Bias + VWAP Pullback — v4 (PA + BOS/CHOCH)Simple idea: I identify the trend (bias) from the larger timeframe, and only trade pullbacks to the VWAP/EMA during liquidity (London/New York). When the trend is clear, gold moves strongly, and its pullbacks to the balance lines provide clear opportunities.

Timeframe and Sessions (Cairo Time)

Analysis: H1 to determine the trend.

Implementation: 5m (or 1m if professional).

Trading window:

London Opening: 10:00–12:30

New York Opening: 16:30–19:00

(avoid the rest of the day unless there is exceptional traffic).

Direction determination (BIAS)

On H1:

If the price is above the 200 EMA and the daily VWAP is bullish and the price is above it → uptrend (long-only).

If the price is below the 200 EMA and the daily VWAP is bearish and the price is below it → bearish trend (short-only).

Determine your levels: yesterday's high/low (PDH/PDL) + approximate Asia range (03:00–09:30).

Entry Rules (Setup A: Trend Continuation)

Asia range breakout towards Bias during liquidity window.

Wait for a withdrawal to:

Daily VWAP, or

EMA50 on 5m frame (best if both cross).

Confirmation: Confirmation low/high on 5m (HL buy/LH sell) + clear impulse candle (Body is greater than average of last 10 candles).

Entry:

Buy: When the price returns above VWAP/EMA50 with a confirmation candle close.

Sell: The exact opposite.

Stop Loss (SL): Below/above the last confirmation low/high or ATR(14, 5m) x 1.5 (largest).

Objectives:

TP1 = 1R (Close 50% and move the rest Break-even).

TP2 = 2.5R to 3R or at an important HTF level (PDH/PDL/Bid/Demand Zone).

Entry Rules (Setup B: Reversion to VWAP – “Mean Reversion”)

Use with extreme caution, once daily maximum:

Price deviation from VWAP by more than ~1.5 x ATR(14, 5m) with rejection candles appearing near PDH/PDL.

Reverse entry towards the return of VWAP.

SL small behind rejection top/bottom.

Main target: VWAP. (Don't get greedy — this scenario is for extended periods only.)

News Filtering and Risk Management

Avoid trading 15–30 minutes before/after strong US news (CPI, NFP, FOMC).

Maximum daily loss: 1.5–2% of account balance.

Risk per trade: 0.25–0.5% (if you are learning) or 0.5–1% (if you are experienced).

Do not exceed two consecutive losing trades per day.

Don't chase the market after the opportunity has passed — wait for the next pullback.

Smart Deal Management

After TP1: Move stop to entry point + trail the rest with EMA20 on 5m or ATR Trailing = ATR(14)×1.0.

If the price touches a strong daily level (PDH/PDL) and fails to break, consider taking additional profit.

If VWAP starts to flatten and breaks against the trend on H1, stop trading for the day.

Quick Checklist (Before Entry)

H1 trend is clear and consistent with 200EMA + VWAP.

Penetrating the Asia range towards Bias.

Clean pull to VWAP/EMA50 on 5m.

Confirmation candle and real push.

SL is logical (behind swing/ATR×1.5) and R :R ≥ 1:2.

No red news coming soon.

Example of "ready-made" settings

EMA: 20, 50, 200 on 5m, 200 only on H1.

VWAP: Daily (reset daily).

ATR: 14 on 5m.

Levels: PDH/PDL + Asia Band (03:00–09:30 Cairo).

Gold Notes

Gold is fast and sharp at the open; don't get in early — wait for the draw.

Fakeouts are common before news: it is best to call with the trend after the price returns above/below VWAP.

Don't expect 80% consistent wins every day — the advantage comes from discipline, filtering out bad days, and only withdrawing when you're on the right track.

تعتبر شركة الماسة الألمانية أحد المؤسسات العاملة بالمملكة العربية السعودية ولها تاريخ طويل من الخدمات الكثيرة والمتنوعة التى مازالت تقدمها للكثير من العملاء داخل جميع مدن وأحياء المملكة حيث نقدم أفضل ما لدينا من خلال مجموعة الشركات التالية والتي من خلالها ستتلقي كل ما تحتاج إلية في كل المجال المختلفة فنحن نعمل منذ عام 2015 ولنا سابقات اعمال فى مختلف المجالات الحيوية التى نخدم من خلالها عملائنا ونوفر لهم أرخص الأسعار وبأعلى جودة من الممكن توفرها فى المجالات التالية :-

خدمات تنظيف المنازل والفلل والشقق

خدمات عزل الخزانات تنظيف غسيل صيانة اصلاح

خدمات جلي البلاط والرخام والسيراميك

خدمات نقل العفش عمالة فلبينية مدربة

خدمات مكافحة الحشرات بجدة

كل هذة الخدمات وأكثر نوفرها لكل المتعاقدين بأفضل الطرق مع توفير خطط وبرامج متنوعة لأتمام العمل المسنود إلينا بأفضل وأحدث الطرق الحديثة والعصرية سواء فى شركات النظافة بجدة ومكة المكرمة أو شركات نقل العفش بجدة عمالة فلبينية وباقى الخدمات مثل جلي وتلميع الرخام بمكة وجدة ولا ننسي شركة مكافحة حشرات بجدة التى ساعدت آلاف المواطنين على تنظيف منازلهم من الحشرات بأفضل مبيدات حشرية.

