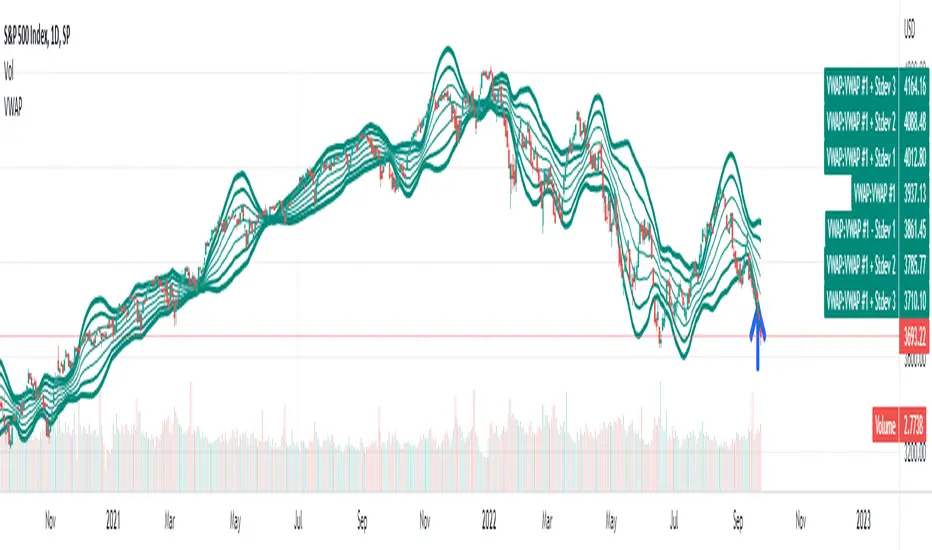

VWAP Boulevard [vnhilton](OVERVIEW)

The idea of this indicator comes from traders identifying supply to mainly look for shorts. Scenarios would be gap ups or pump & dumps where huge volume is transacted, & bag-holders are present. Some traders would draw resistance lines, I myself used to draw supply zones using the volume profile on that day, & others used the day VWAP on those days. VWAP Boulevard (I believe the name comes from the trader named team3dstocks) draws day VWAP lines from the highest volume days for a given period (excluding the current day).

(FEATURES)

- Draws horizontal & vertical lines from up to 250 highest volume days out of up to 3568 days, with the ability to hide either of these lines, their thicknesses, styles

- Extend/cut horizontal lines, or extend them all the way to the right

- Show the day VWAP, volume & age for these days in labels, with the ability to show what information you want to see only

- Separate customizable color forms for the lines & labels - ordinary (1 color); volume (2 color gradient from lowest to highest volume of the highest volume days); age (2 color gradient from youngest to oldest volume of the highest volume days)

- Edit offset & size of labels, & hide them

- Hide vertical lines

From left to right: Age color; ordinary color; volume color

250 highest volume days in the past year. Very messy so it's very likely you won't be using this but the ability to draw lines from 250 highest volume days is there if needed

(DRAWDOWNS)

- This indicator will only on the daily timeframe (error message will show up if unaware of this, & can be toggled off). Unfortunately, this would mean you would have to draw the lines manually yourself if you wish to use them on intraday timeframes.

- You may also encounter the 'Pine cannot determine the referencing length of a series. Try using max_bars_back' error. This occurs when the lookback period is very high & the indicator attempts to recalculate I believe. If this happens then reload the indicator.

The logic I used to obtain the highest volume days were to put all of the volume days in a given period in 1 array, then to sort them from highest to lowest, & also store their sorted indices in an separate array as well, so that drawings for each volume day could be done from the 2 arrays.

