Weighted percentile nearest rankYo, posting it for the whole internet, took the whole day to find / to design the actual working solution for weighted percentile 'nearest rank' algorithm, almost no reliable info online and a lot of library-style/textbook-style solutions that don't provide on real world production level.

The principle:

0) initial data

data = 22, 33, 11, 44, 55

weights = 5 , 3 , 2 , 1 , 4

array(s) size = 5

1) sort data array, apply the sorting pattern to the weights array, resulting:

data = 11, 22, 33, 44, 55

weights = 2 , 5 , 3 , 1 , 4

2) get weights cumsum and sum:

weights = 2, 5, 3 , 1 , 4

weights_cum = 2, 7, 10, 11, 15

weights_sum = 15

3) say we wanna find 50th percentile, get a threshold value:

n = 50

thres = weights_sum / 100 * n

7.5 = 15 / 100 * 50

4) iterate through weights_cum until you find a value that >= the threshold:

for i = 0 to size - 1

2 >= 7.5 ? nah

7 >= 7.5 ? nah

10 >= 7.5 ? aye

5) take the iteration index that resulted "aye", and find the data value with the same index, that's gonna be the resulting percentile.

i = 2

data = 33

This one is not an approximation, not an estimator, it's the actual weighted percentile nearest rank as it is.

I tested the thing extensively and it works perfectly.

For the skeptics, check lines 40, 41, 69 in the code, you can comment/uncomment dem to switch for unit (1) weights, resulting in the usual non-weighted percentile nearest rank that ideally matches the TV's built-in function.

Shoutout for @wallneradam for the sorting function mane

...

Live Long and Prosper

In den Scripts nach "机械革命无界15+时不时闪屏" suchen

Inside Bar SetupScript Details

- This script plots Inside Bar for given day in selected time-frame (applicable only for Timeframes < Day)

- Basis plotted inside bar, relevant targets are marked on the chart

- Targets can be customised from script settings. Example, if range of mother candle is 10 points, then T1 is 10 * x above/below mother candle and T2 is 10 * y above/below mother candle. This x & y are configured via script settings

How to use this script ?

- This script works well on 10-15 mins timeframe for stocks, 15/30 mins timeframe for nifty index and 30/60 mins time frame for bank nifty index

- If mother candle high is broken, take long trade with SL of mother candle low and if low is broken, take short trade with SL of mother candle high

Remember:

1. Above logic is to be combined with support/resistances i.e. price action. This script is an add-on to price action analysis giving you more conviction.

2. If range of mother candle is very high, it is recommended to avoid the trade.

3. Basis inside bar formed on higher time frame, take trade on basis of lower time frame i.e if inside bar is formed on 60 mins, take trade on the basis of 10-15 mins time frame

Example:

1. As seen in the chart, Nifty is near it's resistance and we are seeing Inside Bar being formed, In such scenario, even if High of Mother Candle is broken, we should be more interested to short as we are near resistance and probability of getting our targets in long side is less.

2. So, if I see breakdown of mother candle i.e. price going below low of mother candle, we will short with SL of high of mother candle.

3. As seen in the chart, both the targets are achieved.

Additional Info:

1. Targets on Long/Short Side can be configured via settings. For indices 1 times/1.5 times the range works well.

2. This script plots targets basis the first inside bar formed in the day for selected time frame.

3. Inside bars formed through out the day are coloured separately but lines are plotted only on the basis of 1st formed inside bar as this strategy works well for the first formed inside bar)

4. Don't forget to check volume in case of breakout/breakdown.

Note:

1. Mother Candle - First Candle of Inside Bar

2. Child Candle - Candle formed inside Mother Candle (Second Candle of Inside Bar)

Happy Trading :)

Trade HourThis script is just finds the best hour to buy and sell hour in a day by checking chart movements in past

For example if the red line is on the 0.63 on BTC/USDT chart it mean the start of 12AM hour on a day is the best hour to buy (all based on

It's just for 1 hour time-frame but you can test it on other charts.

IMPORTANT: You can change time Zone in strategy settings.to get the real hours as your location timezone

IMPORTANT: Its for now just for BTC/USDT but you can optimize and test for other charts...

IMPORTANT: A green and red background color calculated for show the user the best places of buy and sell (green : positive signal, red: negative signals)

settings :

timezone : We choice a time frame for our indicator as our geo location

source : A source to calculate rate of change for it

Time Period : Time period of ROC indicator

About Calculations:

1- We first get a plot that just showing the present hour as a zigzag plot

2- So we use an indicator ( Rate of change ) to calculate chart movements as positive and negative numbers. I tested ROC is the best indicator but you can test close-open or real indicator or etc as indicator.

3 - for observe effects of all previous data we should indicator_cum that just a full sum of indicator values.

4- now we need to split this effects to hours and find out which hour is the best place to buy and which is the best for sell. Ok we should just calculate multiple of hour*indicator and get complete sum of it so:

5- we will divide this number to indicator_cum : (indicator_mul_hour_cum) / indicator_cum

6- Now we have the best hour to buy! and for best sell we should just reverse the ROC indicator and recalculate the best hour for it!

7- A green and red background color calculated for show the user the best places of buy and sell that dynamically changing with observing green and red plots(green : positive signal, red: negative signals) when green plot on 15 so each day on hour 15 the background of strategy indicator will change to 15 and if its go upper after some days and reached to 16 the background green color will move to 16 dynamically.

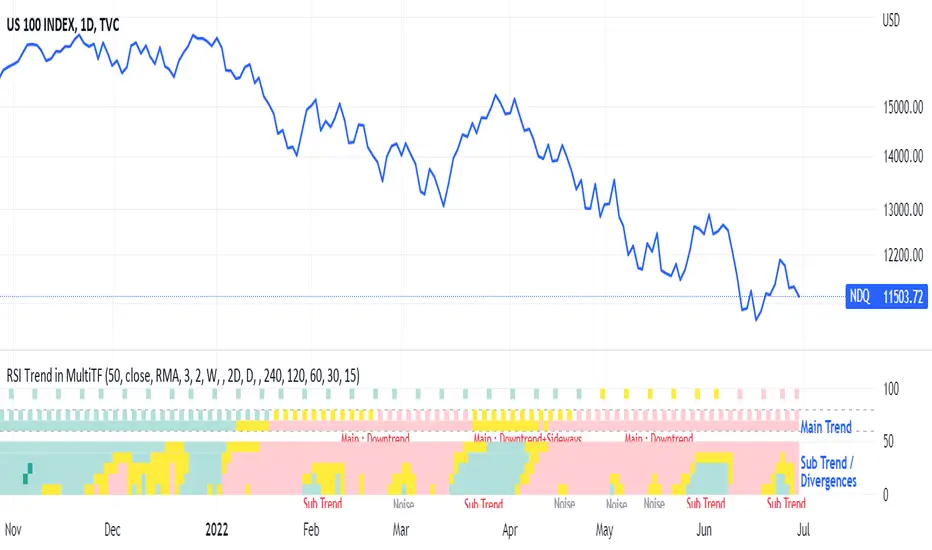

RSI Trend Heatmap in Multi TimeframesRSI Trend Heatmap in Multi Timeframes

Description

Sometimes you want to look at the RSI Trend across multiple time frames.

