Imbalance(FVG) DetectorImbalance (FVG) Detector

Overview

The Imbalance (FVG) Detector is a technical analysis tool designed to highlight price inefficiencies by identifying Fair Value Gaps (FVGs). These gaps occur when rapid price movement leaves an area with little to no traded volume, which may later act as a zone of interest. The indicator automatically detects and marks these imbalances on the chart, allowing users to observe historical price behavior more effectively.

Key Features

- Automatic Imbalance Detection: Identifies bullish and bearish imbalances based on a structured three-bar price action model.

- Customizable Sensitivity: Users can adjust the minimum imbalance percentage threshold to tailor detection settings to different assets and market conditions.

- Real-time Visualization: Marked imbalances are displayed as colored boxes directly on the chart.

- Dynamic Box Updates: Imbalance zones extend forward in time until price interacts with them.

- Alert System: Users can set alerts for when new imbalances appear or when price tests an existing imbalance.

How It Works

The indicator identifies market imbalances using a three-bar price structure:

- Bullish Imbalance: Occurs when the high of three bars ago is lower than the low of the previous bar, forming a price gap.

- Bearish Imbalance: Occurs when the low of three bars ago is higher than the high of the previous bar, creating a downward gap.

When an imbalance is detected:

- Green Boxes indicate bullish imbalances.

- Red Boxes indicate bearish imbalances.

- Once price interacts with an imbalance, the box fades to gray, marking it as tested.

! Designed for Crypto Markets

This indicator is particularly useful in crypto markets, where frequent volatility can create price inefficiencies. It provides a structured way to visualize gaps in price movement, helping users analyze historical liquidity areas.

Customization Options

- Min Imbalance Percentage Size: Adjusts the sensitivity of the imbalance detection.

- Alerts: Users can enable alerts to stay notified of new or tested imbalances.

Important Notes

- This indicator is a technical analysis tool and does not provide trading signals or financial advice.

- It does not predict future price movement but highlights historical price inefficiencies.

- Always use this tool alongside other market analysis methods and risk management strategies.

In den Scripts nach "gaps" suchen

TR FVG Finder 1.0TR FVG Finder 1.0 - Identify High-Probability Trading Zones

Unlock the power of Fair Value Gaps (FVGs) with this advanced TradingView indicator! Designed for traders seeking high-probability setups, the Fair Value Gap Detector identifies key price imbalances on your chart, helping you spot potential reversal and continuation zones with precision.

Key Features:

Accurate FVG Detection: Automatically detects bullish and bearish Fair Value Gaps based on a proven 3-candle pattern, highlighting areas where price is likely to return.

Customizable Display: Shows the most recent 3 FVGs by default (combined bullish and bearish), with an option to adjust the number of FVGs displayed.

Visual Clarity: Draws semi-transparent boxes (green for bullish FVGs, red for bearish FVGs) that extend 15 candles to the right, making it easy to track key levels.

Versatile for All Markets: Works on any timeframe and instrument—perfect for forex, stocks, crypto, and commodities like XAU/USD (gold).

User-Friendly: Simple to use with customizable settings, ideal for both beginner and experienced traders.

How It Works:

The indicator identifies FVGs by analyzing a 3-candle pattern:

- Bullish FVG: When the high of the candle two bars back is below the low of the current candle.

- Bearish FVG: When the low of the candle two bars back is above the high of the current candle. These gaps often act as magnets for price, making them powerful zones for trading strategies like breakouts, pullbacks, or reversals.

Why Use This Indicator?

- Enhance your technical analysis with a proven concept used by institutional traders.

- Spot high-probability trading opportunities with clear visual cues.

- Save time by automating FVG detection—no manual drawing required.

Best Practices:

- Use on lower timeframes (e.g., 15-minute or 1-hour) for more frequent FVGs, especially in volatile markets like forex or crypto.

- Combine with other indicators (e.g., support/resistance, volume) for confirmation.

- Ideal for strategies like ICT (Inner Circle Trader) concepts, Smart Money trading, and price action analysis.

Regards,

Trader Riaz

Quarterly Theory ICT 03 [TradingFinder] Precision Swing Points🔵 Introduction

Precision Swing Point (PSP) is a divergence pattern in the closing of candles between two correlated assets, which can indicate a potential trend reversal. This structure appears at market turning points and highlights discrepancies between the price behavior of two related assets.

PSP typically forms in key timeframes such as 5-minute, 15-minute, and 90-minute charts, and is often used in combination with Smart Money Concepts (SMT) to confirm trade entries.

PSP is categorized into Bearish PSP and Bullish PSP :

Bearish PSP : Occurs when an asset breaks its previous high, and its middle candle closes bullish, while the correlated asset closes bearish at the same level. This divergence signals weakness in the uptrend and a potential price reversal downward.

Bullish PSP : Occurs when an asset breaks its previous low, and its middle candle closes bearish, while the correlated asset closes bullish at the same level. This suggests weakness in the downtrend and a potential price increase.

🟣 Trading Strategies Using Precision Swing Point (PSP)

PSP can be integrated into various trading strategies to improve entry accuracy and filter out false signals. One common method is combining PSP with SMT (divergence between correlated assets), where traders identify divergence and enter a trade only after PSP confirms the move.

Additionally, PSP can act as a liquidity gap, meaning that price tends to react to the wick of the PSP candle, making it a favorable entry point with a tight stop-loss and high risk-to-reward ratio. Furthermore, PSP combined with Order Blocks and Fair Value Gaps in higher timeframes allows traders to identify stronger reversal zones.

In lower timeframes, such as 5-minute or 15-minute charts, PSP can serve as a confirmation for more precise entries in the direction of the higher timeframe trend. This is particularly useful in scalping and intraday trading, helping traders execute smarter entries while minimizing unnecessary stop-outs.

🔵 How to Use

PSP is a trading pattern based on divergence in candle closures between two correlated assets. This divergence signals a difference in trend strength and can be used to identify precise market turning points. PSP is divided into Bullish PSP and Bearish PSP, each applicable for long and short trades.

🟣 Bullish PSP

A Bullish PSP forms when, at a market turning point, the middle candle of one asset closes bearish while the correlated asset closes bullish. This discrepancy indicates weakness in the downtrend and a potential price reversal upward.

Traders can use this as a signal for long (buy) trades. The best approach is to wait for price to return to the wick of the PSP candle, as this area typically acts as a liquidity level.

f PSP forms within an Order Block or Fair Value Gap in a higher timeframe, its reliability increases, allowing for entries with tight stop-loss and optimal risk-to-reward ratios.

🟣 Bearish PSP

A Bearish PSP forms when, at a market turning point, the middle candle of one asset closes bullish while the correlated asset closes bearish. This indicates weakness in the uptrend and a potential price decline.

Traders use this pattern to enter short (sell) trades. The best entry occurs when price retests the wick of the PSP candle, as this level often acts as a resistance zone, pushing price lower.

If PSP aligns with a significant liquidity area or Order Block in a higher timeframe, traders can enter with greater confidence and place their stop-loss just above the PSP wick.

Overall, PSP is a highly effective tool for filtering false signals and improving trade entry precision. Combining PSP with SMT, Order Blocks, and Fair Value Gaps across multiple timeframes allows traders to execute higher-accuracy trades with lower risk.

🔵 Settings

Mode :

2 Symbol : Identifies PSP and PCP between two correlated assets.

3 Symbol : Compares three assets to detect more complex divergences and stronger confirmation signals.

Second Symbol : The second asset used in PSP and correlation calculations.

Third Symbol : Used in three-symbol mode for deeper PSP and PCP analysis.

Filter Precision X Point : Enables or disables filtering for more precise PSP and PCP detection. This filter only identifies PSP and PCP when the base asset's candle qualifies as a Pin Bar.

Trend Effect : By changing the Trend Effect status to "Off," all Pin bars, whether bullish or bearish, are displayed regardless of the current market trend. If the status remains "On," only Pin bars in the direction of the main market trend are shown.

Bullish Pin Bar Setting : Using the "Ratio Lower Shadow to Body" and "Ratio Lower Shadow to Higher Shadow" settings, you can customize your bullish Pin bar candles. Larger numbers impose stricter conditions for identifying bullish Pin bars.