//Volume for last N periods

var int pastVol = array.new_int(lookbackPeriodFixed)

for i = 0 to lookbackPeriodFixed - 1

array.set(pastVol, i, int(volume ))

sortedIndices = array.sort_indices(pastVol, order.descending) //All Indices of sorted volume from highest to lowest

sortedIndices2 = array.slice(sortedIndices, 0, highestVolDays) //Indices of sorted volume from highest to lowest

array.sort(pastVol, order.descending) //All Volume sorted from highest to lowest

pastVol2 = array.slice(pastVol, 0, highestVolDays) //Volume sorted from highest to lowest

//Drawings

for i = 0 to highestVolDays - 1

index := array.get(sortedIndices, i)

vol := array.get(pastVol, i)

Since these array sizes were determined from the lookback period, it would mean that the request.security() function used to obtain daily values on intraday timeframes wouldn't work for a lookback period >20 (20 * 2 values I believe, which are the day VWAP & the day volume) as TradingView has put a maximum amount of calls of 40 in 1 script. Therefore, for intraday plots to work I would have to change the logic for getting the day VWAP & day volume for the highest days, as the request.security() function doesn't work on for loops, & this would also mean that the user would only be able to draw lines from up to 20 highest volume days instead of 250. I couldn't go forward with this as I wasn't able to find the logic to pick the highest volume days & their day VWAPs & times (indexes) without using a for loop. If anyone has any solutions (including for the 'Pine cannot determine the referencing length of a series. Try using max_bars_back' error) then please let me know. I've also left commented-out code for dealing with intraday drawings for future use.

Volume Weighted Average Price (VWAP)

Power Indicator - EMAs + VWAP + Volume BarThe Power Indicator is intended to return some exponential moving average, vwap, volume bar, and others. With this compilation, you will be able to use them as one indicator in Trading View.

The components are:

- EMA9 - Exponential Moving Average of 9 days

- EMA21 - Exponential Moving Average of 21 days

- EMA50 - Exponential Moving Average of 50 days

- EMA200 - Exponential Moving Average of 200 days

- Volume Bar - This indicator provides the volume of the candle and its strength by showing different colors. It's a way to check expressive volume in one bar.

- Vwap line

- Indicator

If you have any questions, let me know!

Custom_AVWAP_Harpal's-AnchorsAutomated VWAP Indicator written in PineScript for TradingView charts. Automatically Anchored at key swing H/L levels extracted from price and volume time-series.

Indicator takes one Argument, "LookBack (# of Periods)", and then for a given security finds three key anchors, the highest and lowest values in the 'hlc3' column (average of high low and close on the daily timeframe) in the last 'LookBack' # of days. The script displays up to three color coded time-series corresponding to a trailing Volume Weighted Average Price beginning at the anchor dates corresponding to the anchor points listed above.

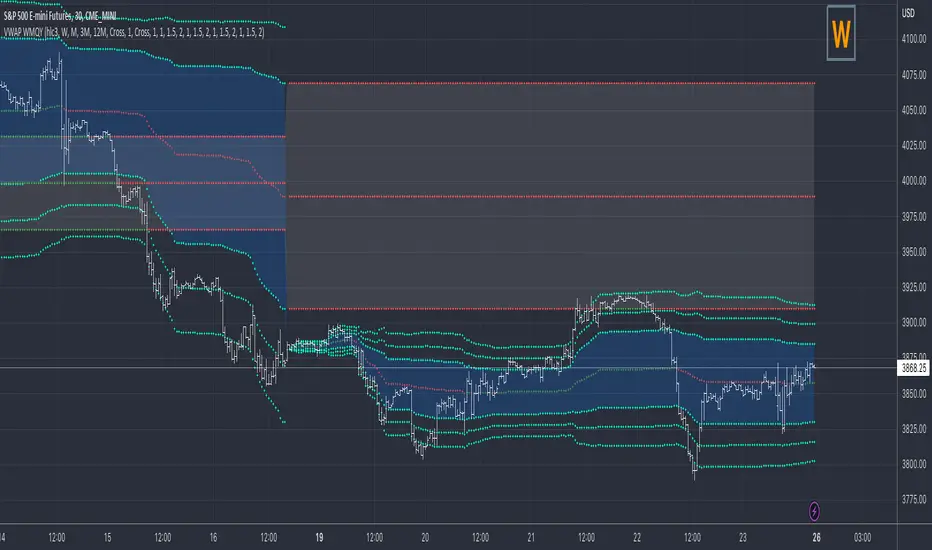

VWAP Previous VWAP WMQY StdDev Extensions Nadro StyleDisplays Multi-TF VWAP with Std Dev Bands.

