Key Levels | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Key Levels indicator! This indicator allows you to see the key levels on the current chart such as previous day lows / highs, pre-market data, yesterday's close, today's open, pivot points, and much more! It's highly user-friendly with every line being individually customizable and having a wide range of text options.

Features of the new Key Levels indicator :

Today & Yesterday High, Low, Open & Close

Previous 3-10th Day Highs & Lows

Pre-Market Highs & Lows

Previous Month High & Low

High & Low Pivots

Combination Of Same Levels

Wide Customization Options

📌 HOW DOES IT WORK ?

Key levels are important areas in a chart where a significant reaction is expected. In this indicator, you can enable up to the previous 10 days highs and lows, yesterday's close / today's open, and the latest pivot points. Key levels generally act like support & resistance. Here are a few examples :

As shown, key levels play an important role determining the current trend and can be useful in identifying potential levels where the market will reverse or breakout.

🚩UNIQUENESS

1. More Key Levels

We believe that past key levels may be as important as current ones. Some of the key-levels indicators do not include them even though strong reactions can happen around them. Thus, our indicator let's you check up to 10 days backwards.

You can select the ones you think that are the most important and just enable them, making the indicator customizable to your liking.

2. Pre-Market Data

With assets that have pre-market data available, it's crucial to analyze it to have a better understanding of the market in regular trading hours. Our indicator will plot pre-market highs and lows, even if your chart is in the regular trading hours only mode. We believe this will be helpful with your analyzing process.

3. Combination

The indicator can dynamically combine same key levels, so you can have a clear look to the chart without lines & text colliding with each other. This would also help you determine stronger key levels as if a key level occured more than a time, it could be a sign that it's a stronger one. An example :

To summarize, using key levels is an essential skill while detecting zones where strong reactions are expected. This indicator provides up to 10 day's high and low levels, and all of them can be individually turned on / off. Traders that believe older key levels can be important and want to look at the whole picture may use this feature. Also for assets that have pre-market data available, the indicator provides pre-market levels as well. Besides all that, High & Low pivots will provide latest key levels so traders can use them in their decisions.

⚙️SETTINGS

1. General Configuration

You can enable / disable :

1. Today's High / Low / Open

2. Yesterday's High / Low / Close

3. 3th-10th Day High / Low

4. Pre-Market High / Low

5. Previous Month High / Low

You can also change the colors and switch their line styles between solid, dashed and dotted.

2. High & Low Pivots

Enabled -> Enable / Disable High & Low Pivots

Pivot Range -> The range used in the detection of pivot points. Larger values will result in less pivot points, while smaller values will provide more pivot points. This essentially determines how many bars to the right & left shouldn't exceed the pivot's high or low.

You can also change the text color and text size of the pivots from the settings.

3. Style settings

Text Offset -> How many bars of offset should the texts have to the right. Increase if text collides with bars while Align Labels option is set to "Right".

Extend Lines -> If enabled, lines will be extended infinitely to right & left. If disabled, all lines will be clamped in their timelines.

Show Line Values -> If enabled, line information text will contain their price.

Align Labels ->

Right = Align line labels to right.

Center = Line labels will always be at the center of the screen.

Unterstützung und Widerstand

[F][IND] FVG IdentifierMastering Market Imbalances with Ease

The FVG Identifier stands as a groundbreaking TradingView indicator, crafted to illuminate the often-overlooked Fair Value Gaps (FVG) in the dynamic world of price action trading. Let’s dive into how this tool is transforming the approach to identifying market inefficiencies.

Decoding Fair Value Gaps

Central to the concept of FVGs is the identification of market imbalances — moments where the equilibrium between buying and selling pressures is disrupted. These gaps are typically seen in a sequence of three candles, where a dominant candle is surrounded by others whose wicks fail to fully overlap it. These formations are critical as they often influence future price directions, acting as potential magnets.

Simplifying the Detection of FVGs

The FVG Identifier is engineered to enhance the visibility of Fair Value Gaps, making them starkly apparent even in complex market charts. Its algorithms ensure that these vital market indicators are easily and promptly recognized, allowing traders to spot valuable trading opportunities with minimal effort.

Features of the FVG Identifier

1. Intuitive Interface: The indicator is designed for ease of use, accommodating both beginners and experienced traders.

2. Customizable Settings: It offers flexible configuration options, allowing for adaptation to various trading styles and strategies.

3. Strategic Trading Insight: By highlighting FVGs, the tool provides traders with actionable insights for strategic entry and exit points based on potential price movements.

Elevating Your Trading Strategy

Incorporating the FVG Identifier into your trading arsenal equips you with a nuanced perspective on market analysis. It not only assists in identifying significant market imbalances but also enriches your technical analysis with powerful, data-backed insights.

Revolutionizing Price Action Trading

The FVG Identifier transcends the role of a mere indicator; it represents a significant leap in trading methodology. Compatible with various trading platforms, this tool is ready to enhance your market understanding and application of Fair Value Gaps.

Embrace the FVG Identifier to uncover the hidden dynamics of market gaps and translate these insights into efficient and profitable trading strategies.

Disclaimer:

This indicator is provided for educational purposes only. Trading involves risk, and users should consult with a financial professional before making any trading decisions.

Your Feedback Matters!

Please feel free to comment or reach out if you have any improvement suggestions or if you would like to request the development of a specific indicator. Your feedback is invaluable!

CANDLE LEVELS [PRO]This indicator provides you with 55 levels! with labels to help you identify quickly where current price is in relation to the OPEN, CLOSE, HIGH OF DAY and LOW OF DAY to a respective level. Choose from levels as low as the 5 minute time frame all the way up to 200 days. All of the levels except the day's OPEN, HIGH OF DAY AND LOW OF DAY use the PREVIOUS time frame's level. In other words, when you're looking at the "1 DAY HIGH", that's actually the previous day's HIGH OF DAY. Whether you're a scalper on the lower time frames or a swing trader that mainly uses the 1 hour and above, these candle levels can be an invaluable source of support and resistance; in other words you'll often see price bounce off of a level (whether price is increasing or decreasing) once or multiple times and that could be an indication of a price's direction. Another way that you could utilize this indicator is to use it in confluence with other popular signals, such as an EMA crossover. For instance, you could watch as price rises above the 21 EMA all the while price is also crossing up and over the previous day's HIGH OF DAY with a relative volume that's double that of the previous week's average. These are just a few of some potential bullish signals that you could look for to go long on a trade using the candle levels provided.

