Autocorrelation OscillatorReleasing the autocorrelation oscillator.

NOTE! Please be sure to read the description. This is a theoretical indicator and its important to understand the theory behind its use.

About the indicator:

Before getting into the indicator and its functionality, its important to discuss the theoretical underpinnings of the indicator.

The autocorrelation oscillator operates on two theories of market behaviour that go hand in hand. Those theories are the market efficiency theory and the random walk theory (or hypothesis ).

Market efficiency theory: The market efficiency theory or "Efficient Market Hypothesis (EMH)" postulates that all available information is reflected in a ticker's price almost instantaneously and thus it is impossible for an investor or trader to get ahead of the market because we cannot respond to the speed that the market responds. Of course, there are many holes in this theory, the most notable being that the market is a function of humans. Absent humans and their technological integrations into the market, the market would cease to react at all. But that's besides the point. This is a widely accepted theory and one in which I can mathematically observe through statistical tests. The truth behind this theory is the market is efficient for responding to evolving economic and financial information, likely owning to huge amounts of computer and algorithmic integration into trading, and thus the market is more efficient than the average person is capable (absent computerized algorithms and integration) of ascertaining nuanced financial and economic circumstances. By the time we the people can appraise information, the market has already acted on it. And that is the main premise of the EMH.

The next theory is the Random Walk Theory or Hypothesis (RWH). This builds on the EMH and essentially postulates that the market reacts so quickly to price in current circumstances that it is too random for people to truly exploit and benefit from.

The result of these two theories is two-fold and can be summarized as such:

a) The market behaves in a chaotic fashion that is seemingly random and is incapable of being predicted effectively; and

b) The market is more efficient than a person in incorporating key fundamental information, contributing to the high degree of seemingly random behaviour.

So, how does this help us?

It is said, because of the EMH and the RWH, the only way to truly exploit the market for profit is by:

a) Buying and holding and investing under the bias that stocks will eventually rise in value; or

b) For short term trading, exploiting the pricing anomalies within the data.

So how do we exploit pricing anomalies within the data?

Well, in my own research on market efficiency and behaviour, I have identified many ways of figuring out some anomalies. One of the most effective ways is by looking at simple correlation of lagged values, or autocorrelation for short.

What is autocorrelation and how to use it in relation to EMH and RWH?

Autocorrelation refers to the correlative relationship among the values in a series. Put simply, its the relationship of the same variable over time. For example, if we wanted to look at the auto-correlation of a ticker's high price, we would take, say, 5 to 7 previous high prices and correlate them with the current high price in a series dataset. If the EMH and RWH are true, the correlation among all the variables should have an average less than 0.5 or greater than -0.5. This would indicate true randomness in the dataset and thus an efficient market.

However, if the average of all of the sum's of these correlations are greater than or equal to 0.5 or less than or equal to -0.5, that indicates there is a high degree of autocorrelation and thus the EMH ad RWH is being invalidated as the market is not operating efficiently. This is an anomaly and this anomaly can be exploited.

So how do we exploit it?

Well, when the EMH and RWH hypothesis is being invalidated, we can expect what I coin as a "Regression to Chaos" i.e. the market will revert back to an efficient equilibrium state. So if we have a high correlation of the lagged variables and a strong uptrend or downtrend correlation, we can expect an inefficient market to correct back to an efficient market (i.e. have a reversal from the current trend).

So how does the indicator work?

The indicator measures the lagged correlation of the previous 5 highs and lows of a ticker. A high correlation among all of the highs and lows that exceeds 0.8 would be an invalidation of the EMH and RWH and thus signal a correction to come (i.e. a Regression to Chaos).

The indicator will display this by changing colour. Red for a bearish reversal and green for a bullish. Let's take a look below using the ticker MSFT:

Above we can see the indicator identifying observed inefficiencies within the MSFT ticker on the 1 minute timeframe. The green vertical lines correspond to potential bullish reversals as a result of bearish inefficiencies, the red correspond to bearish reversals as a result of bullish inefficiencies.

You can see these lead to reversals within the ticker.

Components of the indicator:

In the chart above we see the following that are being indicated by arrows:

Red Arrows: Show the identified inefficiencies. Red for bullish inefficiencies (i.e. bearish reversal), green for bearish inefficiencies (i.e. bullish reversal)

Yellow Arrow: The lagged variable chart. This will display the current correlation among all the lagged variables the indicator is assessing.

Teal arrow: Displays the current strength of the trend by correlating the trend to time. A strong negative value (i.e. a value less than or equal to -0.5) indicates a strong downtrend, a strong positive value indicates the inverse.

You can unselect the data-tables in the settings menu if you just want to view the correlation line itself. This part of the indicator is customizable. You can also define the lookback period; however, it is strongly recommended to leave it at 14 as this maintains the use of this indicator as an oscillator.

And that is the indicator! Let me know your comments, questions and feedback below.

Safe trades everyone!

In den Scripts nach "通达信+选股公式+换手率+0.5+源码" suchen

Ticker Correlation Reference IndicatorHello,

I am super excited to be releasing this Ticker Correlation assessment indicator. This is a big one so let us get right into it!

Inspiration:

The inspiration for this indicator came from a similar indicator by Balipour called the Correlation with P-Value and Confidence Interval. It’s a great indicator, you should check it out!

I used it quite a lot when looking for correlations; however, there were some limitations to this indicator’s functionality that I wanted. So I decided to make my own indicator that had the functionality I wanted. I have been using this for some time but decided to actual spruce it up a bit and make it user friendly so that I could share it publically. So let me get into what this indicator does and, most importantly, the expanded functionality of this indicator.

What it does:

This indicator determines the correlation between 2 separate tickers. The user selects the two tickers they wish to compare and it performs a correlation assessment over a defaulted 14 period length and displays the results. However, the indicator takes this much further. The complete functionality of this indicator includes the following:

1. Assesses the correlation of all 4 ticker variables (Open, High, Low and Close) over a user defined period of time (defaulted to 14);

2. Converts both tickers to a Z-Score in order to standardize the data and provide a side by side comparison;

3. Displays areas of high and low correlation between all 4 variables;

4. Looks back over the consistency of the relationship (is correlation consistent among the two tickers or infrequent?);

5. Displays the variance in the correlation (there may be a statistically significant relationship, but if there is a high variance, it means the relationship is unstable);

6. Permits manual conversion between prices; and

7. Determines the degree of statistical significance (be it stable, unstable or non-existent).

I will discuss each of these functions below.

Function 1: Assesses the correlation of all 4 variables.

The only other indicator that does this only determines the correlation of the close price. However, correlation between all 4 variables varies. The correlation between open prices, high prices, low prices and close prices varies in statistically significant ways. As such, this indicator plots the correlation of all 4 ticker variables and displays each correlation.

Assessing this matters because sometimes a stock may not have the same magnitude in highs and lows as another stock (one stock may be more bullish, i.e. attain higher highs in comparison to another stock). Close price is helpful but does not pain the full picture. As such, the indicator displays the correlation relationship between all 4 variables (image below):

Function 2: Converts both tickers to Z-Score

Z-Score is a way of standardizing data. It simply measures how far a stock is trading in relation to its mean. As such, it is a way to express both tickers on a level playing field. Z-Score was also chosen because the Z-Score Values (0 – 4) also provide an appropriate scale to plot correlation lines (which range from 0 to 1).

