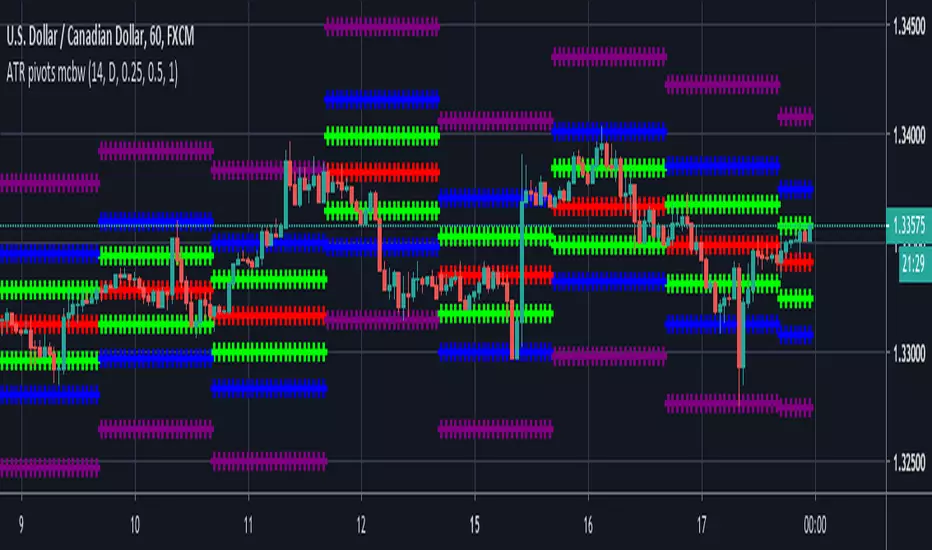

ATR based Pivots mcbwHey everyone this is an exciting new script I have prepared for you.

I was reading an old forex bulletin article some time ago when I came across this: solar.murty.net (or you can download the full bulletin with lots of other good articles here: www.forexfactory.com).

You can already buy this for metatrader (www.mql5.com) so I figured to make it for free for tradingview.

This bulletin suggested that you can reasonably predict daily volatility by adding or subtracting multiples of the daily ATR to the daily opening. Using this you can choose multiples to use as price targets and alternatively as stop losses. For example, if you already have a sense of market direction you can buy at market open place a stop loss at - 1 daily ATR and a profit target at + 3 ATRs for a risk to reward ratio of 3. If you are looking for smaller/quicker moves with a ratio of 3 you can have a stop loss at -0.25 ATR and a take profit at +0.75 ATR.

Alternatively this article also suggests to use this method to catch volatility breakouts. If price is higher than the + 1 ATR area then you can safely assume it will be going to the +2 ATR area so you can put a buy stop at + 1 ATR with a profit target at + 2 ATR with a stop loss at +0.5 ATR to catch a volatility breakout with a risk to reward ratio of 2!

Even further there are methods that you can use with ATRs of multiple window sizes, for example by opening two copies of this indicator and measuring recent volatility with a 1 week window and long term volatility within a 1 month window. If the short term volatility is crossing the long term volatility then there is a high probability chance that even more price movement will occur.

However I have found that this method is good for more than daily volatility , it can also be used to measure weekly volatility , and monthly volatility and use these multiples as good long term price targets.

To select if you want daily, weekly, or monthly values of the ATR of volatility you're using go to the settings and click on the options in the "Opening period". The default window of the ATR here is 14 periods, but you can change this if you want to in "ATR period". Most importantly you are able to select which multiples of the ATR you would like to use in the settings in "ATR multiple 1" which is the green line, "ATR multiple 2" which is the blue line, and "ATR multiple 3" which is the purple line. You can select any values you want to put in these, the choice of 0.25, 0.5, and 1 is not special, some people use fibonacci numbers here or simply 0.33, 0.66, and 0.99.

Repainting issue: This script uses the daily value of the Average True Range (ATR), which measures the volatility that is happening today. If price becomes more volatile then the value of the ATR can increase throughout the day, but it can never decrease. What this means is that the ATR based pivots are able to expand away from the opening price, which should not affect the trades that you take based on these areas. If you base your take profit on one of these ATR multiples and the daily volatility increase this means that your take profit area will be closer to your entry than the ATR multiple. Meaning that your trades will be more conservative.