I've made this indicator extremely customizable:

⚡Each level has 2 labels: 1 "at level" and 1 "at right", each label and price can be disabled

⚡Each label has its own input for label padding. The "at right" label padding input allows you to zoom in and out of a chart without the labels moving along their respective axis

⚡Each label's text can be customized via an "input.string" code base

⚡Each level's label can be changed via a plot style setting to determine if the label is centered with it's respective level or rides along the top of it

⚡Significant figures input allows you to round price up or down

⚡A "bias EMA" tool that color codes the candles and price line to show you where price is in relation to the 21 EMA (or another value that you pick). As a result, this can be an effective visual to help reduce cognitive load

⚡A "fill level" where color is determined by price opening above or below the previous day's close

⚡A "use current close" setting that's great to use in pre-market as it shows you where price is in relation to the previous days' close

----------------------------------------------------------------------------------------------------------------------

🙏Thanks to (c)satymahajan for the inspiration behind the ATR "previous close" and "bias candle" code base

🙏Thanks to my mentor (c)SimpleCryptoLife for the libraries and extensive code to help create this indicator

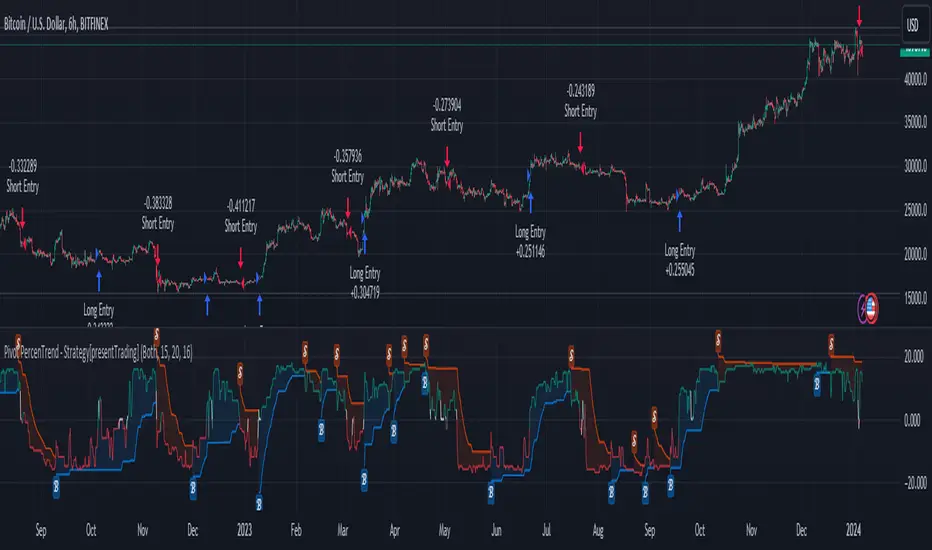

Pivot Percentile Trend - Strategy [presentTrading]

█ Introduction and How it is Different

The "Pivot Percentile Trend - Strategy" from PresentTrading represents a paradigm shift in technical trading strategies. What sets this strategy apart is its innovative use of pivot percentiles, a method that goes beyond traditional indicator-based analyses. Unlike standard strategies that might depend on single-dimensional signals, this approach takes a multi-layered view of market movements, blending percentile calculations with SuperTrend indicators for a more nuanced and dynamic market analysis.

This strategy stands out for its ability to process multiple data points across various timeframes and pivot lengths, thereby capturing a broader and more detailed picture of market trends. It's not just about following the price; it's about understanding its position in the context of recent historical highs and lows, offering a more profound insight into potential market movements.

BTC 6h L/S

Where traditional methods might react to market changes, the Pivot Percentile Trend strategy anticipates them, using a calculated approach to identify trend strengths and weaknesses. This foresight gives traders a significant advantage, allowing for more strategic decision-making and potentially increasing the chances of successful trades.

In essence, this strategy introduces a more comprehensive and proactive approach to trading, harnessing the power of advanced percentile calculations combined with the robustness of SuperTrend indicators. It's a strategy designed for traders who seek a deeper understanding of market dynamics and a more calculated approach to their trading decisions.

Local picture

█ Strategy, How It Works: Detailed Explanation

🔶 Percentile Calculations

- The strategy employs percentile calculations to assess the relative position of current market prices against historical data.

- For a set of lengths (e.g., `length * 1`, `length * 2`, up to `length * 7`), it calculates the 75th percentile for high values (`percentilesHigh`) and the 25th percentile for low values (`percentilesLow`).

- These percentiles provide a sense of where the current price stands compared to recent price ranges.

Length - 10

Length - 15

🔶 SuperTrend Indicator

- The SuperTrend indicator is a key component, providing trend direction signals.

- It uses the `currentTrendValue`, derived from the difference between bull and bear strengths calculated from the percentile data.

* used the Supertrend toolkit by @EliCobra

🔶 Trend Strength Counts

- The strategy calculates counts of bullish and bearish indicators based on comparisons between the current high and low against high and low percentiles.

- `countBull` and `countBear` track the number of times the current high is above the high percentiles and the current low is below the low percentiles, respectively.

- Weak bullish (`weakBullCount`) and bearish (`weakBearCount`) counts are also determined by how often the current lows and highs fall within the percentile range.

*The idea of this strength counts mainly comes from 'Trend Strength Over Time' @federalTacos5392b

🔶 Trend Value Calculation

- The `currentTrendValue` is a crucial metric, computed as `bullStrength - bearStrength`.

- It indicates the market's trend direction, where a positive value suggests a bullish trend and a negative value indicates a bearish trend.

🔶 Trade Entry and Exit Logic

- The entry points for trades are determined by the combination of the trend value and the direction indicated by the SuperTrend indicator.

- For a long entry (`shouldEnterLong`), the `currentTrendValue` must be positive and the SuperTrend indicator should show a downtrend.

- Conversely, for a short entry (`shouldEnterShort`), the `currentTrendValue` should be negative with the SuperTrend indicating an uptrend.

- The strategy closes positions when these conditions reverse.

█ Trade Direction

The strategy is versatile, allowing traders to choose their preferred trading direction: long, short, or both. This flexibility enables traders to tailor their strategies to their market outlook and risk appetite.

█ Default Settings and Customization

1. Trade Direction: Selectable as Long, Short, or Both, affecting the type of trades executed.

2. Indicator Source: Pivot Percentile Calculations, key for identifying market trends and reversals.

3. Lengths for Percentile Calculation: Various configurable lengths, influencing the scope of trend analysis.

4. SuperTrend Settings: ATR Length 20, Multiplier 18, affecting indicator sensitivity and trend detection.

5. Style Options: Custom colors for bullish (green) and bearish (red) trends, aiding visual interpretation.

6. Additional Settings: Includes contrarian signals and UI enhancements, offering strategic and visual flexibility.

Order Blocks | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Volumized Order Blocks indicator! This new indicator can render order blocks with their volumetric information. It's highly customizable with detection, invalidation and style settings.

