Volume Flow Indicator Signals | iSolani

Volume Flow Indicator Signals | iSolani: Decoding Trend Momentum with Volume Precision

In markets where trends are fueled by institutional participation, discerning genuine momentum from false moves is critical. The Volume Flow Indicator Signals | iSolani cuts through this noise by synthesizing price action with volume dynamics, generating high-confidence signals when capital flows align with directional bias. This tool reimagines traditional volume analysis by incorporating volatility-adjusted thresholds and dual-layer smoothing, offering traders a laser-focused approach to trend identification.

Core Methodology

The indicator employs a multi-stage calculation to quantify volume-driven momentum:

Volatility-Adjusted Filter: Measures price changes via log returns, scaling significance using a 30-bar standard deviation multiplied by user-defined sensitivity (default: 2x).

Volume Normalization: Caps extreme volume spikes at 3x the 50-bar moving average, preventing distortion from anomalous trades.

Directional Volume Flow: Assigns positive/negative values to volume based on whether price movement exceeds volatility-derived thresholds.

Dual Smoothing: Applies consecutive SMA (3-bar) and EMA (14-bar) to create the Volume Flow Indicator (VFI) and its signal line, filtering out transient fluctuations.

Breaking New Ground

This implementation introduces three key innovations:

Adaptive Noise Gates: Unlike static volume oscillators, the sensitivity coefficient dynamically adjusts to market volatility, reducing false signals during choppy conditions.

Institutional Volume Capping: The vcoef parameter limits the influence of outlier volume spikes, focusing on sustained institutional activity rather than one-off trades.

Non-Repainting Signals: Generates single-per-trend labels (buy below bars, sell above) to avoid chart clutter while maintaining visual clarity.

Engine Under the Hood

The script executes through five systematic stages:

Data Preparation: Computes HLC3 typical price and its logarithmic rate of change.

Threshold Calculation: Derives dynamic cutoff levels using 30-period volatility scaled by user sensitivity.

Volume Processing: Filters raw volume through a 50-bar SMA, capping extremes at 3x average.

VFI Construction: Sums directional volume flow over 50 bars, smoothed with a 3-bar SMA.

Signal Generation: Triggers alerts when VFI crosses zero, confirmed by a 14-bar EMA crossover.

Standard Configuration

Optimized defaults balance responsiveness and reliability:

Volume MA: 50-bar smoothing window

Sensitivity: 2.0 (doubles volatility threshold)

Signal Smoothing: 14-bar EMA

Volume Cap: 3x average (hidden parameter)

VFI Smoothing: Enabled (3-bar SMA)

By fusing adaptive volume filtering with price confirmation logic, the Volume Flow Indicator Signals | iSolani transforms raw market data into institutional-grade trend signals. Its ability to mute choppy price action while amplifying high-conviction volume moves makes it particularly effective for spotting early trend reversals in equities, forex, and futures markets.

Signals

TradFi Fundamentals: Enhanced Macroeconomic Momentum Trading Introduction

The "Enhanced Momentum with Advanced Normalization and Smoothing" indicator is a tool that combines traditional price momentum with a broad range of macroeconomic factors. I introduced the basic version from a research paper in my last script. This one leverages not only the price action of a security but also incorporates key economic data—such as GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and market volatility (VIX)—to create a comprehensive, normalized momentum score.

Previous indicator

Explanation

In plain terms, the indicator calculates a raw momentum value based on the change in price over a defined lookback period. It then normalizes this momentum, along with several economic indicators, using a method chosen by the user (options include simple, exponential, or weighted moving averages, as well as a median absolute deviation (MAD) approach). Each normalized component is assigned a weight reflecting its relative importance, and these weighted values are summed to produce an overall momentum score.

To reduce noise, the combined momentum score can be further smoothed using a user-selected method.

Signals

For generating trade signals, the indicator offers two modes:

Zero Cross Mode: Signals occur when the smoothed momentum line crosses the zero threshold.

Zone Mode: Overbought and oversold boundaries (which are user defined) provide signals when the momentum line crosses these preset limits.

Definition of the Settings

Price Momentum Settings:

Price Momentum Lookback: The number of days used to compute the percentage change in price (default 50 days).

Normalization Period (Price Momentum): The period over which the price momentum is normalized (default 200 days).

Economic Data Settings:

Normalization Period (Economic Data): The period used to normalize all economic indicators (default 200 days).

Normalization Method: Choose among SMA, EMA, WMA, or MAD to standardize both price and economic data. If MAD is chosen, a multiplier factor is applied (default is 1.4826).

Smoothing Options:

Apply Smoothing: A toggle to enable further smoothing of the combined momentum score.

Smoothing Period & Method: Define the period and type (SMA, EMA, or WMA) used to smooth the final momentum score.

Signal Generation Settings:

Signal Mode: Select whether signals are based on a zero-line crossover or by crossing user-defined overbought/oversold (OB/OS) zones.

OB/OS Zones: Define the upper and lower boundaries (default upper zones at 1.0 and 2.0, lower zones at -1.0 and -2.0) for zone-based signals.

Weights:

Each component (price momentum, GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and VIX) has an associated weight that determines its contribution to the overall score. These can be adjusted to reflect different market views or risk preferences.

Visual Aspects

The indicator plots the smoothed combined momentum score as a continuous blue line against a dotted zero-line reference. If the Zone signal mode is selected, the indicator also displays the upper and lower OB/OS boundaries as horizontal lines (red for overbought and green for oversold). Buy and sell signals are marked by small labels ("B" for buy and "S" for sell) that appear at the bottom or top of the chart when the score crosses the defined thresholds, allowing traders to quickly identify potential entry or exit points.

Conclusion

This enhanced indicator provides traders with a robust approach to momentum trading by integrating traditional price-based signals with a suite of macroeconomic indicators. Its normalization and smoothing techniques help reduce noise and mitigate the effects of outliers, while the flexible signal generation modes offer multiple ways to interpret market conditions. Overall, this tool is designed to deliver a more nuanced perspective on market momentum.

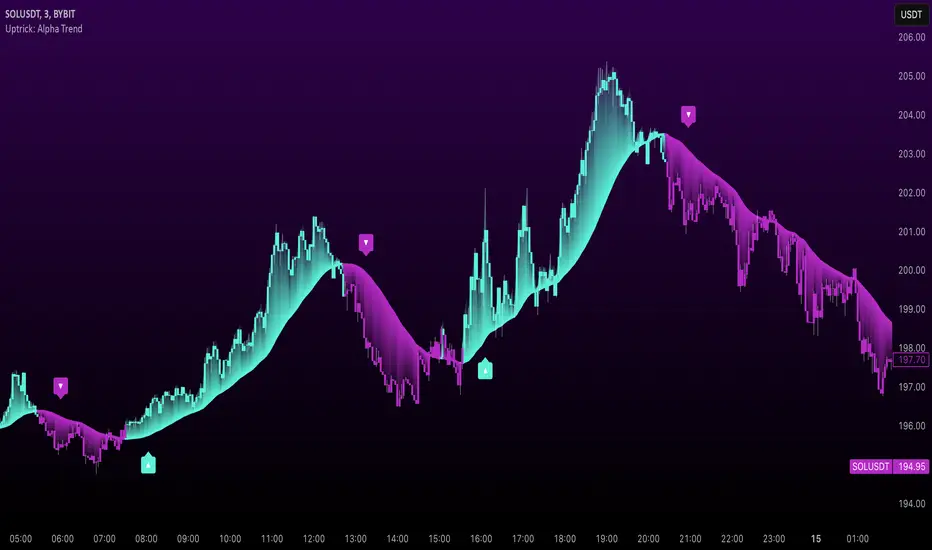

Uptrick: Alpha TrendIntroduction

Uptrick: Alpha Trend is a comprehensive technical analysis indicator designed to provide traders with detailed insights into market trends, momentum, and risk metrics. It adapts to various trading styles—from quick scalps to longer-term positions—by dynamically adjusting its calculations and visual elements. By combining multiple smoothing techniques, advanced color schemes, and customizable data tables, the indicator offers a holistic view of market behavior.