Developing VWAP and Std Dev Bands

Previous VWAP and Std Dev Bands

Previous VWAP Extensions

Some Examples

Anchored VWAP BandSimple script to anchor vwap to a drag and drop spot on the chart and display it as a band instead of a line.

the AVAP Band displays:

1. The AVWAP using High as the source

2. The AVWAP using OHLC4 as the source

3. The AVWAP using Low as the source

This is just a different way of visualising VWAP from an anchored point in time (Band vs Line)

VWAP PredatorUsing VWAP as a start point, the VWAP Predator uses proprietary Fibonacci bands to help determine signal criteria. Most traders use VWAP in a simple way to determine whether an instrument is in a bearish or bullish state, but that doesn't help choosing the correct time to go long or short.

The xBat VWAP Predator uses behavioural analysis with volume, price action with open and close proximities to the Fibonacci bands/zones (Fib Zones). The following describes how the xBrat VWAP Predator is different to any standard use of Volume Weighted Average Price and uses xBrat Proprietary Behavioural logic to determine high probability long and Short signals. All of this heavy lifting and logic is done behind the scenes, keeping traders charts clean.

Long Trading Signals - Candle Coloured in Blue - There are many states with the logic to produce these signals, which are briefly described below:

1. The only standard criteria here - The price action must be above the VWAP Line

2. The Price must open below the boundary of one Fib Zone and close into the next Fib Zone

3. That Same Candle has to be an Accumulation Candle (more volume than the preceding candle and More Buyers) - This is determined with our proprietary logic coding

4. The Same signal candle also has to be higher than average volume. Again, our proprietary xBrat Logic just doesn't look back over a set number of bars, it looks at times of day and day of week, plus more to determine a true valuation of higher, lower or equal to average volume.

5. Only when these states are met, plus two more ema proximity logic, Does the xBrat VWAP predator give a Long Signal.

6. Trade Management is either set targets or indeed a simple ema cross which we provide as a ribbon on the chart to help traders. These ema's are different to entry logic. When the Ribbon turns from green to red, the trader should consider exiting the trade

Short Trading Signals - Candle Coloured in Pink - There are many states with the logic to produce these signals, which are briefly described below:

1. The only standard criteria here - The price action must be below the VWAP Line

2. The Price must open above the boundary of one Fib Zone and close into the next Fib Zone

3. That Same Candle has to be a Distribution Candle (more volume than the preceding candle and More Sellers) - This is determined with our proprietary logic coding

4. The Same signal candle also has to be higher than average volume. Again, our proprietary xBrat Logic just doesn't look back over a set number of bars, it looks at times of day and day of week, plus more to determine a true valuation of higher, lower or equal to average volume.

5. Only when these states are met, plus two more ema proximity logic, Does the xBrat VWAP predator give a Short Signal.

6. Trade Management is either set targets or indeed a simple ema cross which we provide as a ribbon on the chart to help traders. These ema's are different to entry logic. When the Ribbon turns from red to green, the trader should consider exiting the trade.

VWAP Predator is a day trading and scalping signals trading indicator.

ZenBot Signals - Trend StrengthI developed this indicator as a "regime detection" for my algo trading bot. It uses the ADX +/- values with a few twists.

- If ADX DI+ is over 30 and DI- is below 20 and falling (inverse for shorts)

- Price action rising/falling thru various VWAP standard deviations indicates a strong trend break

- Some other custom juju (open source so have fun).

I use this primarily to monitor the SPY index as a backdrop for my long and short trades. If the colored line below price bars is red or green, a strong trend is present and there is a decent trade environment.

Outlier Detecting Cumulative Moving Average (ODCMA)This is a simple moving average with a rolling length that resets whenever there is an outlier in the data. I have also included volume weighting.

