Stablecoin Liquidity Delta v2 (Aggregate Market Cap Flow)Updated version of Stablecoin Liquidity Delta (Aggregate Market Cap Flow).

Hi All,

This indicator visualizes the bar-to-bar change in the aggregate market capitalization of major stablecoins, including USDT, USDC, DAI, and others. It serves as a proxy for monitoring on-chain liquidity and measuring capital inflows or outflows across the crypto market.

Stablecoins are the primary liquidity layer of the crypto economy. Their combined market capitalization acts as a mirror of the available fiat-denominated liquidity in digital markets:

🟩 An increase in the total stablecoin market capitalization indicates new issuance (capital entering the market).

🟥 A decrease reflects redemption or burning (liquidity exiting the system).

Tracking these flows helps anticipate macro-level liquidity trends that often lead overall market direction, providing context for broader price movements.

All values are derived from TradingView’s public CRYPTOCAP tickers, which represent the market capitalization of each stablecoin. While minor deviations can occur due to small price fluctuations around the $1 peg, these figures serve as a proxy for circulating supply and net issuance across the stablecoin ecosystem.

In den Scripts nach "liquidity" suchen

Stablecoin Liquidity Delta (Aggregate Market Cap Flow)Hi All,

This indicator visualizes the bar-to-bar change in the aggregate market capitalization of major stablecoins, including USDT, USDC, DAI, and others. It serves as a proxy for monitoring on-chain liquidity and measuring capital inflows or outflows across the crypto market.

Stablecoins are the primary liquidity layer of the crypto economy. Their combined market capitalization acts as a mirror of the available fiat-denominated liquidity in digital markets:

🟩 An increase in the total stablecoin market capitalization indicates new issuance (capital entering the market).

🟥 A decrease reflects redemption or burning (liquidity exiting the system).

Tracking these flows helps anticipate macro-level liquidity trends that often lead overall market direction, providing context for broader price movements.

All values are derived from TradingView’s public CRYPTOCAP tickers, which represent the market capitalization of each stablecoin. While minor deviations can occur due to small price fluctuations around the $1 peg, these figures serve as a proxy for circulating supply and net issuance across the stablecoin ecosystem.

Simulated Liquidity Zone Heatmap (SLZH) v5 (Stable)# 📈 Simulated Liquidity Zone Heatmap (SLZH) v5 - Order Flow Proxy & Adaptive VWAP

## 💡 Overview

The **Simulated Liquidity Zone Heatmap (SLZH)** is an advanced, stable Pine Script indicator designed to give traders an edge by visualizing **structural market liquidity** and **institutional order flow**. It acts as a powerful proxy for structural zones (like average cost basis) that are often missed by traditional technical analysis.

SLZH achieves this by combining two highly effective components:

1. **Volume-Based Liquidity Zones (VBLZ):** A dynamic, adaptive heatmap based on **Volume-Weighted Average Price (VWAP)** and Standard Deviation.

2. **Order Block (OB) Signals:** Stable, high-conviction signals marking the origin of strong impulsive moves.

---

## 📊 Key Features & Interpretation

### 1. Volume-Based Liquidity Zones (VBLZ) - The Adaptive Heatmap

The VBLZ dynamically paints a three-tiered support/resistance system, representing the market's average cost basis and conviction. This is primarily used as a **mean-reversion tool**.

| Component | Interpretation | Trading Action |

| :--- | :--- | :--- |

| **VWAP Center** (White Line) | The **Center of Liquidity**. Price is often attracted back to this line. | Use as a **Primary Target** when trading from the outer zones. |

| **Strong VBLZ** (Darkest Color) | **Highest Volume Concentration** (1 StdDev). Primary structural support/resistance. | Look for **Reversals** when price enters this zone. |

| **Mid/Weak VBLZ** (Lighter Colors) | Secondary areas of interest. | Use as **Secondary Targets** or to confirm an extended move. |

### 2. Order Block (OB) Signals - Structural Support/Resistance

The OB signals mark the last counter-trend candle before a strong, sustained move, indicating a potential institutional supply or demand zone. These are displayed as stable triangles on the chart.

* **Bullish OB** (Green Triangle Up): Marks a potential **Demand Zone**. Look for high-probability **long entries** when price returns to the area of this signal.

* **Bearish OB** (Red Triangle Down): Marks a potential **Supply Zone**. Look for high-probability **short entries** when price returns to the area of this signal.

---

## 🎯 High-Conviction Trading Strategy

The most effective way to use SLZH is to look for **confluence** between the dynamic VBLZ and the static OB signals. This combination creates the highest probability trade setups.

| Trade Setup | VBLZ Condition | OB Signal Condition | Action | Rationale |

| :--- | :--- | :--- | :--- | :--- |

| **High-Conviction Long** | Price is near or entering the **Strong VBLZ** from above. | A **Bullish OB Signal** is present in the same area. | **Enter Long** | Strong alignment between the market's average cost basis (VBLZ) and a structural demand zone (OB). |

| **High-Conviction Short** | Price is near or entering the **Strong VBLZ** from below. | A **Bearish OB Signal** is present in the same area. | **Enter Short** | Strong alignment between the market's average cost basis (VBLZ) and a structural supply zone (OB). |

### Setting Up Alerts

The script is equipped with three critical alert conditions for automated monitoring:

1. **Price in Strong VBLZ:** Notifies you when price enters the highest conviction heatmap zone.

2. **Bullish OB Signal:** Notifies you when a new Demand Zone is established.

3. **Bearish OB Signal:** Notifies you when a new Supply Zone is established.

---

## ⚙️ Customization (Inputs)

Adjust the indicator's sensitivity via the settings menu:

* **VBLZ Lookback Length:** Controls the recency of the heatmap calculation. **Higher values** create a smoother, longer-term zone.

* **OB Min Price Move (ATR Multiplier):** Filters the Order Blocks. **Increase this value** to show only the highest-conviction zones that led to the most powerful price moves.

---

**Note on Stability:** This is **v5**, a highly stable version optimized to avoid common Pine Script runtime errors. It uses stable `plotshape` signals instead of persistent boxes for the Order Blocks to ensure reliable performance on all charts.

Swing Points & Liquidity — ENHANCED PRO (Dark/Light Mode)This indicator — “Swing Points & Liquidity — ENHANCED PRO (Dark/Light Mode)” — automatically detects and visualizes swing highs, swing lows, and liquidity levels on the chart with rich analytics and customizable visuals.

🔍 Core Features

Smart Swing Detection: Identifies pivot highs/lows based on adjustable left/right bar settings.

Liquidity Visualization: Draws dynamic boxes and lines for liquidity pools and swing zones.

Volume & OI Integration: Filters and colors levels using volume and Open Interest Δ (change).

Strength Meter: Highlights strong liquidity levels with color gradients based on OI + volume intensity.

Automatic Trendlines: Connects swing points with selectable style and width.

Fibonacci Mapping: Automatically projects fib retracements (23.6%, 38.2%, 50%, 61.8%, 78.6%) from swing-to-swing for confluence zones.

Statistics Panel: Displays live metrics — total levels, active/filled count, success rate, and average strength.

Alerts System: Alerts for new swing formations and when price touches or breaks a level.

Multi-Timeframe Option: Analyze swing structures from higher timeframes on any chart.

Dual Theme Mode: Fully optimized for both Dark and Light interface preferences.