In den Scripts nach "央行:下调个人住房公积金贷款利率0.25个百分点" suchen

TRI - Multi-Timeframe BIASTRI - MULTI-TIMEFRAME BIAS INDICATOR

DESCRIPTION:

Advanced multi-timeframe bias indicator that analyzes market sentiment across

5 different timeframes (15m, 1h, 4h, 1d, 1w) using adaptive technical analysis.

Provides clear directional bias signals to help determine market momentum.

KEY FEATURES:

ADAPTIVE PARAMETERS: Uses different EMA lengths and weights for each timeframe

EMA TREND ANALYSIS: Fast/slow EMA crossovers with slope analysis for momentum

RSI MOMENTUM: Adaptive overbought/oversold levels based on timeframe

ADX STRENGTH: Directional movement confirmation with DI+/DI- analysis

COMPOSITE SCORING: Weighted combination of trend, momentum, and strength

TIMEFRAME ANALYSIS:

15m: EMA9/21 + High momentum weight (45%) - Ultra-responsive for scalping

1h: EMA21/50 + Medium momentum weight (35%) - Balanced for day trading

4h: EMA50/200 + Lower momentum weight (25%) - Swing trading focus

1d: EMA50/200 + Trend focused (55%) - Position trading signals

1w: EMA50/200 + Maximum trend weight (60%) - Long-term bias

BIAS SIGNALS:

STRONG BULLISH/BEARISH: Score ≥ 0.5 - Very strong directional momentum

BULLISH/BEARISH: Score ≥ 0.25 - Clear directional signals

WEAK BULLISH/BEARISH: Score ≥ 0.1 - Mild directional bias

NEUTRAL: Score < 0.1 - No clear directional preference

ALERTS:

Major Bullish/Bearish: When 4H and 1D timeframes align

High confidence signals for strategic decision making

USAGE:

Higher timeframes (1d, 1w) show primary market direction

Lower timeframes (15m, 1h) provide entry timing

Look for alignment across multiple timeframes for stronger signals

Use confidence levels to assess signal reliability

TECHNICAL COMPONENTS:

Exponential Moving Averages (EMA) for responsive trend detection

Relative Strength Index (RSI) for momentum analysis

Average Directional Index (ADX) with DI+/DI- for trend strength

Volume ratio confirmation for signal validation

Adaptive thresholds optimized for each timeframe's characteristics

Gann Fan Strategy [KedarArc Quant]Description

A single-concept, rule-based strategy that trades around a programmatic Gann Fan.

It anchors to a swing (or a manual point), builds 1×1 and related fan lines numerically, and triggers entries when price interacts with the 1×1 (breakout or bounce). Management is done entirely with the fan structure (next/previous line) plus optional ATR trailing.

What TV indicators are used

* Pivots: `ta.pivothigh/ta.pivotlow` to confirm swing highs/lows for anchor selection.

* ATR: `ta.atr` only to scale the 1×1 slope (optional) and for an optional trailing stop.

* EMA: `ta.ema` as a trend filter (e.g., only long above the EMA, short below).

No RSI/MACD/Stoch/Heikin/etc. The logic is one coherent framework: Gann price–time geometry, with ATR as a scale and EMA as a risk filter.

How it works

1. Anchor

* Auto: chooses the most recent *confirmed* pivot (you control Left/Right).

* Manual: set a price and bar index and the fan will hold that point (no re-anchoring).

* Optional Re-anchor when a newer pivot confirms.

2. 1×1 Slope (numeric, not cosmetic)

* ATR mode: `1×1 = ATR(Length) × Multiplier` (adapts to volatility).

* Fixed mode: `ticks per bar` (constant slope).

Because slope is numeric, it doesn’t change with chart zoom, unlike the drawing tool.

3. Fan Lines

Builds classic ratios around the 1×1: 1/8, 1/4, 1/3, 1/2, 1/1, 2/1, 3/1, 4/1, 8/1.

4. Signals

* Breakout: cross of price over/under the 1×1 in the EMA-aligned direction.

* Bounce (optional): touch + reversal across the 1×1 to reduce whipsaw.

5. Exits & Risk

* Take-profit at the next fan line; Stop at the previous fan line.

* If a level is missing (right after re-anchor), a fallback Risk-Reward (RR) is used.

* Optional ATR trailing stop.

Why this is unique

* True numeric fan: The 1×1 slope is calculated from ATR or fixed ticks—not from screen geometry—so it is scale-invariant and reproducible across users/timeframes.

* Deterministic anchor logic: Uses confirmed pivots (with your L/R settings). No look-ahead; anchors update only when the right bars complete.

