Auto Volume Spread Analysis (VSA) [TANHEF]Auto Volume Spread Analysis (visible volume and spread bars auto-scaled): Understanding Market Intentions through the Interpretation of Volume and Price Movements.

All the sections below contain the same descriptions as my other indicator "Volume Spread Analysis" with the exception of 'Auto Scaling'.

█ Auto-Scaling

This indicator auto-scales spread bars to match the visible volume bars, unlike the previous "Volume Spread Analysis " version which limited the number of visible spread bars to a fixed count. The auto-scaling feature allows for easier navigation through historical data, enabling both more historical spread bars to be viewed and more historical VSA pattern labels being displayed without requiring using the bar replay tool. Please note that this indicator’s auto-scaling feature recalculates the visible bars on the chart, causing the indicator to reload whenever the chart is moved.

Auto-scaled spread bars have two display options (set via 'Spread Bars Method' setting):

Lines: a bar lookback limit of 500 bars.

Polylines: no bar lookback limit as only plotted on visible bars on chart, which uses multiple polylines are used.

█ Simple Explanation:

The Volume Spread Analysis (VSA) indicator is a comprehensive tool that helps traders identify key market patterns and trends based on volume and spread data. This indicator highlights significant VSA patterns and provides insights into market behavior through color-coded volume/spread bars and identification of bars indicating strength, weakness, and neutrality between buyers and sellers. It also includes powerful volume and spread forecasting capabilities.

█ Laws of Volume Spread Analysis (VSA):

The origin of VSA begins with Richard Wyckoff, a pivotal figure in its development. Wyckoff made significant contributions to trading theory, including the formulation of three basic laws:

The Law of Supply and Demand: This fundamental law states that supply and demand balance each other over time. High demand and low supply lead to rising prices until demand falls to a level where supply can meet it. Conversely, low demand and high supply cause prices to fall until demand increases enough to absorb the excess supply.

The Law of Cause and Effect: This law assumes that a 'cause' will result in an 'effect' proportional to the 'cause'. A strong 'cause' will lead to a strong trend (effect), while a weak 'cause' will lead to a weak trend.

The Law of Effort vs. Result: This law asserts that the result should reflect the effort exerted. In trading terms, a large volume should result in a significant price move (spread). If the spread is small, the volume should also be small. Any deviation from this pattern is considered an anomaly.

█ Volume and Spread Analysis Bars:

Display: Volume and spread bars that consist of color coded levels, with the spread bars scaled to match the volume bars. A displayable table (Legend) of bar colors and levels can give context and clarify to each volume/spread bar.

Calculation: Levels are calculated using multipliers applied to moving averages to represent key levels based on historical data: low, normal, high, ultra. This method smooths out short-term fluctuations and focuses on longer-term trends.

Low Level: Indicates reduced volatility and market interest.

Normal Level: Reflects typical market activity and volatility.

High Level: Indicates increased activity and volatility.

Ultra Level: Identifies extreme levels of activity and volatility.

This illustrates the appearance of Volume and Spread bars when scaled and plotted together:

█ Forecasting Capabilities:

Display: Forecasted volume and spread levels using predictive models.

Calculation: Volume and Spread prediction calculations differ as volume is linear and spread is non-linear.

Volume Forecast (Linear Forecasting): Predicts future volume based on current volume rate and bar time till close.

Spread Forecast (Non-Linear Dynamic Forecasting): Predicts future spread using a dynamic multiplier, less near midpoint (consolidation) and more near low or high (trending), reflecting non-linear expansion.

Moving Averages: In forecasting, moving averages utilize forecasted levels instead of actual levels to ensure the correct level is forecasted (low, normal, high, or ultra).

The following compares forecasted volume with actual resulting volume, highlighting the power of early identifying increased volume through forecasted levels:

█ VSA Patterns:

Criteria and descriptions for each VSA pattern are available as tooltips beside them within the indicator’s settings. These tooltips provide explanations of potential developments based on the volume and spread data.

Signs of Strength (🟢): Patterns indicating strong buying pressure and potential market upturns.

Down Thrust

Selling Climax

No Effort ➤ Bearish Result

Bearish Effort ➤ No Result

Inverse Down Thrust

Failed Selling Climax

Bull Outside Reversal

End of Falling Market (Bag Holder)

Pseudo Down Thrust

No Supply

Signs of Weakness (🔴): Patterns indicating strong selling pressure and potential market downturns.

Up Thrust

Buying Climax

No Effort ➤ Bullish Result

Bullish Effort ➤ No Result

Inverse Up Thrust

Failed Buying Climax

Bear Outside Reversal

End of Rising Market (Bag Seller)

Pseudo Up Thrust

No Demand

Neutral Patterns (🔵): Patterns indicating market indecision and potential for continuation or reversal.

Quiet Doji

Balanced Doji

Strong Doji

Quiet Spinning Top

Balanced Spinning Top

Strong Spinning Top

Quiet High Wave

Balanced High Wave

Strong High Wave

Consolidation

Bar Patterns (🟡): Common candlestick patterns that offer insights into market sentiment. These are required in some VSA patterns and can also be displayed independently.

Bull Pin Bar

Bear Pin Bar

Doji

Spinning Top

High Wave

Consolidation

This demonstrates the acronym and descriptive options for displaying bar patterns, with the ability to hover over text to reveal the descriptive text along with what type of pattern:

█ Alerts:

VSA Pattern Alerts: Notifications for identified VSA patterns at bar close.

Volume and Spread Alerts: Alerts for confirmed and forecasted volume/spread levels (Low, High, Ultra).

Forecasted Volume and Spread Alerts: Alerts for forecasted volume/spread levels (High, Ultra) include a minimum percent time elapsed input to reduce false early signals by ensuring sufficient bar time has passed.

█ Inputs and Settings:

Indicator Bar Color: Select color schemes for bars (Normal, Detail, Levels).

Indicator Moving Average Color: Select schemes for bars (Fill, Lines, None).

Price Bar Colors: Options to color price bars based on VSA patterns and volume levels.

Legend: Display a table of bar colors and levels for context and clarity of volume/spread bars.

Forecast: Configure forecast display and prediction details for volume and spread.

Average Multipliers: Define multipliers for different levels (Low, High, Ultra) to refine the analysis.

Moving Average: Set volume and spread moving average settings.

VSA: Select the VSA patterns to be calculated and displayed (Strength, Weakness, Neutral).

Bar Patterns: Criteria for bar patterns used in VSA (Doji, Bull Pin Bar, Bear Pin Bar, Spinning Top, Consolidation, High Wave).

Colors: Set exact colors used for indicator bars, indicator moving averages, and price bars.

More Display Options: Specify how VSA pattern text is displayed (Acronym, Descriptive), positioning, and sizes.

Alerts: Configure alerts for VSA patterns, volume, and spread levels, including forecasted levels.

█ Usage:

The Volume Spread Analysis indicator is a helpful tool for leveraging volume spread analysis to make informed trading decisions. It offers comprehensive visual and textual cues on the chart, making it easier to identify market conditions, potential reversals, and continuations. Whether analyzing historical data or forecasting future trends, this indicator provides insights into the underlying factors driving market movements.

Spread

Bitcoin Futures vs. Spot Tri-Frame - Strategy [presentTrading]Prove idea with a backtest is always true for trading.