The length represents the lookback period for the outlier detection and the "Outlier Detection" is the deviation level to trigger the detection. You can select from: price detection, volume detection, price or volume detection, price and volume detection.

I hope you can find this script useful. Its like a session weighted moving average but instead it retriggers the cumulative sum whenever there is an outlier.

GIRISH indicatorHello traders,

This indicator is the enhancement to my previous indicator (RSI+OBV). There is combined RSI and OBV with DMI. This new indicator is combination of RSI and OBV with VWAP . I have been using this indicator for intraday trades in NIFTY & BANKNIFTY .

The white line indicates the movement of VWAP wrt current price. There default range for this has been defined as -40 to 40 .

Entry for long: When white line goes below -40, we need to wait for green background. Entry has to be taken when green background appears. If price goes below the entry point, averaging can be done once. Price will surely go long and give us good profit.

Entry for short: When white line goes above 40 , we need to wait for red background (if darker red comes, it is better) . Entry has to be taken when red background appears. If price goes above the entry point, averaging can be done once. Price will surely go down and give us good profit on short side.

PS: Please do back testing in chart before taking trades.

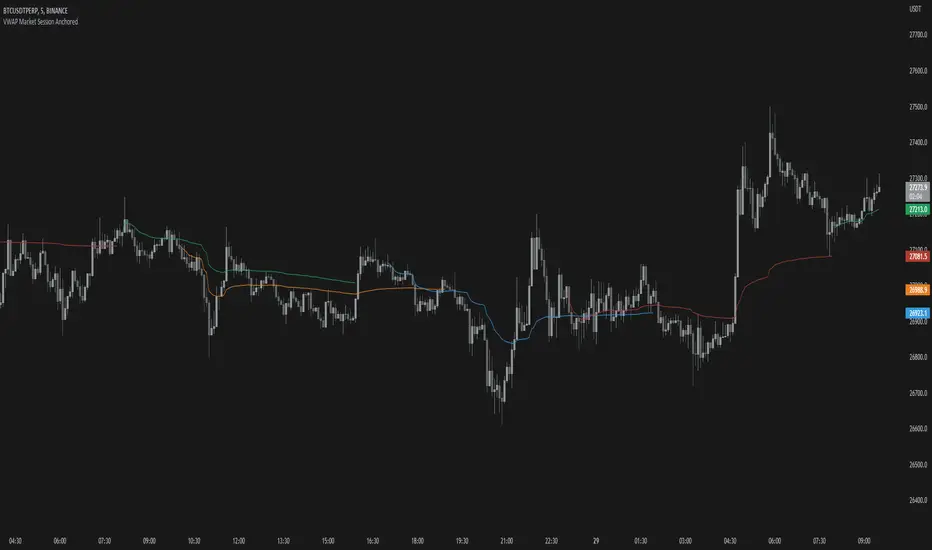

VWAP Market Session AnchoredVWAP Market Session Anchored differs from the traditional VWAP or VWAP Auto Anchored indicator in that the Volume Weighted Average Price calculation is automatically anchored to four major market session starts: Sydney, London, Tokyo, New York.

Settings

Source: the source for the VWAP calculation.

Offset: changing this number will move the VWAP either Forwards or Backwards, relative to the current market. Zero is the default.

Band: enabling this will show Standard Deviation bands.

Band Multiplier: the value the Standard Deviation bands will be multiplied by before being plotted on the chart.

Sessions : enabling the sessions will plot the respective anchored VWAP on chart.

Custom: enabling this will show a custom user-defined session.

Custom UTC : the custom session is defined by a starting UTC hour followed by the ending UTC hour.

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

VWAP & Previous VWAP - MTF█ Volume Weighted Average Price & Previous Volume Weighted Average Price - Multi Timeframe

This script can display the daily, weekly, monthly, quarterly, yearly and rolling VWAP but also the previous ones.

█ Volume Weighted Average Price (VWAP)

The VWAP is a technical analysis tool used to measure the average price weighted by volume.