Features of the new Volumized Order Blocks indicator :

Render Bullish & Bearish Order Blocks

Enable / Disable Volumetric Information

Enable / Disable Historic Zones

Visual Customizability

📌 HOW DOES IT WORK ?

Order blocks occur when there is a high amount of market orders exist on a price range. It is possible to find order blocks using specific formations on the chart.

The high & low volume of order blocks should be taken into consideration while determining their strengths. The determination of the high & low volume of order blocks are similar to FVGs, in a bullish order block, the high volume is the last 2 bars' total volume, while the low volume is the oldest bar's volume. In a bearish order block scenario, the low volume becomes the last 2 bars' total volume.

🚩UNIQUENESS

The ability to render the total volume of Order Blocks as well as bullish / bearish volume ratio is what sets this Order Block indicator apart from others. Also the ability to combine overlapping Order Block zones will result in cleaner charts for traders.

⚙️SETTINGS

1. General Configuration

Volumetric Info -> The volumetric information of the Order Blocks will be rendered if activated.

Zone Invalidation -> Select between Wick & Close price for Order Block Invalidation.

Swing Length -> Swing length is used when finding order block formations. Smaller values will result in finding smaller order blocks.

Breaker Blocks | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Volumized Breaker Blocks indicator! This new indicator can render breaker blocks with their volumetric information. It's highly customizable with detection, invalidation and style settings.

Features of the new Volumized Breaker Block indicator :

Render Bullish & Bearish Breaker Blocks

Enable / Disable Volumetric Information

Enable / Disable Historic Zones

Visual Customizability

📌 HOW DOES IT WORK ?

Breaker blocks form when an order block fails, or "breaks". It is often associated with market going in the opposite direction of the broken order block, and they can be spotted by following order blocks and finding the point they get broken, ie. price goes below a bullish order block.

The volume of a breaker block is simply the total volume of the bar that the original order block is broken.

🚩UNIQUENESS

This indicator can not only detect breaker blocks, but it can also detect them with their volumetric information. Volumetric information can be crucial when considering an breaker block's strength, which can be a crucial form of confluence in certain trading strategies.

⚙️SETTINGS

1. General Configuration

Volumetric Info -> The volumetric information of the Breaker Blocks will be rendered if activated.

Zone Invalidation -> Select between Wick & Close price for Breaker Block Invalidation.

Swing Length -> Swing length is used when finding breaker block formations. Smaller values will result in finding smaller breaker blocks.

Trend Lines, Supports and Resistances█ OVERVIEW

This is a simple script that draws trend lines, supports and resistances based on the highs and lows of pivots and is developed solely for practice purposes while learning the Pine Script language.

█ FEATURES:

Ability to change pivot length and mark pivots on chart.

Ability to change amount of pivot points that used to generate trend lines or support and resistances.

Ability to set exception for last "n" bars for breaks.

Ability to set exception up to "n" times for breaks.

Ability to see broken trend lines as ghosts.

Ability to set alarms for breaks.

Ability to change colors and line widths.

And many more...

█ DISCLAIMER:

Trading is risky and most of the day traders lose money eventually. This indicator is only for educational purposes and should not be construed as financial advice. Past performances does not guarantee future results.

VWAP RangeThe VWAP Range indicator is a highly versatile and innovative tool designed with trading signals for trading the supply and demand within consolidation ranges.

What's a VWAP?

A VWAP (Volume Weighted Average Price) represents an equilibrium point in the market, balancing supply and demand over a specified period. Unlike simple moving averages, VWAP gives more weight to periods with higher volume. This is crucial because large volumes indicate significant trading activity, often by institutional traders, whose actions can reflect deeper market insights or create substantial market movements. The VWAP is also often used as a benchmark to evaluate the efficiency of executed trades. If a trader buys below the VWAP and sells above it, they are generally considered to have transacted favourably.

This is how it works:

Multiple VWAP Anchors:

This indicator uses multiple VWAPs anchored to different optional time periods, such as Daily, Weekly, Monthly, as well as to the highest high a lowest low within those periods. This multiplicity allows for a comprehensive view of the market’s average price based on volume and price, tailored to different trading styles and strategies.

Dynamic and Fixed Periods:

Traders can choose between using dynamic ranges, which reset at the start of each selected period, and specifying a date and time for a particular fixed range to trade. This flexibility is crucial for analyzing price movements within specific ranges or market phases.

Fixed ranges allow VWAPs to be calculated and anchored to a significant market event, the beginning of a consolidation phase or after a major news announcement.

Signal Generation:

The indicator generates buy and sell signals based on the relationship of the price to the VWAPs. It also allows for setting a maximum number of signals in one direction to avoid overtrading or pyramiding. Be sure to wait for the candle close before trading on the signals.

Average Buy/Sell Signal Lines:

Lines can be plotted to display the average buy and sell signal prices. The difference between the lines shows the average profit per trade when trading on the signals in that range. It's a good way to see how profitable a range is on average without backtesting the signals. The lines will also often turn into support and resistance areas, similar to value areas in a volume profile.

Customizable Settings:

Traders have control over various settings, such as the VWAP calculation method and bar color. There are also tooltips for every function.

Hidden Feature:

There's a subtle feature in this indicator: if you have 'Indicator values' turned on in TradingView, you'll see a Sell/Buy Ratio displayed only in the status line. This ratio indicates whether there are more sell signals than buy signals in a range, regardless of the Max Signals setting. A red value above 1 suggests that the market is trending upward, indicating you might want to hold your long positions a bit longer. Conversely, a green value below 1 implies a downward trend.

Catching Trend Reversals by shorting tops and buying bottomsHOLP (High of the low period) and LOHP (Low of the high period)

Catching Trend Reversals by shorting tops and buying bottoms

using this Swing High/Low Indicator

Trading Strategy comes from Mastering the Trade, by John Carter pg 300.

Trading Rules for Sells, Buys are reversed

1. Identifying a trending market, where today's price is making a 20-day high (17-18 day highs are also fine)

Note this is configurable by setting the trending period variable (defaults to 20)

For example if price is making a 20 period high or 20 period low, it will show a triangle up/down above the candle.

2. Identify the high bar in the uptrend

3. Go short once the price action closes below the low of this high bar

4. The initial stop is the high of the high bar.

5. If you are in the trade on the third day or period, use a 2 bar trailing stop.

You can check 2-bar trailing stop to draw the line, defaults to off.