⚙️ Advanced Options

Adjustable lookback range

Hide or extend filled levels

Configurable volume and OI thresholds

Supports multiple OI data sources (Binance, BitMEX, Kraken)

Fully dynamic text, color, and label alignment settings

💡 Use Case

Perfect for Smart Money Concept (SMC) and ICT-style analysis, liquidity sweeps, and swing-based trading.

Traders can quickly visualize where liquidity sits, track how it gets filled, and monitor structure shifts in real time.

Estimated Manipulation Movement Signal [AlgoPoint]Follow the Footprints of Whale Movements That Drive the Market

Overview

The market is not always driven by natural supply and demand. Large players—often called "whales" or institutions—can create artificial price movements to trigger stop-losses, induce panic or FOMO, and build their large positions at favorable prices. These events are known as "stop hunts" or "liquidity grabs."

The EMMS indicator is a specialized tool designed to detect these specific moments of potential market manipulation. It does not follow trends in a traditional sense; instead, it identifies high-probability reversal points created by the calculated actions of Smart Money trapping other market participants.

How It Works: The 3-Module Logic

The indicator uses a multi-stage confirmation process to identify a potential stop hunt:

1. Anomaly Detection: The engine first scans the chart for "Anomaly Candles." These are candles with unusually high volume and a very long wick relative to their body. This combination signals a sudden, forceful, and potentially unnatural price push.

2. Liquidity Zone Detection: The indicator automatically identifies and tracks recent significant swing highs and lows. These levels are considered "Liquidity Zones" because they are areas where a large number of stop-loss orders are likely clustered. These are the "hunting grounds" for whales.

3. The Stop Hunt Signal: A final signal is generated only when these two events align in a specific sequence:

An Anomaly Candle (high volume, long wick) spikes through a previously identified Liquidity Zone.

The same candle then reverses, closing back inside the previous price range.

This sequence confirms that the move was likely a "trap" designed to engineer liquidity, and a reversal in the opposite direction is now highly probable.

How to Interpret & Use This Indicator

BUY Signal: A BUY signal appears after a sharp price drop that pierces a recent swing low (taking out the stops of long positions) and then aggressively reverses to close higher. This suggests that Smart Money has absorbed the panic selling they just induced. The signal indicates a potential move UP.

SELL Signal: A SELL signal appears after a sharp price spike that pierces a recent swing high (taking out the stops of short positions) and then aggressively reverses to close lower. This suggests that Smart Money has sold into the FOMO buying they just created. The signal indicates a potential move DOWN.

This indicator is best used as a high-probability confirmation tool, ideally in conjunction with your understanding of the overall market trend and structure.

[Shoshi] Liquidity SuiteChatGPT řekl:

Přemýšlení po dobu 24s

Liquidity Suite

A powerful, modular toolkit for liquidity-based trading — now with level merging, per-TF/global label offsets, and a master Liquidity toggle.

• Highs/Lows from Custom, 4H, D, W, M, Y

• Previous/Current candle anchoring (wick-anchored)

• Per-TF horizontal offsets + a global right-edge offset for tidy columns

• Optional “Merging levels” with % tolerance (e.g., 0.03%) — clusters nearby levels into one label (Y / pM / …) using the highest-TF color

• Custom line style/width/color and label mode (name/price/both), auto visibility by chart TF

• Buyside/Sellside inducements and FVG/Voids (visible count cap)

• NEW: Global “Show Liquidity” switch — instantly hides and clears all liquidity graphics regardless of other settings

• Asia, London, NY, Custom sessions

• Top/Mid/Bottom + open markers/labels

• Horizontal zones and optional vertical markers (Start/Start+End), extendable lines/background

• Killzones/Day/Week/Month opens

• Optional vertical shading; configurable line + label

• Daily/Weekly/Monthly VWAP with styles Line/Step/Area/Circles/Cross

• Right-edge labels (name/price/both), theme-aware colors

• Dark/White theme

• Separate configs per session/VWAP, per-TF level offsets, and merge tolerance

• Optimized for performance with object limits (lines/labels/boxes)

• Clean, uncluttered visuals for focused execution

NDOG & NWOG - Liquidity + Sunday Box rroielDescription:

This script combines NDOG & NWOG liquidity levels with a Sunday Box framework to provide traders with structured levels for weekly bias, liquidity mapping, and potential entry/exit zones.

Features:

• Automatic plotting of NDOG & NWOG liquidity zones.

• Sunday Box (weekly open range) drawn to define structure and bias.

• Highlights liquidity sweeps and retests for trade confirmation.

• Configurable settings for box time, liquidity range, and display options.

• Built to support ROI/EL strategies by aligning liquidity with weekly key levels.

Use Case:

Helps traders identify where price is likely to react by combining liquidity-based zones with the Sunday box framework. Designed for clarity, confluence, and efficiency in execution.

SMC - Institutional Confidence Oscillator [PhenLabs]📊 Institutional Confidence Oscillator

Version: PineScript™v6

📌 Description

The Institutional Confidence Oscillator (ICO) revolutionizes market analysis by automatically detecting and evaluating institutional activity at key support and resistance levels using our own in-house detection system. This sophisticated indicator combines volume analysis, volatility measurements, and mathematical confidence algorithms to provide real-time readings of institutional sentiment and zone strength.

Using our advanced thin liquidity detection, the ICO identifies high-volume, narrow-range bars that signal institutional zone formation, then tracks how these zones perform under market pressure. The result is a dual-wave confidence oscillator that shows traders when institutions are actively defending price levels versus when they’re abandoning positions.

The indicator transforms complex institutional behavior patterns into clear, actionable confidence percentiles, helping traders align with smart money movements and avoid common retail trading pitfalls.

🚀 Points of Innovation

Automated thin liquidity zone detection using volume threshold multipliers and zone size filtering

Dual-sided confidence tracking for both support and resistance levels simultaneously

Sigmoid function processing for enhanced mathematical accuracy in confidence calculations

Real-time institutional defense pattern analysis through complete test cycles

Advanced visual smoothing options with multiple algorithmic methods (EMA, SMA, WMA, ALMA)

Integrated momentum indicators and gradient visualization for enhanced signal clarity

🔧 Core Components

Volume Threshold System: Analyzes volume ratios against baseline averages to identify institutional activity spikes

Zone Detection Algorithm: Automatically identifies thin liquidity zones based on customizable volume and size parameters

Confidence Lifecycle Engine: Tracks institutional defense patterns through complete observation windows

Mathematical Processing Core: Uses sigmoid functions to convert raw market data into normalized confidence percentiles

Visual Enhancement Suite: Provides multiple smoothing methods and customizable display options for optimal chart interpretation

🔥 Key Features

Auto-Detection Technology: Automatically scans for institutional zones without manual intervention, saving analysis time

Dual Confidence Tracking: Simultaneously monitors both support and resistance institutional activity for comprehensive market view

Smart Zone Validation: Evaluates zone strength through volume analysis, adverse excursion measurement, and defense success rates

Customizable Parameters: Extensive input options for volume thresholds, observation windows, and visual preferences

Real-Time Updates: Continuously processes market data to provide current institutional confidence readings

Enhanced Visualization: Features gradient fills, momentum indicators, and information panels for clear signal interpretation

🎨 Visualization

Dual Oscillator Lines: Support confidence (cyan) and resistance confidence (red) plotted as percentage values 0-100%

Gradient Fill Areas: Color-coded regions showing confidence dominance and strength levels

Reference Grid Lines: Horizontal markers at 25%, 50%, and 75% levels for easy interpretation