You have to waste time browsing through them.

So we've put together every time frame you want to see in one indicator.

We have 10 layers of RSI Trend heatmap available for you.

You can set the timeframe as you want on the Settings page.

Description of Parameter RSI Setting ** You can change it by setting.

RSI Trend Length : (Default 50)

Source : (Default close)

RSI Sideways Length : (Default 2 = RSI between 48 .. 52)

Description of Parameter RSI Timeframe ** You can change it by setting.

""=None,

"M"=1Month, "2W"=2Weeks, "W"=1Week,

"3D"=3Days, "2D"=2Days, "D"=1Day,

"720"=12Hours, "480"=4Hours, "240"=4Hours, "180"=3Hours, "120"=2Hours,

"60"=60Minutes, "30"=30Minutes, "15"=15Minutes, "5"=5Minutes, "1"=1Minute

Default Configurate of RSI Timeframe (for a time frame of 1 hour to 1 day)

"W"= Timeframe 1 month shown in line 90-100 --> Represent Long Trend of RSI

---------------------------------------

"D2"= Timeframe 2 days shown in line 70-80 --> Represent Trend of RSI

"D"= Timeframe 1 day shown in line 60-70 --> Represent Trend of RSI

---------------------------------------

"240"= Timeframe 3 hours shown in line 40-50 --> Represent Signal Up/Signal Down/Divergence of RSI

"120"= Timeframe 2 hours shown in line 30-40 --> Represent Signal Up/Signal Down/Divergence of RSI

"60"= Timeframe 1 hour shown in line 20-30 --> Represent Signal Up/Signal Down/Divergence of RSI

"30"= Timeframe 30 minutes shown in line 10-20 --> Represent Signal Up/Signal Down/Divergence of RSI

"15"= Timeframe 15 minutes shown in line 00-10 --> Represent Signal Up/Signal Down/Divergence of RSI

Description of Colors

Dark Bule = Extreme Uptrend / Overbought / Bull Market (RSI > 67)

Light Bule = Uptrend (RSI between 50-52 .. 67)

Yellow = Sideways Trend / Trend Reversal (RSI between 48 .. 52) ** You can change it by setting.

Light Red = Downtrend (RSI between 33 .. 48-50)

Dark Red = Extreme Downtrend / Oversold / Bear Market (RSI < 33)

How to use

1. You must first know what the main trend of the RSI is (look at the 60-80 line). If it is red, it is a downtrend. and if it's blue shows that it is an uptrend

2. Throughout the period of the main trend There will always be a reversal of the sub-trend. (Can see from the 0-50 line), but eventually will return to follow the main trend.

3. Unless the sub trend persists for a long time until the main trend changes.

Bollinger CloudsThis indicator plots Bollinger Bands for your current timeframe (e.g 5 minutes) and also plots the Bollinger Bands for a higher timeframe (15 minutes for 5 minute timeframe). Then the gaps between the current and higher timeframe upper and lower bands is filled to create clouds which can be used as entry zones. Like Bollinger Bands, this indicator shouldn't be solely used for entries, use it in conjunction with other indicators.

Bollinger Band Timeframes

Current / Higher

1 minute / 5 minutes

3 minutes / 10 minutes

5 minutes / 15 minutes

10 minutes / 30 minutes

15 minutes / 1 hour

30 minutes / 2 hours

45 minutes / 1.5 hours

1 hour / 4 hours

2 hours / 8 hours

2.5 hours / 10 hours

4 hours / 1 Day

1 Day / 3 Days

3 Days / 9 Days

5 Days / 2 Weeks

1 Week / 1 Month

GANN Square Of 9 PivotsGANN Square Of 9 Pivots

How to use for Intraday ?

Method 01 (From 9:05 am to 9:15 am or pre-open market)

Take the Weighted Average Price or Volume Weighted Average Price (VWAP) or Time Weighted Average Price (TWAP) of any stock or index.

You can use TWAP for Index as volume is not available.

Method 02 (From 9:05 am to 9:15 am or pre-open market)

Take the Last Traded Price (LTP) of index or stock

Method 03 (After 9:30 am or after 1st 15 min)

Only take Last Traded Price (LTP) of stock or index

Ideal Time

15min to 1hr after market opens

Indicator Features

Lines

Gray Dashed Line: Calculation Price

Teal Solid Line: Long Above

Red Solid Line: Short Below

3 Teal Dotted Lines: Bullish Targets 1, 2 & 3

3 Red Dotted Lines: Bearish Targets 1, 2 & 3

Labels

1st Numbers: Price

2nd Numbers in (): % change from LTP to that Level

For Index

As VWAP is not available for Index, TWAP (Time Weighted Average Price) values can be used for Index.