VWAP is typically used with intraday charts as a way to determine the general direction of intraday prices.

VWAP is similar to a moving average in that when price is above VWAP, prices are rising and when price is below VWAP, prices are falling.

VWAP is primarily used by technical analysts to identify market trends.

█ Rolling VWAP

The typical VWAP is designed to be used on intraday charts, as it resets at the beginning of the day.

Such VWAPs cannot be used on daily, weekly or monthly charts. Instead, this rolling VWAP uses a time period that automatically adjusts to the chart's timeframe.

You can thus use the rolling VWAP on any chart that includes volume information in its data feed.

Because the rolling VWAP uses a moving window, it does not exhibit the jumpiness of VWAP plots that reset.

For the version with standard deviation bands.

MTF VWAP & StDev Bands

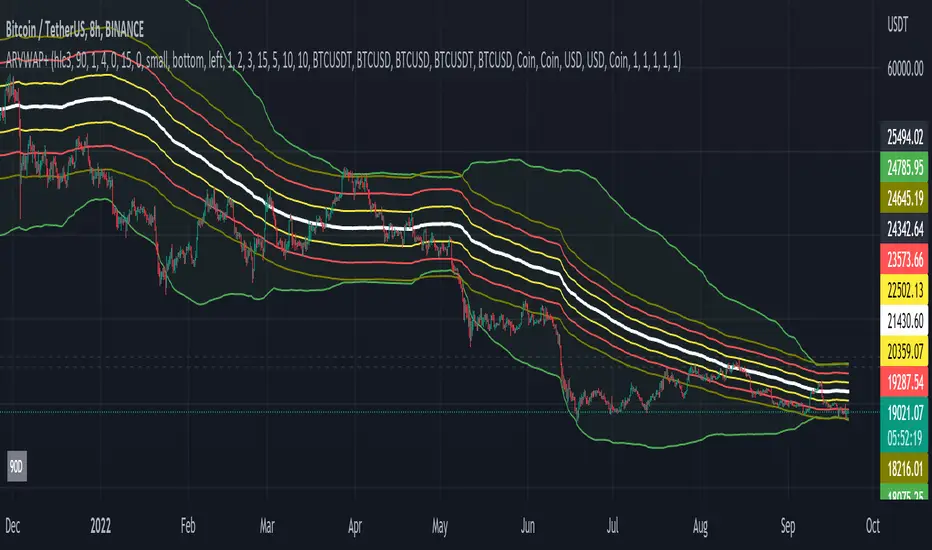

Adaptive VWAP Stdev BandsIntroduction

Heyo, here are some adaptive VWAP Standard Deviation Bands with nice colors.

I used Ehlers dominant cycle theories and ZLSMA smoothing to create this indicator.

You can choose between different algorithms to determine the dominant cycle and this will be used as reset period.

Everytime bar_index can be divided through the dominant cycle length and the result is zero VWAP resets if have chosen an adaptive mode in the settings.

The other reset event you can use is just a simple time-based event, e.g. reset every day.

Usage

I think people buy/sell when it reaches extreme zones.

Enjoy!

---

Credits to:

@SandroTurriate - VWAP Stdev Bands

@blackcat1402 - Dominant Cycle Analysis

@DasanC - Dominant Cycle Analysis

@veryfid - ZLSMA

(Sry, too lazy for linking)

I took parts of their code. Ty guys for your work! Just awesome.

RTH & ETH VWAPs [vnhilton]Plots 2 different VWAPs for regular & extended trading sessions, with option for a plot fill between the 2 (using pinescript's new vertical gradient feature).

VWAP - Volume-Weighted Average PriceVolume-Weighted Average Price (VWAP) is calculating day, week, month or year average price where transaction prices are weighted with the volume value.

This way script is estimating the average price based on both volume and price.

