = MACD line is below signal line (bearish)

→ = Flat or neutral signal

Each signal is assigned a numerical score. These are aggregated per timeframe to compute a combined score that reflects the directional bias for that specific time window.

🧠 Adaptive Logic by Asset:

This script is designed to be universally compatible across all asset types — including forex, crypto, stocks, indices, and commodities.

Thanks to its multi-timeframe nature and flexible indicator presets, the script automatically adjusts its behavior based on the asset selected, ensuring relevant analysis without requiring manual recalibration.

🧾 Summary Table Output:

At the bottom of the dashboard, a combined sentiment is displayed for:

3TF → 5m, 15m, 30m

4TF → Adds 1h

5TF → Adds 4h

Each row shows:

Signal → LONG / SHORT / NEUTRAL

Confidence (%) → Based on score aggregation and signal consistency

📌 Customization Options:

Table Position: Left, Right, or Center

Text Size: Small, Normal, or Large

Full Manual Configuration: All MA, RSI, and MACD parameters can be adjusted as needed

⚠️ Disclaimer:

This script is for educational and analytical purposes only.

It does not constitute financial advice or guarantee any trading results.

Always do your own research and apply responsible risk management.

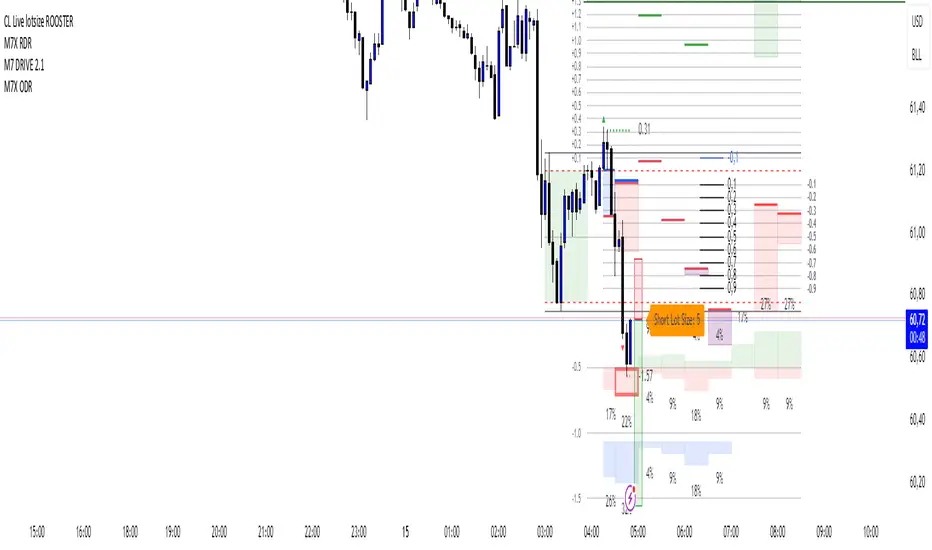

CL Live lotsize ROOSTER📄 Description:

This is a utility script designed for manual futures traders who enter with market orders and want to size their positions precisely based on $ risk.

⚙️ Features:

✅ Calculates live contract size based on:

A fixed dollar risk amount (e.g. $100)

A manually set static stop-loss price

The live market price as your entry

✅ Uses a configurable risk-reward ratio (e.g. 1:3)

✅ Plots entry, stop, and target levels on the chart

✅ Displays calculated contract size as a floating label

🎯 Why this tool?

Built to support fast execution workflows , this tool helps traders who:

Enter trades at candle close or open

Want to pre-calculate their market order size before the signal

Prefer a visual, consistent, real-time R:R validation system

Avoid fumbling with the long/short position tool at the last second

🔧 Settings:

Static Stop-Loss Price: Enter the price level where you'd place your SL

Account Risk ($): How much you’re willing to risk per trade

Risk-Reward Ratio: Set your target multiplier (e.g. 3 for 3R)

ATR Volatility giua64ATR Volatility giua64 – Smart Signal + VIX Filter

📘 Script Explanation (in English)

Title: ATR Volatility giua64 – Smart Signal + VIX Filter

This script analyzes market volatility using the Average True Range (ATR) and compares it to its moving average to determine whether volatility is HIGH, MEDIUM, or LOW.

It includes:

✅ Custom or preset configurations for different asset classes (Forex, Indices, Gold, etc.).

✅ An optional external volatility index input (like the VIX) to refine directional bias.

✅ A directional signal (LONG, SHORT, FLAT) based on ATR strength, direction, and external volatility conditions.

✅ A clean visual table showing key values such as ATR, ATR average, ATR %, VIX level, current range, extended range, and final signal.