Stop is indicated by the white dot.

Code Converted from TradeStation EasyLanguage

I can't find the original source anymore for the swing high/low plots, but if someone knows,

let me know and I'll credit here.

Fair Value Gaps (Volumetric) | Flux Charts💎 GENERAL OVERVIEW

Introducing a brand new Fair Value Gaps (FVG) indicator, now with Volumetric Zones! You can now see the total volume of FVG zones, as well as their bullish & bearish volume ratio.

Features of the Volumetric FVG Indicator :

Render Bullish / Bearish FVG Zones

See Total Volume Of The FVG Zones

See The Ratio Of Bullish / Bearish Bar Volume Of FVG Zones

Combination Of Overlapping FVG Zones

Variety Of Zone Detection/ Sensitivity / Filtering / Invalidation Settings

High Customizability

🚩UNIQUENESS

The ability to render the total volume of FVGs as well as bullish / bearish volume ratio is what sets this FVG indicator apart from others. Also the ability to combine overlapping FVG zones will result in cleaner charts for traders.

⚙️SETTINGS

1. General Configuration

Zone Invalidation -> Select between Wick & Close price for FVG Zone Invalidation.

Zone Filtering -> With "Average Range" selected, algorithm will find FVG zones in comparison with average range of last bars in the chart. With the "Volume Threshold" option, you may select a Volume Threshold % to spot FVGs with a larger total volume than average.

FVG Detection -> With the "Same Type" option, all 3 bars that formed the FVG should be the same type. (Bullish / Bearish). If the "All" option is selected, bar types may vary between Bullish / Bearish.

Detection Sensitivity -> You may select between Low, Normal or High FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivities resulting in spotting bigger FVGs, and higher sensitivities resulting in spotting all sizes of FVGs.

Show Historic Zones -> If this option is on, the indicator will render invalidated FVG zones as well as current FVG zones. For a cleaner look at current FVG zones which are not invalidated yet, you can turn this option off.

Re-Anchoring Fibo LevelsThe " Re-Anchoring Fibo Levels " offers a dynamic and systematic approach on how to use Fibonacci retracements. The resistance levels are based on the all-time high and the subsequent lowest low. The support levels are based on the lowest low after the all-time high and the following highest high. This method provides traders with automatically updated support and resistance levels based on current significant pivot points.

How It Works

Resistance Levels: The levels are calculated based on the current all-time high and the following lowest low. This range is multiplied with the defined Fibonacci ratios and the levels are plotted.

Support Levels: The support levels are calculated based on the lowest low and highest high after and below the current all-time high. The range between those to pivot points is multiplied with the defined Fibonacci ratios and the levels are plotted.

How To Use

By comparing current prices to dynamically adjusted Fibonacci levels, traders can gain insights into the strength and potential direction of market trends and are also presented with potentially significant levels that can function either as resistance or support.

Support and Resistance (MTF) | Flux Charts💎 GENERAL OVERVIEW

Introducing a groundbreaking support and resistance indicator designed to revolutionize your trading experience on TradingView! This innovative tool operates across three distinct timeframes, offering a comprehensive view of market dynamics to help you make informed trading decisions.

The indicator offers a large variety of features :

Select Up To 3 Timeframes

Select Strength Of Supports & Resistances

Select Between Zones & Lines

Show Breaks & Restests

Break & Retest Alerts

Avoid False Breaks

Inverse Color After Broken

Expand Lines & Zones

🚩UNIQUENESS

What sets this indicator apart is its ability to seamlessly integrate and analyze support and resistance levels across multiple timeframes simultaneously. By combining data from three different timeframes, this indicator provides a holistic perspective on market trends and key levels. The adaptive nature of this tool ensures a dynamic assessment of support and resistance zones, empowering traders to adapt to changing market conditions efficiently.

⚙️SETTINGS

1. General Configration

Support & Resistance Count -> Select between 1-3 support & resistance zones for each timeframe.

Pivot Range -> The pivot range is taken into calculations when finding high & low pivots in the chart. Increase if you need a more general look at the support & support zones, or decrease if you need a more detailed look.

Strength -> The strength of the support & resistance zones are determined by how many times the price touched the zone in the past. You can increase the strength up to 4.

Expand Lines & Zones -> If enabled, the support & resistance zones will be expanded to both left and right infinitely. If disabled, the support & resistance zones will be clamped between the time they are first seen, and the time they become broken.

2. Support & Resistance Zones

Enable Zones -> The support & resitsance lines will be converted to zones if enabled.

Zone Width -> The width of the zones. 1 -> %0.05, 2 -> %0.06, 3 -> %0.075.

3. Timeframes

Enable & Disable up to 3 different timeframes using the checkboxes. You can set the timeframes using the selectboxes.

4. Breaks & Retests

Show Breaks -> Points the break points with a blue label with the text "B" on it.

Show Retests -> Points the times when the support & resistance zones are being retested in the current chart.

Avoid False Breaks -> If enabled, the algorithm will try to avoid false break points by comparing the average volume of the point to a longer average volume.

Break Volume Threshold % -> If "Avoid False Breaks" option is enabled, the average volume of the break point should surpass the general average volume by this percent. Higher values mean it's less likely to be a break.

Inverse Color After Broken -> As broken support & resistance zones often become resistance & support zones respectively, if you enable this option the broken zones will inverse their color.

5. Alerts

To make the alerts work, you'll need to add an alert to the chart using the TradingView® alert feature.

Enable Retest Alerts -> You will receive alerts when restests happen on any of the support & resistance zones. "Show Retests" option needs to be enabled to get alerts of this category.

Enable Break Alerts -> You will receive alerts when breaks happen on any of the support & resistance zones.

CT - Candle TrendHighlight candle tails in a trend in order to find previous area of resistance or support.

Recommended for D, W or higher timeframes.

Machine Learning: STDEV Oscillator [YinYangAlgorithms]This Indicator aims to fill a gap within traditional Standard Deviation Analysis. Rather than its usual applications, this Indicator focuses on applying Standard Deviation within an Oscillator and likewise applying a Machine Learning approach to it. By doing so, we may hope to achieve an Adaptive Oscillator which can help display when the price is deviating from its standard movement. This Indicator may help display both when the price is Overbought or Underbought, and likewise, where the price may face Support and Resistance. The reason for this is that rather than simply plotting a Machine Learning Standard Deviation (STDEV), we instead create a High and a Low variant of STDEV, and then use its Highest and Lowest values calculated within another Deviation to create Deviation Zones. These zones may help to display these Support and Resistance locations; and likewise may help to show if the price is Overbought or Oversold based on its placement within these zones. This Oscillator may also help display Momentum when the High and/or Low STDEV crosses the midline (0). Lastly, this Oscillator may also be useful for seeing the spacing between the High and Low of the STDEV; large spacing may represent volatility within the STDEV which may be helpful for seeing when there is Momentum in the form of volatility.