Features:

Drawing VWAP for days, weeks, months or years

Drawing initial periods (% with or without weekends)

Drawing last close value

3 standard deviation slots

Labels with values

Script Settings:

| Volume-Weighted Average Price visualization |

Type - Chart type selection:

D(ay) - Daily Volume Weighted Average Price

W(eek) - Weekly Volume Weighted Average Price

M(onth) - Monthly Volume Weighted Average Price

Y(ear) - Annual Volume Weighted Average Price

Draw VWAP - VWAP visiblity checkbox, color and line width used for VWAP visualization, checkbox for label with value.

Previous close - Drawing last VWAP close value. Color and line width used for drawing. checkbox for label with value.

Establishing period - Drawing initial area (described as % of the chart type period). Color picker for warning box background. VWAP is restarted with each period start. In the initial period VWAP value and it's deviations are not accurate and some traiding technics recommend to skip initial periods.

Include weekends - Checkbox if establishing period calculations should include weekends. Stock exchanges are not working during weekends (should be not checked) and crypto markets are working 7 days a week (should be checked).

| Standard deviation |

Slot1 - Standard deviation multiplier (0 is hiding), color and line width.

Slot2 - Standard deviation multiplier (0 is hiding), color and line width.

Slot3 - Standard deviation multiplier (o is hiding), color and line width.

Troubleshooting:

In case of any problems, please contact the author of the script. To improve speed of solving problem first check if script is drawn, and if there is a "!" character after script params. If you can see "!" character, move cursor over it for detail. Send message with error details, ticker and interval to us. The more precise will be your description the faster we will be able to help you.

ST_EMA+VWAP_V0.0Scalping strategy using relative position of price, intraday VWAP and EMAs

ex of timeframes for scalping 3 and 5 min chart

*** Default settings

- EMA 8 / 20

- Intraday VWAP

*** For bull conditions:

- Price must close twice above all lines above

- EMA 8 must be above EMA20

- should have a recent crossover between EMA8 and EMA20

Volume Weighted Reversal BandsThis is a vwap & vwma hybrid with upper & lower deviation bands that provide excellent price channels and reversal areas. It can be used on lower & higher timeframes, just increase the deviation % for higher timeframes. Try out the 1 minute timeframe with .5% deviation for great scalping levels.

Here is the calculation used for the main line.

(VWMA100 + VWMA500 + VWMA1000 + VWAP) / 4

So it combines 3 VWMAs with the VWAP and divides that number by 4 to give us a moving average. Then we add new levels above and below that moving average to get our channels. The channels are separated by the % deviation you choose in the settings. For tighter bands, lower the percentage deviation and for wider bands, increase the percentage deviation.

The fattest line in the middle is the main moving average and you can expect price to regularly return to this level. The thick lines are the main moving average plus or minus the percentage deviation you have set. There are 10 levels in each direction from the main moving average. The is also a thin short term moving average as well with a custom calculation. It takes 4 different length moving averages that are weighted and 4 more that are volume weighted and divides the total by 8.The lines will be green when price is above the line and red when price is below the line. The thin white line is the VWAP on its own.

These lines will act as dynamic support and resistance so you can scalp them back and forth. These levels work so well because they are volume weighted and the algos hedge their positions back and forth constantly.

For best results, use this indicator on tickers with the highest volume and trading action as the price will stick to these levels better when the big money players are hedging. Some great tickers for this indicator are APPL, SPY, BTC, ETH.

All colors and linewidths can be customized in the settings easily as well as turning off the VWAP or short moving average and adjusting the percentage deviation for the channels.

***MARKETS***

This indicator can be used on all markets, including stocks, crypto, futures and forex.

***TIMEFRAMES***

This indicator can be used on all timeframes.

***TIPS***

Try using numerous indicators of ours on your chart for extra confirmation. Our favorites to pair with these bands are the Scalper Ribbon and Trend Friend Signals. The 3 combined give you a lot of extra confirmation on whether the market is going to reverse at these levels.

VWAP Bollinger BandsWhat makes this different from vwap bands / bollinger bands?

This indicator takes a bit of inspiration from bollinger but instead of utilizing built in pine script std dev that uses simple moving average internally, this version replaces that with vwap.