I developed and open-sourced it as an educational material for crypto traders to understand that the futures and spot spread may be effective but not be as effective as they might think. It serves as an indicator of sentiment rather than a reliable predictor of market trends over certain periods. It is better suited for specific trading environments, which require further research.

█ Introduction and How it is Different

The "Bitcoin Futures vs. Spot Tri-Frame Strategy" utilizes three different timeframes to calculate the Z-Score of the spread between BTC futures and spot prices on Binance and OKX exchanges. The strategy executes long or short trades based on composite Z-Score conditions across the three timeframes.

The spread refers to the difference in price between BTC futures and BTC spot prices, calculated by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges.

BTCUSD 1D L/S Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Spread

The spread is the difference in price between BTC futures and BTC spot prices. The strategy calculates the spread by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges. This spread serves as the primary metric for identifying trading opportunities.

Spread = Weighted Average Futures Price - Weighted Average Spot Price

🔶 Z-Score Calculation

The Z-Score measures how many standard deviations the current spread is from its historical mean. This is calculated for each timeframe as follows:

Spread Mean_tf = SMA(Spread_tf, longTermSMA)

Spread StdDev_tf = STDEV(Spread_tf, longTermSMA)

Z-Score_tf = (Spread_tf - Spread Mean_tf) / Spread StdDev_tf

Local performance

🔶 Composite Entry Conditions

The strategy triggers long and short entries based on composite Z-Score conditions across all three timeframes:

- Long Condition: All three Z-Scores must be greater than the long entry threshold.

Long Condition = (Z-Score_tf1 > zScoreLongEntryThreshold) and (Z-Score_tf2 > zScoreLongEntryThreshold) and (Z-Score_tf3 > zScoreLongEntryThreshold)

- Short Condition: All three Z-Scores must be less than the short entry threshold.

Short Condition = (Z-Score_tf1 < zScoreShortEntryThreshold) and (Z-Score_tf2 < zScoreShortEntryThreshold) and (Z-Score_tf3 < zScoreShortEntryThreshold)

█ Trade Direction

The strategy allows the user to specify the trading direction:

- Long: Only long trades are executed.

- Short: Only short trades are executed.

- Both: Both long and short trades are executed based on the Z-Score conditions.

█ Usage

The strategy can be applied to BTC or Crypto trading on major exchanges like Binance and OKX. By leveraging discrepancies between futures and spot prices, traders can exploit market inefficiencies. This strategy is suitable for traders who prefer a statistical approach and want to diversify their timeframes to validate signals.

█ Default Settings

- Input TF 1 (60 minutes): Sets the first timeframe for Z-Score calculation.

- Input TF 2 (120 minutes): Sets the second timeframe for Z-Score calculation.

- Input TF 3 (180 minutes): Sets the third timeframe for Z-Score calculation.

- Long Entry Z-Score Threshold (3): Defines the threshold above which a long trade is triggered.

- Short Entry Z-Score Threshold (-3): Defines the threshold below which a short trade is triggered.

- Long-Term SMA Period (100): The period used to calculate the simple moving average for the spread.

- Use Hold Days (true): Enables holding trades for a specified number of days.

- Hold Days (5): Number of days to hold the trade before exiting.

- TPSL Condition (None): Defines the conditions for taking profit and stop loss.

- Take Profit (%) (30.0): The percentage at which the trade will take profit.

- Stop Loss (%) (20.0): The percentage at which the trade will stop loss.

By fine-tuning these settings, traders can optimize the strategy to suit their risk tolerance and trading style, enhancing overall performance.

Volume Spread Analysis [TANHEF]Volume Spread Analysis: Understanding Market Intentions through the Interpretation of Volume and Price Movements.

█ Simple Explanation:

The Volume Spread Analysis (VSA) indicator is a comprehensive tool that helps traders identify key market patterns and trends based on volume and spread data. This indicator highlights significant VSA patterns and provides insights into market behavior through color-coded volume/spread bars and identification of bars indicating strength, weakness, and neutrality between buyers and sellers. It also includes powerful volume and spread forecasting capabilities.

█ Laws of Volume Spread Analysis (VSA):

The origin of VSA begins with Richard Wyckoff, a pivotal figure in its development. Wyckoff made significant contributions to trading theory, including the formulation of three basic laws:

The Law of Supply and Demand: This fundamental law states that supply and demand balance each other over time. High demand and low supply lead to rising prices until demand falls to a level where supply can meet it. Conversely, low demand and high supply cause prices to fall until demand increases enough to absorb the excess supply.

The Law of Cause and Effect: This law assumes that a 'cause' will result in an 'effect' proportional to the 'cause'. A strong 'cause' will lead to a strong trend (effect), while a weak 'cause' will lead to a weak trend.

The Law of Effort vs. Result: This law asserts that the result should reflect the effort exerted. In trading terms, a large volume should result in a significant price move (spread). If the spread is small, the volume should also be small. Any deviation from this pattern is considered an anomaly.

█ Volume and Spread Analysis Bars:

Display: Volume and/or spread bars that consist of color coded levels. If both of these are displayed, the number of spread bars can be limited for visual appeal and understanding, with the spread bars scaled to match the volume bars. While automatic calculation of the number of visual bars for auto scaling is possible, it is avoided to prevent the indicator from reloading whenever the number of visual price bars on the chart is adjusted, ensuring uninterrupted analysis. A displayable table (Legend) of bar colors and levels can give context and clarify to each volume/spread bar.

Calculation: Levels are calculated using multipliers applied to moving averages to represent key levels based on historical data: low, normal, high, ultra. This method smooths out short-term fluctuations and focuses on longer-term trends.

Low Level: Indicates reduced volatility and market interest.

Normal Level: Reflects typical market activity and volatility.

High Level: Indicates increased activity and volatility.

Ultra Level: Identifies extreme levels of activity and volatility.

This illustrates the appearance of Volume and Spread bars when scaled and plotted together:

█ Forecasting Capabilities:

Display: Forecasted volume and spread levels using predictive models.

Calculation: Volume and Spread prediction calculations differ as volume is linear and spread is non-linear.

Volume Forecast (Linear Forecasting): Predicts future volume based on current volume rate and bar time till close.

Spread Forecast (Non-Linear Dynamic Forecasting): Predicts future spread using a dynamic multiplier, less near midpoint (consolidation) and more near low or high (trending), reflecting non-linear expansion.

Moving Averages: In forecasting, moving averages utilize forecasted levels instead of actual levels to ensure the correct level is forecasted (low, normal, high, or ultra).

The following compares forecasted volume with actual resulting volume, highlighting the power of early identifying increased volume through forecasted levels:

█ VSA Patterns:

Criteria and descriptions for each VSA pattern are available as tooltips beside them within the indicator’s settings. These tooltips provide explanations of potential developments based on the volume and spread data.

Signs of Strength (🟢): Patterns indicating strong buying pressure and potential market upturns.

Down Thrust

Selling Climax

No Effort → Bearish Result

Bearish Effort → No Result

Inverse Down Thrust

Failed Selling Climax

Bull Outside Reversal

End of Falling Market (Bag Holder)

Pseudo Down Thrust

No Supply

Signs of Weakness (🔴): Patterns indicating strong selling pressure and potential market downturns.

Up Thrust

Buying Climax

No Effort → Bullish Result

Bullish Effort → No Result

Inverse Up Thrust

Failed Buying Climax

Bear Outside Reversal

End of Rising Market (Bag Seller)

Pseudo Up Thrust

No Demand

Neutral Patterns (🔵): Patterns indicating market indecision and potential for continuation or reversal.