The primary ticker (Ticker 1) is plotted in blue, the secondary comparison ticker (Ticker 2) is plotted in a colour changing format (which will be discussed below). See the image below:

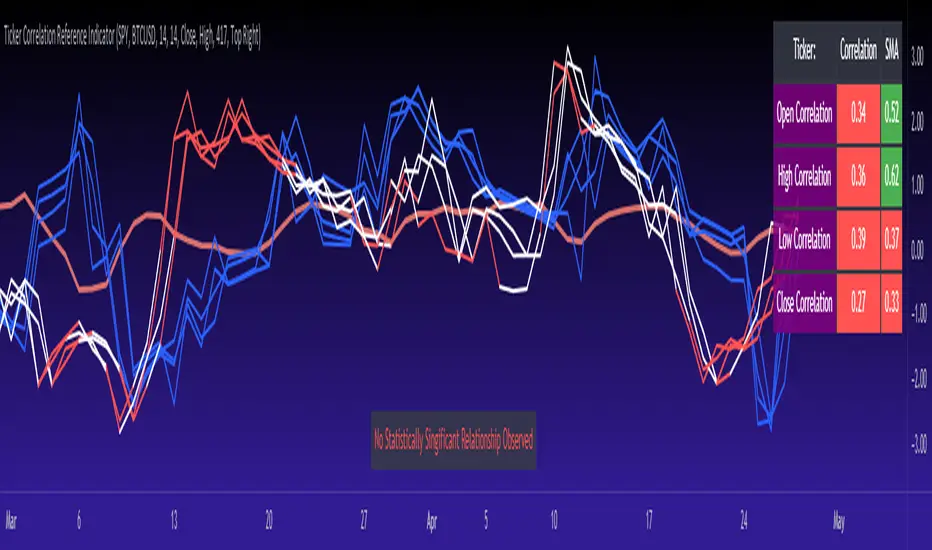

Function 3: Displays areas of high and low correlation

While Ticker 1 is plotted in a static blue, Ticker 2 (the comparison ticker) is plotted in a dynamic, colour changing format. It will display areas of high correlation (i.e. areas with a P value greater than or equal to 0.9 or less than and equal to -0.9) in green, areas of moderate correlation in white. Areas of low correlation (between 0.4 and 0 or -0.4 and 0) are in red. (see image below):

Function 4: Checks consistency of relationship

While at the time of assessing a stock there very well maybe a high correlation, whether that correlation is consistent or not is the question. The indicator employs the use of the SMA function to plot the average correlation over a defined period of time. If the correlation is consistently high, the SMA should be within an area of statistical significance (over 0.5 or under -0.5). If the relationship is inconsistent, the SMA will read a lower value than the actual correlation.

You can see an example of this when you compare ETH to Tezos in the image below:

You can see that the correlation between ETH and Tezo’s on the high level seems to be inconsistent. While the current correlation is significant, the SMA is showing that the average correlation between the highs is actually less than 0.5.

The indicator also tells the user narratively the degree of consistency in the statistical relationship. This will be discussed later.

Function 5: Displays the variance

When it comes to correlation, variance is important. Variance simply means the distance between the highest and lowest value. The indicator assess the variance. A high degree of variance (i.e. a number surpassing 0.5 or greater) generally means the consistency and stability of the relationship is in issue. If there is a high variance, it means that the two tickers, while seemingly significantly correlated, tend to deviate from each other quite extensively.

The indicator will tell the user the variance in the narrative bar at the bottom of the chart (see image below):

Function 6: Permits manual conversion of price

One thing that I frequently want and like to do is convert prices between tickers. If I am looking at SPX and I want to calculate a price on SPY, I want to be able to do that quickly. This indicator permits you to do that by employing a regression based formula to convert Ticker 1 to Ticker 2.

The user can actually input which variable they would like to convert, whether they want to convert Ticker 1 Close to Ticker 2 Close, or Ticker 1 High to Ticker 2 High, or low or open.

To do this, open the settings and click “Permit Manual Conversion”. This will then take the current Ticker 1 Close price and convert it to Ticker 2 based on the regression calculations.

If you want to know what a specific price on Ticker 1 is on Ticker 2, simply click the “Allow Manual Price Input” variable and type in the price of Ticker 1 you want to know on Ticker 2. It will perform the calculation for you and will also list the standard error of the calculation.

Below is an example of calculating a SPY price using SPX data:

Above, the indicator was asked to convert an SPX price of 4,100 to a SPY price. The result was 408.83 with a standard error of 4.31, meaning we can expect 4,100 to fall within 408.83 +/- 4.31 on SPY.

Function 7: Determines the degree of statistical significance

The indicator will provide the user with a narrative output of the degree of statistical significance. The indicator looks beyond simply what the correlation is at the time of the assessment. It uses the SMA and the highest and lowest function to make an assessment of the stability of the statistical relationship and then indicates this to the user. Below is an example of IWM compared to SPY:

You will see, the indicator indicates that, while there is a statistically significant positive relationship, the relationship is somewhat unstable and inconsistent. Not only does it tell you this, but it indicates the degree of inconsistencies by listing the variance and the range of the inconsistencies.

And below is SPY to DIA:

SPY to BTCUSD:

And finally SPY to USDCAD Currency:

Other functions:

The indicator will also plot the raw or smoothed correlation result for the Open, High, Low or Close price. The default is to close price and smoothed. Smoothed just means it is displaying the SMA over the raw correlation score. Unsmoothing it will show you the raw correlation score.

The user also has the ability to toggle on and off the correlation table and the narrative table so that they can just review the chart (the side by side comparison of the 2 tickers).

Customizability

All of the functions are customizable for the most part. The user can determine the length of lookback, etc. The default parameters for all are 14. The only thing not customizable is the assessment used for determining the stability of a statistical relationship (set at 100 candle lookback) and the regression analysis used to convert price (10 candle lookback).

User Notes and important application tips:

#1: If using the manual calculation function to convert price, it is recommended to use this on the hourly or daily chart.

#2: Leaving pre-market data on can cause some errors. It is recommended to use the indicator with regular market hours enabled and extended market hours disabled.

#3: No ticker is off limits. You can compare anything against anything! Have fun with it and experiment!

Non-Indicator Specific Discussions:

Why does correlation between stocks mater?

This can matter for a number of reasons. For investors, it is good to diversify your portfolio and have a good array of stocks that operate somewhat independently of each other. This will allow you to see how your investments compare to each other and the degree of the relationship.

Another function may be getting exposure to more expensive tickers. I am guilty of trading IWM to gain exposure to SPY at a reduced cost basis :-).

What is a statistically significant correlation?

The rule of thumb is anything 0.5 or greater is considered statistically significant. The ideal setup is 0.9 or more as the effect is almost identical. That said, a lot of factors play into statistical significance. For example, the consistency and variance are 2 important factors most do not consider when ascertaining significance. Perhaps IWM and SPY are significantly correlated today, but is that a reliable relationship and can that be counted on as a rule?

These are things that should be considered when trading one ticker against another and these are things that I have attempted to address with this indicator!

Final notes:

I know I usually do tutorial videos. I have not done one here, but I will. Check back later for this.

I hope you enjoy the indicator and please feel free to share your thoughts and suggestions!

Safe trades all!

Market Structure - By LeviathanThis indicator helps you identify market structure by plotting swing highs and lows (HH, LH, HL, LL), BOS/CHOCH and 0.5 retracement levels. Other functionalities will be added in future updates.

Indicator Settings Overview

SWING LENGTH

The number of leftbars and rightbars when searching for swing points. The lower the value, the more swing points are shown and the higher the value, the less swing points are shown. I suggest adjusting it to fit your style and when switching between different timeframes.

BOS CONFIRMATION

Choose whether a Break of Structure is determined by a candle close or a wick breaching previous swing point. Using the "Wick" confirmation option will result in more breaks of structure.

CHOCH

Turning this ON renames the first counter trend Break of Structure (BOS) to CHoCH (Change of Character) and therefore signaling a possible trend shift.

SHOW 0.5 RETRACEMENT LEVEL

This will show a level halfway between a swing low and a swing high of an expansion move, which can act as an approximate retracement point if the trend continues.

In uptrends, 0.5 level is drawn between Higher Lows (HL) and Higher Highs ( HHs ). Long entries can be placed around that level if you suspect that the uptrend will continue.

In downtrends, 0.5 level is drawn between Lower Highs (LH) and Lower Lows (LLs). Short entries can be placed around that level if you suspect that the downtrend will continue.