Originality

The Alpha Trend indicator distinguishes itself by blending established technical concepts with innovative adaptations. It employs three different smoothing techniques tailored to specific trading modes (Scalp, Swing, and Position), and it dynamically adjusts its parameters to match the chosen mode. The indicator also offers a wide range of color palettes and multiple on-screen tables that display key metrics. This unique combination of features, along with its ability to adapt in real time, sets it apart as a versatile tool for both novice and experienced traders.

Features

1. Multi-Mode Trend Line

The indicator automatically selects a smoothing method based on the trading mode:

- Scalp Mode uses the Hull Moving Average (HMA) for rapid responsiveness.

- Swing Mode employs the Exponential Moving Average (EMA) for balanced reactivity.

- Position Mode applies the Weighted Moving Average (WMA) for smoother, long-term trends.

Each method is chosen to best capture the price action dynamics appropriate to the trader’s timeframe.

2. Adaptive Momentum Thresholds

It tracks bullish and bearish momentum with counters that increment as the trend confirms directional movement. When these counters exceed a user-defined threshold, the indicator generates optional buy or sell signals. This approach helps filter out minor fluctuations and highlights significant market moves.

3. Gradient Fills

Two types of fills enhance visual clarity:

- Standard Gradient Fill displays ATR-based zones above and below the trend line, indicating potential bullish and bearish areas.

- Fading Gradient Fill creates a smooth transition between the trend line and the price, visually emphasizing the distance between them.

4. Bar Coloring and Signal Markers

The indicator can color-code bars based on market conditions—bullish, bearish, or neutral—allowing for immediate visual assessment. Additionally, signal markers such as buy and sell arrows are plotted when momentum thresholds are breached.

5. Comprehensive Data Tables

Uptrick: Alpha Trend offers several optional tables for detailed analysis:

- Insider Info: Displays key metrics like the current trend value, bullish/bearish momentum counts, and ATR.

- Indicator Metrics: Lists input settings such as trend length, damping, signal threshold, and net momentum.

- Market Analysis: Summarizes overall trend direction, trend strength, Sortino ratio, return, and volatility.

- Price & Trend Dynamics: Details price deviation from the trend, trend slope, and ATR ratio.

- Momentum & Volatility Insights: Presents RSI, standard deviation (volatility), and net momentum.

- Performance & Acceleration Metrics: Focuses on the Sortino ratio, trend acceleration, return, and trend strength.

Each table can be positioned flexibly on the chart, allowing traders to customize the layout according to their needs.

Why It Combines Specific Smoothing Techniques

Smoothing techniques are essential for filtering out market noise and revealing underlying trends. The indicator combines three smoothing methods for the following reasons:

- The Hull Moving Average (HMA) in Scalp Mode minimizes lag and responds quickly to price changes, which is critical for short-term trading.

- The Exponential Moving Average (EMA) in Swing Mode gives more weight to recent data, striking a balance between speed and smoothness. This makes it suitable for mid-term trend analysis.

- The Weighted Moving Average (WMA) in Position Mode smooths out short-term fluctuations, offering a clear view of longer-term trends and reducing the impact of transient market volatility.

By using these specific methods in their respective trading modes, the indicator ensures that the trend line is appropriately responsive for the intended time frame, enhancing decision-making while maintaining clarity.

Inputs

1. Trend Length (Default: 30)

Defines the lookback period for the smoothing calculation. A shorter trend length results in a more responsive line, while a longer length produces a smoother, less volatile trend.

2. Trend Damping (Default: 0.75)

Controls the degree of smoothing applied to the trend line. Lower values lead to a smoother curve, whereas higher values increase sensitivity to price fluctuations.

3. Signal Strength Threshold (Default: 5)

Specifies the number of consecutive bullish or bearish bars required to trigger a signal. Higher thresholds reduce the frequency of signals, focusing on stronger moves.

4. Enable Bar Coloring (Default: True)

Toggles whether each price bar is colored to indicate bullish, bearish, or neutral conditions.

5. Enable Signals (Default: True)

When enabled, this option plots buy or sell arrows on the chart once the momentum thresholds are met.

6. Enable Standard Gradient Fill (Default: False)

Activates ATR-based gradient fills around the trend line to visualize potential support and resistance zones.

7. Enable Fading Gradient Fill (Default: True)

Draws a gradual color transition between the trend line and the current price, emphasizing their divergence.

8. Trading Mode (Options: Scalp, Swing, Position)

Determines which smoothing method and ATR period to use, adapting the indicator’s behavior to short-term, medium-term, or long-term trading.

9. Table Position Inputs

Allows users to select from nine possible chart positions (top, middle, bottom; left, center, right) for each data table.

10. Show Table Booleans

Separate toggles control the display of each table (Insider Info, Indicator Metrics, Market Analysis, and the three Deep Tables), enabling a customized view of the data.

Color Schemes

(Default) - The colors in the preview image of the indicator.

(Emerald)

(Sapphire)

(Golden Blaze)

(Mystic)

(Monochrome)

(Pastel)

(Vibrant)

(Earth)

(Neon)

Calculations

1. Trend Line Methods

- Scalp Mode: Utilizes the Hull Moving Average (HMA), which computes two weighted moving averages (one at half the length and one at full length), subtracts them, and then applies a final weighted average based on the square root of the length. This method minimizes lag and increases responsiveness.

- Swing Mode: Uses the Exponential Moving Average (EMA), which assigns greater weight to recent prices, thus balancing quick reaction with smoothness.

- Position Mode: Applies the Weighted Moving Average (WMA) to focus on longer-term trends by emphasizing the entire lookback period and reducing the impact of short-term volatility.

2. Momentum Tracking

The indicator maintains separate counters for bullish and bearish momentum. These counters increase as the trend confirms directional movement and reset when the trend reverses. When a counter exceeds the defined signal strength threshold, a corresponding signal (buy or sell) is triggered.

3. Volatility and ATR Zones

The Average True Range (ATR) is calculated using a period that adapts to the selected trading mode (shorter for Scalp, longer for Position). The ATR value is then used to define upper and lower zones around the trend line, highlighting the current level of market volatility.

4. Return and Trend Acceleration

- Return is calculated as the difference between the current and previous closing prices, providing a simple measure of price change.

- Trend Acceleration is derived from the change in the trend line’s movement (its first derivative) compared to the previous bar. This metric indicates whether the trend is gaining or losing momentum.

5. Sortino Ratio and Standard Deviation

- The Sortino Ratio measures risk-adjusted performance by comparing returns to downside volatility (only considering negative price changes).

- Standard Deviation is computed over the lookback period to assess the extent of price fluctuations, offering insights into market stability.

Usage

This indicator is suitable for various time frames and market instruments. Traders can enable or disable specific visual elements such as gradient fills, bar coloring, and signal markers based on their preference. For a minimalist approach, one might choose to display only the primary trend line. For a deeper analysis, enabling multiple tables can provide extensive data on momentum, volatility, trend dynamics, and risk metrics.

Important Note on Risk

Trading involves inherent risk, and no indicator can eliminate the uncertainty of the markets. Past performance is not indicative of future results. It is essential to use proper risk management, test any new tool thoroughly, and consult multiple sources or professional advice before making trading decisions.

Conclusion

Uptrick: Alpha Trend unifies a diverse set of calculations, adaptive smoothing techniques, and customizable visual elements into one powerful tool. By combining the Hull, Exponential, and Weighted Moving Averages, the indicator is able to provide a trend line that is both responsive and smooth, depending on the trading mode. Its advanced color schemes, gradient fills, and detailed data tables deliver a comprehensive analysis of market trends, momentum, and risk. Whether you are a short-term trader or a long-term investor, this indicator aims to clarify price action and assist you in making more informed trading decisions.

ZenAlgo - QZenAlgo - Q

Description

ZenAlgo - Q is an oscillator based on the QQE (Quantitative Qualitative Estimation) method. This version incorporates refinements for additional visualization and interpretation options. It is designed to help traders observe momentum changes and divergence patterns in price movements.

Key Features

QQE-Based Calculation : Derived from the open-source QQE script by Glaz (Metastock Version of QQE), with modifications for alternative visualization.

Dual RSI-Based Analysis : Uses two RSI calculations to provide additional context on price movements.

Adaptive Trend Bands : Adjust dynamically based on the market conditions.

Divergence Identification : Highlights potential differences between price action and oscillator movement.

Dynamic Color Coding : Displays histogram bars to illustrate shifts in oscillator values.

