Scientific Correlation Testing FrameworkScientific Correlation Testing Framework - Comprehensive Guide

Introduction to Correlation Analysis

What is Correlation?

Correlation is a statistical measure that describes the degree to which two assets move in relation to each other. Think of it like measuring how closely two dancers move together on a dance floor.

Perfect Positive Correlation (+1.0): Both dancers move in perfect sync, same direction, same speed

Perfect Negative Correlation (-1.0): Both dancers move in perfect sync but in opposite directions

Zero Correlation (0): The dancers move completely independently of each other

In financial markets, correlation helps us understand relationships between different assets, which is crucial for:

Portfolio diversification

Risk management

Pairs trading strategies

Hedging positions

Market analysis

Why This Script is Special

This script goes beyond simple correlation calculations by providing:

Two different correlation methods (Pearson and Spearman)

Statistical significance testing to ensure results are meaningful

Rolling correlation analysis to track how relationships change over time

Visual representation for easy interpretation

Comprehensive statistics table with detailed metrics

Deep Dive into the Script's Components

1. Input Parameters Explained-

Symbol Selection:

This allows you to select the second asset to compare with the chart's primary asset

Default is Apple (NASDAQ:AAPL), but you can change this to any symbol

Example: If you're viewing a Bitcoin chart, you might set this to "NASDAQ:TSLA" to see if Bitcoin and Tesla are correlated

Correlation Window (60): This is the number of periods used to calculate the main correlation

Larger values (e.g., 100-500) provide more stable, long-term correlation measures

Smaller values (e.g., 10-50) are more responsive to recent price movements

60 is a good balance for most daily charts (about 3 months of trading days)

Rolling Correlation Window (20): A shorter window to detect recent changes in correlation

This helps identify when the relationship between assets is strengthening or weakening

Default of 20 is roughly one month of trading days

Return Type: This determines how price changes are calculated

Simple Returns: (Today's Price - Yesterday's Price) / Yesterday's Price

Easy to understand: "The asset went up 2% today"

Log Returns: Natural logarithm of (Today's Price / Yesterday's Price)

More mathematically elegant for statistical analysis

Better for time-additive properties (returns over multiple periods)

Less sensitive to extreme values.

Confidence Level (95%): This determines how certain we want to be about our results

95% confidence means we accept a 5% chance of being wrong (false positive)

Higher confidence (e.g., 99%) makes the test more strict

Lower confidence (e.g., 90%) makes the test more lenient

95% is the standard in most scientific research

Show Statistical Significance: When enabled, the script will test if the correlation is statistically significant or just due to random chance.

Display options control what you see on the chart:

Show Pearson/Spearman/Rolling Correlation: Toggle each correlation type on/off

Show Scatter Plot: Displays a scatter plot of returns (limited to recent points to avoid performance issues)

Show Statistical Tests: Enables the detailed statistics table

Table Text Size: Adjusts the size of text in the statistics table

2.Functions explained-

calcReturns():

This function calculates price returns based on your selected method:

Log Returns:

Formula: ln(Price_t / Price_t-1)

Example: If a stock goes from $100 to $101, the log return is ln(101/100) = ln(1.01) ≈ 0.00995 or 0.995%

Benefits: More symmetric, time-additive, and better for statistical modeling

Simple Returns:

Formula: (Price_t - Price_t-1) / Price_t-1

Example: If a stock goes from $100 to $101, the simple return is (101-100)/100 = 0.01 or 1%

Benefits: More intuitive and easier to understand

rankArray():

This function calculates the rank of each value in an array, which is used for Spearman correlation:

How ranking works:

The smallest value gets rank 1

The second smallest gets rank 2, and so on

For ties (equal values), they get the average of their ranks

Example: For values

Sorted:

Ranks: (the two 2s tie for ranks 1 and 2, so they both get 1.5)

Why this matters: Spearman correlation uses ranks instead of actual values, making it less sensitive to outliers and non-linear relationships.

pearsonCorr():

This function calculates the Pearson correlation coefficient:

Mathematical Formula:

r = (nΣxy - ΣxΣy) / √

Where x and y are the two variables, and n is the sample size

What it measures:

The strength and direction of the linear relationship between two variables

Values range from -1 (perfect negative linear relationship) to +1 (perfect positive linear relationship)

0 indicates no linear relationship

Example:

If two stocks have a Pearson correlation of 0.8, they have a strong positive linear relationship

When one stock goes up, the other tends to go up in a fairly consistent proportion

spearmanCorr():

This function calculates the Spearman rank correlation:

How it works:

Convert each value in both datasets to its rank

Calculate the Pearson correlation on the ranks instead of the original values

What it measures:

The strength and direction of the monotonic relationship between two variables

A monotonic relationship is one where as one variable increases, the other either consistently increases or decreases

It doesn't require the relationship to be linear

When to use it instead of Pearson:

When the relationship is monotonic but not linear

When there are significant outliers in the data

When the data is ordinal (ranked) rather than interval/ratio

Example:

If two stocks have a Spearman correlation of 0.7, they have a strong positive monotonic relationship

When one stock goes up, the other tends to go up, but not necessarily in a straight-line relationship

tStatistic():

This function calculates the t-statistic for correlation:

Mathematical Formula: t = r × √((n-2)/(1-r²))

Where r is the correlation coefficient and n is the sample size

What it measures:

How many standard errors the correlation is away from zero

Used to test the null hypothesis that the true correlation is zero

Interpretation:

Larger absolute t-values indicate stronger evidence against the null hypothesis

Generally, a t-value greater than 2 (in absolute terms) is considered statistically significant at the 95% confidence level

criticalT() and pValue():

These functions provide approximations for statistical significance testing:

criticalT():

Returns the critical t-value for a given degrees of freedom (df) and significance level

The critical value is the threshold that the t-statistic must exceed to be considered statistically significant

Uses approximations since Pine Script doesn't have built-in statistical distribution functions

pValue():

Estimates the p-value for a given t-statistic and degrees of freedom

The p-value is the probability of observing a correlation as strong as the one calculated, assuming the true correlation is zero

Smaller p-values indicate stronger evidence against the null hypothesis

Standard interpretation:

p < 0.01: Very strong evidence (marked with **)

p < 0.05: Strong evidence (marked with *)

p ≥ 0.05: Weak evidence, not statistically significant

stdev():

This function calculates the standard deviation of a dataset:

Mathematical Formula: σ = √(Σ(x-μ)²/(n-1))

Where x is each value, μ is the mean, and n is the sample size

What it measures:

The amount of variation or dispersion in a set of values

A low standard deviation indicates that the values tend to be close to the mean

A high standard deviation indicates that the values are spread out over a wider range

Why it matters for correlation:

Standard deviation is used in calculating the correlation coefficient

It also provides information about the volatility of each asset's returns

Comparing standard deviations helps understand the relative riskiness of the two assets.

3.Getting Price Data-

price1: The closing price of the primary asset (the chart you're viewing)

price2: The closing price of the secondary asset (the one you selected in the input parameters)

Returns are used instead of raw prices because:

Returns are typically stationary (mean and variance stay constant over time)

Returns normalize for price levels, allowing comparison between assets of different values

Returns represent what investors actually care about: percentage changes in value

4.Information Table-

Creates a table to display statistics

Only shows on the last bar to avoid performance issues

Positioned in the top right of the chart

Has 2 columns and 15 rows

Populating the Table

The script then populates the table with various statistics:

Header Row: "Metric" and "Value"

Sample Information: Sample size and return type

Pearson Correlation: Value, t-statistic, p-value, and significance

Spearman Correlation: Value, t-statistic, p-value, and significance

Rolling Correlation: Current value

Standard Deviations: For both assets

Interpretation: Text description of the correlation strength

The table uses color coding to highlight important information:

Green for significant positive results

Red for significant negative results

Yellow for borderline significance

Color-coded headers for each section

=> Practical Applications and Interpretation

How to Interpret the Results

Correlation Strength

0.0 to 0.3 (or 0.0 to -0.3): Weak or no correlation

The assets move mostly independently of each other

Good for diversification purposes

0.3 to 0.7 (or -0.3 to -0.7): Moderate correlation

The assets show some tendency to move together (or in opposite directions)

May be useful for certain trading strategies but not extremely reliable

0.7 to 1.0 (or -0.7 to -1.0): Strong correlation

The assets show a strong tendency to move together (or in opposite directions)

Can be useful for pairs trading, hedging, or as a market indicator

Statistical Significance

p < 0.01: Very strong evidence that the correlation is real

Marked with ** in the table

Very unlikely to be due to random chance

p < 0.05: Strong evidence that the correlation is real

Marked with * in the table

Unlikely to be due to random chance

p ≥ 0.05: Weak evidence that the correlation is real

Not marked in the table

Could easily be due to random chance

Rolling Correlation

The rolling correlation shows how the relationship between assets changes over time

If the rolling correlation is much different from the long-term correlation, it suggests the relationship is changing

This can indicate:

A shift in market regime

Changing fundamentals of one or both assets

Temporary market dislocations that might present trading opportunities

Trading Applications

1. Portfolio Diversification

Goal: Reduce overall portfolio risk by combining assets that don't move together

Strategy: Look for assets with low or negative correlations

Example: If you hold tech stocks, you might add some utilities or bonds that have low correlation with tech

2. Pairs Trading

Goal: Profit from the relative price movements of two correlated assets

Strategy:

Find two assets with strong historical correlation

When their prices diverge (one goes up while the other goes down)

Buy the underperforming asset and short the outperforming asset

Close the positions when they converge back to their normal relationship

Example: If Coca-Cola and Pepsi are highly correlated but Coca-Cola drops while Pepsi rises, you might buy Coca-Cola and short Pepsi

3. Hedging

Goal: Reduce risk by taking an offsetting position in a negatively correlated asset

Strategy: Find assets that tend to move in opposite directions

Example: If you hold a portfolio of stocks, you might buy some gold or government bonds that tend to rise when stocks fall

4. Market Analysis

Goal: Understand market dynamics and interrelationships

Strategy: Analyze correlations between different sectors or asset classes

Example:

If tech stocks and semiconductor stocks are highly correlated, movements in one might predict movements in the other

If the correlation between stocks and bonds changes, it might signal a shift in market expectations

5. Risk Management

Goal: Understand and manage portfolio risk

Strategy: Monitor correlations to identify when diversification benefits might be breaking down

Example: During market crises, many assets that normally have low correlations can become highly correlated (correlation convergence), reducing diversification benefits

Advanced Interpretation and Caveats

Correlation vs. Causation

Important Note: Correlation does not imply causation

Example: Ice cream sales and drowning incidents are correlated (both increase in summer), but one doesn't cause the other

Implication: Just because two assets move together doesn't mean one causes the other to move

Solution: Look for fundamental economic reasons why assets might be correlated

Non-Stationary Correlations

Problem: Correlations between assets can change over time

Causes:

Changing market conditions

Shifts in monetary policy

Structural changes in the economy

Changes in the underlying businesses

Solution: Use rolling correlations to monitor how relationships change over time

Outliers and Extreme Events

Problem: Extreme market events can distort correlation measurements

Example: During a market crash, many assets may move in the same direction regardless of their normal relationship

Solution:

Use Spearman correlation, which is less sensitive to outliers

Be cautious when interpreting correlations during extreme market conditions

Sample Size Considerations

Problem: Small sample sizes can produce unreliable correlation estimates

Rule of Thumb: Use at least 30 data points for a rough estimate, 60+ for more reliable results

Solution:

Use the default correlation length of 60 or higher

Be skeptical of correlations calculated with small samples

Timeframe Considerations

Problem: Correlations can vary across different timeframes

Example: Two assets might be positively correlated on a daily basis but negatively correlated on a weekly basis

Solution:

Test correlations on multiple timeframes

Use the timeframe that matches your trading horizon

Look-Ahead Bias

Problem: Using information that wouldn't have been available at the time of trading

Example: Calculating correlation using future data

Solution: This script avoids look-ahead bias by using only historical data

Best Practices for Using This Script

1. Appropriate Parameter Selection

Correlation Window:

For short-term trading: 20-50 periods

For medium-term analysis: 50-100 periods

For long-term analysis: 100-500 periods

Rolling Window:

Should be shorter than the main correlation window

Typically 1/3 to 1/2 of the main window

Return Type:

For most applications: Log Returns (better statistical properties)

For simplicity: Simple Returns (easier to interpret)

2. Validation and Testing

Out-of-Sample Testing:

Calculate correlations on one time period

Test if they hold in a different time period

Multiple Timeframes:

Check if correlations are consistent across different timeframes

Economic Rationale:

Ensure there's a logical reason why assets should be correlated

3. Monitoring and Maintenance

Regular Review:

Correlations can change, so review them regularly

Alerts:

Set up alerts for significant correlation changes

Documentation:

Keep notes on why certain assets are correlated and what might change that relationship

4. Integration with Other Analysis

Fundamental Analysis:

Combine correlation analysis with fundamental factors

Technical Analysis:

Use correlation analysis alongside technical indicators

Market Context:

Consider how market conditions might affect correlations

Conclusion

This Scientific Correlation Testing Framework provides a comprehensive tool for analyzing relationships between financial assets. By offering both Pearson and Spearman correlation methods, statistical significance testing, and rolling correlation analysis, it goes beyond simple correlation measures to provide deeper insights.

For beginners, this script might seem complex, but it's built on fundamental statistical concepts that become clearer with use. Start with the default settings and focus on interpreting the main correlation lines and the statistics table. As you become more comfortable, you can adjust the parameters and explore more advanced applications.

Remember that correlation analysis is just one tool in a trader's toolkit. It should be used in conjunction with other forms of analysis and with a clear understanding of its limitations. When used properly, it can provide valuable insights for portfolio construction, risk management, and pair trading strategy development.

In den Scripts nach "如何用wind搜索股票的发行价和份数" suchen

Halt-Risk Guard (5-min / 10%) — TTP Safe🛑 Halt-Risk Guard (5-min / 10%) — TTP Safe

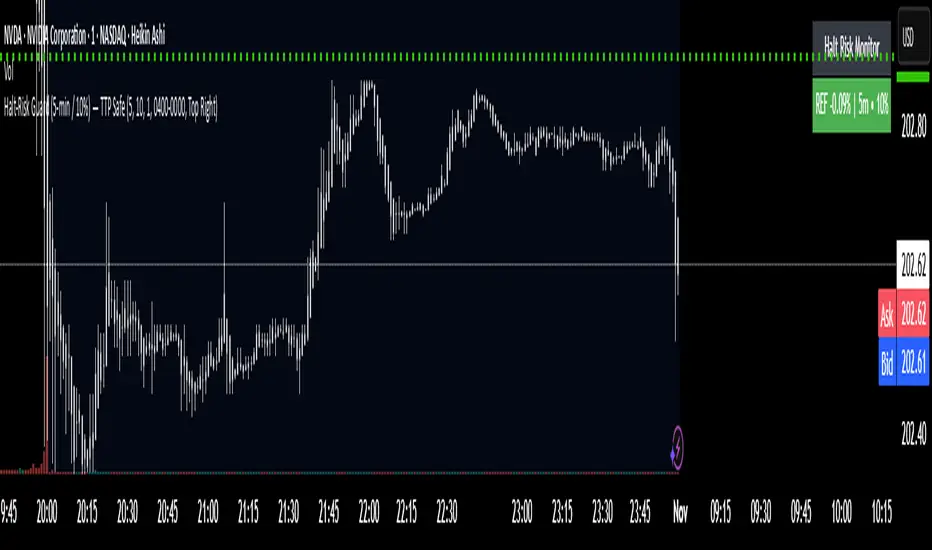

Stay clear of halts, invalidations, and over-extended moves.