Writer Extendible Option [Loxx]These options can be exercised at their initial maturity date /I but are extended to T2 if the option is out-of-the-money at ti. The payoff from a writer-extendible call option at time T1 (T1 < T2) is (via "The Complete Guide to Option Pricing Formulas")

c(S, X1, X2, t1, T2) = (S - X1) if S>= X1 else cBSM(S, X2, T2-T1)

and for a writer-extendible put is

c(S, X1, X2, T1, T2) = (X1 - S) if S< X1 else pBSM(S, X2, T2-T1)

Writer-Extendible Call

c = cBSM(S, X1, T1) + Se^(b-r)T2 * M(Z1, -Z2; -p) - X2e^-rT2 * M(Z1 - vT^0.5, -Z2 + vT^0.5; -p)

Writer-Extendible Put

p = cBSM(S, X1, T1) + X2e^-rT2 * M(-Z1 + vT^0.5, Z2 - vT^0.5; -p) - Se^(b-r)T2 * M(-Z1, Z2; -p)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

Asset price ( S )

Initial strike price ( X1 )

Extended strike price ( X2 )

Initial time to maturity ( t1 )

Extended time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Output

Delta

Elasticity

Gamma

DGammaDvol

GammaP

Vega

DvegaDvol

VegaP

Theta (1 day)

Rho

Rho futures option

Phi/Rho2

Carry

DDeltaDvol

Speed

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

American Approximation Bjerksund & Stensland 1993 [Loxx]American Approximation Bjerksund & Stensland 1993 is an American Options pricing model. This indicator also includes numerical greeks. You can compare the output of the American Approximation to the Black-Scholes-Merton value on the output of the options panel.

The Bjerksund and Stensland (1993) approximation can be used to price American options on stocks, futures, and currencies. The method is analytical and extremely computer-efficient. Bjerksund and Stensland's approximation is based on an exercise strategy corresponding to a flat boundary / (trigger price). Numerical investigation indicates that the Bjerksund and Stensland model is somewhat more accurate for long-term options than the Barone-Adesi and Whaley model. (The Complete Guide to Option Pricing Formulas)

C = alpha * X^beta - alpha Ø(S, T, beta, I, I) + Ø(S, T, I, I, I) - Ø(S, T, I, X, I) - XØ(S, T, 0, I, I) + XØ(S, T, 0, X, I)

where

alpha = (1 - X) * I^-beta

beta = (1/2 - b/v^2) + ((b/v^2 - 1/2)^2 + 2*(r/v^2))^0.5

The function Ø(S, T, y, H, I) is given by

Ø(S, T, gamma, H, I) = e^lambda * S^gamma * (N(d) - (I/S)^k * N(d - (2 * log(I/S)) / v*T^0.5))

lambda = (-r + gamma * b + 1/2 * gamma(gamma - 1) * v^2) * T

d = (log(S/H) + (b + (gamma - 1/2) * v^2) * T) / (v * T^0.5)

k = 2*b/v^2 + (2 * gamma - 1)

and the trigger price I is defined as

I = B0 + (B(+infi) - B0) * (1 - e^h(T))

h(T) = -(b*T + 2*v*T^0.5) * (B0 / (B(+infi) - B0))

B(+infi) = (B / (B - 1)) * X

B0 = max(X, (r / (r - b)) * X)

If s > I, it is optimal to exercise the option immediately, and the value must be equal to the intrinsic value of S - X. On the other hand, if b > r, it will never be optimal to exercise the American call option before expiration, and the value can be found using the generalized BSM formula. The value of the American put is given by the Bjerksund and Stensland put-call transformation

P(S, X, T, r, b, v) = C(X, S, T, r -b, -b, v)

where C(*) is the value of the American call with risk-free rate r - b and drift -b. With the use of this transformation, it is not necessary to develop a separate formula for an American put option.

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

cbnd3(x) = Cumulative Bivariate Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

DOW 30 - Market BreadthDOW 30 indicator is intended for short-term intraday analysis and should not be used solely alone. Best to use this indicator in a combination with technical and fundamental analysis.

This indicator is calculated from all stocks in the DJI as of 8/9/2022;

- Evaluating VWAP,

- 9 EMA,

- 20 EMA.

Vwap Calculations;

Stock above Vwap = 1 (Vwap Bull),

Stock below Vwap = 1 (Vwap Bear),

As there are 30 stocks in the DJI, there is a max value of 30 Vwap Bulls/ Vwap Bears.

Ema Calculation;

Stock above 9 EMA = 0.5 (EMA Bulls),

Stock below 9 EMA = 0.5 (EMA Bears),

Stock above 20 EMA = 0.5 (EMA Bulls),

Stock below 20 EMA = 0.5 (EMA Bears),

For the EMA Bulls to reach 30 all stocks must be trading above both the 9 EMA and 20 EMA to reach a Max Value of 30.

The reasoning for this calculation is to suggest the current strength and speed of the current turn in the market.

Horizontal Lines:

There are three horizontal lines, MAX, MIN & Neutral;

MAX & MIN

Resides at the 30 & 0 levels suggesting the market is currently at an extreme. Representing all stocks are moving in the same direction together.

When the MAX or MIN are represented in the VWAP Line this represents directional conviction in the underlining DJI.

Neutral

Neutral resides at the 15 level and represents that the market is either about to make a decision or is choppy.

EXAMPLE

Below are some examples of how the DOW 30 indicator is able to represent the current market conditions.

Understand Current Market Conditions, either being Bullish, Neutral, or Bearish.

See live Market Mechanics, and understand the current market direction on a short-term timeframe.

DOW 30 indicator is intended for short-term intraday analysis and should not be used solely alone. Best to use this indicator in a combination with technical and fundamental analysis.

If there are any additional requests to the indicator feel free to leave a comment or privet message.

Best of luck trading.

BTC Risk Metric - Estimates the risk of BTC price versus the USD

- To be used on the daily timeframe

- Works best on a BTC pair that has a lot of bars, e.g. The Bitcoin All Time History Index

- 0 is the lowest risk, 1 is the highest risk

- Historically, buying when the risk was low and selling when the risk was high would have yielded good ROI

- The risk bands are 0.1 in width and are highlighted on the plot

Typical Strategy:

- weighted DCA into the market when risk <0.5, do nothing between 0.5-0.6 and weighted DCA out of the market when risk >0.6

- x = buy amount per DCA interval

- y = 1/10th total BTC held by the user

- if 0 ≤ Risk < 0.1 then buy 5x

- if 0.1 ≤ Risk < 0.2 then buy 4x

- if 0.2 ≤ Risk < 0.3 then buy 3x

- if 0.3 ≤ Risk < 0.4 then buy 2x

- if 0.4 ≤ Risk < 0.5 then buy x

- if 0.5 ≤ Risk < 0.6 then do nothing

- if 0.6 ≤ Risk < 0.7 then sell y

- if 0.7 ≤ Risk < 0.8 then sell 2y

- if 0.8 ≤ Risk < 0.9 then sell 3y

- if 0.9 ≤ Risk ≤ 1.0 then sell 4y

Technical Ratings on Multi-frames / Assets█ OVERVIEW

This indicator is a modified version of TECHNICAL RATING v1.0 available in the public library to provide a quick overview of consolidated technical ratings performed on 12 assets in 3 timeframes.The purpose of the indicator is to provide a quick overview of the current status of the custom 12 (24) assets and to help focus on the appropriate asset.

█ MODIFICATIONS

- Markers, visualizations and alerts have been deleted

- Due to the limitation on maximum number of security (40), the results of 12 assets evaluated in 3 different time frames can be shown at the same time.

- An additional 12 assets can be configured in the settings so that you do not have to choose each ticker one by one to facilitate a quick change, but can switch between the 12 -12 assets with a single click on "Second sets?".

- The position, colors and parameters of the table can be widely customized in the settings.

- The 12 assets can be arranged in rows 3, 4, 6 and 12 with Table Rows options, which can also be used to create a simple mobile view.

- The default gradient color setting has been changed to red/yellow/green traffic lights

ORIGINAL DESCRIPTION ABOUT TECHNICAL RATING v1.0

█ OVERVIEW

This indicator calculates TradingView's well-known "Strong Buy", "Buy", "Neutral", "Sell" or "Strong Sell" states using the aggregate biases of 26 different technical indicators.

█ WARNING

This version is similar, but not identical, to our recently published "Technical Ratings" built-in, which reproduces our "Technicals" ratings displayed as a gauge in the right panel of charts, or in the "Rating" indicator available in the TradingView Screener. This is a fork and refactoring of the code base used in the "Technical Ratings" built-in. Its calculations will not always match those of the built-in, but it provides options not available in the built-in. Up to you to decide which one you prefer to use.

█ FEATURES

Differences with the built-in version

• The built-in version produces values matching the states displayed in the "Technicals" ratings gauge; this one does not always.

• A strategy version is also available as a built-in; this script is an indicator—not a strategy.