Configurable Alerts : Enables notifications for specific oscillator conditions.

How It Works

The indicator calculates a smoothed RSI-based oscillator that tracks the relative strength of price movement. It applies an exponential moving average (EMA) smoothing to reduce noise while maintaining responsiveness.

Two adaptive bands are calculated using a variation of the QQE method, which helps define dynamic overbought and oversold conditions.

The histogram bars shift in color based on the position of the oscillator relative to the bands. Lighter shades indicate weaker momentum, while stronger momentum is represented by more saturated colors.

The script also includes a secondary RSI component, which provides an additional layer of analysis. This secondary RSI helps refine momentum trends by smoothing out short-term fluctuations.

Divergence identification is built-in, highlighting where price action deviates from oscillator readings. Bullish divergence occurs when price forms a lower low while the oscillator forms a higher low, and bearish divergence is identified when price forms a higher high while the oscillator forms a lower high.

The indicator does not generate buy or sell signals but instead provides contextual information that can be used alongside other trading strategies.

Use Cases

Trend Observation : Traders can use the histogram to observe whether momentum is strengthening or weakening over time. A shift in color can indicate a potential change in trend strength.

Divergence Analysis : By comparing oscillator divergence with price movement, traders can identify situations where price action may be losing momentum. Divergences do not guarantee reversals but can serve as an early warning to re-evaluate positions.

Momentum Tracking : The dual RSI structure allows users to monitor both short-term and long-term momentum. When both RSI components are aligned, it suggests a more stable trend, while divergence between them may indicate potential consolidation or trend shifts.

Supplementary Analysis : This indicator is best used as a supporting tool alongside volume-based or trend-following indicators. It helps visualize underlying price behavior but should not be used in isolation for decision-making.

Market Context Interpretation : The combination of adaptive bands and histogram visualization allows traders to assess how recent price action compares to historical movement, helping to place current conditions in a broader market context.

Attribution

This script is an adaptation of the open-source QQE script originally developed by Glaz. We acknowledge and appreciate the original author's work, which served as a foundation for our modifications.

Disclaimer

This indicator is intended for informational purposes only. It should not be interpreted as financial advice. Always conduct independent research and risk management before making trading decisions.

Trending Market Toolkit [LuxAlgo]The Trending Market Toolkit focuses exclusively on trending market structures and high-confluence, high-risk-to-reward entry models. It is designed to complement discretionary trading by offering different entry strategies based on market structure.

🔶 USAGE

In the chart above we can see how the tool detects several reversals, draws the broken trendlines, the reversal areas from which the tool starts looking for a trigger, and when it finally happens, a potential trade with risk and reward areas and the risk/reward ratio.

🔹 Detection Mode

Traders can choose between three different modes: trend only, reversal only, or both.

If both are active, reversals have priority over trends, so the tool will not detect a trend if a reversal is active.

In the chart above we can see all three modes.

🔹 Detection on Higher Timeframes

Traders can choose to identify structures on the chart timeframe or on a higher timeframe.

In the chart above, we have the SP500 futures on the 5m timeframe with different settings: chart timeframe, 30m, and 1H.

🔹 Risk And Targets

Depending on whether the high-risk/reward parameter is enabled, traders can choose between three different targets and two different stops.

The chart above shows how different choices affect the risk/reward ratio for the same potential trade on the Gold Futures 2m chart.

🔶 SETTINGS

Show: Traders can choose between Trends, Reversals or Both.

🔹 Structures

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

Custom Timeframe: Traders can make use of the current chart timeframe, or choose a custom timeframe.

Reversal Area Threshold: A higher number increases the reversal area.

🔹 Trades

Trade Trigger Length: Number of candles to confirm an internal high or internal low. A lower number detects smaller swings. It must be the same size or smaller than the swing length.

Target: Traders can choose between the default target (0) or two extended targets (0.27 or 0.618).

Risk to Reward Threshold: Set the minimum risk-to-reward ratio to detect trades. Use the 0 value to detect all trades.

High Risk to Reward: Enable/Disable the high risk to reward mode.

Time-based Alerts for Trading Windows🌟 Time-based Alerts for Trading Windows 🌐📈

This is a re-uploaded script as the previous one got hidden.

This Time-based Alerts for Trading Windows script is a highly customizable and reliable tool designed to assist traders in managing automated strategies or manually monitoring specific market conditions. Inspired by CrossTrade's Time-based Alert, this script is tailored for those who rely on precise time windows to trigger actions, such as sending webhook signals or managing Expert Advisors (EAs).

Whether you are a scalper, day trader, or algorithmic trader, this script empowers you to stay on top of your trades with fully customizable time-based alerts.

🛠️ Customizable Time Alerts

This indicator allows you to create up to 12 unique time windows by specifying the exact hour and minute for each alert. Each time window corresponds to an individual alert condition, making it perfect for managing trades during specific market sessions or key time periods.

For example:

Alert 1 can be set at 9:30 AM (market open).

Alert 2 can be set at 3:55 PM (just before market close).

Each alert can be toggled on or off in the indicator settings, allowing you to manage alerts without having to reconfigure your script.

You can adjust the colours to fit any colour scheme you like!

🕒 Odd and Even Time Alerts

The script comes with three built-in alert type categories:

Odd Alerts (marked with a green triangle on the chart): These correspond to odd-numbered inputs like Alert 1, Alert 3, Alert 5, and so on.

Even Alerts (marked with a red triangle on the chart): These correspond to even-numbered inputs like Alert 2, Alert 4, Alert 6, and so on.

You can also customize all 12 alerts individually to include a custom alert message

These alerts serve as a convenient way to differentiate between multiple trading strategies or market conditions. You can customize alert messages for odd and even alerts directly from TradingView’s alert panel.

🔗 Webhook Integration for Automation

This script is fully compatible with webhook-based automation. By configuring your alerts in TradingView, you can send signals to trading bots, EAs, or any third-party system. For example, you can:

Turn off an EA at a specific time (e.g., 3:55 PM EST).

Send buy/sell signals to your bot during predefined trading windows.

Simply use TradingView’s alert message editor to format webhook payloads for your automation system.

🌐 Timezone Flexibility

Trading happens across multiple time zones, and this script accounts for that. You can toggle between:

Eastern Time (New York): Ideal for most US-based markets.

Central Time (Exchange): Useful for futures and commodities traders.

This ensures your alerts are always in sync with your preferred time zone, eliminating confusion.

🎨 Visual Indicators

The script plots visual markers directly on your chart to indicate active alerts:

Up Facing Triangles: Represent odd-numbered alerts, providing a quick reference for these time windows.

Down Facing Triangles: Represent even-numbered alerts, helping you track different strategies or conditions.

These visual markers make it easy to see when alerts are triggered, even at a glance.

📈 Practical Use Case

Let’s say you’re trading the USTEC index on a 1-minute chart. You want to:

Turn off your trading bot at 16:55 EST to avoid after-market volatility.

Trigger a re-entry signal at 17:30 EST to capture moves during the Asian session.

Visually monitor these actions on your chart for easy reference.

This script makes it possible with precision alerts and webhook integration. Simply configure the time windows in the settings and set up your alerts in TradingView.

🚨 How to Set Up Alerts

Enable or Disable Alerts: Use the script’s settings to toggle specific alerts on or off as needed.

Set Custom Time Windows: Define the hour and minute for each alert in the settings panel.

Create Alerts in TradingView:

Go to the TradingView alert panel.

Select the condition (e.g., "Odd Time-based Alert (Green)" or "Even Time-based Alert (Red)").

Customize the alert message for webhook integration or personal notification.

Choose the trigger type: Once Per Bar or Once Per Bar Close to keep the alert active.

Integrate with Webhooks: Use the alert message field to format payloads for automation systems like MT4, MT5, or third-party bots.

📋 Key Notes

Alerts can trigger indefinitely if set to "Once Per Bar" or "Once Per Bar Close".

Always ensure the expiration date is set far in the future to avoid unexpected alert deactivation.

Test webhook messages and alert configurations thoroughly before using them in live trading.

This script is a powerful addition to your trading toolbox, offering precision, flexibility, and automation capabilities. Whether you’re turning off an EA, managing trades during market sessions, or automating strategies via webhooks, this script is here to support you.

