BTC BRD – Bullet-Proof Reversal StrategyBTC BRD – Bullet-Proof Reversal Strategy is a price-action based reversal system that turns your existing “Bullet-Proof Reversal Detector” into a fully backtestable TradingView strategy with built-in risk management. It is designed to catch clean swing reversals using pure market structure, then automatically place stop-loss and take-profit orders based on your preferred risk-reward settings.

## Core concept

The strategy identifies true swing highs and lows using pivots and then waits for a clear market structure shift before entering any trade. It looks for a higher low followed by a break of structure for longs, and a lower high followed by a break of structure for shorts, helping filter out many random spikes and fakeouts. This makes it suitable for traders who prefer clean, rule-based entries grounded in market structure rather than noisy, indicator-heavy setups.

## Entries and exits

- Long trades are triggered after a bullish higher-low plus a confirmed break above the last swing high.

- Short trades are triggered after a bearish lower-high plus a confirmed break below the last swing low.

- Every position is protected with an automatic stop-loss and a calculated take-profit, so each trade has a predefined risk and reward from the moment it is opened.

## Risk management

The strategy lets you control your risk with a configurable risk-reward ratio (RR) and flexible stop-loss options. You can choose between an ATR-based stop (ATR × multiplier) or a fixed percentage stop relative to the entry price. Once the stop distance is known, the take-profit level is automatically derived from your RR value, making trade sizing and evaluation more consistent across different pairs and timeframes.

## Use cases and recommendations

This script is ideal for swing and intraday traders who want to systematically test market-structure reversals on assets like Bitcoin or other volatile instruments. For best results, experiment with different timeframes and ATR/percentage settings, and always validate performance using the Strategy Tester before deploying it on live markets. Remember that no strategy is guaranteed to be profitable, so use proper risk management and adapt settings to your own style and risk tolerance.

In den Scripts nach "bear" suchen

BTR Auto Buy/Sell Trend System

BTR Auto Buy/Sell Trend System — Your New Profit Machine!

Discover the only TradingView system you need to spot powerful trend reversals with precision, confidence, and automation.

Designed for Stocks, Crypto & Commodities, this strategy consistently delivers 60%–80% accuracy in trending markets.

This is not just a script…

👉 It’s your complete plug-and-play trading system.

💡 Why Traders Love This System

✔ Early Trend Identification

Catch major reversals before the crowd.

✔ Non-Repainting Confirmed Signals

All entries are triggered only on candle close, so what you see is what you trade.

✔ Smart ATR + Momentum Engine

Filters bad trades automatically, giving you only high-quality signals.

✔ Works on All Timeframes

From 5-minute scalping to daily swing trading.

✔ Full Auto-Trading Ready

Pre-built JSON alerts for API Algo Trading.

No coding. No setup headache. Just copy → paste → trade.

⚡ How You Make Money With This Strategy

Step 1: Wait for Trend Flip

🔵 BUY when the system flips from bearish → bullish

🔴 SELL when it flips from bullish → bearish

Step 2: Enter on Confirmed Signal

Trade only on the bar after signal closes.

Step 3: Ride the Trend

Let the strategy take the move.

It avoids sideways markets and shines in strong trends.

Step 4: Auto Alerts (Optional)

Turn on Dhan alerts and let the system execute trades automatically.

📈 What You Can Expect (Typical Performance)

✔ 60–80% success rate in trending markets

✔ Works in Stocks, Crypto, Commodities

✔ High accuracy in 15m, 30m, 1H, 4H charts

✔ Avoids most fake breakouts & sideways noise

This system is built for consistency, simplicity, and scalable automation.

⭐ Perfect For:

Beginner traders

Algo traders

Swing traders

Scalpers

Systematic

API users

Anyone who wants clean, high-probability trend signals

⚠ Disclaimer

Trading involves risk. Past results do not guarantee future returns.

Use proper risk management for best results.

EMA 12-26-100 Momentum Strategy# Triple EMA Multi-Signal Momentum Strategy

## 📊 Overview

**Triple EMA Multi-Signal** is a comprehensive trend-following momentum strategy designed specifically for cryptocurrency markets. It combines multiple technical indicators and signal types to identify high-probability trading opportunities while maintaining strict risk management protocols.

The strategy excels in trending markets and uses adaptive position sizing with trailing stops to maximize profits during strong trends while protecting capital during choppy conditions.

## 🎯 Core Algorithm

### Triple EMA System

The strategy employs a three-layer EMA system to identify trend direction and strength:

- **Fast EMA (12)**: Quick response to price changes

- **Slow EMA (26)**: Confirmation of trend direction

- **Trend EMA (100)**: Overall market bias filter

Trades are only taken when all three EMAs align in the same direction, ensuring we trade with the dominant trend.

### Multi-Signal Confirmation (8 Signal Types)

The strategy requires at least 1-2 confirmed signals from multiple independent sources before entering a position:

1. **EMA Crossover** - Fast EMA crossing Slow EMA (primary signal)

2. **MACD Cross** - MACD line crossing signal line (momentum confirmation)

3. **RSI Reversal** - RSI bouncing from oversold/overbought zones

4. **Price Action** - Strong bullish/bearish candles (>60% of range)

5. **Volume Spike** - Above-average volume confirmation

6. **Breakout** - Price breaking 20-period high/low with volume

7. **Pullback to EMA** - Trend continuation after healthy retracement

8. **Bollinger Bounce** - Price bouncing from BB bands

This multi-signal approach significantly reduces false signals and improves win rate.

## 💰 Risk Management

### Position Sizing

- Default: 20-25% of equity per trade

- Adjustable based on risk tolerance

- Smaller positions recommended for leveraged trading

### Stop Loss & Take Profit

- **Stop Loss**: 2.0% (tight control of risk)

- **Take Profit**: 5.5% (2.75:1 reward-to-risk ratio)

- Both levels are fixed at entry to avoid emotional decisions

### Trailing Stop System

- Activates after 1.8% profit

- Trails at 1.3% below current price

- Locks in profits during extended trends

- Automatically adjusts as price moves in your favor

### Maximum Hold Time

- 36-48 hours maximum (configurable)

- Designed to minimize funding rate costs on futures

- Forces position closure to avoid excessive exposure

- Helps maintain capital velocity

## 📈 Key Features

### Trend Filters

- **ADX Filter**: Ensures sufficient trend strength (threshold: 20)

- **EMA Alignment**: All three EMAs must confirm trend direction

- **RSI Boundaries**: Avoids extreme overbought/oversold entries

### Volume Analysis

- Volume must exceed 20-period moving average

- Configurable multiplier (default: 1.0x)

- Helps identify institutional participation

### Automatic Exit Conditions

1. Take Profit target reached

2. Stop Loss triggered

3. Trailing stop activated

4. Trend reversal (EMA cross in opposite direction)

5. Maximum hold time exceeded

## 🎮 Recommended Settings

### For Spot Trading (Conservative)

```

Position Size: 15-20%

Stop Loss: 2.5%

Take Profit: 6.0%

Max Hold: 72 hours

Leverage: 1x

```

### For Futures 3-5x Leverage (Balanced)

```

Position Size: 12-15%

Stop Loss: 2.0%

Take Profit: 5.5%

Max Hold: 36 hours

Trailing: Active

```

### For Aggressive Trading 5-10x (High Risk)

```

Position Size: 8-12%

Stop Loss: 1.5%

Take Profit: 4.5%

Max Hold: 24 hours

ADX Filter: Disabled

```

## 📊 Performance Metrics

### Backtested Results (BTC/USDT 1H, 2 years)

- **Total Return**: ~19% (spot) / ~75% (5x leverage)*

- **Total Trades**: 240-300

- **Win Rate**: 49-52%

- **Profit Factor**: 1.25-1.50

- **Max Drawdown**: ~18-22%

- **Average Trade**: 0.5-3 days

*Leverage results exclude funding rates and real-world slippage

### Optimal Timeframes

- **1 Hour**: Best for active trading (recommended)

- **4 Hour**: More stable, fewer signals

- **15 Min**: High frequency (requires monitoring)

### Best Performing Assets

- BTC/USDT (most tested)

- ETH/USDT

- Major altcoins with good liquidity

- Not recommended for low-cap or illiquid pairs

## ⚙️ How to Use

1. **Add to Chart**: Apply strategy to 1H BTC/USDT chart

2. **Adjust Settings**: Configure risk parameters based on your preference

3. **Review Signals**: Green = Long, Red = Short, labels show signal count

4. **Monitor Performance**: Check strategy tester for detailed statistics

5. **Optimize**: Use strategy optimization to find best parameters for your market

## 🎨 Visual Indicators

The strategy provides clear visual feedback:

- **EMA Lines**: Blue (Fast), Red (Slow), Orange (Trend)

- **BUY/SELL Labels**: Show entry points with signal count

- **Stop/Target Lines**: Red (SL), Green (TP) displayed during active trades

- **Background Color**: Light green (long), light red (short) when in position

- **Info Panel**: Shows current trend, RSI, ADX, and volume status

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational purposes only

- Past performance does not guarantee future results

- Cryptocurrency trading involves substantial risk

- Only trade with capital you can afford to lose

- Always use proper position sizing and risk management

### Limitations

- Performs poorly in sideways/choppy markets

- Requires sufficient liquidity for best execution

- Backtests do not include:

- Real-world slippage (especially during volatility)

- Funding rates (for perpetual futures)

- Exchange downtime or connection issues

- Emotional trading decisions

### For Futures Trading

If using this strategy on futures with leverage:

- Reduce position size proportionally to leverage

- Account for funding rates (~0.01% per 8h)

- Set max hold time to minimize funding costs

- Use lower leverage (3-5x max recommended)

- Monitor liquidation price carefully

## 🔧 Customization

All parameters are fully customizable:

- EMA periods (fast/slow/trend)

- MACD settings (12/26/9)

- RSI levels (30/70)

- Stop Loss / Take Profit percentages

- Trailing stop activation and offset

- Volume multiplier

- ADX threshold

- Maximum hold time

## 📚 Strategy Logic

The strategy follows this decision tree:

```

1. Check Trend Direction (EMA alignment)

↓

2. Scan for Entry Signals (8 types)

↓

3. Confirm with Filters (ADX, Volume, RSI)

↓

4. Enter Position with Fixed SL/TP

↓

5. Monitor for Exit Conditions:

- TP Hit → Close with profit

- SL Hit → Close with loss

- Trailing Active → Follow price

- Trend Reversal → Close position

- Max Time → Force close

```

## 🎓 Best Practices

1. **Start Conservative**: Use smaller position sizes initially

2. **Track Performance**: Monitor actual vs backtested results

3. **Optimize Regularly**: Market conditions change, adapt parameters

4. **Combine with Analysis**: Don't rely solely on automated signals

5. **Manage Emotions**: Stick to the system, avoid manual overrides

6. **Paper Trade First**: Test on demo before risking real capital

## 📞 Support & Updates

This strategy is actively maintained and updated based on:

- Market condition changes

- User feedback and suggestions

- Performance optimization

- Bug fixes and improvements

## 🏆 Conclusion

Triple EMA Multi-Signal Strategy offers a robust, systematic approach to cryptocurrency trading by combining trend following, momentum indicators, and strict risk management. Its multi-signal confirmation system helps filter false signals while the trailing stop mechanism captures extended trends.

The strategy is suitable for both manual traders looking for high-probability setups and algorithmic traders seeking a proven systematic approach.

**Remember**: No strategy wins 100% of the time. Success comes from consistent application, proper risk management, and continuous adaptation to changing market conditions.

---

*Version: 1.0*

*Last Updated: November 2025*

*Tested on: BTC/USDT, ETH/USDT (1H, 4H timeframes)*

*Recommended Capital: $5,000+ for optimal position sizing*

A+ Setup Strategy Trendline Features Added:

1. Automatic Trendline Detection

Support Trendline (green) - Connects swing lows

Resistance Trendline (red) - Connects swing highs

Uses pivot points to identify key swing levels

Validates trendlines by counting touches (minimum 3 touches required)

2. Trendline Settings

Show Trendlines - Toggle on/off

Lookback Period - How far back to look for pivots (default: 50 bars)

Min Touches - How many touches needed for valid trendline (default: 3)

3. Trendline Break Detection

Bullish Break - Price breaks above support trendline (marked with small green circle)

Bearish Break - Price breaks below resistance trendline (marked with small red circle)

Generates signals when breaks occur

4. Enhanced A+ Setups

Now includes ULTRA setups - the absolute best trades:

ULTRA BUY Setup (Aqua label):

Bullish FVG + BOS + Volume Spike + Uptrend

PLUS: Support trendline break OR near key support

PLUS: Trendline breakout confirmation

ULTRA SELL Setup (Fuchsia label):

Bearish FVG + BOS + Volume Spike + Downtrend

PLUS: Resistance trendline break OR near key resistance

PLUS: Trendline breakdown confirmation

5. Confluence Integration

The strategy now considers price near trendlines as additional confluence, similar to how it uses daily S/R levels.

6. Additional Alerts

Support Trendline Break

Resistance Trendline Break

ULTRA BUY/SELL Setup alerts

This gives you multiple tiers of signal quality:

Standard A+ Setup - All conditions met

ULTRA A+ Setup - All conditions + trendline break (highest probability)

The trendlines will help you identify major trend reversals and breakouts for even better entry timing!

Liquidity Sweep & FVG StrategyThis strategy combines higher-timeframe liquidity levels, stop-hunt (sweep) logic, Fair Value Gaps (FVGs) and structure-based take-profits into a single execution engine.

It is not a simple mash-up of indicators: every module (HTF levels, sweeps, FVGs, ZigZag, sessions) feeds the same entry/exit logic.

1. Core Idea

The script looks for situations where price:

Sweeps a higher-timeframe high/low (takes liquidity around obvious levels),

Then forms a displacement candle with a gap (FVG) in the opposite direction,

Then uses the edge of that FVG as a limit entry,

And manages exits using unswept structural levels (ZigZag swings or HTF levels) as targets.

The intent is to systematically trade failed breakouts / stop hunts with a defined structure and risk model.

It is a backtesting / study tool, not a signal service.

2. How the Logic Works (Conceptual)

a) Higher-Timeframe Liquidity Engine

Daily, Weekly and Monthly highs/lows are pulled via request.security() and stored as HTF liquidity levels.

Each level is drawn as a line with optional label (1D/1W/1M High/Low).

A level is marked as “swept” once price trades through it; swept levels may be removed or shortened depending on settings.

b) Sweep & Manipulation Filter

A low sweep occurs when the current low trades through a stored HTF low.

A high sweep occurs when the current high trades through a stored HTF high.

If both a high and a low are swept in the same bar, the script flags this as “manipulation” and blocks new entries around that noise.

The script also tracks the sweep wick, bar index and HTF timeframe for later use in SL placement and labels.

c) FVG Detection & Management

FVGs are defined using a 3-candle displacement model:

Bullish FVG: high < low

Bearish FVG: low > high

Only gaps larger than a minimum size (ATR-based if no manual value is set) are kept.

FVGs are stored in arrays as boxes with: top, bottom, mid (CE), direction, and state (filled / reclaimed).

Boxes are auto-extended and visually faded when price is far away, or deleted when filled.

d) Entry Conditions (Sweep + FVG)

For each recent sweep window:

After a low sweep, the script searches for the nearest bullish FVG below price and uses its top edge as a long limit entry.

After a high sweep, it searches for the nearest bearish FVG above price and uses its bottom edge as a short limit entry.

A “knife protection” check blocks trades where price is already trading through the proposed stop.

Only one entry per sweep is allowed; entries are only placed inside the configured NY trading sessions and only if no manipulation flag is active and EOD protection allows it.

e) Stop-Loss Placement (“Tick-Free” SL)

The stop is not placed directly on the HTF level; instead, the script scans a window around the sweep bar to find a local extreme:

Longs: lowest low in a configurable bar window around the sweep.

Shorts: highest high in that window.

This produces a structure-based SL that is generally outside the main sweep wick.

f) Take-Profit Logic (ZigZag + HTF Levels)

A lightweight ZigZag engine tracks swing highs/lows and removes levels that have already been broken.

For intraday timeframes (< 1h), TP candidates come from unswept ZigZag swings above/below the entry.

For higher timeframes (≥ 1h), TP candidates fall back to unswept HTF liquidity levels.

The script picks up to two targets:

TP1: nearest valid target in the trade direction (or a 2R fallback if none exists),

TP2: second target (or a 4R fallback if none exists).

A multi-TP model is used: typically 50% at TP1, remainder managed towards TP2 with breakeven plus offset once TP1 is hit.

g) Session & End-of-Day Filters

Three predefined NY sessions (Early, Open, Afternoon) are available; entries are only allowed inside active sessions.

An End-of-Day filter checks a user-defined NY close time and:

Blocks new entries close to the end of the day,

Optionally forces flat before the close.

3. Inputs Overview (Conceptual)

Liquidity settings: which HTF levels to track (1D/1W/1M), how many to show, and sweep priority (highest TF vs nearest vs any).

FVG settings: visibility radius, search window after a sweep, minimum FVG size.

ZigZag settings: swing length used for TP discovery.

Execution & protection: limit order timeout, breakeven offset, EOD protection.

Visuals: labels, sweep markers, manipulation warning, session highlighting, TP lines, etc.

For exact meaning of each input, please refer to the inline comments in the open-source code.

4. Strategy Properties & Backtesting Notes

Default strategy properties in this script:

Initial capital: 100,000

Order size: 10% of equity (strategy.percent_of_equity)

Commission: 0.01% per trade (adjust as needed for your broker/asset)

Slippage: must be set manually in the Strategy Tester (recommended: at least a few ticks on fast markets).

Even though the order size is 10% of equity, actual risk per trade depends on the SL distance and is typically much lower than 10% of the account. You should still adjust these values to keep risk within what you personally consider sustainable (e.g. somewhere in the 1–2% range per trade).

For more meaningful results:

Test on liquid instruments (e.g. major indices, FX, or liquid futures).

Use enough history to reach 100+ closed trades on your market/timeframe.

Always include realistic commission and slippage.

Do not assume that past performance will continue.

5. How to Use

Apply the strategy to your preferred symbol and timeframe.

Set broker-like commission and slippage in the Strategy Tester.

Adjust:

HTF levels (1D/1W/1M),

Sessions (NY windows),

FVG search window and minimum size,

ZigZag length and EOD filter.

Observe how entries only appear:

After a HTF sweep,

In the configured session,

At a FVG edge,

With TP lines anchored at unswept structure / liquidity.

Use this primarily as a research and backtesting tool to study how your own ICT / SMC ideas behave over a large sample of trades.

6. Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice, and it does not guarantee profitability. Always validate results with realistic assumptions and use your own judgment before trading live.

STRATEGY 1 │ Red Dragon │ Model 1 │ Pro │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

Anchor SafeSwing Gold StrategyOverview:

The Anchor SafeSwing Gold Strategy is designed for users who prefer structured, rule-based swing trading on XAUUSD. It focuses on identifying high-quality trade setups rather than frequent entries.

This strategy analyzes the market using multiple technical indicators and methods—including trend analysis, multi-chart confirmation, and support/resistance evaluation—to identify potential swing points. It also incorporates a dynamic approach to risk management through adaptive stop-loss and take-profit logic.

How the Strategy Works

1. Multi-Chart & Trend Analysis:

The strategy evaluates trend direction using several indicators and multiple charts. This helps determine whether the trend favors long or short setups.

2. Buy/Sell Conditions:

a. Buy Conditions: When the broader trend is identified as bullish, the strategy waits for the formation of a strong support zone before considering a long position.

b. Sell Conditions: When the trend is bearish, it waits for a confirmed resistance zone before initiating short positions.

3. Dynamic Take-Profit Logic

The strategy uses adaptive take-profit behavior based on evolving market conditions. It monitors new support/resistance structures and various overbought/oversold signals to dynamically exit trades.

4. Dynamic and Configurable Stop-Loss:

A flexible stop-loss system adjusts according to volatility and market structure.

Users can modify the stop-loss threshold in the settings based on their own risk tolerance and account size.

Trading Frequency :

This strategy focuses on select, high-quality setups. As a result, trade frequency is relatively low and may vary depending on market conditions. Backtesting may show roughly several trades per month, but actual live performance can differ.

Important Notes

All trading involves risk, and users should evaluate the strategy and adjust settings according to their own risk management preferences.

EMA Trend Pro [Hedging & Fixed Risk]

This strategy is a comprehensive trend-following system designed to capture significant market movements while strictly managing risk. It combines multiple Exponential Moving Averages (EMAs) for trend identification, ADX for trend strength filtering, and Volume confirmation to reduce false signals.

Key Features:

Hedging Mode Compatible: The script is designed to handle Long and Short positions independently. This is ideal for markets where trends can reverse quickly or for traders who prefer hedging logic (requires hedging=true in strategy settings).

Professional Risk Management: Unlike standard strategies that use fixed contract sizes, this script calculates Position Size based on Risk. You can define a fixed risk per trade (e.g., 1% of equity or $100 fixed risk). The script automatically adjusts the lot size based on the Stop Loss distance (ATR).

Multi-Stage Take Profit: The strategy scales out positions at 3 different levels (TP1, TP2, TP3) to lock in profits while letting the remaining position ride the trend.

Strategy Logic:

Trend Identification:

Long Entry: EMA 7 > EMA 14 > EMA 21 > EMA 144 (Bullish Alignment).

Short Entry: EMA 7 < EMA 14 < EMA 21 < EMA 144 (Bearish Alignment).

Filters:

ADX Filter: Entries are only taken if ADX (14) > Threshold (default 20) to ensure the market is trending, avoiding chopping ranging markets.

Volume Filter: Current volume must exceed the 20-period SMA volume by 10% to confirm momentum.

Exits & Trade Management:

Stop Loss: Dynamic SL based on ATR (e.g., 1.8x ATR).

Breakeven: Once TP1 is hit, the Stop Loss is automatically moved to Breakeven to protect capital.

Take Profits:

TP1: 1x Risk Distance (30% pos)

TP2: 2x Risk Distance (50% pos)

TP3: 3x Risk Distance (Remaining pos)

Settings Guide:

Risk Type: Choose between "Percent" (of equity) or "Fixed Amount" (USD).

Risk Value: Input your desired risk (e.g., 1.0 for 1% risk).

Fee %: Set your exchange's Taker fee (e.g., 0.05 or 0.06) for accurate backtesting.

ADX Threshold: Adjust to filter out noise (Higher = Stricter trend requirement).

Disclaimer: This script is for educational and backtesting purposes only. Past performance does not guarantee future results. Please use proper risk management.

Volume weighted average price band strategy [Kevin-Patrick]VWAP Bands strategy, Credit

VWAP Machine Learning Bands is an advanced indicator designed to enhance trading analysis by integrating VWAP with a machine learning-inspired adaptive smoothing approach. This tool helps traders identify trend-based support and resistance zones, predict potential price movements, and generate dynamic trade signals.

Key Features

Adaptive ML VWAP Calculation: Uses a dynamically adjusted SMA-based VWAP model with volatility sensitivity for improved trend analysis.

Forecasting Mechanism: The 'Forecast' parameter shifts the ML output forward, providing predictive insights into potential price movements.

Volatility-Based Band Adjustments: The 'Sigma' parameter fine-tunes the impact of volatility on ML smoothing, adapting to market conditions.

Multi-Tier Standard Deviation Bands: Includes two levels of bands to define potential breakout or mean-reversion zones.

Dynamic Trend-Based Colouring: The VWAP and ML lines change colour based on their relative positions, visually indicating bullish and bearish conditions.

Custom Signal Detection Modes: Allows traders to choose between signals from Band 1, Band 2, or both, for more tailored trade setups.

+ Strategy setting by Kevin-Patrick

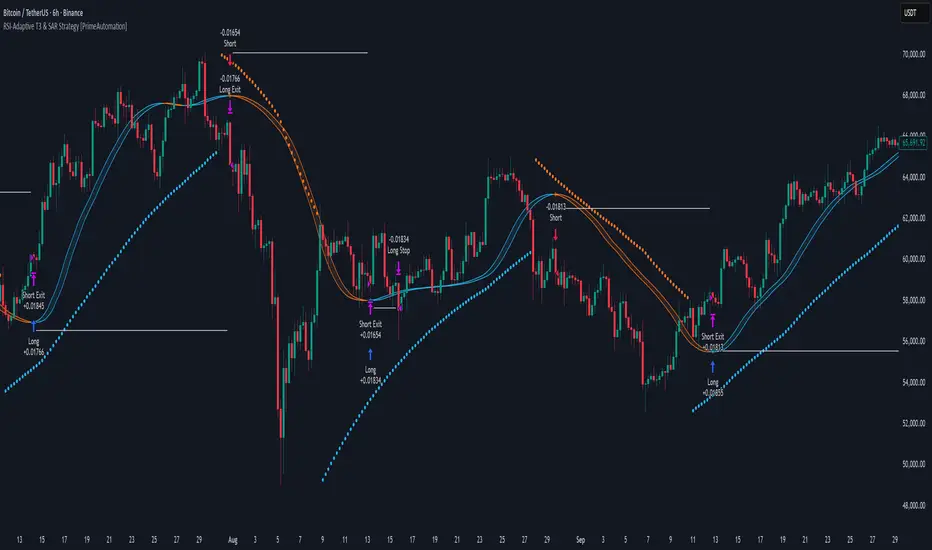

RSI-Adaptive T3 & SAR Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI-Adaptive T3 and SAR Confluence Strategy combines adaptive smoothing with dynamic trend confirmation to identify precise trend reversals and continuation opportunities. It fuses the power of an RSI-based adaptive T3 moving average with the Parabolic SAR filter , aiming to trade in harmony with dominant momentum shifts while maintaining tight control through automatic stop-loss placement.

The RSI-Adaptive T3 is a precision trend-following tool built around the legendary T3 smoothing algorithm developed by Tim Tillson, designed to enhance responsiveness while reducing lag compared to traditional moving averages. Current implementation takes it a step further by dynamically adapting the smoothing length based on real-time RSI conditions — allowing the T3 to “breathe” with market volatility. This dynamic length makes the curve faster in trending moves and smoother during consolidations.

To help traders visualize volatility and directional momentum, adaptive volatility bands are plotted around the T3 line, with visual crossover markers and a dynamic info panel on the chart. It’s ideal for identifying trend shifts, spotting momentum surges, and adapting strategy execution to the pace of the market.

⯁ LOGIC

The T3 moving average length dynamically adjusts based on RSI values — when RSI is high, the smoothing period shortens to react faster; when RSI is low, the period increases for stability in slow markets.

A Parabolic SAR filter confirms directional bias, ensuring trades only occur in alignment with the broader market trend.

Long Entries: Trigger when the T3 curve crosses upward while the current price remains above the SAR — signaling bullish momentum alignment.

Short Entries: Trigger when the T3 crosses downward while the price remains below the SAR — confirming bearish trend alignment.

Stops: Dynamic stops are placed using the highest or lowest price over a set lookback period, adapting automatically to market volatility.

⯁ FEATURES

RSI-Adaptive T3 Filter: Adjusts smoothing in real time to market conditions, blending responsiveness with noise reduction.

SAR Confluence Check: Prevents counter-trend entries by confirming momentum direction via the Parabolic SAR.

Automatic Stop Placement: Uses recent highs or lows as stop-loss anchors, minimizing risk exposure.

Color-coded Visualization: The T3 line dynamically changes color based on slope direction, making momentum shifts visually intuitive.

Smoothed Trend Structure: Reduces market noise, allowing cleaner, more reliable trend recognition across different assets.

⯁ CONCLUSION

The RSI-Adaptive T3 and SAR Confluence Strategy delivers an advanced fusion of adaptive smoothing and structural confirmation. By combining RSI-driven reactivity with Parabolic SAR trend validation, this strategy offers a balanced approach to identifying sustainable momentum reversals while maintaining strong risk management through automatic stop levels. Ideal for traders who seek precision entries aligned with adaptive trend dynamics.

EMA Velocity Dual TF Momentum 1h (v2)BINANCE:SOLUSDT

The result is calculated on futures x10

### EMA Velocity Dual TF Momentum (v2) – Public Description

**Overview**

EMA Velocity Dual TF Momentum (v1) is a trend-following momentum strategy that uses the *speed of change* of Exponential Moving Averages (EMA) on two timeframes: the chart timeframe 1h.

The strategy looks for moments when both timeframes point in the same direction and the short‑term momentum is significantly stronger than usual, then manages trades with configurable ATR filtering, stop‑loss / take‑profit and early exit logic.

---

### Core Idea (high level, without formulas)

- On the **lower timeframe** (LTF), the strategy tracks how fast the EMA is moving (its “velocity”) and detects **impulse bars** where this velocity is unusually strong compared to its recent history.

- On the **higher timeframe** (HTF), it also measures EMA velocity and requires that the HTF trend direction is **aligned** with the LTF (both bullish or both bearish), if enabled.

- A **long trade** is opened when:

- LTF EMA velocity is positive (upward momentum),

- LTF momentum is strong enough (impulse),

- HTF EMA velocity is also upwards (if HTF filter is enabled),

- and ATR‑based volatility is above the minimum threshold.

- A **short trade** is opened in the symmetric situation (downward momentum on both timeframes).

- Positions are closed using configurable stop‑loss and take‑profit, and can be partially exited, moved to break‑even and trailed using early‑exit options.

---

### Inputs and Parameters

#### Trend & Momentum (Lower Timeframe)

- **`LTF EMA length (emaLenLTF)`**

Length of the EMA on the chart timeframe used to measure short‑term trend and momentum. Smaller values react faster; larger values are smoother and slower.

- **`LTF velocity lookback (velKLTF)`**

Lookback for computing EMA “velocity” on LTF. Controls how sensitive the momentum calculation is to recent price changes.

- **`LTF impulse lookback bars (impLookback)`**

Window size used to estimate the “normal” average absolute velocity. The strategy compares current momentum against this baseline to detect strong impulse moves.

- **`LTF |velocity| multiplier vs average (impMult)`**

Multiplier for defining what counts as a strong impulse. Higher values = fewer but stronger signals; lower values = more frequent, weaker impulses.

#### Trend & Momentum (Higher Timeframe)

- **`Use higher timeframe alignment (useHTF)`**

If enabled, trades are only taken when the higher‑timeframe EMA velocity confirms the same direction as the lower timeframe.

- **`HTF timeframe (htf_tf)`**

Higher timeframe used for confirmation (e.g. 60 minutes). Defines the “macro” context above the chart timeframe.

- **`HTF EMA length (emaLenHTF)`**

Length of the EMA on the higher timeframe. Controls how smooth and slow the higher‑timeframe trend filter is.

- **`HTF velocity lookback (velKHTF)`**

Lookback for the EMA velocity on HTF. Smaller values react quicker to changes in the higher‑timeframe trend.

#### Volatility / ATR Filter

- **`Use ATR filter (useAtrFilter)`**

Enables a volatility filter based on Average True Range. When active, trades are allowed only if market volatility is not too low.

- **`ATR Period (atrPeriod)`**

Lookback period for ATR calculation. Shorter periods react faster to recent volatility shifts; longer ones are more stable.

- **`ATR Min % for trading (atrMinPerc)`**

Minimum ATR as a percentage of price required to trade. Filters out very quiet, choppy periods where the strategy is more likely to be whipsawed.

#### Risk Management

- **`Use stops (SL/TP) (useStops)`**

Enables fixed stop‑loss and take‑profit exits. If disabled, positions are managed only by early exit logic and manual closing.

- **`Stop Loss % (stopLossPerc)`**

Distance of the protective stop from entry, in percent. Higher values give trades more room but increase risk per trade.

- **`Take Profit % (takeProfitPerc)`**

Distance of the primary profit target from entry, in percent. Controls the reward‑to‑risk profile of each trade.

#### Early Exit / Break‑Even / Trailing

- **`Enable early exit module (useEarlyExit)`**

Master switch for all early exit features: partial profit taking, break‑even stops and trailing exits.

- **`Take partial profit at +% (close 50%) (partialTP)`**

Profit level (in %) at which the strategy closes a partial portion of the position (e.g. 50%), locking in gains while leaving a runner.

- **`Trailing TP distance (%) (trailTP)`**

Distance (in %) for dynamic trailing stop after entry. When positive, the strategy trails the price to protect profits as the move extends.

- **`Break-even stop after +% profit (useBreakEven)`**

Enables automatic move of the stop to the entry price once a certain profit threshold is reached.

- **`Break-even activation (+%) (breakEvenPerc)`**

Profit level (in %) at which the stop is moved to break‑even. Higher values require a larger unrealized profit before break‑even protection kicks in.

#### Visuals

- **`Show labels (showLabels)`**

Toggles on‑chart labels that mark long and short entry signals for easier visual analysis.

- **`Label offset (labelOffset)`**

Horizontal offset (in bars) for placing labels relative to the signal bar. Used only for visual clarity; does not affect trading logic.

---

Если нужно, могу на основе этого текста сразу подготовить компактную версию (ограниченную по символам) специально под поле описания публичного скрипта в TradingView.

SMC Trend Filter Strategy (EMA50/EMA200 + FVG)Overview

This strategy implements a multi-timeframe Smart Money Concept (SMC) trading system designed for intraday and swing trading.

It combines a Daily trend filter, Break of Structure (BOS) detection, Order Block (OB) zones, Fair Value Gap (FVG) confirmation, and an ATR-based trailing stop system to achieve structured and rule-based entries.

The strategy is fully automated for backtesting and allows users to evaluate SMC concepts without repainting or discretionary interpretation.

- Core Components

1. Higher-Timeframe Trend Filter (Daily EMA50/EMA200)

The strategy retrieves D1 data and determines market direction using EMA50 and EMA200:

Uptrend → EMA50 > EMA200

Downtrend → EMA50 < EMA200

Trades are only taken in the direction of the Daily trend to avoid counter-trend setups.

2. Market Structure & Break of Structure (BOS)

The strategy identifies swing highs/lows and detects when price breaks beyond them:

Bullish BOS: price closes above previous swing high

Bearish BOS: price closes below previous swing low

This forms the foundation of SMC market structure recognition.

3. Order Block Zone (OB)

Upon detecting a BOS, the strategy marks the previous candle as a potential Order Block:

For bullish BOS → OB = previous candle’s high/low

For bearish BOS → OB = previous candle’s high/low

The OB zone is visualized using a semi-transparent box extended forward

Vital Wave 20-50Simplicity is almost always the most effective approach, and here I’m giving you a trend-following system that exploits the bullish bias of traditional markets and their trending nature, with very basic rules.

Rules (long entries only)

• Market entry: When the EMA 20 crosses above the EMA 50 (from below)

• Main market exit: When the EMA 20 crosses below the EMA 50 (from above)

• Fixed Stop Loss: Placed at the price level of the Lower Bollinger Band at the moment the trade is entered.

In my strategy, the primary exit is when the EMA 20 crosses below the EMA 50. However, this crossover can sometimes take a while to occur, and in the meantime the price may have already dropped significantly. The Stop Loss based on the Lower Bollinger Band is designed to limit losses in case the market moves sharply against the position without giving the bearish crossover signal in time. Having two exit conditions makes the strategy much more robust in terms of risk management.

Risk Management:

• Initial capital: $10,000

• Position size: 10% of available capital per trade

• Commissions: 0.1% on traded volume

• Stop Loss: Based on the Lower Bollinger Band

• Take Profit / Exit: When EMA 20 crosses below EMA 50

Recommended Markets:

XAUUSD (OANDA) (Daily)

Period: January 3, 1833 – November 23, 2025

Total Profit & Loss: +$6,030.62 USD (+57.57%)

Maximum Drawdown: $541.53 USD (3.83%)

Total Trades: 136

Winning Trades (Win Rate): 36.03% (49/136)

Profit Factor: 2.483

XAUUSD (OANDA) (12-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,209.56 USD (+11.89%)

Maximum Drawdown: $384.58 USD (3.61%)

Total Trades: 97

Winning Trades (Win Rate): 35.05% (34/97)

Profit Factor: 1.676

XAUUSD (OANDA) (8-hour)

Period: March 19, 2006 – November 23, 2025

Total Profit & Loss: +$1,179.36 USD (+11.81%)

Maximum Drawdown: $246.88 USD (2.32%)

Total Trades: 147

Winning Trades (Win Rate): 31.97% (47/147)

Profit Factor: 1.626

Tesla (NASDAQ) (4-hour)

Period: June 29, 2010 – November 23, 2025

Total Profit & Loss (Absolute): +$11,687.90 USD (+116.88%)

Maximum Drawdown: $922.05 USD (6.50%)

Total Trades: 68

Winning Trades (Win Rate): 39.71% (27/68)

Profit Factor: 4.156

Tesla (NASDAQ) (3-hour)

Total Profit & Loss: +$11,522.33 USD (+115.22%)

Maximum Drawdown: $1,247.60 USD (8.80%)

Total Trades: 114

Winning Trades: 33.33% (38/114)

Profit Factor: 2.811

Additional Recommendations

(These assets have shown good trending behavior with the same strategy across multiple timeframes):

• NVDA (15 min, 30 min, 1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• NFLX (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• MA (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• META (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• AAPL (1h, 2h, 3h, 4h, 6h, 8h, 12h, Daily)

• SPY (12h, Daily)

About the Code

The user can modify:

• EMA periods (20 and 50 by default)

• Bollinger Bands length (20 periods)

• Standard deviation (2.0)

Visualization

• EMA 20: Blue line

• EMA 50: Red line

• Green background when EMA20 > EMA50 (bullish trend)

• Red background when EMA20 < EMA50 (bearish trend)

Important Note:

We can significantly increase the profit factor and overall profitability by risking a fixed percentage per trade instead of a fixed amount. This would prevent losses from fluctuating with changes in volatility.

This could be implemented by reducing position size or adjusting leverage based on the volatility percentage required for each trade, but I’m not sure if this is fully possible in Pine Script. In my other script, “ Golden Cross 50/200 EMA ,” I go deeper into this topic and provide examples.

I hope you enjoy this contribution. Best regards!

STRATEGY 1 │ Red Dragon │ Model 1 │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

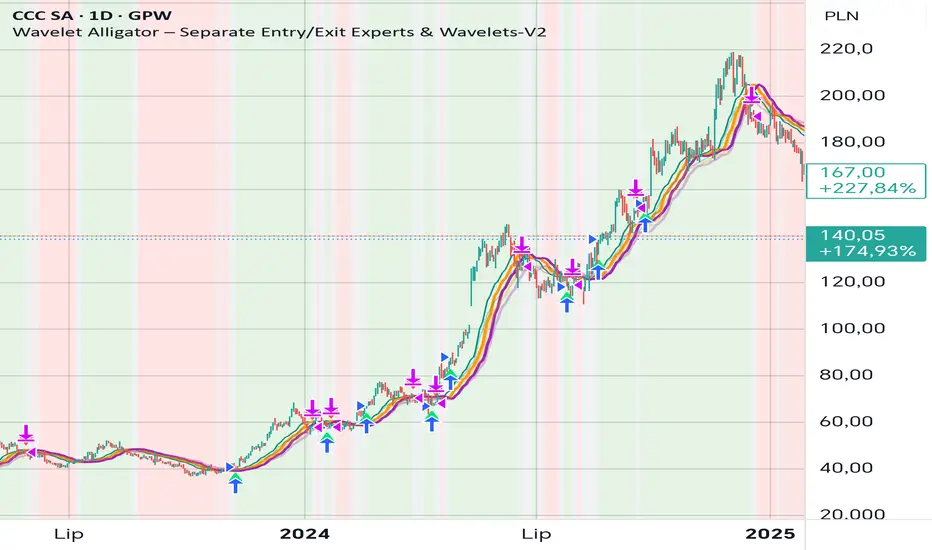

Wavelet Alligator – Separate Entry/Exit Experts & Wavelets-V2

Wavelet Alligator – Strategy Explanation & How to Use

1. Concept Overview

The Wavelet Alligator strategy combines:

- Wavelet transforms (Daubechies, Haar, Symlet, Mexican Hat, Morlet)

- Fractional calculus kernels: Caputo-Fabrizio (CF) and Atangana-Baleanu (AB)

- Three-layer “alligator-like” wavelet smoothing (soft → medium → strong)

- Expert-based entry/exit routing (RAW, CF, AB, or Majority vote)

- Independent wavelets for ENTRY and EXIT

- Main trend defined by AB wavelet ordering

This creates a multi-structure, multi-kernel trend engine capable of capturing extended moves with high signal quality.

2. Wavelet Alligator Structure

Each source (RAW, CF, AB) is transformed into three wavelet layers:

Soft = fastest reaction

Medium = mid smoothing

Strong = trend backbone

Wavelets:

- Daubechies: stable trend

- Haar: fast impulse detection

- Symlet: balanced

- Mexican Hat: curvature and reversal detection

- Morlet: cyclic, oscillatory

3. Entry Logic

Long entry occurs when:

- AB wavelet shows bullish structure (soft > medium > strong, medium rising)

- Selected entry expert approves (RAW / CF / AB / Majority)

- Wavelet condition: soft > strong AND medium crosses above strong

4. Exit Logic

Exit is independent from entry:

- Controlled by chosen exit expert

- Wavelet reversal condition: soft < strong AND medium crosses below strong

- Forced exit when AB trend turns neutral or bearish

5. Background Color (Regime)

- Green: bullish AB regime

- Red: bearish AB regime

- Gray: neutral/transition

6. How to Use

Step 1 – Choose entry wavelet

Daubechies: stable trend

Haar: breakout scalping

Mexican Hat: early reversals

Symlet: balanced

Morlet: cyclic markets

Step 2 – Choose exit wavelet

Mexican Hat: best precision

Daubechies: smooth exits

Haar: aggressive exits

Step 3 – Select entry/exit experts

CF only – fast fractional trend

AB only – stable long-memory trend

RAW only – pure price structure

Majority – safest, noise-filtered

Step 4 – Run the strategy

Entries occur only during AB bullish trend.

Exits occur on wavelet reversal or AB trend failure.

7. Why This Strategy Works

It fuses:

- Fractional calculus (memory)

- Wavelets (shape/curvature)

- Alligator ordering (trend hierarchy)

Result: high-quality entries, strong trend holding, noise-resistant signals.

Dami's HMA Strategy"Dami's HMA Strategy: Dynamic Crossover with Momentum Filter"

Key Points to Include:

Foundation: The strategy is based on the Hull Moving Average (HMA), noted for its speed and reduced lag, making it ideal for identifying trend inflection points early.

Enhanced Logic: Unlike a simple moving average crossover, this strategy incorporates a momentum filter. A signal is only triggered if the HMA crossover coincides with a candle moving in the direction of the new trend (bullish candle for Long, bearish candle for Short). This aims to confirm the impulse and avoid false entries during consolidation periods or 'weak' crossovers.

100% Market Coverage System: It is a continuous reversal system. Every new signal (Long or Short) closes the opposite position, ensuring the trader is always positioned in the direction indicated by the HMA.

Complementary Visualization: It includes the 8-Period High/Low Bands (Dami's Bands) to provide visual context of the recent price range, although they do not affect trading orders.

Adjustment and Optimization: The HMA length (hma_len=9 by default) is the key parameter to optimize based on the specific pair and timeframe. Higher values will generate fewer signals and be slower, while lower values (like the current 9) make it more sensitive.

15m ORB + FVG Strategy (ChadAnt)Core Logic

The indicator's logic revolves around three main phases:

1. Defining the 15-Minute Opening Range (ORB)

The script calculates the highest high (rangeHigh) and lowest low (rangeLow) that occurred during the first 15 minutes of the trading day.

This time window is defined by the sessionStr input, which defaults to 0930-0945 (exchange time).

The high and low of this range are plotted as small gray dots once the session ends (rangeSet = true).

2. Identifying a Fair Value Gap (FVG) Setup

After the 15-minute range is set, the indicator waits for a breakout of either the range high or range low.

A "Strict FVG breakout" requires two conditions on the first candle that closes beyond the range:

The candle before the breakout candle ( bars ago) must have been inside the range.

The breakout candle ( bar ago) must have closed outside the range.

A Fair Value Gap (FVG) must form on the most recent three candles (the current bar and the two previous bars).

Bullish FVG (Long Setup): The low of the current bar (low) is greater than the high of the bar two periods prior (high ). This FVG represents a price inefficiency that the trade expects to fill.

Bearish FVG (Short Setup): The high of the current bar (high) is less than the low of the bar two periods prior (low ).

If a valid FVG setup occurs, the indicator marks a pending setup and draws a colored box to highlight the FVG area (Green for Bullish FVG, Red for Bearish FVG).

3. Trade Entry and Management

If a pending setup is identified, the trade is structured as a re-entry trade into the FVG zone:

Entry Price: Set at the outer boundary of the FVG, which is the low of the current bar for a Long setup, or the high of the current bar for a Short setup.

Stop Loss (SL): Set at the opposite boundary of the FVG, which is the low for a Long setup, or the high for a Short setup.

The trade is triggered (tradeActive = true) once the price retraces to the pendingEntry level.

Risk/Reward (RR) Targets: Three Take Profit (TP) levels are calculated based on the distance between the Entry and Stop Loss:

$$\text{Risk} = | \text{Entry} - \text{SL} |$$

$$\text{TP}n = \text{Entry} \pm (\text{Risk} \times \text{RR}n)$$

where $n$ is 1, 2, or 3, corresponding to the input $\text{RR}1$, $\text{RR}2$, and $\text{RR}3$ values (defaults: 1.0, 1.5, and 2.0).

Trade Lines: Upon triggering, lines for the Entry, Stop Loss, and three Take Profit levels are drawn on the chart for a specified length (lineLength).

A crucial feature is the directional lock (highBroken / lowBroken):

If the price breaks a range level (e.g., simpleBrokeHigh) but without a valid FVG setup, the corresponding directional flag (e.g., highBroken) is set to true permanently for the day.

This prevents the indicator from looking for any subsequent trade setups in that direction for the rest of the day, suggesting that the initial move, without an FVG, exhausted the opportunity.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

ChadAnt

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied

CNN Fear and Greed StrategyAdaptation of the CNN Fear and Greed Index Indicator (Original by EdgeTools)

The following changes have been implemented:

Put/Call Ratio Data Source: The data source for the Put/Call Ratio has been updated.

Bond Data Source: The data sources for the bond components (Safe Haven Demand and Junk Bond Demand) have been updated.

Normalization Adjustment: The normalization method has been adjusted to allow the CNN Fear and Greed Index to display over a longer historical period, optimizing it for backtesting purposes.

Style Modification: The display style has been modified for a simpler and cleaner appearance.

Strategy Logic Addition: Added a new strategy entry condition: index >= 25 AND index crosses over its 5-period Simple Moving Average (SMA), and a corresponding exit condition of holding the position for 252 bars (days).

CNN Fear & Greed Backtest Strategy (Adapted)

This script is an adaptation of the popular CNN Fear & Greed Index, originally created by EdgeTools, with significant modifications to optimize it for long-term backtesting on the TradingView platform.

The core function of the Fear & Greed Index is to measure the current emotional state of the stock market, ranging from 0 (Extreme Fear) to 100 (Extreme Greed). It operates on the principle that excessive fear drives prices too low (a potential buying opportunity), and excessive greed drives them too high (a potential selling opportunity).

Key Components of the Index (7 Factors)

The composite index is calculated as a weighted average of seven market indicators, each normalized to a score between 0 and 100:

Market Momentum: S&P 500's current level vs. its 125-day Moving Average.

Stock Price Strength: Stocks hitting 52-week highs vs. those hitting 52-week lows.

Stock Price Breadth: Measured by the McClellan Volume Summation Index (or similar volume/breadth metric).

Put/Call Ratio: The relationship between volume of put options (bearish bets) and call options (bullish bets).

Market Volatility: The CBOE VIX Index relative to its 50-day Moving Average.

Safe Haven Demand: The relative performance of stocks (S&P 500) vs. bonds.

Junk Bond Demand: The spread between high-yield (junk) bonds and U.S. Treasury yields.

Critical Adaptations for Backtesting

To improve the index's utility for quantitative analysis, the following changes were made:

Long-Term Normalization: The original normalization method (ta.stdev over a short LENGTH) has been replaced or adjusted to use longer historical data. This change ensures the index generates consistent and comparable sentiment scores across decades of market history, which is crucial for reliable backtesting results.

Updated Data Sources: Specific ticker requests for the Put/Call Ratio and Bond components (Safe Haven and Junk Bond Demand) have been updated to use the most reliable and long-running data available on TradingView, reducing data gaps and improving chart continuity.

Simplified Visuals: The chart display is streamlined, focusing only on the final Fear & Greed Index line and key threshold levels (25, 50, 75) for quick visual assessment.

Integrated Trading Strategy

This script also includes a simple, rules-based strategy designed to test the counter-trend philosophy of the index:

Entry Logic (Long Position): A long position is initiated when the market shows increasing fear, specifically when the index score is less than or equal to the configurable FEAR_LEVEL (default 25) and the index crosses above its own short-term 5-period Simple Moving Average (SMA). This crossover acts as a confirmation that sentiment may be starting to turn around from peak fear.

Exit Logic (Time-Based): All positions are subject to a time-based exit after holding for 252 trading days (approximately one year). This fixed holding period aims to capture the typical duration of a cyclical market recovery following a major panic event.

Mirror Blocks: StrategyMirror Blocks is an educational structural-wave model built around a unique concept:

the interaction of mirrored weighted moving averages (“blocks”) that reflect shifts in market structure as price transitions between layered symmetry zones.

Rather than attempting to “predict” markets, the Mirror Blocks framework visualizes how price behaves when it expands away from, contracts toward, or flips across stacked WMA structures. These mirrored layers form a wave-like block system that highlights transitional zones in a clean, mechanical way.

This strategy version allows you to study how these structural transitions behave in different environments and on different timeframes.

The goal is understanding wave structure, not generating signals.

How It Works

Mirror Blocks builds three mirrored layers:

Top Block (Structural High Symmetry)

Base Block (Neutral Wave)

Bottom Block (Structural Low Symmetry)

The relative position of these blocks — and how price interacts with them — helps visualize:

Compression and expansion

Reversal zones

Wave stability

Momentum transitions

Structure flips

A structure is considered bullish-stack aligned when:

Top > Base > Bottom

and bearish-stack aligned when:

Bottom > Base > Top

These formations create the core of the Mirror Blocks wave engine.

What the Strategy Version Adds

This version includes:

Long Only, Short Only, or Long & Short modes

Adjustable symmetry distance (Mirror Distance)

Configurable WMA smoothing length

Optional trend filter using fast/slow MA comparison

ENTER / EXIT / LONG / SHORT labels for structural transitions

Fixed stop-loss controls for research

A clean, transparent structure with no hidden components

It is optimized for educational chart study, not automated signals.

Intended Purpose

Mirror Blocks is meant to help traders:

Study structural transitions

Understand symmetry-based wave models

Explore how price interacts with mirrored layers

Examine reversals and expansions from a mechanical perspective

Conduct long and short backtesting for research

Develop a deeper sense of market rhythm

This is not a prediction model.

It is a visual and structural framework for understanding movement.

Backtesting Disclaimer

Backtest results can vary depending on:

Slippage settings

Commission settings

Timeframe

Asset volatility

Structural sensitivity parameters

Past performance does not guarantee future results.

Use this as a research tool only.

Warnings & Compliance

This script is educational.

It is not financial advice.

It does not provide signals.

It does not promise profitability.

The purpose is to help visualize structure, not predict price.

The strategy features are simply here to help users study how structural transitions behave under various conditions.

License

Released under the Michael Culpepper Gratitude License (2025).

Use and modify freely for education and research with attribution.

No resale.

No promises of profitability.

Purpose is understanding, not signals.

Hash Momentum Strategy# Hash Momentum Strategy

## 📊 Overview

The **Hash Momentum Strategy** is a professional-grade momentum trading system designed to capture strong directional price movements with precision timing and intelligent risk management. Unlike traditional EMA crossover strategies, this system uses momentum acceleration as its primary signal, resulting in earlier entries and better risk-to-reward ratios.

---

## ⚡ What Makes This Strategy Unique

### 1. Momentum-Based Entry System

Most strategies rely on lagging indicators like moving average crossovers. This strategy captures momentum *acceleration* - entering when price movement is gaining strength, not after the move has already happened.

### 2. Programmable Risk-to-Reward

Set your exact R:R ratio (1:2, 1:2.5, 1:3, etc.) and the strategy automatically calculates stop loss and take profit levels. No more guessing or manual calculations.

### 3. Smart Partial Profit Taking

Lock in profits at multiple stages:

- **First TP**: Take 50% off at 2R

- **Second TP**: Take 40% off at 2.5R

- **Final TP**: Let 10% ride to maximum target

This approach locks in gains while letting winners run.

### 4. Dynamic Momentum Threshold

Uses ATR (Average True Range) multiplied by your threshold setting to adapt to market volatility. Volatile markets = higher threshold. Quiet markets = lower threshold.

### 5. Trade Cooldown System

Prevents overtrading and revenge trading by enforcing a cooldown period between trades. Configurable from 1-24 bars.