Quiet Doji

Balanced Doji

Strong Doji

Quiet Spinning Top

Balanced Spinning Top

Strong Spinning Top

Quiet High Wave

Balanced High Wave

Strong High Wave

Consolidation

Bar Patterns (🟡): Common candlestick patterns that offer insights into market sentiment. These are required in some VSA patterns and can also be displayed independently.

Bull Pin Bar

Bear Pin Bar

Doji

Spinning Top

High Wave

Consolidation

This demonstrates the acronym and descriptive options for displaying bar patterns, with the ability to hover over text to reveal the descriptive text along with what type of pattern:

█ Alerts:

VSA Pattern Alerts: Notifications for identified VSA patterns at bar close.

Volume and Spread Alerts: Alerts for confirmed and forecasted volume/spread levels (Low, High, Ultra).

Forecasted Volume and Spread Alerts: Alerts for forecasted volume/spread levels (High, Ultra) include a minimum percent time elapsed input to reduce false early signals by ensuring sufficient bar time has passed.

█ Inputs and Settings:

Display Volume and/or Spread: Choose between displaying volume bars, spread bars, or both with different lookback periods.

Indicator Bar Color: Select color schemes for bars (Normal, Detail, Levels).

Indicator Moving Average Color: Select schemes for bars (Fill, Lines, None).

Price Bar Colors: Options to color price bars based on VSA patterns and volume levels.

Legend: Display a table of bar colors and levels for context and clarity of volume/spread bars.

Forecast: Configure forecast display and prediction details for volume and spread.

Average Multipliers: Define multipliers for different levels (Low, High, Ultra) to refine the analysis.

Moving Average: Set volume and spread moving average settings.

VSA: Select the VSA patterns to be calculated and displayed (Strength, Weakness, Neutral).

Bar Patterns: Criteria for bar patterns used in VSA (Doji, Bull Pin Bar, Bear Pin Bar, Spinning Top, Consolidation, High Wave).

Colors: Set exact colors used for indicator bars, indicator moving averages, and price bars.

More Display Options: Specify how VSA pattern text is displayed (Acronym, Descriptive), positioning, and sizes.

Alerts: Configure alerts for VSA patterns, volume, and spread levels, including forecasted levels.

█ Usage:

The Volume Spread Analysis indicator is a helpful tool for leveraging volume spread analysis to make informed trading decisions. It offers comprehensive visual and textual cues on the chart, making it easier to identify market conditions, potential reversals, and continuations. Whether analyzing historical data or forecasting future trends, this indicator provides insights into the underlying factors driving market movements.

VolumeSpreadAnalysisLibrary "VolumeSpreadAnalysis"

A library for Volume Spread Analysis (VSA).

spread(_barIndex)

Calculates the spread of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The spread of the bar.

volume(_barIndex)

Retrieves the volume of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The volume of the bar.

body(_barIndex)

Calculates the body of a bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The body size of the bar.

wickUpper(_barIndex)

Calculates the upper wick of a bar (upper shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The upper wick size of the bar.

wickLower(_barIndex)

Calculates the lower wick of a bar (lower shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The lower wick size of the bar.

calcForecastedSMA(_source, _length, _forecastedLevel)

Calculates the forecasted Simple Moving Average (SMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the SMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted SMA value.

calcForecastedEMA(_source, _length, _forecastedLevel)

Calculates the forecasted Exponential Moving Average (EMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the EMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted EMA value.

calcForecastedRMA(_source, _length, _forecastedLevel)

Calculates the forecasted Relative Moving Average (RMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the RMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted RMA value.

calcForecastedWMA(_source, _length, _forecastedLevel)

Calculates the forecasted Weighted Moving Average (WMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the WMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted WMA value.

calcElapsedTimePercent()

Calculates the elapsed time percent of the current bar.

Returns: (float) The elapsed time percent.

calcForecastedSpread(multiplierAtMidpoints, multiplierAtPeaks)

Calculates the forecasted spread using elapsed time and dynamic multipliers, handling spread's non-linear nature.

Parameters:

multiplierAtMidpoints (float) : (float) The multiplier value at midpoints.

multiplierAtPeaks (float) : (float) The multiplier value at peaks.

Returns: (float) The forecasted spread value.

calcForecastedVolume()

Calculates the forecasted volume using elapsed time, satisfying volume's linear nature.

Returns: (float) The forecasted volume value.

calcForecastedMA(_source, _length, _forecastedSource, _type)

Calculates the forecasted Moving Average (MA) based on the specified type.

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the MA.

_forecastedSource (float) : (float) The forecasted level to include in the calculation.

_type (simple string) : (string) The type of the MA ("SMA", "EMA", "SMMA (RMA)", "WMA").

Returns: (float) The forecasted MA value.

calcMA(_source, _length, _type)

Calculates the Moving Average (MA) based on the specified type.

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the MA.

_type (simple string) : (string) The type of the MA ("SMA", "EMA", "SMMA (RMA)", "WMA").

Returns: (float) The MA value.

bullBar(_barIndex)

Determines if the bar is bullish.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if the bar is bullish, otherwise false.

bearBar(_barIndex)

Determines if the bar is bearish.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if the bar is bearish, otherwise false.

breakout(_barIndex)

Determines if there is a breakout above the previous bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if there is a breakout, otherwise false.

breakdown(_barIndex)

Determines if there is a breakdown below the previous bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (bool) True if there is a breakdown, otherwise false.

rejectionWickUpper(_rejectionWick)

Determines if the upper wick is a rejection wick.

Parameters:

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if the upper wick is a rejection wick, otherwise false.

rejectionWickLower(_rejectionWick)

Determines if the lower wick is a rejection wick.

Parameters:

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if the lower wick is a rejection wick, otherwise false.

setupDataVolume(_data, _mult_Low, _mult_High, _mult_Ultra, _maLengthVolume, _maTypeVolume)

Sets up data for volume levels.

Parameters:

_data (map) : (map) The map to store the levels.

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthVolume (simple int) : (int) The length for MA.

_maTypeVolume (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataSpread(_data, _mult_Low, _mult_High, _mult_Ultra, _maLengthSpread, _maTypeSpread)

Sets up data for spread levels.

Parameters:

_data (map) : (map) The map to store the levels.

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthSpread (simple int) : (int) The length for MA.

_maTypeSpread (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataForecastVolume(_dataForecast, _mult_Low, _mult_High, _mult_Ultra, _maLengthVolume, _predictedLevelVolume, _maTypeVolume)

Sets up data for volume and spread levels for forecast.

Parameters:

_dataForecast (map)

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthVolume (simple int) : (int) The length for MA.

_predictedLevelVolume (float) : (float) The predicted level for MA.

_maTypeVolume (simple string) : (string) The type for MA.

Returns: (void) Nothing.

setupDataForecastSpread(_dataForecast, _mult_Low, _mult_High, _mult_Ultra, _maLengthSpread, _predictedLevelSpread, _maTypeSpread)

Sets up data for spread levels for forecast.

Parameters:

_dataForecast (map)

_mult_Low (simple float) : (float) The multiplier for low level.

_mult_High (simple float) : (float) The multiplier for high level.

_mult_Ultra (simple float) : (float) The multiplier for ultra level.

_maLengthSpread (simple int) : (int) The length for MA.

_predictedLevelSpread (float) : (float) The predicted level for MA.