🔍 Overview

The Halt-Risk Guard helps traders avoid sudden invalidations by monitoring price velocity over the past X minutes (default: 5 min) and flagging when moves exceed a configurable threshold (default: 10%).

Originally built to meet Trade The Pool (TTP) risk-management rules — where even non-halted 10% moves can void trades — this tool provides a clear, visual warning system and optional entry blocker.

⚙️ Key Features

✅ Halt-Risk Detection – Calculates both reference-based and swing-based (high↔low) percentage change over the chosen lookback period.

✅ TTP Safe Mode – “Swing mode” captures extreme volatility spikes that may invalidate trades even when the market stays open.

✅ Entry Blocker (optional) – Automatically greys candles and dims the background during risky conditions to prevent impulsive entries.

✅ Customisable Positioning – Move the on-chart info box to any corner of your chart (Top Left / Top Right / Bottom Left / Bottom Right).

✅ Clean Alerts –

⚠️ At/Above Threshold

✅ Back to Safe

⛔ Entry Blocker Active

✅ Visual Table Display – Compact dashboard shows current % move, lookback window, and threshold with intuitive green/red status.

✅ Strategy-Ready Output – A hidden 0/1 plot lets you block or filter trades in automated systems.

⚡ How It Works

Monitors the selected symbol using your chosen computation timeframe (recommended 1-minute).

Evaluates either:

REF mode: Close-to-close change over the lookback window.

SWING mode: High-to-low range within the same window.

If the move ≥ Threshold %, the script highlights a halt-risk condition and optionally activates the entry blocker.

🎨 Recommended Settings

Lookback: 5 minutes

Threshold: 10 %

Swing mode: ON (TTP-safe)

Computation timeframe: 1 minute

Entry blocker: ON

Dim background: ON

🧠 Use Cases

TTP and other prop-firm evaluations enforcing price-movement limits.

Volatility-based scalping systems to avoid chasing extended candles.

Strategy filters for algorithmic entries (e.g. pause trading during halt-risk windows).

⚠️ Disclaimer

This tool provides visual and alert-based guidance only. It does not guarantee compliance with any specific firm’s rules or eliminate trading risk. Always verify thresholds and rules with your broker or evaluation provider.

BTC/USD Breakout Hours – IST (Hyderabad)This indicator highlights the most volatile BTC/USD trading hours based on Hyderabad (IST) time.

It marks three key breakout windows:

London–US Overlap (17:30–20:30 IST) – Highest liquidity & volatility

US Market Open Momentum (19:00–23:30 IST) – Strong trend moves

Early London Session (12:30–15:30 IST) – Pre-US setup moves

The script automatically converts chart time to IST, shades each breakout window, and includes optional alerts for:

Window start

15 minutes before start

Ideal for traders who want to align entries with high-probability market moves while avoiding low-volume hours.

Closed Market / Back-Test Filter x 'Bull_Trap_9'Hello TradingView Traders!

This is a very valuable tool that I believe all traders will find useful.

This indicator / filter is '1 of 2'. I prefer it as a filter because it is not meant for live trade analysis. It is designed to make a trader aware of their individual trade sessions and to help aid in static chart candlestick back-testing.

Also, look for my indicator / filter, '2 of 2': 'Red Report Filter'

There are two functions to this filter.

Primary use: It allows a trader to set a session window: Open / Close.

During a trade session, like YM, I only trade 9:30 - 15:00. Without the filter, many times I have traded past my cutoff because I was focused on the chart and not the time.

With this filter on as close nears with an open trade and the filter starts to apply, I know I am at session close with no more trades upon exit. Otherwise, I know the session is done with no further trades.

It is also nice to have the filter on during the session open as a demarcation boundary.

Secondary use: It is used as a chart back-test tool.

When applied to a traders back-test chart, the trader can control their trade session envelopes for easier and more precise evaluation. The filter will allow only the candles per session that the trader wants to focus on and will filter all other non-session candles.