Information Panel: Real-time display of current confidence percentiles with color-coded dominance indicators

Momentum Indicators: Rate of change visualization for confidence trends

Background Highlights: Extreme confidence level alerts when readings exceed 80%

📖 Usage Guidelines

Auto-Detection Settings

Use Auto-Detection

Default: true

Description: Enables automatic thin liquidity zone identification based on volume and size criteria

Volume Threshold Multiplier

Default: 6.0, Range: 1.0+

Description: Controls sensitivity of volume spike detection for zone identification, higher values require more significant volume increases

Volume MA Length

Default: 15, Range: 1+

Description: Period for volume moving average baseline calculation, affects volume spike sensitivity

Max Zone Height %

Default: 0.5%, Range: 0.05%+

Description: Filters out wide price bars, keeping only thin liquidity zones as percentage of current price

Confidence Logic Settings

Test Observation Window

Default: 20 bars, Range: 2+

Description: Number of bars to monitor zone tests for confidence calculation, longer windows provide more stable readings

Clean Break Threshold

Default: 1.5 ATR, Range: 0.1+

Description: ATR multiple required for zone invalidation, higher values make zones more persistent

Visual Settings

Smoothing Method

Default: EMA, Options: SMA/EMA/WMA/ALMA

Description: Algorithm for signal smoothing, EMA responds faster while SMA provides more stability

Smoothing Length

Default: 5, Range: 1-50

Description: Period for smoothing calculation, higher values create smoother lines with more lag

✅ Best Use Cases

Trending market analysis where institutional zones provide reliable support/resistance levels

Breakout confirmation by validating zone strength before position entry

Divergence analysis when confidence shifts between support and resistance levels

Risk management through identification of high-confidence institutional backing

Market structure analysis for understanding institutional sentiment changes

⚠️ Limitations

Performs best in liquid markets with clear institutional participation

May produce false signals during low-volume or holiday trading periods

Requires sufficient price history for accurate confidence calculations

Confidence readings can fluctuate rapidly during high-impact news events

Manual fallback zones may not reflect actual institutional activity

💡 What Makes This Unique

Automated Detection: First Pine Script indicator to automatically identify thin liquidity zones using sophisticated volume analysis

Dual-Sided Analysis: Simultaneously tracks institutional confidence for both support and resistance levels

Mathematical Precision: Uses sigmoid functions for enhanced accuracy in confidence percentage calculations

Real-Time Processing: Continuously evaluates institutional defense patterns as market conditions change

Visual Innovation: Advanced smoothing options and gradient visualization for superior chart clarity

🔬 How It Works

1. Zone Identification Process:

Scans for high-volume bars that exceed the volume threshold multiplier

Filters bars by maximum zone height percentage to identify thin liquidity conditions

Stores qualified zones with proximity threshold filtering for relevance

2. Confidence Calculation Process:

Monitors price interaction with identified zones during observation windows

Measures volume ratios and adverse excursions during zone tests

Applies sigmoid function processing to normalize raw data into confidence percentiles

3. Real-Time Analysis Process:

Continuously updates confidence readings as new market data becomes available

Tracks institutional defense success rates and zone validation patterns

Provides visual and numerical feedback through the oscillator display

💡 Note:

The ICO works best when combined with traditional technical analysis and proper risk management. Higher confidence readings indicate stronger institutional backing but should be confirmed with price action and volume analysis. Consider using multiple timeframes for comprehensive market structure understanding.

[c3s] CWS - M2 Global Liquidity Index & BTC Correlation CWS - M2 Global Liquidity Index with Offset BTC Correlation

This custom indicator visualizes and analyzes the relationship between the global M2 money supply and Bitcoin (BTC) price movements. It calculates the correlation between these two variables to provide insights into how changes in global liquidity may impact Bitcoin’s price over time.

Key Features:

Global M2 Liquidity Index Calculation:

Fetches M2 money supply data from multiple economies (China, US, EU, Japan, UK) and normalizes using currency exchange rates (e.g., CNY/USD, EUR/USD).

Combines all M2 data points and normalizes by dividing by 1 trillion (1e12) for easier visualization.

Offset for M2 Data:

The offset parameter allows users to shift the M2 data by a specified number of days, helping track the influence of past global liquidity on Bitcoin.

BTC Price Correlation:

Computes the correlation between shifted global M2 liquidity and Bitcoin (BTC) price, using a 52-day lookback period by default.

Correlation Quality Display:

Categorizes correlation quality as:

Excellent : Correlation >= 0.8

Good : Correlation >= 0.6 and < 0.8

Weak : Correlation >= 0.4 and < 0.6

Very Weak : Correlation < 0.4

Displays correlation quality as a label on the chart for easy assessment.

Visual Enhancements:

Labels : Displays dynamic labels on the chart with metrics like M2 value and correlation.

Plot Shapes : Uses shapes to indicate data availability for global M2 and correlation.

Data Table : Optionally shows a data table in the top-right corner summarizing:

Global M2 value (in trillions)

The correlation between global M2 and BTC

The correlation quality

Optional Debugging:

Debug plots help identify when data is missing for M2 or correlation, ensuring transparency and accurate functionality.

Inputs:

Offset: Shift the M2 data (in days) to see past liquidity effects on Bitcoin.

Lookback Period: Number of periods (default 52) used to calculate the correlation.

Show Labels: Toggle to show or hide labels for M2 and correlation values.

Show Table: Toggle to show or hide the data table in the top-right corner.

Usage:

Ideal for traders and analysts seeking to understand the relationship between global liquidity and Bitcoin price. The offset and lookback period can be adjusted to explore different timeframes and correlation strengths, aiding more informed trading decisions.

Real-Time Swing High/Low Detector with liquidity sweepThis script identifies the most important market structure points (swing highs/lows) and liquidity sweeps in a configurable and timeframe-adaptive manner.

By default:

It shows 5 recent swing highs and lows to keep your charts readable.

It detects and illustrates up to 3 Liquidity Sweeps (very close new highs/lows to earlier extremes).

It automatically adjusts how tight the sweep detection is based on your chart’s timeframe to balance precision and noise.

You can tweak all these numbers via the input settings panel to customize the indicator to your personal trading style and chart preferences

Configurable Parameters

Pivot Length (pivot_length)

What it does: Determines how many bars to the left and right the script looks at when identifying swing highs and lows.

Effect: Increasing this value results in fewer, more significant swings; decreasing it makes the indicator more sensitive and detects more swings.

Default: 5

Suggested: Adjust based on your trading timeframe and style to balance sensitivity and noise.

Show Labels (show_labels)

What it does: Toggles the display of swing labels such as HH, HL, LH, LL on the chart.

Effect: If enabled, the script marks swing points with their corresponding label for easier visual reference.

Default: true

Use: Turn off if you prefer a cleaner chart without textual swing indicators.

Show Current Levels (show_current_levels)

What it does: Toggles horizontal lines extending from the latest swing highs and lows.

Effect: Provides visual support/resistance zones on the chart.

Default: true

Use: Helpful for visualizing major price levels based on recent swings.

Max Swing Points (max_swings)

What it does: Limits the number of swing points stored and displayed.

Effect: Prevents chart clutter and performance issues by controlling history length.

Default: 20

Use: Increase for longer history; decrease for lighter charts.

Liquidity Sweep Threshold (liq_sweep_threshold_pc)

What it does: Defines the maximum percentage price difference allowed to consider a new high/low "very close" to the previous one, detecting a Liquidity Sweep.