_maTypeSpread (simple string) : (string) The type for MA.

Returns: (void) Nothing.

isVolumeLow(_data, _barIndex)

Determines if the volume is low.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is low, otherwise false.

isVolumeNormal(_data, _barIndex)

Determines if the volume is normal.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is normal, otherwise false.

isVolumeHigh(_data, _barIndex)

Determines if the volume is high.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is high, otherwise false.

isVolumeUltra(_data, _barIndex)

Determines if the volume is ultra.

Parameters:

_data (map) : (map) The data map with volume levels.

_barIndex (int)

Returns: (bool) True if the volume is ultra, otherwise false.

isSpreadLow(_data, _barIndex)

Determines if the spread is low.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is low, otherwise false.

isSpreadNormal(_data, _barIndex)

Determines if the spread is normal.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is normal, otherwise false.

isSpreadHigh(_data, _barIndex)

Determines if the spread is high.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is high, otherwise false.

isSpreadUltra(_data, _barIndex)

Determines if the spread is ultra.

Parameters:

_data (map) : (map) The data map with spread levels.

_barIndex (int)

Returns: (bool) True if the spread is ultra, otherwise false.

isVolumeText(_data)

Determines text string representing the volume area level.

Parameters:

_data (map) : (map) The data map with volume levels.

Returns: (string) Text string of Low, Normal, High, or Ultra.

isSpreadText(_data)

Determines text string representing the spread area level.

Parameters:

_data (map) : (map) The data map with spread levels.

Returns: (string) Text string of Low, Normal, High, or Ultra.

calcBarColor(_value, _level)

Calculates the color based level.

Parameters:

_value (float) : (float) The value to check.

_level (float) : (float) The value level for comparison.

Returns: (color) The color for the bar.

bullPinBar(_maxBodyPercent, _minWickPercent)

Determines if the bar is a bull pin bar.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

Returns: (bool) True if the bar is a bull pin bar, otherwise false.

bearPinBar(_maxBodyPercent, _minWickPercent)

Determines if the bar is a bear pin bar.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

Returns: (bool) True if the bar is a bear pin bar, otherwise false.

dojiBar(_maxBodyPercent)

Determines if the bar is a doji.

Parameters:

_maxBodyPercent (simple float) : (float) The maximum body percentage.

Returns: (bool) True if the bar is a doji, otherwise false.

spinningTopBar(_minWicksPercent, _emaLength)

Determines if the bar is a spinning top.

Parameters:

_minWicksPercent (simple float) : (float) The minimum wicks percentage.

_emaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if the bar is a spinning top, otherwise false.

highWaveBar(_minBodyPercent, _minWickPercent, _bars)

Determines if the bar is a high wave bar.

Parameters:

_minBodyPercent (simple float) : (float) The minimum body percentage.

_minWickPercent (simple float) : (float) The minimum wick percentage.

_bars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if the bar is a high wave bar, otherwise false.

consolidationBar(_data, _spread, _bars)

Determines if the bars are in consolidation.

Parameters:

_data (map) : (map) The data map with spread levels.

_spread (simple float) : (float) The spread percentage for comparison.

_bars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if the bars are in consolidation, otherwise false.

S_DownThrust(_data, _bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (DownThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (DownThrust), otherwise false.

S_SellingClimax(_data, _rejectionWick)

Determines if there is a sign of strength (Selling Climax).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if there is a sign of strength (Selling Climax), otherwise false.

S_NoEffortBearishResult()

Determines if there is a sign of strength (No Effort Bearish Result).

Returns: (bool) True if there is a sign of strength (No Effort Bearish Result), otherwise false.

S_BearishEffortNoResult()

Determines if there is a sign of strength (Bearish Effort No Result).

Returns: (bool) True if there is a sign of strength (Bearish Effort No Result), otherwise false.

S_InverseDownThrust(_data, _bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of strength (Inverse DownThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of strength (Inverse DownThrust), otherwise false.

S_FailedSellingClimax()

Determines if there is a sign of strength (Failed Selling Climax).

Returns: (bool) True if there is a sign of strength (Failed Selling Climax), otherwise false.

S_BullOutsideReversal(_data)

Determines if there is a sign of strength (Bull Outside Reversal).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of strength (Bull Outside Reversal), otherwise false.

S_EndOfFallingMarket(_data)

Determines if there is a sign of strength (End of Falling Market).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of strength (End of Falling Market), otherwise false.

S_PseudoDownThrust(_bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (Pseudo DownThrust).

Parameters:

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (Pseudo DownThrust), otherwise false.

S_NoSupply(_bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of strength (No Supply).

Parameters:

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of strength (No Supply), otherwise false.

W_UpThrust(_data, _bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (UpThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (UpThrust), otherwise false.

W_BuyingClimax(_data, _rejectionWick)

Determines if there is a sign of weakness (Buying Climax).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_rejectionWick (simple float) : (float) The rejection wick percentage.

Returns: (bool) True if there is a sign of weakness (Buying Climax), otherwise false.

W_NoEffortBullishResult()

Determines if there is a sign of weakness (No Effort Bullish Result).

Returns: (bool) True if there is a sign of weakness (No Effort Bullish Result), otherwise false.

W_BullishEffortNoResult()

Determines if there is a sign of weakness (Bullish Effort No Result).

Returns: (bool) True if there is a sign of weakness (Bullish Effort No Result), otherwise false.

W_InverseUpThrust(_data, _bullPinBarMaxBody, _bullPinBarMinWick)

Determines if there is a sign of weakness (Inverse UpThrust).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_bullPinBarMaxBody (simple float) : (float) The maximum body percentage for bull pin bar.

_bullPinBarMinWick (simple float) : (float) The minimum wick percentage for bull pin bar.

Returns: (bool) True if there is a sign of weakness (Inverse UpThrust), otherwise false.

W_FailedBuyingClimax()

Determines if there is a sign of weakness (Failed Buying Climax).

Returns: (bool) True if there is a sign of weakness (Failed Buying Climax), otherwise false.

W_BearOutsideReversal(_data)

Determines if there is a sign of weakness (Bear Outside Reversal).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of weakness (Bear Outside Reversal), otherwise false.

W_EndOfRisingMarket(_data)

Determines if there is a sign of weakness (End of Rising Market).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

Returns: (bool) True if there is a sign of weakness (End of Rising Market), otherwise false.

W_PseudoUpThrust(_bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (Pseudo UpThrust).

Parameters:

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (Pseudo UpThrust), otherwise false.

W_NoDemand(_bearPinBarMaxBody, _bearPinBarMinWick)

Determines if there is a sign of weakness (No Demand).

Parameters:

_bearPinBarMaxBody (simple float) : (float) The maximum body percentage for bear pin bar.

_bearPinBarMinWick (simple float) : (float) The minimum wick percentage for bear pin bar.

Returns: (bool) True if there is a sign of weakness (No Demand), otherwise false.

N_QuietDoji(_dojiBarMaxBody)

Determines if there is a neutral signal (Quiet Doji).

Parameters:

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Quiet Doji), otherwise false.

N_BalancedDoji(_data, _dojiBarMaxBody)

Determines if there is a neutral signal (Balanced Doji).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Balanced Doji), otherwise false.

N_StrongDoji(_dojiBarMaxBody)

Determines if there is a neutral signal (Strong Doji).

Parameters:

_dojiBarMaxBody (simple float) : (float) The maximum body percentage for doji bar.