* Fan-native trade management: Both entries and exits come from the fan structure itself (with a minimal ATR/EMA assist), keeping the method pure.

* Two entry archetypes: Breakout for momentum days; Bounce for range days—switchable without changing the core model.

* Manual mode: Lock a session’s bias by anchoring to a chosen swing (e.g., day’s first major low/high) and keep the fan constant all day.

Inputs (quick guide)

* Auto Anchor (Left/Right): pivot sensitivity. Higher values = fewer, stronger anchors.

* Re-anchor: refresh to newer pivots as they confirm.

* Manual Anchor Price / Bar Index: fixes the fan (turn Auto off).

* Scale 1×1 by ATR: on = adaptive; off = use ticks per bar.

* ATR Length / ATR Multiplier: controls adaptive slope; start around 14 / 0.25–0.35.

* Ticks per bar: exact fixed slope (match a hand-drawn fan by computing slope ÷ mintick).

* EMA Trend Filter: e.g., 50–100; trades only in EMA direction.

* Use Bounce: require touch + reverse across 1×1 (helps in chop).

* TP/SL at fan lines; Fallback RR for missing levels; ATR Trailing Stop optional.

* Transparency/Plot EMA: visual preferences.

Tips

* Range days: larger pivots (L/R 8–12), Bounce ON, ATR Multiplier \~0.30–0.40, EMA 100.

* Trend days: L/R 5–6, Breakout, Multiplier \~0.20–0.30, EMA 50, ATR trail 1.0–1.5.

* Match the TV Gann Fan drawing: turn ATR scale OFF, set ticks per bar = `(Δprice between anchor and 1×1 target) / (bars) / mintick`.

Repainting & testing notes

* Pivots require Right bars to confirm; anchors are set after confirmation (no look-ahead).

* Signals use the current bar close with TradingView strategy mechanics; real-time vs. bar-close can differ slightly, as with any strategy.

* Re-anchoring legitimately moves the structure when new pivots confirm—by design.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Deadband Hysteresis Filter [BackQuant]Deadband Hysteresis Filter

What this is

This tool builds a “debounced” price baseline that ignores small fluctuations and only reacts when price meaningfully departs from its recent path. It uses a deadband to define how much deviation matters and a hysteresis scheme to avoid rapid flip-flops around the decision boundary. The baseline’s slope provides a simple trend cue, used to color candles and to trigger up and down alerts.

Why deadband and hysteresis help

They filter micro noise so the baseline does not react to every tiny tick.

They stabilize state changes. Hysteresis means the rule to start moving is stricter than the rule to keep holding, which reduces whipsaw.

They produce a stepped, readable path that advances during sustained moves and stays flat during chop.

How it works (conceptual)

At each bar the script maintains a running baseline dbhf and compares it to the input price p .

Compute a base threshold baseTau using the selected mode (ATR, Percent, Ticks, or Points).

Build an enter band tauEnter = baseTau × Enter Mult and an exit band tauExit = baseTau × Exit Mult where typically Exit Mult < Enter Mult .

Let diff = p − dbhf .

If diff > +tauEnter , raise the baseline by response × (diff − tauEnter) .

If diff < −tauEnter , lower the baseline by response × (diff + tauEnter) .

Otherwise, hold the prior value.

Trend state is derived from slope: dbhf > dbhf → up trend, dbhf < dbhf → down trend.

Inputs and what they control

Threshold mode

ATR — baseTau = ATR(atrLen) × atrMult . Adapts to volatility. Useful when regimes change.

Percent — baseTau = |price| × pctThresh% . Scale-free across symbols of different prices.

Ticks — baseTau = syminfo.mintick × tickThresh . Good for futures where tick size matters.

Points — baseTau = ptsThresh . Fixed distance in price units.

Band multipliers and response

Enter Mult — outer band. Price must travel at least this far from the baseline before an update occurs. Larger values reject more noise but increase lag.

Exit Mult — inner band for hysteresis. Keep this smaller than Enter Mult to create a hold zone that resists small re-entries.

Response — step size when outside the enter band. Higher response tracks faster; lower response is smoother.

UI settings

Show Filtered Price — plots the baseline on price.

Paint candles — colors bars by the filtered slope using your long/short colors.

How it can be used

Trend qualifier — take entries only in the direction of the baseline slope and skip trades against it.

Debounced crossovers — use the baseline as a stabilized surrogate for price in moving-average or channel crossover rules.

Trailing logic — trail stops a small distance beyond the baseline so small pullbacks do not eject the trade.

Session aware filtering — widen Enter Mult or switch to ATR mode for volatile sessions; tighten in quiet sessions.

Parameter interactions and tuning

Enter Mult vs Response — both govern sensitivity. If you see too many flips, increase Enter Mult or reduce Response. If turns feel late, do the opposite.

Exit Mult — widening the gap between Enter and Exit expands the hold zone and reduces oscillation around the threshold.

Mode choice — ATR adapts automatically; Percent keeps behavior consistent across instruments; Ticks or Points are useful when you think in fixed increments.