Start using the Time-based Alerts for Trading Windows today and trade with confidence! 🚀✨

TradFi Fundamentals: Momentum Trading with Macroeconomic DataIntroduction

This indicator combines traditional price momentum with key macroeconomic data. By retrieving GDP, inflation, unemployment, and interest rates using security calls, the script automatically adapts to the latest economic data. The goal is to blend technical analysis with fundamental insights to generate a more robust momentum signal.

Original Research Paper by Mohit Apte, B. Tech Scholar, Department of Computer Science and Engineering, COEP Technological University, Pune, India

Link to paper

Explanation

Price Momentum Calculation:

The indicator computes price momentum as the percentage change in price over a configurable lookback period (default is 50 days). This raw momentum is then normalized using a rolling simple moving average and standard deviation over a defined period (default 200 days) to ensure comparability with the economic indicators.

Fetching and Normalizing Economic Data:

Instead of manually inputting economic values, the script uses TradingView’s security function to retrieve:

GDP from ticker "GDP"

Inflation (CPI) from ticker "USCCPI"

Unemployment rate from ticker "UNRATE"

Interest rates from ticker "USINTR"

Each series is normalized over a configurable normalization period (default 200 days) by subtracting its moving average and dividing by its standard deviation. This standardization converts each economic indicator into a z-score for direct integration into the momentum score.

Combined Momentum Score:

The normalized price momentum and economic indicators are each multiplied by user-defined weights (default: 50% price momentum, 20% GDP, and 10% each for inflation, unemployment, and interest rates). The weighted components are then summed to form a comprehensive momentum score. A horizontal zero line is plotted for reference.

Trading Signals:

Buy signals are generated when the combined momentum score crosses above zero, and sell signals occur when it crosses below zero. Visual markers are added to the chart to assist with trade timing, and alert conditions are provided for automated notifications.

Settings

Price Momentum Lookback: Defines the period (in days) used to compute the raw price momentum.

Normalization Period for Price Momentum: Sets the window over which the price momentum is normalized.

Normalization Period for Economic Data: Sets the window over which each macroeconomic series is normalized.

Weights: Adjust the influence of each component (price momentum, GDP, inflation, unemployment, and interest rate) on the overall momentum score.

Conclusion

This implementation leverages TradingView’s economic data feeds to integrate real-time macroeconomic data into a momentum trading strategy. By normalizing and weighting both technical and economic inputs, the indicator offers traders a more holistic view of market conditions. The enhanced momentum signal provides additional context to traditional momentum analysis, potentially leading to more informed trading decisions and improved risk management.

The next script I release will be an improved version of this that I have added my own flavor to, improving the signals.

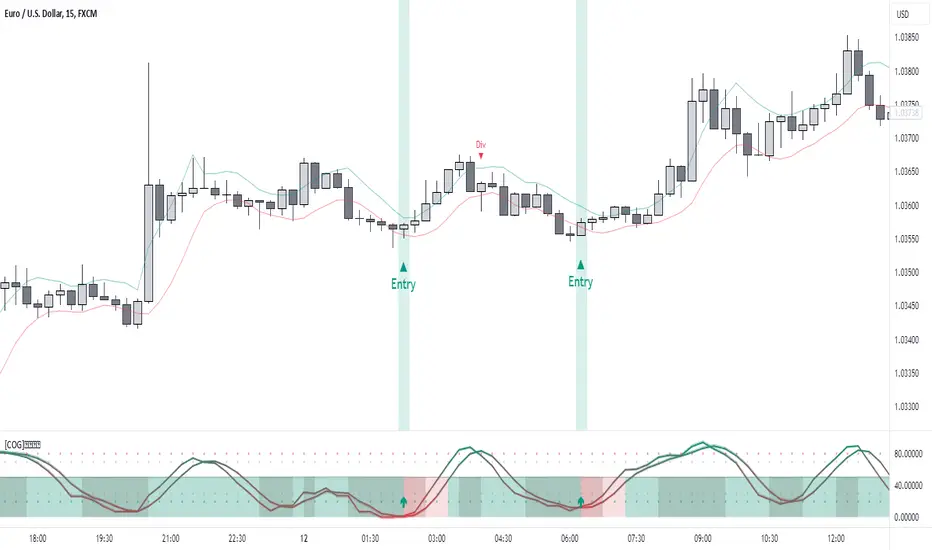

[COG]StochRSI Zenith📊 StochRSI Zenith

This indicator combines the traditional Stochastic RSI with enhanced visualization features and multi-timeframe analysis capabilities. It's designed to provide traders with a comprehensive view of market conditions through various technical components.

🔑 Key Features:

• Advanced StochRSI Implementation

- Customizable RSI and Stochastic calculation periods

- Multiple moving average type options (SMA, EMA, SMMA, LWMA)

- Adjustable signal line parameters

• Visual Enhancement System

- Dynamic wave effect visualization

- Energy field display for momentum visualization

- Customizable color schemes for bullish and bearish signals

- Adaptive transparency settings

• Multi-Timeframe Analysis

- Higher timeframe confirmation

- Synchronized market structure analysis

- Cross-timeframe signal validation

• Divergence Detection

- Automated bullish and bearish divergence identification

- Customizable lookback period

- Clear visual signals for confirmed divergences

• Signal Generation Framework

- Price action confirmation

- SMA-based trend filtering

- Multiple confirmation levels for reduced noise

- Clear entry signals with customizable display options

📈 Technical Components:

1. Core Oscillator

- Base calculation: 13-period RSI (adjustable)

- Stochastic calculation: 8-period (adjustable)

- Signal lines: 5,3 smoothing (adjustable)

2. Visual Systems

- Wave effect with three layers of visualization

- Energy field display with dynamic intensity

- Reference bands at 20/30/50/70/80 levels

3. Confirmation Mechanisms

- SMA trend filter

- Higher timeframe alignment

- Price action validation

- Divergence confirmation

⚙️ Customization Options:

• Visual Parameters

- Wave effect intensity and speed

- Energy field sensitivity

- Color schemes for bullish/bearish signals

- Signal display preferences

• Technical Parameters

- All core calculation periods

- Moving average types

- Divergence detection settings

- Signal confirmation criteria

• Display Settings

- Chart and indicator signal placement

- SMA line visualization

- Background highlighting options

- Label positioning and size

🔍 Technical Implementation:

The indicator combines several advanced techniques to generate signals. Here are key components with code examples:

1. Core StochRSI Calculation:

// Base RSI calculation

rsi = ta.rsi(close, rsi_length)

// StochRSI transformation

stochRSI = ((ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) != 0) ?

(100 * (rsi - ta.lowest(rsi, stoch_length))) /

(ta.highest(rsi, stoch_length) - ta.lowest(rsi, stoch_length)) : 0

2. Signal Generation System:

// Core signal conditions

crossover_buy = crossOver(sk, sd, cross_threshold)

valid_buy_zone = sk < 30 and sd < 30

price_within_sma_bands = close <= sma_high and close >= sma_low

// Enhanced signal generation

if crossover_buy and valid_buy_zone and price_within_sma_bands and htf_allows_long

if is_bullish_candle

long_signal := true

else

awaiting_bull_confirmation := true

3. Multi-Timeframe Analysis:

= request.security(syminfo.tickerid, mtf_period,

)

The HTF filter looks at a higher timeframe (default: 4H) to confirm the trend

It only allows:

Long trades when the higher timeframe is bullish

Short trades when the higher timeframe is bearish

📈 Trading Application Guide:

1. Signal Identification

• Oversold Opportunities (< 30 level)

- Look for bullish crosses of K-line above D-line

- Confirm with higher timeframe alignment

- Wait for price action confirmation (bullish candle)

• Overbought Conditions (> 70 level)

- Watch for bearish crosses of K-line below D-line

- Verify higher timeframe condition

- Confirm with bearish price action

2. Divergence Trading

• Bullish Divergence

- Price makes lower lows while indicator makes higher lows

- Most effective when occurring in oversold territory

- Use with support levels for entry timing

• Bearish Divergence

- Price makes higher highs while indicator shows lower highs

- Most reliable in overbought conditions

- Combine with resistance levels

3. Wave Effect Analysis

• Strong Waves

- Multiple wave lines moving in same direction indicate momentum

- Wider wave spread suggests increased volatility

- Use for trend strength confirmation

• Energy Field

- Higher intensity in trading zones suggests stronger moves

- Use for momentum confirmation

- Watch for energy field convergence with price action

The energy field is like a heat map that shows momentum strength

It gets stronger (more visible) when:

Price is in oversold (<30) or overbought (>70) zones

The indicator lines are moving apart quickly

A strong signal is forming

Think of it as a "strength meter" - the more visible the energy field, the stronger the potential move

4. Risk Management Integration

• Entry Confirmation

- Wait for all signal components to align

- Use higher timeframe for trend direction

- Confirm with price action and SMA positions

• Stop Loss Placement

- Consider placing stops beyond recent swing points

- Use ATR for dynamic stop calculation

- Account for market volatility

5. Position Management

• Partial Profit Taking

- Consider scaling out at overbought/oversold levels

- Use wave effect intensity for exit timing

- Monitor energy field for momentum shifts

• Trade Duration

- Short-term: Use primary signals in trading zones

- Swing trades: Focus on divergence signals

- Position trades: Utilize higher timeframe signals

⚠️ Important Usage Notes:

• Avoid:

- Trading against strong trends

- Relying solely on single signals

- Ignoring higher timeframe context

- Over-leveraging based on signals

Remember: This tool is designed to assist in analysis but should never be used as the sole decision-maker for trades. Always maintain proper risk management and combine with other forms of analysis.

[SHORT ONLY] 10 Bar Low Pullback█ STRATEGY DESCRIPTION

The "10 Bar Low Pullback" strategy is a contrarian short trading system designed to capture pullbacks after a new 10‐bar low is made. it identifies a potential short opportunity when the current bar’s low breaks below the lowest low of the previous 10 bars, provided that the bar exhibits strong internal momentum as measured by its IBS value. An optional trend filter further refines entries by requiring that the close is below a 200-period EMA.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

ibs = (close - low) / (high - low)

- Low IBS (≤ 0.2): Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8): Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current bar’s low is below the lowest low of the past X bars (default: 10).

The bar’s IBS is greater than the specified threshold (default: 0.85).

The signal occurs within the defined trading window (between Start Time and End Time).

If the EMA Filter is enabled, the close must be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

Lookback Period: Defines the number of bars (default is 10) over which the lowest low is calculated.

IBS Threshold: Sets the minimum required IBS value (default is 0.85) to qualify as a pullback.

Trading Window: Trades are only executed between the user-defined Start Time and End Time.

EMA Filter (Optional): When enabled, short entries are only considered if the current close is below the 200-period EMA, with the EMA period being adjustable (default is 200).

█ PERFORMANCE OVERVIEW

Designed for shorting opportunities, this strategy aims to capture pullbacks following an aggressive 10-bar low break.

It leverages a combination of a lookback low and IBS measurement to identify overextended bullish moves that may revert.

The optional EMA filter helps confirm a bearish market environment by ensuring the price remains under the trend line.

Suitable for use on various assets, including stocks and ETFs, on daily or similar timeframes.

Backtesting and parameter optimization are recommended to tailor the strategy to specific market conditions.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

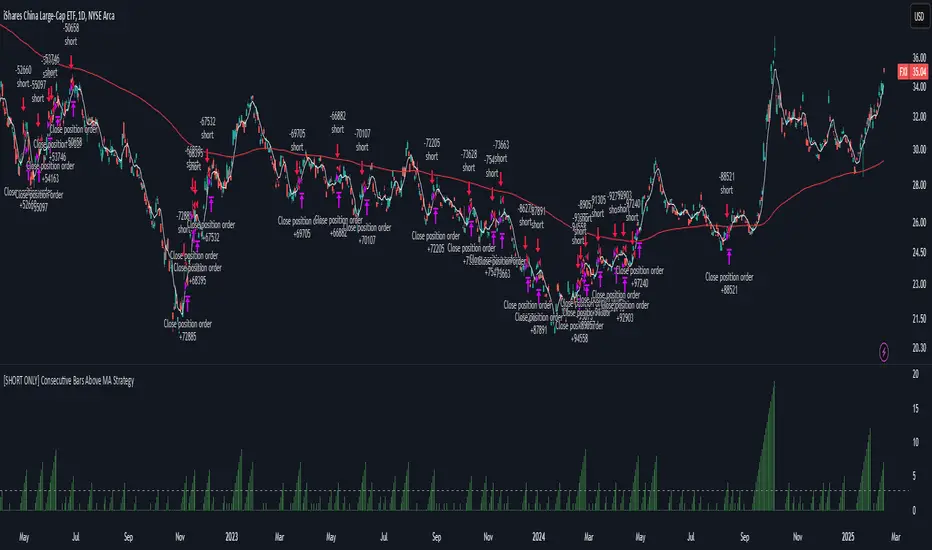

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

[SHORT ONLY] Consecutive Close>High[1] Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Consecutive Close > High " Mean Reversion Strategy is a contrarian daily trading system for stocks and ETFs. It identifies potential shorting opportunities by counting consecutive days where the closing price exceeds the previous day's high. When this consecutive day count reaches a predetermined threshold, and if the close is below a 200-period EMA (if enabled), a short entry is triggered, anticipating a corrective pullback.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy uses a counter variable called `bullCount` to track how many consecutive bars meet a bullish condition. Here’s a breakdown of the process:

Initialize the Counter

var int bullCount = 0

Bullish Bar Detection

Every time the close exceeds the previous bar's high, increment the counter:

if close > high

bullCount += 1

Reset on Bearish Bar

When there is a clear bearish reversal, the counter is reset to zero:

if close < low

bullCount := 0

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The count of consecutive bullish closes (where close > high ) reaches or exceeds the defined threshold (default: 3).

The signal occurs within the specified trading window (between Start Time and End Time).

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish closes required to trigger a short entry (default is 3).

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

EMA Filter (Optional): When enabled, short entries are only triggered if the current close is below the 200-period EMA.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs on the Daily timeframe and targets overextended bullish moves.

It aims to capture mean reversion by entering short after a series of consecutive bullish closes.

Further optimization is possible with additional filters (e.g., EMA, volume, or volatility).

Backtesting should be used to fine-tune the threshold and filter settings for specific market conditions.

[SHORT ONLY] Internal Bar Strength (IBS) Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a short position when the IBS indicates overbought conditions and exits when the IBS reaches oversold levels. This strategy is Short-Only and was designed to be used on the Daily timeframe for Stocks and ETFs.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- Low IBS (≤ 0.2) : Indicates the close is near the bar's low, suggesting oversold conditions.

- High IBS (≥ 0.8) : Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The IBS value rises to or above the Upper Threshold (default: 0.9).

The Closing price is greater than the previous bars High (close>high ).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

An exit Signal is generated when the IBS value drops to or below the Lower Threshold (default: 0.3). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy enters trades. Default is 0.9.

Lower Threshold: The IBS level at which the strategy exits short positions. Default is 0.3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for Stocks and ETFs markets and performs best when prices frequently revert to the mean.

The strategy can be optimized further using additional conditions such as using volume or volatility filters.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Range Filtered Trend Signals [AlgoAlpha]Introducing the Range Filtered Trend Signals , a cutting-edge trading indicator designed to detect market trends and ranging conditions with high accuracy. This indicator leverages a combination of Kalman filtering and Supertrend analysis to smooth out price fluctuations while maintaining responsiveness to trend shifts. By incorporating volatility-based range filtering, it ensures traders can differentiate between trending and ranging conditions effectively, reducing false signals and enhancing trade decision-making.

:key: Key Features

:white_check_mark: Kalman Filter Smoothing – Minimizes market noise while preserving trend clarity.

:bar_chart: Supertrend Integration – A dynamic trend-following mechanism for spotting reversals.

:fire: Volatility-Based Range Detection – Detects trending vs. ranging conditions with precision.

:art: Color-Coded Trend Signals – Instantly recognize bullish, bearish, and ranging market states.

:gear: Customizable Inputs – Fine-tune Kalman parameters, Supertrend settings, and color themes to match your strategy.

:bell: Alerts for Trend Shifts – Get real-time notifications when market conditions change!

:tools: How to Use

Add the Indicator – Click the star icon to add it to your TradingView favorites.

Analyze Market Conditions – Observe the color-coded signals and range boundaries to identify trend strength and direction.