Custom Price Inputs

Price of your choice can be given manually by selecting:

Source > Custom

Enter Price > (type the price)

Timeframe

Higher timeframes like Weekly, Monthly can be changed using Timeframe Option

For More Reading

Reading: traderji.com/community/threads/intraday-trading-using-gann-calculator.39185/#post-419677

Calculator: stockmaniacs.net/freebies/free-tools/gann-square-of-9-calculator/

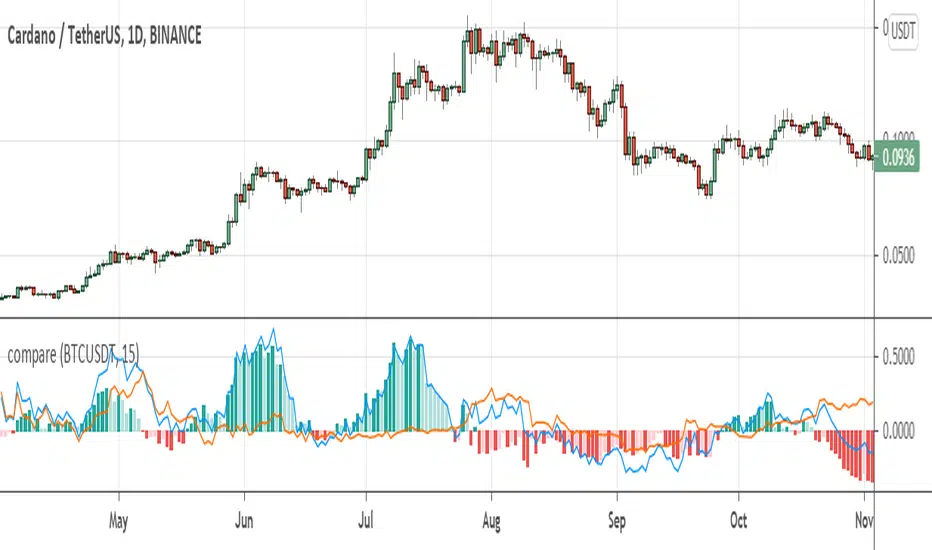

compare returnsIt could be very useful to analyze market with events in the market instead of only looking at the isolated chart. This indicator helps you to compare returns of chart symbol with any other symbol in the same timeframe.

For example, in crypto market coins move with the Bitcoin and BTC is driver of the market, so it could be useful to compare returns of a coin with the Bitcoin. There is a compare feature in tradingview, but it only compare from the beginning of the chart, not showing historical difference between returns which can reveals statistical opportunities or money flow in the market or between markets.

This indicator take two parameters including base symbol and period:

base symbol is the one which you need comparison with and period sets the period of comparison.

For instance, with base symbol: BTCUSDT and period: 15, return of BTCUSDT from 15 previous candles is compared with the chart in 15 previous candles (on same timeframe).

It could be helpful if you use this indicator to compare these pairs:

- altcoins return with BTCUSDT return

- stocks with their market index or industry index.

- market indices: crypto total market cap with SP500 and GOLD

please leave comment for me and this indicator to share your idea with me.

thanks,

hadi jamshidi

ADX of VortexHow to Trade

> Rising ADX of Vortex from 10 to 15 is trend building area to be noticed.

> If ADX of Vortex is falling but above 10 and below 15 avoid trade in such case because even if signal is generated by cross over of Vi-Plus and VI-Minus it may not give good profit.

> Once the position is taken and Price is steady but ADX of Vortex is falling then keep eye on cross over of Vi-Plus and VI-Minus to exit from trade.

> ADX rising above 15 is strong trending signal.

Rainbow Trend IndicatorThis is an indicator based on the MA rainbow concept. It is possible to choose between 15 or 20 MA's and if all 15 MA's is picked, the calculation will be calculated on 15 MA's and if 20 is picked the calculation is calculated on 20 MA's. The indicator will then be a line which is assigned a value from the calculation based on the MA's. If the line is above the dashed zero line, meaning the line's last value is a positive value, the price is in a uptrend and if the line is below the dashed zero line, meaning the line's last value is a negative value, the price is in a downtrend.

In short

If the line is green, the price is in a uptrend. If the line is red, the price is in a downtrend.

Day start top and bottomThis code is modified to draw the first 15 minutes(variable in setting by default 15m is set) of the high and lows through out the day.

It will work on time frames less than than or equal to 1st input. Hope this code helps you all.

IMPORTANT SETTING DETAILS:

1.Res = input(title="Starting X minutes lines to be Displayed",defval="15", type=input.resolution)

2.Day_start_15m=input("0915-0930",title="your country's Trading session time (starting X minutes)")

make sure to enter the starting 15 min of your country trading time in the input in 2nd input

both the above input 1 and 2 must be equal in time i.e "0915-0930"=15min and first one is also 15m

you need to make sure that the input settings are correct. It is By default set For INDIAs trading start time, you have to set start time according to your country.

mForex - Keltner channel + EMA Scalping systemTransaction setup parameters

Time frame: M5, M15

Currency pair: EUR / USD , GPB / USD

Transaction: London, USA

Number of orders / day: 10 - 15 orders

Trading strategies

=== BUY ===

Candles close on the upper Keltner

EMA10 crosses the upper Keltner range from below

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

=== SELL ===

Candles close below Keltner below

EMA10 crosses the Keltner range below from above

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

ADD for SPX intraday (NYSE Adv-Decl) -Tom1traderThis is the NYSE Advancers - decliners which the SPX pretty much follows. You can chart it like any index (ADD -NYSE $ADV MINUS $DECL) but I find it more useful in a separate panel with colors for direction.

The level gives an idea of days move (example: plus or minus 500 is not much movement through the session) but I follow the direction as when more stocks advance (green) or decline (red) the index tends to track it pretty closely.

On SPX, SPY and correlateds - very useful for intra-day trading (Scalping or 0DTE option trades) but not for higher time frames at all. If you chart the ADD in a chart and compare 5 minute to daily you will see what I mean.

I left it at 5 minutes timeframe which displays well on any intraday chart. You can change it by changing the "5" in the security function on line 13 to what you want ("1" 1 minute, "15" 15 minutes) or change it to timeframe.period (no quotes) so that it will follow the timeframe of the current chart. I like 5 min as it displays better on higher timeframes i.e. 15 min. or hour.

A simple moving average with a length of 10 is added to help gauge momemtum.

Hope this helps with trading or scripting ideas, questions or feed back welcome. Keep Smiling.

Bar Balance [LucF]Bar Balance extracts the number of up, down and neutral intrabars contained in each chart bar, revealing information on the strength of price movement. It can display stacked columns representing raw up/down/neutral intrabar counts, or an up/down balance line which can be calculated and visualized in many different ways.

WARNING: This is an analysis tool that works on historical bars only. It does not show any realtime information, and thus cannot be used to issue alerts or for automated trading. When realtime bars elapse, the indicator will require a browser refresh, a change to its Inputs or to the chart's timeframe/symbol to recalculate and display information on those elapsed bars. Once a trader understands this, the indicator can be used advantageously to make discretionary trading decisions.