This tool is ideal for traders looking to:

Monitor the intensity of price movements

Filter trading strategies based on volatility conditions

Identify momentum acceleration or exhaustion

⚙️ Settings Guide

Here’s a breakdown of the user inputs:

🔹 ATR Settings

Setting Description

ATR Length Number of periods for ATR calculation (default: 14)

ATR Smoothing Type of moving average used (RMA, SMA, EMA, WMA)

ATR Average Length Period for the ATR moving average baseline

🔹 Asset Class Preset

Choose between:

Manual – Define your own point multiplier and thresholds

Forex (Pips) – Auto-set for FX markets (high precision)

Indices (0.1 Points) – For index instruments like DAX or S&P

Gold (USD) – Preset suitable for XAU/USD

If Manual is selected, configure:

Setting Description

Points Multiplier Multiplies raw price ranges into useful units (e.g., 10 for Gold)

Low Volatility Threshold Threshold to define "LOW" volatility

High Volatility Threshold Threshold to define "HIGH" volatility

🔹 Extended Range and VIX

Setting Description

Timeframe for Extended High/Low Used to compare larger price ranges (e.g., Daily or Weekly)

External Volatility Index (VIX) Symbol for a volatility index like "VIX" or "EUVI"

Low VIX Threshold Below this level, VIX is considered "low" (default: 20)

High VIX Threshold Above this level, VIX is considered "high" (default: 30)

🔹 Table Display

Setting Description

Table Position Where the visual table appears on the chart (e.g., bottom_center, top_left)

Show ATR Line on Chart Whether to display the ATR line directly on the chart

✅ Signal Logic Summary

The script determines the final signal based on:

ATR being above or below its average

ATR rising or falling

ATR percentage being significant (>2%)

VIX being high or low

Conditions Signal

ATR rising + high volatility + low VIX LONG

ATR falling + high volatility + high VIX SHORT

ATR flat or low volatility or low %ATR FLAT

Thai Gold BahtIndicator Name: Thai Gold Baht

Short Title: Thai Gold Baht

Purpose

This indicator calculates and visualizes the real-time price of 1 Thai Gold Baht (15.244 grams) based on the global gold price ( XAU/USD ) and the USD/THB exchange rate .

Users can customize gold weight and purity to simulate the local Thai gold market price.

What it does

Retrieves live gold price per troy ounce in USD

Retrieves current USD to Thai Baht exchange rate

Converts the value using user-defined weight and purity

Displays result as a real-time chart

Shows calculation details in the Data Window

Ideal for

Traders tracking Thai gold based on international prices

Analysts comparing local and global bullion markets

Anyone needing a configurable, transparent gold price conversion

Pine Script Functionality

// Uses XAU/USD and USD/THB as inputs

// Calculates 1 Baht Gold (96.5% default purity)

// Outputs the value in THB as a chart line

ชื่ออินดิเคเตอร์: Thai Gold Baht

ชื่อย่อ: Thai Gold Baht

วัตถุประสงค์

อินดิเคเตอร์นี้ใช้คำนวณและแสดงราคาทองคำไทย 1 บาท (15.244 กรัม) แบบเรียลไทม์

โดยอ้างอิงจากราคาทองคำในตลาดโลก ( XAU/USD ) และอัตราแลกเปลี่ยน USD/THB

ผู้ใช้สามารถกำหนดน้ำหนักทองและความบริสุทธิ์เองได้ เพื่อจำลองราคาทองคำในประเทศไทยอย่างแม่นยำ

สิ่งที่อินดิเคเตอร์นี้ทำ

ดึงราคาทองคำแบบเรียลไทม์ต่อทรอยออนซ์ในสกุลเงิน USD

ดึงอัตราแลกเปลี่ยน USD → THB แบบเรียลไทม์

คำนวณราคาจากน้ำหนักและเปอร์เซ็นต์ความบริสุทธิ์ที่ผู้ใช้กำหนด

แสดงผลลัพธ์เป็นกราฟแบบเรียลไทม์ในหน่วยบาทไทย

แสดงรายละเอียดการคำนวณในหน้าต่าง Data Window ของ TradingView

เหมาะสำหรับ

นักเทรดที่ต้องการติดตามราคาทองคำไทยจากราคาทองคำตลาดโลก

นักวิเคราะห์ที่เปรียบเทียบราคาทองคำในประเทศและต่างประเทศ

ผู้ใช้งานที่ต้องการการแปลงราคาทองคำระหว่างประเทศให้โปร่งใสและปรับแต่งได้

การทำงานของ Pine Script

// ใช้ข้อมูล XAU/USD และ USD/THB เป็นอินพุต

// คำนวณราคาทองคำไทย 1 บาท (ความบริสุทธิ์เริ่มต้นที่ 96.5%)

// แสดงผลเป็นเส้นกราฟของราคาทองคำในหน่วยบาทไทย

Gold/Silver RatioOverview

This indicator displays the Gold/Silver Ratio by dividing the price of gold (XAUUSD) by the price of silver (XAGUSD) on the same timeframe. It is a widely used tool in macroeconomic and precious metals analysis, helping traders and investors evaluate the relative value of gold compared to silver.