While this all may sound very technical it is super intuitive, throw this on your chart and play around with it :)

Happy trading!

In den Scripts nach "META股价历史数据" suchen

Pentuple Exponential Moving Average (PEMA)This type of moving average was originally developed by Bruno Pio in 2010. I just ported the original code from MetaTrader 5. The method uses a linear combination of EMA cascades to achieve better smoothness. Well, actually you can create your own X-uple EMA, but be sure that the combination' coefficients are valid.

Quadruple Exponential Moving Average (QEMA)This type of moving average was originally developed by Bruno Pio in 2010. I just ported the original code from MetaTrader 5.

Anchor ZonesL.A. Little, who wrote two books on trend trading, explained a key timing concept called anchor zones which was used, within his trading system, to enter and exit the market at appropriate times.

Anchor zones are formed from anchor bars. An anchor bar is a bar that has one or more of these components: wide range, high volume or gaps. For this script we're going to require two or more of the components. When an anchor bar forms, we'll note the high and low of the bar and draw a zone across time as prices develops. For this script, we'll also note the open and close of the candle to hint at other levels of support or resistance. The boundaries of these zones can act as support or resistance, but they also mark out the areas where price can often get trapped.

A breakout from these zones on high volume can suggest the beginning of a new trend. In general, anchor zones are a good compliment to price action strategies. For more information on how to use these, refer to L.A. Little's books.

References

onlinelibrary.wiley.com

www.tradingsetupsreview.com

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Pocket PivotsPocket Pivots are described in the book "Trade like an O'Neil Discipline" by Dr. Chris Kacher and Gil Morales. There’s no exact definition of Pocket Pivots, but there is an exact definition for the volume signature: The volume should be higher than the largest down volume of the last 10 trading days.

This is a modification of Pocket Pivots. We use the level where the Pocket Pivot occurred and draw a zone across the chart until the criteria for another Pocket Pivot is met again. This way we can use them as support/resistance zones. Instead of the volume being higher than the volume for each of the previous periods, we just use an SMA of the volume and make sure the volume on the final candle is higher than the average for the previous periods. Last but not least, we have the possibility to draw support/resistance levels off the back of different counts. Seven-count for hyper-aggressive pocket pivots, eight-count for aggressive, nine for measured and ten for passive.

Hyper-aggressive Pocket Pivots

Aggressive Pocket Pivots

Measured Pocket Pivots

Passive Pocket Pivots

All

Using "All" to see all the pivots can be messy, but the confluence of support/resistance is more than helpful for defining truly important levels.

People have created a methodology/rules for buying and selling with Pivot Points, but as I understand there's no general consensus on their application, so please do some research before you decide to use them in your trading.

References

www.chartmill.com

www.mypivots.com

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Yang & Zheng Extension of Garman & KlassFirst off, a huge thank you to the following people:

theheirophant: www.tradingview.com

alexgrover: www.tradingview.com

NGBaltic: www.tradingview.com

This is the Yang & Zhang extension of Garman & Klass. The equation was modified to include the logarithm of the open price divided by the preceding close price. As a result, this function uses the open, high, low and close prices to estimate volatility. This modification allows the volatility estimator to account for the opening jumps, but as the original function, it assumes that the underlying follows a Brownian motion with zero drift (the historical mean return should be equal to zero). This estimator tends to overestimate the volatility when the drift is different from zero, however, for a zero drift motion, this estimator has an efficiency of eight times the classic close-to-close estimator (standard deviation).

This script allows you to transform the volatility reading. The intention of this is to be able to compare volatility across different assets and timeframes. Having a relative reading of volatility also allows you to better gauge volatility within the context of current market conditions.

For the signal lie I chose a repulsion moving average to remove choppy crossovers of the estimator and the signal. This may have been a mistake, so in the near-future I might update so that the MA can be selected. Let me know if you have any opinions either way.