Traders used to work with my Delta Volume Columns Pro will feel right at home in this indicator's Inputs . It has lots of options, allowing it to be used in many different ways. If you value the bar balance information this indicator mines, I hope you will find the time required to master the use of Bar Balance well worth the investment.

█ OVERVIEW

The indicator has two modes: Columns and Line .

Columns

• In Columns mode you can display stacked Up/Down/Neutral columns.

• The "Up" section represents the count of intrabars where `close > open`, "Down" where `close < open` and "Neutral" where `close = open`.

• The Up section always appears above the centerline, the Down section below. The Neutral section overlaps the centerline, split halfway above and below it.

The Up and Down sections start where the Neutral section ends, when there is one.

• The Up and Down sections can be colored independently using 7 different methods.

• The signal line plotted in Line mode can also be displayed in Columns mode.

Line

• Displays a single balance line using a zero centerline.

• A variable number of independent methods can be used to calculate the line (6), determine its color (5), and color the fill (5).

You can thus evaluate the state of 3 different components with this single line.

• A "Divergence Levels" feature will use the line to automatically draw expanding levels on divergence events.

Features available in both modes

• The color of all components can be selected from 15 base colors, with 16 gradient levels used for each base color in the indicator's gradients.

• A zero line can show a 6-state aggregate value of the three main volume balance modes.

• The background can be colored using any of 5 different methods.

• Chart bars can be colored using 5 different methods.

• Divergence and large neutral count ratio events can be shown in either Columns or Line mode, calculated in one of 4 different methods.

• Markers on 6 different conditions can be displayed.

█ CONCEPTS

Intrabar inspection

Intrabar inspection means the indicator looks at lower timeframe bars ( intrabars ) making up a given chart bar to gather its information. If your chart is on a 1-hour timeframe and the intrabar resolution determined by the indicator is 5 minutes, then 12 intrabars will be analyzed for each chart bar and the count of up/down/neutral intrabars among those will be tallied.

Bar Balances and calculation methods

The indicator uses a variety of methods to evaluate bar balance and to derive other calculations from them:

1. Balance on Bar : Uses the relative importance of instant Up and Down counts on the bar.

2. Balance Averages : Uses the difference between the EMAs of Up and Down counts.

3. Balance Momentum : Starts by calculating, separately for both Up and Down counts, the difference between the same EMAs used in Balance Averages and an SMA of double the period used for the EMAs. These differences are then aggregated and finally, a bounded momentum of that aggregate is calculated using RSI.

4. Markers Bias : It sums the bull/bear occurrences of the four previous markers over a user-defined period (the default is 14).

5. Combined Balances : This is the aggregate of the instant bull/bear bias of the three main bar balances.

6. Dual Up/Down Averages : This is a display mode showing the EMA calculated for each of the Up and Down counts.

Interpretation of neutral intrabars

What do neutral intrabars mean? When price does not change during a bar, it can be because there is simply no interest in the market, or because of a perfect balance between buyers and sellers. The latter being more improbable, Bar Balance assumes that neutral bars reveal a lack of interest, which entails uncertainty. That is the reason why the option is provided to interpret ratios of neutral intrabars greater than 50% as divergences. It is also the rationale behind the option to dampen signal lines on the inverse ratio of neutral intrabars, so that zero intrabars do not affect the signal, and progressively larger proportions of neutral intrabars will reduce the signal's amplitude, as the balance calcs using the up/down counts lose significance. The impact of the dampening will vary with markets. Weaker markets such as cryptos will often contain greater numbers of neutral intrabars, so dampening the Line in that sector will have a greater impact than in more liquid markets.

█ FEATURES

1 — Columns

• While the size of the Up/Down columns always represents their respective importance on the bar, their coloring mode is independent. The default setup uses a standard coloring mode where the Up/Down columns over/under the zero line are always in the bull/bear color with a higher intensity for the winning side. Six other coloring modes allow you to pack more information in the columns. When choosing to color the top columns using a bull/bear gradient on Balance Averages, for example, you will end up with bull/bear colored tops. In order for the color of the bottom columns to continue to show the instant bar balance, you can then choose the "Up/Down Ratio on Bar — Dual Solid Colors" coloring mode to make those bars the color of the winning side for that bar.

• Line mode shows only the line, but Columns mode allows displaying the line along with it. If the scale of the line is different than that of the scale of the columns, the line will often appear flat. Traders may find even a flat line useful as its bull/bear colors will be easily distinguishable.

2 — Line

• The default setup for Line mode uses a calculation on "Balance Momentum", with a fill on the longer-term "Balance Averages" and a line color based on the "Markers Bias". With the background set on "Line vs Divergence Levels" and the zero line on the hard-coded "Combined Bar Balances", you have access to five distinct sources of information at a glance, to which you can add divergences, divergences levels and chart bar coloring. This provides powerful potential in displaying bar balance information.

• When no columns are displayed, Line mode can show the full scale of whichever line you choose to calculate because the columns' scale no longer interferes with the line's scale.

• Note that when "Balance on Bar" is selected, the Neutral count is also displayed as a ratio of the balance line. This is the only instance where the Neutral count is displayed in Line mode.

• The "Dual Up/Down Averages" is an exception as it displays two lines: one average for the Up counts and another for the Down counts. This mode will be most useful when Columns are also displayed, as it provides a reference for the top and bottom columns.

3 — Zero Line

The zero line can be colored using two methods, both based on the Combined Balances, i.e., the aggregate of the instant bull/bear bias of the three main bar balances.

• In "Six-state Dual Color Gradient" mode, a dot appears on every bar. Its color reflects the bull/bear state of the Combined Balances, and the dot's brightness reflects the tally of balance biases.

• In "Dual Solid Colors (All Bull/All Bear Only)" a dot only appears when all three balances are either bullish or bearish. The resulting pattern is identical to that of Marker 1.

4 — Divergences

• Divergences are displayed as a small circle at the top of the scale. Four different types of divergence events can be detected. Divergences occur whenever the bull/bear bias of the method used diverges with the bar's price direction.

• An option allows you to include in divergence events instances where the count of neutral intrabars exceeds 50% of the total intrabar count.