Tutorial:

Above is an example of how this Indicator looks on BTC/USDT 1 Day. As you may see, when the price has parabolic movement, so does the STDEV. This is due to this price movement deviating from the mean of the data. Therefore when these parabolic movements occur, we create the Deviation Zones accordingly, in hopes that it may help to project future Support and Resistance locations as well as helping to display when the price is Overbought and Oversold.

If we zoom in a little bit, you may notice that the Support Zone (Blue) is smaller than the Resistance Zone (Orange). This is simply because during the last Bull Market there was more parabolic price deviation than there was during the Bear Market. You may see this if you refer to their values; the Resistance Zone goes to ~18k whereas the Support Zone is ~10.5k. This is completely normal and the way it is supposed to work. Due to the nature of how STDEV works, this Oscillator doesn’t use a 1:1 ratio and instead can develop and expand as exponential price action occurs.

The Neutral (0) line may also act as a Support and Resistance location. In the example above we can see how when the STDEV is below it, it acts as Resistance; and when it’s above it, it acts as Support.

This Neutral line may also provide us with insight as towards the momentum within the market and when it has shifted. When the STDEV is below the Neutral line, the market may be considered Bearish. When the STDEV is above the Neutral line, the market may be considered Bullish.

The Red Line represents the STDEV’s High and the Green Line represents the STDEV’s Low. When the STDEV’s High and Low get tight and close together, this may represent there is currently Low Volatility in the market. Low Volatility may cause consolidation to occur, however it also leaves room for expansion.

However, when the STDEV’s High and Low are quite spaced apart, this may represent High levels of Volatility in the market. This may mean the market is more prone to parabolic movements and expansion.

We will conclude our Tutorial here. Hopefully this has given you some insight into how applying Machine Learning to a High and Low STDEV then creating Deviation Zones based on it may help project when the Momentum of the Market is Bullish or Bearish; likewise when the price is Overbought or Oversold; and lastly where the price may face Support and Resistance in the form of STDEV.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Adaptive MFT Extremum Pivots [Elysian_Mind]Adaptive MFT Extremum Pivots

Overview:

The Adaptive MFT Extremum Pivots indicator, developed by Elysian_Mind, is a powerful Pine Script tool that dynamically displays key market levels, including Monthly Highs/Lows, Weekly Extremums, Pivot Points, and dynamic Resistances/Supports. The term "dynamic" emphasizes the adaptive nature of the calculated levels, ensuring they reflect real-time market conditions. I thank Zandalin for the excellent table design.

---

Chart Explanation:

The table, a visual output of the script, is conveniently positioned in the bottom right corner of the screen, showcasing the indicator's dynamic results. The configuration block, elucidated in the documentation, empowers users to customize the display position. The default placement is at the bottom right, exemplified in the accompanying chart.

The deliberate design ensures that the table does not obscure the candlesticks, with traders commonly situating it outside the candle area. However, the flexibility exists to overlay the table onto the candles. Thanks to transparent cells, the underlying chart remains visible even with the table displayed atop.

In the initial column of the table, users will find labels for the monthly high and low, accompanied by their respective numerical values. The default precision for these values is set at #.###, yet this can be adjusted within the configuration block to suit markets with varying degrees of volatility.

Mirroring this layout, the last column of the table presents the weekly high and low data. This arrangement is part of the upper half of the table. Transitioning to the lower half, users encounter the resistance levels in the first column and the support levels in the last column.

At the center of the table, prominently displayed, is the monthly pivot point. For a comprehensive understanding of the calculations governing these values, users can refer to the documentation. Importantly, users retain the freedom to modify these mathematical calculations, with the table seamlessly updating to reflect any adjustments made.

Noteworthy is the table's persistence; it continues to display reliably even if users choose to customize the mathematical calculations, providing a consistent and adaptable tool for informed decision-making in trading.

This detailed breakdown offers traders a clear guide to interpreting the information presented by the table, ensuring optimal use and understanding of the Adaptive MFT Extremum Pivots indicator.

---

Usage:

Table Layout:

The table is a crucial component of this indicator, providing a structured representation of various market levels. Color-coded cells enhance readability, with blue indicating key levels and a semi-transparent background to maintain chart visibility.

1. Utilizing a Table for Enhanced Visibility:

In presenting this wealth of information, the indicator employs a table format beneath the chart. The use of a table is deliberate and offers several advantages:

2. Structured Organization:

The table organizes the diverse data into a structured format, enhancing clarity and making it easier for traders to locate specific information.

3. Concise Presentation:

A table allows for the concise presentation of multiple data points without cluttering the main chart. Traders can quickly reference key levels without distraction.

4. Dynamic Visibility:

As the market dynamically evolves, the table seamlessly updates in real-time, ensuring that the most relevant information is readily visible without obstructing the candlestick chart.

5. Color Coding for Readability:

Color-coded cells in the table not only add visual appeal but also serve a functional purpose by improving readability. Key levels are easily distinguishable, contributing to efficient analysis.

Data Values:

Numerical values for each level are displayed in their respective cells, with precision defined by the iPrecision configuration parameter.

Configuration:

// User configuration: You can modify this part without code understanding

// Table location configuration

// Position: Table

const string iPosition = position.bottom_right

// Width: Table borders

const int iBorderWidth = 1

// Color configuration

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

// Color: Characters

const color iCharColor = color.white

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

// Precision: Numerical data

const int iPrecision = 3

// End of configuration

The code includes a configuration block where users can customize the following parameters:

Precision of Numerical Table Data (iPrecision):

// Precision: Numerical data

const int iPrecision = 3

This parameter (iPrecision) sets the precision of the numerical values displayed in the table. The default value is 3, displaying numbers in #.### format.

Position of the Table (iPosition):

// Position: Table

const string iPosition = position.bottom_right

This parameter (iPosition) sets the position of the table on the chart. The default is position.bottom_right.

Color preferences

Table borders (iBorderColor):

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

This parameters (iBorderColor) sets the color of the borders everywhere within the window.

Table Background (iTableColor):

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

This is the background color of the table. If you've got cells without custom background color, this color will be their background.

Title Cell Background (iTitleCellColor):

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

This is the background color the title cells. You can set the background of data cells and text color elsewhere.