Timeframe coupling — on higher timeframes you can often lower Enter Mult or raise Response because raw noise is already reduced.

Concrete starter recipes

General purpose — ATR mode, atrLen=14 , atrMult=1.0–1.5 , Enter=1.0 , Exit=0.5 , Response=0.20 . Balanced noise rejection and lag.

Choppy range filter — ATR mode, increase atrMult to 2.0, keep Response≈0.15 . Stronger suppression of micro-moves.

Fast intraday — Percent mode, pctThresh=0.1–0.3 , Enter=1.0 , Exit=0.4–0.6 , Response=0.30–0.40 . Quicker turns for scalping.

Futures ticks — Ticks mode, set tickThresh to a few spreads beyond typical noise; start with Enter=1.0 , Exit=0.5 , Response=0.25 .

Strengths

Clear, explainable logic with an explicit noise budget.

Multiple threshold modes so the same tool fits equities, futures, and crypto.

Built-in hysteresis that reduces flip-flop near the boundary.

Slope-based coloring and alerts that make state changes obvious in real time.

Limitations and notes

All filters add lag. Larger thresholds and smaller response trade faster reaction for fewer false turns.

Fixed Points or Ticks can under- or over-filter when volatility regime shifts. ATR adapts, but will also expand bands during spikes.

On extremely choppy symbols, even a well tuned band will step frequently. Widen Enter Mult or reduce Response if needed.

This is a chart study. It does not include commissions, slippage, funding, or gap risks.

Alerts

DBHF Up Slope — baseline turns from down to up on the latest bar.

DBHF Down Slope — baseline turns from up to down on the latest bar.

Implementation details worth knowing

Initialization sets the baseline to the first observed price to avoid a cold-start jump.

Slope is evaluated bar-to-bar. The up and down alerts check for a change of slope rather than raw price crossings.

Candle colors and the baseline plot share the same long/short palette with transparency applied to the line.

Practical workflow

Pick a mode that matches how you think about distance. ATR for volatility aware, Percent for scale-free, Ticks or Points for fixed increments.

Tune Enter Mult until the number of flips feels appropriate for your timeframe.

Set Exit Mult clearly below Enter Mult to create a real hold zone.

Adjust Response last to control “how fast” the baseline chases price once it decides to move.

Final thoughts

Deadband plus hysteresis gives you a principled way to “only care when it matters.” With a sensible threshold and response, the filter yields a stable, low-chop trend cue you can use directly for bias or plug into your own entries, exits, and risk rules.

Market Outlook Score (MOS)Overview

The "Market Outlook Score (MOS)" is a custom technical indicator designed for TradingView, written in Pine Script version 6. It provides a quantitative assessment of market conditions by aggregating multiple factors, including trend strength across different timeframes, directional movement (via ADX), momentum (via RSI changes), volume dynamics, and volatility stability (via ATR). The MOS is calculated as a weighted score that ranges typically between -1 and +1 (though it can exceed these bounds in extreme conditions), where positive values suggest bullish (long) opportunities, negative values indicate bearish (short) setups, and values near zero imply neutral or indecisive markets.

This indicator is particularly useful for traders seeking a holistic "outlook" score to gauge potential entry points or market bias. It overlays on a separate pane (non-overlay mode) and visualizes the score through horizontal threshold lines and dynamic labels showing the numeric MOS value along with a simple trading decision ("Long", "Short", or "Neutral"). The script avoids using the plot function for compatibility reasons (e.g., potential TradingView bugs) and instead relies on hline for static lines and label.new for per-bar annotations.

Key features:

Multi-Timeframe Analysis: Incorporates slope data from 5-minute, 15-minute, and 30-minute charts to capture short-term trends.

Trend and Strength Integration: Uses ADX to weight trend bias, ensuring stronger signals in trending markets.

Momentum and Volume: Includes RSI momentum impulses and volume deviations for added confirmation.

Volatility Adjustment: Factors in ATR changes to assess market stability.

Customizable Inputs: Allows users to tweak periods for lookback, ADX, and ATR.

Decision Labels: Automatically classifies the MOS into actionable categories with visual labels.

This indicator is best suited for intraday or swing trading on volatile assets like stocks, forex, or cryptocurrencies. It does not generate buy/sell signals directly but can be combined with other tools (e.g., moving averages or oscillators) for comprehensive strategies.

Inputs

The script provides three user-configurable inputs via TradingView's input panel:

Lookback Period (lookback):

Type: Integer

Default: 20

Range: Minimum 10, Maximum 50

Purpose: Defines the number of bars used in slope calculations for trend analysis. A shorter lookback makes the indicator more sensitive to recent price action, while a longer one smooths out noise for longer-term trends.

ADX Period (adxPeriod):

Type: Integer

Default: 14

Range: Minimum 5, Maximum 30

Purpose: Sets the smoothing period for the Average Directional Index (ADX) and its components (DI+ and DI-). Standard value is 14, but shorter periods increase responsiveness, and longer ones reduce false signals.