References

www.rdocumentation.org

www.quantshare.com

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Parkinson Historical VolatilityFirst off, a huge thank you to the following people:

theheirophant: www.tradingview.com

alexgrover: www.tradingview.com

NGBaltic: www.tradingview.com

The Parkinson Historical Volatility (PHV), developed in 1980 by the physicist Michael Parkinson, aims to estimate the volatility of returns for a random walk using the high and low in any particular period. An important use of the PHV is the assessment of the distribution prices during the day as well as a better understanding of the market dynamics. Comparing the PHV and a periodically sampled volatility helps traders understand the tendency towards mean reversion in the market as well as the distribution of stop-losses.

This script allows you to transform the volatility reading. The intention of this is to be able to compare volatility across different assets and timeframes. Having a relative reading of volatility also allows you to better gauge volatility within the context of current market conditions.

For the signal lie I chose a repulsion moving average to remove choppy crossovers of the estimator and the signal. This may have been a mistake, so in the near-future I might update so that the MA can be selected. Let me know if you have any opinions either way.

References

www.rdocumentation.org

www.ivolatility.com

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Rogers & Satchell Volatility EstimationFirst off, a huge thank you to the following people:

theheirophant: www.tradingview.com

alexgrover: www.tradingview.com

NGBaltic: www.tradingview.com

The Rogers & Satchell function is a volatility estimator that outperforms other estimators when the underlying follows a geometric Brownian motion with a drift (historical data mean returns different from zero). As a result, it provides a better volatility estimation when the underlying is trending. However, the Rogers & Satchell estimator does not account for jumps in price (gaps). It assumes no opening jump. The function uses the open, close, high, and low price series in its calculation and it has only one parameter, which is the period to use to estimate the volatility.

This script allows you to transform the volatility reading. The intention of this is to be able to compare volatility across different assets and timeframes. Having a relative reading of volatility also allows you to better gauge volatility within the context of current market conditions.

For the signal lie I chose a repulsion moving average to remove choppy crossovers of the estimator and the signal. This may have been a mistake, so in the near-future I might update so that the MA can be selected. Let me know if you have any opinions either way.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Godmode 4.0.2 [Supply/Demand]First off, a huge thank you to the following people:

LEGION:

LazyBear: www.tradingview.com

xSilas: www.tradingview.com

Ni6HTH4awK: www.tradingview.com

sco77m4r7and:

SNOW_CITY: www.tradingview.com

oh92: www.tradingview.com

alexgrover: www.tradingview.com

cI8DH: www.tradingview.com

DonovanWall: www.tradingview.com

shtcoinr: www.tradingview.com

This is the third iteration of Godmode. This time I borrowed the method used by shtcoinr to render supply/demand, resistance and support zones. The idea here is to input the appropriate benchmark tickerid to the asset class you're trading and to paint zones according to the price activity of the selected tickerid. This works very well trying to paint meaningful zones against noisy stocks, currencies, commodities etc. Use a correlation coefficient to determine the best benchmark for your asset class.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Function for Least Squares Moving AverageThank you to alexgrover for putting me wide to this, after putting up with long conversations and stupid questions. Follow him and behold: www.tradingview.com

What is this?

This is simply the function for a Least Squares Moving Average. You can render this on the chart by using the linreg() function in Pine.

Personally I like to use the slope of the LSMA to help determine what direction to take a trade in, but I'm sure there are other, more exotic ways of using it and, if you know how to get your fingers dirty with Pine, you can create more exotic versions of it by modifying the function provided.