📈 What it does

Plots the ratio between gold and silver prices as a line on the chart.

Displays two key horizontal levels:

Overbought level at 90 (dashed red line).

Oversold level at 70 (dashed green line).

Highlights the chart background to show extreme conditions:

Red shading when the ratio exceeds 90 (gold is likely overvalued relative to silver).

Green shading when the ratio drops below 70 (silver is likely overvalued relative to gold).

🧠 How to Use

When the ratio exceeds 90, it suggests that gold may be overbought or silver may be undervalued. Historically, these have been good times to consider shifting exposure from gold to silver.

When the ratio falls below 70, it may indicate silver is overbought or gold is undervalued.

This tool is best used in conjunction with technical analysis, macroeconomic trends, or RSI/Bollinger Bands applied to the ratio.

⚙️ Inputs

This version of the script uses OANDA's XAUUSD and XAGUSD pairs for spot gold and silver prices. You may edit the request.security() calls to change data sources (e.g., FXCM, FOREXCOM, or CFD tickers from your broker).

✅ Best For:

Macro traders

Commodity investors

Ratio and spread traders

Long-term portfolio reallocators

Global M2 [BizFing]MARKETSCOM:BITCOIN ECONOMICS:USM2

This is an indicator designed to show the correlation between the global M2 money supply and Bitcoin.

This indicator basically provides a Global M2 index by summing the M2 money supply data from the United States, South Korea, China, Japan, the EU, and the United Kingdom.

Furthermore, it is configured to allow you to add or remove the M2 data of desired countries within the settings.

I hope this proves to be a small aid in predicting the future price of Bitcoin.

If you have any questions or require any improvements while using it, please feel free to contact me.

Thank you.

Planting & Harvesting SeasonsHello all,

as a commodity trader, I use a lot of seasonal patterns in my analysis. Some time ago, I came up with the idea to develop a simple script that visually overlays the typical planting and harvesting periods for key agricultural futures directly on the chart.

This script automatically detects the underlying commodity based on the symbol (e.g. ZC, ZW, ZS, CT) and displays color-coded zones for each seasonal window. These zones are based on historical crop calendars and help identify when planting or harvesting typically takes place. The goal is to better align technical setups with fundamental seasonal factors.

This is a basic version and meant as a visual aid — not a trading signal in itself.

Hope you enjoy it and any feedback is highly appreciated!

Gas/Oil SpreadGas/Oil Spread Analyzer with Static Overbought/Oversold Zones

This indicator measures the spread between the actual price of natural gas and its oil-based equivalent, derived from a defined oil/gas ratio. It helps traders identify potential mispricings and mean-reversion opportunities between the two energy commodities.

Key Features:

- Calculates spread: Gas Price – Oil-Based Equivalent Price

- Supports dynamic or static oil/gas ratio

- Plots a smoothed version of the spread (SMA)

- Displays static overbought and oversold zones to highlight extreme deviations

Use Cases:

- Detect overvalued or undervalued gas relative to oil

- Spot potential reversion setups in intermarket trading

- Evaluate energy market dislocations and hedging opportunities

Oil/gas ratio MAOil/Gas Ratio-Based Equivalent Price

This indicator calculates the gas-equivalent price based on the current oil price and a defined oil/gas ratio. It helps identify relative overvaluation or undervaluation of natural gas compared to oil.

Features:

- Choose between a static or dynamic (SMA-based) oil/gas ratio

- Displays the fair value of gas derived from oil prices

- Works with any oil ticker symbol (e.g. BRENT, USOIL, etc.)

Useful for traders analyzing intermarket relationships and looking for relative value signals between energy commodities.

Reversal Strength Meter – Adib NooraniThe Reversal Strength Meter is an oscillator designed to identify potential reversal zones based on supply and demand dynamics. It uses smoothed stochastic logic to reduce noise and highlight areas where momentum may be weakening, signaling possible market turning points.

🔹 Smooth, noise-reduced stochastic oscillator

🔹 Custom zones to highlight potential supply and demand imbalances

🔹 Non-repainting, compatible across all timeframes and assets

🔹 Visual-only tool — intended to support discretionary trading decisions

This oscillator assists scalpers and intraday traders in tracking subtle shifts in momentum, helping them identify when a market may be preparing to reverse — always keeping in mind that trading is based on probabilities, not certainties.

📘 How to Use the Indicator Efficiently

For Reversal Trading:

Buy Setup

– When the blue line dips below the 20 level, wait for it to re-enter above 20.

– Look for reversal candlestick patterns (e.g., bullish engulfing, hammer, or morning star).

– Enter above the pattern’s high, with a stop loss below its low.

Sell Setup

– When the blue line rises above the 80 level, wait for it to re-enter below 80.

– Look for bearish candlestick patterns (e.g., bearish engulfing, inverted hammer, or evening star).