Text (iCharColor):

// Color: Characters

const color iCharColor = color.white

This is the color of the text - titles and data - within the table window. If you change any of the background colors, you might want to change this parameter to ensure visibility.

Data Cell Background: (iDataCellColor):

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

The data cells have a background color to differ from title cells. You can configure this is a different parameter (iDataColor). You might even set the same color for data as for the titles if you will.

---

Mathematical Background:

Monthly and Weekly Extremums:

The indicator calculates the High (H) and Low (L) of the previous month and week, ensuring accurate representation of these key levels.

Standard Monthly Pivot Point:

The standard pivot point is determined based on the previous month's data using the formula:

PivotPoint = (PrevMonthHigh + PrevMonthLow + Close ) / 3

Monthly Pivot Points (R1, R2, R3, S1, S2, S3):

Additional pivot points are calculated for Resistances (R) and Supports (S) using the monthly data:

R1 = 2 * PivotPoint - PrevMonthLow

S1 = 2 * PivotPoint - PrevMonthHigh

R2 = PivotPoint + (PrevMonthHigh - PrevMonthLow)

S2 = PivotPoint - (PrevMonthHigh - PrevMonthLow)

R3 = PrevMonthHigh + 2 * (PivotPoint - PrevMonthLow)

S3 = PrevMonthLow - 2 * (PrevMonthHigh - PivotPoint)

---

Code Explanation and Interpretation:

The table displayed beneath the chart provides the following information:

Monthly Extremums:

(H) High of the previous month

(L) Low of the previous month

// Function to get the high and low of the previous month

getPrevMonthHighLow() =>

var float prevMonthHigh = na

var float prevMonthLow = na

monthChanged = month(time) != month(time )

if (monthChanged)

prevMonthHigh := high

prevMonthLow := low

Weekly Extremums:

(H) High of the previous week

(L) Low of the previous week

// Function to get the high and low of the previous week

getPrevWeekHighLow() =>

var float prevWeekHigh = na

var float prevWeekLow = na

weekChanged = weekofyear(time) != weekofyear(time )

if (weekChanged)

prevWeekHigh := high

prevWeekLow := low

Monthly Pivots:

Pivot: Standard pivot point based on the previous month's data

// Function to calculate the standard pivot point based on the previous month's data

getStandardPivotPoint() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

Resistances:

R3, R2, R1: Monthly resistance levels

// Function to calculate additional pivot points based on the monthly data

getMonthlyPivotPoints() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

r1 = (2 * pivotPoint) - prevMonthLow

s1 = (2 * pivotPoint) - prevMonthHigh

r2 = pivotPoint + (prevMonthHigh - prevMonthLow)

s2 = pivotPoint - (prevMonthHigh - prevMonthLow)

r3 = prevMonthHigh + 2 * (pivotPoint - prevMonthLow)

s3 = prevMonthLow - 2 * (prevMonthHigh - pivotPoint)

Initializing and Populating the Table:

The myTable variable initializes the table with a blue background, and subsequent table.cell functions populate the table with headers and data.

// Initialize the table with adjusted bgcolor

var myTable = table.new(position = iPosition, columns = 5, rows = 10, bgcolor = color.new(color.blue, 90), border_width = 1, border_color = color.new(color.blue, 70))

Dynamic Data Population:

Data is dynamically populated in the table using the calculated values for Monthly Extremums, Weekly Extremums, Monthly Pivot Points, Resistances, and Supports.

// Add rows dynamically with data

= getPrevMonthHighLow()

= getPrevWeekHighLow()

= getMonthlyPivotPoints()

---

Conclusion:

The Adaptive MFT Extremum Pivots indicator offers traders a detailed and clear representation of critical market levels, empowering them to make informed decisions. However, users should carefully analyze the market and consider their individual risk tolerance before making any trading decisions. The indicator's disclaimer emphasizes that it is not investment advice, and the author and script provider are not responsible for any financial losses incurred.

---

Disclaimer:

This indicator is not investment advice. Trading decisions should be made based on a careful analysis of the market and individual risk tolerance. The author and script provider are not responsible for any financial losses incurred.

Kind regards,

Ely

Renko Box Chart Overlay by BDThis is Renko chart overlay for Candles chart. You can use it to identify market direction and potential key points.

To use it simply select box size and any timeframe you want.

With this overlay you can be sure that you'll see every brick on a chart showing general market direction with all the details of a candles chart.

Alternatives Renko overlay charts:

If you don't have access to 1s timeframe or you don't want to use low TF here is the situation with built in Renko chart on 5m TF:

This Renko boxes are linked to chart by time(candle) and price. It will draw a box even if price didn't close above(or below) of box level:

But be careful when setting box size too small because it will produce bad results:

The issue is known and I'll work on fixing it in next update, for now use box size at least the size of a body of a candle, after all renko is for general market movement and not for marking up every tick.

Let me know if you want to see any additions.

Price Cross Time Custom Range Interactive█ OVERVIEW

This indicator was a time-based indicator and intended as educational purpose only based on pine script v5 functions for ta.cross() , ta.crossover() and ta.crossunder() .

I realised that there is some overlap price with the cross functions, hence I integrate them into Custom Range Interactive with value variance and overlap displayed into table.

This was my submission for Pinefest #1 , I decided to share this as public, I may accidentally delete this as long as i keep as private.

█ INSPIRATION

Inspired by design, code and usage of CAGR. Basic usage of custom range / interactive, pretty much explained here . Credits to TradingView.

█ FEATURES

1. Custom Range Interactive

2. Label can be resize and change color.

3. Label show tooltip for price and time.

4. Label can be offset to improve readability.

5. Table can show price variance when any cross is true.

6. Table can show overlap if found crosss is overlap either with crossover and crossunder.

7. Table text color automatically change based on chart background (light / dark mode).

8. Source 2 is drawn as straight line, while Source 1 will draw as label either above line for crossover, below line for crossunder and marked 'X' if crossing with Source 2's line.

9. Cross 'X' label can be offset to improve readability.

10. Both Source 1 and Source 2 can select Open, Close, High and Low, which can be displayed into table.

█ LIMITATIONS

1. Table is limited to intraday timeframe only as time format is not accurate for daily timeframe and above. Example daily timeframe will give result less 1 day from actual date.