Effect: Controls how sensitively the script detects these sweep points.

Default: Automatically set based on chart timeframe:

For timeframes below 1 hour: 0.05% (stricter, less tolerant)

For 1 hour and above: 0.1% (more tolerant)

Use: This dynamic setting ensures relevance of Liquidity Sweeps across different timeframes.

Liquidity Sweep Label Transparency (liq_sweep_alpha)

What it does: Controls the opacity of "Liquidity Sweep" labels, with 0 being fully opaque and 255 fully transparent.

Default: 10 (mostly opaque but slightly transparent)

Use: You can increase this value if you want the labels to be more subtle.

CHoCH + BOS + LQ Sweep v6.3.8 PRO+The CHoCH + BOS + LQ Sweep PRO indicator is a comprehensive Smart Money Concepts (SMC) tool designed to identify market structure shifts, liquidity sweeps, and key supply-demand zones across multiple timeframes. It helps traders visualize crucial price action patterns like Change of Character (CHoCH), Break of Structure (BOS), and liquidity grabs that often precede significant market reversals or continuations.

This tool is especially suited for traders applying multi-timeframe analysis and liquidity-based trading strategies on Forex, crypto, indices, or commodities.

1. Liquidity Sweeps (LQ Sweeps)

Identifies when price sweeps previous highs/lows (stop hunts/liquidity grabs).

Configurable strength setting to filter minor vs. major sweeps.

Optional stop at wick or stop at close logic for more precise entries.

Old sweeps can be displayed or hidden, with user-defined limits for historical sweeps.

2. Multi-Timeframe (HTF) Sweeps

Displays liquidity sweeps from higher timeframes (M15, H1, H4, D1, W1).

Individual checkboxes allow flexible combinations (e.g., show only H1 & H4 sweeps).

Unique colors for each timeframe to differentiate visually on the chart.

3. Supply/Demand Zones

Automatically plots zones around swing highs and lows.

Zones are dynamically updated and locked once price interacts with them.

Configurable view: Show both bullish/bearish zones or filter for one side only.

Option to display/hide old zones and limit the number of zones shown.

4. Historical Sweep Management

Stores up to 5000 sweeps internally, while adhering to TradingView’s rendering limits (max 500 drawn).

Ensures chart clarity by prioritizing the most recent sweeps.

Time-based LiquidityThis TradingView indicator identifies key liquidity zones based on previous highs and lows across multiple timeframes:

Monthly High/Low: Shows the previous month’s high and low levels, often acting as strong liquidity points where price may reverse or sweep before continuation.

Weekly High/Low: Highlights the previous week’s high and low, useful for short- to medium-term traders tracking breakout or fakeout zones.

Daily High/Low: Marks the high and low of the previous day, commonly targeted during intraday moves or liquidity grabs.

Session Zones (London & New York): Plots real-time highs and lows during the London and New York trading sessions. These zones are critical for identifying short-term liquidity sweeps and intraday volatility.

Traders use this tool to spot potential liquidity grabs, displacement entries, and reversal or continuation setups around institutional levels.

Simple Turnover with TOMCAPOverview

Turnover, or the total value traded over a given period, helps you gauge whether there’s enough liquidity in the instrument being traded. This indicator calculates the average turnover and presents it as a bar-by-bar plot. It also calculates the turnover-to-market capitalization (Tomcap) ratio, and presents this in a configurable table or text summary.

Introduction

Volume indicates the total number of shares that have been bought or sold in a specific period or during the trading day.

A company's market capitalization at any given time can be determined by multiplying its stock price by the number of shares outstanding.

Share turnover is a measure of stock liquidity, calculated by dividing the total number of shares traded during some period by the average number of shares outstanding for the same period. The higher the share turnover, the more liquid company shares are.

Compared to traditional volumes, potting the change in turnover can provide a better representation of the flow of money.

At its simplest, the daily turnover on each bar is computed as the closing price for a stock multiplied by its average volume:

turnover = volume * close / 10000000

The script calculates this by using average prices for both:

turnover = sma_volume * sma_close / 10000000

Script Basics

The script computes & plots the n-period average turnover by multiplying the moving average of price and volume.

By default, the market cap is plotted bar by bar as a background behind the turnover bars.

Every time the turnover reaches a new high in a quarter, the color of the turnover bars turns dark green. This represents the HTQ (Highest Turnover in a Quarter) , and multiple consecutive HTQs indicate a significant influx of funds into that stock.

Uses

The primary purpose of the script is to assist traders in making more informed decisions regarding stock selection.

1. Screen out non-tradable stocks

Quickly spot low-turnover names (illiquid stocks) to avoid wide spreads. Filter out any stocks whose average daily turnover is below, say, ₹5 Cr. This helps in eliminating tickers whose average turnover never clears your minimum threshold.

Example of a high-turnover stock:

Example of a low-turnover stock:

2. Turnover expansion

Observe when the average turnover suddenly expands from its previously subdued values. This occurs when money begins to flow in due to a catalyst, sectoral push, news flow, or any institutional activity.

Example:

3. Relative liquidity comparison

Even average turnover can sometimes overlook the context if we don’t know the company's size. That’s why the script also measures:

Turnover vs. Market cap (TOMCAP) , answering “What percent of the company’s value trades each day?”

Turnover vs. Free Float (TOFF) , showing liquidity against shares actually available for trading.

For example:

A small-cap stock with ₹1 Cr turnover but only ₹50 Cr market cap (Tomcap = 2 %)

vs. a large-cap with ₹10 Cr turnover and ₹20,000 Cr cap (Tomcap = 0.05 %)

Customization

A. Appearance

Dark Mode toggle switches colors to match your dark layout

Show turnover in Crores or Millions

B. What to show

Select the table size and position (e.g., top-left, bottom-center)

Under Table Settings, enable or disable any row:

Turnover

Mcap (market capitalization)

FF (free float)

1-Min liquidity (average turnover on 1-min bars)

Tomcap (Turnover to market capitalization) or Toff (Turnover to Free Float) ratio

C. Display mode

Table: a multi-row grid with colored cells

Text: a single summary string

Swing High/Low with Liquidity Sweeps🧠 Overview

This indicator identifies swing highs and swing lows based on user-defined candle lengths and checks for liquidity sweeps—situations where the price breaks a previous swing level but then closes back inside, indicating a potential false breakout or stop hunt. It also supports visual labeling and alerts for these events.

⚙️ Inputs

Swing Length (must be odd number ≥ 3):

Determines how many candles are used to identify swing highs/lows. The central candle must be higher or lower than all neighbors within the range.

Example: If swingLength = 5, the central candle must be higher/lower than the 2 candles on both sides.

Sweep Lookback (bars):

Defines how many bars to look back for possible liquidity sweeps.

Show Swing Labels (checkbox):

Optionally display labels on the chart when a swing high or low is detected.

Show Sweep Labels (checkbox):

Optionally display labels on the chart when a liquidity sweep occurs.

🕯️ Swing Detection Logic

A Swing High is detected when the high of the central candle is greater than the highs of all candles around it (as per the defined length).

A Swing Low is detected when the low of the central candle is lower than the lows of surrounding candles.

Swing labels are placed slightly above (for highs) or below (for lows) the candle.

💧 Liquidity Sweep Logic

A Sweep High is triggered if:

The current high breaks above a previously detected swing high,

And then the candle closes below that swing high,

Within the configured lookback window.