– Enter below the pattern’s low, with a stop loss above its high.

🛡 Risk Management Guidelines

Risk only 0.5% of your capital per trade

Book 50% profits at a 1:1 risk-reward ratio

Trail the remaining 50% using price action or other supporting indicators

Reversal Scalping Ribbon - Adib NooraniThe Reversal Scalping Ribbon is a trend-following overlay tool designed to visually identify potential reversal zones based on price extremes and dynamic volatility bands. It calculates adaptive upper and lower bands using price action and custom ATR logic, helping traders quickly assess market direction and possible turning points

🔹 Volatility-adjusted bands based on price highs/lows

🔹 Color-coded ribbons to indicate trend bias and potential reversal shifts

🔹 No repainting, works on all timeframes and assets

🔹 Visual-only display, no trade signals — supports discretion-based entries

This ribbon is designed for scalpers and intraday traders to spot reversal setups with clarity. It enhances your trading by showing real-time market bias without unnecessary distractions. By focusing on probabilities, it helps to improve decision-making in fast-paced environments

How to use the indicator efficiently

For Reversal Trading:

Buy: When price closes below the green ribbon with a red candle, then re-enters with a green candle. Enter above the high of the green candle with a stop loss below the lowest low of the recent green/red candles

Sell: When price closes above the red ribbon with a green candle, then re-enters with a red candle. Enter below the low of the red candle with a stop loss above the highest high of the recent red/green candles

Risk Management:

Limit risk to 0.5% of your capital per trade

Take 50% profit at a 1:1 risk-reward ratio

For the remaining 50%, trail using the lower edge of the green band for buys and the upper edge of the red band for sells

RiskCalc FX & GoldRiskCalc FX & Gold is a multi-market position sizing tool designed to help you manage risk quickly and accurately. With this script, simply enter your account capital, the percentage of risk you wish to take, and your stop in ticks. Depending on the selected market—Forex or XAUUSD—the script automatically adjusts its calculations:

Forex: Assumes 1 lot equals 100,000 units.

XAUUSD: Assumes 1 lot equals 100 ounces.

The script calculates your risk in dollars and, using a fixed value of 1 USD per tick per lot, determines the ideal position size in both lots and total contracts. Results are displayed in a clear, centralized table at the top of the chart for real-time decision-making.

Perfect for traders operating across multiple markets who need an automated and consistent approach to risk management.

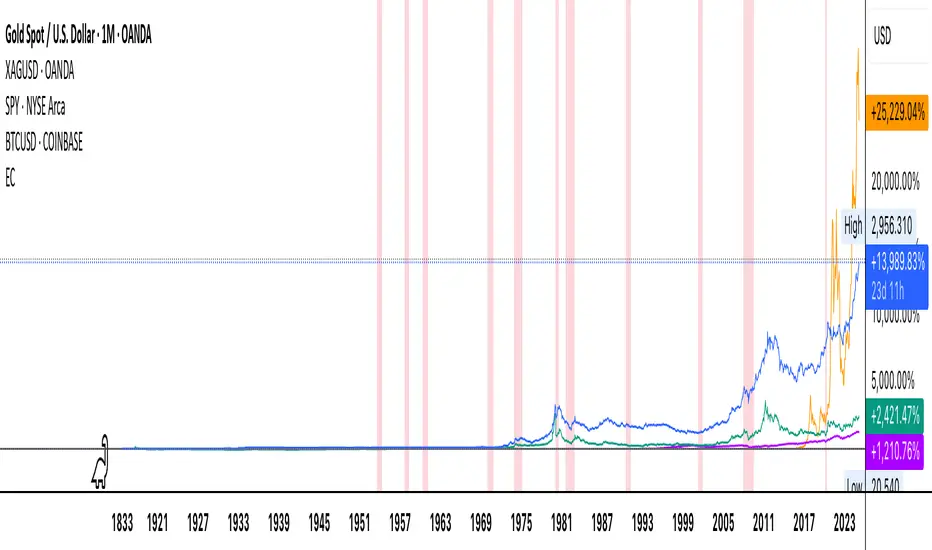

Economic Crises by @zeusbottradingEconomic Crises Indicator by @zeusbottrading

Description and Use Case

Overview

The Economic Crises Highlight Indicator is designed to visually mark major economic crises on a TradingView chart by shading these periods in red. It provides a historical context for financial analysis by indicating when major recessions occurred, helping traders and analysts assess the performance of assets before, during, and after these crises.

What This Indicator Shows

This indicator highlights the following major economic crises (from 1953 to 2020), which significantly impacted global markets:

• 1953 Korean War Recession

• 1957 Monetary Tightening Recession

• 1960 Investment Decline Recession

• 1969 Employment Crisis

• 1973 Oil Crisis

• 1980 Inflation Crisis

• 1981 Fed Monetary Policy Recession

• 1990 Oil Crisis and Gulf War Recession

• 2001 Dot-Com Bubble Crash

• 2008 Global Financial Crisis (Great Recession)

• 2020 COVID-19 Recession

Each of these periods is shaded in red with 80% transparency, allowing you to clearly see the impact of economic downturns on various financial assets.