Returns: (bool) True if there is a neutral signal (Strong Doji), otherwise false.

N_QuietSpinningTop(_spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Quiet Spinning Top).

Parameters:

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Quiet Spinning Top), otherwise false.

N_BalancedSpinningTop(_data, _spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Balanced Spinning Top).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Balanced Spinning Top), otherwise false.

N_StrongSpinningTop(_spinningTopBarMinWicks, _spinningTopBarEmaLength)

Determines if there is a neutral signal (Strong Spinning Top).

Parameters:

_spinningTopBarMinWicks (simple float) : (float) The minimum wicks percentage for spinning top bar.

_spinningTopBarEmaLength (simple int) : (int) The length for EMA calculation.

Returns: (bool) True if there is a neutral signal (Strong Spinning Top), otherwise false.

N_QuietHighWave(_highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Quiet High Wave).

Parameters:

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Quiet High Wave), otherwise false.

N_BalancedHighWave(_data, _highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Balanced High Wave).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Balanced High Wave), otherwise false.

N_StrongHighWave(_highWaveBarMinBody, _highWaveBarMinWick, _highWaveBarBars)

Determines if there is a neutral signal (Strong High Wave).

Parameters:

_highWaveBarMinBody (simple float) : (float) The minimum body percentage for high wave bar.

_highWaveBarMinWick (simple float) : (float) The minimum wick percentage for high wave bar.

_highWaveBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Strong High Wave), otherwise false.

N_Consolidation(_data, _consolidationBarSpread, _consolidationBarBars)

Determines if there is a neutral signal (Consolidation).

Parameters:

_data (map) : (map) The data map with volume and spread levels.

_consolidationBarSpread (simple float) : (float) The spread percentage for consolidation bar.

_consolidationBarBars (simple int) : (int) The number of bars for comparison.

Returns: (bool) True if there is a neutral signal (Consolidation), otherwise false.

Fourier Smoothed Hybrid Volume Spread AnalysisIndicator id:

USER;91bdff47320b4284a375f428f683b21e

(only relevant to those that use API requests)

MEANINGFUL DESCRIPTION:

The Fourier Smoothed Hybrid Volume Spread Analysis (FSHVSA) indicator is an innovative trading tool designed to fuse volume analysis with trend detection capabilities, offering traders a comprehensive view of market dynamics.

This indicator stands apart by integrating the principles of the Discrete Fourier Transform (DFT) and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the FSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

HOW TO USE THE INDICATOR:

The FSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

ORIGINALITY & USEFULNESS:

The FSHVSA is unique because it applies DFT for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread ?

It results in a neutral, not trending price action.

Thus the indicator returns 0.

In the next Image you can see that trend is negative on 4h, neutral on 12h and neutral on 1D. That means trend is negative .

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Euler approximation of a spread are taken from aprox library.

Key Features:

Noise Reduction leverages Euler's White noise capabilities for effective Volume smoothing, providing a cleaner and more accurate representation of market dynamics.

Choose between the innovative Double Discrete Fourier Transform (DTF32) and Regular Open & Close price series.

Mathematical equations presented in Pinescript:

Fourier of the real (x axis) discrete:

x_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

x_1 = array.get(x, 0) + array.get(x, 1) * math.cos( -2 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -4 * math.pi * _dir / 3 )

x_2 = array.get(x, 0) + array.get(x, 1) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -8 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -8 * math.pi * _dir / 3 )

Fourier of the imaginary (y axis) discrete:

y_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

y_1 = array.get(x, 0) + array.get(x, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(y, 1) * math.cos( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(y, 2) * math.cos( -4 * math.pi * _dir / 3 )

y_2 = array.get(x, 0) + array.get(x, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(y, 1) * math.cos( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.sin( -8 * math.pi * _dir / 3 ) + array.get(y, 2) * math.cos( -8 * math.pi * _dir / 3 )

Euler's Smooth with Discrete Furrier approximated Volume.

a = math.sqrt(2) * math.pi / _devided

b = math.cos(math.sqrt(2) * 180 / _devided)

c2 = 2 * math.pow(a, 2) * b

c3 = math.pow(a, 4)

c1 = 1 - 2 * math.pow(a, 2) * math.cos(b) + math.pow(a, 4)

filt := na(filt ) ? 0 : c1 * (w + nz(w )) / 2.0 + c2 * nz(filt ) + c3 * nz(filt )

Usecase:

First option:

Leverage the script to identify Bullish and Bearish trends, shown with green and red triangle.

Combine Different Timeframes to accurately determine market trend.

Second option:

Pull the data with API sockets to automate your trading journey.

plot(close, title="ClosePrice", display=display.status_line)

plot(open, title="OpenPrice", display=display.status_line)

plot(greencon ? 1 : redcon ? -1 : 0, title="position", display=display.status_line)

Use ClosePrice, OpenPrice and "position" titles to easily read and backtest your strategy utilising more than 1 Time Frame.

Indicator id:

USER;91bdff47320b4284a375f428f683b21e

(only relevant to those that use API requests)

Crypto MVRV ZScore - Strategy [PresentTrading]█ Introduction and How it is Different

The "Crypto Valuation Extremes: MVRV ZScore - Strategy " represents a cutting-edge approach to cryptocurrency trading, leveraging the Market Value to Realized Value (MVRV) Z-Score. This metric is pivotal for identifying overvalued or undervalued conditions in the crypto market, particularly Bitcoin. It assesses the current market valuation against the realized capitalization, providing insights that are not apparent through conventional analysis.

BTCUSD 6h Long/Short Performance

Local

█ Strategy, How It Works: Detailed Explanation

The strategy leverages the Market Value to Realized Value (MVRV) Z-Score, specifically designed for cryptocurrencies, with a focus on Bitcoin. This metric is crucial for determining whether Bitcoin is currently undervalued or overvalued compared to its historical 'realized' price. Below is an in-depth explanation of the strategy's components and calculations.

🔶Conceptual Foundation

- Market Capitalization (MC): This represents the total dollar market value of Bitcoin's circulating supply. It is calculated as the current price of Bitcoin multiplied by the number of coins in circulation.

- Realized Capitalization (RC): Unlike MC, which values all coins at the current market price, RC is computed by valuing each coin at the price it was last moved or traded. Essentially, it is a summation of the value of all bitcoins, priced at the time they were last transacted.

- MVRV Ratio: This ratio is derived by dividing the Market Capitalization by the Realized Capitalization (The ratio of MC to RC (MVRV Ratio = MC / RC)). A ratio greater than 1 indicates that the current price is higher than the average price at which all bitcoins were purchased, suggesting potential overvaluation. Conversely, a ratio below 1 suggests undervaluation.

🔶 MVRV Z-Score Calculation

The Z-Score is a statistical measure that indicates the number of standard deviations an element is from the mean. For this strategy, the MVRV Z-Score is calculated as follows:

MVRV Z-Score = (MC - RC) / Standard Deviation of (MC - RC)

This formula quantifies Bitcoin's deviation from its 'normal' valuation range, offering insights into market sentiment and potential price reversals.

🔶 Spread Z-Score for Trading Signals

The strategy refines this approach by calculating a 'spread Z-Score', which adjusts the MVRV Z-Score over a specific period (default: 252 days). This is done to smooth out short-term market volatility and focus on longer-term valuation trends. The spread Z-Score is calculated as follows:

Spread Z-Score = (Market Z-Score - MVVR Ratio - SMA of Spread) / Standard Deviation of Spread

Where:

- SMA of Spread is the simple moving average of the spread over the specified period.