ATR Period (atrPeriod):

Type: Integer

Default: 14

Range: Minimum 5, Maximum 30

Purpose: Determines the period for the Average True Range (ATR) calculation, which measures volatility. Adjust this to match your trading timeframe—shorter for scalping, longer for positional trading.

These inputs allow customization without editing the code, making the indicator adaptable to different market conditions or user preferences.

Core Calculations

The MOS is computed through a series of steps, blending trend, momentum, volume, and volatility metrics. Here's a breakdown:

Multi-Timeframe Slopes:

The script fetches data from higher timeframes (5m, 15m, 30m) using request.security.

Slope calculation: For each timeframe, it computes the linear regression slope of price over the lookback period using the formula:

textslope = correlation(close, bar_index, lookback) * stdev(close, lookback) / stdev(bar_index, lookback)

This measures the rate of price change, where positive slopes indicate uptrends and negative slopes indicate downtrends.

Variables: slope5m, slope15m, slope30m.

ATR (Average True Range):

Calculated using ta.atr(atrPeriod).

Represents average volatility over the specified period. Used later to derive volatility stability.

ADX (Average Directional Index):

A detailed, manual implementation (not using built-in ta.adx for customization):

Computes upward movement (upMove = high - high ) and downward movement (downMove = low - low).

Derives +DM (Plus Directional Movement) and -DM (Minus Directional Movement) by filtering non-relevant moves.

Smooths true range (trur = ta.rma(ta.tr(true), adxPeriod)).

Calculates +DI and -DI: plusDI = 100 * ta.rma(plusDM, adxPeriod) / trur, similarly for minusDI.

DX: dx = 100 * abs(plusDI - minusDI) / max(plusDI + minusDI, 0.0001).

ADX: adx = ta.rma(dx, adxPeriod).

ADX values above 25 typically indicate strong trends; here, it's normalized (divided by 50) to influence the trend bias.

Volume Delta (5m Timeframe):

Fetches 5m volume: volume_5m = request.security(syminfo.tickerid, "5", volume, lookahead=barmerge.lookahead_on).

Computes a 12-period SMA of volume: avgVolume = ta.sma(volume_5m, 12).

Delta: (volume_5m - avgVolume) / avgVolume (or 0 if avgVolume is zero).

This measures relative volume spikes, where positive deltas suggest increased interest (bullish) and negative suggest waning activity (bearish).

MOS Components and Final Calculation:

Trend Bias: Average of the three slopes, normalized by close price and scaled by 100, then weighted by ADX influence: (slope5m + slope15m + slope30m) / 3 / close * 100 * (adx / 50).

Emphasizes trends in strong ADX conditions.

Momentum Impulse: Change in 5m RSI(14) over 1 bar, divided by 50: ta.change(request.security(syminfo.tickerid, "5", ta.rsi(close, 14), lookahead=barmerge.lookahead_on), 1) / 50.

Captures short-term momentum shifts.

Volatility Clarity: 1 - ta.change(atr, 1) / max(atr, 0.0001).

Measures ATR stability; values near 1 indicate low volatility changes (clearer trends), while lower values suggest erratic markets.

MOS Formula: Weighted average:

textmos = (0.35 * trendBias + 0.25 * momentumImpulse + 0.2 * volumeDelta + 0.2 * volatilityClarity)

Weights prioritize trend (35%) and momentum (25%), with volume and volatility at 20% each. These can be adjusted in code for experimentation.

Trading Decision:

A variable mosDecision starts as "Neutral".

If mos > 0.15, set to "Long".

If mos < -0.15, set to "Short".

Thresholds (0.15 and -0.15) are hardcoded but can be modified.

Visualization and Outputs

Threshold Lines (using hline):

Long Threshold: Horizontal dashed green line at +0.15.

Short Threshold: Horizontal dashed red line at -0.15.

Neutral Line: Horizontal dashed gray line at 0.

These provide visual reference points for MOS interpretation.

Dynamic Labels (using label.new):

Placed at each bar's index and MOS value.

Text: Formatted MOS value (e.g., "0.2345") followed by a newline and the decision (e.g., "Long").

Style: Downward-pointing label with gray background and white text for readability.

This replaces a traditional plot line, showing exact values and decisions per bar without cluttering the chart.

The indicator appears in a separate pane below the main price chart, making it easy to monitor alongside price action.

Usage Instructions

Adding to TradingView:

Copy the script into TradingView's Pine Script editor.

Save and add to your chart via the "Indicators" menu.

Select a symbol and timeframe (e.g., 1-minute for intraday).

Interpretation:

Long Signal: MOS > 0.15 – Consider bullish positions if supported by other indicators.

Short Signal: MOS < -0.15 – Potential bearish setups.

Neutral: Between -0.15 and 0.15 – Avoid trades or wait for confirmation.

Watch for MOS crossings of thresholds for momentum shifts.

Combine with price patterns, support/resistance, or volume for better accuracy.

Limitations and Considerations:

Lookahead Bias: Uses barmerge.lookahead_on for multi-timeframe data, which may introduce minor forward-looking bias in backtesting (use with caution).

