Recession Warning Traffic LightThis is an indicator that uses 6 different metrics to determine the combined probability of a recession and compares the high probability warning periods against actual historical periods of recession.

GREEN tells us that the referenced recession indicators are not exhibiting any warning. Observe the long stretches of “all-green” in between recessionary periods in the chart above.

RED will show a full-on warning level for that particular recession indicator, signaling that monitoring of this sector is clearly showing a problem – which has in the past, reliably exhibited itself as a forewarning of recessions.

Adding green and red together can help determine a combined probability of recession.

IMPORTANT: Your chart should be on 1d and set to SPX , DJI ,or NDQ indices

Precious metals: This indicator calculates the relative prices of Gold & rhodium. Gold is a flight-to-quality asset. Rhodium is the rarest of precious industrial metals and prices spike when the economy is heating up. In front of a recession, the upper relative movement of rhodium precedes gold.

Stock markets: This indicator compares closing prices to growth rate curves of the SPX. This indication is the noisiest but tells us very well when the recession has ended. Stock market indices, which respond to “smart money” moving out of markets when the other indicators begin to warn of recession, or when markets become overheated and rise to historically unsustainable levels.

Yield curve: This indicator compares the 3m & 10y treasuries and detects yield curve inversions. Interest rates are controlled by the Federal Reserve and by the purchasers in the Federal Treasury auction markets, which together create the treasury yield curve. This inversion is the most reliable recession indicator. These happen during a flight to quality.

Federal Reserve: This indicator measures GDP and detects contraction which is technically a recession. This is usually one of the last indicators to enter a Warning state, and it could be 6 months delayed simply confirming what may have already been projected.

Money Supply. This indicator measures the M2 money supply, which typically grows about 1% per calendar quarter. When this shrinks, it's tapping the brakes on the economy. This can also lead to yield curve inversion. This is also a measure of inflation and its effects on the aggregate money supply (liquid capital) available for short-term economic activity, or which can be directed into the purchase of long-term, less liquid assets.

Leading Economic factors: There is a whole basket of leading economic indicators that, as collections, reflect overall growth or contraction of economic activity. These indicators include measures of level and growth in productivity, employment, housing, consumer confidence, industrial purchasing confidence, and much more. These indicators may or may not be detached from the broader economy, and often provide up to 6 months of foresight. For more information please visit www.conference-board.org

Actual Recession: Central Bank indicators are published by the Federal Reserve and reflect their own analysis of national and regional economic health, as well as their calculations of the likelihood of a recession. The Federal Reserve has a recession ticker which is used to plot periods of actual recessions on this indicator for comparison.

In den Scripts nach "curve" suchen

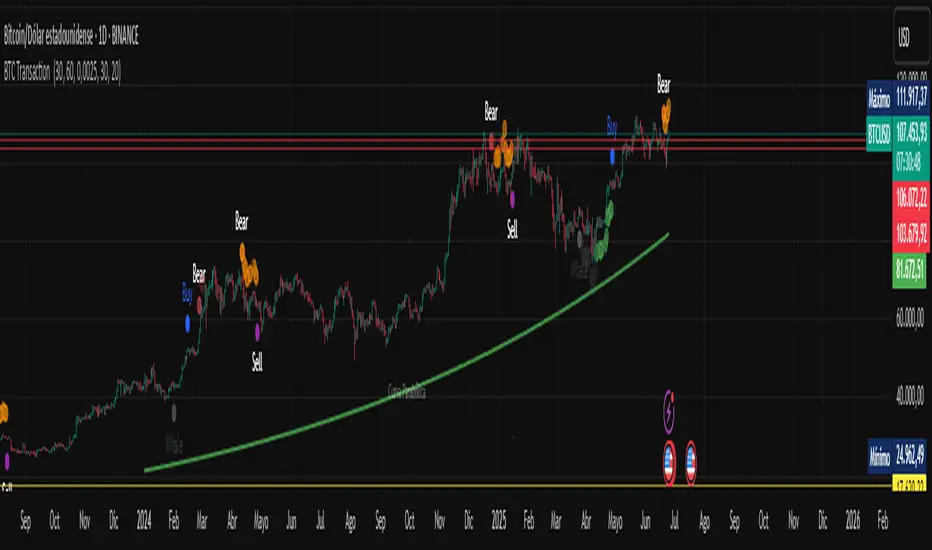

BTC Transaction Indicator Name: "Bitcoin On-Chain Volume & Dynamic Parabolic Curve Signals"

Purpose:

This indicator is designed for Bitcoin traders and long-term holders. It combines the analysis of Bitcoin's on-chain transaction volume with price action to generate "Whale" and "Bear" signals. Additionally, it features a unique dynamic parabolic curve that acts as a visual support line, adapting its visibility based on price interaction with a key Exponential Moving Average (EMA).

Key Components:

On-Chain Volume Analysis:

Utilizes Estimated Transaction Volume (ETRAV) data from the Bitcoin blockchain.

Calculates fast and slow Simple Moving Averages (SMAs) of this volume.

Identifies volume trends (up/down) and significant volume increases/decreases.

Employs fixed thresholds (2,500,000 for low volume and 25,000,000 for high volume) to define key activity levels, similar to how historical on-chain analysis defined accumulation and distribution zones.

Price Action Analysis:

Calculates fast and slow SMAs of the price.

Detects price trends (up/down), recoveries, and declines based on these price SMAs.

"Whale" and "Bear" Signals:

Whale Signals (Buy-side): Generated when there's an upward volume trend, significant volume increase, and a downward price trend followed by price recovery. These indicate potential accumulation phases.

Bear Signals (Sell-side): Generated when there's a downward volume trend, significant volume decrease, and an upward price trend followed by price decline. These indicate potential distribution phases.

Visuals: Both types of signals are plotted as small, colored circles directly on the price chart, with corresponding text labels ("Whale," "Buy," "Bear," "Sell," "Price Recovering," "Price Declining").

Dynamic Parabolic Curve:

Concept: A green parabolic (exponential) curve that serves as a dynamic visual support line.

Activation: The curve starts drawing automatically only when the price crosses over the EMA 500 (Exponential Moving Average of 500 periods). The curve's starting point is set at a user-defined percentage below the EMA 500 value at that exact crossover point.

Visibility: The curve remains visible and continues its trajectory only as long as the price stays above the EMA 500.

Deactivation: The curve disappears instantly if the price falls below or equals the EMA 500. It will only reappear if the price crosses above the EMA 500 again.

Customization: The curve's steepness (Tasa Crecimiento Curva) and its initial distance from the EMA 500 (Inicio Curva % por debajo de EMA500) are adjustable.

Dynamic Label: A "Parabólico" text label is plotted near the center of the active curve segment, with an adjustable vertical offset to ensure it stays visually appealing below the curve.

What is PLOTTED on the chart:

The small, colored circle signals for Whale/Buy and Bear/Sell activity.

The green dynamic parabolic curve.

What is NOT PLOTTED:

EMA 200, EMA 500 lines (though they are calculated internally for logic).

Raw volume data or volume Moving Averages (these are only used for signal calculation, not plotted).

Ideal for:

Bitcoin traders and investors focused on long-term trends and cycle analysis, who want visual cues for accumulation/distribution phases based on on-chain activity, complemented by a unique, dynamically appearing parabolic support curve.

Important Notes:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe for optimal on-chain data relevance.

️Omega RatioThe Omega Ratio is a risk-return performance measure of an investment asset, portfolio, or strategy. It is defined as the probability-weighted ratio, of gains versus losses for some threshold return target. The ratio is an alternative for the widely used Sharpe ratio and is based on information the Sharpe ratio discards.

█ OVERVIEW

As we have mentioned many times, stock market returns are usually not normally distributed. Therefore the models that assume a normal distribution of returns may provide us with misleading information. The Omega Ratio improves upon the common normality assumption among other risk-return ratios by taking into account the distribution as a whole.

█ CONCEPTS

Two distributions with the same mean and variance, would according to the most commonly used Sharpe Ratio suggest that the underlying assets of the distribution offer the same risk-return ratio. But as we have mentioned in our Moments indicator, variance and standard deviation are not a sufficient measure of risk in the stock market since other shape features of a distribution like skewness and excess kurtosis come into play. Omega Ratio tackles this problem by employing all four Moments of the distribution and therefore taking into account the differences in the shape features of the distributions. Another important feature of the Omega Ratio is that it does not require any estimation but is rather calculated directly from the observed data. This gives it an advantage over standard statistical estimators that require estimation of parameters and are therefore sampling uncertainty in its calculations.

█ WAYS TO USE THIS INDICATOR

Omega calculates a probability-adjusted ratio of gains to losses, relative to the Minimum Acceptable Return (MAR). This means that at a given MAR using the simple rule of preferring more to less, an asset with a higher value of Omega is preferable to one with a lower value. The indicator displays the values of Omega at increasing levels of MARs and creating the so-called Omega Curve. Knowing this one can compare Omega Curves of different assets and decide which is preferable given the MAR of your strategy. The indicator plots two Omega Curves. One for the on chart symbol and another for the off chart symbol that u can use for comparison.

When comparing curves of different assets make sure their trading days are the same in order to ensure the same period for the Omega calculations. Value interpretation: Omega<1 will indicate that the risk outweighs the reward and therefore there are more excess negative returns than positive. Omega>1 will indicate that the reward outweighs the risk and that there are more excess positive returns than negative. Omega=1 will indicate that the minimum acceptable return equals the mean return of an asset. And that the probability of gain is equal to the probability of loss.

█ FEATURES

• "Low-Risk security" lets you select the security that you want to use as a benchmark for Omega calculations.

• "Omega Period" is the size of the sample that is used for the calculations.

• “Increments” is the number of Minimal Acceptable Return levels the calculation is carried on. • “Other Symbol” lets you select the source of the second curve.

• “Color Settings” you can set the color for each curve.

Gann Box (Zeiierman)█ Overview

The Gann Box (Zeiierman) is an indicator that provides visual insights using the principles of W.D. Gann's trading methods. Gann's techniques are based on geometry, astronomy, and astrology, and are used to predict important price levels and market trends. This indicator helps traders identify potential support and resistance levels, and forecast future price movements.

Gann used angles and various geometric constructions to divide time and price into proportionate parts. Gann indicators are often used to predict areas of support and resistance, key tops and bottoms, and future price moves.

█ How It Works

The indicator operates by identifying high and low points within a visible range on the chart and drawing a Gann Box between these points. The box is divided into segments based on selected percentages, which represent key levels for observing market reactions. It includes options to display labels, a Gann fan, and Gann angles for analysis. Advanced features allow extending the box into the future for predictive analysis and reversing its orientation for alternative viewpoints.

High and Low Points Identification: It starts by locating the highest and lowest price points visible on the chart.

Gann Box Construction: Draws a box from these points and divides it according to specified percentages, highlighting potential support and resistance levels.

█ How to Use

Support and Resistance Levels

Using a Gann angle to forecast support and resistance is probably the most popular way they are used. This technique frames the market, allowing the analyst to read the movement of the market inside this framework.

The lines within the Gann Box, drawn at the key percentages, create a grid of potential support and resistance levels. As prices fluctuate, these lines can act as barriers to price movement, with the price often pausing or reversing at these intervals.

Forecasting with the 'Extend' Feature: The indicator's ability to extend lines and boxes into the future provides traders with a forward-looking tool to anticipate potential market movements and prepare for them.

Gann Fan: This feature draws lines at a significant price angle, helping traders identify potential support and resistance levels based on the theory that prices move in predictable patterns.

Gann Curves: Gann Curves display dynamic support and resistance levels, aiding in the analysis of momentum and trend strength.

█ Settings

The indicator includes several settings that allow customization of its appearance and functionality:

⚪ General Settings

Reverse: This setting changes the orientation of labels and calculations within the Gann Box, providing alternative analytical perspectives. It essentially flips the Gann Box's direction, which can be useful in different market conditions or analysis scenarios.

Extend: Extends the drawing of Gann lines or boxes into the future beyond the current last bar. This feature is essential for forecasting future price movements and identifying potential support or resistance levels that lie outside the current price action.

⚪ Gann Box

Show Box: Toggles the visibility of the Gann Box on the chart. The Gann Box is a fundamental tool in Gann analysis, highlighting key levels based on selected high and low points to identify potential support and resistance areas.

Show Fibonacci Labels: Controls the display of Fibonacci labels within the Gann Box. These labels mark specific Fibonacci retracement levels, aiding traders in recognizing significant levels for potential reversals.

Box Visibility: Allows users to enable or disable individual boxes within the Gann Box, providing flexibility in focusing on specific levels of interest.

Percentage Levels: Defines the Fibonacci levels within the Gann Box. Traders can adjust these levels to customize the Gann Box according to their specific analysis needs.

Coloring: Customizes the color of each level within the Gann Box, enhancing visual clarity and differentiation between levels.

⚪ Gann Fan

Show Fan: Enables the Gann Fan, which draws lines at significant Gann angles from a particular point on the chart, helping identify potential support and resistance levels.

Fan Percentages and Coloring: Similar to the Gann Box, these settings allow traders to customize which Gann angles are displayed and how they are colored.

⚪ Gann Curves

Show Curves: When enabled, this setting draws Gann Curves on the chart. These curves are based on Gann percentages and provide a dynamic view of support and resistance levels as they adapt to changing market conditions.

Curve Percentages and Coloring: Define which curves are displayed and their colors, allowing for a tailored analysis experience.

⚪ Gann Angles

Show Angles: Toggles the display of Gann Angles, which are crucial for understanding the market's price and time dynamics, offering insights into future support and resistance levels.

Coloring: Customizes the color of the Gann Angles, making it easier to differentiate between various angles on the chart.

█ Alerts

The indicator includes several alert conditions for price breakouts from the Gann Box and specific levels, enabling traders to be notified of significant market movements.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

ETH - Log Regression BandsETH – Log Regression Bands: Detailed Description (Math + How to Use)

Overview

This indicator plots a long-term “fair value” growth curve for ETH and surrounds it with multiple upper and lower bands. The goal is to estimate where price sits relative to a long-term trend that is best interpreted in **logarithmic (percentage) terms**, not raw dollars.

The bands create clear zones showing when ETH is historically cheap or expensive relative to that long-term curve.

---

Why use logarithms?

Price action is typically more meaningful in **percentage moves** than in absolute dollar moves.

* A move from $100 → $200 is +100%

* A move from $2000 → $2100 is only +5%

By modelling the natural logarithm of price, multiplicative growth becomes additive. That makes long-term growth easier to model and band spacing more consistent across very different price regimes.

So instead of modelling (P), the indicator models:

---

The growth model: Power-law curve

The indicator uses “time since inception” as the x-axis. However, rather than using time directly, it uses the logarithm of time:

where (t) is the number of days (or bars) since the first data point.

It then fits a straight-line model in log-log space:

Substituting back in:

Exponentiating both sides gives the curve in normal price units:

This is a **power-law** trend curve. It naturally produces a smooth, slowly bending long-term curve similar to the “log regression” curves often seen in macro crypto reports.

---

What “expanding regression” means

The model uses all data available from the beginning of the chart up to the current bar. That means:

* Early in the asset’s history the curve can change more because there are fewer points.

* Over time the curve becomes more stable as more history is included.

Important note: this does **not** repaint past bars. It simply means the current curve will update as new data comes in.

---

Measuring “typical deviation” from the curve (residual volatility)

Once the trend curve is fitted in log space, the indicator measures how far price typically wanders away from it.

At any time point:

* Actual log price is (y = \ln(P))

* Predicted log price from the curve is (\hat{y} = a + b\ln(t))

The **residual** is:

The indicator computes the standard deviation of these residuals:

This (\sigma) is a measure of typical “distance from trend” in log terms.

---

Building the bands (the key idea)

The bands are evenly spaced in **log space** using multiples of (\sigma). A band number (k) is created by shifting the log-trend up or down:

Upper band (k):

Lower band (k):

Where:

* (k) is the band number (1, 2, 3, …)

* (s) is a user-chosen spacing factor (band spacing)

* (\sigma) is the residual standard deviation

Converting back to normal price:

Upper band (k):

Lower band (k):

Why bands look like “translated copies”

Because shifting by a constant in log space equals multiplying by a constant in price space:

So the bands are the same underlying curve scaled up or down by fixed multipliers. That produces the smooth “stacked curve” look associated with macro log regression charts.

---

Optional curve shift (manual adjustment)

A manual offset can be applied in log space. This is useful if you want to align the entire structure slightly higher or lower.

Because the shift is applied to (\ln(P)), this is not an additive dollar adjustment. It scales the entire curve by a constant factor:

* Positive shift → multiplies all bands upward

* Negative shift → multiplies all bands downward

---

How to interpret the zones

The base curve represents a long-term “trend center” in log-growth terms.

* Price near the base curve → near long-term trend

* Price in upper bands → expensive relative to long-term trend

* Price in lower bands → cheap relative to long-term trend

Because the bands are built using residual volatility in log space, “cheap/expensive” is measured in a way that remains meaningful across different eras and price levels.

---

Long-term buy zones (Lower 1 and Lower 2)

**Lower 1** and **Lower 2** are intended as **long-term accumulation zones**.

When ETH trades in these zones, it is significantly below the long-term growth curve in log terms, which typically corresponds to:

* deep bear markets,

* high fear / capitulation phases,

* long accumulation periods.

A simple long-term framework many users apply:

* **Accumulate gradually when price enters Lower 1**

* **Accumulate more aggressively when price enters Lower 2**

* Reduce risk / take profits progressively in higher upper bands

These are not guarantees — they are **statistical “distance from trend” zones**, designed to help structure long-term decisions.

---

## Notes / limitations

* This indicator is a **macro trend tool**, not an intraday trading system.

* The curve is derived from historical behavior; it can shift slowly as new data arrives.

* Extremely new market regimes or structural changes can reduce reliability.

* Use alongside risk management and additional confirmation if trading.

---

Finite Difference - Backward (mcbw_)In calculus there exists a 'derivative', which simply just measures the difference between two points on a curve. For well behaved mathematical functions there are infinitely many points and so there exists a derivative at every point. Where there are infinitely many points in a curve that curve is called 'continuous'. Continuous curves are very nice to deal with since each point on it exists almost exactly where its neighbors are. However, if the curve does not have infinitely many points on it, but instead has a finite number of points on it, that curve is called 'discrete' instead of continuous. Taking the derivative of discrete curves is much trickier business since there are none of the mathematical conveniences that a continuous offers. In the real world everything we measure is a discrete curve, including Price (since we measure it a finite number of times, aka each candlestick)!

The branch of Discrete Mathematics has found an approach to measure the derivative along a discrete curve, that approach is aptly called " Finite Difference ". To get a more accurate approximation of a discrete derivative, the finite difference approach uses weighted combinations of neighboring points. The most common type of finite difference is a 'central' difference, this uses a combination of points before and after the point of interest to approximate the discrete derivative. This is great for historical analysis but is not of much use for trading algorithms since it technically means using future prices to calculate the derivative of the current point. Instead we can use a less common variant called a ' Backwards Difference ' that only uses a combination of points before the current one to help approximate the current derivative.

In this script you can choose the " Order " of your derivative and the " Accuracy " of its approximation. This script is for educational purposes for folks building trading algorithms. Many trading algorithms often have an element of seeing how much Price has changed from the previous candle to the current candle. This approach is the lowest accuracy derivative possible, and using the backwards finite differences, made available for the first time on TradingView (!!), algorithms that use derivatives can now have higher orders of accuracy!

Happy Trading/Developing!

[MAD] Acceleration based dampened SMA projectionsThis indicator utilizes concepts of arrays inside arrays to calculate and display projections of multiple Smoothed Moving Average (SMA) lines via polylines.

This is partly an experiment as an educational post, on how to work with multidimensional arrays by using User-Defined Types

------------------

Input Controls for User Interaction:

The indicator provides several input controls, allowing users to adjust parameters like the SMA window, acceleration window, and dampening factors.

This flexibility lets users customize the behavior and appearance of the indicator to fit their analysis needs.

sma length:

Defines the length of the simple moving average (SMA).

acceleration window:

Sets the window size for calculating the acceleration of the SMA.

Input Series:

Selects the input source for calculating the SMA (typically the closing price).

Offset:

Determines the offset for the input source, affecting the positioning of the SMA. Here it´s possible to add external indicators like bollinger bands,.. in that case as double sma this sma should be very short.

(Thanks Fikira for that idea)

Startfactor dampening:

Initial dampening factor for the polynomial curve projections, influencing their starting curvature.

Growfactor dampening:

Growth rate of the dampening factor, affecting how the curvature of the projections changes over time.

Prediction length:

Sets the length of the projected polylines, extending beyond the current bar.

cleanup history:

Boolean input to control whether to clear the previous polyline projections before drawing new ones.

Key technologies used in this indicator include:

User-Defined Types (UDT) :

This indicator uses UDT to create a custom type named type_polypaths.

This type is designed to store information for each polyline, including an array of points (array), a color for the polyline, and a dampening factor.

UDTs in Pine Script enable the creation of complex data structures, which are essential for organizing and manipulating data efficiently.

type type_polypaths

array polyline_points = na

color polyline_color = na

float dampening_factor= na

Arrays and Nested Arrays:

The script heavily utilizes arrays.

For example, it uses a color array (colorpreset) to store different colors for the polyline.

Moreover, an array of type_polypaths (polypaths) is used, which is an array consisting of user-defined types. Each element of this array contains another array (polyline_points), demonstrating nested array usage.

This structure is essential for handling multiple polylines, each with its set of points and attributes.

var type_polypaths polypaths = array.new()

Polyline Creation and Manipulation:

The core visual aspect of the indicator is the creation of polylines.

Polyline points are calculated based on a dampened polynomial curve, which is influenced by the SMA's slope and acceleration.

Filling initial dampening data

array_size = 9

middle_index = math.floor(array_size / 2)

for i = 0 to array_size - 1

damp_factor = f_calculate_damp_factor(i, middle_index, Startfactor, Growfactor)

polyline_color = colorpreset.get(i)

polypaths.push(type_polypaths.new(array.new(0, na), polyline_color, damp_factor))

The script dynamically generates these polyline points and stores them in the polyline_points array of each type_polypaths instance based on those prefilled dampening factors

if barstate.islast or cleanup == false

for damp_factor_index = 0 to polypaths.size() - 1

GET_RW = polypaths.get(damp_factor_index)

GET_RW.polyline_points.clear()

for i = 0 to predictionlength

y = f_dampened_poly_curve(bar_index + i , src_input , sma_slope , sma_acceleration , GET_RW.dampening_factor)

p = chart.point.from_index(bar_index + i - src_off, y)

GET_RW.polyline_points.push(p)

polypaths.set(damp_factor_index, GET_RW)

Polyline Drawout

The polyline is then drawn on the chart using the polyline.new() function, which uses these points and additional attributes like color and width.

for pl_s = 0 to polypaths.size() - 1

GET_RO = polypaths.get(pl_s)

polyline.new(points = GET_RO.polyline_points, line_width = 1, line_color = GET_RO.polyline_color, xloc = xloc.bar_index)

If the cleanup input is enabled, existing polylines are deleted before new ones are drawn, maintaining clarity and accuracy in the visualization.

if cleanup

for pl_delete in polyline.all

pl_delete.delete()

------------------

The mathematics

in the (ABDP) indicator primarily focuses on projecting the behavior of a Smoothed Moving Average (SMA) based on its current trend and acceleration.

SMA Calculation:

The indicator computes a simple moving average (SMA) over a specified window (sma_window). This SMA serves as the baseline for further calculations.

Slope and Acceleration Analysis:

It calculates the slope of the SMA by subtracting the current SMA value from its previous value. Additionally, it computes the SMA's acceleration by evaluating the sum of differences between consecutive SMA values over an acceleration window (acceleration_window). This acceleration represents the rate of change of the SMA's slope.

sma_slope = src_input - src_input

sma_acceleration = sma_acceleration_sum_calc(src_input, acceleration_window) / acceleration_window

sma_acceleration_sum_calc(src, window) =>

sum = 0.0

for i = 0 to window - 1

if not na(src )

sum := sum + src - 2 * src + src

sum

Dampening Factors:

Custom dampening factors for each polyline, which are based on the user-defined starting and growth factors (Startfactor, Growfactor).

These factors adjust the curvature of the projected polylines, simulating various future scenarios of SMA movement.

f_calculate_damp_factor(index, middle, start_factor, growth_factor) =>

start_factor + (index - middle) * growth_factor

Polynomial Curve Projection:

Using the SMA value, its slope, acceleration, and dampening factors, the script calculates points for polynomial curves. These curves represent potential future paths of the SMA, factoring in its current direction and rate of change.

f_dampened_poly_curve(index, initial_value, initial_slope, acceleration, damp_factor) =>

delta = index - bar_index

initial_value + initial_slope * delta + 0.5 * damp_factor * acceleration * delta * delta

damp_factor = f_calculate_damp_factor(i, middle_index, Startfactor, Growfactor)

Have fun trading :-)

Analog Flow [KedArc Quant]Overview

AnalogFlow is an advanced analogue based market projection engine that reconstructs future price tendencies by matching current price behavior to historical analogues in the same instrument. Instead of using traditional indicators such as moving averages, RSI, or regression, AnalogFlow applies pattern vector similarity analysis - a data driven technique that identifies historically similar sequences and aggregates their subsequent movements into a smooth, forward looking curve.

Think of it as a market memory system:

If the current pattern looks like one we have seen before, how did price move afterward?

Why AnalogFlow Is Unique

1. Pattern centric - it does not rely on any standard indicator formula; it directly analyzes price movement vectors.

2. Adaptive - it learns from the same instrument's past behavior, making it self calibrating to volatility and regime shifts.

3. Non repainting - the projection is generated on the latest completed bar and remains fixed until new data is available.

4. Noise resistant - the EMA Blend engine smooths the projected trajectory, reducing random variance between analogues.

Inputs and Configuration

Pattern Bars

Number of bars in the reference pattern window: 40

Projection Bars

Number of bars forward to project: 30

Search Depth

Number of bars back to look for matching analogues: 600

Distance Metric

Comparison method: Euclidean, Manhattan, or Cosine (default Euclidean)

Matches

Number of top analogues to blend (1-5): Top 3

Build Mode

Projection type: Cumulative, MeanStep, or EMA Blend (default EMA Blend)

EMA Blend Length

Smoothness of the projected path: 15

Normalize Pattern

Enable Z score normalization for shape matching: true

Dissimilarity Mode

If true, finds inverse analogues for mean reversion analysis: false

Line Color and Width

Style settings for projection curve: Blue, width 2

How It Works with Past Data

1. The system builds a memory bank of patterns from the last N bars based on the scanDepth value.

2. It compares the latest Pattern Bars segment to each historical segment.

3. It selects the Top K most similar or dissimilar analogues.

4. For each analogue, it retrieves what happened after that pattern historically.

5. It averages or smooths those forward moves into a single composite forecast curve.

6. The forecast (blue line) is drawn ahead of the current candle using line.new with no repainting.

Output Explained

Blue Path

The weighted mean future trajectory based on historical analogues.

Smoother when EMA Blend mode is enabled.

Flat Section

Indicates low directional consensus or equilibrium across analogues.

Upward or Downward Slope

Represents historical tendency toward continuation or reversal following similar conditions.

Recommended Timeframes

Scalping / Short Term

1m - 5m : Short winLen (20-30), small ahead (10-15)

Swing Trading

15m - 1h : Balanced settings (winLen 40-60, ahead 20-30)

Positional / Multi Day

4h - 1D : Large windows (winLen 80-120, ahead 30-50)

Instrument Compatibility

Works seamlessly on:

Stocks and ETFs

Indices

Cryptocurrency

Commodities (Gold, Crude, etc.)

Futures and F&O (both intraday and positional)

Forex

No symbol specific calibration needed. It self adapts to volatility.

How Traders Can Use It

Forecast Context

Identify likely short term price path or drift direction.

Reversal Detection

Flip seekOpp to true for mean reversion pattern analysis.

Scenario Comparison

Observe whether the current regime tends to continue or stall.

Momentum Confirmation

Combine with trend tools such as EMA or MACD for directional bias.

Backtesting Support

Compare projected path versus realized price to evaluate reliability.

FAQ

Q1. Does AnalogFlow repaint?

No. It calculates only once per completed bar and projects forward. The future path remains static until a new bar closes.

Q2. Is it a neural network or AI model?

Not in the machine learning sense. It is a deterministic analogue matching engine using statistical distance metrics.

Q3. Why does the projection sometimes flatten?

That means similar historical setups had no clear consensus in direction (neutral expectation).

Q4. Can I use it for live trading signals?

AnalogFlow is not a signal generator. It provides probabilistic context for upcoming movement.

Q5. Does higher scanDepth improve accuracy?

Up to a point. More depth gives more analogues, but too much can dilute recency. Try 400 to 800.

Glossary

Analogue

A past pattern similar to the current price behavior.

Distance Metric

Mathematical formula for pattern similarity.

Step Vector

Difference between consecutive closing prices.

EMA Blend

Exponential smoothing of the projected path.

Cumulative Mode

Adds sequential historical deltas directly.

Z Score Normalization

Rescaling to mean 0 and variance 1 for shape comparison.

Summary

AnalogFlow converts the market's historical echoes into a structured, statistically weighted forward projection. It gives traders a contextual roadmap, not a signal, showing how similar past setups evolved and allowing better informed entries, exits, and scenario planning across all asset classes.

Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and proper risk management when applying this strategy.

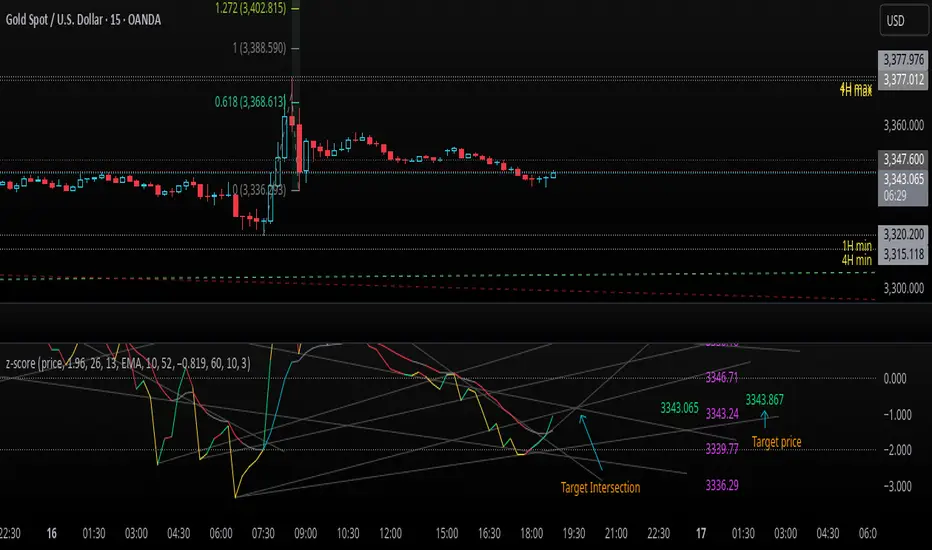

z-score-calkusi-v1.143z-scores incorporate the moment of N look-back bars to allow future price projection.

z-score = (X - mean)/std.deviation ; X = close

z-scores update with each new close print and with each new bar. Each new bar augments the mean and std.deviation for the N bars considered. The old Nth bar falls away from consideration with each new historical bar.

The indicator allows two other options for X: RSI or Moving Average.

NOTE: While trading use the "price" option only.

The other two options are provided for visualisation of RSI and Moving Average as z-score curves.

Use z-scores to identify tops and bottoms in the future as well as intermediate intersections through which a z-score will pass through with each new close and each new bar.

Draw lines from peaks and troughs in the past through intermediate peaks and troughs to identify projected intersections in the future. The most likely intersections are those that are formed from a line that comes from a peak in the past and another line that comes from a trough in the past. Try getting at least two lines from historical peaks and two lines from historical troughs to pass through a future intersection.

Compute the target intersection price in the future by clicking on the z-score indicator header to see a drag-able horizontal line to drag over the intersection. The target price is the last value displayed in the indicator's status bar after the closing price.

When the indicator header is clicked, a white horizontal drag-able line will appear to allow dragging the line over an intersection that has been drawn on the indicator for a future z-score projection and the associated future closing price.

With each new bar that appears, it is necessary to repeat the procedure of clicking the z-score indicator header to be able to drag the drag-able horizontal line to see the new target price for the selected intersection. The projected price will be different from the current close price providing a price arbitrage in time.

New intermediate peaks and troughs that appear require new lines be drawn from the past through the new intermediate peak to find a new intersection in the future and a new projected price. Since z-score curves are sort of cyclical in nature, it is possible to see where one has to locate a future intersection by drawing lines from past peaks and troughs.

Do not get fixated on any one projected price as the market decides which projected price will be realised. All prospective targets should be manually updated with each new bar.

When the z-score plot moves outside a channel comprised of lines that are drawn from the past, be ready to adjust to new market conditions.

z-score plots that move above the zero line indicate price action that is either rising or ranging. Similarly, z-score plots that move below the zero line indicate price action that is either falling or ranging. Be ready to adjust to new market conditions when z-scores move back and forth across the zero line.

A bar with highest absolute z-score for a cycle screams "reversal approaching" and is followed by a bar with a lower absolute z-score where close price tops and bottoms are realised. This can occur either on the next bar or a few bars later.

The indicator also displays the required N for a Normal(0,1) distribution that can be set for finer granularity for the z-score curve.This works with the Confidence Interval (CI) z-score setting. The default z-score is 1.96 for 95% CI.

Common Confidence Interval z-scores to find N for Normal(0,1) with a Margin of Error (MOE) of 1:

70% 1.036

75% 1.150

80% 1.282

85% 1.440

90% 1.645

95% 1.960

98% 2.326

99% 2.576

99.5% 2.807

99.9% 3.291

99.99% 3.891

99.999% 4.417

9-Jun-2025

Added a feature to display price projection labels at z-score levels 3, 2, 1, 0, -1, -2, 3.

This provides a range for prices available at the current time to help decide whether it is worth entering a trade. If the range of prices from say z=|2| to z=|1| is too narrow, then a trade at the current time may not be worth the risk.

Added plot for z-score moving average.

28-Jun-2025

Added Settings option for # of Std.Deviation level Price Labels to display. The default is 3. Min is 2. Max is 6.

This feature allows likelihood assessment for Fibonacci price projections from higher time frames at lower time frames. A Fibonacci price projection that falls outside |3.x| Std.Deviations is not likely.

Added Settings option for Chart Bar Count and Target Label Offset to allow placement of price labels for the standard z-score levels to the right of the window so that these are still visible in the window.

Target Label Offset allows adjustment of placement of Target Price Label in cases when the Target Price Label is either obscured by the price labels for the standard z-score levels or is too far right to be visible in the window.

9-Jul-2025

z-score 1.142 updates:

Displays in the status line before the close price the range for the selected Std. Deviation levels specified in Settings and |z-zMa|.

When |z-zMa| > |avg(z-zMa)| and zMa rising, |z-zMa| and zMa displays in aqua.

When |z-zMa| > |avg(z-zMa)| and zMa falling, |z-zMa| and zMa displays in red.

When |z-zMa| <= |avg(z-zMa)|, z and zMa display in gray.

z usually crosses over zMa when zMa is gray but not always. So if cross-over occurs when zMa is not gray, it implies a strong move in progress.

Practice makes perfect.

Use this indicator at your own risk

DeeptestDeeptest: Quantitative Backtesting Library for Pine Script

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ OVERVIEW

Deeptest is a Pine Script library that provides quantitative analysis tools for strategy backtesting. It calculates over 100 statistical metrics including risk-adjusted return ratios (Sharpe, Sortino, Calmar), drawdown analysis, Value at Risk (VaR), Conditional VaR, and performs Monte Carlo simulation and Walk-Forward Analysis.

█ WHY THIS LIBRARY MATTERS

Pine Script is a simple yet effective coding language for algorithmic and quantitative trading. Its accessibility enables traders to quickly prototype and test ideas directly within TradingView. However, the built-in strategy tester provides only basic metrics (net profit, win rate, drawdown), which is often insufficient for serious strategy evaluation.

Due to this limitation, many traders migrate to alternative backtesting platforms that offer comprehensive analytics. These platforms require other language programming knowledge, environment setup, and significant time investment—often just to test a simple trading idea.

Deeptest bridges this gap by bringing institutional-level quantitative analytics directly to Pine Script. Traders can now perform sophisticated analysis without leaving TradingView or learning complex external platforms. All calculations are derived from strategy.closedtrades.* , ensuring compatibility with any existing Pine Script strategy.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY AND USEFULNESS

This library is original work that adds value to the TradingView community in the following ways:

1. Comprehensive Metric Suite: Implements 112+ statistical calculations in a single library, including advanced metrics not available in TradingView's built-in tester (p-value, Z-score, Skewness, Kurtosis, Risk of Ruin).

2. Monte Carlo Simulation: Implements trade-sequence randomization to stress-test strategy robustness by simulating 1000+ alternative equity curves.

3. Walk-Forward Analysis: Divides historical data into rolling in-sample and out-of-sample windows to detect overfitting by comparing training vs. testing performance.

4. Rolling Window Statistics: Calculates time-varying Sharpe, Sortino, and Expectancy to analyze metric consistency throughout the backtest period.

5. Interactive Table Display: Renders professional-grade tables with color-coded thresholds, tooltips explaining each metric, and period analysis cards for drawdowns/trades.

6. Benchmark Comparison: Automatically fetches S&P 500 data to calculate Alpha, Beta, and R-squared, enabling objective assessment of strategy skill vs. passive investing.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ KEY FEATURES

Performance Metrics

Net Profit, CAGR, Monthly Return, Expectancy

Profit Factor, Payoff Ratio, Sample Size

Compounding Effect Analysis

Risk Metrics

Sharpe Ratio, Sortino Ratio, Calmar Ratio (MAR)

Martin Ratio, Ulcer Index

Max Drawdown, Average Drawdown, Drawdown Duration

Risk of Ruin, R-squared (equity curve linearity)

Statistical Distribution

Value at Risk (VaR 95%), Conditional VaR

Skewness (return asymmetry)

Kurtosis (tail fatness)

Z-Score, p-value (statistical significance testing)

Trade Analysis

Win Rate, Breakeven Rate, Loss Rate

Average Trade Duration, Time in Market

Consecutive Win/Loss Streaks with Expected values

Top/Worst Trades with R-multiple tracking

Advanced Analytics

Monte Carlo Simulation (1000+ iterations)

Walk-Forward Analysis (rolling windows)

Rolling Statistics (time-varying metrics)

Out-of-Sample Testing

Benchmark Comparison

Alpha (excess return vs. benchmark)

Beta (systematic risk correlation)

Buy & Hold comparison

R-squared vs. benchmark

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK START

Basic Usage

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as *

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ METRIC EXPLANATIONS

The Deeptest table displays 23 metrics across the main row, with 23 additional metrics in the complementary row. Each metric includes detailed tooltips accessible by hovering over the value.

Main Row — Performance Metrics (Columns 0-6)

Net Profit — (Final Equity - Initial Capital) / Initial Capital × 100

— >20%: Excellent, >0%: Profitable, <0%: Loss

— Total return percentage over entire backtest period

Payoff Ratio — Average Win / Average Loss

— >1.5: Excellent, >1.0: Good, <1.0: Losses exceed wins

— Average winning trade size relative to average losing trade. Breakeven win rate = 100% / (1 + Payoff)

Sample Size — Count of closed trades

— >=30: Statistically valid, <30: Insufficient data

— Number of completed trades. Includes 95% confidence interval for win rate in tooltip

Profit Factor — Gross Profit / Gross Loss

— >=1.5: Excellent, >1.0: Profitable, <1.0: Losing

— Ratio of total winnings to total losses. Uses absolute values unlike payoff ratio

CAGR — (Final / Initial)^(365.25 / Days) - 1

— >=10%: Excellent, >0%: Positive growth

— Compound Annual Growth Rate - annualized return accounting for compounding

Expectancy — Sum of all returns / Trade count

— >0.20%: Excellent, >0%: Positive edge

— Average return per trade as percentage. Positive expectancy indicates profitable edge

Monthly Return — Net Profit / (Months in test)

— >0%: Profitable month average

— Average monthly return. Geometric monthly also shown in tooltip

Main Row — Trade Statistics (Columns 7-14)

Avg Duration — Average time in position per trade

— Mean holding period from entry to exit. Influenced by timeframe and trading style

Max CW — Longest consecutive winning streak

— Maximum consecutive wins. Expected value = ln(trades) / ln(1/winRate)

Max CL — Longest consecutive losing streak

— Maximum consecutive losses. Important for psychological risk tolerance

Win Rate — Wins / Total Trades

— Higher is better

— Percentage of profitable trades. Breakeven win rate shown in tooltip

BE Rate — Breakeven Trades / Total Trades

— Lower is better

— Percentage of trades that broke even (neither profit nor loss)

Loss Rate — Losses / Total Trades

— Lower is better

— Percentage of unprofitable trades. Together with win rate and BE rate, sums to 100%

Frequency — Trades per month

— Trading activity level. Displays intelligently (e.g., "12/mo", "1.5/wk", "3/day")

Exposure — Time in market / Total time × 100

— Lower = less risk

— Percentage of time the strategy had open positions

Main Row — Risk Metrics (Columns 15-22)

Sharpe Ratio — (Return - Rf) / StdDev × sqrt(Periods)

— >=3: Excellent, >=2: Good, >=1: Fair, <1: Poor

— Measures risk-adjusted return using total volatility. Annualized using sqrt(252) for daily

Sortino Ratio — (Return - Rf) / DownsideDev × sqrt(Periods)

— >=2: Excellent, >=1: Good, <1: Needs improvement

— Similar to Sharpe but only penalizes downside volatility. Can be higher than Sharpe

Max DD — (Peak - Trough) / Peak × 100

— <5%: Excellent, 5-15%: Moderate, 15-30%: High, >30%: Severe

— Largest peak-to-trough decline in equity. Critical for risk tolerance and position sizing

RoR — Risk of Ruin probability

— <1%: Excellent, 1-5%: Acceptable, 5-10%: Elevated, >10%: Dangerous

— Probability of losing entire trading account based on win rate and payoff ratio

R² — R-squared of equity curve vs. time

— >=0.95: Excellent, 0.90-0.95: Good, 0.80-0.90: Moderate, <0.80: Erratic

— Coefficient of determination measuring linearity of equity growth

MAR — CAGR / |Max Drawdown|

— Higher is better, negative = bad

— Calmar Ratio. Reward relative to worst-case loss. Negative if max DD exceeds CAGR

CVaR — Average of returns below VaR threshold

— Lower absolute is better

— Conditional Value at Risk (Expected Shortfall). Average loss in worst 5% of outcomes

p-value — Binomial test probability

— <0.05: Significant, 0.05-0.10: Marginal, >0.10: Likely random

— Probability that observed results are due to chance. Low p-value means statistically significant edge

Complementary Row — Extended Metrics

Compounding — (Compounded Return / Total Return) × 100

— Percentage of total profit attributable to compounding (position sizing)

Avg Win — Sum of wins / Win count

— Average profitable trade return in percentage

Avg Trade — Sum of all returns / Total trades

— Same as Expectancy (Column 5). Displayed here for convenience

Avg Loss — Sum of losses / Loss count

— Average unprofitable trade return in percentage (negative value)

Martin Ratio — CAGR / Ulcer Index

— Similar to Calmar but uses Ulcer Index instead of Max DD

Rolling Expectancy — Mean of rolling window expectancies

— Average expectancy calculated across rolling windows. Shows consistency of edge

Avg W Dur — Avg duration of winning trades

— Average time from entry to exit for winning trades only

Max Eq — Highest equity value reached

— Peak equity achieved during backtest

Min Eq — Lowest equity value reached

— Trough equity point. Important for understanding worst-case absolute loss

Buy & Hold — (Close_last / Close_first - 1) × 100

— >0%: Passive profit

— Return of simply buying and holding the asset from backtest start to end

Alpha — Strategy CAGR - Benchmark CAGR

— >0: Has skill (beats benchmark)

— Excess return above passive benchmark. Positive alpha indicates genuine value-added skill

Beta — Covariance(Strategy, Benchmark) / Variance(Benchmark)

— <1: Less volatile than market, >1: More volatile

— Systematic risk correlation with benchmark

Avg L Dur — Avg duration of losing trades

— Average time from entry to exit for losing trades only

Rolling Sharpe/Sortino — Dynamic based on win rate

— >2: Good consistency

— Rolling metric across sliding windows. Shows Sharpe if win rate >50%, Sortino if <=50%

Curr DD — Current drawdown from peak

— Lower is better

— Present drawdown percentage. Zero means at new equity high

DAR — CAGR adjusted for target DD

— Higher is better

— Drawdown-Adjusted Return. DAR^5 = CAGR if max DD = 5%

Kurtosis — Fourth moment / StdDev^4 - 3

— ~0: Normal, >0: Fat tails, <0: Thin tails

— Measures "tailedness" of return distribution (excess kurtosis)

Skewness — Third moment / StdDev^3

— >0: Positive skew (big wins), <0: Negative skew (big losses)

— Return distribution asymmetry

VaR — 5th percentile of returns

— Lower absolute is better

— Value at Risk at 95% confidence. Maximum expected loss in worst 5% of outcomes

Ulcer — sqrt(mean(drawdown^2))

— Lower is better

— Ulcer Index - root mean square of drawdowns. Penalizes both depth AND duration

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ MONTE CARLO SIMULATION

Purpose

Monte Carlo simulation tests strategy robustness by randomizing the order of trades while keeping trade returns unchanged. This simulates alternative equity curves to assess outcome variability.

Method

Extract all historical trade returns

Randomly shuffle the sequence (1000+ iterations)

Calculate cumulative equity for each shuffle

Build distribution of final outcomes

Output

The stress test table shows:

Median Outcome: 50th percentile result

5th Percentile: Worst 5% of outcomes

95th Percentile: Best 95% of outcomes

Success Rate: Percentage of simulations that were profitable

Interpretation

If 95% of simulations are profitable: Strategy is robust

If median is far from actual result: High variance/unreliability

If 5th percentile shows large loss: High tail risk

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WALK-FORWARD ANALYSIS

Purpose

Walk-Forward Analysis (WFA) is the gold standard for detecting strategy overfitting. It simulates real-world trading by dividing historical data into rolling "training" (in-sample) and "validation" (out-of-sample) periods. A strategy that performs well on unseen data is more likely to succeed in live trading.

Method

The implementation uses a non-overlapping window approach following AmiBroker's gold standard methodology:

Segment Calculation: Total trades divided into N windows (default: 12), IS = ~75%, OOS = ~25%, Step = OOS length

Window Structure: Each window has IS (training) followed by OOS (validation). Each OOS becomes the next window's IS (rolling forward)

Metrics Calculated: CAGR, Sharpe, Sortino, MaxDD, Win Rate, Expectancy, Profit Factor, Payoff

Aggregation: IS metrics averaged across all IS periods, OOS metrics averaged across all OOS periods

Output

IS CAGR: In-sample annualized return

OOS CAGR: Out-of-sample annualized return ( THE key metric )

IS/OOS Sharpe: In/out-of-sample risk-adjusted return

Success Rate: % of OOS windows that were profitable

Interpretation

Robust: IS/OOS CAGR gap <20%, OOS Success Rate >80%

Some Overfitting: CAGR gap 20-50%, Success Rate 50-80%

Severe Overfitting: CAGR gap >50%, Success Rate <50%

Key Principles:

OOS is what matters — Only OOS predicts live performance

Consistency > Magnitude — 10% IS / 9% OOS beats 30% IS / 5% OOS

Window count — More windows = more reliable validation

Non-overlapping OOS — Prevents data leakage

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ TABLE DISPLAY

Main Table — Organized into three sections:

Performance Metrics (Cols 0-6): Net Profit, Payoff, Sample Size, Profit Factor, CAGR, Expectancy, Monthly

Trade Statistics (Cols 7-14): Avg Duration, Max CW, Max CL, Win, BE, Loss, Frequency, Exposure

Risk Metrics (Cols 15-22): Sharpe, Sortino, Max DD, RoR, R², MAR, CVaR, p-value

Color Coding

🟢 Green: Excellent performance

🟠 Orange: Acceptable performance

⚪ Gray: Neutral / Fair

🔴 Red: Poor performance

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ IMPLEMENTATION NOTES

Data Source: All metrics calculated from strategy.closedtrades , ensuring compatibility with any Pine Script strategy

Calculation Timing: All calculations occur on barstate.islastconfirmedhistory to optimize performance

Limitations: Requires at least 1 closed trade for basic metrics, 30+ trades for reliable statistical analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ QUICK NOTES

➙ This library has been developed and refined over two years of real-world strategy testing. Every calculation has been validated against industry-standard quantitative finance references.

➙ The entire codebase is thoroughly documented inline. If you are curious about how a metric is calculated or want to understand the implementation details, dive into the source code -- it is written to be read and learned from.

➙ This description focuses on usage and concepts rather than exhaustively listing every exported type and function. The library source code is thoroughly documented inline -- explore it to understand implementation details and internal logic.

➙ All calculations execute on barstate.islastconfirmedhistory to minimize runtime overhead. The library is designed for efficiency without sacrificing accuracy.

➙ Beyond analysis, this library serves as a learning resource. Study the source code to understand quantitative finance concepts, Pine Script advanced techniques, and proper statistical methodology.

➙ Metrics are their own not binary good/bad indicators. A high Sharpe ratio with low sample size is misleading. A deep drawdown during a market crash may be acceptable. Study each function and metric individually -- evaluate your strategy contextually, not by threshold alone.

➙ All strategies face alpha decay over time. Instead of over-optimizing a single strategy on one timeframe and market, build a diversified portfolio across multiple markets and timeframes. Deeptest helps you validate each component so you can combine robust strategies into a trading portfolio.

➙ Screenshots shown in the documentation are solely for visual representation to demonstrate how the tables and metrics will be displayed. Please do not compare your strategy's performance with the metrics shown in these screenshots -- they are illustrative examples only, not performance targets or benchmarks.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW-TO

Using Deeptest is intentionally straightforward. Just import the library and call DT.runDeeptest() at the end of your strategy code in main scope. .

//@version=6

strategy("My Strategy", overlay=true)

// Import the library

import Fractalyst/Deeptest/1 as DT

// Your strategy logic

fastMA = ta.sma(close, 10)

slowMA = ta.sma(close, 30)

if ta.crossover(fastMA, slowMA)

strategy.entry("Long", strategy.long)

if ta.crossunder(fastMA, slowMA)

strategy.close("Long")

// Run the analysis

DT.runDeeptest()

And yes... it's compatible with any TradingView Strategy! 🪄

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Author: @Fractalyst

Font Library: by @fikira - @kaigouthro - @Duyck

Community: Inspired by the @PineCoders community initiative, encouraging developers to contribute open-source libraries and continuously enhance the Pine Script ecosystem for all traders.

if you find Deeptest valuable in your trading journey, feel free to use it in your strategies and give a shoutout to @Fractalyst -- Your recognition directly supports ongoing development and open-source contributions to Pine Script.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ DISCLAIMER

This library is provided for educational and research purposes. Past performance does not guarantee future results. Always test thoroughly and use proper risk management. The author is not responsible for any trading losses incurred through the use of this code.

Quality-Controlled Trend Strategy v2 (Expectancy Focused)This script focuses on quality control rather than curve-fitting.

No repainting, no intrabar tricks, no fake equity curves.

It uses confirmed-bar entries, ATR-based risk, and clean trend logic so backtests reflect what could actually be traded live.

If you publish scripts, this is the minimum structure worth sharing.

Why this script exists

TradingView’s public scripts are flooded with:

repainting indicators

no stop-loss logic

curve-fit entries that collapse live

strategies that look good only in hindsight

This script is intentionally boring but honest.

No repainting.

No intrabar tricks.

No fake equity curves

The goal is quality control, not hype.

What this strategy enforces

✔ Confirmed bars only

✔ Single source of truth for indicators

✔ Fixed risk structure

✔ No signal repainting

✔ Clean exits with unique IDs

✔ Works on any liquid market

Trading Logic (simple & auditable)

Trend filter

EMA 50 vs EMA 200

Entry

Pullback to EMA 50

RSI confirms momentum (not oversold/overbought)

Risk

ATR-based stop

Fixed R:R

One position at a time

This is the minimum bar for a strategy to be considered publish-worthy.

Why this helps TradingView quality

Most low-value scripts fail because they:

hide repainting logic

skip exits entirely

use inconsistent calculations

rely on hindsight candles

This strategy forces discipline:

every signal is confirmed

every trade has defined risk

behavior is repeatable across symbols & timeframes

If more scripts followed this baseline, TradingView’s public library would be far more usable.

4MA / 4MA[1] Forward Projection with 4 SD Forecast Bands4MA / 4MA Projection + 4 SD Bands + Cross Table is a forward-projection tool built around a simple moving average pair: the 4-period SMA (MA4) and its 1-bar lagged value (MA4 ). It takes a prior MA behavior pattern, projects that structure forward, and wraps the projected mean path with four Standard Deviation (SD) bands to visualize probable future price ranges.

This indicator is designed to help you anticipate:

Where the MA structure is likely to travel next

How wide the “expected” future price corridor may be

Where a future MA4 vs MA4 crossover is most likely to occur

When the real (live) crossover actually prints on the chart

What you see on the chart

1) Live moving averages (current market)

MA4 tracks the short-term mean of price.

MA4 is simply the previous bar’s MA4 value (a 1-bar lag).

Their relationship (MA4 above/below MA4 ) gives a clean, minimal read on trend alignment and directional bias.

2) Projected MA path (forward curve)

A forward “ghost” of the MA structure is drawn ahead of price. This projected curve represents the indicator’s best estimate of how the moving average structure may evolve if the market continues to rhyme with the selected historical behavior window.

3) 4 Standard Deviation bands (predictive future price ranges)

Surrounding the projected mean path are four SD envelopes. Think of these as forecast corridors:

Inner bands = tighter “expected” range

Outer bands = wider “stress / extreme” range

These bands are not a guarantee—rather, they’re a structured way to visualize “how far price can reasonably swing” around the projected mean based on observed volatility.

4) Vertical projection lines (most probable cross zone)

Within the projected region you’ll see vertical lines running through the bands. These lines mark the most probable zone where MA4 and MA4 are expected to cross in the projection.

In plain terms:

The projected MAs are two curves.

When those curves are forecasted to intersect, the script marks the intersection region with a vertical line.

This gives you a forward “timing window” for a potential MA shift.

5) Cross Table (top-right)

The table is your confirmation layer. It reports:

Current MA4 value

Current MA4 value

Whether MA4 is above or below MA4

The most recent BUY / SELL cross event

When a real, live crossover happens on the actual chart:

It registers as BUY (MA4 crosses above MA4 )

Or SELL (MA4 crosses below MA4 )

…and the table updates immediately so you can confirm the event without guessing.

How to use it

Practical workflow

Use the projected SD bands as future range context

If price is projected to sit comfortably inside inner bands, the market is behaving “normally.”

If price reaches outer bands, you’re in a higher-volatility / stretched scenario.

Use vertical lines as a “watch zone”

Vertical lines do not force a trade.

They act like a forward “heads-up”: this is the most likely window for an MA crossover to occur if the projection holds.

Use the table for confirmation

When the crossover happens for real, the table is your confirmation signal.

Combine it with structure (support/resistance, trendlines, market context) rather than trading it in isolation.

Notes and best practices

This is a projection tool: it helps visualize a structured forward hypothesis, not a certainty.

SD bands are best used as forecast corridors (risk framing, range planning, and expectation management).

The table is the execution/confirmation layer: it tells you what the MAs are doing now.

Wavelet Candle Constructor (Inc. Morlet) 2Here is the detailed description of the **Wavelet Candle** construction principles based on the code provided.

This indicator is not a simple smoothing mechanism (like a Moving Average). It utilizes the **Discrete Wavelet Transform (DWT)**, specifically the Stationary variant (SWT / à Trous Algorithm), to separate "noise" (high frequencies) from the "trend" (low frequencies).

Here is how it works step-by-step:

###1. The Wavelet Kernel (Coefficients)The heart of the algorithm lies in the coefficients (the `h` array in the `get_coeffs` function). Each wavelet type represents a different set of mathematical weights that define how price data is analyzed:

* **Haar:** The simplest wavelet. It acts like a simple average of neighboring candles. It reacts quickly but produces a "boxy" or "jagged" output.

* **Daubechies 4:** An asymmetric wavelet. It is better at detecting sudden trend changes and the fractal structure of the market, though it introduces a slight phase shift.

* **Symlet / Coiflet:** More symmetric than Daubechies. They attempt to minimize lag (phase shift) while maintaining smoothness.

* **Morlet (Gaussian):** Implemented in this code as a Gaussian approximation (bell curve). It provides the smoothest, most "organic" effect, ideal for filtering noise without jagged edges.

###2. The Convolution EngineInstead of a simple average, the code performs a mathematical operation called **convolution**:

For every candle on the chart, the algorithm takes past prices, multiplies them by the Wavelet Kernel weights, and sums them up. This acts as a **digital low-pass filter**—it allows the main price movements to pass through while cutting out the noise.

###3. The "à Trous" Algorithm (Stationary Wavelet Transform)This is the key difference between this indicator and standard data compression.

In a classic wavelet transform, every second data point is usually discarded (downsampling). Here, the **Stationary** approach is used:

* **Level 1:** Convolution every **1** candle.

* **Level 2:** Convolution every **2** candles (skipping one in between).

* **Level 3:** Convolution every **4** candles.

* **Level 4:** Convolution every **8** candles.

Because of this, **we do not lose time resolution**. The Wavelet Candle is drawn exactly where the original candle is, but it represents the trend structure from a broader perspective. The higher the `Decomposition Level`, the deeper the denoising (looking at a wider context).

###4. Independent OHLC ProcessingThe algorithm processes each component of the candle separately:

1. Filters the **Open** series.

2. Filters the **High** series.

3. Filters the **Low** series.

4. Filters the **Close** series.

This results in four smoothed curves: `w_open`, `w_high`, `w_low`, `w_close`.

###5. Geometric Reconstruction (Logic Repair)Since each price series is filtered independently, the mathematics can sometimes lead to physically impossible situations (e.g., the smoothed `Low` being higher than the smoothed `High`).

The code includes a repair section:

```pinescript

real_high = math.max(w_high, w_low)

real_high := math.max(real_high, math.max(w_open, w_close))

// Same logic for Low (math.min)

```

This guarantees that the final Wavelet Candle always has a valid construction: wicks encapsulate the body, and the `High` is strictly the highest point.

---

###Summary of ApplicationThis construction makes the Wavelet Candle an **excellent trend-following tool**.

* If the candle is **green**, it means that after filtering the noise (according to the selected wavelet), the market energy is bullish.

* If it is **red**, the energy is bearish.

* The wicks show volatility that exists within the bounds of the selected decomposition level.

Here is a descriptive comparison of **Wavelet Candles** against other popular chart types. As requested, this is a narrative explanation focusing on the differences in mechanics, interpretation philosophy, and the specific pros and cons of each approach.

---

###1. Wavelet Candles vs. Standard (Japanese) CandlesThis is a clash between "the raw truth" and "mathematical interpretation." Standard Japanese candles display raw market data—exactly what happened on the exchange. Wavelet Candles are a synthetic image created by a signal processor.

**Differences and Philosophy:**

A standard candle is full of emotion and noise. Every single price tick impacts its shape. The Wavelet Candle treats this noise as interference that must be removed to reveal the true energy of the trend. Wavelets decompose the price, reject high frequencies (noise), and reconstruct the candle using only low frequencies (the trend).

* **Wavelet Advantages:** The main advantage is clarity. Where a standard chart shows a series of confusing candles (e.g., a long green one, followed by a short red one, then a doji), the Wavelet Candle often draws a smooth, uniform wave in a single color. This makes it psychologically easier to hold a position and ignore temporary pullbacks.

* **Wavelet Disadvantages:** The biggest drawback is the loss of price precision. The Open, Close, High, and Low values on a Wavelet candle are calculated, not real. You **cannot** place Stop Loss orders or enter trades based on these levels, as the actual market price might be in a completely different place than the smoothed candle suggests. They also introduce lag, which depends on the chosen wavelet—whereas a standard candle reacts instantly.

###2. Wavelet Candles vs. Heikin AshiThese are close cousins, but they share very different "DNA." Both methods aim to smooth the trend, but they achieve it differently.

**Differences and Philosophy:**

Heikin Ashi (HA) is based on a simple recursive arithmetic average. The current HA candle depends on the previous one, making it react linearly.

The Wavelet Candle uses **convolution**. This means the shape of the current candle depends on a "window" (group) of past candles multiplied by weights (Gaussian curve, Daubechies, etc.). This results in a more "organic" and elastic reaction.

* **Wavelet Advantages:** Wavelets are highly customizable. With Heikin Ashi, you are stuck with one algorithm. With Wavelet Candles, you can change the kernel to "Haar" for a fast (boxy) reaction or "Morlet" for an ultra-smooth, wave-like effect. Wavelets handle the separation of market cycles better than simple HA averaging, which can generate many false color flips during consolidation.

* **Wavelet Disadvantages:** They are computationally much more complex and harder to understand intuitively ("Why is this candle red if the price is going up?"). In strong, vertical breakouts (pumps), Heikin Ashi often "chases" the price faster, whereas deep wavelet decomposition (High Level) may show more inertia and change color more slowly.

###3. Wavelet Candles vs. RenkoThis compares two different dimensions: Time vs. Price.

**Differences and Philosophy:**

Renko completely ignores time. A new brick is formed only when the price moves by a specific amount. If the market stands still for 5 hours, nothing happens on a Renko chart.

The Wavelet Candle is **time-synchronous**. If the market stands still for 5 hours, the Wavelet algorithm will draw a series of flat, small candles (the "wavelet decays").

* **Wavelet Advantages:** They preserve the context of time, which is crucial for traders who consider trading sessions (London/New York) or macroeconomic data releases. On a wavelet chart, you can see when volatility drops (candles become small), whereas Renko hides periods of stagnation, which can be misleading for options traders or intraday strategies.

* **Wavelet Disadvantages:** In sideways trends (chop), Wavelet Candles—despite the smoothing—will still draw a "snake" that flips colors (unless you set a very high decomposition level). Renko can remain perfectly clean and static during the same period, not drawing any new bricks, which for many traders is the ultimate filter against overtrading in a flat market.

###Summary**Wavelet Candles** are a tool for the analyst who wants to visualize the **structure of the wave and market cycle**, accepting some lag in exchange for noise reduction, but without giving up the time axis (like in Renko) or relying on simple averaging (like in Heikin Ashi). It serves best as a "roadmap" for the trend rather than a "sniper scope" for precise entries.

Fourier Extrapolator of 'Caterpillar' SSA of Price [Loxx]Fourier Extrapolator of 'Caterpillar' SSA of Price is a forecasting indicator that applies Singular Spectrum Analysis to input price and then injects that transformed value into the Quinn-Fernandes Fourier Transform algorithm to generate a price forecast. The indicator plots two curves: the green/red curve indicates modeled past values and the yellow/fuchsia dotted curve indicates the future extrapolated values.

What is the Fourier Transform Extrapolator of price?

Fourier Extrapolator of Price is a multi-harmonic (or multi-tone) trigonometric model of a price series xi, i=1..n, is given by:

xi = m + Sum( a*Cos(w*i) + b*Sin(w*i), h=1..H )

Where:

xi - past price at i-th bar, total n past prices;

m - bias;

a and b - scaling coefficients of harmonics;

w - frequency of a harmonic ;

h - harmonic number;

H - total number of fitted harmonics.

Fitting this model means finding m, a, b, and w that make the modeled values to be close to real values. Finding the harmonic frequencies w is the most difficult part of fitting a trigonometric model. In the case of a Fourier series, these frequencies are set at 2*pi*h/n. But, the Fourier series extrapolation means simply repeating the n past prices into the future.

Quinn-Fernandes algorithm find sthe harmonic frequencies. It fits harmonics of the trigonometric series one by one until the specified total number of harmonics H is reached. After fitting a new harmonic , the coded algorithm computes the residue between the updated model and the real values and fits a new harmonic to the residue.

see here: A Fast Efficient Technique for the Estimation of Frequency , B. G. Quinn and J. M. Fernandes, Biometrika, Vol. 78, No. 3 (Sep., 1991), pp . 489-497 (9 pages) Published By: Oxford University Press

Fourier Transform Extrapolator of Price inputs are as follows:

npast - number of past bars, to which trigonometric series is fitted;

nharm - total number of harmonics in model;

frqtol - tolerance of frequency calculations.

What is Singular Spectrum Analysis ( SSA )?

Singular spectrum analysis ( SSA ) is a technique of time series analysis and forecasting. It combines elements of classical time series analysis, multivariate statistics, multivariate geometry, dynamical systems and signal processing. SSA aims at decomposing the original series into a sum of a small number of interpretable components such as a slowly varying trend, oscillatory components and a ‘structureless’ noise. It is based on the singular value decomposition ( SVD ) of a specific matrix constructed upon the time series. Neither a parametric model nor stationarity-type conditions have to be assumed for the time series. This makes SSA a model-free method and hence enables SSA to have a very wide range of applicability.