Bearish Pin Bar Setting : Using the "Ratio Higher Shadow to Body" and "Ratio Higher Shadow to Lower Shadow" settings, you can customize your bearish Pin bar candles. Larger numbers impose stricter conditions for identifying bearish Pin bars.

🔵 Conclusion

Precision Swing Point (PSP) is a powerful analytical tool in Smart Money trading strategies, helping traders identify precise market turning points by detecting divergences in candle closures between correlated assets. PSP is classified into Bullish PSP and Bearish PSP, each playing a crucial role in detecting trend weaknesses and determining optimal entry points for long and short trades.

Using the PSP wick as a key liquidity level, integrating it with SMT, Order Blocks, and Fair Value Gaps, and analyzing higher timeframes are effective techniques to enhance trade entries. Ultimately, PSP serves as a complementary tool for improving entry accuracy and reducing unnecessary stop-outs, making it a valuable addition to Smart Money trading methodologies.

TJR SEEK AND DESTROYTJR SEEK AND DESTROY – Intraday ICT Trading Tool

Built for day traders, TJR SEEK AND DESTROY combines Smart Money concepts like order blocks, fair value gaps, and liquidity sweeps with structure breaks and daily bias to pinpoint high-probability trades during US market hours (9:30–16:00). Ideal for scalping or intraday strategies on stocks, futures, or forex.

What Makes It Unique?

Unlike standalone ICT indicators, this script integrates:

Order Blocks with volume and range filters for precise support/resistance zones.

Fair Value Gaps (FVG) to spot pre-market price imbalances.

Break of Structure (BOS) and Liquidity Sweeps for trend and reversal signals.

A 1H MA-based Bias to align trades with the day’s direction.

BUY/SELL Labels triggered only when bias, BOS, and sweeps align, reducing noise.

How Does It Work?

Order Blocks: Marks zones with high volume (>1.5x 20-period SMA) and low range (<0.5x ATR20) as teal boxes—potential reversal points.

Fair Value Gap: Compares the prior day’s close to the current open (pre- or post-9:30), shown as a purple line and label (e.g., "FVG: 0.005").

Pivot Point: Calculates (prevHigh + prevLow + prevClose) / 3 from the prior day, plotted as an orange line for equilibrium.

Break of Structure: Detects crossovers of 5-bar highs/lows (gray lines), marked with red triangles.

Liquidity Sweeps: Tracks breaches of the prior day’s high/low (yellow lines), marked with yellow triangles.

Daily Bias: Uses 1H close vs. 20-period MA (blue line) for bullish (green background), bearish (red), or neutral (gray) context.

Signals: BUY (green label) when bias is bullish, price breaks up, and sweeps the prior high; SELL (red label) when bias is bearish, price breaks down, and sweeps the prior low.

How to Use It

Setup: Apply to 1M–15M charts for US session trading (9:30–16:00 EST).

Trading:

Wait for a BUY label after a yellow sweep triangle above the prior day’s high in a green (bullish) background.

Wait for a SELL label after a yellow sweep triangle below the prior day’s low in a red (bearish) background.

Use order blocks (teal boxes) as support/resistance for stop-loss or take-profit.

Markets: Best for SPY, ES futures, or forex pairs with US session volatility.

Underlying Concepts

Order Blocks: High-volume, low-range bars suggest institutional activity.

FVG: Gaps between close and open indicate imbalance to be filled.

BOS & Sweeps: Price breaking key levels signals momentum or stop-hunting.

Bias: 1H MA filters trades by broader trend.

Chart Setup

Displays order blocks (teal boxes), pivot (orange), open (purple), bias (colored background), BOS/sweeps (triangles), and signals (labels). Keep other indicators off for clarity.

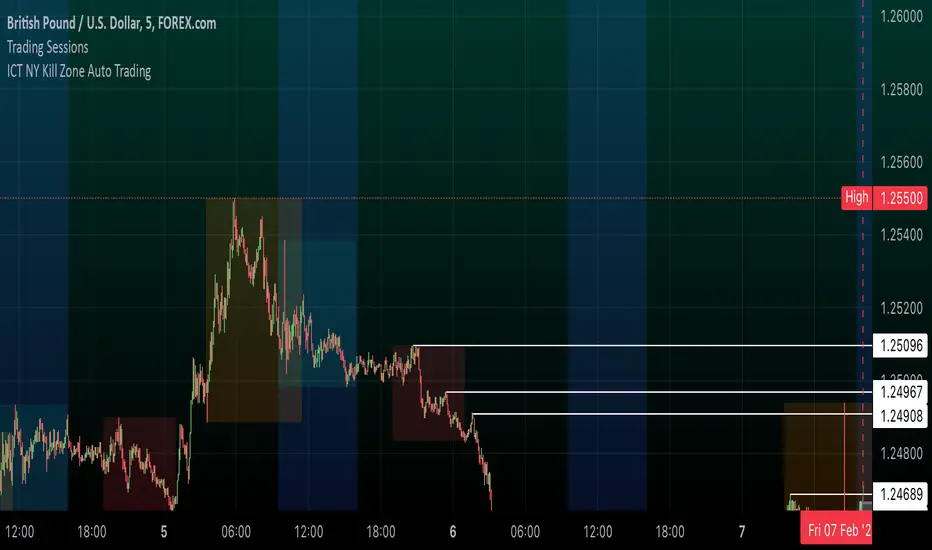

ICT NY Kill Zone Auto Trading### **ICT NY Kill Zone Auto Trading Strategy (5-Min Chart)**

#### **Overview:**

This strategy is based on Inner Circle Trader (ICT) concepts, focusing on the **New York Kill Zone**. It is designed for trading GBP/USD exclusively on the **5-minute chart**, automatically entering and exiting trades during the US session.

#### **Key Components:**

1. **Time Filter**

- The strategy only operates during the **New York Kill Zone (9:30 AM - 11:00 AM NY Time)**.

- It ensures execution only on the **5-minute timeframe**.

2. **Fair Value Gaps (FVGs) Detection**

- The script identifies areas where price action left an imbalance, known as Fair Value Gaps (FVGs).

- These gaps indicate potential liquidity zones where price may return before continuing in the original direction.

3. **Order Blocks (OBs) Identification**

- **Bullish Order Block:** Occurs when price forms a strong bullish pattern, suggesting further upside movement.

- **Bearish Order Block:** Identified when a strong bearish formation signals potential downside continuation.

4. **Trade Execution**

- **Long Trade:** Entered when a bullish order block forms within the NY Kill Zone and aligns with an FVG.

- **Short Trade:** Entered when a bearish order block forms within the Kill Zone and aligns with an FVG.

5. **Risk Management**

- **Stop Loss:** Fixed at **30 pips** to limit downside risk.

- **Take Profit:** Set at **60 pips**, providing a **2:1 risk-reward ratio**.

6. **Visual Aids**

- The **Kill Zone is highlighted in blue** to help traders visually confirm the active session.

**Objective:**

This script aims to **capitalize on institutional price movements** within the New York session by leveraging ICT concepts such as FVGs and Order Blocks. By automating trade entries and exits, it eliminates emotions and ensures a disciplined trading approach.

Turtle Soup Model [PhenLabs]📊 Turtle Soup Model

Version: PineScript™ v6

Description

The Turtle Soup Model is an innovative technical analysis tool that combines market structure analysis with inter-market comparison and gap detection. Unlike traditional structure indicators, it validates market movements against a comparison symbol (default: ES1!) to identify high-probability trading opportunities. The indicator features a unique “soup pattern” detection system, comprehensive gap analysis, and real-time structure breaks visualization.