No Alerts Built-In: Add custom alerts via TradingView's alert system based on MOS conditions.

Performance: Tested for compatibility; may require adjustments for illiquid assets or extreme volatility.

Backtesting: Use TradingView's strategy tester to evaluate historical performance, but remember past results don't guarantee future outcomes.

Customization: Edit weights in the MOS formula or thresholds to fit your strategy.

This indicator distills complex market data into a single score, aiding decision-making while encouraging users to verify signals with additional analysis. If you need modifications, such as restoring plot functionality or adding features, provide details for further refinement.

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

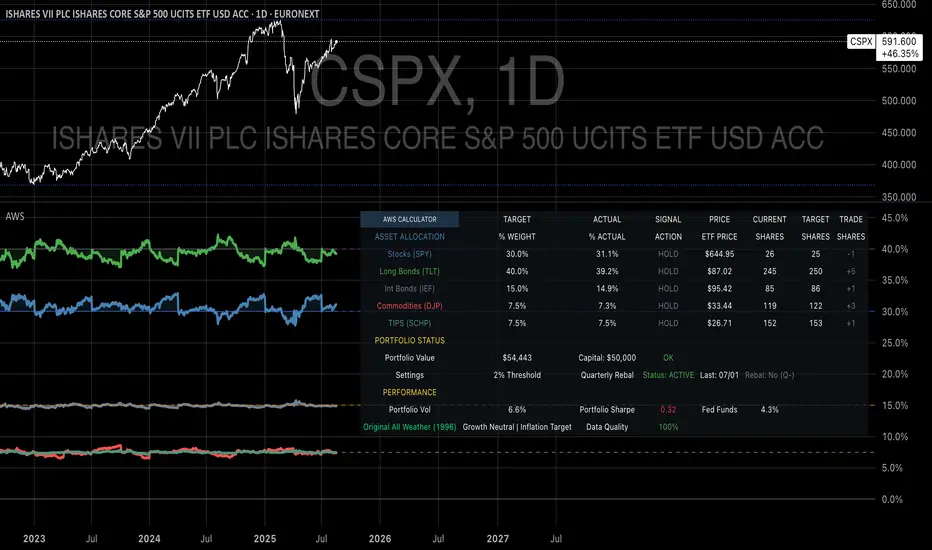

Ray Dalio's All Weather Strategy - Portfolio CalculatorTHE ALL WEATHER STRATEGY INDICATOR: A GUIDE TO RAY DALIO'S LEGENDARY PORTFOLIO APPROACH

Introduction: The Genesis of Financial Resilience

In the sprawling corridors of Bridgewater Associates, the world's largest hedge fund managing over 150 billion dollars in assets, Ray Dalio conceived what would become one of the most influential investment strategies of the modern era. The All Weather Strategy, born from decades of market observation and rigorous backtesting, represents a paradigm shift from traditional portfolio construction methods that have dominated Wall Street since Harry Markowitz's seminal work on Modern Portfolio Theory in 1952.

Unlike conventional approaches that chase returns through market timing or stock picking, the All Weather Strategy embraces a fundamental truth that has humbled countless investors throughout history: nobody can consistently predict the future direction of markets. Instead of fighting this uncertainty, Dalio's approach harnesses it, creating a portfolio designed to perform reasonably well across all economic environments, hence the evocative name "All Weather."

The strategy emerged from Bridgewater's extensive research into economic cycles and asset class behavior, culminating in what Dalio describes as "the Holy Grail of investing" in his bestselling book "Principles" (Dalio, 2017). This Holy Grail isn't about achieving spectacular returns, but rather about achieving consistent, risk-adjusted returns that compound steadily over time, much like the tortoise defeating the hare in Aesop's timeless fable.

HISTORICAL DEVELOPMENT AND EVOLUTION

The All Weather Strategy's origins trace back to the tumultuous economic periods of the 1970s and 1980s, when traditional portfolio construction methods proved inadequate for navigating simultaneous inflation and recession. Raymond Thomas Dalio, born in 1949 in Queens, New York, founded Bridgewater Associates from his Manhattan apartment in 1975, initially focusing on currency and fixed-income consulting for corporate clients.

Dalio's early experiences during the 1970s stagflation period profoundly shaped his investment philosophy. Unlike many of his contemporaries who viewed inflation and deflation as opposing forces, Dalio recognized that both conditions could coexist with either economic growth or contraction, creating four distinct economic environments rather than the traditional two-factor models that dominated academic finance.

The conceptual breakthrough came in the late 1980s when Dalio began systematically analyzing asset class performance across different economic regimes. Working with a small team of researchers, Bridgewater developed sophisticated models that decomposed economic conditions into growth and inflation components, then mapped historical asset class returns against these regimes. This research revealed that traditional portfolio construction, heavily weighted toward stocks and bonds, left investors vulnerable to specific economic scenarios.