Want to learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Godmode 4.0.1 [Correlator]First off, a huge thank you to the following people:

@LEGION:

@LazyBear: www.tradingview.com

@xSilas: www.tradingview.com

@Ni6HTH4awK: www.tradingview.com

@sco77m4r7and:

@SNOW_CITY: www.tradingview.com

@oh92: www.tradingview.com

@alexgrover: www.tradingview.com

@cI8DH: www.tradingview.com

@DonovanWall: www.tradingview.com

This is my second iteration of Godmode. This time I allowed the possibility to correlate two benchmarks against one another, thereby giving you twice the signals (once there's a strong correlation between the two, inverse or otherwise). That aside, there are no changes to this indicator that the first iteration doesn't have:

There are still more iterations planned, but if you guys have any ideas or wishes regarding what direction I go, then please let me know.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources as well as any other scripts I publish.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

Godmode 4.0.0 [Oscillator]First off, a huge thank you to the following people:

LEGION:

LazyBear: www.tradingview.com

xSilas: www.tradingview.com

Ni6HTH4awK: www.tradingview.com

sco77m4r7and:

SNOW_CITY: www.tradingview.com

oh92: www.tradingview.com

alexgrover: www.tradingview.com

cI8DH: www.tradingview.com

DonovanWall: www.tradingview.com

Since I've been on TradingView I've become somewhat enthralled by Godmode and the collective work that goes in to it, so I decided to publish my own iteration, building off the ideas already present. (This is a great way to get familiar with Pine by the way, just in case there are any beginners reading this)

Changes

The first change I made was to allow the user to select whatever tickerid they wanted as a benchmark. If trading XBTUSD on BitMEX for example, the indicator will react to exchange-specific activity, which means it will respond to all the little whipsaws, whipsaws that can be especially present on a futures exchange. By typing CRYPTOCAP:BTC or CRYPTOCAP:TOTAL we endeavor to remove noise. It can also signal earlier. Less noise and less lag. Another idea would be to choose a benchmark that has a strong inverse relationship with the asset you're trading: try CRYPTOCAP:USDT as the benchmark against BTC to see what I mean.

I also added the ability to smooth the plot, yet again removing noise but adding considerable lag.

The linear regression of the wave-trend is calculated in place of the EMA. This is plotted as columns with the midline (50) as the base. This is just calculating the slope of the wave-trend and can signal a weakening trend before a reversal takes place.

Using cI8DH's True RSI script () as inspiration, I added a function for calculating the True TSI in an attempt to remove any bullish bias. Funnily enough, when I tried to do the same with the RSI I had some problems. I'll try to resolve this in the coming weeks.

Made slight changes to the aesthetics. Tried to bring the two main plots alive by making their bold, opaque colors stand off the subtle tones in the background.

To Do List

1. I would like to sort out the issue with the True RSI.

2. When the plots are smoothed, there's an issue with the green 'Caution!' dots appearing in the lower half of the indicator.

3. I'd like to adjust the code so that if the 'Benchmark' box is empty, that it will automatically register the current tickerid as the 'Benchmark'.

If anyone has any suggestions on other fixes or how to apply the fixes mentioned by me, please don't hesitate to reach out to me here or through other media platforms.

Want to Learn?

If you'd like the opportunity to learn Pine but you have difficulty finding resources to guide you, take a look at this rudimentary list: docs.google.com

The list will be updated in the future as more people share the resources that have helped, or continue to help, them. Follow me on Twitter to keep up-to-date with the growing list of resources.

Suggestions or Questions?

Don't even kinda hesitate to forward them to me. My (metaphorical) door is always open.