Use Alerts for Trade Execution – Set alerts for trend shifts and market conditions to stay ahead without constantly monitoring charts.

:mag: How It Works

The Kalman filter smooths price fluctuations by dynamically adjusting its weighting based on market volatility. It helps remove noise while keeping the signal reactive to trend changes. The Supertrend calculation is then applied to the filtered price data, providing a robust trend-following mechanism. To enhance signal accuracy, a volatility-weighted range filter is incorporated, creating upper and lower boundaries that define trend conditions. When price breaks out of these boundaries, the indicator confirms trend continuation, while signals within the range indicate market consolidation. Traders can leverage this tool to enhance trade timing, filter false breakouts, and identify optimal entry/exit zones.

Price Step Channel [BigBeluga]Price Step Channel is designed to provide a structured look at price trends through a dynamic step line channel, highlighting trend direction and volatility boundaries.

🔵 Key Features:

Step Line with Boundaries: The central step line adjusts with price movements, creating upper and lower boundaries based on price volatility. The channel is green during uptrends and red during downtrends, visually signaling the trend’s direction.

Fakeout Markers: "✖" markers identify potential fakeouts—moments when the price breaches the channel boundary without confirming a trend change. These markers help you spot possible mean reversion points.

Dynamic Boundary Labels: Labels at the end of the channel show the price levels of the upper and lower boundaries. In uptrends, the upper label turns green; in downtrends, the lower label turns red, providing an instant read on the trend's direction.

Customizable Display: You can toggle off the boundaries and labels for a cleaner view, focusing only on the step line and its color-coded trend signals.

🔵 When to Use:

Price Step Channel is ideal for traders looking to follow structured trends with defined volatility boundaries. The step line and color-coded channel provide clear trend insights, while the fakeout markers and customizable display options enhance flexibility in different market conditions. Whether you’re focusing on clean trend signals or detailed boundary interactions, this tool adapts to your style.

[COG] Adaptive Squeeze Intensity 📊 Adaptive Squeeze Intensity (ASI) Indicator

🎯 Overview

The Adaptive Squeeze Intensity (ASI) indicator is an advanced technical analysis tool that combines the power of volatility compression analysis with momentum, volume, and trend confirmation to identify high-probability trading opportunities. It quantifies the degree of price compression using a sophisticated scoring system and provides clear entry signals for both long and short positions.

⭐ Key Features

- 📈 Comprehensive squeeze intensity scoring system (0-100)

- 📏 Multiple Keltner Channel compression zones

- 📊 Volume analysis integration

- 🎯 EMA-based trend confirmation

- 🎨 Proximity-based entry validation

- 📱 Visual status monitoring

- 🎨 Customizable color schemes

- ⚡ Clear entry signals with directional indicators

🔧 Components

1. 📐 Squeeze Intensity Score (0-100)

The indicator calculates a total squeeze intensity score based on four components:

- 📊 Band Convergence (0-40 points): Measures the relationship between Bollinger Bands and Keltner Channels

- 📍 Price Position (0-20 points): Evaluates price location relative to the base channels

- 📈 Volume Intensity (0-20 points): Analyzes volume patterns and thresholds

- ⚡ Momentum (0-20 points): Assesses price momentum and direction

2. 🎨 Compression Zones

Visual representation of squeeze intensity levels:

- 🔴 Extreme Squeeze (80-100): Red zone

- 🟠 Strong Squeeze (60-80): Orange zone

- 🟡 Moderate Squeeze (40-60): Yellow zone

- 🟢 Light Squeeze (20-40): Green zone

- ⚪ No Squeeze (0-20): Base zone

3. 🎯 Entry Signals

The indicator generates entry signals based on:

- ✨ Squeeze release confirmation

- ➡️ Momentum direction

- 📊 Candlestick pattern confirmation

- 📈 Optional EMA trend alignment

- 🎯 Customizable EMA proximity validation

⚙️ Settings

🔧 Main Settings

- Base Length: Determines the calculation period for main indicators

- BB Multiplier: Sets the Bollinger Bands deviation multiplier

- Keltner Channel Multipliers: Three separate multipliers for different compression zones

📈 Trend Confirmation

- Four customizable EMA periods (default: 21, 34, 55, 89)

- Optional trend requirement for entry signals

- Adjustable EMA proximity threshold

📊 Volume Analysis

- Customizable volume MA length

- Adjustable volume threshold for signal confirmation

- Option to enable/disable volume analysis

🎨 Visualization

- Customizable bullish/bearish colors

- Optional intensity zones display

- Status monitor with real-time score and state information

- Clear entry arrows and background highlights

💻 Technical Code Breakdown

1. Core Calculations

// Base calculations for EMAs

ema_1 = ta.ema(close, ema_length_1)

ema_2 = ta.ema(close, ema_length_2)

ema_3 = ta.ema(close, ema_length_3)

ema_4 = ta.ema(close, ema_length_4)

// Proximity calculation for entry validation

ema_prox_raw = math.abs(close - ema_1) / ema_1 * 100

is_close_to_ema_long = close > ema_1 and ema_prox_raw <= prox_percent

```

### 2. Squeeze Detection System

```pine

// Bollinger Bands setup

BB_basis = ta.sma(close, length)

BB_dev = ta.stdev(close, length)

BB_upper = BB_basis + BB_mult * BB_dev

BB_lower = BB_basis - BB_mult * BB_dev

// Keltner Channels setup

KC_basis = ta.sma(close, length)

KC_range = ta.sma(ta.tr, length)

KC_upper_high = KC_basis + KC_range * KC_mult_high

KC_lower_high = KC_basis - KC_range * KC_mult_high

```

### 3. Scoring System Implementation

```pine

// Band Convergence Score

band_ratio = BB_width / KC_width

convergence_score = math.max(0, 40 * (1 - band_ratio))

// Price Position Score

price_range = math.abs(close - KC_basis) / (KC_upper_low - KC_lower_low)

position_score = 20 * (1 - price_range)

// Final Score Calculation

squeeze_score = convergence_score + position_score + vol_score + mom_score

```

### 4. Signal Generation