• This indicator will show a slightly different vertical scale, as it does not use a fixed scale like the built-in.

• This version allows control over repainting of the signal when you do not use a higher timeframe. Higher timeframe (HTF) information from this version does not repaint.

• You can adjust the weight of the Oscillators and MAs components of the rating here.

• You can configure markers on signal breaches of configurable levels, or on advances declines of the signal.

The indicator's settings allow you to:

• Choose the timeframe you want calculations to be made on.

• When not using a HTF, you can select a repainting or non-repainting signal.

• When using both MAs and Oscillators groups to calculate the rating, you can vary the weight of each group in the calculation. The default is 50/50.

Because the MAs group uses longer periods for some of its components, its value is not as jumpy as the Oscillators value.

Increasing the weight of the MAs group will thus have a calming effect on the signal.

• Alerts can be created on the indicator using the conditions configured to control the display of markers.

Display

The calculated rating is displayed as columns, but you can change the style in the inputs. The color of the signal can be one of three colors: bull, bear, or neutral. You can choose from a few presets, or check one and edit its color. The color is determined from the rating's value. Between 0.1 and -0.1 it is in the neutral color. Above/below 0.1/-0.1 it will appear in the bull/bear color. The intensity of the bull/bear color is determined by cumulative advances/declines in the rating. It is capped to 5, so there are five intensities for each of the bull/bear colors.

The "Strong Buy", "Buy", "Neutral", "Sell" or "Strong Sell" state of the last calculated value is displayed to the right of the last bar for each of the three groups: All, MAs and Oscillators. The first value always reflects your selection in the "Rating uses" field and is the one used to display the signal. A "Strong Buy" or "Strong Sell" state appears when the signal is above/below the 0.5/-0.5 level. A "Buy" or "Sell" state appears when the signal is above/below the 0.1/-0.1 level. The "Neutral" state appears when the signal is between 0.1 and -0.1 inclusively.

Five levels are always displayed: 0.5 and 0.1 in the bull color, zero in the neutral color, and -0.1 and - 0.5 in the bull color.

█ CALCULATIONS

The indicator calculates the aggregate value of two groups of indicators: moving averages and oscillators.

The "MAs" group is comprised of 15 different components:

• Six Simple Moving Averages of periods 10, 20, 30, 50, 100 and 200

• Six Exponential Moving Averages of the same periods

• A Hull Moving Average of period 9

• A Volume-weighed Moving Average of period 20

• Ichimoku

The "Oscillators" group includes 11 components:

• RSI

• Stochastic

• CCI

• ADX

• Awesome Oscillator

• Momentum

• MACD

• Stochastic RSI

• Wiliams %R

• Bull Bear Power

• Ultimate Oscillator

[GJ]IFRSITHE INVERSE FISHER TRANSFORM STOCH RSI

HOW IT WORKS

This indicator uses the inverse fisher transform on the stoch RSI for clear buying and selling signals. The stoch rsi is used to limit it in the range of 0 and 100. We subtract 50 from this to get it into the range of -50 to +50 and multiply by .1 to get it in the range of -5 to +5. We then use the 9 period weighted MA to remove some "random" trade signals before we finally use the inverse fisher transform to get the output between -1 and +1

HOW TO USE

Buy when the indicator crosses over –0.5 or crosses over +0.5 if it has not previously crossed over –0.5.

Sell when the indicator crosses under +0.5 or crosses under –0.5 if it has not previously crossed under +0.5.

We can see multiple examples of good buy and sell signals from this indicator on the attached chart for QCOM. Let me know if you have any suggestions or thoughts!

Technical Ratings█ OVERVIEW

This indicator calculates TradingView's well-known "Strong Buy", "Buy", "Neutral", "Sell" or "Strong Sell" states using the aggregate biases of 26 different technical indicators.

█ FEATURES

Differences with the built-in version

• You can adjust the weight of the Oscillators and MAs components of the rating here.

• The built-in version produces values matching the states displayed in the "Technicals" ratings gauge; this one does not always, where weighting is used.

• A strategy version is also available as a built-in; this script is an indicator—not a strategy.

• This indicator will show a slightly different vertical scale, as it does not use a fixed scale like the built-in.

• This version allows control over repainting of the signal when you do not use a higher timeframe. Higher timeframe (HTF) information from this version does not repaint.

• You can configure markers on signal breaches of configurable levels, or on advances declines of the signal.

The indicator's settings allow you to:

• Choose the timeframe you want calculations to be made on.

• When not using a HTF, you can select a repainting or non-repainting signal.

• When using both MAs and Oscillators groups to calculate the rating, you can vary the weight of each group in the calculation. The default is 50/50.

Because the MAs group uses longer periods for some of its components, its value is not as jumpy as the Oscillators value.

Increasing the weight of the MAs group will thus have a calming effect on the signal.

• Alerts can be created on the indicator using the conditions configured to control the display of markers.

Display

The calculated rating is displayed as columns, but you can change the style in the inputs. The color of the signal can be one of three colors: bull, bear, or neutral. You can choose from a few presets, or check one and edit its color. The color is determined from the rating's value. Between 0.1 and -0.1 it is in the neutral color. Above/below 0.1/-0.1 it will appear in the bull/bear color. The intensity of the bull/bear color is determined by cumulative advances/declines in the rating. It is capped to 5, so there are five intensities for each of the bull/bear colors.

The "Strong Buy", "Buy", "Neutral", "Sell" or "Strong Sell" state of the last calculated value is displayed to the right of the last bar for each of the three groups: All, MAs and Oscillators. The first value always reflects your selection in the "Rating uses" field and is the one used to display the signal. A "Strong Buy" or "Strong Sell" state appears when the signal is above/below the 0.5/-0.5 level. A "Buy" or "Sell" state appears when the signal is above/below the 0.1/-0.1 level. The "Neutral" state appears when the signal is between 0.1 and -0.1 inclusively.

Five levels are always displayed: 0.5 and 0.1 in the bull color, zero in the neutral color, and -0.1 and - 0.5 in the bull color.

The levels that can be used to determine the breaches displaying long/short markers will only be visible when their respective long/short markers are turned on in the "Direction" input. The levels appear as a bright dotted line in bull/bear colors. You can control both levels separately through the "Longs Level" and "Shorts Level" inputs.

If you specify a higher timeframe that is not greater than the chart's timeframe, an error message will appear and the indicator's background will turn red, as it doesn't make sense to use a lower timeframe than the chart's.

Markers

Markers are small triangles that appear at the bottom and top of the indicator's pane. The marker settings define the conditions that will trigger an alert when you configure an alert on the indicator. You can:

• Choose if you want long, short or both long and short markers.

• Determine the signal level and/or the number of cumulative advances/declines in the signal which must be reached for either a long or short marker to appear.

Reminder: the number of advances/declines is also what controls the brightness of the plotted signal.

• Decide if you want to restrict markers to ones that alternate between longs and shorts, if you are displaying both directions.

This helps to minimize the number of markers, e.g., only the first long marker will be displayed, and then no more long markers will appear until a short comes in, then a long, etc.

Alerts

When you create an alert from this indicator, that alert will trigger whenever your marker conditions are confirmed. Before creating your alert, configure the makers so they reflect the conditions you want your alert to trigger on.

The script uses the alert() function, which entails that you select the "Any alert() function call" condition from the "Create Alert" dialog box when creating alerts on the script. The alert messages can be configured in the inputs. You can safely disregard the warning popup that appears when you create alerts from this script. Alerts will not repaint. Markers will appear, and thus alerts will trigger, at the opening of the bar following the confirmation of the marker condition. Markers will never disappear from the bar once they appear.

Repainting

This indicator uses a two-pronged approach to control repainting. The repainting of the displayed signal is controlled through the "Repainting" field in the script's inputs. This only applies when you have "Same as chart" selected in the "Timeframe" field, as higher timeframe data never repaints. Regardless of that setting, markers and thus alerts never repaint.

When using the chart's timeframe, choosing a non-repainting signal makes the signal one bar late, so that it only displays a value once the bar it was calculated has elapsed. When using a higher timeframe, new values are only displayed once the higher timeframe completes.

Because the markers never repaint, their logic adapts to the repainting setting used for the signal. When the signal repaints, markers will only appear at the close of a realtime bar. When the signal does not repaint (or if you use a higher timeframe), alerts will appear at the beginning of the realtime bar, since they are calculated on values that already do not repaint.