How This Indicator is Useful

This indicator is particularly valuable for:

✅ Comparative Performance Analysis – It allows traders and investors to compare how different assets (e.g., Gold, Silver, S&P 500, Bitcoin) performed before, during, and after major economic crises.

✅ Identifying Market Trends – Helps recognize recurring patterns in asset price movements during times of financial distress.

✅ Risk Management & Strategy Development – Understanding how markets reacted in the past can assist in making better-informed investment decisions for future downturns.

✅ Gold, Silver & Bitcoin as Safe Havens – Comparing precious metals and cryptocurrencies against traditional stocks (e.g., SPY) to analyze their performance as hedges during economic turmoil.

How to Use It in Your Analysis

By overlaying this indicator on your Gold, Silver, SPY, and Bitcoin chart (for example), you can quickly spot historical market reactions and use that insight to predict possible behaviors in future downturns.

⸻

How to Apply This in TradingView?

1. Click on Use on chart under the image.

2. Overlay it with Gold ( OANDA:XAUUSD ), Silver ( OANDA:XAGUSD ), SPY ( AMEX:SPY ), and Bitcoin ( COINBASE:BTCUSD ) for comparative analysis.

⸻

Conclusion

This indicator serves as a powerful historical reference for traders analyzing asset performance during economic downturns. By studying past crises, you can develop a data-driven investment strategy and improve your market insights. 🚀📈

Let me know if you need any modifications or enhancements!

MATA GOLD RATIOMata Gold Instrument: User Guide

The Instrument to Gold Oscillator is a technical analysis tool that normalizes the ratio of an instrument's price (e.g., BTC/USD) to the price of gold (XAU/USD) into a 0-100 scale. This provides a clear and intuitive way to evaluate the relative performance of an instrument compared to gold over a specified period.

---

How It Works

1. Calculation of the Ratio:

The ratio is calculated as:

\text{Ratio} = \frac{\text{Instrument Price}}{\text{Gold Price}}

2. Normalization:

The ratio is normalized using the highest and lowest values over a user-defined period (length), typically 14 periods:

\text{Normalized Ratio} = \frac{\text{Ratio} - \text{Min(Ratio)}}{\text{Max(Ratio)} - \text{Min(Ratio)}} \times 100

3. Overbought/Oversold Levels:

Above 80: The instrument is relatively expensive compared to gold (overbought).

Below 20: The instrument is relatively cheap compared to gold (oversold).

---

How to Use the Oscillator

1. Identify Overbought and Oversold Levels:

If the oscillator rises above 80, the instrument may be overvalued relative to gold. This could signal a potential reversal or correction.

If the oscillator falls below 20, the instrument may be undervalued relative to gold. This could signal a buying opportunity.

2. Track Trends:

Rising oscillator values indicate the instrument is gaining value relative to gold.

Falling oscillator values indicate the instrument is losing value relative to gold.

3. Crossing the Midline (50):

When the oscillator crosses above 50, the instrument's value is gaining strength relative to gold.

When it crosses below 50, the instrument is weakening relative to gold.

4. Combine with Other Indicators:

Use this oscillator alongside other technical indicators (e.g., RSI, MACD, STOCH) for more robust decision-making.

Confirm signals from the oscillator with price action or volume analysis.

---

Example Scenarios

1. Trading Cryptocurrencies Against Gold:

If BTC/USD's oscillator value is above 80, Bitcoin may be overvalued relative to gold. Consider reducing exposure or looking for short opportunities.

If BTC/USD's oscillator value is below 20, Bitcoin may be undervalued relative to gold. This could be a good time to accumulate.

2. Commodities vs. Gold:

Analyze the relative strength of commodities (e.g., oil, silver) against gold using the oscillator to identify periods of overperformance or underperformance.

---

Advantages of the Oscillator

Relative Performance Insight: Tracks the performance of an instrument relative to gold, providing a macro perspective.

Clear Visual Representation: The 0-100 scale makes it easy to identify overbought/oversold conditions and trend shifts.

Customizable Periods: The user-defined length allows flexibility in analyzing short- or long-term trends.

---

Limitations

Dependence on Gold: As the oscillator is based on gold prices, any external shocks to gold (e.g., geopolitical events) can influence its signals.

No Absolute Buy/Sell Signals: The oscillator should not be used in isolation but as part of a broader analysis strategy.

---

By using the Instrument to Gold Oscillator effectively, traders and investors can gain valuable insights into the relative valuation and performance of assets compared to gold, enabling more informed trading and investment decisions.