• The divergence levels are dynamic levels that automatically build from the line's values on divergence events. On consecutive divergences, the levels will expand, creating a channel. This implementation of the divergence levels corresponds to my view that divergences indicate anomalies, hesitations, points of uncertainty if you will. It excludes any association of a pre-determined bullish/bearish bias to divergences. Accordingly, the levels merely take note of divergence events and mark those points in time with levels. Traders then have a reference point from which they can evaluate further movement. The bull/bear/neutral colors used to plot the levels are also congruent with this view in that they are determined by price's position relative to the levels, which is how I think divergences can be put to the most effective use.

5 — Background

• The background can show a bull/bear gradient on four different calculations. You can adjust its brightness to make its visual importance proportional to how you use it in your analysis.

6 — Chart bars

• Chart bars can be colored using five different methods.

• You have the option of emptying the body of bars where volume does not increase, as does my TLD indicator, the idea behind this being that movement on bars where volume does not increase is less relevant.

7 — Intrabar Resolution

You can choose between three modes. Two of them are automatic and one is manual:

a) Fast, Longer history, Auto-Steps (~12 intrabars) : Optimized for speed and deeper history. Uses an average minimum of 12 intrabars.

b) More Precise, Shorter History Auto-Steps (~24 intrabars) : Uses finer intrabar resolution. It is slower and provides less history. Uses an average minimum of 24 intrabars.

c) Fixed : Uses the fixed resolution of your choice.

Auto-Steps calculations vary for 24/7 and conventional markets in order to achieve the proper target of minimum intrabars.

You can choose to view the intrabar resolution currently used to calculate delta volume. It is the default.

The proper selection of the intrabar resolution is important. It must achieve maximal granularity to produce precise results while not unduly slowing down calculations, or worse, causing runtime errors.

8 — Markers

Six markers are available:

1. Combined Balances Agreement : All three Bar Balances are either bullish or bearish.

2. Up or Down % Agrees With Bar : An up marker will appear when the percentage of up intrabars in an up chart bar is greater than the specified percentage. Conditions mirror to down bars.

3. Divergence confirmations By Price : One of the four types of balance calculations can be used to detect divergences with price. Confirmations occur when the bar following the divergence confirms the balance bias. Note that the divergence events used here do not include neutral intrabar events.

4. Balance Transitions : Bull/bear transitions of the selected balance.

5. Markers Bias Transitions : Bull/bear transitions of the Markers Bias.

6. Divergence Confirmations By Line : Marks points where the line first breaches a divergence level.

Markers appear when the condition is detected, without delay. Since nothing is plotted in realtime, markers do not appear on the realtime bar.

9 — Settings

• Two modes can be selected to dampen the line on the ratio of neutral intrabars.

• A distinct weight can be attributed to the count of the latter half of intrabars, on the assumption that later intrabars may be more important in determining the outcome of chart bars.

• Allows control over the periods of the different moving averages used in calculations.

• The default periods used for the various calculations define the following hierarchy from slow to fast:

Balance Averages: 50,

Balance Momentum: 20,

Dual Up/Down Averages: 20,

Marker Bias: 10.

█ LIMITATIONS

• This script uses a special characteristic of the `security()` function allowing the inspection of intrabars—which is not officially supported by TradingView.

• The method used does not work on the realtime bar—only on historical bars.

• The indicator only works on some chart resolutions: 3, 5, 10, 15 and 30 minutes, 1, 2, 4, 6, and 12 hours, 1 day, 1 week and 1 month. The script’s code can be modified to run on other resolutions, but chart resolutions must be divisible by the lower resolution used for intrabars and the stepping mechanism could require adaptation.

• When using the "Line vs Divergence Levels — Dual Color Gradient" color mode to fill the line, background or chart bars, keep in mind that a line calculation mode must be defined for it to work, as it determines gradients on the movement of the line relative to divergence levels. If the line is hidden, it will not work.

• When the difference between the chart’s resolution and the intrabar resolution is too great, runtime errors will occur. The Auto-Steps selection mechanisms should avoid this.

• Alerts do not work reliably when `security()` is used at intrabar resolutions. Accordingly, no alerts are configured in the indicator.

• The color model used in the indicator provides for fancy visuals that come at a price; when you change values in Inputs , it can take 20 seconds for the changes to materialize. Luckily, once your color setup is complete, the color model does not have a large performance impact, as in normal operation the `security()` calls will become the most important factor in determining response time. Also, once in a while a runtime error will occur when you change inputs. Just making another change will usually bring the indicator back up.

█ RAMBLINGS

Is this thing useful?

I'll let you decide. Bar Balance acts somewhat like an X-Ray on bars. The intrabars it analyzes are no secret; one can simply change the chart's resolution to see the same intrabars the indicator uses. What the indicator brings to traders is the precise count of up/down/neutral intrabars and, more importantly, the calculations it derives from them to present the information in a way that can make it easier to use in trading decisions.

How reliable is Bar Balance information?

By the same token that an up bar does not guarantee that more up bars will follow, future price movements cannot be inferred from the mere count of up/down/neutral intrabars. Price movement during any chart bar for which, let's say, 12 intrabars are analyzed, could be due to only one of those intrabars. One can thus easily see how only relying on bar balance information could be very misleading. The rationale behind Bar Balance is that when the information mined for multiple chart bars is aggregated, it can provide insight into the history behind chart bars, and thus some bias as to the strength of movements. An up chart bar where 11/12 intrabars are also up is assumed to be stronger than the same up bar where only 2/12 intrabars are up. This logic is not bulletproof, and sometimes Bar Balance will stray. Also, keep in mind that balance lines do not represent price momentum as RSI would. Bar Balance calculations have no idea where price is. Their perspective, like that of any historian, is very limited, constrained that it is to the narrow universe of up/down/neutral intrabar counts. You will thus see instances where price is moving up while Balance Momentum, for example, is moving down. When Bar Balance performs as intended, this indicates that the rally is weakening, which does necessarily imply that price will reverse. Occasionally, price will merrily continue to advance on weakening strength.

Divergences

Most of the divergence detection methods used here rely on a difference between the bias of a calculation involving a multi-bar average and a given bar's price direction. When using "Bar Balance on Bar" however, only the bar's balance and price movement are used. This is the default mode.

As usual, divergences are points of interest because they reveal imbalances, which may or may not become turning points. I do not share the overwhelming enthusiasm traders have for the purported ability of bullish/bearish divergences to indicate imminent reversals.