Innovation Points:

First indicator to combine structure analysis with gap detection and inter-market validation

Advanced memory management system for efficient long-term analysis

Sophisticated pattern recognition with multi-market confirmation

Real-time structure break detection with comparative validation

🔧 Core Components

Structure Analysis: Advanced pivot detection with inter-market validation

Gap Detection: Sophisticated gap identification and classification system

Inversion Patterns: “Soup pattern” recognition for reversal opportunities

Visual System: Dynamic rendering of structure levels and gaps

Alert Framework: Multi-condition notification system

🚨 Key Features 🚨

The indicator provides comprehensive analysis through:

Structure Levels: Validated support and resistance zones

Gap Patterns: Identification of significant market gaps

Inversion Signals: Detection of potential reversal points

Real-time Comparison: Continuous inter-market analysis

Visual Alerts: Dynamic structure break notifications

📈 Visualization

Structure Lines: Color-coded for highs and lows

Gap Boxes: Visual representation of gap zones

Inversion Patterns: Clear marking of potential reversal points

Comparison Overlay: Inter-market divergence visualization

Alert Indicators: Visual signals for structure breaks

💡Example

📌 Usage Guidelines

The indicator offers multiple customization options:

Structure Settings:

Pivot Period: Adjustable for different market conditions

Comparison Symbol: Customizable reference market

Visual Style: Configurable colors and line widths

Gap Analysis:

Signal Mode: Choice between close and wick-based signals

Box Rendering: Automatic gap zone visualization

Middle Line: Reference point for gap measurements

✅ Best Practices:

🚨Use comparison symbol from related market🚨

Monitor both structure breaks and gap inversions

Combine signals for higher probability trades

Pay attention to inter-market divergences

⚠️ Limitations

Requires comparison symbol data

Performance depends on market correlation

Best suited for liquid markets

What Makes This Unique

Inter-market Validation: Uses comparison symbol for signal confirmation

Gap Integration: Combines structure and gap analysis

Soup Pattern Detection: Identifies specific reversal patterns

Dynamic Structure Management: Automatically updates and removes invalid levels

Memory-Efficient Design: Optimized for long-term chart analysis

🔧 How It Works

The indicator processes market data through three main components:

1. Structure Analysis:

Detects pivot points with comparison validation

Tracks structure levels with array management

Identifies and processes structure breaks

2. Gap Analysis:

Identifies significant market gaps

Processes gap inversions

Manages gap zones visualization

3. Pattern Recognition:

Detects “soup” patterns

Validates with comparison market

Generates structure break signals

💡 Note: The indicator performs best when used with correlated comparison symbols and appropriate timeframe selection. Its unique inter-market validation system provides additional confirmation for traditional structure-based trading strategies.

LRLR [TakingProphets]LRLR (Low Resistance Liquidity Run) Indicator

This indicator identifies potential liquidity runs in areas of low resistance, based on ICT (Inner Circle Trader) concepts. It specifically looks for a series of unmitigated swing highs in a downtrend that form without any bearish fair value gaps (FVGs) between them.

What is an LRLR?

- A Low Resistance Liquidity Run occurs when price creates a series of lower highs without any bearish fair value gaps in between

- The absence of bearish FVGs indicates there is no significant resistance in the area

- These formations often become targets for smart money to collect liquidity above the swing highs

How to Use the Indicator:

1. The indicator will draw a diagonal line connecting a series of qualifying swing highs

2. A small "LRLR" label appears to mark the pattern

3. These areas often become targets for future price moves, as they represent zones of accumulated liquidity with minimal resistance

Key Points:

- Minimum of 4 consecutive lower swing highs

- No bearish fair value gaps can exist between these swing highs

- The diagonal line helps visualize the liquidity run formation

- Can be used for trade planning and identifying potential reversal zones

Settings:

- Show Labels: Toggle the "LRLR" label visibility

- LRLR Line Color: Customize the appearance of the diagonal line

Best Practices:

1. Use in conjunction with other ICT concepts and market structure analysis

2. Pay attention to how price reacts when returning to these levels

3. Consider these areas as potential targets for smart money liquidity grabs

4. Most effective when used on higher timeframes (4H and above)

Note: This is an educational tool and should be used as part of a complete trading strategy, not in isolation.

Line Break Chart StrategyHello All!

We should not pass this year without a gift!

My last publication in 2024 is Complete Line Break Chart Strategy with many features!

What is Line Break Chart?

" Line Break is a Japanese chart style that disregards time intervals and only focuses on price movements, similar to the Kagi and Renko chart styles. Line Break charts form a series of up and down bars (referred to as lines). Up lines represent rising prices, and down lines represent falling prices. New confirmed lines only form on the chart when closing prices break the range covered by previous lines. Users can control the number of past lines used in the calculation via the "Number of Lines" input in the chart settings. The typical "Number of Lines" setting is 3, meaning the chart forms a new up line when the closing price is above the high prices of the last three lines, and it forms a new down line when the closing price is below the past three lines' low prices. If the current price is higher, it is an up line and if it is lower, it is a down line. If the current closing price is the same or the move in the opposite direction is not large enough to warrant a reversal, l then no new line is draw n" by Tradingview. You can find it here

Now let's start examining the features of the indicator:

By using Line break reversals it shows trend on the main chart. You can create alert .

Moreover, you can decide which trade should be taken by using Risk Management in the indicator. You can set the " Maximum Risk " and then if the risk is more than you set then the trade is not taken. When trend changed it checks the distance between reversal level and open price and compare it with the Maximum Risk

Breakout:

It can find breakouts and shows on the chart. You can create alert for breakouts

It can show breakouts on the main chart:

Flip-Flops:

Upon looking at set of price break charts, the trader will notice that there are instances when uptrend blocks is followed by one reversal block, and then by a reversal to a series of uptrend blocks. The opposite is also possible: a series of downtrend blocks is followed by one reversal box and then by an immediate reversal to downtrend. This price action is called a " Flip-Flop ". This structure usually produces trend continuation signal. when we see this then we better use Buy/Sell stop order. lets see this on the chart:

Temporal Sequence Table:

Sequence frequency shows the frequency distribution of the number of sequential highs and the number of sequential lows that have been generated. This is quite important to the trader who is seeking to join a trend or put on a trade when the price break reverses into a new trend direction. For example, if the pattern over the past year has been that there never were more than nine consecutive high closes, it would make sense not to enter a position late into the sequence of new high closes.

also you can see market structure. I have tried to formalize it and show it under the table. so you can understand if it's choppy market.

"Number of Lines" has very important role. While using low time frames such seconds/minutes time frame you may want to choose higher number of lines such 5,6. ( this may minimize the risk of a whipsaw )

Gaps feature:

You can set Gaps on/off. if Gaps on then you can see how long it takes for each box

Reversal and Continuation Probability:

The script calculated Reversal level and Continuation probability of the trend by using Sequence frequency.

It also shows unconfirmed box and current closing price level:

Last but not least it has Overlay option for all items, and can show all items in the main chart!

P.S. I added alerts :)

Wish you all a happy new year!

Enjoy!

Candle Range Theory | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Candle Range Theory Indicator! This powerful tool offers a strategy built around the Candle Range Theory, which analyzes market movements through the relative size and structure of price candles. For more information about the process, check the "HOW DOES IT WORK" section.

Features of the new Candle Range Theory Indicator :

Implementation of the Candle Range Theory

FVG & Order Block Entry Methods

2 Different TP / SL Methods

Customizable Execution Settings

Customizable Backtesting Dashboard

Alerts for Buy, Sell, TP & SL Signals

📌 HOW DOES IT WORK ?

The Candle Range Theory (CRT) indicator operates by identifying significant price movements through the relative size and structure of candlesticks. A key part of the strategy is determining large candles based on their range compared to the Average True Range (ATR) in a higher timeframe. Once identified, a breakout of either the high wick or the low wick of the large candle is required. This breakout is considered a liquidity grab. After that, the indicator waits for confirmation through Fair Value Gaps (FVGs) or Order Blocks (OBs). The confirmation structure must be the opposite direction of the breakout, for example if the high wick is broken, a bearish FVG is required for the short entry. After a confirmation signal is received, the indicator will trigger entry points based on your chosen entry method (FVG or OB), and exit points will be calculated using either a dynamic ATR-based TP/SL method or fixed percentages. Alerts for Buy, Sell, Take-Proft, and Stop-Loss are available.

🚩 UNIQUENESS

This indicator stands out because it combines two highly effective entry methods: Fair Value Gaps (FVGs) and Order Blocks (OBs). You can choose between these strategies depending on market conditions. Additionally, the dynamic TP/SL system uses the ticker's volatility to automatically calculate stop-loss and take-profit targets. The backtesting dashboard provides metrics about the performance of the indicator. You can use it to tune the settings for best use in the current tiker. The Candle Range Theory approach offers more flexibility compared to traditional indicators, allowing for better customization and control based on your risk tolerance.