█ CALCULATIONS

The indicator calculates the aggregate value of two groups of indicators: moving averages and oscillators.

The "MAs" group is comprised of 15 different components:

• Six Simple Moving Averages of periods 10, 20, 30, 50, 100 and 200

• Six Exponential Moving Averages of the same periods

• A Hull Moving Average of period 9

• A Volume-weighed Moving Average of period 20

• Ichimoku

The "Oscillators" group includes 11 components:

• RSI

• Stochastic

• CCI

• ADX

• Awesome Oscillator

• Momentum

• MACD

• Stochastic RSI

• Wiliams %R

• Bull Bear Power

• Ultimate Oscillator

The state of each group's components is evaluated to a +1/0/-1 value corresponding to its bull/neutral/bear bias. The resulting value for each of the two groups are then averaged to produce the overall value for the indicator, which oscillates between +1 and -1. The complete conditions used in the calculations are documented in the Help Center .

█ NOTES

Accuracy

When comparing values to the other versions of the Rating, make sure you are comparing similar timeframes, as the "Technicals" gauge in the chart's right pane, for example, uses a 1D timeframe by default.

For coders

We use a handy characteristic of array.avg() which, contrary to avg() , does not return na when one of the averaged values is na . It will average only the array elements which are not na . This is useful in the context where the functions used to calculate the bull/neutral/bear bias for each component used in the rating include special checks to return na whenever the dataset does not yet contain enough data to provide reliable values. This way, components gradually kick in the calculations as the script calculates on more and more historical data.

We also use the new `group` and `tooltip` parameters to input() , as well as dynamic color generation of different transparencies from the bull/bear/neutral colors selected by the user.

Our script was written using the PineCoders Coding Conventions for Pine .

The description was formatted using the techniques explained in the How We Write and Format Script Descriptions PineCoders publication.

Bits and pieces were lifted from the PineCoders' MTF Selection Framework .

Look first. Then leap.

Inverse Fisher Transform of SMI and sto. RSI, MTF confirmedThe system uses 1 hour and 15 min timeframe data. Signals coming from 15 min Inverse Fisher Transform of SMI and stochastic RSI are confirmed by 1 hour Inverse Fisher Transform SMI, according to the following rules:

long cond.: 15 min IFTSMI crosses ABOVE -0.5 or SRSI k-line crosses ABOVE 50 while 1-hour IFTSMI is already ABOVE -0.5

short cond.:15 min IFTSMI crosses BELOW 0.5 or SRSI k-line crosses BELOW 50 while 1-hour IFTSMI is already BELOW 0.5

SMI and Inverse Fisher Transform of SMI codes belong to @kivancozbilgic.

Tradingview - Screener RatingsEver wondered what is behind the the Tradingview Screener Signals:

www.tradingview.com

Strong buy is between 0.5 and 1

Buy is between 0 and 0.5

Sell is between 0 and -0.5

Strong Sell is between -0.5 and -1

Volatility Switch Indicator [LazyBear]The Volatility Switch (VOLSWITCH) indicator, by Ron McEwan, estimates current volatility in respect to historical data, thus indicating whether the market is trending or in mean reversion mode. Range is normalized to 0 - 1.

When Volatility Switch rises above the 0.5 level, volatility in the market is increasing, thus the price action can be expected to become choppier with abrupt moves. When the indicator falls below the 0.5 level from recent high readings, volatility decreases, which may be considered a sign of trend formation.

Trading strategy as suggested by Ron McEwan is:

- If VOLSWITCH is less than 0.5, volatility decreases, which may be considered a sign of trend formation

- If VOLSWITCH is greater than 0.5, market is in high volatility mode. Can be choppy. Use RSI to look for OB/OS levels.

I have implemented support for 2 lengths (14 and 21) Note that, Pine doesn't support loops. Once it is introduced, I will publish an updated version.

Building a strategy out of this is straightforward (refer to my strategy explanation above), I strongly encourage new Pinescript coders to try to a plotarrow() based overlay indicator to get more familiar with Pine.

More info:

---------

The Volatility (Regime) Switch Indicator : traders.com

Complete list of my indicators:

-------------------------------------

docs.google.com

POC Migration Velocity (POC-MV) [PhenLabs]📊POC Migration Velocity (POC-MV)

Version: PineScript™v6

📌Description

The POC Migration Velocity indicator revolutionizes market structure analysis by tracking the movement, speed, and acceleration of Point of Control (POC) levels in real-time. This tool combines sophisticated volume distribution estimation with velocity calculations to reveal hidden market dynamics that conventional indicators miss.

POC-MV provides traders with unprecedented insight into volume-based price movement patterns, enabling the early identification of continuation and exhaustion signals before they become apparent to the broader market. By measuring how quickly and consistently the POC migrates across price levels, traders gain early warning signals for significant market shifts and can position themselves advantageously.

The indicator employs advanced algorithms to estimate intra-bar volume distribution without requiring lower timeframe data, making it accessible across all chart timeframes while maintaining sophisticated analytical capabilities.

🚀Points of Innovation

Micro-POC calculation using advanced OHLC-based volume distribution estimation

Real-time velocity and acceleration tracking normalized by ATR for cross-market consistency

Persistence scoring system that quantifies directional consistency over multiple periods

Multi-signal detection combining continuation patterns, exhaustion signals, and gap alerts

Dynamic color-coded visualization system with intensity-based feedback

Comprehensive customization options for resolution, periods, and thresholds

🔧Core Components

POC Calculation Engine: Estimates volume distribution within each bar using configurable price bands and sophisticated weighting algorithms

Velocity Measurement System: Tracks the rate of POC movement over customizable lookback periods with ATR normalization

Acceleration Calculator: Measures the rate of change of velocity to identify momentum shifts in POC migration

Persistence Analyzer: Quantifies how consistently POC moves in the same direction using exponential weighting

Signal Detection Framework: Combines trend analysis, velocity thresholds, and persistence requirements for signal generation

Visual Rendering System: Provides dynamic color-coded lines and heat ribbons based on velocity and price-POC relationships

🔥Key Features

Real-time POC calculation with 10-100 configurable price bands for optimal precision

Velocity tracking with customizable lookback periods from 5 to 50 bars

Acceleration measurement for detecting momentum changes in POC movement

Persistence scoring to validate signal strength and filter false signals

Dynamic visual feedback with blue/orange color scheme indicating bullish/bearish conditions

Comprehensive alert system for continuation patterns, exhaustion signals, and POC gaps

Adjustable information table displaying real-time metrics and current signals

Heat ribbon visualization showing price-POC relationship intensity

Multiple threshold settings for customizing signal sensitivity

Export capability for use with separate panel indicators

🎨Visualization

POC Connecting Lines: Color-coded lines showing POC levels with intensity based on velocity magnitude

Heat Ribbon: Dynamic colored ribbon around price showing POC-price basis intensity

Signal Markers: Clear exhaustion top/bottom signals with labeled shapes

Information Table: Real-time display of POC value, velocity, acceleration, basis, persistence, and current signal status

Color Gradients: Blue gradients for bullish conditions, orange gradients for bearish conditions

📖Usage Guidelines

POC Calculation Settings

POC Resolution (Price Bands): Default 20, Range 10-100. Controls the number of price bands used to estimate volume distribution within each bar

Volume Weight Factor: Default 0.7, Range 0.1-1.0. Adjusts the influence of volume in POC calculation

POC Smoothing: Default 3, Range 1-10. EMA smoothing period applied to the calculated POC to reduce noise

Velocity Settings

Velocity Lookback Period: Default 14, Range 5-50. Number of bars used to calculate POC velocity

Acceleration Period: Default 7, Range 3-20. Period for calculating POC acceleration

Velocity Significance Threshold: Default 0.5, Range 0.1-2.0. Minimum normalized velocity for continuation signals

Persistence Settings

Persistence Lookback: Default 5, Range 3-20. Number of bars examined for persistence score calculation

Persistence Threshold: Default 0.7, Range 0.5-1.0. Minimum persistence score required for continuation signals

Visual Settings

Show POC Connecting Lines: Toggle display of colored lines connecting POC levels

Show Heat Ribbon: Toggle display of colored ribbon showing POC-price relationship