Superfluity

In "The Bed of Procrustes", Nassim Nicholas Taleb writes: To bankrupt a fool, give him information . Bar Balance can display lots of information. While learning to use a new indicator inevitably requires an adaptation period where we put it through its paces and try out all its options, once you have become used to Bar Balance and decide to adopt it, rigorously eliminate the components you don't use and configure the remaining ones so their visual prominence reflects their relative importance in your analysis. I tried to provide flexible options for traders to control this indicator's visuals for that exact reason—not for window dressing.

█ NOTES

For traders

• To avoid misleading traders who don't read script descriptions, the indicator shows nothing in the realtime bar.

• The Data Window shows key values for the indicator.

• All gradients used in this indicator determine their brightness intensities using advances/declines in the signal—not their relative position in a fixed scale.

• Note that because of the way gradients are optimized internally, changing their brightness will sometimes require bringing down the value a few steps before you see an impact.

• Because this indicator does not use volume, it will work on all markets.

For coders

• For those interested in gradients, this script uses an advanced version of the Advance/Decline gradient function from the PineCoders Color Gradient (16 colors) Framework . It allows more precise control over the range, steps and min/max values of the gradients.

• I use the PineCoders Coding Conventions for Pine to write my scripts.

• I used functions modified from the PineCoders MTF Selection Framework for the selection of timeframes.

█ THANKS TO:

— alexgrover who helped me think through the dampening method used to attenuate signal lines on high ratios of neutral intrabars.

— A guy called Kuan who commented on a Backtest Rookies presentation of their Volume Profile indicator . The technique I use to inspect intrabars is derived from Kuan's code.

— theheirophant , my partner in the exploration of the sometimes weird abysses of `security()`’s behavior at intrabar resolutions.

— midtownsk8rguy , my brilliant companion in mining the depths of Pine graphics. He is also the co-author of the PineCoders Color Gradient Frameworks .

(JS)DMI BarsAlright - so this is my own version of John Carter's "10x Bars"... I have done multiple things that are different from his version so they are slightly different..

So first of all the main indicator is based off of the ADX and the DMI;

For those who aren't familiar with it, Directional Movement is what you'd pull up under "built-in's" from the indicators tab (if you want to check it out).

The standard interpretation of this however, is when the ADX is above 20 that suggests the trend is strong, whereas under 20 suggests it is weak.

Also, when the D+ is above the D- that suggests a bullish trend, and D- above D+ suggests a bearish trend.

These bars take away the need to have it at the bottom of your screen, and places the data on the bars on your chart instead.

=========================================================================================================================================

So here's what the colors stand for -

Yellow - The ADX is under 20, no strength in trend

Shades of green occur when the ADX is above 20 and there's a bullish trend (D+ higher than D-)

Bright Green (Lime) - Bullish trend, D+ above 30

Green - Bullish Trend

Yellow Green - Bullish trend, D+ below 15

Shades of red occur when the ADX is above 20 and there's a bearish trend (D- higher than D+)

Bright Red - Bearish trend, D- above 30

Red - Bearish Trend

Orange - Bearish trend, D- below 15

=========================================================================================================================================

I have also added multiple time frame labels (label script used is the one created by Ricardo Santos)

These labels are color coded the same as the bars/candles, and they appear off to the right of your screen using every built in time increment from TradingView.

The purpose is to show you in real time, and on any chart resolution, what the current trend is on every individual time frame.

So using just one single chart you'll see your current resolutions candles, but also on the labels you'll see:

1 Minute

3 Minute

5 Minute

15 Minute

30 Minute

45 Minute

1 Hour

2 Hour

3 Hour

4 Hour

Daily

Weekly

Monthly

There is an input I added that allows you to adjust where your labels appear on the side of your screen as well!

=========================================================================================================================================

Now onto the volume spike portion of the indicator. This will plot a blue dot under each bar that has a spike in volume which meets your specified criteria.

I have 500% as the default setting.

What that means is that this indicator looks back and gets the 50 bar volume average and then applies dots where volume is 500% above average.

=========================================================================================================================================

Now finally, the reversal arrows. This is another simple to understand concept that I first read in John Carter's book "Mastering the Trade" that he calls "HOLP/LOHP".

I have added the ability to change the look back period you'd like the indicator to watch for highs and lows on.

What that stands for is 'High of Low Period' and 'Low of High Period', and it is used like this-

Whenever a bar makes a new high the indicator watches the low on that highest bar. Then when a bar afterwards makes a lower low then the one on the high bar,

a reversal arrow is given. Apply this same concept in the other direction in for the highs on the lowest bars.

=========================================================================================================================================

Now, I didn't want to make a "set" or have a bunch of different indicators out there that are all intended for the same package, so I took the time to put them together,

and if there's a part of it you don't care for they can easily be turned off in the settings.

Enjoy!

Delta Volume Columns [LucF]Displays delta volume columns using intrabar volume information. Each volume column is divided into three sections: buying, selling and neutral volume. Volume for each section is determined from the volume and price movement of each intrabar at a user-selected lower resolution.

Features include:

- Choice of color themes for either dark or light chart backgrounds

- Delta volume columns

- Volume Balance displayed as the difference between the MAs of buying and selling volume

- Display of divergences between a bar’s volume balance and the bar’s price movement (example: buying volume > selling volume but close < open). Divergences can be shown in 2 different color schemes (including green/red showing a tentative direction), on volume columns and/or on chart bars

- Display of bar by bar volume balance with highlighting of above average volume

- Display of the usual total volume MA

- Choice of the lower resolution used to retrieve intrabar information

- Alerts configurable on any combination of the markers, with control over long/short direction

- Choice of 3 different markers:

1. Double bumps: two consecutive bars where buying or selling volume is in the same direction and where volume > volume MA

2. Divergence confirmations: direction of the price bar following a price/volume balance divergence

3. Volume balance shifts: zero level crossings of the volume balance MA delta

The chart shows the two main modes of display:

- Top pane : shows the stacked volume columns with divergences in orange and the flattened volume balance MAs delta at the bottom of the volume columns. This volume balance is the same shown in the bottom pane. The top pane also shows the instant volume balance strip above the volume columns. The strip’s colors show which of the buying or selling volume was greater, and colors are brighter if the total volume was above the total volume MA.