- Spread refers to the difference between the Market Z-Score and the MVRV Ratio.

🔶 Trading Signals

- Long Entry Condition: A long (buy) signal is generated when the spread Z-Score crosses above the long entry threshold, indicating that Bitcoin is potentially undervalued.

- Short Entry Condition: A short (sell) signal is triggered when the spread Z-Score falls below the short entry threshold, suggesting overvaluation.

These conditions are based on the premise that extreme deviations from the mean (as indicated by the Z-Score) are likely to revert to the mean over time, presenting opportunities for strategic entry and exit points.

█ Practical Application

Traders use these signals to make informed decisions about opening or closing positions in the Bitcoin market. By quantifying market valuation extremes, the strategy aims to capitalize on the cyclical nature of price movements, identifying high-probability entry and exit points based on historical valuation norms.

█ Trade Direction

A unique feature of this strategy is its configurable trade direction. Users can specify their preference for engaging in long positions, short positions, or both. This flexibility allows traders to tailor the strategy according to their risk tolerance, market outlook, or trading style, making it adaptable to various market conditions and trader objectives.

█ Usage

To implement this strategy, traders should first adjust the input parameters to align with their trading preferences and risk management practices. These parameters include the trade direction, Z-Score calculation period, and the thresholds for long and short entries. Once configured, the strategy automatically generates trading signals based on the calculated spread Z-Score, providing clear indications for potential entry and exit points.

It is advisable for traders to backtest the strategy under different market conditions to validate its effectiveness and adjust the settings as necessary. Continuous monitoring and adjustment are crucial, as market dynamics evolve over time.

█ Default Settings

- Trade Direction: Both (Allows for both long and short positions)

- Z-Score Calculation Period: 252 days (Approximately one trading year, capturing a comprehensive market cycle)

- Long Entry Threshold: 0.382 (Indicative of moderate undervaluation)

- Short Entry Threshold: -0.382 (Signifies moderate overvaluation)

These default settings are designed to balance sensitivity to market valuation extremes with a pragmatic approach to trade execution. They aim to filter out noise and focus on significant market movements, providing a solid foundation for both new and experienced traders looking to exploit the unique insights offered by the MVRV Z-Score in the cryptocurrency market.

Divergence AnalyzerUnlock the potential of your trading strategy with the Divergence Analyzer, a sophisticated indicator designed to identify divergence patterns between two financial instruments. Whether you're a seasoned trader or just starting, this tool provides valuable insights into market trends and potential trading opportunities.

Key Features:

1. Versatility in Symbol Selection:

- Choose from a wide range of symbols for comparison, including popular indices like XAUUSD and SPX.

- Seamlessly toggle between symbols to analyze divergences and make informed trading decisions.

2. Flexible Calculation Options:

- Customizable options allow you to use a different symbol for calculation instead of the chart symbol.

- Fine-tune your analysis by selecting specific symbols for comparison based on your trading preferences.

3. Logarithmic Scale Analysis:

- Utilizes logarithmic scales for accurate representation of price movements.

- Linear regression coefficients are calculated on the logarithmic scale, providing a comprehensive view of trend strength.

4. Dynamic Length and Smoothing:

- Adjust the length parameter to adapt the indicator to different market conditions.

- Smoothed linear regression with exponential moving averages enhances clarity and reduces noise.

5. Standard Deviation Normalization:

- Normalizes standard deviations over 200 periods, offering a standardized view of price volatility.

- Easily compare volatility levels across different symbols for effective divergence analysis.

6. Color-Coded Divergence Visualization:

- Clearly distinguish positive and negative divergences with customizable color options.

- Visualize divergence deltas with an intuitive color scheme for quick and effective interpretation.

7. Symbol Information Table:

- An included table provides at-a-glance information about the selected symbols.

- Identify Symbol 1 and Symbol 2, along with their corresponding positive and negative divergence colors.

How to Use:

1. Select symbols for analysis using the user-friendly inputs.

2. Customize calculation options based on your preferences.

3. Analyze the divergence delta plot for clear visual indications.

4. Refer to the symbol information table for a quick overview of selected instruments.

Empower your trading strategy with the Divergence Analyzer and gain a competitive edge in the dynamic world of financial markets. Start making more informed decisions today!

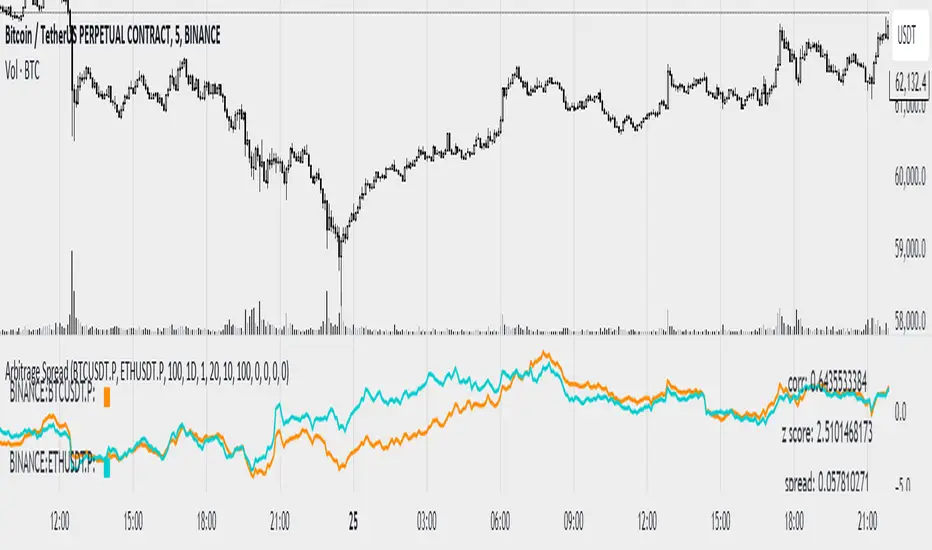

Arbitrage SpreadThis indicator helps to find spreads between cryptocurrencies, assess their correlation, spread, z score and atr z score.

The graphs are plotted as a percentage. Because of the limitation in pine tradingview for 5000 bars a period was introduced (after which a new starting point of the graph construction will be started), if you want it can be disabled

The multiplier parameter affects only the construction of the joint diagram on which z score and atr z score are calculated (construction of the diagram is done by dividing one pair by another and multiplying by the multiplier parameter) is shown with a red line

To create a notification you have to specify the data for parameters other than zero which you want to monitor. For parameters z score and atr z score data are counted in both directions

The data can be tracked via the data window

Link to image of the data window prnt.sc

Inter-Exchanges Crypto Price Spread Clouds (Tartigradia)Display variations in min-max and median values of high, low and close across exchanges. It's a kind of realized volatility indicator, as the idea is that in times of high volatility (high emotions, fear, uncertainty), it's more likely that market inefficiencies will appear for the same asset between different market makers, ie, the price can temporarily differ a lot. This indicator will catch these instants of high differences between exchanges, even if they lasted only an instant (because we use high and low values).

Compared with my other "Inter-Exchanges Crypto Price Spread Deviation" indicator, this one overlays directly on the chart, and offers a different take based on the same premisses. Instead of summarizing volatility via standard deviation, here we display clouds of the range of values that were observed.