The formal All Weather Strategy emerged in 1996 when Bridgewater was approached by a wealthy family seeking a portfolio that could protect their wealth across various economic conditions without requiring active management or market timing. Unlike Bridgewater's flagship Pure Alpha fund, which relied on active trading and leverage, the All Weather approach needed to be completely passive and unleveraged while still providing adequate diversification.

Dalio and his team spent months developing and testing various allocation schemes, ultimately settling on the 30/40/15/7.5/7.5 framework that balances risk contributions rather than dollar amounts. This approach was revolutionary because it focused on risk budgeting—ensuring that no single asset class dominated the portfolio's risk profile—rather than the traditional approach of equal dollar allocations or market-cap weighting.

The strategy's first institutional implementation began in 1996 with a family office client, followed by gradual expansion to other wealthy families and eventually institutional investors. By 2005, Bridgewater was managing over $15 billion in All Weather assets, making it one of the largest systematic strategy implementations in institutional investing.

The 2008 financial crisis provided the ultimate test of the All Weather methodology. While the S&P 500 declined by 37% and many hedge funds suffered double-digit losses, the All Weather strategy generated positive returns, validating Dalio's risk-balancing approach. This performance during extreme market stress attracted significant institutional attention, leading to rapid asset growth in subsequent years.

The strategy's theoretical foundations evolved throughout the 2000s as Bridgewater's research team, led by co-chief investment officers Greg Jensen and Bob Prince, refined the economic framework and incorporated insights from behavioral economics and complexity theory. Their research, published in numerous institutional white papers, demonstrated that traditional portfolio optimization methods consistently underperformed simpler risk-balanced approaches across various time periods and market conditions.

Academic validation came through partnerships with leading business schools and collaboration with prominent economists. The strategy's risk parity principles influenced an entire generation of institutional investors, leading to the creation of numerous risk parity funds managing hundreds of billions in aggregate assets.

In recent years, the democratization of sophisticated financial tools has made All Weather-style investing accessible to individual investors through ETFs and systematic platforms. The availability of high-quality, low-cost ETFs covering each required asset class has eliminated many of the barriers that previously limited sophisticated portfolio construction to institutional investors.

The development of advanced portfolio management software and platforms like TradingView has further democratized access to institutional-quality analytics and implementation tools. The All Weather Strategy Indicator represents the culmination of this trend, providing individual investors with capabilities that previously required teams of portfolio managers and risk analysts.

Understanding the Four Economic Seasons

The All Weather Strategy's theoretical foundation rests on Dalio's observation that all economic environments can be characterized by two primary variables: economic growth and inflation. These variables create four distinct "economic seasons," each favoring different asset classes. Rising growth benefits stocks and commodities, while falling growth favors bonds. Rising inflation helps commodities and inflation-protected securities, while falling inflation benefits nominal bonds and stocks.

This framework, detailed extensively in Bridgewater's research papers from the 1990s, suggests that by holding assets that perform well in each economic season, an investor can create a portfolio that remains resilient regardless of which season unfolds. The elegance lies not in predicting which season will occur, but in being prepared for all of them simultaneously.

Academic research supports this multi-environment approach. Ang and Bekaert (2002) demonstrated that regime changes in economic conditions significantly impact asset returns, while Fama and French (2004) showed that different asset classes exhibit varying sensitivities to economic factors. The All Weather Strategy essentially operationalizes these academic insights into a practical investment framework.

The Original All Weather Allocation: Simplicity Masquerading as Sophistication

The core All Weather portfolio, as implemented by Bridgewater for institutional clients and later adapted for retail investors, maintains a deceptively simple static allocation: 30% stocks, 40% long-term bonds, 15% intermediate-term bonds, 7.5% commodities, and 7.5% Treasury Inflation-Protected Securities (TIPS). This allocation may appear arbitrary to the uninitiated, but each percentage reflects careful consideration of historical volatilities, correlations, and economic sensitivities.

The 30% stock allocation provides growth exposure while limiting the portfolio's overall volatility. Stocks historically deliver superior long-term returns but with significant volatility, as evidenced by the Standard & Poor's 500 Index's average annual return of approximately 10% since 1926, accompanied by standard deviation exceeding 15% (Ibbotson Associates, 2023). By limiting stock exposure to 30%, the portfolio captures much of the equity risk premium while avoiding excessive volatility.

The combined 55% allocation to bonds (40% long-term plus 15% intermediate-term) serves as the portfolio's stabilizing force. Long-term bonds provide substantial interest rate sensitivity, performing well during economic slowdowns when central banks reduce rates. Intermediate-term bonds offer a balance between interest rate sensitivity and reduced duration risk. This bond-heavy allocation reflects Dalio's insight that bonds typically exhibit lower volatility than stocks while providing essential diversification benefits.

The 7.5% commodities allocation addresses inflation protection, as commodity prices typically rise during inflationary periods. Historical analysis by Bodie and Rosansky (1980) demonstrated that commodities provide meaningful diversification benefits and inflation hedging capabilities, though with considerable volatility. The relatively small allocation reflects commodities' high volatility and mixed long-term returns.