2. I did not include other sources such external source or any built in sources such as hl2, hlc3, ohlc4 and hlcc4.

█ CODE EXPLAINATION

I pretty much create custom function with method which returns tuple value.

method crossVariant(float price = na, chart.point ref = na) =>

cross = ta.cross( price, ref.price)

over = ta.crossover( price, ref.price)

under = ta.crossunder(price, ref.price)

Unfortunately, I unable make the labels into array which i plan to return string value by getting the text value from array label, hence i use label.all and add incremental int value as reference.

series label labelCross = na, labelCross.delete()

var int num = 0

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

I realised cross value can be overlap with crossover and crossunder, hence I add bool to enable force overlap and add additional bools.

series label labelCross = na, labelCross.delete()

var int num = 0

if forceOverlap

if over

num += 1

labelCross := label.new()

if under

num += 1

labelCross := label.new()

if cross

num += 1

labelCross := label.new()

else

if cross and over

num += 1

labelCross := label.new()

if cross and under

num += 1

labelCross := label.new()

if cross and not over and not under

num += 1

labelCross := label.new()

█ USAGE / EXAMPLES

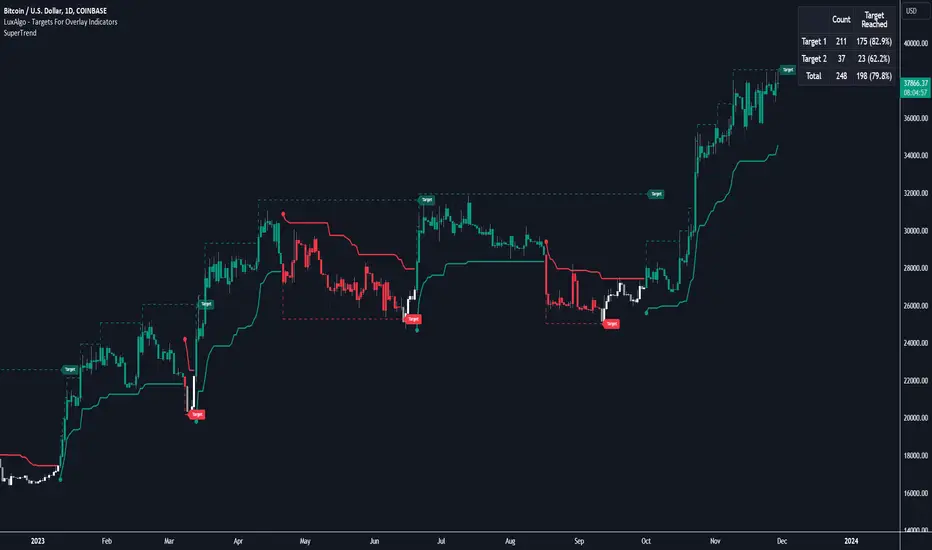

Targets For Overlay Indicators [LuxAlgo]The Targets For Overlay Indicators is a useful utility tool able to display targets during crossings made between the price and external indicators on the user chart. Users can display a series of two targets, one for crossover events and another one for crossunder event.

Alerts are included for the occurrence of a new target as well as for reached targets.

🔶 USAGE

In order for targets to be displayed users need to select an appropriate input source from the "Source" drop-down input setting. In the example above we apply the indicator to a volatility stop.

This can also easily be done by adding the "Targets For Overlay Indicators" script on the VStop indicator directly.

Targets can help users determine the price limit where the price might start deviating from an indication given by one or multiple indicators. In the context of trading, targets can help secure profits/reduce losses of a trade, as such this tool can be useful to evaluate/determine user take profits/stop losses.

Due to these essentially being horizontal levels, they can also serve as potential support/resistances, with breakouts potentially confirming new trends.

Users might be interested in obtaining new targets once one is reached, this can be done by enabling "New Target When Reached" in the target logic setting section, resulting in more frequent targets.

Lastly, users can restrict new target creation until current ones are reached. This can result in fewer and longer-term targets, with a higher reach rate.

🔹 Examples

The indicator can be applied to many overlay indicators that naturally produce crosses with the price, such as moving average, trailing stops, bands...etc.

Users can use trailing stops such as the SuperTrend or VStop to more easily create clean targets. Do note that certain SuperTrend scripts separate the upper and lower extremities of the SuperTrend into two different plot, which cannot be used with this tool, you may use the provided SuperTrend script below to have a compatible version with our tool:

//@version=5

indicator("SuperTrend", overlay = true)

factor = input.float(3, 'Factor', minval = 0)

atrLen = input.int(10, 'ATR Length', minval = 1)

= ta.supertrend(factor, atrLen)

plot(spt, 'SuperTrend', dir != dir ? na : dir < 0 ? #089981 : #f23645, 2)

plot(spt, 'Circles', dir > dir ? #f23645 : dir < dir ? #089981 : na, 3, plot.style_circles)

Using moving averages can produce more targets than other overlay indicators.

Users can apply the tool twice when using bands or any overlay indicator returning two outputs, using crossover targets for obtaining targets using the upper band as source and crossunder targets for targets using the lower band. We can also use the Trendlines with breaks indicator as example:

🔹 Dashboard

A dashboard is displayed on the top right of the chart, displaying the amount, reach rate of targets 1/2, and total amount.

This dashboard can be useful to evaluate the selected target distances relative to the selected conditions, with a higher reach rate suggesting the distance of the targets from the price allows them to be reached.

🔶 SETTINGS

Source: Indicator source used to create targets. Targets are created when the closing price crosses the specified source.

Show Target Labels: Display target labels on the chart.

Candle Coloring: Apply candle coloring based on the most recent active target.

🔹 Target

Crossover and Crossunder targets use the same settings below:

Show Target: Determines if the target is displayed or not.

Above Price Target: If selected, will create targets above the closing price.

Wait Until Reached: When enabled will not create a new target until an existing one is reached.

New Target When Reached: Will create a new target when an existing one is reached.

Evaluate Wicks: Will use high/low prices to determine if a target is reached. Unselecting this setting will use the closing price.

Target Distance From Price: Controls the distance of a target from the price. Can be determined in currencies/points, percentages, ATR multiples, or ticks.

Opening Range & Prior Day High/Low [Gorb]Introduction:

Opening Range & Prior Day High/Low indicator is an easy to use day traders tool. This indicator automatically plots the previous days high and low, as well as drawing a box from the opening range that the user specifies in the settings. These two together can help provide an indication of market sentiment and price trends for the day. They are often used as a trading strategy for day traders.

Overview:

The Opening Range , draws a box from the high to the low of the user defined time period and is extended until the end of the trading session. Most common are the 5/15/30min opening ranges.

Prior Day High/Low , draws lines from the previous days high and low that extend across the current session. These are used as support/resistance and also a marker to see market sentiment by crossing one of these levels.

The indicator is designed for all kinds of traders, offering a simple approach to automatically plot levels for you.