Fractal levels Gold [AstroHub]This indicator detects key fractal points on a price chart and visually marks them with shapes and levels. It helps traders identify potential reversal zones and dynamic support/resistance levels, enhancing market analysis.

Key Features:

Fractal Detection:

The indicator identifies top and bottom fractals using a 5-bar pattern.

A top fractal forms when the middle bar has a higher high compared to the two bars on either side.

A bottom fractal forms when the middle bar has a lower low compared to the two bars on either side.

Fractal Filtering:

The indicator can filter out "pristine" fractals (uninterrupted fractal patterns) based on custom conditions, making it more selective and reducing false signals.

Fractal Plotting:

are plotted as downward triangles.

are plotted as upward triangles.

Users can choose to display or hide fractal points and their corresponding labels.

Fractal Levels:

The indicator automatically plots fractals' levels on the chart, marking potential resistance and support zones.

Fractal levels change dynamically as new fractals are identified.

Customizable Display Options:

Show or hide fractals and levels with adjustable settings.

Choose whether to apply filtering for pristine fractals.

Display the pivot labels to easily track fractal positions.

How It Works:

The indicator uses a simple approach to recognize top and bottom fractals . When a valid fractal is detected, it highlights it on the chart and plots the corresponding price level.

By default, top fractals are shown above the bars (red color), and bottom fractals are shown below the bars (green color).

Fractal levels represent potential reversal points and can act as dynamic support and resistance zones.

Best Use:

The indicator is particularly useful in identifying reversal points and trend changes, helping traders to spot key price levels.

It can be used across various timeframes and markets, particularly for trend-following or reversal strategies.

Customizable Settings:

Show Pivots: Toggle the display of pivot points.

Show Pivot Labels: Display labels for pivot levels.

Show Fractals: Toggle fractal points on the chart.

Show Fractal Levels: Show or hide the levels corresponding to the detected fractals.

Filter for Pristine Fractals: Enable this option to filter out non-pristine fractals for higher accuracy.

Conclusion:

This indicator provides clear, actionable fractal signals, helping traders easily identify critical levels for entry and exit. With customizable settings and visual cues, it's suitable for both novice and expe

Marcel's Dynamic Profit / Loss Calculator for GoldOverview

This Dynamic Risk / Reward Tool for Gold is designed to help traders efficiently plan and manage their trades in the volatile gold market. This script provides a clear visualisation of trade levels (Entry, Stop Loss, Take Profit) while dynamically calculating potential profit and loss. It ensures gold traders can assess their positions with precision, saving time and improving risk management.

Key Features

1. Trade Level Visualisation:

Plots Entry (Blue), Stop Loss (Red), and Take Profit (Green) lines directly on the chart.

Helps you visualise and confirm trade setups quickly which is good for scalping and day trades.

2. Dynamic Risk and Reward Calculations:

Calculates potential profit and loss in real time based on user-defined inputs such as position size, leverage, and account equity.

Displays a summary panel showing risk/reward metrics directly on the chart.

3. Customisable Settings:

Allows you to adjust key parameters like account equity, position size, leverage, and specific price levels for Entry, Stop Loss, and Take Profit.

Defaults are dynamically generated for convenience but remain fully adjustable for flexibility.

How It Works

The script uses gold-specific conventions (e.g., 1 lot = 100 ounces, 1 pip = 0.01 price change) to calculate accurate risk and reward metrics.

It dynamically positions Stop Loss and Take Profit levels relative to the entry price, based on user-defined or default offsets.

A real-time summary panel is displayed in the bottom-right corner of the chart, showing:

Potential Profit: The monetary value if the Take Profit is hit.

Potential Lo

ss: The monetary value if the Stop Loss is hit.

How to Use It

1. Add the script to your chart on a gold trading pair (e.g., XAUUSD).

2. Input your:

Account equity.

Leverage.

Position size (in lots).

Desired En

try Price (default: current close price).

3. Adjust the Stop Loss and Take Profit levels to your strategy, or let the script use default offsets of:

500 pips below the Entry for Stop Loss.

1000 pips above the Entry for Take Profit.

4. Review the plotted levels and the summary panel to confirm your trade aligns with your risk/reward goals.

Why Use This Tool?

Clarity and Precision:

Provides clear trade visuals and financial metrics for confident decision-making.

Time-Saving:

Automates the calculations needed to evaluate trade risk and reward.

Improved Risk Management:

Ensures you never trade without knowing your exact potential loss and gain.

This script is particularly useful for both novice and experienced traders looking to enhance their risk management and trading discipline in the Gold market. Enjoy clearer trades at speed.

Cantom Chart - CL CTG vs BKDEnglish : This Pine Script indicator, named "Cantom Chart - CL CTG vs BKD," uniquely analyzes the immediate state of oil futures contracts to determine if they are in contango or backwardation. The script uses the price ratio between the nearest (CL1) and the next nearest (CL2) NYMEX crude oil futures contracts. It multiplies this ratio by 100 for clarity and scales fluctuations for enhanced visibility.