⚙️ SETTINGS

1. General Configuration

Higher Timeframe: Customize the higher timeframe for analysis. Recommended combinations include M15 -> H4, H4 -> Daily, Daily -> Weekly, and Weekly -> Monthly.

HTF Candle Size: Define the size of the higher timeframe candles as Big, Normal, or Small to filter valid setups based on their range relative to ATR.

Entry Mode: Choose between FVGs and Order Blocks for your entry triggers.

Require Retracement: Enable this option if you want a retracement to the FVG or OB for entry confirmation.

Show HTF Candle Lines: Toggle to display the higher timeframe candle lines for better visual clarity.

2. Fair Value Gaps

FVG Sensitivity: You may select between Low, Normal, High or Extreme FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivities resulting in spotting bigger FVGs, and higher sensitivities resulting in spotting all sizes of FVGs.

3. Order Blocks

Swing Length: Swing length is used when finding order block formations. Smaller values will result in finding smaller order blocks.

4. TP / SL

TP / SL Method:

a) Dynamic: The TP / SL zones will be auto-determined by the algorithm based on the Average True Range (ATR) of the current ticker.

b) Fixed : You can adjust the exact TP / SL ratios from the settings below.

Dynamic Risk: The risk you're willing to take if "Dynamic" TP / SL Method is selected. Higher risk usually means a better winrate at the cost of losing more if the strategy fails. This setting is has a crucial effect on the performance of the indicator, as different tickers may have different volatility so the indicator may have increased performance when this setting is correctly adjusted.

HTF Inversion Fair Value Gap | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Higher Timeframe Inversion Fair Value Gaps (IFVG) indicator! Inversion Fair Value Gaps occur when a Fair Value Gap becomes invalidated. They reverse the role of the original Fair Value Gap, making a bullish zone bearish and vice versa. This indicator finds the latest IFVG in a higher timeframe and renders it in the current chart with it's divergence. For more information about the process, read the "HOW DOES IT WORK" section of the description.

Features of the new Higher Timeframe IFVG Indicator :

Renders The Higher Timeframe IFVG

Invalidation Borders

Variety Of Zone Detection / Sensitivity / Filtering / Invalidation Settings

High Customizability

🚩 UNIQUENESS

This indicator lets you take a look at the bigger picture by rendering the latest IFVG in a higher timeframe. You can see the current IFVG divergence to see how is the price action acting around the IFVG. You also can customize the FVG Filtering method, FVG & IFVG Zone Invalidation, Detection Sensitivity etc. according to your needs to get the best performance from the indicator.

📌 HOW DOES IT WORK ?

A Fair Value Gap generally occur when there is an imbalance in the market. They can be detected by specific formations within the chart. An Inversion Fair Value Gap is when a FVG becomes invalidated, thus reversing the direction of the FVG.

This indicator then renders the IFVG in a higher timeframe in your chart like this :

The opaque dashed lines at the top and the bottom of the IFVG indicate the bars that formed the original FVG. The middle dashed line that is semi-transparent shows the candlestick that invalidated the original FVG, thus created the current IFVG. The vertical solid top & bottom wicks indicate the current divergence of the highest & lowest points to the current IFVG.

The IFVGs can act as strong support & resistance points, depending on their creation volume and invalidation volume. Traders can use them for confirmation signals to their positions.

⚙️ SETTINGS

1. General Configuration

Higher Timeframe -> The higher timeframe to detect latest IFVG from. Keep in mind that his setting must be higher than the current timeframe.

IFVG Zone Invalidation -> Select between Wick & Close price for IFVG Zone Invalidation.

2. Fair Value Gaps

FVG Zone Invalidation -> Select between Wick & Close price for FVG Zone Invalidation.

Zone Filtering -> With "Average Range" selected, algorithm will find FVG zones in comparison with average range of last bars in the chart. With the "Volume Threshold" option, you may select a Volume Threshold % to spot FVGs with a larger total volume than average.

FVG Detection -> With the "Same Type" option, all 3 bars that formed the FVG should be the same type. (Bullish / Bearish). If the "All" option is selected, bar types may vary between Bullish / Bearish.

Detection Sensitivity -> You may select between Low, Normal or High FVG detection sensitivity. This will essentially determine the size of the spotted FVGs, with lower sensitivities resulting in spotting bigger FVGs, and higher sensitivities resulting in spotting all sizes of FVGs.

3. Dasboard

You can enable / disable the mitigation dashboard and customize it here.

4. Customization

Offset -> The number of candlesticks the IFVG will be rendered to the right of the latest bar.

Width -> The width of the rendered IFVG in candlesticks.

ICT HTF FVGs v2 (fadi)NOTICE: Instead of updating the existing ICT HTF FVGs indicator, this indicator is being published separately due to the requests to keep the original by some traders and because of the drastic change in behavior/configurations. If the original v1 version is more appropriate for your style of trading, feel free to continue to use it.

ICT HTF FVGs v2

In trading, Fair Value Gaps (FVGs) refer to market inefficiencies or imbalances that occur when buying and selling activities are not equal. These gaps can be identified on various timeframes and are used in different trading strategies.

FVGs are crucial in price action trading as they highlight the difference between the current market price of an asset and its fair value. Traders use these gaps to identify potential trading opportunities, as they often indicate areas where the market may correct itself

This indicator will overlap the higher timeframe (HTF) FVGS over the current timeframe to help traders anticipate and plan their trades.

Features

Up to 6 higher timeframes (HTF) can be overlayed on a chart

Traders can limit the number of HTF FVGs to preset number of HTFs

Lower and current timeframes can be included

Configurable spacing of HTF FVGs to prevent overlapping

Configurable Smart Expansion of FVGs based on proximity to current price

Traders can decide what constitutes a Mitigated FVG

Show or hide mitigated FVGs to declutter the chart

Flexible display settings that controls how the FVGs are displayed

Flexible labeling of the FVG levels and content

Higher Timeframes Display Settings

This indicator provides the ability to select up to 6 HTF intervals. These intervals are based on the trader's timeframes including any custom timeframes.

Timeframe Configurations

Enable or Disable a Timeframe

The Timeframe to Display

Bullish / BISI FVG Color

Bearish / SIBI FVG Color

The number of FVGs For The Selected Timeframe

Limit to the next HTFs only can be used to display the selected number of HTF FVGs. For example, if the trader selects 3 then only 3 HTF FVGs will be displayed.

Note: If either of the next two options is selected, they will take up spots from this count.

Hide lower Timeframes restricts the FVGs to higher timeframes only. If this option is disabled, it will show lower timeframes FVGs as well.

Hide Current Timeframe removes current timeframe from the selected list of HTF FVGs. If this option is disabled, it will show current timeframe FVGs as well.

Background Transparency Enable or disable the background color (shaded area) of the FVG. If it is enabled, it will set the transparency amount. The higher the value, the more transparent the background.

Extend lines controls when and how to extend the FVG levels. There are three options:

Extension Only extends the FVGs by the specified number provided below only.

Current Candle Plus Extension extends all the FVGs beyond the current candle by the number provided below.

When in Range will only extend the FVGs near current price based on the advanced settings below. This setting will use Average True Range multiplier to calculate the range (shows FVGs that are higher or lower by the average candle size multiplied by the number in Advanced section).

Mitigated shows or hides the mitigated HTF FVGs. A FVG is considered mitigated based on one of the following options:

None will ignore mitigation and show all FVGs.

Touched when a HTF FVG is touched regardless of how deep the price get inside the FVG.

Wick filled the FVG is closed by a wick or body of a candle.

Body filled the FVG is closed by the body of a candle

Wick filled half a candle's wick or body has reached the C.E. of the FVG

Body filled half a candle body has reached the C.E. of the FVG

Extend mitigated lines sets the number of candles to extend the mitigated FVG levels by for better visibility.

Important Note: Mitigation is calculated based on the timeframe of the FVG, not current timeframe.

Display

Display settings focus on how the FVGs will be displayed. The trader is in total control and there are multiple ways to overlay FVGs on the chart.

Open / Close / C.E. / Link controls the borders. Traders can enable or disable any of them as well as set the thickness and style. Link is the right border.