Features:

All skill-level friendly presets, easy to enable with one-click

Opening Range: Allows user to choose what time the range starts and ends to measure the high & low.

Extend Range Lines: allows the user to choose when the box stops extending according to the trading session time.

Enable Opening Range Box: allows the user to choose to plot the opening range or not.

ORB Border Color: allows the user to change the box border color.

ORB Box Shade Color: allows the user to change the background of the opening range box.

ORB Line Width: allows users to chose the width of the opening range box lines.

Enable Previous Day High: allows users to enable the previous days high to be plotted.

Enable Previous Day Low: allows users to enable the previous days high to be plotted.

Previous Day High Color: allows users to choose the color for this line.

Previous Day Low Color: allows users to choose the color for this line.

All colors are changeable for the user to customize to their liking.

Usage Demonstration

In the image below, we can see a basic example of how these 3 features function.

As explained above, the opening range is customizable to meet the users needs and can be disabled with one click. Same goes for the prior day high(green) and low(red) lines. All 3 are plotted each day automatically for the user if enabled.

In the image below, we can see an example of using the opening range break and prior day high together for a trading strategy.

This is a great example of using the prior day high with the opening range to use as a day trading strategy. It provides the trader with levels to watch for price to break out from for possible trade setups.

In this next image, we can see a failed breakdown from the opening range that results in a bullish breakout.

The first move was a fake breakdown with the failed rejection on the retest of the opening range lows. This led to a breakout above the range and a confirmation bounce on the breakout retest. Price did break above the prior day high and confirmed with a retest bounce on that level as well.

In the image below, we can see how previous days levels can act as resistance to use with the opening range.

Price didn't reject the opening range low, but it did reject the prior day high for the second time. This could be used as an entry or once price breaks down out of the opening range again.

Conclusion:

We believe in providing user-friendly tools to help speed up traders technical analysis and implement easy trading strategies. The goal is to provide a user-friendly indicator to automatically draw opening ranges and previous days levels to suit the users needs and trading style.

RISK DISCLAIMER

All content, tools, scripts & education provided by Monstanzer or Gorb Algo LLC are for informational & educational purposes only. Trading is risk and most lose their money, past performance does not guarantee future results.

OHLC BreakThis indicator shows the Support and Resistance zones in a different way with Boxes that extend to the right and show the candle that has broken a minimum number of High or Low

The user has the possibility to:

- Choose to show High or Low levels not yet broken

- Shows candles that have broken a total of high or Low that you pre-set

- Choose to show a Box on candles that have broken the minimum of the preset levels

- Choose to show the total of broken levels with a Label on the candle

The indicator should be used as OHLC shows in its concepts, it can also be implemented to your Support and Resistance strategies, it can be implemented to Sessions strategies as in the Example

Below I show various examples on how to set the indicator for show High or Low levels not yet broken

If something is not clear, comment below and I will reply as soon as possible.

Donchian Trend SignalsThe Donchian Trend Signals is an indicator developed to help traders identify the current trend direction and potential liquidity grabs.

The usage of the indicator is very simple, on the chart you'll see a modified version of the classic and popular Donchian channel, calculated using the closing prices, that changes the color of the average middle line to indicate the direction of the current trend. The indicator also colors the candlestick.

Using the option "Complex Mode" will give your indicator additional data by changing the calculation method. These changes make the lines become the average between different lengths of the same Donchian channel formula.

Additionally, the indicator plots on the chart some buy or sell signals, displayed as diamonds above or below the candles. The signals are calculated to find potential liquidity grabs using the wicks, the true range of the candles, and the volume compared to his average value.

Savage MorningMade for those Savage morning where you need to plot your values quicker.

The following section defines several input variables with default values that can be configured by the user:

resistance, weak_resistance, support, weak_support, gap_price, gap_price2, last_close, key_price, key_price1, key_price2, key_price3: These variables represent various price levels such as resistance, support, gap prices, and key levels. Users can input their own values for these levels when adding the indicator to their chart.

Next, there are boolean input variables that control the visibility of each line:

show_res, show_weak_res, show_sup, show_weak_sup, show_gap, show_gap2, show_last_close, show_key, show_key1, show_key2, show_key3: These variables allow users to choose which lines should be displayed on the chart by toggling them on or off.

Following that, there are multiple plot statements. These statements create plot series for each line that may be displayed on the chart. The plot function determines the value to be plotted based on the user's input and the visibility settings:

plot_res, plot_weak_res, plot_sup, plot_weak_sup, plot_gap, plot_gap2, plot_last_close, plot_key, plot_key1, plot_key2, plot_key3: These variables store the values to be plotted for the respective lines based on the user's input and visibility settings.

After defining the plot series, there are multiple plot statements that actually plot the lines on the chart. Each line has its own color and title specified.

Finally, labels are added on the right side of the lines to provide additional information. The label.new function is used to create labels for each line, displaying their names ("Res," "Weak Res," "Sup," etc.) at the corresponding price levels on the chart.

In summary, this Pine Script code creates a custom indicator named "Savage Morning" that allows users to input various price levels and choose which of these levels should be displayed on their chart. It plots these levels as lines with different colors and labels them for easy identification on the chart. The indicator is designed to help traders visualize important price levels and gaps that they have determined for themselves and make it easier for them to plot or change their own levels.

Smooth Trail V2Please, enjoy your new game-changing tradingview indicator, may I present to you: the Smooth Trail (second version), with an updated script and open source script to let anyone use it freely.

The Smooth Trail is an indicator that works just like a super trend, but it has a completely different usage and potential.

The super trend works by following the price and displaying a line that uses the ATR to determine how far it has to be from the actual price, and many new traders like to use the indicator thanks to its easy readability and the buy-sell signals that it shows, unfortunately, this is not the best usage of the indicator and it often leads to losing money on the markets.

The main characteristic that this indicator has is that, not like the normal super trend, it follows the trend better adapting itself in the retracement phases.

The second feature that dictates the best usage of this indicator, is that it shows a zone in which to buy or sell to have the best risk-to-reward ratio.

The indicator also works as the dynamic level of support and resistance and can be used best for trend-following strategies to maximize profits.

The first input, the multiplier, is used to determine how many times the ATR has to be added or subtracted in order to plot the indicator.

The second input, the length, is used to determine how many candles the indicator and the ATR have to consider for the calculation.

The third and last input, the zone width, is used to calculate the width of the zone displayed by the indicator, and is the factor that will be multiplied by the ATR, this means that if you leave the settings as default, the zone will be 1 ATR or 34 candle width.

This indicator is great to use in confluence with other indicators or with various candlestick patterns.