Key Features:

Dynamic Ratio Calculation: Computes the ratio (CL1/CL2 * 100) to determine the immediate market state.

Market State Interpretation: A ratio above 100 indicates backwardation, suggesting higher demand than supply, while a ratio below 100 indicates contango, suggesting higher supply than demand.

Volatility Adjustment: Amplifies market state changes by tripling the deviation from the baseline of 100, making it easier to observe subtle shifts.

Anomaly Detection: Caps the adjusted ratio at 125 for highs and 75 for lows, maintaining these limits until the ratio returns to normal levels.

Usage: This indicator is especially useful for traders analyzing supply-demand dynamics and inflationary pressures in the oil market. To apply it, simply add the script to your TradingView chart and adjust the 'Lower Threshold' and 'Upper Threshold' lines as needed based on your trading strategy.

-----

日本語 : この「Cantom Chart - CL CTG vs BKD」Pine Scriptインジケーターは、直近の原油先物契約がコンタンゴまたはバックワーデーションにあるかを特定するための独自の分析を提供します。最近の(CL1)と次の(CL2)NYMEX原油先物契約間の価格比を使用し、この比率に100を掛けて明確性を高め、変動の視認性を向上させます。

主要機能:

動的比率計算: 市場の即時状態を判断するために比率(CL1/CL2 * 100)を計算します。

市場状態の解釈: 比率が100を超える場合はバックワーデーション(需要が供給を上回る)、100未満の場合はコンタンゴ(供給が需要を上回る)を示します。

変動調整: 基準値100からの偏差を3倍にして、微妙な変化を容易に観察できるようにします。

異常値検出: 調整された比率を高値で125、低値で75に制限し、通常のレベルに戻るまでこれらの限界を維持します。

使用方法: このインジケーターは、原油市場における需給ダイナミクスとインフレ圧力を分析するトレーダーにとって特に有用です。使用するには、このスクリプトをTradingViewチャートに追加し、トレーディング戦略に基づいて「Lower Threshold」と「Upper Threshold」のラインを必要に応じて調整します。

Williams Percent Range with Trendlines and BreakoutsHere is my "Williams Percent Range with Trendlines and Breakouts" indicator, a simple yet powerful tool for traders. This indicator combines the classic Williams %R oscillator, which helps identify overbought and oversold levels, with added trendlines for easier trend analysis at a glance.

It's designed to make spotting potential breakouts easier by drawing attention to significant price movements. With customizable settings for the Williams %R period and trendline sensitivity, it's a flexible tool for various symbols and trading styles.

Whether you're looking to refine your trading strategy or just need a clearer view of market trends, this indicator should offer a straight forward approach to hopefully enhance your trading decisions.

Disclaimer: This indicator is intended for educational and informational purposes only. Always conduct your own research and analysis before making trading decisions.

Trend Change IndicatorThe Trend Change Indicator is an all-in-one, user-friendly trend-following tool designed to identify bullish and bearish trends in asset prices. It features adjustable input values and a built-in alert system that promptly notifies investors of potential shifts in both short-term and long-term price trends. This alert system is crucial for helping less active investors correctly position themselves ahead of major trend shifts and assists in risk management after a trend is established. It's important to note that this indicator is most effective with assets that historically exhibit strong trends.

At the heart of this tool is the interaction between the 30-day and 60-day Exponential Moving Averages (EMA). A bullish trend is indicated in green when the 30-day EMA is above the 60-day EMA, while a bearish trend is signaled in red when the 30-day EMA is below the 60-day EMA. The appearance of gray alerts users to potential shifts in the current trend as the EMAs converge, falling below the Average True Range (ATR) safety margin. This analysis is conducted across both hourly and daily timeframes, with the 4-hour timeframe providing early signals for daily trend changes. The band visually represents the interaction between the daily EMAs and is also displayed in the second row of the table, with the first row showing the same EMA interaction on the 4-hour timeframe.

This indicator also includes a 140-day (20-week) Simple Moving Average (SMA), visually represented by a line with predictive dots. This feature significantly enhances the investor's ability to understand long-term trends in asset prices, offering forward-looking insights by projecting the SMA value 10 days into the future. The value of this forecast lies in interpreting the slope of the dots; upward trending dots suggest a bullish underlying trend, while downward trending dots indicate a bearish trend. Generally, prices above the SMA signal bullishness, and prices below indicate bearishness.

In summary, the Trend Change Indicator is a comprehensive solution for identifying price trends and managing risk. Its intuitive, color-coded design makes it an indispensable tool for traders and investors who aim to be well-positioned ahead of trend shifts and manage risk once a trend has been established. While it has proven historically valuable in trending markets such as cryptocurrencies, tech stocks, and commodities, it is advisable to use this indicator in conjunction with other technical analysis tools for a more comprehensive and well-rounded decision-making process.