Ribbon Transparency: Default 70, Range 0-100. Controls transparency level of heat ribbon

Alert Settings

Enable Continuation Alerts: Toggle alerts for continuation pattern detection

Enable Exhaustion Alerts: Toggle alerts for exhaustion pattern detection

Enable POC Gap Alerts: Toggle alerts for significant POC gaps

Gap Threshold: Default 2.0 ATR, Range 0.5-5.0. Minimum gap size to trigger alerts

✅Best Use Cases

Identifying trend continuation opportunities when POC velocity aligns with price direction

Spotting potential reversal points through exhaustion pattern detection

Confirming breakout validity by monitoring POC gap behavior

Adding volume-based context to traditional technical analysis

Managing position sizing based on POC-price basis strength

⚠️Limitations

POC calculations are estimations based on OHLC data, not true tick-by-tick volume distribution

Effectiveness may vary in low-volume or highly volatile market conditions

Requires complementary analysis tools for complete trading decisions

Signal frequency may be lower in ranging markets compared to trending conditions

Performance optimization needed for very short timeframes below 1-minute

💡What Makes This Unique

Advanced Estimation Algorithm: Sophisticated method for calculating POC without requiring lower timeframe data

Velocity-Based Analysis: Focus on POC movement dynamics rather than static levels

Comprehensive Signal Framework: Integration of continuation, exhaustion, and gap detection in one indicator

Dynamic Visual Feedback: Intensity-based color coding that adapts to market conditions

Persistence Validation: Unique scoring system to filter signals based on directional consistency

🔬How It Works

Volume Distribution Estimation:

Divides each bar into configurable price bands for volume analysis

Applies sophisticated weighting based on OHLC relationships and proximity to close

Identifies the price level with maximum estimated volume as the POC

Velocity and Acceleration Calculation:

Measures POC rate of change over specified lookback periods

Normalizes values using ATR for consistent cross-market performance

Calculates acceleration as the rate of change of velocity

Signal Generation Process:

Combines trend direction analysis using EMA crossovers

Applies velocity and persistence thresholds to filter signals

Generates continuation, exhaustion, and gap alerts based on specific criteria

💡Note:

This indicator provides estimated POC calculations based on available OHLC data and should be used in conjunction with other analysis methods. The velocity-based approach offers unique insights into market structure dynamics but requires proper risk management and complementary analysis for optimal trading decisions.

Imbalance RSI Divergence Strategy# Imbalance RSI Divergence Strategy - User Guide

## What is This Strategy?

This strategy identifies **imbalance** zones in the market and combines them with **RSI divergence** to generate trading signals. It aims to capitalize on price gaps left by institutional investors and large volume movements.

### Main Settings

- **RSI Period (14)**: Period used for RSI calculation. Lower values = more sensitive, higher values = more stable signals.

- **ATR Period (10)**: Period for volatility measurement using Average True Range.

- **ATR Stop Loss Multiplier (2.0)**: How many ATR units to use for stop loss calculation.

- **Risk:Reward Ratio (4.0)**: Risk-reward ratio. 2.0 = 2 units of reward for 1 unit of risk.

- **Use RSI Divergence Filter (true)**: Enables/disables the RSI divergence filter.

### Imbalance Filters

- **Minimum Imbalance Size (ATR) (0.3)**: Minimum imbalance size in ATR units to filter out small imbalances.

- **Enable Lookback Limit (false)**: Activates historical lookback limitations.

- **Maximum Lookback Bars (300)**: Maximum number of bars to look back.

### Visual Settings

- **Show Imbalance Size**: Displays imbalance size in ATR units.

- **Show RSI Divergence Lines**: Shows/hides divergence lines.

- **Divergence Line Colors**: Colors for bullish/bearish divergence lines.

### Volatility-Based Adjustments

- **Low volatility markets**:

- Minimum Imbalance Size: 0.2-0.4 ATR

- ATR Stop Loss Multiplier: 1.5-2.0

- **High volatility markets**:

- Minimum Imbalance Size: 0.5-1.0 ATR

- ATR Stop Loss Multiplier: 2.5-3.5

### Risk Tolerance

- **Conservative approach**:

- Risk:Reward Ratio: 2.0-3.0

- RSI Divergence Filter: Enabled

- Minimum Imbalance Size: Higher (0.5+ ATR)

- **Aggressive approach**:

- Risk:Reward Ratio: 4.0-6.0

- Minimum Imbalance Size: Lower (0.2-0.3 ATR)

###Market Conditions

- **Trending markets**: Higher RSI Period (21-28)

- **Sideways markets**: Lower RSI Period (10-14)

- **Volatile markets**: Higher ATR Multiplier

## Recommended Testing Procedure

1. **Start with default settings** and backtest on 3-6 months of historical data

2. **Adjust RSI Period** to see which value produces better results

3. **Optimize ATR Multiplier** for stop loss levels

4. **Test different Risk:Reward ratios** comparatively

5. **Fine-tune Minimum Imbalance Size** to improve signal quality

## Important Considerations

- **False positive signals**: Imbalances may be less reliable during low volatility periods

- **Market openings**: First hours often produce more imbalances but can be riskier

- **News events**: Consider disabling strategy during major news releases

- **Backtesting**: Test across different market conditions (trending, sideways, volatile)

## Recommended Settings for Beginners

**Safe settings for new users:**

- RSI Period: 14

- ATR Period: 14

- ATR Stop Loss Multiplier: 2.5

- Risk:Reward Ratio: 3.0

- Minimum Imbalance Size: 0.5 ATR

- RSI Divergence Filter: Enabled

## Advanced Tips

### Signal Quality Improvement

- **Combine with market structure**: Look for imbalances near key support/resistance levels

- **Volume confirmation**: Higher volume during imbalance formation increases reliability

- **Multiple timeframe analysis**: Confirm signals on higher timeframes

### Risk Management

- **Position sizing**: Never risk more than 1-2% of account per trade

- **Maximum drawdown**: Set overall stop loss for the strategy

- **Market hours**: Consider avoiding low liquidity periods

### Performance Monitoring

- **Win rate**: Track percentage of profitable trades

- **Average R:R**: Monitor actual risk-reward achieved vs. target

- **Maximum consecutive losses**: Set alerts for strategy review

This strategy works best when combined with proper risk management and market analysis. Always backtest thoroughly before using real money and adjust parameters based on your specific market and trading style.

Machine Learning BBPct [BackQuant]Machine Learning BBPct

What this is (in one line)

A Bollinger Band %B oscillator enhanced with a simplified K-Nearest Neighbors (KNN) pattern matcher. The model compares today’s context (volatility, momentum, volume, and position inside the bands) to similar situations in recent history and blends that historical consensus back into the raw %B to reduce noise and improve context awareness. It is informational and diagnostic—designed to describe market state, not to sell a trading system.

Background: %B in plain terms

Bollinger %B measures where price sits inside its dynamic envelope: 0 at the lower band, 1 at the upper band, ~ 0.5 near the basis (the moving average). Readings toward 1 indicate pressure near the envelope’s upper edge (often strength or stretch), while readings toward 0 indicate pressure near the lower edge (often weakness or stretch). Because bands adapt to volatility, %B is naturally comparable across regimes.

Why add (simplified) KNN?

Classic %B is reactive and can be whippy in fast regimes. The simplified KNN layer builds a “nearest-neighbor memory” of recent market states and asks: “When the market looked like this before, where did %B tend to be next bar?” It then blends that estimate with the current %B. Key ideas:

• Feature vector . Each bar is summarized by up to five normalized features:

– %B itself (normalized)

– Band width (volatility proxy)

– Price momentum (ROC)

– Volume momentum (ROC of volume)

– Price position within the bands

• Distance metric . Euclidean distance ranks the most similar recent bars.

• Prediction . Average the neighbors’ prior %B (lagged to avoid lookahead), inverse-weighted by distance.

• Blend . Linearly combine raw %B and KNN-predicted %B with a configurable weight; optional filtering then adapts to confidence.

This remains “simplified” KNN: no training/validation split, no KD-trees, no scaling beyond windowed min-max, and no probabilistic calibration.

How the script is organized (by input groups)

1) BBPct Settings

• Price Source – Which price to evaluate (%B is computed from this).

• Calculation Period – Lookback for SMA basis and standard deviation.