BITMEX:XBTUSD

CRYPTOCAP:BTC

CRYPTOCAP:TOTAL

CRYPTOCAP:USDT.D

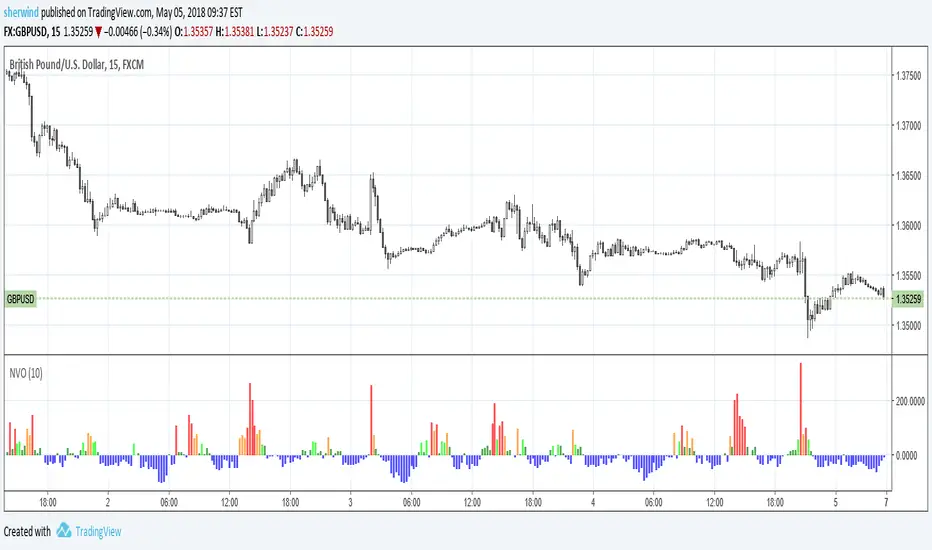

Normalized Volume OscillatorThis volume indicator works best on comparatively small timeframes (15 minutes, for example).

Based on:

- Normalized Volume Oscillator - indicator for MetaTrader 4

- Using Tick Volume in Forex: A Clear NVO Based Example

See also:

- Are price updates a good proxy for actual traded volume in FX?

BO Swing Finder R0.6 by JustUncleLThis indicator alert study attempts to detect confirmed Swing points. It uses Bollinger Band centre line crosses as the main signal. The main detection occurs by looking for the first BB centre line cross that was initiated from outside the Bollinger Channel (alternatively KC channel can be used).

The optional HullMA (any any other MA pair) are used to confirm the swing direction. The indicator also plots the two KitKat Support and Resistance lines with optional High/Low labelling on KitKat1 lines.

This indicator tool is suitable for any time frame and can be traded with Binary Option (even 1min) orders (2-3 candle expiry) or as Forex trade orders. It is suitable for Currencies, Cryptocurrencies and Metals. May also be useful on other markets as well.

The MA filtering options, each MA line can be a different type, with an optional offset:

SMA = Simple Moving Average.

EMA = Exponential Moving Average.

WMA = Weighted Moving Average

VWMA = Volume Weighted Moving Average

SMMA = Smoothed Simple Moving Average.

DEMA = Double Exponential Moving Average

TEMA = Triple Exponential Moving Average.

HullMA = Hull Moving Average, fast moving MA.

SSMA = Ehlers Super Smoother Moving average, similar results to HullMA.

ZEMA = Near Zero Lag Exponential Moving Average.

TMA = Triangular (smoothed) Simple Moving Average.

NOTE: The signal calculations do occur on the current candle, so the state of the signal may re-build until the current candle is closed. I have designed the script to behave this way on purpose. This gives traders the option of

preparing their trade early or even taking the trade early if they want. Otherwise the trader can be more conservative and wait for signal candle to close, to give them a confirmed signal. (This is NOT re-painting as the historical signal states are fixed and will not change, unless you change some setup options.)

Hints:

1) As with all indicator and alerting tools, not all signals will yield a tradable successful swing. You need to apply you own analysis on each signal to determine the probability of success.

2) When using the MA to filter the signals you should use it for two types of filtering:

Supportive that confirm swing like fast moving MAs with fairly short lengths, eg HullMA(21,25).

Long Term Direction with smoother longer length MAs like SMMA(180,220) to show up swings back into direction of the longer term trends.

Inspiration: @Lyiness

References:

Momentum VMA KITKAT CROSS v2.1 by vdubus (- Vdubus_Channel www.vdubus.co.uk)