```pine

// Entry Signal Logic

long_signal = squeeze_release and

is_momentum_positive and

(not use_ema_trend or (bullish_trend and is_close_to_ema_long)) and

is_bullish_candle

short_signal = squeeze_release and

is_momentum_negative and

(not use_ema_trend or (bearish_trend and is_close_to_ema_short)) and

is_bearish_candle

```

📈 Trading Signals

🚀 Long Entry Conditions

- Squeeze release detected

- Positive momentum

- Bullish candlestick

- Price above relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

🔻 Short Entry Conditions

- Squeeze release detected

- Negative momentum

- Bearish candlestick

- Price below relevant EMAs (if enabled)

- Within EMA proximity threshold (if enabled)

- Sufficient volume confirmation (if enabled)

⚠️ Alert Conditions

- 🔔 Extreme squeeze level reached (score crosses above 80)

- 🚀 Long squeeze release signal

- 🔻 Short squeeze release signal

💡 Tips for Usage

1. 📱 Use the status monitor to track real-time squeeze intensity and state

2. 🎨 Pay attention to the color gradient for trend direction and strength

3. ⏰ Consider using multiple timeframes for confirmation

4. ⚙️ Adjust EMA and proximity settings based on your trading style

5. 📊 Use volume analysis for additional confirmation in liquid markets

📝 Notes

- 🔧 The indicator combines multiple technical analysis concepts for robust signal generation

- 📈 Suitable for all tradable markets and timeframes

- ⭐ Best results typically achieved in trending markets with clear volatility cycles

- 🎯 Consider using in conjunction with other technical analysis tools for confirmation

⚠️ Disclaimer

This technical indicator is designed to assist in analysis but should not be considered as financial advice. Always perform your own analysis and risk management when trading.

Adaptive Resonance Oscillator [AlgoAlpha]Introducing the Adaptive Resonance Oscillator , an advanced momentum-based oscillator designed to dynamically adjust to changing market conditions. This innovative indicator detects market frequency through a Hilbert Transform approach, adapting in real-time to identify overbought and oversold conditions with improved accuracy. With built-in divergence detection, trend analysis, and customizable smoothing, this tool is perfect for traders looking to refine their entries and exits based on adaptive oscillation mechanics.

🚀 Key Features :

🔹 Adaptive Frequency Detection – Uses Hilbert Transform principles to dynamically determine market cycle length for precise oscillator calculation.

⚙️ Customizable Smoothing – Option to apply a Hull Moving Average (HMA) for enhanced signal clarity.

📈 Divergence Detection – Identifies bullish and bearish divergences with visual markers, helping traders spot early trend reversals.

🟢 Overbought & Oversold Signals – Highlights extreme momentum conditions with adjustable thresholds.

🔔 Real-Time Alerts – Get notified for crossovers, divergences, and strong trend shifts directly on your TradingView chart.

🎨 Fully Customizable Appearance – Modify colors, divergence sensitivity, and smoothing options to fit your trading style.

🛠 How to Use :

Add the Adaptive Resonance Oscillator to your TradingView chart by clicking the ★ to favorite it.

Monitor the Charts , switch between smoothed and I smoothed modes to identify trend and price swings, use divergences and reversal signals for potential entry/exits.

Set alerts for bullish/bearish crossovers and divergence signals to stay ahead of market moves.

⚙ How It Works :

The indicator begins by applying a Hilbert Transform frequency estimation to the price series, identifying the dominant market cycle length. This is used to calculate a period for the RSI that matches its resonant frequency with the dominant market frequency, dynamically adjusting the Oscillator. The oscillator then applies an optional Hull Moving Average (HMA) smoothing for signal refinement. Additionally, the indicator scans for bullish and bearish divergences by comparing oscillator movements against price action, plotting signals accordingly. When overbought/oversold conditions or divergence events occur, alerts are triggered to notify the trader in real time.

[COG] WeatherForecaster🌤️ Just like a weather forecast that adjusts as new data emerges, this TMA Pivot Points Forecaster adapts to evolving market conditions!

Description:

This indicator combines the power of a Triple Moving Average (TMA) with pivot point analysis to identify potential market turning points and trend directions. Like a meteorologist using various atmospheric data to predict weather patterns, this tool analyzes price action through multiple lenses to forecast potential market movements.

Key Features:

- Dynamic TMA Line: Acts as our "atmospheric pressure system," showing the underlying market direction

- Adaptive Pivot Points: Like weather stations, these pivots identify key market levels where the "climate" might change

- Smart Entry Signals: ☀️ and 🌧️ icons appear when conditions align for potential trades

- Timeframe-Adaptive: Automatically adjusts sensitivity across different timeframes

- Customizable Visuals: Adjust colors and styles to match your trading environment

Settings Include:

✓ TMA Length and Slope Sensitivity

✓ Pivot Point Parameters

✓ Visual Customization Options

✓ Toggle Entry Signals

✓ Toggle Pivot Lines

Note: Like weather forecasts that update with new data, this indicator recalculates as market conditions evolve. Past signals may adjust as more price action develops. Always use proper risk management and combine with other analysis tools.

Usage Guide:

The indicator works best when used as part of a complete trading system. Here's how to interpret the signals:

📈 Bullish Conditions:

- TMA Line turns green: Indicates upward momentum

- "Buy above 🌋" level appears: Potential resistance turned support level

- ☀️ Signal: Indicates favorable buying conditions

📉 Bearish Conditions:

- TMA Line turns red: Indicates downward momentum

- "Sell below 🌋" level appears: Potential support turned resistance level

- 🌧️ Signal: Indicates favorable selling conditions

⏺️ Ranging Conditions:

- TMA Line turns yellow: Market in consolidation

- 💤 Signal: Suggests waiting for clearer direction

Best Practices:

1. Higher timeframes (4H, Daily) tend to produce more reliable signals

2. Use the pivot lines as potential entry/exit reference points

3. Adjust the TMA length based on your trading style:

• Shorter lengths (20-30) for more active trading

• Longer lengths (50-60) for trend following

Settings Explained:

TMA Settings:

- TMA Length: Determines the smoothing period (default: 30)

- Slope Threshold: Controls trend sensitivity (default: 0.015)

Pivot Settings:

- Left/Right Bars: Controls pivot point calculation

- Line Length: Adjusts the visual length of pivot lines

- Line Style & Colors: Customize the visual appearance

Disclaimer:

Past performance does not guarantee future results. This indicator, like any technical tool, provides possibilities rather than certainties. Please test thoroughly on your preferred timeframes and markets before using with real capital.

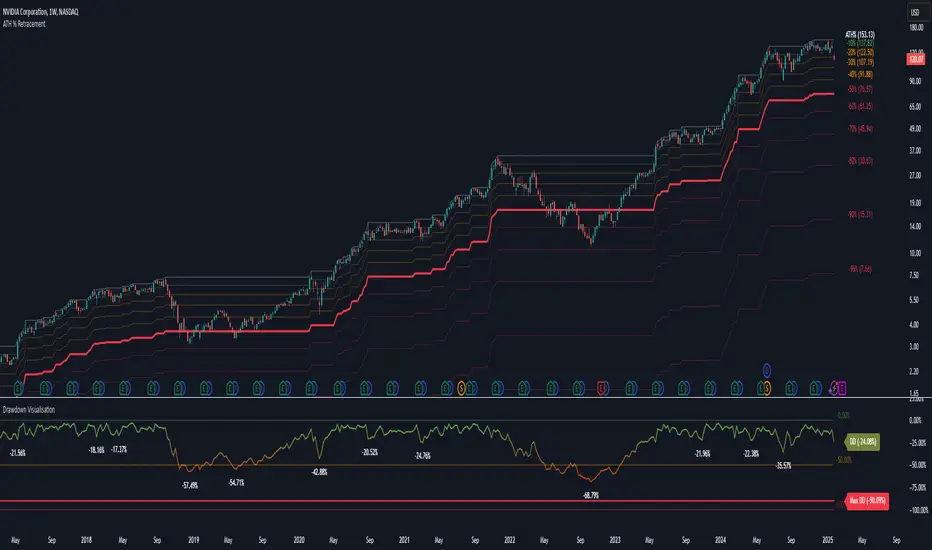

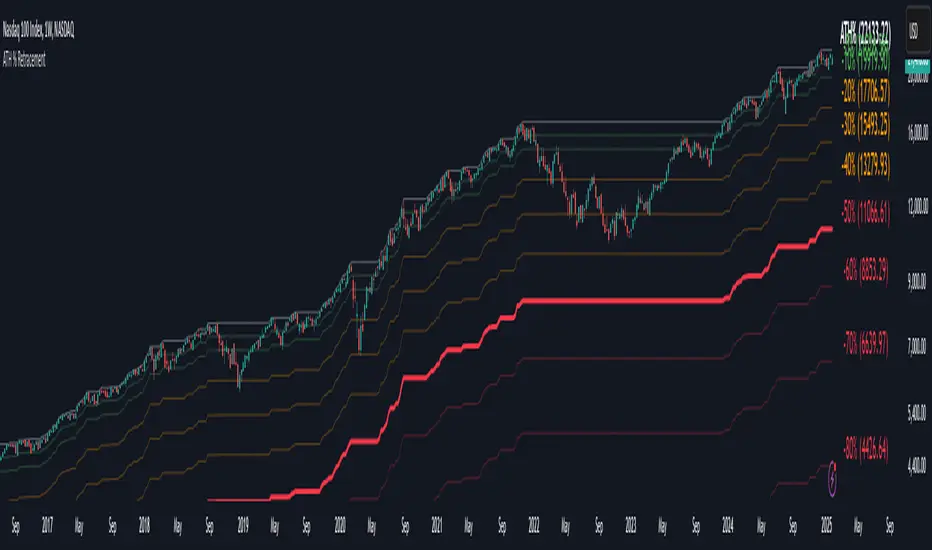

Drawdown Visualisation█ OVERVIEW

The Drawdown Visualisation indicator calculates and displays the instrument’s drawdown (in percent) relative to its all‐time high (ATH) from a user‐defined start date. It provides customisable options for label appearance, threshold lines (0%, –50%, –100%), and can plot historic drawdown levels via pivot detection.

█ USAGE

This indicator should be used with the Percentage Retracement from ATH indicator.

█ KEY FEATURES

Custom Date Settings — Use a custom start date so that only specified price action is considered.

Retracement Level Calculation — Determines ATH and computes multiple retracement levels using percentages from 0% to –100%.

Visual Signals and Customisation — Plots configurable horizontal lines and labels that display retracement percentages and prices.

Time Filtering — Bases calculations on data from the desired time period.

Historic Drawdowns — Display historical drawdowns

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

Percentage Retracement from ATH█ OVERVIEW

The Percentage Retracement from ATH indicator is a dynamic trading utility designed to help traders gauge market pullbacks from the peak price. By calculating key retracement levels based on the All-Time High (ATH) and user‑defined percentage inputs, it offers clear visual cues to assist in identifying potential support and resistance zones.

█ KEY FEATURES