Market Health MonitorThe Market Health Monitor is a comprehensive tool designed to assess and visualize the economic health of a market, providing traders with vital insights into both current and future market conditions. This script integrates a range of critical economic indicators, including unemployment rates, inflation, Federal Reserve funds rates, consumer confidence, and housing market indices, to form a robust understanding of the overall economic landscape.

Drawing on a variety of data sources, the Market Health Monitor employs moving averages over periods of 3, 12, 36, and 120 months, corresponding to quarterly, annual, three-year, and ten-year economic cycles. This selection of timeframes is specifically chosen to capture the nuances of economic movements across different phases, providing a balanced view that is sensitive to both immediate changes and long-term trends.

Key Features:

Economic Indicators Integration: The script synthesizes crucial economic data such as unemployment rates, inflation levels, and housing market trends, offering a multi-dimensional perspective on market health.

Adaptability to Market Conditions: The inclusion of both short-term and long-term moving averages allows the Market Health Monitor to adapt to varying market conditions, making it a versatile tool for different trading strategies.

Oscillator Thresholds for Recession and Growth: The script sets specific thresholds that, when crossed, indicate either potential economic downturns (recessions) or periods of growth (expansions), allowing traders to anticipate and react to changing market conditions proactively.

Color-Coded Visualization: The Market Health Monitor employs a color-coding system for ease of interpretation:

-- A red background signals unhealthy economic conditions, cautioning traders about potential risks.

-- A bright red background indicates a confirmed recession, as declared by the NBER, signaling a critical time for traders to reassess risk exposure.

-- A green background suggests a healthy market with expected economic expansion, pointing towards growth-oriented opportunities.

Comprehensive Market Analysis: By combining various economic indicators, the script offers a holistic view of the market, enabling traders to make well-informed decisions based on a thorough understanding of the economic environment.

Key Criteria and Parameters:

Economic Indicators:

Labor Market: The unemployment rate is a critical indicator of economic health.

High or rising unemployment indicates reduced consumer spending and economic stress.

Inflation: Key for understanding monetary policy and consumer purchasing power.

Persistent high inflation can lead to economic instability, while deflation can signal weak

demand.

Monetary Policy: Reflected by the Federal Reserve funds rate.

Changes in the rate can influence economic activity, borrowing costs, and investor

sentiment.

Consumer Confidence: A predictor of consumer spending and economic activity.

Reflects the public’s perception of the economy

Housing Market: The housing market often leads the economy into recession and recovery.

Weakness here can signal broader economic problems.

Market Data:

Stock Market Indices: Reflect overall investor sentiment and economic

expectations. No gains in a stock market could potentially indicate that economy is

slowing down.

Credit Conditions: Indicated by the tightness of bank lending, signaling risk

perception.

Commodity Insight:

Crude Oil Prices: A proxy for global economic activity.

Indicator Timeframe:

A default monthly timeframe is chosen to align with the release frequency of many economic indicators, offering a balanced view between timely data and avoiding too much noise from short-term fluctuations. Surely, it can be chosen by trader / analyst.

The Market Health Monitor is more than just a trading tool—it's a comprehensive economic guide. It's designed for traders who value an in-depth understanding of the economic climate. By offering insights into both current conditions and future trends, it encourages traders to navigate the markets with confidence, whether through turbulent times or in periods of growth. This tool doesn't just help you follow the market—it helps you understand it.

GOLD MonitorI'm using this platform from sometime and I carry out trading on Gold, using a kind of scalping strategy.

Scalping is not an easy task to do. Personally I found a lot of problems while detecting the trend direction.

So I decided to develop an indicator that is capable, in a discrete way, to give an instant-view on the market that is interesting.

This indicator can summarize in a small table all interesting figures related to gold scalping trading and is useful while joined with technical and fundamental analysis.

In this way it is possible to easy take under control all important aspects related to gold trading that I summarize here and you can find inside the table:

1) Gold / USD current direction

2) USD dollar strength (instant DXY) indicator take under consideration the DXY value every each tick and measures the increase or decrease in percentage. If there is a decrease the indicator displays a red low arrow, if there is an increase the indicator displays a green high arrow

also Gold friends are important so it is possible to find also:

3) NZDUSD (that is a Gold friend) variation percentage. If there is a decrease the indicator displays a red low arrow, if there is an increase the indicator displays a green high arrow

4) AUDUSD (that is a Gold friend) variation percentage. If there is a decrease the indicator displays a red low arrow, if there is an increase the indicator displays a green high arrow

then it is possible to find DXY USD dollar strength calculated between previous period (e.g. in timeframe M5 last 5 minutes) and current period (current 5 minutes). This indication is represented by an high arrow if there has been an increase, or by an low arrow if there has been a decrease.

Last but not least the information about the Gold trend itself with the possible forecast for the current period. This information must be carefully interpreted together with other instruments for technical analysis like Fibonacci lines.