• Multiplier – Standard deviation width (e.g., 2.0).

• Apply Smoothing / Type / Length – Optional smoothing of the %B stream before ML (EMA, RMA, DEMA, TEMA, LINREG, HMA, etc.). Turning this off gives you the raw %B.

2) Thresholds

• Overbought/Oversold – Default 0.8 / 0.2 (inside ).

• Extreme OB/OS – Stricter zones (e.g., 0.95 / 0.05) to flag stretch conditions.

3) KNN Machine Learning

• Enable KNN – Switch between pure %B and hybrid.

• K (neighbors) – How many historical analogs to blend (default 8).

• Historical Period – Size of the search window for neighbors.

• ML Weight – Blend between raw %B and KNN estimate.

• Number of Features – Use 2–5 features; higher counts add context but raise the risk of overfitting in short windows.

4) Filtering

• Method – None, Adaptive, Kalman-style (first-order),

or Hull smoothing.

• Strength – How aggressively to smooth. “Adaptive” uses model confidence to modulate its alpha: higher confidence → stronger reliance on the ML estimate.

5) Performance Tracking

• Win-rate Period – Simple running score of past signal outcomes based on target/stop/time-out logic (informational, not a robust backtest).

• Early Entry Lookback – Horizon for forecasting a potential threshold cross.

• Profit Target / Stop Loss – Used only by the internal win-rate heuristic.

6) Self-Optimization

• Enable Self-Optimization – Lightweight, rolling comparison of a few canned settings (K = 8/14/21 via simple rules on %B extremes).

• Optimization Window & Stability Threshold – Governs how quickly preferred K changes and how sensitive the overfitting alarm is.

• Adaptive Thresholds – Adjust the OB/OS lines with volatility regime (ATR ratio), widening in calm markets and tightening in turbulent ones (bounded 0.7–0.9 and 0.1–0.3).

7) UI Settings

• Show Table / Zones / ML Prediction / Early Signals – Toggle informational overlays.

• Signal Line Width, Candle Painting, Colors – Visual preferences.

Step-by-step logic

A) Compute %B

Basis = SMA(source, len); dev = stdev(source, len) × multiplier; Upper/Lower = Basis ± dev.

%B = (price − Lower) / (Upper − Lower). Optional smoothing yields standardBB .

B) Build the feature vector

All features are min-max normalized over the KNN window so distances are in comparable units. Features include normalized %B, normalized band width, normalized price ROC, normalized volume ROC, and normalized position within bands. You can limit to the first N features (2–5).

C) Find nearest neighbors

For each bar inside the lookback window, compute the Euclidean distance between current features and that bar’s features. Sort by distance, keep the top K .

D) Predict and blend

Use inverse-distance weights (with a strong cap for near-zero distances) to average neighbors’ prior %B (lagged by one bar). This becomes the KNN estimate. Blend it with raw %B via the ML weight. A variance of neighbor %B around the prediction becomes an uncertainty proxy ; combined with a stability score (how long parameters remain unchanged), it forms mlConfidence ∈ . The Adaptive filter optionally transforms that confidence into a smoothing coefficient.

E) Adaptive thresholds

Volatility regime (ATR(14) divided by its 50-bar SMA) nudges OB/OS thresholds wider or narrower within fixed bounds. The aim: comparable extremeness across regimes.

F) Early entry heuristic

A tiny two-step slope/acceleration probe extrapolates finalBB forward a few bars. If it is on track to cross OB/OS soon (and slope/acceleration agree), it flags an EARLY_BUY/SELL candidate with an internal confidence score. This is explicitly a heuristic—use as an attention cue, not a signal by itself.

G) Informational win-rate

The script keeps a rolling array of trade outcomes derived from signal transitions + rudimentary exits (target/stop/time). The percentage shown is a rough diagnostic , not a validated backtest.

Outputs and visual language

• ML Bollinger %B (finalBB) – The main line after KNN blending and optional filtering.

• Gradient fill – Greenish tones above 0.5, reddish below, with intensity following distance from the midline.

• Adaptive zones – Overbought/oversold and extreme bands; shaded backgrounds appear at extremes.

• ML Prediction (dots) – The KNN estimate plotted as faint circles; becomes bright white when confidence > 0.7.

• Early arrows – Optional small triangles for approaching OB/OS.

• Candle painting – Light green above the midline, light red below (optional).

• Info panel – Current value, signal classification, ML confidence, optimized K, stability, volatility regime, adaptive thresholds, overfitting flag, early-entry status, and total signals processed.

Signal classification (informational)

The indicator does not fire trade commands; it labels state:

• STRONG_BUY / STRONG_SELL – finalBB beyond extreme OS/OB thresholds.

• BUY / SELL – finalBB beyond adaptive OS/OB.

• EARLY_BUY / EARLY_SELL – forecast suggests a near-term cross with decent internal confidence.

• NEUTRAL – between adaptive bands.

Alerts (what you can automate)

• Entering adaptive OB/OS and extreme OB/OS.

• Midline cross (0.5).

• Overfitting detected (frequent parameter flipping).

• Early signals when early confidence > 0.7.

These are purely descriptive triggers around the indicator’s state.

Practical interpretation

• Mean-reversion context – In range markets, adaptive OS/OB with ML smoothing can reduce whipsaws relative to raw %B.

• Trend context – In persistent trends, the KNN blend can keep finalBB nearer the mid/upper region during healthy pullbacks if history supports similar contexts.

• Regime awareness – Watch the volatility regime and adaptive thresholds. If thresholds compress (high vol), “OB/OS” comes sooner; if thresholds widen (calm), it takes more stretch to flag.

• Confidence as a weight – High mlConfidence implies neighbors agree; you may rely more on the ML curve. Low confidence argues for de-emphasizing ML and leaning on raw %B or other tools.

• Stability score – Rising stability indicates consistent parameter selection and fewer flips; dropping stability hints at a shifting backdrop.

Methodological notes

• Normalization uses rolling min-max over the KNN window. This is simple and scale-agnostic but sensitive to outliers; the distance metric will reflect that.

• Distance is unweighted Euclidean. If you raise featureCount, you increase dimensionality; consider keeping K larger and lookback ample to avoid sparse-neighbor artifacts.

• Lag handling intentionally uses neighbors’ previous %B for prediction to avoid lookahead bias.

• Self-optimization is deliberately modest: it only compares a few canned K/threshold choices using simple “did an extreme anticipate movement?” scoring, then enforces a stability regime and an overfitting guard. It is not a grid search or GA.

• Kalman option is a first-order recursive filter (fixed gain), not a full state-space estimator.

• Hull option derives a dynamic length from 1/strength; it is a convenience smoothing alternative.

Limitations and cautions

• Non-stationarity – Nearest neighbors from the recent window may not represent the future under structural breaks (policy shifts, liquidity shocks).

• Curse of dimensionality – Adding features without sufficient lookback can make genuine neighbors rare.

• Overfitting risk – The script includes a crude overfitting detector (frequent parameter flips) and will fall back to defaults when triggered, but this is only a guardrail.

• Win-rate display – The internal score is illustrative; it does not constitute a tradable backtest.

• Latency vs. smoothness – Smoothing and ML blending reduce noise but add lag; tune to your timeframe and objectives.

Tuning guide

• Short-term scalping – Lower len (10–14), slightly lower multiplier (1.8–2.0), small K (5–8), featureCount 3–4, Adaptive filter ON, moderate strength.

• Swing trading – len (20–30), multiplier ~2.0, K (8–14), featureCount 4–5, Adaptive thresholds ON, filter modest.

• Strong trends – Consider higher adaptive_upper/lower bounds (or let volatility regime do it), keep ML weight moderate so raw %B still reflects surges.

• Chop – Higher ML weight and stronger Adaptive filtering; accept lag in exchange for fewer false extremes.

How to use it responsibly

Treat this as a state descriptor and context filter. Pair it with your execution signals (structure breaks, volume footprints, higher-timeframe bias) and risk management. If mlConfidence is low or stability is falling, lean less on the ML line and more on raw %B or external confirmation.

Summary

Machine Learning BBPct augments a familiar oscillator with a transparent, simplified KNN memory of recent conditions. By blending neighbors’ behavior into %B and adapting thresholds to volatility regime—while exposing confidence, stability, and a plain early-entry heuristic—it provides an informational, probability-minded view of stretch and reversion that you can interpret alongside your own process.