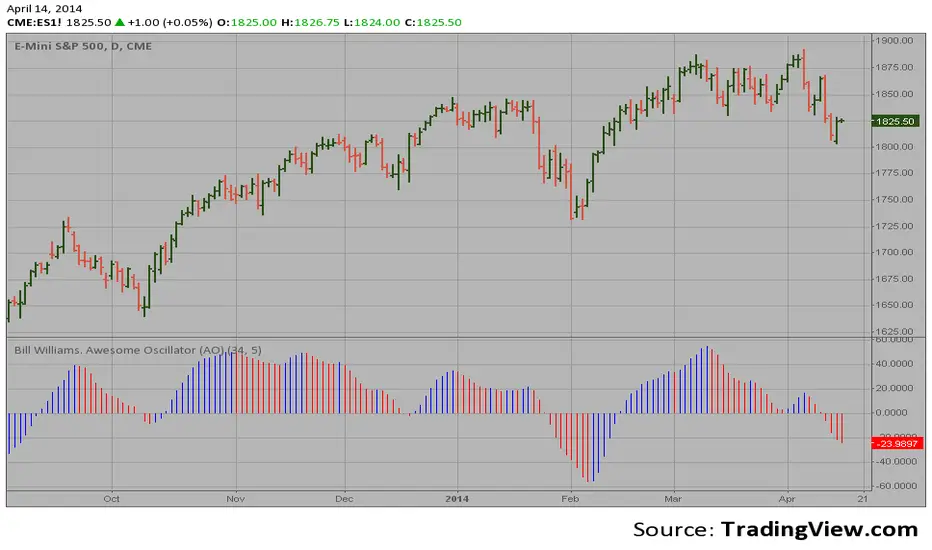

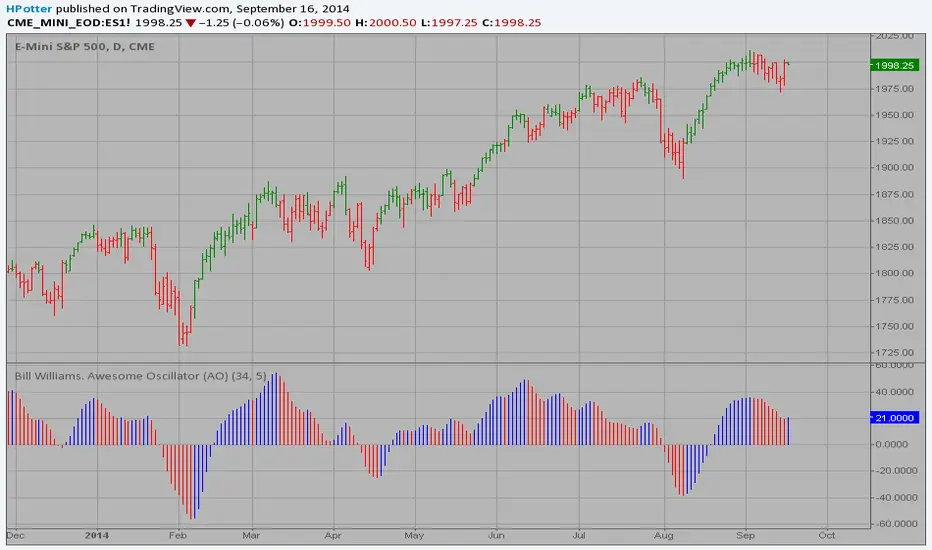

Bill Williams. Awesome Oscillator (AO) Backtest This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Basic MAAll-in-one basic indicators:

- MA Fast (12)

- MA Medium (26)

- MA Slow (200)

- Parabolic SAR www.investopedia.com

- Dynamic Fibonnaci channel with 2 channels - www.forexstrategiesresources.com

Vegas TunnelThis indicator adds and subtracts fib levels from the moving average. I suppose profits are meant to be taken at certain levels. Additionally, it may help in finding tops and bottoms. There's more info here: www.forexstrategiesresources.com

The fib levels should be changed depending on time frame:

short) 5, 8, 13, 21

intermediate) 34, 55, 89, 144

long) 55, 89, 144, 233

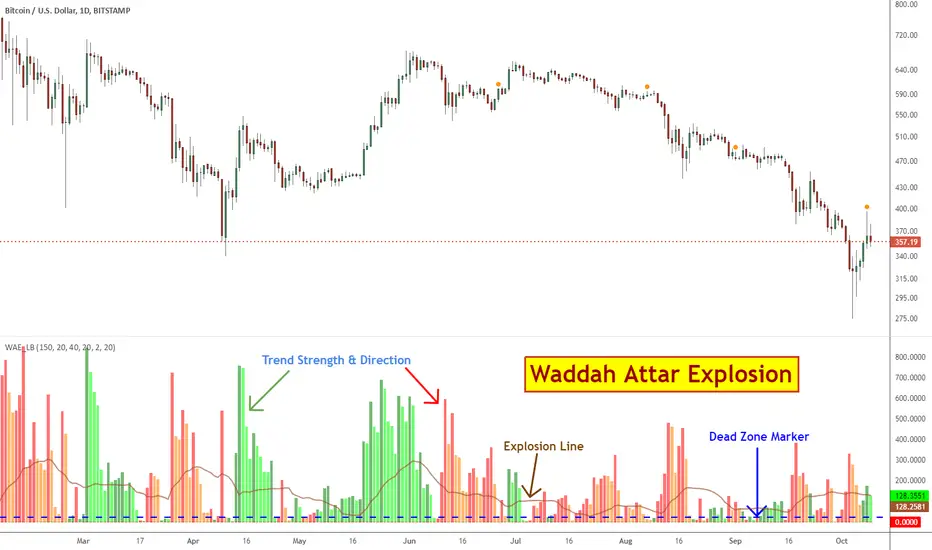

Waddah Attar Explosion [LazyBear]This is a port of a famous MT4 indicator, as requested by user @maximus71. This indicator uses MACD/BB to track trend direction and strength. Author suggests using this indicator on 30mins.

Explanation from the indicator developer:

"Various components of the indicator are:

Dead Zone Line: Works as a filter for weak signals. Do not trade when the red or green histogram is below it.

Histograms:

- Red histogram shows the current down trend.

- Green histogram shows the current up trend.

- Sienna line shows the explosion in price up or down.

Signal for ENTER_BUY: All the following conditions must be met.

- Green histo is raising.

- Green histo above Explosion line.

- Explosion line raising.

- Both green histo and Explosion line above DeadZone line.

Signal for EXIT_BUY: Exit when green histo crosses below Explosion line.

Signal for ENTER_SELL: All the following conditions must be met.

- Red histo is raising.

- Red histo above Explosion line.

- Explosion line raising.

- Both red histo and Explosion line above DeadZone line.

Signal for EXIT_SELL: Exit when red histo crosses below Explosion line. "

All of the parameters are configurable via options page. You may have to tune it for your instrument.

More info:

Author note: www.forex-tsd.com

Video (French): www.youtube.com

List of my other indicators:

- GDoc: docs.google.com

- Chart:

Bill Williams. Awesome Oscillator (AO) Signal Line This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

Strategy Bill Williams. Awesome Oscillator (AO) This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.

Bill Williams. Awesome Oscillator (AO) Hi

Let me introduce my Bill Williams. Awesome Oscillator (AO) script.

This indicator is based on Bill Williams` recommendations from his book

"New Trading Dimensions". We recommend this book to you as most useful reading.

The wisdom, technical expertise, and skillful teaching style of Williams make

it a truly revolutionary-level source. A must-have new book for stock and

commodity traders.

The 1st 2 chapters are somewhat of ramble where the author describes the

"metaphysics" of trading. Still some good ideas are offered. The book references

chaos theory, and leaves it up to the reader to believe whether "supercomputers"

were used in formulating the various trading methods (the author wants to come across

as an applied mathemetician, but he sure looks like a stock trader). There isn't any

obvious connection with Chaos Theory - despite of the weak link between the title and

content, the trading methodologies do work. Most readers think the author's systems to

be a perfect filter and trigger for a short term trading system. He states a goal of

10%/month, but when these filters & axioms are correctly combined with a good momentum

system, much more is a probable result.

There's better written & more informative books out there for less money, but this author

does have the "Holy Grail" of stock trading. A set of filters, axioms, and methods which are

the "missing link" for any trading system which is based upon conventional indicators.

This indicator plots the oscillator as a histogram where periods fit for buying are marked

as blue, and periods fit for selling as red. If the current value of AC (Awesome Oscillator)

is over the previous, the period is deemed fit for buying and the indicator is marked blue.

If the AC values is not over the previous, the period is deemed fir for selling and the indicator

is marked red.