A Sweep Low is triggered if:

The current low breaks below a previous swing low,

And then closes above it,

Within the lookback window.

These are often seen as stop hunts or fake breakouts.

🔔 Alerts

Sweep High Alert: Triggered when a sweep above a swing high occurs.

Sweep Low Alert: Triggered when a sweep below a swing low occurs.

You can use these to set up TradingView alerts to notify you of potential liquidity grabs.

📊 Use Cases

Identifying market structure shifts.

Spotting fake breakouts and potential reversals.

Assisting in smart money concepts and liquidity-based trading.

Supporting entry timing in trend continuation or reversal strategies.

BTC-OTHERS Liquidity PivotBTC-OTHERS Liquidity Map – 1-hour Multi-Asset Pivot Scanner

WHAT IT DOES

This script tracks liquidity shifts between Bitcoin (BTC) and the broader alt-coin market (the OTHERS market-cap index that excludes the top-10 coins). It labels every confirmed 1-hour swing high or low on both assets, then flags four states:

BearPivot – BTC prints a new swing High while OTHERS does not; liquidity crowds into BTC and alts are weak.

BullPivot – BTC prints a swing Low and OTHERS forms a Higher Low; fresh liquidity starts flowing into stronger alts.

BearCon – BTC prints a swing Low and OTHERS forms a Lower Low; down-trend continuation.

BullCon – No new BTC Low while OTHERS makes a Higher High; up-trend continuation.

Signals appear on the actual pivot bar (offset back by the look-back length), so they never repaint after confirmation.

HOW THE PIVOTS ARE FOUND

• Symmetrical window: “Pivot Len” bars to the left and right (default 21).

• Full confirmation on both sides delivers stable, non-repainting pivots at the cost of about Pivot Len bars’ delay.

• Labels are offset –Pivot Len so they sit on the genuine extreme.

INPUTS

Symbols: BTC symbol and an OTHERS symbol so you can switch exchanges or choose another alt index.

Pivot Len: tighten for faster but noisier signals; widen for cleaner pivots.

Style: customise shape and text colours.

PLOTS AND ALERTS

Four labelled shapes (BearPivot, BullPivot, BearCon, BullCon) plot above or below price. Each label is linked to an alertcondition, so you can create one-click alerts and stay informed without watching the screen.

TYPICAL WORKFLOW

1. Attach the script to any 1-hour BTC chart (or leave the script’s timeframe empty to follow your current chart TF).

2. Turn on alerts to receive push/email notifications.

3. Use the labels as a liquidity compass, combining them with volume, funding or your own strategy for actual entries and exits.

Enjoy and trade safe.

Pivot Liquidity Sweep [scalpmeister]📌 Pivot Liquidity Sweep

Scalp-oriented, liquidity sweep-based advanced signal and strategy indicator.

This indicator analyzes the price's sweeping of significant pivot levels and the subsequent breakouts to generate long/short signals based on different logics. It is sensitive to both classic sweep logic and strong reversal candles. Additionally, it visually marks liquidity gathering zones, offering excellent opportunities especially for scalp and intraday traders.

⚙️ Features and Strategy Types

🟢 Automatic Pivot Detection:

Pivot high/low levels are detected and stored based on the number of left and right bars.

🔴 Sweep Detection (Stop Hunt):

If the price violates a pivot level with a wick and closes inside, it is considered a sweep (liquidity cleaning). Strategies activate after this sweep.

🧠 5 Different Signal Styles:

SweepBreak:

It is expected that the extreme (high/low) level of the sweeping candle is broken with a close.

PivotBreak:

After the sweep, the first newly formed pivot in the trend direction is expected to break. (It is dynamically determined and drawn on the chart.)

StrongSweep:

It is sufficient if the candle following the sweep surpasses the previous candle with a single candle. No additional breakout is expected.

StrongCandle:

Strong momentum candles measured with a special RSI calculation are taken into account. It considers strong opposite-direction candles formed shortly after a pivot sweep.

ReversalCandleSweep:

Reversal candles that close in the opposite direction after a sweep (e.g., a red close on a sweep candle formed at the top or a green close at the bottom) are directly considered as signals.

📐 Technical Details:

Signals are triggered only once (triggered control).

Sweep lines (green/red), Long and Short lines (Orange)

Strong candles are filtered using an RSI-momentum-based measurement system (StrongCandle).

Sweep and breakout zones are dynamically invalidated. That is, if the zones are violated by the price, the signals and lines are automatically canceled.

🎯 Who Should Use It?

Professional traders working with liquidity zones

Scalp and intraday strategy practitioners

Those focused on stop hunts, sweeps, and reversal zones

🔔 Alert Support:

Sweep High / Low Alert

Long / Short Signal Alert

IU Liquidity Flow TrackerDESCRIPTION

The IU Liquidity Flow Tracker is a powerful market analysis tool designed to visualize hidden buying and selling activity by analyzing price action, volume behavior, market pressure, and depth. It provides a composite view of liquidity dynamics to help traders identify accumulation, distribution, and neutral phases with high clarity.

This indicator is ideal for traders who want to gauge the flow of market participants and make informed entry/exit decisions based on the underlying liquidity structure.

USER INPUTS:

* Flow Analysis Period: Length used for analyzing price spread and volume flow.

* Pressure Sensitivity: Adjusts the sensitivity of threshold detection for flow classification.

* Flow Smoothing: Controls the smoothing applied to raw flow data.

* Market Depth Analysis: Sets the depth range for rejection and wick analysis.

* Colors: Customize colors for accumulation, distribution, neutral zones, and pressure visualization.

INDICATOR LOGIC:

The IU Liquidity Flow Tracker uses a multi-factor model to evaluate market behavior:

1. Liquidity Pressure: Combines price spread, price efficiency, and volume imbalance.

2. Flow Direction: Weighted momentum using short, medium, and long-term price changes adjusted for volume.

3. Market Depth: Wick-based rejection scoring to estimate buying/selling aggressiveness at price extremes.

4. Composite Flow Index: Blended value of flow direction, pressure, and depth—smoothed for clarity.

5. Dynamic Thresholds: Automatically adjusts based on volatility to classify the market into:

* Accumulation: Strong buying signals.

* Distribution: Strong selling signals.

* Neutral: No significant flow dominance.

6. Entry Signals: Long/Short signals are generated when flow state shifts, supported by momentum, volume surge, and depth strength.

WHY IT IS UNIQUE:

Unlike typical indicators that rely solely on price or volume, this tool combines spread behavior, volume polarity, momentum weighting, and price rejection zones into a single visual interface. It dynamically adjusts sensitivity based on market volatility, helping avoid false signals during sideways or low-volume periods.

It is not based on any traditional indicator (RSI, MACD, etc.), making it ideal for traders looking for an original and data-driven market read.

HOW USER CAN BENEFIT FROM IT:

* Understand Market Context: Know whether the market is being accumulated, distributed, or ranging.

* Improve Entries/Exits: Use flow transitions combined with volume confirmation for high-probability setups.

* Spot Institutional Activity: Detect subtle shifts in liquidity that precede major price moves.

* Reduce Whipsaws: Dynamic thresholds and multi-factor confirmation help filter noise.

* Use with Any Style: Whether you're a swing trader, day trader, or scalper, this tool adapts to different timeframes and strategies.