Information-Geometric Market DynamicsInformation-Geometric Market Dynamics

The Information Field: A Geometric Approach to Market Dynamics

By: DskyzInvestments

Foreword: Beyond the Shadows on the Wall

If you have traded for any length of time, you know " the feeling ." It is the frustration of a perfect setup that fails, the whipsaw that stops you out just before the real move, the nagging sense that the chart is telling you only half the story. For decades, technical analysis has relied on interpreting the shadows—the patterns left behind by price. We draw lines on these shadows, apply indicators to them, and hope they reveal the future.

But what if we could stop looking at the shadows and, instead, analyze the object casting them?

This script introduces a new paradigm for market analysis: Information-Geometric Market Dynamics (IGMD) . The core premise of IGMD is that the price chart is merely a one-dimensional projection of a much richer, higher-dimensional reality—an " information field " generated by the collective actions and beliefs of all market participants.

This is not just another collection of indicators. It is a unified framework for measuring the geometry of the market's information field—its memory, its complexity, its uncertainty, its causal flows—and making high-probability decisions based on that deeper reality. By fusing advanced mathematical and informational concepts, IGMD provides a multi-faceted lens through which to view market behavior, moving beyond simple price action into the very structure of market information itself.

Prepare to move beyond the flatland of the price chart. Welcome to the information field.

The IGMD Framework: A Multi-Kernel Approach

What is a Kernel? The Heart of Transformation

In mathematics and data science, a kernel is a powerful and elegant concept. At its core, a kernel is a function that takes complex, often inscrutable data and transforms it into a more useful format. Think of it as a specialized lens or a mathematical "probe." You cannot directly measure abstract concepts like "market memory" or "trend quality" by looking at a price number. First, you must process the raw price data through a specific mathematical machine—a kernel—that is designed to output a measurement of that specific property. Kernels operate by performing a sort of "similarity test," projecting data into a higher-dimensional space where hidden patterns and relationships become visible and measurable.

Why do creators use them? We use kernels to extract features —meaningful pieces of information—that are not explicitly present in the raw data. They are the essential tools for moving beyond surface-level analysis into the very DNA of market behavior. A simple moving average can tell you the average price; a suite of well-chosen kernels can tell you about the character of the price action itself.

The Alchemist's Challenge: The Art of Fusion

Using a single kernel is a challenge. Using five distinct, computationally demanding mathematical engines in unison is an immense undertaking. The true difficulty—and artistry—lies not just in using one kernel, but in fusing the outputs of many . Each kernel provides a different perspective, and they can often give conflicting signals. One kernel might detect a strong trend, while another signals rising chaos and uncertainty. The IGMD script's greatest strength is its ability to act as this alchemist, synthesizing these disparate viewpoints through a weighted fusion process to produce a single, coherent picture of the market's state. It required countless hours of testing and calibration to balance the influence of these five distinct analytical engines so they work in harmony rather than cacophony.

The Five Kernels of Market Dynamics

The IGMD script is built upon a foundation of five distinct kernels, each chosen to probe a unique and critical dimension of the market's information field.

1. The Wavelet Kernel (The "Microscope")

What it is: The Wavelet Kernel is a signal processing function designed to decompose a signal into different frequency scales. Unlike a Fourier Transform that analyzes the entire signal at once, the wavelet slides across the data, providing information about both what frequencies are present and when they occurred.

The Kernels I Use:

Haar Kernel: The simplest wavelet, a square-wave shape defined by the coefficients . It excels at detecting sharp, sudden changes.

Daubechies 2 (db2) Kernel: A more complex and smoother wavelet shape that provides a better balance for analyzing the nuanced ebb and flow of typical market trends.

How it Works in the Script: This kernel is applied iteratively. It first separates the finest "noise" (detail d1) from the first level of trend (approximation a1). It then takes the trend a1 and repeats the process, extracting the next level of cycle (d2) and trend (a2), and so on. This hierarchical decomposition allows us to separate short-term noise from the long-term market "thesis."

2. The Hurst Exponent Kernel (The "Memory Gauge")

What it is: The Hurst Exponent is derived from a statistical analysis kernel that measures the "long-term memory" or persistence of a time series. It is the definitive measure of whether a series is trending (H > 0.5), mean-reverting (H < 0.5), or random (H = 0.5).

How it Works in the Script: The script employs a method based on Rescaled Range (R/S) analysis. It calculates the average range of price movements over increasingly larger time lags (m1, m2, m4, m8...). The slope of the line plotting log(range) vs. log(lag) is the Hurst Exponent. Applying this complex statistical analysis not to the raw price, but to the clean, wavelet-decomposed trend lines, is a key innovation of IGMD.

3. The Fractal Dimension Kernel (The "Complexity Compass")

What it is: This kernel measures the geometric complexity or "jaggedness" of a price path, based on the principles of fractal geometry. A straight line has a dimension of 1; a chaotic, space-filling line approaches a dimension of 2.

How it Works in the Script: We use a version based on Ehlers' Fractal Dimension Index (FDI). It calculates the rate of price change over a full lookback period (N3) and compares it to the sum of the rates of change over the two halves of that period (N1 + N2). The formula d = (log(N1 + N2) - log(N3)) / log(2) quantifies how much "longer" and more convoluted the price path was than a simple straight line. This kernel is our primary filter for tradeable (low complexity) vs. untradeable (high complexity) conditions.

4. The Shannon Entropy Kernel (The "Uncertainty Meter")

What it is: This kernel comes from Information Theory and provides the purest mathematical measure of information, surprise, or uncertainty within a system. It is not a measure of volatility; a market moving predictably up by 10 points every bar has high volatility but zero entropy .

How it Works in the Script: The script normalizes price returns by the ATR, categorizes them into a discrete number of "bins" over a lookback window, and forms a probability distribution. The Shannon Entropy H = -Σ(p_i * log(p_i)) is calculated from this distribution. A low H means returns are predictable. A high H means returns are chaotic. This kernel is our ultimate gauge of market conviction.

5. The Transfer Entropy Kernel (The "Causality Probe")

What it is: This is by far the most advanced and computationally intensive kernel in the script. Transfer Entropy is a non-parametric measure of directed information flow between two time series. It moves beyond correlation to ask: "Does knowing the past of Volume genuinely reduce our uncertainty about the future of Price?"

How it Works in the Script: To make this work, the script discretizes both price returns and the chosen "driver" (e.g., OBV) into three states: "up," "down," or "neutral." It then builds complex conditional probability tables to measure the flow of information in both directions. The Net Transfer Entropy (TE Driver→Price minus TE Price→Driver) gives us a direct measure of causality . A positive score means the driver is leading price, confirming the validity of the move. This is a profound leap beyond traditional indicator analysis.

Chapter 3: Fusion & Interpretation - The Field Score & Dashboard

Each kernel is a specialist providing a piece of the puzzle. The Field Score is where they are fused into a single, comprehensive reading. It's a weighted sum of the normalized scores from all five kernels, producing a single number from -1 (maximum bearish information field) to +1 (maximum bullish information field). This is the ultimate "at-a-glance" metric for the market's net state, and it is interpreted through the dashboard.

The Dashboard: Your Mission Control

Field Score & Regime: The master metric and its plain-English interpretation ("Uptrend Field", "Downtrend Field", "Transitional").

Kernel Readouts (Wave Align, H(w), FDI, etc.): The live scores of each individual kernel. This allows you to see why the Field Score is what it is. A high Field Score with all components in agreement (all green or red) is a state of High Coherence and represents a high-quality setup.

Market Context: Standard metrics like RSI and Volume for additional confluence.

Signals: The raw and adjusted confluence counts and the final, calculated probability scores for potential long and short entries.

Pattern: Shows the dominant candlestick pattern detected within the currently forming APEX range box and its calculated confidence percentage.

Chapter 4: Mastering the Controls - The Inputs Menu

Every parameter is a lever to fine-tune the IGMD engine.

📊 Wavelet Transform: Kernel ( Haar for sharp moves, db2 for smooth trends) and Scales (depth of analysis) let you tune the script's core microscope to your asset's personality.

📈 Hurst Exponent: The Window determines if you're assessing short-term or long-term market memory.