- Bottom pane : shows the volume balance MAs delta with markers 1 and 2. Given that this graphic has no price momentum component, I find quite eerie how it often looks like a momentum-based signal.

The default 5 minute intrabar resolution is used in combination with the weekly chart, which is excessive.

This script uses a special characteristic of the security() function’s behavior when it is sent to a resolution lower than the chart’s resolution. Details are given in the script’s comments. This method has the advantage of working under more circumstances than some of the other loop-based methods, but it also has its limits.

IMPORTANT

This is what you need to know:

- The method used does not work on the realtime bar—only on historical bars. Consequently, the volume column shown on the realtime bar is a normal volume column plotted in green or red, following price movement. The column will only show delta volume information after it closes and becomes a historical bar.

- The indicator only works on some chart resolutions: 5, 10, 15 and 30 minutes, 1, 2, 4, 6, and 12 hours, 1 day, 1 week and 1 month. The script’s code can be modified to run on other resolutions, but chart resolutions must be divisible by the lower resolution used for intrabars.

- Intrabar resolutions can be selected from 1, 5, 15, 30, 45 minutes, 1, 2, 3, 4 hours, 1 day, 1 week and 1 month. The intrabar resolution must of course be smaller than the chart’s resolution.

- Contrary to my other indicators where alerts must be configured to trigger “Once Per Bar Close” in order to avoid false triggers (or repainting), all this indicator’s alerts are designed to trigger using previous bar information since the indicator’s calculations in the realtime bar are not exact. Markers are not plotted with a negative offset; they appear at the beginning of the realtime bar following confirmation of the marker’s condition on the previous bar. Alerts for this indicator should thus be configured to trigger “Once Per Bar” so they trigger at the beginning of the realtime bar. Note that the penalty is not that great, as it is simply the instant between the close of the previous realtime bar and the opening of the next. The advantage of using this technique is that the indicator does not repaint; a marker that appears at the beginning of the realtime bar will never disappear.

- The script only plots information that is reliable in the realtime bar, i.e., total volume and markers. All other plots are set to n/a to prevent misleading traders.

- When the difference between the chart’s resolution and the lower resolution is too important, volume columns will not calculate for all bars in the dataset.

On Delta Volume

Buying or selling volume are misnomers, as every unit of volume transacted is both bought and sold by 2 different traders. There is no such thing as “buy only” or “sell only” volume, but trader lingo is riddled with original fabulations.

Without access to order book information, traders work with the assumption that when price moves up during a bar, there was more buying pressure than selling pressure. The built-in volume indicator available on TradingView uses this logic to color the volume columns green or red. While this script’s numbers are more precise because it analyses a number of intrabars to calculate its information, it uses the exact same imperfect logic to calculate its buying/selling/neutral sections.

Until Pine scripts can have access to how much volume was transacted at the bid/ask prices, our so-called buying/selling volume information will always be a mere proxy.

Divergences

You may wonder how there can be divergences between buying/selling volume information and price movement. This will sometimes be due to the methodology’s shortcomings we have just discussed, but divergences may also occur in instances where because of order book structure, it takes less volume to increase the price of an asset than it takes to decrease it.

As usual, divergences are points of interest because they reveal imbalances, which may or may not become turning points. I do not share the overwhelming enthusiasm traders have for divergences. To your pattern-hungry brain, the orange bars this indicator shows on chart will—as divergences on other indicators do–appear to often indicate turnarounds. My opinion is that reality is generally quite sobering, as many who have tried building automated rules based on divergences will tell you. I do not have hard numbers on the lack of performance of divergences—only many failed attempts to make them perform, which a few experienced strategy modelers I know share with me. Please don’t try to read too much into them. While they look great on past data, I find they are often difficult to use in realtime to make bets with good odds.

Thanks to:

- A guy called Kuan who commented on a Backtest Rookies presentation of an intrabar delta volume indicator using a for loop. The heart of “my” indicator is code borrowed from Kuan; I just built a hopefully useful wrapper around it.

- @theheirophant, my partner in the exploration of the sometimes weird abysses of security() ’s behavior at lower resolutions.

Divergences for many indicators v2.0A gift from me to all.

This script is developed to find Divergences for many indicators. it analyses divergences and then draws line on the graph. red for negatif, lime for positive divergences.

Currently script checks divergence for RSI, MACD, MACD Histogram, Stochastic, CCI, Momentum, OBV, Diosc, VWMACD and CMF indicators. You can use some or all of these indicators to check divergences as you wish by choosing them on the menu. Also you can add/remove many other indicators to the script to check if there is divergence.

The script first calculates tops/bottoms by using higher time frame zig zag and then finds divergences.

Higher Time Frames are

if currend period 1 min => HTF = 5 mins

if currend period 3 mins => HTF = 15 mins

if currend period 5 mins => HTF = 15 mins

if currend period 15 mins => HTF = 1 hour

if currend period 30 mins => HTF = 1 hour

if currend period 45 mins => HTF = 1 hour

if currend period 1 hour => HTF = 4 hours

if currend period 2 hours => HTF = 4 hours

if currend period 3 hours => HTF = 4 hours

if currend period 4 hours => HTF = 1 day

if currend period 1 day => HTF = 1 week

if currend period 1 week => HTF = 1 week

future plan : script finds regular divergences, soon I will add hidden divergences and also I plan to add alert ;)

lsi (study about length and MTF) Here in this example I took lazy bear famous momentum squeeze indicator . the problem that there is lagging in the indicator so the buy and sell will be late . So instead the KC length that the original script had we put

int1=input(30)

int2=input(60)

lengthKC=isintraday and interval >= int1 ? int2/interval * 7 : isintraday and interval < 60 ? 60/interval * 24 * 7 : 7

this allow us to create a time and length related function to indicator and result in better output with no lagging

The second and most important thing is the ability to create indicator with time function as MTF without the security function that create repaint

all you need to do is to change int2 (to the time min of your choice ) and you can create an indicator with MTF function without the security function .And by this hopefully avoid the repainting issue

when you use this indicator change the setting of int1 and int 2 according to time frame that you use

lets say 15 min graph

make the int1 <15 min and the int2 at 15 min. if you want to see it as MTF just increase the int2 to the time set of your choice and play little with int1 to best setting

Mby_VolumeThis indicator added some options.

bases 15 SMA.