DISCLAIMER:

This indicator is created for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset. All trading involves risk, and users should conduct their own analysis or consult with a qualified financial advisor before making any trading decisions. The creator is not responsible for any losses incurred through the use of this tool. Use at your own discretion.

Stop Hunt Indicator ║ BullVision 🧠 Overview

The Stop Hunt Indicator (SmartTrap Radar) is an original tool designed to identify potential liquidity traps caused by institutional stop hunts. It visually maps out historically significant levels where price has repeatedly reversed or rejected — and dynamically detects real-time sweep patterns based on volume, structure, and candle rejection behavior.

This script does not repurpose existing public indicators, nor does it use default TradingView built-ins such as RSI, MACD, or MAs. Its core logic is fully proprietary and was developed from scratch to support discretionary and data-driven traders in visualizing volatility risks and manipulation zones.

🔍 What the Indicator Does

This indicator identifies and visualizes potential stop hunt zones using:

Historical structure analysis: Swing highs/lows are identified via a configurable lookback period.

Liquidity level tracking: Once detected, levels are monitored for touches, age, and volume strength.

Proprietary scoring model: Each level receives a real-time significance score based on:

Age (how long the level has held)

Number of rejections (touches)

Relative volume strength

Proximity to current price

The glow intensity of plotted levels is dynamically mapped based on this score. Bright glow = higher institutional interest probability.

⚙️ Stop Hunt Detection Logic

A stop hunt is flagged when all of the following are met:

Price sweeps through a high/low beyond a user-defined penetration threshold

Wick rejection occurs (i.e., candle closes back inside the level)

Volume spikes above the average in a recent window

The script automatically:

Detects bullish stop hunts (below support) and bearish ones (above resistance)

Marks detected sweeps on-chart with optional 🔰/🚨 signals

Adjusts glow visuals based on score even after the sweep occurs

These sweeps often precede local reversals or high-volatility zones — this is not predictive, but rather a reactive mapping of market manipulation behavior.

📌 Why This Is Not Just Another Liquidity Tool

Unlike typical liquidity heatmaps or S/R indicators, this script includes:

A proprietary significance score instead of fixed rules

Multi-layer glow rendering to reflect level importance visually

Real-time scoring updates as new volume and touches occur

Combined volume × rejection × structure logic to validate stop hunts

Fully customizable detection logic (lookback, wick %, volume filters, max bars, etc.)

This indicator provides a specialized view focused solely on visualizing trap setups — not generic trend signals.

🧪 Usage Recommendations

To get started:

Add the indicator to your chart (volume-enabled instruments only)

Customize detection:

Lookback Period for structure

Penetration % for how far price must sweep

Volume Spike Multiplier

Wick rejection strength

Enable/disable features:

Glow effects

Hunt markers

Score labels

Volume highlights

Watch for:

🔰 Bullish Sweeps (below support)

🚨 Bearish Sweeps (above resistance)

Bright glowing zones = high-liquidity targets

This tool can be used for both confluence and risk assessment, especially around high-impact sessions, liquidation events, or range extremes.

📊 Volume Dependency Notice

⚠️ This indicator requires real volume data to function correctly. On instruments without volume (e.g., synthetic pairs), certain features like spike detection and scoring will be disabled or inaccurate.

🔐 Closed-Source Disclosure

This script is published as invite-only to protect its proprietary scoring, glow mapping, and detection logic. While the full implementation remains confidential, this description outlines all key mechanics and configurable logic for user transparency.

(ICT)Liquidity Grab + FVG + MSS/BOSThis script is a comprehensive educational indicator that combines and enhances several well-known trading concepts:

Liquidity Grabs (Swing Failure Patterns)

Fair Value Gaps (FVG)

Market Structure Shifts / Break of Structure (MSS/BOS)

Alerts

It identifies potential bullish and bearish liquidity grabs, confirms them optionally using volume validation on a lower timeframe, and tracks subsequent price structure changes. The indicator visually marks key swing highs/lows, FVG zones, and BOS/MSS levels—allowing traders to observe how price reacts to liquidity and imbalance zones.

🔍 Features:

Swing Failure Patterns (SFP):

Highlights possible liquidity grabs based on recent highs/lows and candle structure.

Volume Validation (Optional):

Filter signals using relative volume outside the swing on a lower timeframe. Adjustable threshold.

Fair Value Gaps (FVG):

Detects imbalance gaps and extends them for easy visualization.

Market Structure (MSS/BOS):

Displays Break of Structure (BOS) and Market Structure Shift (MSS) based on pivot highs/lows and closing conditions.

Dashboard:

A compact info panel displaying lower timeframe settings and validation status.

Custom Styling:

Adjustable colors, line styles, and label visibility for clean charting.

🧠 Ideal For:

Traders studying ICT concepts, smart money theories, and price-action-based strategies who want a visual tool for analysis and backtesting.

How to Use:

Wait for a Liquidity Grab (SFP) to form

The first condition for a potential entry is the formation of a Stop Hunt / Swing Failure Pattern (SFP).

This indicates that liquidity has been taken above or below a key level (e.g., previous high/low), and the market may be ready to reverse.

Confirmation with Fair Value Gap (FVG) and Market Structure Shift (MSS)

After the SFP, do not enter immediately. Wait for confirmation:

FVG : A Fair Value Gap (an imbalance in price action) must appear, signaling potential institutional activity.

MSS : A Market Structure Shift (break in the current trend) confirms a possible trend reversal or strong corrective move.

Enter the trade

Once both the FVG and MSS are confirmed after the SFP, you can safely enter a trade in the direction of the shift.

Alert Feature

The indicator includes an alert system to notify you when all conditions are met (SFP + FVG + MSS), so you can react quickly without constantly watching the chart.

AMD Liquidity Sweep with AlertsAMD Liquidity Sweep with Alerts

Identify key liquidity levels from the Asian trading session with visual markers and alerts.

📌 Key Features:

Asia Session Detection

Customizable start/end hours (0-23) to match your trading timezone

Automatically calculates session high/low

Smart Swing Level Identification

Finds the closest significant swing high ≥ Asia high

Finds the closest significant swing low ≤ Asia low

Adjustable pivot sensitivity (# of left/right bars)

Professional Visuals

Dashed reference lines extending into the future

Blue-highlighted key levels

Clean label formatting with precise price levels

Trading Alerts

Price-cross alerts for liquidity breaks

Visual markers (triangles) when levels are breached

Separate alerts for buy-side/sell-side liquidity

Customization Options

Toggle intermediate swing highlights

Adjust label sizes

💡 Trading Applications:

Institutional Levels: Identify zones where Asian session liquidity pools exist

Breakout Trading: Get alerted when price breaches Asian session ranges

S/R Flip Zones: Watch how price reacts at these key reference levels

London/NY Open: Use Asian levels for early European session trades

🔧 How to Use:

Set your preferred Asia session hours

Adjust pivot sensitivity (default 1 bar works for most timeframes)

Enable alerts for breakouts if desired

Watch for reactions at the plotted levels

Enhanced Volume w/ Pocket Pivots, Milestones & LiquiditySure! Here’s a professional and clear **description** you can use when saving or publishing the script on TradingView:

---

## 📄 Script Description: *Enhanced Volume w/ Pocket Pivots, Milestones & Liquidity*

This custom volume indicator enhances the default volume view by combining key institutional-level insights into a single tool. It highlights meaningful volume activity, liquidity conditions, and milestone events to help traders better understand accumulation/distribution and smart money participation.