C.E. also offers the option of setting the bullish (BISI) and bearish (SIBI) colors of the C.E. level

Labeling controls if the labels should be displayed next to the FVG, their color, background, and font size.

Label levels to display controls which levels to show. Open, High. or the C.E.

Label display content controls what to show in the labels, the timeframe of the label, is it a BISI or a SIBI, and a label to indicate if it is the Open or the Close.

Note: if the distance between the open and close has the potential of overlapping the labels, then the indicator will only show the C.E. label for visual clarity.

Advanced Settings

Advanced settings controls some internal calculations:

Proximity factor based on daily range used to calculate possible range of FVGs within a day's range to keep the chart clean. The higher the value, the more FVGs will be shown.

Combine labels factor for visibility used to calculate the distance between the open and close and if all the labels or only the C.E. should be displayed. The higher the value, the bigger the distance for combination (smaller numbers will show more labels).

Range should be within X candles used when "When in Range" option is selected. This is the ATR multiplier used to extend the FVGs. The higher the number, the more FVGs will be extended.

Once desired settings have been achieved, the settings can be saved as default from the bottom left of the indicator settings page for future use.

FVG (ICT) with Swing LevelsThis indicator, called "Fair Value Gaps (ICT) with Swing Levels", overlays on the main chart and does the following:

Initial Setup:

It defines user-adjustable parameters:

lookback: Lookback period to keep FVGs visible.

swingPeriod: Period for calculating swing highs and lows.

bullColor and bearColor: Colors for bullish and bearish FVGs.

Fair Value Gaps (FVGs) Detection:

Uses a function to identify FVGs by comparing candle high and low prices.

A bullish FVG forms when the low of two candles ago is higher than the high of the current candle.

A bearish FVG forms when the high of two candles ago is lower than the low of the current candle.

Swing Levels Calculation:

Calculates swing highs and lows over the specified period.

These swing levels define the current market range.

Current Range Verification:

Implements a function to check if an FVG is within the range defined by swing levels.

This ensures only the most relevant FVGs for the current market situation are displayed.

FVG Drawing:

When it detects an FVG (bullish or bearish) within the current range, it draws a box on the chart.

Boxes extend from the bar where the FVG formed to the current bar.

Bullish FVGs are drawn in green and bearish in red (colors are customizable).

Old FVGs Management:

On each new bar, the indicator checks all existing FVG boxes.

It removes boxes that are outside the specified lookback period.

It also removes boxes that are no longer within the current range of swing levels.

Swing Levels Visualization:

Draws lines on the chart to show swing highs (in blue) and swing lows (in purple).

These lines help visualize the current market range.

Continuous Update:

The indicator updates on each new candle, constantly refreshing FVGs and swing levels.

In summary, this indicator identifies and visualizes Fair Value Gaps according to the ICT methodology, filtering them based on higher timeframe swing levels. This helps traders focus on the most significant FVGs within the current market context, reducing visual noise and potentially improving trading decision-making.

FVG & IFVG ICT [TradingFinder] Inversion Fair Value Gap Signal🔵 Introduction

🟣 Fair Value Gap (FVG)

To spot a Fair Value Gap (FVG) on a chart, you need to perform a detailed candle-by-candle analysis.

Here’s the process :

Focus on Candles with Large Bodies : Identify a candle with a substantial body and examine it alongside the preceding candle.

Check Surrounding Candles : The candles immediately before and after the central candle should have long shadows.

Ensure No Overlap : The bodies of the candles before and after the central candle should not overlap with the body of the central candle.

Determine the FVG Range : The gap between the shadows of the first and third candles forms the FVG range.

🟣 ICT Inversion Fair Value Gap (IFVG)

An ICT Inversion Fair Value Gap, also known as a reverse FVG, is a failed fair value gap where the price does not respect the gap. An IFVG forms when a fair value gap fails to hold the price and the price moves beyond it, breaking the fair value gap.

This marks the initial shift in price momentum. Typically, when the price moves in one direction, it respects the fair value gaps and continues its trend.

However, if a fair value gap is violated, it acts as an inversion fair value gap, indicating the first change in price momentum, potentially leading to a short-term reversal or a subsequent change in direction.

🟣 Bullish Inversion Fair Value Gap (Bullish IFVG)

🟣 Bearish Inversion Fair Value Gap (Bearish IFVG)

🔵 How to Use

🟣 Identify an Inversion Fair Value Gap

To identify an IFVG, you first need to recognize a fair value gap. Just as fair value gaps come in two types, inversion fair value gaps also fall into two categories:

🟣 Bullish Inversion Fair Value Gap

A bullish IFVG is essentially a bearish fair value gap that is invalidated by the price closing above it.

Here’s how to identify it :

Identify a bearish fair value gap.

When the price closes above this bearish fair value gap, it transforms into a bullish inversion fair value gap.

This gap acts as support for the price and drives it upwards, indicating a reduction in sellers' strength and an initial shift in momentum towards buyers.

🟣 Bearish Inversion Fair Value Gap

A bearish IFVG is primarily a bullish fair value gap that fails to hold the price, with the price closing below it.

Here’s how to identify it :

Identify a bullish fair value gap.

When the price closes below this gap, it becomes a bearish inversion fair value gap.

This gap acts as resistance for the price, pushing it downwards. A bearish inversion fair value gap signifies a decrease in buyers' momentum and an increase in sellers' strength.

🔵 Setting

🟣 Global Setting

Show All FVG : If it is turned off, only the last FVG will be displayed.

S how All Inversion FVG : If it is turned off, only the last FVG will be displayed.

FVG and IFVG Validity Period (Bar) : You can specify the maximum time the FVG and the IFVG remains valid based on the number of candles from the origin.

Switching Colors Theme Mode : Three modes "Off", "Light" and "Dark" are included in this parameter. "Light" mode is for color adjustment for use in "Light Mode".

"Dark" mode is for color adjustment for use in "Dark Mode" and "Off" mode turns off the color adjustment function and the input color to the function is the same as the output color.

🟣 Logic Setting

FVG Filter

When utilizing FVG filtering, the number of identified FVG areas undergoes refinement based on a specified algorithm. This process helps to focus on higher quality signals and eliminate noise.

Here are the types of FVG filters available :

Very Aggressive Filter : Introduces an additional condition to the initial criteria. For an upward FVG, the highest price of the last candle must exceed the highest price of the middle candle. Similarly, for a downward FVG, the lowest price of the last candle should be lower than the lowest price of the middle candle. This mode minimally filters out FVGs.

Aggressive Filter : Builds upon the Very Aggressive mode by considering the size of the middle candle. It ensures the middle candle is not too small, thereby eliminating more FVGs compared to the Very Aggressive mode.

Defensive Filter : In addition to the conditions of the Very Aggressive mode, the Defensive mode incorporates criteria regarding the size and structure of the middle candle. It requires the middle candle to have a substantial body, with specific polarity conditions for the second and third candles relative to the first candle's direction. This mode filters out a significant number of FVGs, focusing on higher-quality signals.

Very Defensive Filter : Further refines filtering by adding conditions that the first and third candles should not be small-bodied doji candles. This stringent mode eliminates the majority of FVGs, retaining only the highest quality signals.

Mitigation Level FVG and IFVG : Its inputs are one of "Proximal", "Distal" or "50 % OB" modes, which you can enter according to your needs. The "50 % OB" line is the middle line between distal and proximal.

🟣 Display Setting

Show Bullish FVG : Enables the display of demand-related boxes, which can be toggled on or off.

Show Bearish FVG : Enables the display of supply-related boxes along the path, which can also be toggled on or off.

Show Bullish IFVG : Enables the display of demand-related boxes, which can be toggled on or off.

Show Bearish IFVG : Enables the display of supply-related boxes along the path, which can also be toggled on or off.

🟣 Alert Setting

Alert FVG Mitigation : If you want to receive the alert about FVG's mitigation after setting the alerts, leave this tick on. Otherwise, turn it off.

Alert Inversion FVG Mitigation : If you want to receive the alert about Inversion FVG's mitigation after setting the alerts, leave this tick on. Otherwise, turn it off.

Message Frequency : This parameter, represented as a string, determines the frequency of announcements. Options include: 'All' (triggers the alert every time the function is called), 'Once Per Bar' (triggers the alert only on the first call within the bar), and 'Once Per Bar Close' (activates the alert only during the final script execution of the real-time bar upon closure). The default setting is 'Once per Bar'.

Show Alert time by Time Zone : The date, hour, and minute displayed in alert messages can be configured to reflect any chosen time zone. For instance, if you prefer London time, you should input 'UTC+1'. By default, this input is configured to the 'UTC' time zone.

Display More Info : The 'Display More Info' option provides details regarding the price range of the order blocks (Zone Price), along with the date, hour, and minute. If you prefer not to include this information in the alert message, you should set it to 'Off'.

RSI TrendsThis TradingView script combines RSI trend analysis with FVG (Fair Value Gap) detection to identify potential buy and sell opportunities in financial markets. The script is customizable and provides extensive visual feedback directly on the chart, enhancing both strategic entry and exit points for traders. Raw code of FVG was taken from LuxAlgo

Features

FVG Detection: Identifies Fair Value Gaps (FVG), and provides options to display these gaps based on user settings.

RSI Trend Bars: Utilizes the Relative Strength Index (RSI) to paint bars indicating overbought and oversold conditions. This helps traders understand current market sentiment and potential reversal points.

Customizable Settings: Users can customize the timeframe, FVG types, and RSI thresholds. This flexibility allows the script to be adapted to various trading styles and timeframes.

Historical Analysis: Option to display or hide historical FVGs, helping users analyze past market behavior without cluttering the chart.

Alert System: Integrated alerts for detected buy and sell signals based on RSI conditions and the presence or absence of FVGs. This feature notifies traders of potential trading opportunities.

Trading Signals

Buy, Buy+, and Buy++ Signals: These signals are triggered based on overbought conditions without corresponding bearish FVG presence, with increasing stringency for higher tiers of buy signals.

Sell, Sell+, and Sell++ Signals: These signals are based on oversold conditions devoid of bullish FVG presence, with each subsequent plus sign indicating a higher level of confirmation required to trigger the signal.

Use Case

Ideal for traders who rely on technical analysis and are looking for an automated way to spot potential buy and sell points using both price action gaps and momentum indicators.

Customization

All input parameters are adjustable directly from the indicator's settings panel, making it easy to tailor the tool to your trading needs and preferences.

lib_fvgLibrary "lib_fvg"

further expansion of my object oriented library toolkit. This lib detects Fair Value Gaps and returns them as objects.

Drawing them is a separate step so the lib can be used with securities. It also allows for usage of current/close price to detect fill/invalidation of a gap and to adjust the fill level dynamically. FVGs can be detected while forming and extended indefinitely while they're unfilled.

method draw(this)

Namespace types: FVG

Parameters:

this (FVG)

method draw(fvgs)

Namespace types: FVG

Parameters:

fvgs (FVG )

is_fvg(mode, precondition, filter_insignificant, filter_insignificant_atr_factor, live)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

precondition (bool) : allows for other confluences to block/enable detection

filter_insignificant (bool) : allows to ignore small gaps

filter_insignificant_atr_factor (float) : allows to adjust how small (compared to a 50 period ATR)

live (bool) : allows to detect FVGs while the third bar is forming -> will cause repainting

Returns: a tuple of (bar_index of gap bar, gap top, gap bottom)

create_fvg(mode, idx, top, btm, filled_at_pc, config)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

idx (int) : the bar_index of the FVG gap bar

top (float) : the top level of the FVG

btm (float) : the bottom level of the FVG

filled_at_pc (float) : the ratio (0-1) that the fill source needs to retrace into the gap to consider it filled/invalidated/ready for removal

config (FVGConfig) : the plot configuration/styles for the FVG

Returns: a new FVG object if there was a new FVG, else na

detect_fvg(mode, filled_at_pc, precondition, filter_insignificant, filter_insignificant_atr_factor, live, config)

Parameters:

mode (int) : switch for detection 1 for bullish FVGs, -1 for bearish FVGs

filled_at_pc (float)

precondition (bool) : allows for other confluences to block/enable detection

filter_insignificant (bool) : allows to ignore small gaps

filter_insignificant_atr_factor (float) : allows to adjust how small (compared to a 50 period ATR)

live (bool) : allows to detect FVGs while the third bar is forming -> will cause repainting

config (FVGConfig)

Returns: a new FVG object if there was a new FVG, else na

method update(this, fill_src)

Namespace types: FVG

Parameters:

this (FVG)

fill_src (float) : allows for usage of different fill source series, e.g. high for bearish FVGs, low vor bullish FVGs or close for both

method update(all, fill_src)

Namespace types: FVG

Parameters:

all (FVG )

fill_src (float)

method remove_filled(unfilled_fvgs)

Namespace types: FVG

Parameters:

unfilled_fvgs (FVG )

method delete(this)

Namespace types: FVG

Parameters:

this (FVG)

method delete_filled_fvgs_buffered(filled_fvgs, max_keep)

Namespace types: FVG

Parameters:

filled_fvgs (FVG )

max_keep (int) : the number of filled, latest FVGs to retain on the chart.

FVGConfig

Fields:

box_args (|robbatt/lib_plot_objects/36;BoxArgs|#OBJ)

line_args (|robbatt/lib_plot_objects/36;LineArgs|#OBJ)

box_show (series__bool)

line_show (series__bool)

keep_filled (series__bool)

extend (series__bool)

FVG

Fields:

config (|FVGConfig|#OBJ)

startbar (series__integer)

mode (series__integer)

top (series__float)

btm (series__float)

center (series__float)

size (series__float)

fill_size (series__float)

fill_lvl_target (series__float)

fill_lvl_current (series__float)

fillbar (series__integer)

filled (series__bool)

_fvg_box (|robbatt/lib_plot_objects/36;Box|#OBJ)

_fill_line (|robbatt/lib_plot_objects/36;Line|#OBJ)

Fair Value Gap Finder with Integrated Gann BoxTitle: Fair Value Gap Finder with Integrated Gann Box Analysis

Description:

The "Fair Value Gap Finder with Integrated Gann Box Analysis" is a unique technical indicator designed for traders who wish to incorporate the concepts of Fair Value Gaps (FVG) and Gann Box methodologies into their trading strategy. This tool is beneficial for both trend-following and scalping techniques across various markets and timeframes.

Functionality:

The indicator identifies Fair Value Gaps, which are areas on the chart where price has skipped a range, creating a 'gap'. Recognizing these zones can be crucial for understanding potential price support and resistance areas. Alongside FVG detection, this script employs Gann Box principles to project potential levels of interest. Gann Boxes are drawn automatically when an FVG is identified, providing additional insights based on W.D. Gann's theories, which relate to time and price symmetry.

Usage:

Upon detecting an FVG, the indicator will highlight the gap on the chart and overlay a Gann Box between the high and low points of the gap. Traders can use these zones to make informed decisions about entry and exit points, stop loss, and take profit levels. The script offers customization options for the appearance and behavior of the FVG boxes and Gann Lines, allowing users to adapt the tool to their preferences.

Originality:

What sets this indicator apart is the integration of FVG with Gann Box levels within a single tool, streamlining the analysis process. It takes the classic approach of identifying gaps and enriches it with the geometric significance of Gann's work, all while allowing users to visualize and interact with these levels in a user-friendly manner.

Open-Source Nature:

This script is open-source, making it a transparent solution for those who wish to understand the underlying calculations. While not all traders are versed in Pine Script, the logic of identifying FVGs and applying Gann Box levels is explained through the script's annotations and the user interface itself.

Instructions for Use:

Apply the script to your chart, and it will automatically detect FVGs.

Adjust the settings in the indicator's input menu to match your trading style and preferences.

Use the FVG and Gann Box levels as potential areas of interest for trade setups.

This script does not guarantee profits and should be used as part of a comprehensive trading plan. It is best used in conjunction with other analysis methods to confirm signals and strategies.

TrendFriendOverview

TrendFriend (TF) combines various technical analysis components, including trend calculations, moving averages, RSI signals, and Fair Value Gaps (FVG) detection to determine trend reversal and continuation points. The FVG feature identifies potential consolidation periods and displays mitigation levels.

Features

Trend Analysis: Utilizes short and long-term Running Moving Averages (RMA) to identify trends.

Average True Range (ATR): Plots ATR to depict market volatility.

RSI Signals: Calculates RSI and provides buy/sell signals based on RSI conditions.

Fair Value Gaps (FVG): Detects FVG patterns and offers options for customization, including dynamic FVG, mitigation levels, and auto threshold.

Usage

Buy Signals: Generated based on pullback conditions, contra-buy signals, and crossovers of specified moving averages.

Sell Signals: Generated based on pullback conditions, contra-sell signals, and crossunders of specified moving averages.

Visualization: FVG areas are visually represented on the chart, and unmitigated levels can be displayed.

Configuration

Adjustable parameters for trend periods, ATR length, RSI settings, FVG threshold, and display preferences.

Dynamic FVG detection and mitigation level visualization can be enabled/disabled.

Usage Example

Trend Analysis: Identify trends with short and long-term moving averages.

RSI Signals: Interpret RSI signals for potential reversals.

FVG Detection: Visualize Fair Value Gaps and mitigation levels on the chart.

Buy/Sell Signals: Receive alerts for buy/sell signals based on specified conditions.

Disclaimer

This Pine Script code is subject to the terms of the Mozilla Public License 2.0. Use this code at your own risk, and always conduct additional analysis before making trading decisions.

Author

Author: devoperator84

License: Mozilla Public License 2.0

Liquidity Voids (FVG) [LuxAlgo]The Liquidity Voids (FVG) indicator is designed to detect liquidity voids/imbalances derived from the fair value gaps and highlight the distribution of the liquidity voids at specific price levels.

Fair value gaps and liquidity voids are both indicators of sell-side and buy-side imbalance in trading. The only difference is how they are represented in the trading chart. Liquidity voids occur when the price moves sharply in one direction forming long-range candles that have little trading activity, whilst a fair value is a gap in price.

🔶 USAGE

Liquidity can help you to determine where the price is likely to head next. In conjunction with higher timeframe market structure, and supply and demand, liquidity can give you insights into potential price movement. It's essential to practice using liquidity alongside trend analysis and supply and demand to read market conditions effectively.

The peculiar thing about liquidity voids is that they almost always fill up. And by “filling”, we mean the price returns to the origin of the gap. The reason for this is that during the gap, an imbalance is created in the asset that has to be made up for. The erasure of this gap is what we call the filling of the void. And while some voids waste no time in filling, some others take multiple periods before they get filled.

🔶 SETTINGS

The script takes into account user-defined parameters and detects the liquidity voids based on them, where detailed usage for each user-defined input parameter in indicator settings is provided with the related input's tooltip.

🔹 Liquidity Detection

Liquidity Voids Threshold: Act as a filter while detecting the Liquidity Voids. When set to 0 basically means no filtering is applied, increasing the value causes the script to check the width of the void compared to a fixed-length ATR value

Bullish: Color customization option for Bullish Liquidity Voids

Bearish: Color customization option for Bearish Liquidity Voids

Labels: Toggles the visibility of the Liquidity Void label

Filled Liquidity Voids: Toggles the visibility of the Filled Liquidity Voids

🔹 Display Options

Mode: Controls the lookback length of detection and visualization

# Bars: Lookback length customization, in case Mode is set to Present

🔶 RELATED SCRIPTS

Buyside-Sellside-Liquidity

Fair-Value-Gaps

Opening Range Gap + Std Dev [starclique]The ICT Opening Range Gap is a concept taught by Inner Circle Trader and is discussed in the videos: 'One Trading Setup For Life' and 2023 ICT Mentorship - Opening Range Gap Repricing Macro

ORGs, or Opening Range Gaps, are gaps that form only on the Regular Trading Hours chart.

The Regular Trading Hours gap occurs between 16:15 PM - 9:29 AM EST (UTC-4)

These times are considered overnight trading, so it is useful to filter the PA (price action) formed there.

The RTH option is only available for futures contracts and continuous futures from CME Group.

To change your chart to RTH, first things first, make sure you’re looking at a futures contract for an asset class, then on the bottom right of your chart, you’ll see ETH (by default) - Click on that, and change it to RTH.

Now your charts are filtering the price action that happened overnight.

To draw out your gap, use the Close of the 4:14 PM candle and the open of the 9:30 AM candle.

How is this concept useful?

Well, It can be used in many ways.

---

How To Use The ORG

One of the ways you can use the opening range gap is simply as support and resistance

If we extend out the ORG from the example above, we can see that there is a clean retest of the opening range gap high after breaking structure to the upside and showing acceptance outside of the gap after consolidating within it.

The ORG High (4:14 Candle Close in this case) was used as support.

We then see an expansion to the upside.

Another way to implement the ORG is by using it as a draw on liquidity (magnet for price)

In this example, if we looked to the left, there was a huge ORG to the downside, leaving a massive gap.

The market will want to rebalance that gap during the regular trading hours.

The market rallies higher, rejects, comes down to clear the current days ORG low, then closes.

That is one example of how you can combine liquidity & ICT market structure concepts with Opening Range Gaps to create a story in the charts.

Now let’s discuss standard deviations.

---

Standard Deviations

Standard Deviations are essentially projection levels for ranges / POIs (Point of Interests)

By this I mean, if you have a range, and you would like to see where it could potentially expand to, you’d place your fibonacci retracement tool on and high and low of the range, then use extension levels to find specific price points where price might reject from.

Since 0 and 1 are your Range High and Low respectively, your projection levels would be something like 1.5, 2, 2.5, and 3, for the extension from your 1 Fib Level, and -0.5, -1, -1.5, and -2 for your 0 Fib level.

The -1 and 2 level produce a 1:1 projection of your range low and high, meaning, if you expect price to expand as much as it did from the range low to range high, then you can project a -1 and 2 on your Fib, and it would show you what ICT calls “symmetrical price”

Now, how are standard deviations relevant here?

Well, if you’ve been paying attention to ICT’s recent videos, you would’ve caught that he’s recently started using Standard Deviation levels on breakers.

So my brain got going while watching his video on ORGs, and I decided to place the fib on the ORG high and low and see what it’d produce.

The results were very interesting.

Using this same example, if we place our fib on the ORG High and Low, and add some projection levels, we can see that we rejected right at the -2 Standard Deviation Level.

---

You can see that I also marked out the EQ (Equilibrium, 50%, 0.5 of Fib) of the ORG. This is because we can use this level as a take profit level if we’re using an old ORG as our draw.

In days like these, where the gap formed was within a consolidation, and it continued to consolidate within the ORG zone that we extended, we can use the EQ in the same way we’d use an EQ for a range.

If it’s showing acceptance above the EQ, we are bullish, and expect the high of the ORG to be tapped, and vice versa.

---

Using The Indicator

Here’s where our indicator comes in play.

To avoid having to do all this work of zooming in and marking out the close and open of the respective ORG candles, we created the Opening Range Gap + Standard Deviations Indicator, with the help of our dedicated Star Clique coder, a1tmaniac.

With the ORG + STD DEV indicator, you will be able to view ORG’s and their projections on the ETH (Electronic Trading Hours) chart.

---

Features

Range Box

- Change the color of your Opening Range Gap to your liking

- Enable or disable the box from appearing using the checkbox

Range Midline

- Change the color of your Opening Range Gap Equilibrium

- Enable or disable the midline from appearing using the checkbox

Std. Dev

- Add whichever standard deviation levels you’d like.

- By default, the indicator comes with 0.5, 1, 1.5, and 2 standard deviation levels.

- Ensure that you add a comma ( , ) in between each standard deviation level

- Enable or disable the standard deviations from appearing using the opacity of the color (change to 0%)

Labels / Offset

- Adjust the offset of the label for the Standard Deviations

- Enable or disable the Labels from appearing using the checkbox

Time

- Adjust the time used for the indicators range

- If you’d like to use this for a Session or ICT Killzone instead, adjust the time

- Adjust the timezone used for the time referenced

- Options are UTC, US (UTC-4, New York Local Time) or UK (UTC+1, London Time)

- By default, the indicator is set to US

Price & Volume Profile (Expo)█ Overview

The Price & Volume Profile provides a holistic perspective on market dynamics by simultaneously tracking price action and trading volume across a range of price levels. So it is not only a volume-based indicator but also a price-based one. In addition to illustrating volume distribution, it quantifies how frequently the price has fallen within a particular range, thus offering a holistic perspective on market dynamics.

This unique and comprehensive approach to market analysis by considering both price action and trading volume, two crucial dimensions of market activity. Its distinctive methodology offers several advantages:

Holistic Market View: By simultaneously tracking the frequency of specific price ranges (Price Profile) and the volume traded at those ranges (Volume Profile), this indicator provides a more complete picture of market behavior. It shows not only where the market is trading but also how much it's trading, reflecting both price acceptance levels and market participation intensity.

Point of Control (POC): The POC, as highlighted by this indicator, serves as a significant reference point for traders. It identifies the price level with the highest trading activity, thus indicating a strong consensus among market participants about the asset's fair value. Observing how price interacts with the POC can offer valuable insights into market sentiment and potential trend reversals.

Support and Resistance Levels: Price levels with high trading activity often act as support or resistance in future price movements. The indicator visually represents these levels, enabling traders to anticipate potential price reactions.

Price Profile

Price and Volume Profile

█ Calculations

The algorithm analyzes both trade frequency and volume across different price levels. It identifies these levels within the visible chart range, then examines each bar to determine if the selected price falls within these levels. If so, it increases a counter and adds the trading volume. This process repeats across the visible range and is visualized as a horizontal histogram, each bar representing a price level and the bar length reflecting trade frequency and volume. Additionally, it calculates the Point of Control (POC), signifying the price level with the highest activity.

In summary: The histogram presents a dual perspective - not only the traded volume at each price level but also the frequency of the price hitting each range. The longer the bar, the more times the price has frequented that specific range, revealing key insights into price behavior and acceptance levels. These frequently visited areas often emerge as strong support or resistance zones, helping traders navigate market movements.

Please note that the indicator adjusts to the visible price range, making it adaptable to changing market conditions. This dynamic analysis can provide more relevant and timely information than static indicators.

█ How to use

This indicator is beneficial for traders as it offers insights into the distribution of trading activity across different price levels. It helps identify key areas of support and resistance and gives a visual representation of market sentiment and liquidity.

The point of control (POC) , which is the price level with the highest traded volume or frequency count, becomes even more crucial in this context. It marks the price at which the most trading activity occurred, signaling a strong consensus among market participants about the asset's fair value. If the market price deviates significantly from the POC, it could suggest an overbought or oversold condition, potentially leading to a price reversion.

Fair Price Areas/gaps are specific price levels or zones where an asset has spent limited time in the past. These areas are considered interesting or significant because they may have an impact on future price action.

Similar to the concept of fair value gaps, which refers to discrepancies between an asset's market price and its estimated intrinsic value, Fair Price Areas/gaps focus on price levels that have been relatively underutilized in terms of trading activity. When an asset's price reaches a Fair Price Area/gap, traders and investors pay attention because they expect the price to react in some way. The rationale behind this concept is that price tends to gravitate towards areas where it has spent less time in the past, as the market perceives them as significant levels.

█ Settings

The indicator is customizable, allowing users to define the number of price levels (rows), the offset, the data source, and whether to display volume or frequency count. It also adjusts dynamically to the visible price range on the chart, ensuring that the analysis remains relevant and timely with changing market conditions.

Source: The price to use for the calculation. Typically, this is the closing price. By considering the user-selected Source (typically the closing price), the indicator determines the frequency with which the price lands within each designated price level (row) over the selected period. In essence, the indicator provides a count of bars where the Source price falls within each range, essentially creating a "Price Profile."

Row Size: The number of price levels (rows) to divide the visible price range into.

Display: Choose whether to display the number of bars ("Counter") or the total volume ("Volume") for each price level.

Offset: The distance of the histogram from the price chart.

Point of Control (POC): If enabled, the indicator will highlight the price level with the most activity.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Displacement (Two FVGs)A simple indicator that attempts to identify displacement in price by alerting you when two simultaneous Fair Value Gaps (FVGs) occur.

When two fair value gaps occur, the indicator will print a green bar (if bullish) or a red bar (if bearish). If you right click on the indicator you can turn on alerts that will pop up every time a dual FVG occurs.

Fair Value Gaps are most commonly used amongst price action traders and are defined as instances in which there are inefficiencies, or imbalances, in the market.

The concept for this indicator is very simple. Apply it to your chart and enable alerts on the instruments and timeframe you trade. When you get an alert, it could indicate larger players getting involved.

This is NOT a trading strategy. Its intention is to save time by alerting you to large imbalances in price on the instruments you trade.

FVG Sessions [LuxAlgo]The FVG Sessions indicator highlights the first fair value gap of the trading session as well as the session range. Detected fair value gaps extend to the end of the trading session.

Alerts are included on the formation of a session fair value gap, price being within a session fair value gap, mitigations, and price crossing session fair value gaps average.

🔶 USAGE

Trader ICT states that the first fair value gap of the trading session can attract the most significant reaction. Having only one FVG per session allows users to further focus on that precise imbalance as well as external elements.

The mitigation of a fair value gap is clearly indicated on the chart with a more transparent color allowing users to see inverse FVGs.

Extending the fair value gaps allows the imbalance area to provide potential support and resistance.

Do note that this script should be used on intraday charts.

🔶 ALERTS

The script includes the following alerts:

🔹 Bullish/Bearish FVG

Alerts on the formation of the first bullish or bearish FVG of the session.

🔹 Bullish/Bearish FVG Mitigation

Alerts when the first bullish or bearish FVG of the session is mitigated.

🔹 Price Within FVG

Alerts when price is within the first bullish or bearish FVG area of the session.

🔹 Price Cross FVG Average

Alerts when price cross the average level of the first bullish or bearish FVG of the session.

FVGs & CEs + Alerts: simple & efficient methodFair Value Gap indicator: Paints FVGs and their midlines (CEs). Stops painting when CE is hit, or when fully filled; user choice of threshold. This threshold is also used in the Alert conditions.

~~Plotted here on ES1! (CME), on the 15m timeframe~~

-A FVG represents a 'naked' body where the wicks/tails on either side do not meet. This can be seen as a type of 'gap', which price will have a tendency to want to re-fill (in part or in full).

-The midline (CE, or 'Consequent encroachment') of FVGs also tend to show price sensitivity.

-This indicator paints all FVGs until priced into, and should give an idea of which are more meaningful and which are best ignored (based on context: location, Time of day, market structure, etc).

-This is a simpler and more efficient method of painting Fair value gaps which auto-stop painting when price reaches them.

//Aims of Publishing:

-Education of ICT concepts of Fair Value Gaps and their midlines (CEs): To easily see via forward testing or backtesting, the sensitivity that price shows to these areas & levels.

-Demonstration of a much more efficient way of plotting FVGs which terminate at price, thanks to a modification of @Bjorgums's clever looping method referenced below.

//Settings:

-Toggle on/off upward and downward FVGs independently(blue and orange by default).

-Toggle on/off midline (CE).

-Standard color/line formatting options.

-Choose Threshold: CE of FVG or Full Fill of FVG: This will determine both the 'stop-painting' trigger and the 'Alert' trigger.

-Choose number of days lookback to control how many historical FVGs paint on chart.

//On alerts:

-Simple choice of 2 alerts:

~~One for price crossing into/above the nearest untouched 'premium' FVG above ( orange ). Trigger is user choice of CE or full fill.

~~Another for price crossing into/below the nearest untouched 'discount' FVG below (blue). Trigger is user choice of CE or full fill.

-Alerts set via the three dots in indicator status line.

//Cautionary notes:

-Do not use the alerts blindly to find trades. Wait until you have identified a good FVG above/below which you think price may show sensitivity to

-Usage on very low timeframes can cause unexpected results with alerts: due to new FVGs forming in realtime the Alert will always trigger at the most recent FVG above/ below having its threshold hit.

-Big thank you to @Bjorgum for his fantastic extendAndRemove method. Modified here for use with boxes and to integrate Alerts.

-Also Credit to ICT (inner circle trader) for the concepts used here: Fair value gaps and their Consequent Encroachment (CE).