50SMA

100SMA

120SMA

Now you Can Check not only 15SMA Volume But also other period SMA.

지표의 옵션을 추가했습니다.

기본 15이동평균선.

50, 100, 120.

여러분들은 이제 15 볼륨 이평선 뿐만 아니라 다른 기간의 이평선 까지 확인 가능하실 겁니다.

감사합니다.

Simple TrenderOriginates from:

I was reading some Impulse Trading literature by A. Elder.. In it, someone named Kerry Lovvorn proposed "An End of Day Trend Following System" for someone lazy.

Originally it is just price closing above an 8 ema (low) for long. Exit when price closes below an 8 ema (low). The opposite for a short position.

Conditions: Buy when price closed below ema (low) for two bars or more, then closes above. Opposite for a short position. I do not follow this condition. Though it may help with whipsaw.

My condition is when price closes above the 26 ema (low) (works the best for me) I place orders above the initial crossing bars high. Opposite for lows.

I look for stocks that are low in price to go long on. I want the run from 2's to 15's

I look for stocks that are mid-teens/20's in price to go short on. I want the run from 20's to 2's

I look for stock with news and earnings that are already running (up or down) to play the pullback.

These conditions can easily be scanned for on thinkorswim

From first glance, the system looks like CMsling shotsystem. Although, I plagiarized some parts of the codes, because I am inept when it comes to that shit, it differs as it is not a moving average crossover system.

It is a price crossing over concept. A moving average VWAP is used for best entries on pullbacks.

Purpose:

--To catch the majority of a trend/wave/run.

--To identify pullback areas to go long or short while in midst of trend. To catch pullbacks off news and earning runners.

--To catch the initial start of trend with clear rules to enter

--Clear rules to exit

Issues

--possibilities of getting ninja sliced the fuck up. Can be mitigated by entering stocks with decent average volume. And also only going long above 200 ema and short below it. ADX won't work, at the initial start of the trend it will show not trending. Can look at blow off volume at the bottom followed by increase in buying for long and vice versa for short.

--Can give some huge gains away through gap ups or gap downs from news or earnings during trend. However, can get huge gain on gaps from news or earning. Nature of the game.

--Need some brass balls and a supply of pepto to stomach through some of the pullbacks. Gut wrenching seeing big gains dwindle. But they all even out at the end, you hope. (see NBEV and IGC, and CRON and others. shit don't go in straight lines, homie)

Pros

--It's simple and easy. Overall, you profit

--works with any security

Cons

--It can be stressful.

--does not work well on lower time frames. Do not recommend going below 15 minutes

--Possibility of working on 5 minutes with a time frame breakout strategy (15,30 min).

Couple it with LazyBear "Weis Wave Volume" indicator. Works well for pullback entries.

Enjoy. Ride some waves.

Physics MACD double// Physics MACD double 12, 26 and 5, 15

// with rsi and cci rise green on bottom

// with macd 15 rising above 0 with macd 26 below 0 green on top

// with macd 15 below 0 and macd 26 above 0 red on top

// CCI low and increasing lime bottom

// low and high volume change red green bottom circle

// use with Physics Bollinger Bands

90009If( MDI(14)>40 AND ADX(14)>40 AND PDI(14)<15 AND RSI(14)<30,1,0)

;If( MDI(14)<15 AND ADX(14)<15 AND PDI(14)>40 AND RSI(14)>70,-1,0)

VWAP forex Yesterday Hi/Low update fix This script is an updte fix of an earlier script that stopped functioning when TradingView updated Pine script. This script plots Forex (24 hour session) VWAP, yesterday's high, low, open and close (HLOC),

the day before's HLOC -

Also plots higher timeframe 20 emas

1 minute 5, 15, 60 period 20 ema

5 minute 15, 60 period 20 ema

15 minute 60, 120 , 240 period 20 ema

60 minute 120, 240 period 20 ema

120 minute 240, D period 20 ema

240 minute D period 20 ema

Also signals inside bars (high is less than or equal to the previous bar's high and the low is greater than or equal to the previous low) the : true inside bars have a maroon triangle below the bar as well as a ">" above the bar.

If subsequest bars are inside the last bar before the last true inside bar they also are marked with an ">"

This is probably a slight variation from the way Leaf_West plots the inside bars.

It appears that he marks all bars that are inside the original bar until one a bar has a high or low

outside the original bar. But I would need to see an example on his charts.

The Time Session Glitch and the Fix FX_IDC, COINBASE and BITSTAMP:

The script will correctly default to 1700 hrs to 1700hrs EDT/EST session for FXCM.

Strangely some securities appear to erroneously start their session at 1200 hrs ie. My guess is that they are somehow tied to GMT+0 instead of New York time (GMT+5). See this for yourself by selecting EURUSD using the FXCM exchange (FX:EURUSD) and then EURUSD from the IDC exchange (FX_IDC:EURUSD). The FX-IDC session opening range starts 5 hours before it actually should at 1700 hrs EDT/EST. To correct for this I have implemented an automatic fix (default) and a user selected "5 hour time shift adjust. ment needed on some securities".

There is also a 4 hour time shift button which might be necessary when New York reverts from Eastern Standard Time to Eastern Daylight Time (1 hour difference) in March (and then back again in November). In the default auto adjust mode you will need to select the 1 hour time shift. That is if this glitch still exists at that time.

I have looked at other scripts, other than my own and where the script is available, that need to use information about the opening bar and all have the same time shift issue

COINBASE and BITSTAMP open at 0000 hours GMT. Since I use lines instead of circles or crosses I had to make a small adjustment to plot the lines correctly.

If it needs work let me know.

Jayy

VWAP forex Yesterday Hi/Low switchThis script plots VWAP, yesterday's high, low, open and close (HLOC), the day before's HLOC -

Also plots higher timeframe 20 emas including:

1 minute 5, 15, 60 period 20 ema

5 minute 15, 60 period 20 ema

15 minute 60, 120 , 240 period 20 ema

60 minute 120, 240 period 20 ema

120 minute 240, D period 20 ema

240 minute D period 20 ema

Also signals inside bars (high is less than or equal to the previous

bar's high and the low is greater than or equal to the previous low) the : true inside bars have a maroon triangle below the bar as well as a ">" above the bar.

If subsequent bars are inside the last bar before the last true inside bar they also are marked with an ">"

If you have suggestions let me know.

Jayy