A big advantage of this approach is that it can also be used to determine safe stop loss levels, especially the values of percentile rank (i.e., what are the high values that were observed in at least 50% of exchanges?).

Indeed, all price levels are displayed in the indicator's status bar:

green for high values,

red for low values,

aqua for median,

purple for average,

The first two values are max and min values of high across exchanges (in green).

The next two values are max and min of low across exchanges (in red).

The next two values are median (aqua) and average (purple).

The last two values are percentile rank values for high (green) and low (red) respectively.

Another advantage is that the high (green) vs low (red) clouds can be seen as representing the buying or selling pressure respectively across exchanges, and this may in itself provide a signal to know whether one side is winning.

Link to my other complementary indicator:

Compared to other inter-exchanges spread indicators, this one offers two major features:

The symbol automatically adapts to the symbol currently selected in user's chart. Hence, switching between tickers does not require the user to modify any option, everything is dynamically updated behind the scenes.

It's easy to add more exchanges (requires some code editing because PineScript v5 does not allow dynamical request.security() calls).

Limitations/things to know:

History is limited to what the ticker itself display. Ie, even if the exchanges specified in this indicator have more data than the ticker currently displayed in the user's chart, the indicator will show only a timeperiod as long as the chart.

The indicator can manage multiple exchanges of different historical length (ie, some exchanges having more data going way earlier in the past than others), in which case they will simply be ignored from calculations when far back in the past. Hence, you should be aware that the further you go in the past, the less exchanges will have such data, and hence the less accurate the measures will be (because the deviation will be calculated from less sources than more recent bars). This is thanks to how the array.* math functions behave in case of na values, they simply skip them from calculations, contrary to math.* functions.

Inter-Exchanges Crypto Price Spread Deviation (Tartigradia)Measures the deviation of price metrics between various exchanges. It's a kind of realized volatility indicator, as the idea is that in times of high volatility (high emotions, fear, uncertainty), it's more likely that market inefficiencies will appear for the same asset between different market makers, ie, the price can temporarily differ a lot. This indicator will catch these instants of high differences between exchanges, even if they lasted only an instant (because we use high and low values).

Both standard deviation and median absolute deviation (more robust to outliers, ie, exchanges with a very different price from others won't influence the median absolute deviation, but the standard deviation yes).

Compared to other inter-exchanges spread indicators, this one offers two major features:

* The symbol automatically adapts to the symbol currently selected in user's chart. Hence, switching between tickers does not require the user to modify any option, everything is dynamically updated behind the scenes.

* It's easy to add more exchanges (requires some code editing because PineScript v5 does not allow dynamical request.security() calls).

Limitations/things to know:

* History is limited to what the ticker itself display. Ie, even if the exchanges specified in this indicator have more data than the ticker currently displayed in the user's chart, the indicator will show only a timeperiod as long as the chart.

* The indicator can manage multiple exchanges of different historical length (ie, some exchanges having more data going way earlier in the past than others), in which case they will simply be ignored from calculations when far back in the past. Hence, you should be aware that the further you go in the past, the less exchanges will have such data, and hence the less accurate the measures will be (because the deviation will be calculated from less sources than more recent bars). This is thanks to how the array.* math functions behave in case of na values, they simply skip them from calculations, contrary to math.* functions.

MAD - Mean Absolute Deviation purpose :implementation of MAD Mean Absolute Deviation in pinescript

implementation by : patmaba

type : measures of spread

Mean absolute deviation

The mean absolute deviation of a dataset is the average distance between each data point and the mean. It gives us an idea about the variability in a dataset.

Here's how to calculate the median absolute deviation.

Step 1: Calculate the mean.

Step 2: Calculate how far away each data point is from the mean using positive distances. These are called absolute deviations.

Step 3: Add those deviations together.

Step 4: Divide the sum by the number of data points.

Source of MAD:

www.khanacademy.org

Formula :

MAD = ( ∑ |xi−µ| ) / n

where

xi = the value of a data point

|xi − µ| = absolute deviation

µ = mean

n = sample size

Spread ChartThis script lets you chart a spread of a maximum of 3 tickers (one of them being the ticker in the main chart).

Y axis is the currency amount of the spread, that is calculated by this formula:

Y = PnL = quantity * price * handleValue

Y is calculated for each ticker specified, and the sum of Ys obtained is plotted.

this way it is possible to view the PnL of the spread directly.

It is necessary to specify the handle value (point value) in the script inputs (not for the main chart ticker).

A table summarizes the spread configuration, containing all inputs.

two_leg_spread_diffThis script helps you discern the relative change of each leg in a two-legged spread over a given period. The main plot is a difference in log return over the number of bars identified by the "lag" parameter. E.g. if "lag" is 10 and leg one has increased 3% over the past ten bars, while leg two has only increased 1%, the plot value is 2%. The main plot is also colored blue when leg one increases while leg two decreases on a given bar, and red if the opposite is true. This feature identifies periods where the correlation between the two legs diminishes. The one and two standard deviation of the main plot is also plotted in faint background lines. Additionally, a table indicates the percentage in which the main plot is within one standard deviation (acc 1) and two standard deviations (acc 2). Note that the standard deviation updates on each bar, so the current standard deviation is not the one used to calculate the accuracy. Rather, if there are N bars, N different standard deviation readings have been used to compute the accuracy statistics.

The inputs are:

- timeframe: the timeframe of the chart

- leg1_sym: the symbol of the first leg

- leg2_sym: the symbol of the second leg

- lag: the number of bars back to reference for computing the log return of each leg

- anchor_to_session_start: for intraday charts only, this overwrites the "lag" input so that the "lag" always sets the point of comparison to the session start. This setting is used to compute the relative change over a single session.

two_leg_spread_returns_zscoreThis script helps assess the relative returns of each leg in a two-legged spread. It shows the z-score of each period's returns, along with a moving average of the difference between the two returns. A negative moving average implies that the second leg is strengthening, on a relative return basis, against the first leg, and vice versa. The inputs are:

- timeframe: the timeframe for the calculations. the default is five minutes.

- leg1_sym: the symbol for the first leg

- leg2_sym: the symbol for the second leg

- ma_length: the length of the moving average. by default it is 48, or the previous four hours, given the default timeframe.

The default symbols are RB and HO, simply as an example of an intercommodity spread.

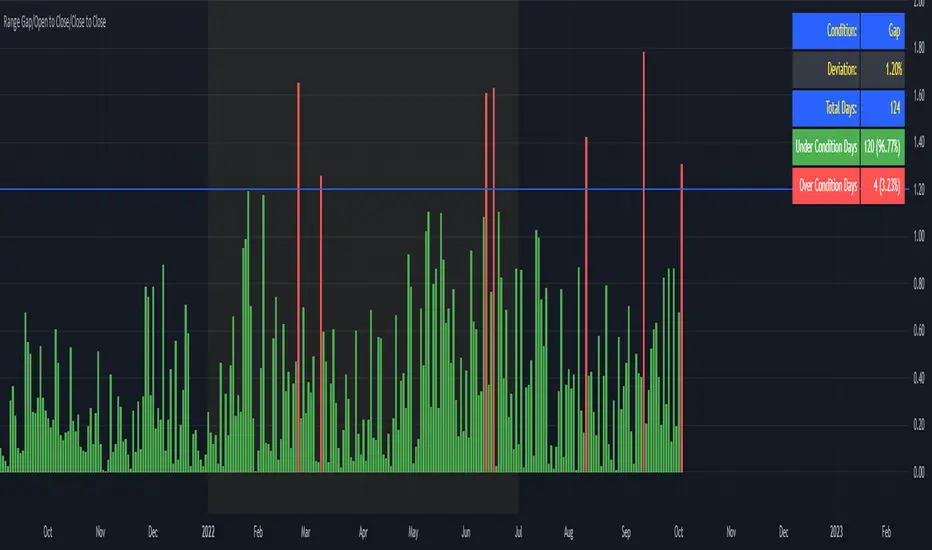

Range Gap/Open to Close/Close to CloseThis indicator shows the percentage variation of:

gap

close to close (day including gap)

open to close (without gap)

The green bars represent the days when the variation did not reach the selected range. The red bars show the days when the variation was higher than the selected range.