### 🔍 Features:

* **Color-coded volume bars**:

* 🔵 **Pocket Pivot Volume (PPV)**: Up-day with volume > highest down-day volume of last 10 bars.

* 🟢 **Up Volume**: Up-day with volume > 50-day average.

* 🔴 **Down Volume**: Down-day with volume > 50-day average.

* 🟠 **Dry Volume**: Low-volume bars < 20% of 50-day average.

* ⚫ **Neutral/Other bars**: No significant signal.

* **Volume Milestones**:

* **HVE**: Highest volume ever (20 years lookback).

* **HVY**: Highest volume in the past 1 year (252 bars).

* **HVQ**: Highest volume in the past quarter (63 bars).

* **Projected Volume**:

* Real-time estimate of end-of-day volume based on elapsed session time.

* **Liquidity Metrics**:

* Displays current and 50-day average dollar volume.

* Estimates 1-minute liquidity for large-position feasibility.

* **Relative Volume Label**:

* Displays how today’s volume compares to the 50-day average.

* **Alerts Included**:

* Set alerts for HVE, HVY, and HVQ to catch key breakout or climactic volume events.

---

### 🧠 Ideal For:

* Growth stock traders

* Volume/price analysts

* Intraday & swing traders

* Institutions or prop traders needing liquidity benchmarks

---

Let me know if you'd like a short or promotional version (for sharing with others).

Power Law Global Liquidity Price Model & OscillatorDescription:

This Pine Script implements a predictive Bitcoin (BTC) price model derived from an observed power-law relationship between BTC price and Global Liquidity (specifically Global M2).

To clarify, the indicator doesn't show M2 directly as many indicators do, but uses an empirical observed relationship between BTC price and M2. This is an important difference from other Global Liquidity indicators and makes it very useful because it allows for making predictions on the future of Bitcoin price.

The model is based on the relationship BTC ~ GL^9.3, where GL represents Global M2, and the best correlation is achieved with an 85-period lead in GL, making it a leading indicator for BTC price movements. The observed correlation is higher than 0.92, giving high confidence in the model's validity. The 85-day lead was chosen by calculating the predictive rate of the model (how many times a positive/negative return in the model correlates with the price) with a given lead. The relationship between a chosen delay and predictive power has a maximum at 85 days.

Features:

BTC Price Model:

Calculates a BTC price model using the power-law relationship (BTC ~ GL^9.3) with an 85-period lead in Global Liquidity data.

The model is superimposed on the chart using forced overlay for clear visualization of the predicted BTC price trend relative to actual price.

Directional Oscillator:

Displayed in a lower panel, the oscillator compares the structural similarity between the actual BTC price and the GL-based price model.

Computes the win rate of the averaged BTC price (over a 1-year period) versus the price model to highlight structural alignment.

Projects future oscillator values based on the 85-period lead in the GL model, providing insight into potential price direction.

This feature is also very unique, and it is not present in most Global Liquidity indicators. The reason to choose the win rate is that this parameter doesn't depend on a precise scaling

between the BTC price and GL. This allows for better identification of changes in features between the 2 time series (for example, a downturn, a run up, peaks, bottoms, and similar).

Purpose:

This script serves as a predictive tool for traders and analysts by leveraging the leading relationship between Global Liquidity and BTC price. The overlay model and oscillator provide both a visual and quantitative framework to anticipate BTC price trends and assess structural alignment with global economic indicators.

The indicator allows for early identification of bottoms, peaks, and possible local bull or bear runs.

Usage Notes:

This indicator works best when used with the "All Time History" BTCUSD index.

The 85-period lead in GL allows for forward-looking projections, making this tool suitable for strategic planning.

The oscillator aids in confirming the structural validity of the model, enhancing confidence in its projections.

Quantify [Trading Model] | FractalystNote: In this description, "TM" refers to Trading Model (not trademark) and "EM" refers to Entry Model

What’s the indicator’s purpose and functionality?

You know how to identify market bias but always struggle with figuring out the best exit method, or even hesitating to take your trades?

I've been there. That's why I built this solution—once and for all—to help traders who know the market bias but need a systematic and quantitative approach for their entries and trade management.

A model that shows you real-time market probabilities and insights, so you can focus on execution with confidence—not doubt or FOMO.

How does this Quantify differentiate from Quantify ?

Have you managed to code or even found an indicator that identifies the market bias for you, so you don’t have to manually spend time analyzing the market and trend?

Then that’s exactly why you might need the Quantify Trading Model.

With the Trading Model (TM) version, the script automatically uses your given bias identification method to determine the trend (bull vs bear and neutral), detect the bias, and provide instant insight into the trades you could’ve taken.

To avoid complications from consecutive signals, it uses a kNN machine learning algorithm that processes market structure and probabilities to predict the best future patterns.

(You don’t have to deal with any complexity—it’s all taken care of for you.)

Quantify TM uses the k-Nearest Neighbors (kNN) machine learning algorithm to learn from historical market patterns and adapt to changing market structures. This means it can recognize similar market conditions from the past and apply those lessons to current trading decisions.

On the other hand, Quantify EM requires you to manually select your directional bias. It then focuses solely on generating entry signals based on that pre-determined bias.

While the entry model version (EM) uses your manual bias selection to determine the trend, it then provides insights into trades you could’ve taken and should be taking.

Trading Model (TM)

- Uses `input.source()` to incorporate your personal methodology for identifying market bias

- Automates everything—from bias detection to entry and exit decisions

- Adapts to market bias changes through kNN machine learning optimization

- Reduces human intervention in trading decisions, limiting emotional interference

Entry Model (EM)

- Focuses specifically on optimizing entry points within your pre-selected directional bias

- Requires manual input for determining market bias

- Provides entry signals without automating alerts or bias rules

Can the indicator be applied to any market approach/trading strategy?

Yes, if you have clear rules for identifying the market bias, then you can code your bias detection and then use the input.source() user input to retrieve the direction from your own indicator, then the Quantify uses machine-learning identify the best setups for you.

Here's an example:

//@version=6

indicator('Moving Averages Bias', overlay = true)

// Input lengths for moving averages

ma10_length = input.int(10, title = 'MA 10 Length')

ma20_length = input.int(20, title = 'MA 20 Length')

ma50_length = input.int(50, title = 'MA 50 Length')

// Calculate moving averages

ma10 = ta.sma(close, ma10_length)

ma20 = ta.sma(close, ma20_length)

ma50 = ta.sma(close, ma50_length)

// Identify bias

var bias = 0

if close > ma10 and close > ma20 and close > ma50 and ma10 > ma20 and ma20 > ma50

bias := 1 // Bullish

bias

else if close < ma10 and close < ma20 and close < ma50 and ma10 < ma20 and ma20 < ma50

bias := -1 // Bearish

bias

else

bias := 0 // Neutral

bias

// Plot the bias

plot(bias, title = 'Identified Bias', color = color.blue,display = display.none)

Once you've created your custom bias indicator, you can integrate it with Quantify :

- Add your bias indicator to your chart

- Open the Quantify settings

- Set the Bias option to "Auto"

- Select your custom indicator as the bias source

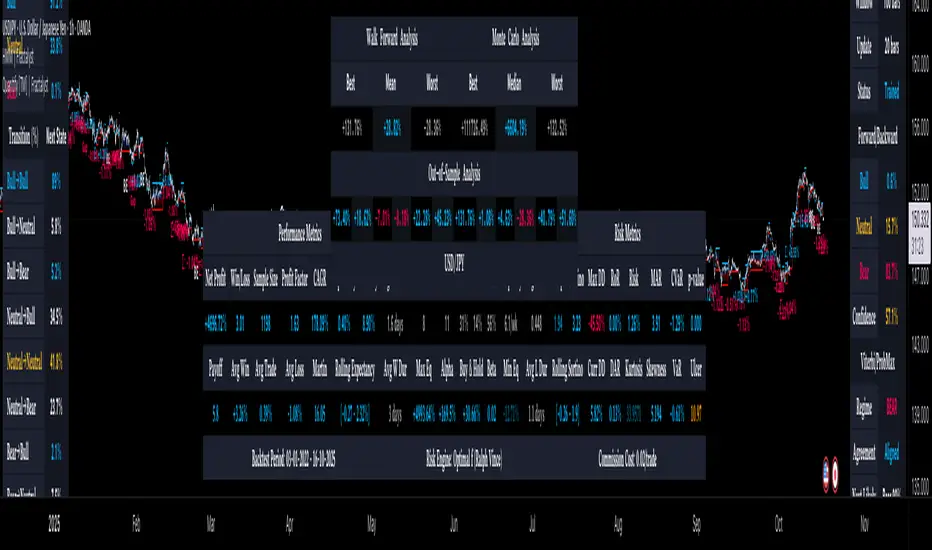

The machine learning algorithms will then analyze historical price action and identify optimal setups based on your defined bias parameters. Performance statistics are displayed in summary tables, allowing you to evaluate effectiveness across different timeframes.

Can the indicator be used for different timeframes or trading styles?

Yes, regardless of the timeframe you’d like to take your entries, the indicator adapts to your trading style.

Whether you’re a swing trader, scalper, or even a position trader, the algorithm dynamically evaluates market conditions across your chosen timeframe.

How Quantify Helps You Trade Profitably?

The Quantify Trading Model offers several powerful features that can significantly improve your trading profitability when used correctly:

Real-Time Edge Assessment

It displays real-time probability of price moving in your favor versus hitting your stoploss

This gives you immediate insight into risk/reward dynamics before entering trades

You can make more informed decisions by knowing the statistical likelihood of success

Historical Edge Validation

Instantly shows whether your trading approach has demonstrated an edge in historical data

Prevents you from trading setups that historically haven't performed well

Gives confidence when entering trades that have proven statistical advantages

Optimized Position Sizing

Analyzes each setup's success rate to determine the adjusted Kelly criterion formula

Customizes position sizing based on your selected maximum drawdown tolerance

Helps prevent account-destroying losses while maximizing growth potential

Advanced Exit Management

Utilizes market structure-based trailing stop-loss mechanisms

Maximizes the average risk-reward ratio profit per winning trade

Helps capture larger moves while protecting gains during market reversals

Emotional Discipline Enforcement

Eliminates emotional bias by adhering to your pre-defined rules for market direction

Prevents impulsive decisions by providing objective entry and exit signals

Creates psychological distance between your emotions and trading decisions

Overtrading Prevention

Highlights only setups that demonstrate positive expectancy

Reduces frequency of low-probability trades

Conserves capital for higher-quality opportunities

Systematic Approach Benefits

By combining machine learning algorithms with your personal bias identification methods, Quantify helps transform discretionary trading approaches into more systematic, probability-based strategies.

What Entry Models are used in Quantify Trading Model version?

The Quantify Trading Model utilizes two primary entry models to identify high-probability trade setups:

Breakout Entry Model

- Identifies potential trade entries when price breaks through significant swing highs and swing lows

- Captures momentum as price moves beyond established trading ranges

- Particularly effective in trending markets when combined with the appropriate bias detection

- Optimized by machine learning to filter false breakouts based on historical performance

Fractals Entry Model

- Utilizes fractal patterns to identify potential reversal or continuation points

- Also uses swing levels to determine optimal entry locations

- Based on the concept that market structure repeats across different timeframes

- Identifies local highs and lows that form natural entry points

- Enhanced by machine learning to recognize the most profitable fractal formations

- These entry models work in conjunction with your custom bias indicator to ensure trades are taken in the direction of the overall market trend. The machine learning component analyzes historical performance of these entry types across different market conditions to optimize entry timing and signal quality.

How Does This Indicator Identify Market Structure?

1. Swing Detection

• The indicator identifies key swing points on the chart. These are local highs or lows where the price reverses direction, forming the foundation of market structure.

2. Structural Break Validation

• A structural break is flagged when a candle closes above a previous swing high (bullish) or below a previous swing low (bearish).

• Break Confirmation Process:

To confirm the break, the indicator applies the following rules:

• Valid Swing Preceding the Break: There must be at least one valid swing point before the break.

3. Numeric Labeling

• Each confirmed structural break is assigned a unique numeric ID starting from 1.

• This helps traders track breaks sequentially and analyze how the market structure evolves over time.

4. Liquidity and Invalidation Zones

• For every confirmed structural break, the indicator highlights two critical zones:

1. Liquidity Zone (LIQ): Represents the structural liquidity level.

2. Invalidation Zone (INV): Acts as Invalidation point if the structure fails to hold.

How does the trailing stop-loss work? what are the underlying calculations?

A trailing stoploss is a dynamic risk management tool that moves with the price as the market trend continues in the trader’s favor. Unlike a fixed take profit, which stays at a set level, the trailing stoploss automatically adjusts itself as the market moves, locking in profits as the price advances.

In Quantify, the trailing stoploss is enhanced by incorporating market structure liquidity levels (explain above). This ensures that the stoploss adjusts intelligently based on key price levels, allowing the trader to stay in the trade as long as the trend remains intact, while also protecting profits if the market reverses.

What is the Kelly Criterion, and how does it work in Quantify?

The Kelly Criterion is a mathematical formula used to determine the optimal position size for each trade, maximizing long-term growth while minimizing the risk of large drawdowns. It calculates the percentage of your portfolio to risk on a trade based on the probability of winning and the expected payoff.

Quantify integrates this with user-defined inputs to dynamically calculate the most effective position size in percentage, aligning with the trader’s risk tolerance and desired exposure.

How does Quantify use the Kelly Criterion in practice?

Quantify uses the Kelly Criterion to optimize position sizing based on the following factors:

1. Confidence Level: The model assesses the confidence level in the trade setup based on historical data and sample size. A higher confidence level increases the suggested position size because the trade has a higher probability of success.

2. Max Allowed Drawdown (User-Defined): Traders can set their preferred maximum allowed drawdown, which dictates how much loss is acceptable before reducing position size or stopping trading. Quantify uses this input to ensure that risk exposure aligns with the trader’s risk tolerance.

3. Probabilities: Quantify calculates the probabilities of success for each trade setup. The higher the probability of a successful trade (based on historical price action and liquidity levels), the larger the position size suggested by the Kelly Criterion.

How can I get started to use the indicator?

1. Set Your Market Bias

• Choose Auto.

• Select the source you want Quantify to use as for bias identification method (explained above)

2. Choose Your Entry Timeframes

• Specify the timeframes you want to focus on for trade entries.

• The indicator will dynamically analyze these timeframes to provide optimal setups.

3. Choose Your Entry Model and BE/TP Levels

• Choose a model that suits your personality

• Choose a level where you'd like the script to take profit or move stop-loss to BE

4. Set and activate the alerts

What tables are used in the Quantify?

• Quarterly

• Monthly

• Weekly

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

- By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.