Custom Date — Use a custom start date so the indicator only considers specified price action.

Retracement Calculation — Determines ATH and calculates levels based on user‑defined percentages (0% to –100%).

Visual Customisation — Plots configurable horizontal lines and labels showing retracement percentages and prices.

Time Filtering — Uses time filtering to base levels on the desired data period.

█ PURPOSE

Assist traders in visualising the depth of price retracements from recent or historical peaks.

Identify critical zones where the market may find support or resistance after reaching an ATH.

Facilitate more informed entry and exit decisions by clearly demarcating retracement levels on the chart.

█ IDEAL USERS

Swing Traders — Looking to exploit pullbacks following strong upward moves.

Technical Analysts — Interested in pinpointing key retracement levels as potential reversal or continuation points.

Price Action Traders — Focused on the nuances of market peaks and subsequent corrections.

Strategy Developers — Keen to backtest and refine approaches centred on retracement dynamics.

Triple Trend Indicator [BigBeluga]Triple Trend Indicator is a versatile trend-following tool designed to help traders identify trend strength and potential pullback levels using a three-band system. Each band represents a varying degree of price deviation from the mean, providing progressively stronger trend signals.

🔵 Key Features:

Three Adaptive Bands:

The indicator dynamically calculates three bands (1, 2, and 3) based on moving averages (SMA, EMA, WMA) and ATR multipliers.

Bands are positioned below the price in an uptrend and above the price in a downtrend, offering clear trend direction visualization.

Signal System:

Signals are generated when price interacts with the bands:

Signal 1: Triggered when the price touches Band 1, indicating a minor pullback within the trend.

Signal 2: Triggered at Band 2, showing a stronger price deviation and trend confirmation.

Signal 3: Triggered at Band 3, representing the most significant price deviation and strongest trend signal.

The further the price deviates from the mean, the stronger the trend signal, with Signal 3 being the most robust.

Color-Coded Bands:

Bands dynamically change color based on the trend direction:

Green bands signify an uptrend.

Brown bands signify a downtrend.

Dynamic Trend Line Changes:

Dashed lines highlight trend changes, helping traders visualize key turning points in the market.

🔵 Usage:

Use the bands to identify trend direction and strength.

Monitor the signal system to assess the level of price deviation and potential pullback strength.

Combine Signal 1, 2, and 3 to confirm trend momentum:

Signal 1 suggests a weaker pullback and continuation.

Signal 2 indicates a stronger trend confirmation.

Signal 3 highlights the strongest momentum and potential exhaustion points.

Utilize the color-coded bands for an intuitive understanding of current market conditions.

The Triple Trend Indicator is an ideal tool for trend traders looking for structured signals and dynamic support and resistance levels to optimize entries and exits.

VWAP Bands with ML [CryptoSea]VWAP Machine Learning Bands is an advanced indicator designed to enhance trading analysis by integrating VWAP with a machine learning-inspired adaptive smoothing approach. This tool helps traders identify trend-based support and resistance zones, predict potential price movements, and generate dynamic trade signals.

Key Features

Adaptive ML VWAP Calculation: Uses a dynamically adjusted SMA-based VWAP model with volatility sensitivity for improved trend analysis.

Forecasting Mechanism: The 'Forecast' parameter shifts the ML output forward, providing predictive insights into potential price movements.

Volatility-Based Band Adjustments: The 'Sigma' parameter fine-tunes the impact of volatility on ML smoothing, adapting to market conditions.

Multi-Tier Standard Deviation Bands: Includes two levels of bands to define potential breakout or mean-reversion zones.

Dynamic Trend-Based Colouring: The VWAP and ML lines change colour based on their relative positions, visually indicating bullish and bearish conditions.

Custom Signal Detection Modes: Allows traders to choose between signals from Band 1, Band 2, or both, for more tailored trade setups.

In the image below, you can see an example of the bands on higher timeframe showing good mean reversion signal opportunities, these tend to work better in ranging markets rather than strong trending ones.

How It Works

VWAP & ML Integration: The script computes VWAP and applies a machine learning-inspired adjustment using SMA smoothing and volatility-based adaptation.

Forecasting Impact: The 'Forecast' setting shifts the ML output forward in time, allowing for anticipatory trend analysis.

Volatility Scaling (Sigma): Adjusts the ML smoothing sensitivity based on market volatility, providing more responsive or stable trend lines.

Trend Confirmation via Colouring: The VWAP line dynamically switches colour depending on whether it is above or below the ML output.

Multi-Level Band Analysis: Two standard deviation-based bands provide a framework for identifying breakouts, trend reversals, or continuation patterns.

In the example below, we can see some of the most reliable signals where we have mean reversion signals from the band whilst the price is also pulling back into the VWAP, these signals have the additional confluence which can give you a higher probabilty move.

Alerts

Bullish Signal Band 1: Alerts when the price crosses above the lower ML Band 1.

Bearish Signal Band 1: Alerts when the price crosses below the upper ML Band 1.

Bullish Signal Band 2: Alerts when the price crosses above the lower ML Band 2.

Bearish Signal Band 2: Alerts when the price crosses below the upper ML Band 2.

Filtered Bullish Signal: Alerts when a bullish signal is triggered based on the selected signal detection mode.

Filtered Bearish Signal: Alerts when a bearish signal is triggered based on the selected signal detection mode.

Application

Trend & Momentum Analysis: Helps traders identify key market trends and potential momentum shifts.

Dynamic Support & Resistance: Standard deviation bands serve as adaptive price zones for potential breakouts or reversals.

Enhanced Trade Signal Confirmation: The integration of ML smoothing with VWAP provides clearer entry and exit signals.

Customizable Risk Management: Allows users to adjust parameters for fine-tuned signal detection, aligning with their trading strategy.

The VWAP Machine Learning Bands indicator offers traders an innovative tool to improve market entries, recognize potential reversals, and enhance trend analysis with intelligent data-driven signals.

Two-Pole Oscillator [BigBeluga]

The Two-Pole Oscillator is an advanced smoothing oscillator designed to provide traders with precise market signals by leveraging deviation-based calculations combined with a unique two-pole filtering technique. It offers clear visual representation and actionable signals for smart trading decisions.

🔵Key Features:

Two-Pole Filtering: Smooths out the main oscillator signal to reduce noise, providing a cleaner and more reliable view of market momentum and trend strength.

// Two-pole smooth filter function

f_two_pole_filter(source, length) =>

var float smooth1 = na

var float smooth2 = na

alpha = 2.0 / (length + 1)

if na(smooth1)

smooth1 := source

else

smooth1 := (1 - alpha) * smooth1 + alpha * source

if na(smooth2)

smooth2 := smooth1

else

smooth2 := (1 - alpha) * smooth2 + alpha * smooth1

Deviation-Based Oscillator: Utilizes price deviations from the mean to generate dynamic signals, making it ideal for detecting overbought and oversold conditions.

float sma1 = ta.sma(close, 25)

float sma_n1 = ((close - sma1) - ta.sma(close - sma1, 25)) / ta.stdev(close - sma1, 25)

Signal Gradient Strength: Signals on the main oscillator line feature gradient coloring based on their proximity to the 0 level:

➔ Closer to 0: More transparent, indicating weaker signals.

➔ Closer to 1 or -1: Less transparent, highlighting stronger signals.

Level-Based Signal Validation: Parallel levels are plotted on the chart for each signal:

➔ If a level is crossed by price, the signal is invalidated, marked by an "X" at the invalidation point.

Trend Continuation

Invalidation Levels: Serve as potential stop-loss or trade-reversal zones, enabling traders to make more informed and disciplined trading decisions.

Dynamic Chart Plotting: Signals are plotted directly on the chart with corresponding levels, providing a comprehensive visual representation for easy interpretation.

🔵How It Works: