Weis pip zigzag jayyWhat you see here is the Weis pip zigzag wave plotted directly on the price chart. This script is the companion to the Weis pip wave ( ) which is plotted in the lower panel of the displayed chart and can be used as an alternate way of plotting the same results. The Weis pip zigzag wave shows how far in terms of price a Weis wave has traveled through the duration of a Weis wave. The Weis pip zigzag wave is used in combination with the Weis cumulative volume wave. The two waves must be set to the same "wave size".

To use this script you must set the wave size. Using the traditional Weis method simply enter the desired wave size in the box "Select Weis Wave Size" In this example, it is set to 5. Each wave for each security and each timeframe requires its own wave size. Although not the traditional method a more automatic way to set wave size would be to use ATR. This is not the true Weis method but it does give you similar waves and, importantly, without the hassle described above. Once the Weis wave size is set then the pip wave will be shown.

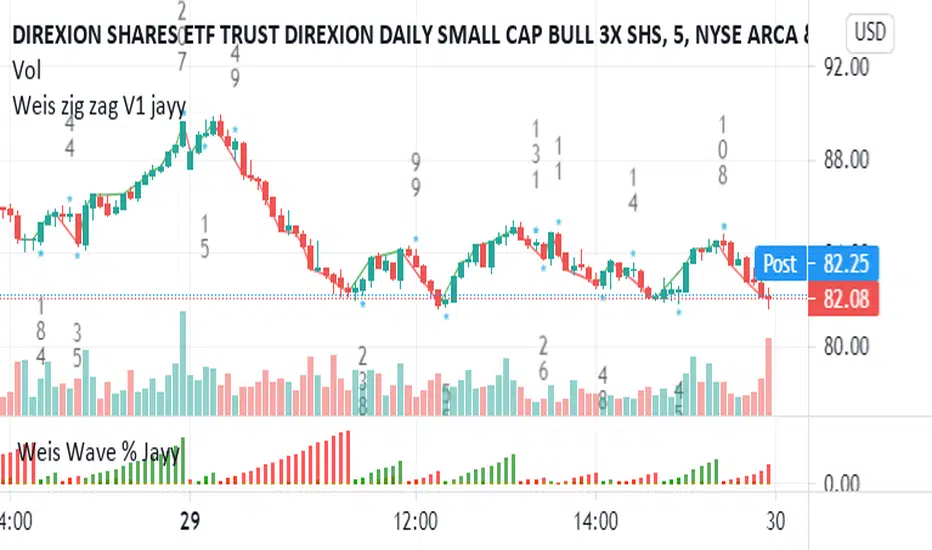

I have put a pip zigzag of a 5 point Weis wave on the bar chart - that is a different script. I have added it to allow your eye to see what a Weis wave looks like. You will notice that the wave is not in straight lines connecting wave tops to bottoms this is a function of the limitations of Pinescript version 1. This script would need to be in version 4 to allow straight lines. There are too many calculations within this script to allow conversion to Pinescript version 4 or even Version 3. I am in the process of rewriting this script to reduce the number of calculations and streamline the algorithm.

The numbers plotted on the chart are calculated to be relative numbers. The script is limited to showing only three numbers vertically. Only the highest three values of a number are shown. For example, if the highest recent pip value is 12,345 only the first 3 numerals would be displayed ie 123. But suppose there is a recent value of 691. It would not be helpful to display 691 if the other wave size is shown as 123. To give the appropriate relative value the script will show a value of 7 instead of 691. This informs you of the relative magnitude of the values. This is done automatically within the script. There is likely no need to manually override the automatically calculated value. I will create a video that demonstrates the manual override method.

What is a Weis wave? David Weis has been recognized as a Wyckoff method analyst he has written two books one of which, Trades About to Happen, describes the evolution of the now popular Weis wave. The method employed by Weis is to identify waves of price action and to compare the strength of the waves on characteristics of wave strength. Chief among the characteristics of strength is the cumulative volume of the wave. There are other markers that Weis uses as well for example how the actual price difference between the start of the Weis wave from start to finish. Weis also uses time, particularly when using a Renko chart. Weis specifically uses candle or bar closes to define all wave action ie a line chart.

David Weis did a futures io video which is a popular source of information about his method.

This is the identical script with the identical settings but without the offending links. If you want to see the pip Weis method in practice then search Weis pip wave. If you want to see Weis chart in pdf then message me and I will give a link or the Weis pdf. Why would you want to see the Weis chart for May 27, 2020? Merely to confirm the veracity of my algorithm. You could compare my Weis chart here () from the same period to the David Weis chart from May 27. Both waves are for the ES!1 4 hour chart and both for a wave size of 5.

In den Scripts nach "algo" suchen

Price Action and 3 EMAs Momentum plus Sessions FilterThis indicator plots on the chart the parameters and signals of the Price Action and 3 EMAs Momentum plus Sessions Filter Algorithmic Strategy. The strategy trades based on time-series (absolute) and relative momentum of price close, highs, lows and 3 EMAs.

I am still learning PS and therefore I have only been able to write the indicator up to the Signal generation. I plan to expand the indicator to Entry Signals as well as the full Strategy.

The strategy works best on EURUSD in the 15 minutes TF during London and New York sessions with 1 to 1 TP and SL of 30 pips with lots resulting in 3% risk of the account per trade. I have already written the full strategy in another language and platform and back tested it for ten years and it was profitable for 7 of the 10 years with average profit of 15% p.a which can be easily increased by increasing risk per trade. I have been trading it live in that platform for over two years and it is profitable.

Contributions from experienced PS coders in completing the Indicator as well as writing the Strategy and back testing it on Trading View will be appreciated.

STRATEGY AND INDICATOR PARAMETERS

Three periods of 12, 48 and 96 in the 15 min TF which are equivalent to 3, 12 and 24 hours i.e (15 min * period / 60 min) are the foundational inputs for all the parameters of the PA & 3 EMAs Momentum + SF Algo Strategy and its Indicator.

3 EMAs momentum parameters and conditions

• FastEMA = ema of 12 periods

• MedEMA = ema of 48 periods

• SlowEMA = ema of 96 periods

• All the EMAs analyse price close for up to 96 (15 min periods) equivalent to 24 hours

• There’s Upward EMA momentum if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA

• There’s Downward EMA momentum if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA

PA momentum parameters and conditions

• HH = Highest High of 48 periods from 1st closed bar before current bar

• LL = Lowest Low of 48 periods from 1st closed bar from current bar

• Previous HH = Highest High of 84 periods from 12th closed bar before current bar

• Previous LL = Lowest Low of 84 periods from 12th closed bar before current bar

• All the HH & LL and prevHH & prevLL are within the 96 periods from the 1st closed bar before current bar and therefore indicative of momentum during the past 24 hours

• There’s Upward PA momentum if price close > HH and HH > prevHH and LL > prevLL

• There’s Downward PA momentum if price close < LL and LL < prevLL and HH < prevHH

Signal conditions and Status (BuySignal, SellSignal or Neutral)

• The strategy generates Buy or Sell Signals if both 3 EMAs and PA momentum conditions are met for each direction and these occur during the London and New York sessions

• BuySignal if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA and price close > HH and HH > prevHH and LL > prevLL and timeinrange (LDN&NY) else Neutral

• SellSignal if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA and price close < LL and LL < prevLL and HH < prevHH and timeinrange (LDN&NY) else Neutral

Entry conditions and Status (EnterBuy, EnterSell or Neutral)(NOT CODED YET)

• ENTRY IS NOT AT THE SIGNAL BAR but at the current bar tick price retracement to FastEMA after the signal

• EnterBuy if current bar tick price <= FastEMA and current bar tick price > prevHH at the time of the Buy Signal

• EnterSell if current bar tick price >= FastEMA and current bar tick price > prevLL at the time of the Sell Signal

NAND PerceptronExperimental NAND Perceptron based upon Python template that aims to predict NAND Gate Outputs. A Perceptron is one of the foundational building blocks of nearly all advanced Neural Network layers and models for Algo trading and Machine Learning.

The goal behind this script was threefold:

To prove and demonstrate that an ACTUAL working neural net can be implemented in Pine, even if incomplete.

To pave the way for other traders and coders to iterate on this script and push the boundaries of Tradingview strategies and indicators.

To see if a self-contained neural network component for parameter optimization within Pinescript was hypothetically possible.

NOTE: This is a highly experimental proof of concept - this is NOT a ready-made template to include or integrate into existing strategies and indicators, yet (emphasis YET - neural networks have a lot of potential utility and potential when utilized and implemented properly).

Hardcoded NAND Gate outputs with Bias column (X0):

// NAND Gate + X0 Bias and Y-true

// X0 // X1 // X2 // Y

// 1 // 0 // 0 // 1

// 1 // 0 // 1 // 1

// 1 // 1 // 0 // 1

// 1 // 1 // 1 // 0

Column X0 is bias feature/input

Column X1 and X2 are the NAND Gate

Column Y is the y-true values for the NAND gate

yhat is the prediction at that timestep

F0,F1,F2,F3 are the Dot products of the Weights (W0,W1,W2) and the input features (X0,X1,X2)

Learning rate and activation function threshold are enabled by default as input parameters

Uncomment sections for more training iterations/epochs:

Loop optimizations would be amazing to have for a selectable length for training iterations/epochs but I'm not sure if it's possible in Pine with how this script is structured.

Error metrics and loss have not been implemented due to difficulty with script length and iterations vs epochs - I haven't been able to configure the input parameters to successfully predict the right values for all four y-true values for the NAND gate (only been able to get 3/4; If you're able to get all four predictions to be correct, let me know, please).

// //---- REFERENCE for final output

// A3 := 1, y0 true

// B3 := 1, y1 true

// C3 := 1, y2 true

// D3 := 0, y3 true

PLEASE READ: Source article/template and main code reference:

towardsdatascience.com

towardsdatascience.com

towardsdatascience.com

Baseline-C [ID: AC-P]The "AC-P" version of jiehonglim's NNFX Baseline script is my personal customized version of the NNFX Baseline concept as part of the NNFX Algorithm stack/structure for 1D Trend Trading for Forex. Everget's JMA implementation is used for the baseline smoothing method, with optional ATR bands at 1.0x and 1.5x from the baseline.

NNFX = No Nonsense Forex

Baseline = Component of the NNFX Algorithm that consists of a single moving average

Baseline ---> Meant to be used in conjunction with ATR/C1/C2/Vol Indicator/Exit Indicator as per NNFX Algorithm setup/structure. C1 is 1st Confirmation Indicator, C2 is 2nd Confirmation Indicator.

JMA (Jurik Moving Average) is used for the baseline and slow baseline.

A slow baseline option is included, but disabled by default.

The faint orange/purple lines are 1.0x/1.5x ATR from the Baseline, and are what I use as potential TP/SL targets or to evaluate when to stay out of a trade (chop/missed entry/exit/other/ATR breach), depending on the trade setup (in conjunction with C1/C2/Vol Indicator/Exit Indicator)

This script is heavily based upon jiehonglim's NNFX Baseline script for signaling, barcoloring, and ATR.

SSL Channel option included but disabled by default (Erwinbeckers SSL component)

POC (Point of Control) from Volume Profile is included/enabled by default for both the current timeframe and 12HR timeframe

03.freeman's InfoPanel Divergence Indicator was used a reference to replace the current/previous ATR information infopanel/info draw from jiehonglim's script. I'm not sure whether I like the previous way ATR info was displayed vs how I have it currently, but it's something that is completely optional:

Specifically: I am tuning this baseline/indicator for 1D trading as part of the NNFX system, for Forex.

DO NOT USE THIS INDICATOR WITHOUT PROPER TUNING/ADJUSTMENT for your timeframe and asset class.

Note about lack of alerts:

Alerts for baseline crosses (and other crosses) have been purposefully omitted for this version upon initial publication. While getting alerts for baseline crosses under certain conditions/filtered conditions that eliminate low-importance signals and crossover whipsaw would be great, it's something I'm still looking into.

SPECIFICALLY: There are entry, exit, take profit, and continuation signal components in relation to the Baseline to the rest of the NNFX Algorithm stack (ATR/C1/C2/Vol Indicator/Exit Indicator), including but limited to the "1 candle rule" and the "7 candle rule" as per NNFX.

Implementing alerts that are significant that also factor in these rules while reducing alert spam/false signals would be ideal, but it's also the HTF/Daily chart - visually, entry/exit/continuation signal alignment is easy to spot when trading 1D - alerts may be redundant/a pursuit in diminishing returns (for now).

//-------------------------------------------------------------------

// Acknowledgements/Reference:

// jiehonglim, NNFX Baseline Script - Moving Averages

//

// Fractured, Many Moving Averages

//

// everget, Jurik Moving Average/JMA

//

// 03.freeman, InfoPanel Divergence Indicator

//

// Ggqmna Volume stops

//

// Libertus RSI Divs

//

// ChrisMoody, CM_Price-Action-Bars-Price Patterns That Work

//

// Erwinbeckers SSL Channel

//

PineStats█ OVERVIEW

PineStats is a comprehensive statistical analysis library for Pine Script v6, providing 104 functions across 6 modules. Built for quantitative traders, researchers, and indicator developers who need professional-grade statistics without reinventing the wheel.

For building mean-reversion strategies, analyzing return distributions, measuring correlations, or testing for market regimes.

█ MODULES

CORE STATISTICS (20 functions)

• Central tendency: mean, median, WMA, EMA

• Dispersion: variance, stdev, MAD, range

• Standardization: z-score, robust z-score, normalize, percentile

• Distribution shape: skewness, kurtosis

PROBABILITY DISTRIBUTIONS (17 functions)

• Normal: PDF, CDF, inverse CDF (quantile function)

• Power-law: Hill estimator, MLE alpha, survival function

• Exponential: PDF, CDF, rate estimation

• Normality testing: Jarque-Bera test

ENTROPY (9 functions)

• Shannon entropy (information theory)

• Tsallis entropy (non-extensive, fat-tail sensitive)

• Permutation entropy (ordinal patterns)

• Approximate entropy (regularity measure)

• Entropy-based regime detection

PROBABILITY (21 functions)

• Win rates and expected value

• First passage time estimation

• TP/SL probability analysis

• Conditional probability and Bayes updates

• Streak and drawdown probabilities

REGRESSION (19 functions)

• Linear regression: slope, intercept, forecast

• Goodness of fit: R², adjusted R², standard error

• Statistical tests: t-statistic, p-value, significance

• Trend analysis: strength, angle, acceleration

• Quadratic regression

CORRELATION (18 functions)

• Pearson, Spearman, Kendall correlation

• Covariance, beta, alpha (Jensen's)

• Rolling correlation analysis

• Autocorrelation and cross-correlation

• Information ratio, tracking error

█ QUICK START

import HenriqueCentieiro/PineStats/1 as stats

// Z-score for mean reversion

z = stats.zscore(close, 20)

// Test if returns are normally distributed

returns = (close - close ) / close

isGaussian = stats.is_normal(returns, 100, 0.05)

// Regression channel

= stats.linreg_channel(close, 50, 2.0)

// Correlation with benchmark

spyReturns = request.security("SPY", timeframe.period, close/close - 1)

beta = stats.beta(returns, spyReturns, 60)

█ USE CASES

✓ Mean Reversion — z-scores, percentiles, Bollinger-style analysis

✓ Regime Detection — entropy measures, correlation regimes

✓ Risk Analysis — drawdown probability, VaR via quantiles

✓ Strategy Evaluation — expected value, win rates, R:R analysis

✓ Distribution Analysis — normality tests, fat-tail detection

✓ Multi-Asset — beta, alpha, correlation, relative strength

█ NOTES

• All functions return `na` on invalid inputs

• Designed for Pine Script v6

• Fully documented in the library header

• Part of the Pine ecosystem: PineStats, PineQuant, PineCriticality, PineWavelet

█ REFERENCES

• Abramowitz & Stegun — Normal CDF approximation

• Acklam's algorithm — Inverse normal CDF

• Hill estimator — Power-law tail estimation

• Tsallis statistics — Non-extensive entropy

Full documentation in the library header.

mean(src, length)

Calculates the arithmetic mean (simple moving average) over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Arithmetic mean of the last `length` values, or `na` if inputs invalid

wma_custom(src, length)

Calculates weighted moving average with linearly decreasing weights

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Weighted moving average, or `na` if inputs invalid

ema_custom(src, length)

Calculates exponential moving average

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Exponential moving average, or `na` if inputs invalid

median(src, length)

Calculates the median value over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Median value, or `na` if inputs invalid

variance(src, length)

Calculates population variance over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Population variance, or `na` if inputs invalid

stdev(src, length)

Calculates population standard deviation over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Population standard deviation, or `na` if inputs invalid

mad(src, length)

Calculates Median Absolute Deviation (MAD) - robust dispersion measure

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: MAD value, or `na` if inputs invalid

data_range(src, length)

Calculates the range (highest - lowest) over a lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Range value, or `na` if inputs invalid

zscore(src, length)

Calculates z-score (number of standard deviations from mean)

Parameters:

src (float) : Source series

length (simple int) : Lookback period for mean and stdev calculation (must be >= 2)

Returns: Z-score, or `na` if inputs invalid or stdev is zero

zscore_robust(src, length)

Calculates robust z-score using median and MAD (resistant to outliers)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Robust z-score, or `na` if inputs invalid or MAD is zero

normalize(src, length)

Normalizes value to range using min-max scaling

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Normalized value in , or `na` if inputs invalid or range is zero

percentile(src, length)

Calculates percentile rank of current value within lookback window

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Percentile rank (0 to 100), or `na` if inputs invalid

winsorize(src, length, lower_pct, upper_pct)

Winsorizes values by clamping to percentile bounds (reduces outlier impact)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

lower_pct (simple float) : Lower percentile bound (0-100, e.g., 5 for 5th percentile)

upper_pct (simple float) : Upper percentile bound (0-100, e.g., 95 for 95th percentile)

Returns: Winsorized value clamped to bounds

skewness(src, length)

Calculates sample skewness (measure of distribution asymmetry)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 3)

Returns: Skewness value (negative = left tail, positive = right tail), or `na` if invalid

kurtosis(src, length)

Calculates excess kurtosis (measure of distribution tail heaviness)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 4)

Returns: Excess kurtosis (>0 = heavy tails, <0 = light tails), or `na` if invalid

count_valid(src, length)

Counts non-na values in lookback window (useful for data quality checks)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Count of valid (non-na) values

sum(src, length)

Calculates sum over lookback period

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 1)

Returns: Sum of values, or `na` if inputs invalid

cumsum(src)

Calculates cumulative sum (running total from first bar)

Parameters:

src (float) : Source series

Returns: Cumulative sum

change(src, length)

Returns the change (difference) from n bars ago

Parameters:

src (float) : Source series

length (simple int) : Number of bars to look back (must be >= 1)

Returns: Current value minus value from `length` bars ago

roc(src, length)

Calculates Rate of Change (percentage change from n bars ago)

Parameters:

src (float) : Source series

length (simple int) : Number of bars to look back (must be >= 1)

Returns: Percentage change as decimal (0.05 = 5%), or `na` if invalid

normal_pdf_standard(x)

Calculates the standard normal probability density function (PDF)

Parameters:

x (float) : The value to evaluate

Returns: PDF value at x for standard normal N(0,1)

normal_pdf(x, mu, sigma)

Calculates the normal probability density function (PDF)

Parameters:

x (float) : The value to evaluate

mu (float) : Mean of the distribution (default: 0)

sigma (float) : Standard deviation (default: 1, must be > 0)

Returns: PDF value at x for normal N(mu, sigma²)

normal_cdf_standard(x)

Calculates the standard normal cumulative distribution function (CDF)

Parameters:

x (float) : The value to evaluate

Returns: Probability P(X <= x) for standard normal N(0,1)

@description Uses Abramowitz & Stegun approximation (formula 7.1.26), accurate to ~1.5e-7

normal_cdf(x, mu, sigma)

Calculates the normal cumulative distribution function (CDF)

Parameters:

x (float) : The value to evaluate

mu (float) : Mean of the distribution (default: 0)

sigma (float) : Standard deviation (default: 1, must be > 0)

Returns: Probability P(X <= x) for normal N(mu, sigma²)

normal_inv_standard(p)

Calculates the inverse standard normal CDF (quantile function)

Parameters:

p (float) : Probability value (must be in (0, 1))

Returns: x such that P(X <= x) = p for standard normal N(0,1)

@description Uses Acklam's algorithm, accurate to ~1.15e-9

normal_inv(p, mu, sigma)

Calculates the inverse normal CDF (quantile function)

Parameters:

p (float) : Probability value (must be in (0, 1))

mu (float) : Mean of the distribution

sigma (float) : Standard deviation (must be > 0)

Returns: x such that P(X <= x) = p for normal N(mu, sigma²)

power_law_alpha(src, length, tail_pct)

Estimates power-law exponent (alpha) using Hill estimator

Parameters:

src (float) : Source series (typically absolute returns or drawdowns)

length (simple int) : Lookback period (must be >= 10 for reliable estimates)

tail_pct (simple float) : Percentage of data to use for tail estimation (default: 0.1 = top 10%)

Returns: Estimated alpha (tail index), typically 2-4 for financial data

@description Alpha < 2 indicates infinite variance (very heavy tails)

@description Alpha < 3 indicates infinite kurtosis

@description Alpha > 4 suggests near-Gaussian behavior

power_law_alpha_mle(src, length, x_min)

Estimates power-law alpha using maximum likelihood (Clauset method)

Parameters:

src (float) : Source series (positive values expected)

length (simple int) : Lookback period (must be >= 20)

x_min (float) : Minimum threshold for power-law behavior

Returns: Estimated alpha using MLE

power_law_pdf(x, alpha, x_min)

Calculates power-law probability density (Pareto Type I)

Parameters:

x (float) : Value to evaluate (must be >= x_min)

alpha (float) : Power-law exponent (must be > 1)

x_min (float) : Minimum value / scale parameter (must be > 0)

Returns: PDF value

power_law_survival(x, alpha, x_min)

Calculates power-law survival function P(X > x)

Parameters:

x (float) : Value to evaluate (must be >= x_min)

alpha (float) : Power-law exponent (must be > 1)

x_min (float) : Minimum value / scale parameter (must be > 0)

Returns: Probability of exceeding x

power_law_ks(src, length, alpha, x_min)

Tests if data follows power-law using simplified Kolmogorov-Smirnov

Parameters:

src (float) : Source series

length (simple int) : Lookback period

alpha (float) : Estimated alpha from power_law_alpha()

x_min (float) : Threshold value

Returns: KS statistic (lower = better fit, typically < 0.1 for good fit)

is_power_law(src, length, tail_pct, ks_threshold)

Simple test if distribution appears to follow power-law

Parameters:

src (float) : Source series

length (simple int) : Lookback period

tail_pct (simple float) : Tail percentage for alpha estimation

ks_threshold (simple float) : Maximum KS statistic for acceptance (default: 0.1)

Returns: true if KS test suggests power-law fit

exp_pdf(x, lambda)

Calculates exponential probability density function

Parameters:

x (float) : Value to evaluate (must be >= 0)

lambda (float) : Rate parameter (must be > 0)

Returns: PDF value

exp_cdf(x, lambda)

Calculates exponential cumulative distribution function

Parameters:

x (float) : Value to evaluate (must be >= 0)

lambda (float) : Rate parameter (must be > 0)

Returns: Probability P(X <= x)

exp_lambda(src, length)

Estimates exponential rate parameter (lambda) using MLE

Parameters:

src (float) : Source series (positive values)

length (simple int) : Lookback period

Returns: Estimated lambda (1/mean)

jarque_bera(src, length)

Calculates Jarque-Bera test statistic for normality

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

Returns: JB statistic (higher = more deviation from normality)

@description Under normality, JB ~ chi-squared(2). JB > 6 suggests non-normality at 5% level

is_normal(src, length, significance)

Tests if distribution is approximately normal

Parameters:

src (float) : Source series

length (simple int) : Lookback period

significance (simple float) : Significance level (default: 0.05)

Returns: true if Jarque-Bera test does not reject normality

shannon_entropy(src, length, n_bins)

Calculates Shannon entropy from a probability distribution

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

n_bins (simple int) : Number of histogram bins for discretization (default: 10)

Returns: Shannon entropy in bits (log base 2)

@description Higher entropy = more randomness/uncertainty, lower = more predictability

shannon_entropy_norm(src, length, n_bins)

Calculates normalized Shannon entropy

Parameters:

src (float) : Source series

length (simple int) : Lookback period

n_bins (simple int) : Number of histogram bins

Returns: Normalized entropy where 0 = perfectly predictable, 1 = maximum randomness

tsallis_entropy(src, length, q, n_bins)

Calculates Tsallis entropy with q-parameter

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 10)

q (float) : Entropic index (q=1 recovers Shannon entropy)

n_bins (simple int) : Number of histogram bins

Returns: Tsallis entropy value

@description q < 1: emphasizes rare events (fat tails)

@description q = 1: equivalent to Shannon entropy

@description q > 1: emphasizes common events

optimal_q(src, length)

Estimates optimal q parameter from kurtosis

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Estimated q value that best captures the distribution's tail behavior

@description Uses relationship: q ≈ (5 + kurtosis) / (3 + kurtosis) for kurtosis > 0

tsallis_q_gaussian(x, q, beta)

Calculates Tsallis q-Gaussian probability density

Parameters:

x (float) : Value to evaluate

q (float) : Tsallis q parameter (must be < 3)

beta (float) : Width parameter (inverse temperature, must be > 0)

Returns: q-Gaussian PDF value

@description q=1 recovers standard Gaussian

permutation_entropy(src, length, order)

Calculates permutation entropy (ordinal pattern complexity)

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 20)

order (simple int) : Embedding dimension / pattern length (2-5, default: 3)

Returns: Normalized permutation entropy

@description Measures complexity of temporal ordering patterns

@description 0 = perfectly predictable sequence, 1 = random

approx_entropy(src, length, m, r)

Calculates Approximate Entropy (ApEn) - regularity measure

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 50)

m (simple int) : Embedding dimension (default: 2)

r (simple float) : Tolerance as fraction of stdev (default: 0.2)

Returns: Approximate entropy value (higher = more irregular/complex)

@description Lower ApEn indicates more self-similarity and predictability

entropy_regime(src, length, q, n_bins)

Detects market regime based on entropy level

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

q (float) : Tsallis q parameter (use optimal_q() or default 1.5)

n_bins (simple int) : Number of histogram bins

Returns: Regime indicator: -1 = trending (low entropy), 0 = transition, 1 = ranging (high entropy)

entropy_risk(src, length)

Calculates entropy-based risk indicator

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

Returns: Risk score where 1 = maximum divergence from Gaussian 1

hit_rate(src, length)

Calculates hit rate (probability of positive outcome) over lookback

Parameters:

src (float) : Source series (positive values count as hits)

length (simple int) : Lookback period

Returns: Hit rate as decimal

hit_rate_cond(condition, length)

Calculates hit rate for custom condition over lookback

Parameters:

condition (bool) : Boolean series (true = hit)

length (simple int) : Lookback period

Returns: Hit rate as decimal

expected_value(src, length)

Calculates expected value of a series

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Expected value (mean)

expected_value_trade(win_prob, take_profit, stop_loss)

Calculates expected value for a trade with TP and SL levels

Parameters:

win_prob (float) : Probability of hitting TP (0-1)

take_profit (float) : Take profit in price units or %

stop_loss (float) : Stop loss in price units or % (positive value)

Returns: Expected value per trade

@description EV = (win_prob * TP) - ((1 - win_prob) * SL)

breakeven_winrate(take_profit, stop_loss)

Calculates breakeven win rate for given TP/SL ratio

Parameters:

take_profit (float) : Take profit distance

stop_loss (float) : Stop loss distance

Returns: Required win rate for breakeven (EV = 0)

reward_risk_ratio(take_profit, stop_loss)

Calculates the reward-to-risk ratio

Parameters:

take_profit (float) : Take profit distance

stop_loss (float) : Stop loss distance

Returns: R:R ratio

fpt_probability(src, length, target, max_bars)

Estimates probability of price reaching target within N bars

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for volatility estimation

target (float) : Target move (in same units as src, e.g., % return)

max_bars (simple int) : Maximum bars to consider

Returns: Probability of reaching target within max_bars

@description Based on random walk with drift approximation

fpt_mean(src, length, target)

Estimates mean first passage time to target level

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for volatility estimation

target (float) : Target move

Returns: Expected number of bars to reach target (can be infinite)

fpt_historical(src, length, target)

Counts historical bars to reach target from each point

Parameters:

src (float) : Source series (typically price or returns)

length (simple int) : Lookback period

target (float) : Target move from each starting point

Returns: Array of first passage times (na if target not reached within lookback)

tp_probability(src, length, tp_distance, sl_distance)

Estimates probability of hitting TP before SL

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback for estimation

tp_distance (float) : Take profit distance (positive)

sl_distance (float) : Stop loss distance (positive)

Returns: Probability of TP being hit first

trade_probability(src, length, tp_pct, sl_pct)

Calculates complete trade probability and EV analysis

Parameters:

src (float) : Source series (typically returns)

length (simple int) : Lookback period

tp_pct (float) : Take profit percentage

sl_pct (float) : Stop loss percentage

Returns: Tuple:

cond_prob(condition_a, condition_b, length)

Calculates conditional probability P(B|A) from historical data

Parameters:

condition_a (bool) : Condition A (the given condition)

condition_b (bool) : Condition B (the outcome)

length (simple int) : Lookback period

Returns: P(B|A) = P(A and B) / P(A)

bayes_update(prior, likelihood, false_positive)

Updates probability using Bayes' theorem

Parameters:

prior (float) : Prior probability P(H)

likelihood (float) : P(E|H) - probability of evidence given hypothesis

false_positive (float) : P(E|~H) - probability of evidence given hypothesis is false

Returns: Posterior probability P(H|E)

streak_prob(win_rate, streak_length)

Calculates probability of N consecutive wins given win rate

Parameters:

win_rate (float) : Single-trade win probability

streak_length (simple int) : Number of consecutive wins

Returns: Probability of streak

losing_streak_prob(win_rate, streak_length)

Calculates probability of experiencing N consecutive losses

Parameters:

win_rate (float) : Single-trade win probability

streak_length (simple int) : Number of consecutive losses

Returns: Probability of losing streak

drawdown_prob(src, length, dd_threshold)

Estimates probability of drawdown exceeding threshold

Parameters:

src (float) : Source series (returns)

length (simple int) : Lookback period

dd_threshold (float) : Drawdown threshold (as positive decimal, e.g., 0.10 = 10%)

Returns: Historical probability of exceeding drawdown threshold

prob_to_odds(prob)

Calculates odds from probability

Parameters:

prob (float) : Probability (0-1)

Returns: Odds (prob / (1 - prob))

odds_to_prob(odds)

Calculates probability from odds

Parameters:

odds (float) : Odds ratio

Returns: Probability (0-1)

implied_prob(decimal_odds)

Calculates implied probability from decimal odds (betting)

Parameters:

decimal_odds (float) : Decimal odds (e.g., 2.5 means $2.50 return per $1 bet)

Returns: Implied probability

logit(prob)

Calculates log-odds (logit) from probability

Parameters:

prob (float) : Probability (must be in (0, 1))

Returns: Log-odds

inv_logit(log_odds)

Calculates probability from log-odds (inverse logit / sigmoid)

Parameters:

log_odds (float) : Log-odds value

Returns: Probability (0-1)

linreg_slope(src, length)

Calculates linear regression slope

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Slope coefficient (change per bar)

linreg_intercept(src, length)

Calculates linear regression intercept

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 2)

Returns: Intercept (predicted value at oldest bar in window)

linreg_value(src, length)

Calculates predicted value at current bar using linear regression

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Predicted value at current bar (end of regression line)

linreg_forecast(src, length, offset)

Forecasts value N bars ahead using linear regression

Parameters:

src (float) : Source series

length (simple int) : Lookback period for regression

offset (simple int) : Bars ahead to forecast (positive = future)

Returns: Forecasted value

linreg_channel(src, length, mult)

Calculates linear regression channel with bands

Parameters:

src (float) : Source series

length (simple int) : Lookback period

mult (simple float) : Standard deviation multiplier for bands

Returns: Tuple:

r_squared(src, length)

Calculates R-squared (coefficient of determination)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: R² value where 1 = perfect linear fit

adj_r_squared(src, length)

Calculates adjusted R-squared (accounts for sample size)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Adjusted R² value

std_error(src, length)

Calculates standard error of estimate (residual standard deviation)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Standard error

residual(src, length)

Calculates residual at current bar

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Residual (actual - predicted)

residuals(src, length)

Returns array of all residuals in lookback window

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Array of residuals

t_statistic(src, length)

Calculates t-statistic for slope coefficient

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: T-statistic (slope / standard error of slope)

slope_pvalue(src, length)

Approximates p-value for slope t-test (two-tailed)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Approximate p-value

is_significant(src, length, alpha)

Tests if regression slope is statistically significant

Parameters:

src (float) : Source series

length (simple int) : Lookback period

alpha (simple float) : Significance level (default: 0.05)

Returns: true if slope is significant at alpha level

trend_strength(src, length)

Calculates normalized trend strength based on R² and slope

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Trend strength where sign indicates direction

trend_angle(src, length)

Calculates trend angle in degrees

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Angle in degrees (positive = uptrend, negative = downtrend)

linreg_acceleration(src, length)

Calculates trend acceleration (second derivative)

Parameters:

src (float) : Source series

length (simple int) : Lookback period for each regression

Returns: Acceleration (change in slope)

linreg_deviation(src, length)

Calculates deviation from regression line in standard error units

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Deviation in standard error units (like z-score)

quadreg_coefficients(src, length)

Fits quadratic regression and returns coefficients

Parameters:

src (float) : Source series

length (simple int) : Lookback period (must be >= 4)

Returns: Tuple: for y = a*x² + b*x + c

quadreg_value(src, length)

Calculates quadratic regression value at current bar

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: Predicted value from quadratic fit

correlation(x, y, length)

Calculates Pearson correlation coefficient between two series

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Correlation coefficient

covariance(x, y, length)

Calculates sample covariance between two series

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 2)

Returns: Covariance value

beta(asset, benchmark, length)

Calculates beta coefficient (slope of regression of y on x)

Parameters:

asset (float) : Asset returns series

benchmark (float) : Benchmark returns series

length (simple int) : Lookback period

Returns: Beta coefficient

@description Beta = Cov(asset, benchmark) / Var(benchmark)

alpha(asset, benchmark, length, risk_free)

Calculates alpha (Jensen's alpha / intercept)

Parameters:

asset (float) : Asset returns series

benchmark (float) : Benchmark returns series

length (simple int) : Lookback period

risk_free (float) : Risk-free rate (default: 0)

Returns: Alpha value (excess return not explained by beta)

spearman(x, y, length)

Calculates Spearman rank correlation coefficient

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Spearman correlation

@description More robust to outliers than Pearson correlation

kendall_tau(x, y, length)

Calculates Kendall's tau rank correlation (simplified)

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period (must be >= 3)

Returns: Kendall's tau

correlation_change(x, y, length, change_period)

Calculates change in correlation over time

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period for correlation

change_period (simple int) : Period over which to measure change

Returns: Change in correlation

correlation_regime(x, y, length, ma_length)

Detects correlation regime based on level and stability

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period for correlation

ma_length (simple int) : Moving average length for smoothing

Returns: Regime: -1 = negative, 0 = uncorrelated, 1 = positive

correlation_stability(x, y, length, stability_length)

Calculates correlation stability (inverse of volatility)

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback for correlation

stability_length (simple int) : Lookback for stability calculation

Returns: Stability score where 1 = perfectly stable

relative_strength(asset, benchmark, length)

Calculates relative strength of asset vs benchmark

Parameters:

asset (float) : Asset price series

benchmark (float) : Benchmark price series

length (simple int) : Smoothing period

Returns: Relative strength ratio (normalized)

tracking_error(asset, benchmark, length)

Calculates tracking error (standard deviation of excess returns)

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

Returns: Tracking error (annualize by multiplying by sqrt(252) for daily data)

information_ratio(asset, benchmark, length)

Calculates information ratio (risk-adjusted excess return)

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

Returns: Information ratio

capture_ratio(asset, benchmark, length, up_capture)

Calculates up/down capture ratio

Parameters:

asset (float) : Asset returns

benchmark (float) : Benchmark returns

length (simple int) : Lookback period

up_capture (simple bool) : If true, calculate up capture; if false, down capture

Returns: Capture ratio

autocorrelation(src, length, lag)

Calculates autocorrelation at specified lag

Parameters:

src (float) : Source series

length (simple int) : Lookback period

lag (simple int) : Lag for autocorrelation (default: 1)

Returns: Autocorrelation at specified lag

partial_autocorr(src, length)

Calculates partial autocorrelation at lag 1

Parameters:

src (float) : Source series

length (simple int) : Lookback period

Returns: PACF at lag 1 (equals ACF at lag 1)

autocorr_test(src, length, max_lag)

Tests for significant autocorrelation (Ljung-Box inspired)

Parameters:

src (float) : Source series

length (simple int) : Lookback period

max_lag (simple int) : Maximum lag to test

Returns: Sum of squared autocorrelations (higher = more autocorrelation)

cross_correlation(x, y, length, lag)

Calculates cross-correlation at specified lag

Parameters:

x (float) : First series

y (float) : Second series (lagged)

length (simple int) : Lookback period

lag (simple int) : Lag to apply to y (positive = y leads x)

Returns: Cross-correlation at specified lag

cross_correlation_peak(x, y, length, max_lag)

Finds lag with maximum cross-correlation

Parameters:

x (float) : First series

y (float) : Second series

length (simple int) : Lookback period

max_lag (simple int) : Maximum lag to search (both directions)

Returns: Tuple:

SR Highlight - Pato WarzaDescriptionThis indicator is a high-precision tool designed to identify and visualize institutional Support and Resistance levels based on structural pivot points. Unlike standard SR indicators that clutter the chart with overlapping lines, this script uses a Smart Clustering Algorithm to merge nearby price levels into single, high-probability zones.Key FeaturesSmart Level Consolidation: Automatically detects and merges price levels that are too close to each other using volatility-based thresholds ( NYSE:ATR $), preventing "visual noise" and overlapping boxes.Strength-Based Hierarchy: Each level is calculated based on historical touches ($Strength$). The more times a price has reacted at a level, the higher its strength.The "King Level" Highlight (Strongest 🔥): The algorithm scans the entire lookback period to identify the single most respected level. This "King Level" is highlighted with a Golden/Yellow border and a fire emoji (🔥) for immediate focus on the day's key pivot.Dynamic Transparency & Layout: Designed specifically for fast-paced trading (15s, 1m, 5m), the zones extend to the left to show historical significance without obstructing the most recent price action.Fully Customizable: Adjust pivot sensitivity, loopback depth, and zone height to fit any asset (Gold, Nasdaq, Forex, or Crypto).How to UseLook for the 🔥: This represents the strongest historical level. Expect high volatility or significant reversals when price approaches this zone.Cluster Zones: Use the thickness of the boxes to gauge the "buffer zone" where price is likely to find liquidity.Trend Alignment: Use these zones in conjunction with your favorite trend indicators to find high-probability "Buy the Dip" or "Sell the Rip" opportunities.Technical Settings (Recommended)Pivot Period: 5 (Standard structural detection).Loopback Period: 300 - 900 (Depending on how much history you want to analyze).Minimum Strength: 3-5 (To filter out minor price noise).

SR Highlight - Pato Warza DescriptionThis indicator is a high-precision tool designed to identify and visualize institutional Support and Resistance levels based on structural pivot points. Unlike standard SR indicators that clutter the chart with overlapping lines, this script uses a Smart Clustering Algorithm to merge nearby price levels into single, high-probability zones.Key FeaturesSmart Level Consolidation: Automatically detects and merges price levels that are too close to each other using volatility-based thresholds ( NYSE:ATR $), preventing "visual noise" and overlapping boxes.Strength-Based Hierarchy: Each level is calculated based on historical touches ($Strength$). The more times a price has reacted at a level, the higher its strength.The "King Level" Highlight (Strongest 🔥): The algorithm scans the entire lookback period to identify the single most respected level. This "King Level" is highlighted with a Golden/Yellow border and a fire emoji (🔥) for immediate focus on the day's key pivot.Dynamic Transparency & Layout: Designed specifically for fast-paced trading (15s, 1m, 5m), the zones extend to the left to show historical significance without obstructing the most recent price action.Fully Customizable: Adjust pivot sensitivity, loopback depth, and zone height to fit any asset (Gold, Nasdaq, Forex, or Crypto).How to UseLook for the 🔥: This represents the strongest historical level. Expect high volatility or significant reversals when price approaches this zone.Cluster Zones: Use the thickness of the boxes to gauge the "buffer zone" where price is likely to find liquidity.Trend Alignment: Use these zones in conjunction with your favorite trend indicators to find high-probability "Buy the Dip" or "Sell the Rip" opportunities.Technical Settings (Recommended)Pivot Period: 5 (Standard structural detection).Loopback Period: 300 - 900 (Depending on how much history you want to analyze).Minimum Strength: 3-5 (To filter out minor price noise).

LibProfLibrary "LibProf"

Core Profiling Library.

This library provides a generic, object-oriented framework for

creating, managing, and analyzing 1D distributions (profiles) on

a customizable coordinate grid.

Unlike traditional Volume Profile libraries, `LibProf` is designed

as a **neutral Engine**. It abstracts away specific concepts

like "Price" or "Volume" in favor of mathematical primitives

("Level" and "Mass"). This allows developers to profile *any*

data series, such as Time-at-Price, Velocity, Delta, or Ticks.

Key Features:

1. **Object-Oriented Design (UDT):** Built around the `Prof`

object, encapsulating grid geometry, two generic data accumulators

(Array A & B), and cached statistical metrics. Supports full

lifecycle management: creation, cloning, clearing, and merging.

2. **Data-Agnostic Abstraction:**

- **Level (X-Axis):** Represents the coordinate system (e.g.,

Price, Time, Oscillator Value).

- **Mass (Y-Axis):** Represents the accumulated quantity

(e.g., Volume, Duration, Count).

- **Resolution (Grain):** The grid represents continuous data

discretized by a customizable resolution step size.

3. **Dual-Mode Geometry (Linear & Logarithmic):**

The engine supports seamless switching between two geometric modes:

- **Linear:** Arithmetic scaling (equal distance).

- **Logarithmic:** Geometric scaling (equal percentage), essential

for consistent density analysis across large ranges (Crypto).

Includes strict domain validation (enforcing positive bounds for log-space)

and physics-based constraints to prevent aliasing.

4. **High-Fidelity Resampling:**

Includes a sophisticated **Trapezoidal Integration Model** to

handle grid resizing and profile merging. When data is moved

between grids of different resolutions or geometries, the

library calculates the exact integral of the mass density

to ensure strict mass conservation.

5. **Dynamic Grid Management:**

- **Adapting:** Automatically expands the coordinate boundaries

to include new data points (`adapt`).

- **Resizing:** Allows changing the resolution (bins) or

boundaries on the fly, triggering the interpolation engine to

re-sample existing data accurately.

6. **Statistical Analysis (Lazy Evaluation):**

Comprehensive metrics calculated on-demand.

In Logarithmic mode, metrics adapt to use **Geometric Mean** and

**Geometric Interpolation** for maximum precision.

- **Location:** Peak (Mode), Weighted Mean (Center of Gravity), Median.

- **Dispersion:** Standard Deviation (Population), Coverage.

- **Shape:** Skewness and Excess Kurtosis.

7. **Structural Analysis:**

Includes a monotonic segmentation algorithm (configured by gapSize)

to decompose the distribution into its fundamental unimodal

segments, aiding in the detection of multi-modal distributions.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

create(bins, upper, lower, resolution, dynamic, isLog, coverage, gapSize)

Construct a new `Prof` object with fixed bin count & bounds.

Parameters:

bins (int) : series int number of level bins ≥ 1

upper (float) : series float upper level bound (absolute)

lower (float) : series float lower level bound (absolute)

resolution (float) : series float Smallest allowed bin size (resolution).

dynamic (bool) : series bool Flag for dynamic adaption of profile bounds

isLog (bool) : series bool Flag to enable Logarithmic bin scaling.

coverage (int) : series int Percentage of total mass to include in the Coverage Area (1..100)

gapSize (int) : series int Noise filter for segmentation. Number of allowed bins against trend.

Returns: Prof freshly initialised profile

method clone(self)

Create a deep copy of the profile.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object to copy

Returns: Prof A new, independent copy of the profile

method merge(self, massA, massB, upper, lower)

Merges mass data from a source profile into the current profile.

If resizing is needed, it performs a high-fidelity re-binning of existing

mass using a linear interpolation model inferred from neighboring bins,

preventing aliasing artifacts and ensuring accurate mass preservation.

Namespace types: Prof

Parameters:

self (Prof) : Prof The target profile object to merge into.

massA (array) : array float The source profile's mass A bin array.

massB (array) : array float The source profile's mass B bin array.

upper (float) : series float The upper level bound of the source profile.

lower (float) : series float The lower level bound of the source profile.

Returns: Prof `self` (chaining), now containing the merged data.

method clear(self)

Reset all bin tallies while keeping configuration intact.

Namespace types: Prof

Parameters:

self (Prof) : Prof profile object

Returns: Prof cleared profile (chaining)

method addMass(self, idx, mass, useMassA)

Adds mass to a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

idx (int) : series int Bin index

mass (float) : series float Mass to add (must be > 0)

useMassA (bool) : series bool If true, adds to Array A, otherwise Array B

method adapt(self, upper, lower)

Automatically adapts the profile's boundaries to include a given level interval.

If the level bound exceeds the current profile bounds, it triggers

the _resizeGrid method to resize the profile and re-bin existing mass.

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

upper (float) : series float The upper level to fit.

lower (float) : series float The lower level to fit.

Returns: Prof `self` (chaining).

method setBins(self, bins)

Sets the number of bins for the profile.

Behavior depends on the `isDynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-binning to a new resolution.

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

bins (int) : series int The new number of bins

Returns: Prof `self` (chaining)

method setBounds(self, upper, lower)

Sets the level bounds for the profile.

Behavior depends on the `dynamic` flag.

- If `dynamic = true`: Works on filled profiles by re-binning existing mass

- If `dynamic = false`: Only works on empty profiles to prevent accidental changes.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

upper (float) : series float The new upper level bound

lower (float) : series float The new lower level bound

Returns: Prof `self` (chaining)

method setResolution(self, resolution)

Sets the minimum resolution size (granularity limit) for the profile.

If the current bin count exceeds the limit imposed by the new

resolution, the profile is automatically resized (downsampled) to fit.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

resolution (float) : series float The new smallest allowed bin size.

Returns: Prof `self` (chaining)

method setLog(self, isLog)

Toggles the geometry of the profile between Linear and Logarithmic.

Behavior depends on the `dynamic` flag.

- If `dynamic = true`: Mass is re-distributed (merged) into the new geometric grid.

- If `dynamic = false`: Only works on empty profiles.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

isLog (bool) : series bool True for Logarithmic, False for Linear.

Returns: Prof `self` (chaining)

method setCoverage(self, coverage)

Set the percentage of mass for the Coverage Area. If the value

changes, the profile is finalized again.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

coverage (int) : series int The new Mass Coverage Percentage (0..100)

Returns: Prof `self` (chaining)

method setGapSize(self, gapSize)

Sets the gapSize (noise filter) for segmentation.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

gapSize (int) : series int Number of bins allowed to violate monotonicity

Returns: Prof `self` (chaining)

method getBins(self)

Returns the current number of bins in the profile.

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

Returns: series int The number of bins.

method getBounds(self)

Returns the current level bounds of the profile.

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

Returns:

upper series float The upper level bound of the profile.

lower series float The lower level bound of the profile.

method getBinWidth(self)

Get Width of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

Returns: series float The width of a bin

method getBinIdx(self, level)

Get Index of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

level (float) : series float absolute coordinate to locate

Returns: series int bin index 0…bins‑1 (clamped)

method getBinBnds(self, idx)

Get Bounds of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

idx (int) : series int Bin index

Returns:

up series float The upper level bound of the bin.

lo series float The lower level bound of the bin.

method getBinMid(self, idx)

Get Mid level of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

idx (int) : series int Bin index

Returns: series float Mid level

method getMassA(self)

Returns a copy of the internal raw data array A (Mass A).

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

Returns: array The internal array for mass A.

method getMassB(self)

Returns a copy of the internal raw data array B (Mass B).

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

Returns: array The internal array for mass B.

method getBinMassA(self, idx)

Get Mass A of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

idx (int) : series int Bin index

Returns: series float mass A

method getBinMassB(self, idx)

Get Mass B of a bin.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

idx (int) : series int Bin index

Returns: series float mass B

method getPeak(self)

Get Peak information.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

Returns:

peakIndex series int The index of the Peak bin.

peakLevel. series float The mid-level of the Peak bin.

method getCoverage(self)

Get Coverage information.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object

Returns:

covUpIndex series int The index of the upper bound bin of the Coverage Area.

covUpLevel series float The upper level bound of the Coverage Area.

covLoIndex series int The index of the lower bound bin of the Coverage Area.

covLoLevel series float The lower level bound of the Coverage Area.

method getMedian(self)

Get the profile's median level and its bin index. Calculates the value on-demand if stale.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object.

Returns:

medianIndex series int The index of the bin containing the Median.

medianLevel series float The Median level of the profile.

method getMean(self)

Get the profile's mean and its bin index. Calculates the value on-demand if stale.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object.

Returns:

meanIndex series int The index of the bin containing the mean.

meanLevel series float The mean of the profile.

method getStdDev(self)

Get the profile's standard deviation. Calculates the value on-demand if stale.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object.

Returns: series float The Standard deviation of the profile.

method getSkewness(self)

Get the profile's skewness. Calculates the value on-demand if stale.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object.

Returns: series float The Skewness of the profile.

method getKurtosis(self)

Get the profile's excess kurtosis. Calculates the value on-demand if stale.

Namespace types: Prof

Parameters:

self (Prof) : Prof Profile object.

Returns: series float The Kurtosis of the profile.

method getSegments(self)

Get the profile's fundamental unimodal segments. Calculates on-demand if stale.

Uses a pivot-based recursive algorithm configured by gapSize.

Namespace types: Prof

Parameters:

self (Prof) : Prof The profile object.

Returns: matrix A 2-column matrix where each row is an pair.

Prof

Prof Generic Profile object containing the grid and two data arrays.

Fields:

_bins (series int) : int Number of discrete containers (bins).

_upper (series float) : float Upper boundary of the domain.

_lower (series float) : float Lower boundary of the domain.

_resolution (series float) : float Smallest atomic grid unit (Resolution).

_isLog (series bool) : bool If true, the grid uses logarithmic scaling.

_logFactor (series float) : float Cached multiplier for log iteration (k = (up/lo)^(1/n)).

_logStep (series float) : float Cached natural logarithm of the factor (ln(k)) for optimized index calculation.

_dynamic (series bool) : bool Flag for dynamic resizing/resampling.

_coverage (series int) : int Target Mass Coverage Percentage (Input for Coverage).

_gapSize (series int) : int Tolerance against trend violations (Noise filter).

_maxBins (series int) : int Hard capacity limit for bins.

_massA (array) : array Generic Mass Array A.

_massB (array) : array Generic Mass Array B.

_peak (series int) : int Index of max mass (Mode).

_covUp (series int) : int Index of Coverage Upper Bound.

_covLo (series int) : int Index of Coverage Lower Bound.

_median (series float) : float Median level of distribution.

_mean (series float) : float Weighted Average Level (Center of Gravity).

_stdDev (series float) : float Population Standard Deviation.

_skewness (series float) : float Asymmetry measure.

_kurtosis (series float) : float Tail heaviness measure.

_segments (matrix) : matrix Identified unimodal segments.

StO Price Action - Daily Outside BarShort Summary

- Outside Bar indicator with multiple range calculation algorithms

- Highlights where the current range fully engulfs the previous

- Works with Daily candles in Daily, H4, and H1 timeframes only

- Highlights the current bar when it engulfs the previous bar according to the selected method

Full Description

Overview

- Identifies bars where the current period's range fully engulfs the prior period's range

- Offers three algorithms for defining the engulfing range:

- High/Low: uses absolute high and low values

- Open/Close: considers candle direction (bull/bear) and compares opens and closes

- Open/Close II: stricter version with exclusive inequalities for engulfing

- Engulfing behavior is detected automatically and highlighted for easy recognition

- Works on multiple markets but restricted to D, H4, and H1 charts for accuracy

Controls

- Year lookback (YLB) configurable to filter older bars

- Custom background color for highlighting Outside Bars

- Simple toggle interface with minimal chart clutter

Visual Representation

- Highlights engulfing bars with configurable background color

- Color transparency adjustable for clarity

Usage

- Use to identify strong market momentum or potential reversals

- Helps spot high-probability setups based on engulfing price action

Notes

- Only compatible with Daily, H4, and H1 timeframes

- Non-repainting: once an Outside Bar is drawn, it will not adjust retroactively

- Best used as a market structure reference not a direct trade signal

NVentures Liquidity Radar ProInstitutional Liquidity Radar Pro

OVERVIEW

This indicator combines three institutional trading concepts into a unified confluence scoring system: Liquidity Zones (swing-based), Order Blocks, and Fair Value Gaps. The unique value lies not in these individual concepts, but in HOW they interact through the confluence scoring algorithm to filter high-probability zones.

HOW THE CONFLUENCE SCORING WORKS

The core innovation is the calcConfluence() function that assigns a numerical score to each detected level:

1. Base Score: Every swing pivot starts with score = 1

2. Zone Overlap Detection: The algorithm iterates through all active zones within confDist * ATR proximity. Each overlapping zone adds +1 to the score

3. Order Block Proximity: If an Order Block's midpoint (top + bottom) / 2 falls within the confluence distance, +1 is added

4. HTF Validation: Using request.security(), the indicator fetches higher timeframe swing pivots. If the current zone aligns with an HTF swing within 2 * confDist * ATR_htf, a +2 bonus is awarded

Zones scoring 4+ are highlighted as high confluence - these represent areas where multiple institutional concepts converge.

HOW LIQUIDITY ZONES ARE CALCULATED

Detection: ta.pivothigh() and ta.pivotlow() with configurable lookback (default: 5 bars left/right)

Zone Width - Three modes available:

- ATR Dynamic: ATR(14) * multiplier (default 0.25)

- Fixed %: close * (percentage / 100)

- Wick Based: max(upperWick, lowerWick) * 1.5

Proximity Filter: isTooClose() prevents clustering by enforcing minimum ATR * minATRdist between zones

HOW ORDER BLOCKS ARE DETECTED

The detectBullishOB() / detectBearishOB() functions identify the last opposing candle before an impulse move:

1. Check if candle is opposing direction (bearish before bullish impulse, vice versa)

2. Validate consecutive candles in impulse direction (configurable, default: 3)

3. Volume confirmation: volume >= volMA * volMult (using 50-period SMA)

4. Minimum move validation: abs(close - close ) > ATR

This filters out weak OBs and focuses on those with institutional volume footprints.

HOW FAIR VALUE GAPS ARE DETECTED

FVGs represent price imbalances:

- Bullish FVG: low - high > ATR * fvgMinSize

- Bearish FVG: low - high > ATR * fvgMinSize

The ATR-relative sizing ensures gaps are significant relative to current volatility.

HOW SWEEP DETECTION WORKS

The checkSweep() function identifies false breakouts through wick analysis:

1. Calculate wick percentage: upperWick / totalRange or lowerWick / totalRange

2. Sweep conditions for resistance: high > zone.upper AND close < zone.price AND wickPct >= threshold

3. Sweep conditions for support: low < zone.lower AND close > zone.price AND wickPct >= threshold

A sweep indicates liquidity was grabbed without genuine continuation - often preceding reversals.

HOW FRESHNESS DECAY WORKS

The calcFreshness() function implements linear decay:

freshness = 1.0 - (age / decayBars)

freshness = max(freshness, minFresh)

This ensures old, tested zones fade visually while fresh zones remain prominent.

WHY THESE COMPONENTS WORK TOGETHER

The synergy is based on the principle that institutional activity leaves multiple footprints:

- Swing Pivots = where retail stops cluster

- Order Blocks = where institutions entered

- FVGs = where aggressive institutional orders created imbalances

- HTF Alignment = where higher timeframe participants are active

When these footprints converge at the same price level (high confluence score), the probability of significant price reaction increases.

CONFIGURATION

- Swing Detection Length: 5-8 for intraday, 8-15 for swing trading

- HTF Timeframe: One level above trading TF (e.g., D for H4)

- Min Confluence to Display: 2 for comprehensive view, 3-4 for high-probability only

- FVGs: Disabled by default for cleaner charts

STATISTICS PANEL

Displays: Active resistance/support zones, high confluence count, swept zones, active OBs, active FVGs, current ATR, selected HTF.

ALERTS

- Price approaching high confluence zone

- Liquidity sweep detected

- Bullish/Bearish Order Block formed

- Bullish/Bearish FVG detected

TECHNICAL NOTES

- Uses User-Defined Types (UDTs) for clean data structure management

- Respects Pine Script drawing limits (500 boxes/labels/lines)

- All calculations are ATR-normalized for cross-market compatibility

Institutional Volatility Expansion & Liquidity Thresholds (IVEL)Overview

The IVEL Engine is an institutional-grade volatility modeling tool designed to identify the mathematical boundaries of price delivery. Unlike retail oscillators that use fixed scales, this script utilizes dynamic ATR-based multiples to map Institutional Premium and Discount zones in real-time.

How to Use

To maximize the effectiveness of the IVEL Engine, traders should focus on Price Delivery at the extreme thresholds:

Identifying Institutional Premium (Short Setup) : When price expands into the Upper Red Zone, it has reached a mathematical exhaustion point. Seek short-side entries when price shows signs of rejection from this level back toward the Fair Value Baseline.

Identifying Institutional Discount (Long Setup) : When price reaches the Lower Green Zone, it is considered "cheap" by institutional algorithms. Look for long-side absorption or accumulation patterns within this zone.

Mean Reversion Targets: The Fair Value Baseline (Center Line) acts as the primary magnetic target. Successful trades taken at the outer thresholds should use the baseline as the first objective for profit-taking.

Alerts & Execution Strategy

The IVEL Engine is designed for automated monitoring so you don't have to watch the screen 24/7. To set up your execution workflow:

Set the Alert : Right-click the indicator and select "Add Alert." Set the condition to "Price Crossing Institutional Premium" (Upper Red) or "Price Crossing Institutional Discount" (Lower Green).

Wait for the Hit : Do not market-enter as soon as the alert fires. The alert tells you price has entered a High-Probability Liquidity Zone.

Confirm the Rejection : Once alerted, drop down to a lower timeframe (e.g., 5m or 15m) and look for a "Shift in Market Structure" or an SMT Divergence.

Execute : Enter once the rejection is confirmed, targeting the Fair Value Baseline as your primary TP1.

Methodology

The script anchors to an EMA-based baseline and projects expansion bands that adapt to current market conditions.

Value Area : The blue inner region where the majority of trading volume occurs.

Liquidity Exhaustion : The red and green outer regions where the probability of "Smart Money" reversal is highest.

Neeson bitcoin Dynamic ATR Trailing SystemNeeson bitcoin Dynamic ATR Trailing System: A Comprehensive Guide to Volatility-Adaptive Trend Following

Introduction

The Dynamic ATR Trailing System (DATR-TS) represents a sophisticated approach to trend following that transcends conventional moving average or breakout-based methodologies. Unlike standard trend-following systems that rely on price pattern recognition or fixed parameter oscillators, this system operates on the principle of volatility-adjusted position management—a nuanced approach that dynamically adapts to changing market conditions rather than imposing rigid rules on market behavior.

Originality and Innovation

Distinct Methodological Approach

What sets DATR-TS apart from hundreds of existing trend-following systems is its dual-layered conditional execution framework. While most trend-following systems fall into one of three broad categories—moving average crossovers, channel breakouts, or momentum oscillators—this system belongs to the more specialized category of volatility-normalized trailing stop systems.

Key Original Contributions:

Volatility-Threshold Signal Filtering: Most trend systems generate signals continuously, leading to overtrading during low-volatility periods. DATR-TS implements a proprietary volatility filter that requires minimum market movement before generating signals, effectively separating high-probatility trend opportunities from market noise.

Self-Contained Position State Management: Unlike traditional systems that require external position tracking, DATR-TS maintains an internal position state that prevents contradictory signals and creates a closed-loop decision framework.