Best timeframe : DAY

10-Year Bond Yields (Interest Rate Differential)With this little script, I have attempted to incorporate fundamental data (in this case, 10-year bond yields) into technical analysis . When pairing two currencies, the one with a higher bond interest rate usually appreciates when the interest rate differential widens, or, to use a simple example: in a currency pair A vs. B, with A showing a higher bond yield than B, a widening interest rate gap is likely to help A and create a buying opportunity (shown as a blue square at the bottom of the chart), while the opposite is true when the gap tightens (sell signal, red square).

While long-term investors know about and make use of the importance of bond yield fluctuations, most short-term traders tend to dismiss the idea of using fundamental data, mostly for lack of quantifiability and limited impact in an intraday environment. After extensive backtesting on daily and intraday charts (6-12 hours), however, I realized this indicator still managed to produce useful results (less useful than on monthly and yearly charts, to be fair, but still useful enough), especially when paired with simple price-driven indicators, such as Heikin Ashi or linear regression .

My personal (and thus subjective) thoughts: worth a try. Buy and sell signals frequently contradicted both more popular indicators and my gut feeling and managed to take out losing trades that I had considered trades with a high winning probability. In other words, when the market lures traders into seemingly promising trading decisions, this indicator might give you an early warning, especially when you manage to adjust period and continuity parameters to your trading strategy.

Currency pairs used in this script are all possible combinations of the eight majors. Each security has been assigned a name ("inst01" to "inst08" in the code) and a broker; if you make changes to the code, be sure not to mess with currency and broker names as this would render the entire script useless. Good luck trading, and feel free to suggest improvements!

Future's spread with base contract (MOEX)English:

Indicator calculates spread between future and it's theoretical price baased on base contract, number of days to expiration and central bank key rate.

I didn't find any means of getting base contract of security on chart so I hardcoded futures and corresponding base contracts.

Hardcoded futures are MOEX (Moscow Exchange) only and key rate used in script is Russian Central Bank's key rate from 2013, but I believe you can easily adapt it to any other key rate history. I can share source code of tiny C++20 utility for easy generation of get_rate(time) function from more human-readable date format rather then UNIX timestamp used in PineScript.

Only quarterly futures are supported. Only in "SIU2022" like notation. "SI1!" like aliases are not supported.

Русский:

Индикатор отображает спред фьючерса к его теоретической цене с учётом усыхания на каждый день.

Не нашёл, как определить базовый актив фьючерса средствами TradingView - поэтому это соответствие захардкожено вручную.

Поддерживаются только квартальные фьючерсы, только MOEX, только хардкор.

Поддерживается история ключевой ставки ЦБ РФ с 2013 года.

Используйте коды фьючерсов вида "SIU2022".

Не поддерживаются альясы вроде "SI1!", "EU1!".

Historical US Bond Yield CurvePreface: I'm just the bartender serving today's freshly blended concoction; I'd like to send a massive THANK YOU to all the coders and PineWizards for the locally-sourced ingredients. I am simply a code editor, not a code author. Many thanks to these original authors!

Source 1 (Aug 8, 2019):

Source 2 (Aug 11, 2019):

About the Indicator: The term yield curve refers to the yields of U.S. treasury bills, notes, and bonds in order from shortest to longest maturity date. The yield curve describes the shapes of the term structures of interest rates and their respective terms to maturity in years. The slope of the yield curve tells us how the bond market expects short-term interest rates to move in the future based on bond traders' expectations about economic activity and inflation. The best use of the yield curve is to get a sense of the economy's direction rather than to try to make an exact prediction. This indicator plots the U.S. yield curve as maturity (x-axis/time) vs yield (y-axis/price) in addition to historical yield curves and advanced data tickers . The visual array of historical yield curves helps investors visualize shifts in the yield curve that are useful when identifying & forecasting economic conditions. The bond market can help predict the direction of the economy which can be useful in crafting your investment strategy. An inverted 10y/2y yield curve for durations longer than 5 consecutive trading days signals an almost certain recession on the horizon. An inversion happens when short-term bonds pay better than longer-term bonds. There is Federal Reserve Board data that suggests the 10y3m may be a better predictor of recessions.

Features: Advanced dual data ticker that performs curve & important spread analysis, plus additional hover info. Advanced yield curve data labels with additional hover info. Customizable historical curves and color theme.

‼ IMPORTANT: Hover over labels/tables for advanced information. Chart asset and timeframe may affect the yield curve results; I have found consistently accurate results using BINANCE:BTCUSDT on 1d timeframe. Historical curve lookbacks will have an effect on whether the curve analysis says the curve is bull/bear steepening/flattening, so please use appropriate lookbacks.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with the original authors, TradingView, Binance, or the Federal Reserve Board.

About the Editor: I am a former FINRA Registered Representative, inventor/patent holder, futures trader, and hobby PineScripter.

Volume Spread for VSA CustomHey everyone, I have been using volume a lot more lately as price action can sometimes get manipulated but volume shows us the truth!

Anyways, I have enjoyed the Volume Spread for VSA indicator but wished I had the code to change a few settings. This volume indicator includes spread analysis with the ability to customize input values and I'm making it open source so you can do with it as you please.

I have made notes all throughout the code to give suggestions on a few changes or why I have written it in such a way. I have also tried to section everything off to make it easier to see where each piece of the code is used. Overall I think it is a good example of how to code cleanly and how to add useful notes when you are learning Pine for yourself :D

The indicator on the price chart is my Donchian Channel indicator, which you can also find on my profile. This is the one I use every day.

Binance Futures Swap-Spot Basis LabelNote: This script will only work with Binance Futures Symbols

This script calculates the basis between the Binance Future and Binance Spot market for the coin you are currently viewing and paints a label on the chart which displays the percentage difference between future and spot. If the future is trading below the spot market the text will be red indicating backwardation and if the future is trading above spot, it will be green indicating contango. Please note this script will only work on Binance perps against Binance spot. The script will change based on what perp you are looking at, no inputs are required.

Aggregated BTC SpreadThis script is used to aggregate the bitcoin spread on futures contracts on different platforms.

It works by averaging the for every selected exchange, and apply an EMA of .

It is supporting

Binance (USD / USDT)

Okex

FTX

Huobi

Deribit

Ascendex

CME (BTC1!)

Stochastic Spread AnalyzerA comparative version of the previously published Stochastic Structure Analyzer. It incorporates the 3-TF stochastics against both price and OBV values of the spread.

Spread of ScriptsHello all

This indicator helps you to find spread between scripts.

Very much helpful for finding spread of script with relative future script. (Index or Stocks).

The are two methods to find spread –

1. Divide

2. Difference

You can select your choice from indicator settings.