Also instead of traditional bollinger band basis of 20 period simple moving average, the basis here for the bands is the vwap.

How to use it?

Usage is similar to vwap itself, though the standard deviation bands will expand and contract like normal bollinger bands instead of vwap bands that just widen as the market movement continues. The bands tell a slightly different story from bollinger bands as the underlying data utilized is the vwap itself.

Which markets is this meant for?

Any market.

What conditions?

This aids in finding conditions of entry standard to vwap, but the bands could give key areas of focus for entries and exits better than standard bollinger bands or vwap bands.

VWAP Anchored Date with multiplierA modified version from the default VWAP indicator with 2 major enhancements:

1- Start date: instead of being limited to applying the indicator on the entire chart, this script allows you to select the start time to show the VWAP. You can also use this option to show VWAP on an instrument starting from a specific time, all time high for example.

2- Multiplier: You can choose a period multiplier for VWAP, like 2 days, 4 month, 3 years and so on

Aggregated Rolling VWAP +Edit of TradingView's original Rolling VWAP

Edit log:

Added Volume Aggregation Capabilities to the Script

- Price Action is impacted by volume executed in all exchanges. Even though a single exchange RVWAP can be useful, using aggregated data makes it more accurate and saves time in symbol switching.

- Aggregation is preset to be done for Bitcoin Spot Pairs. However this can be changed to Aggregate Volume from any other symbol at the bottom of the setup menu.

Added Symmetrical Deviations to the Script

- Symmetrical deviations create range of "tolerance" around the RVWAP at a fixed % distance. This helps in situations when price does not respect the exact RVWAP level and goes slightly above/under.

- Adding multiple Symmetrical Deviations at different percentage values can give relevant levels for scalping, entries and range trading.

Switched default option to manual TF instead of automatic TF

Added TF Presets for quick switching between different settings. (Feature intended for mobile charting)

Added ON/OFF Switch to all individual deviations to make it easier, faster and cleaner to display different data. (Feature intended for mobile charting)

Multiple Non-Anchored VWAPA lot of VWAP scripts are anchored and only allow single VWAP additions. This script allows up to 5 simultaneous VWAPs, for example monthly, quarterly, yearly, 3 years, etc. Can also be used on smaller timeframes. The non-anchored part of the script allows it to be constantly rolling, with no resets.

I do not endorse this script, it was created at my request :)

Average Daily Range Lines + VWAP by TenozenOANDA:EURUSD

Hello! I created an indicator called ADRL (Average Daily Range Lines). This is my first original work, and I hope it's helpful to you guys.

1. Let me explain a bit of how it works...

So first of I need the ADR value, as by default length I use 19 for it. I want this indicator to calculate every start of the new day and break if another new day starts, so if the target level isn't reached, then the value would start to go back to 0 and get the new target level of the day. The target level is based on the first ADR multiplied by how much "percent" we want for the target level to hit, based on the first ADR value of the day. When the new day starts, the algo would start to add up the ADR value. If the added ADR hits the target level, it starts to plot a line by the candlestick by its high, low, and mid-level; it would create a new line if there is a new target being hit. So that's it.

About the VWAP, I took Tradingview's VWAP. I added the anchored part so I can plot a line if there is a new target level being hit. I hope that's okay.

2. How to use it...

- Using this indicator is pretty easy. When a new box is being plotted, that means that's the time when you should trade, as the box is still fresh. The VWAP helps if the market is trending or not.

- You can treat this indicator just like an S&R, as the price tends to respect the box. So best to use it as a pullback trade.

- We can assume if the price above the box, is a buy; vice versa.

3. Best Market to use...

- I suggest a trade in a nonvolatile market. The more volatile the market is, the harder the box is to be respected by the price. But if you really want to trade in that market, I suggest adjusting the inputs by how the box is being respected.

4. Suggestions...

- Use this indicator in 5 minutes chart if you day trade.

- Try using 30 minutes and setting the percent input from 100 to 80 and changing the ADR length from 19 to 14, this is much more suitable if you tend to hold trades.