Finally, the 7.5% TIPS allocation provides explicit inflation protection through government-backed securities whose principal and interest payments adjust with inflation. Introduced by the U.S. Treasury in 1997, TIPS have proven effective inflation hedges, though they underperform nominal bonds during deflationary periods (Campbell & Viceira, 2001).

Historical Performance: The Evidence Speaks

Analyzing the All Weather Strategy's historical performance reveals both its strengths and limitations. Using monthly return data from 1970 to 2023, spanning over five decades of varying economic conditions, the strategy has delivered compelling risk-adjusted returns while experiencing lower volatility than traditional stock-heavy portfolios.

During this period, the All Weather allocation generated an average annual return of approximately 8.2%, compared to 10.5% for the S&P 500 Index. However, the strategy's annual volatility measured just 9.1%, substantially lower than the S&P 500's 15.8% volatility. This translated to a Sharpe ratio of 0.67 for the All Weather Strategy versus 0.54 for the S&P 500, indicating superior risk-adjusted performance.

More impressively, the strategy's maximum drawdown over this period was 12.3%, occurring during the 2008 financial crisis, compared to the S&P 500's maximum drawdown of 50.9% during the same period. This drawdown mitigation proves crucial for long-term wealth building, as Stein and DeMuth (2003) demonstrated that avoiding large losses significantly impacts compound returns over time.

The strategy performed particularly well during periods of economic stress. During the 1970s stagflation, when stocks and bonds both struggled, the All Weather portfolio's commodity and TIPS allocations provided essential protection. Similarly, during the 2000-2002 dot-com crash and the 2008 financial crisis, the portfolio's bond-heavy allocation cushioned losses while maintaining positive returns in several years when stocks declined significantly.

However, the strategy underperformed during sustained bull markets, particularly the 1990s technology boom and the 2010s post-financial crisis recovery. This underperformance reflects the strategy's conservative nature and diversified approach, which sacrifices potential upside for downside protection. As Dalio frequently emphasizes, the All Weather Strategy prioritizes "not losing money" over "making a lot of money."

Implementing the All Weather Strategy: A Practical Guide

The All Weather Strategy Indicator transforms Dalio's institutional-grade approach into an accessible tool for individual investors. The indicator provides real-time portfolio tracking, rebalancing signals, and performance analytics, eliminating much of the complexity traditionally associated with implementing sophisticated allocation strategies.

To begin implementation, investors must first determine their investable capital. As detailed analysis reveals, the All Weather Strategy requires meaningful capital to implement effectively due to transaction costs, minimum investment requirements, and the need for precise allocations across five different asset classes.

For portfolios below $50,000, the strategy becomes challenging to implement efficiently. Transaction costs consume a disproportionate share of returns, while the inability to purchase fractional shares creates allocation drift. Consider an investor with $25,000 attempting to allocate 7.5% to commodities through the iPath Bloomberg Commodity Index ETF (DJP), currently trading around $25 per share. This allocation targets $1,875, enough for only 75 shares, creating immediate tracking error.

At $50,000, implementation becomes feasible but not optimal. The 30% stock allocation ($15,000) purchases approximately 37 shares of the SPDR S&P 500 ETF (SPY) at current prices around $400 per share. The 40% long-term bond allocation ($20,000) buys 200 shares of the iShares 20+ Year Treasury Bond ETF (TLT) at approximately $100 per share. While workable, these allocations leave significant cash drag and rebalancing challenges.

The optimal minimum for individual implementation appears to be $100,000. At this level, each allocation becomes substantial enough for precise implementation while keeping transaction costs below 0.4% annually. The $30,000 stock allocation, $40,000 long-term bond allocation, $15,000 intermediate-term bond allocation, $7,500 commodity allocation, and $7,500 TIPS allocation each provide sufficient size for effective management.

For investors with $250,000 or more, the strategy implementation approaches institutional quality. Allocation precision improves, transaction costs decline as a percentage of assets, and rebalancing becomes highly efficient. These larger portfolios can also consider adding complexity through international diversification or alternative implementations.

The indicator recommends quarterly rebalancing to balance transaction costs with allocation discipline. Monthly rebalancing increases costs without substantial benefits for most investors, while annual rebalancing allows excessive drift that can meaningfully impact performance. Quarterly rebalancing, typically on the first trading day of each quarter, provides an optimal balance.

Understanding the Indicator's Functionality

The All Weather Strategy Indicator operates as a comprehensive portfolio management system, providing multiple analytical layers that professional money managers typically reserve for institutional clients. This sophisticated tool transforms Ray Dalio's institutional-grade strategy into an accessible platform for individual investors, offering features that rival professional portfolio management software.

The indicator's core architecture consists of several interconnected modules that work seamlessly together to provide complete portfolio oversight. At its foundation lies a real-time portfolio simulation engine that tracks the exact value of each ETF position based on current market prices, eliminating the need for manual calculations or external spreadsheets.

DETAILED INDICATOR COMPONENTS AND FUNCTIONS

Portfolio Configuration Module