I can easily compare a whole week of 30m session data, concentrating solely on the filtered trade windows.

Please Note: The filter will be active as far back as the historic data prints.

Thanks for viewing!

Hurst Exponent Oscillator [PhenLabs]📊 Hurst Exponent Oscillator -

Version: PineScript™ v5

📌 Description

The Hurst Exponent Oscillator (HEO) by PhenLabs is a powerful tool developed for traders who want to distinguish between trending, mean-reverting, and random market behaviors with clarity and precision. By estimating the Hurst Exponent—a statistical measure of long-term memory in financial time series—this indicator helps users make sense of underlying market dynamics that are often not visible through traditional moving averages or oscillators.

Traders can quickly know if the market is likely to continue its current direction (trending), revert to the mean, or behave randomly, allowing for more strategic timing of entries and exits. With customizable smoothing and clear visual cues, the HEO enhances decision-making in a wide range of trading environments.

🚀 Points of Innovation

Integrates advanced Hurst Exponent calculation via Rescaled Range (R/S) analysis, providing unique market character insights.

Offers real-time visual cues for trending, mean-reverting, or random price action zones.

User-controllable EMA smoothing reduces noise for clearer interpretation.

Dynamic coloring and fill for immediate visual categorization of market regime.

Configurable visual thresholds for critical Hurst levels (e.g., 0.4, 0.5, 0.6).

Fully customizable appearance settings to fit different charting preferences.

🔧 Core Components

Log Returns Calculation: Computes log returns of the selected price source to feed into the Hurst calculation, ensuring robust and scale-independent analysis.

Rescaled Range (R/S) Analysis: Assesses the dispersion and cumulative deviation over a rolling window, forming the core statistical basis for the Hurst exponent estimate.

Smoothing Engine: Applies Exponential Moving Average (EMA) smoothing to the raw Hurst value for enhanced clarity.

Dynamic Rolling Windows: Utilizes arrays to maintain efficient, real-time calculations over user-defined lengths.

Adaptive Color Logic: Assigns different highlight and fill colors based on the current Hurst value zone.

🔥 Key Features

Visually differentiates between trending, mean-reverting, and random market modes.

User-adjustable lookback and smoothing periods for tailored sensitivity.

Distinct fill and line styles for each regime to avoid ambiguity.

On-chart reference lines for strong trending and mean-reverting thresholds.

Works with any price series (close, open, HL2, etc.) for versatile application.

🎨 Visualization

Hurst Exponent Curve: Primary plotted line (smoothed if EMA is used) reflects the ongoing estimate of the Hurst exponent.

Colored Zone Filling: The area between the Hurst line and the 0.5 reference line is filled, with color and opacity dynamically indicating the current market regime.

Reference Lines: Dash/dot lines mark standard Hurst thresholds (0.4, 0.5, 0.6) to contextualize the current regime.

All visual elements can be customized for thickness, color intensity, and opacity for user preference.

📖 Usage Guidelines

Data Settings

Hurst Calculation Length

Default: 100

Range: 10-300

Description: Number of bars used in Hurst calculation; higher values mean longer-term analysis, lower values for quicker reaction.

Data Source

Default: close

Description: Select which data series to analyze (e.g., Close, Open, HL2).

Smoothing Length (EMA)

Default: 5

Range: 1-50

Description: Length for smoothing the Hurst value; higher settings yield smoother but less responsive results.

Style Settings

Trending Color (Hurst > 0.5)

Default: Blue tone

Description: Color used when trending regime is detected.

Mean-Reverting Color (Hurst < 0.5)

Default: Orange tone

Description: Color used when mean-reverting regime is detected.

Neutral/Random Color

Default: Soft blue

Description: Color when market behavior is indeterminate or shifting.

Fill Opacity

Default: 70-80

Range: 0-100

Description: Transparency of area fills—higher opacity for stronger visual effect.

Line Width

Default: 2

Range: 1-5

Description: Thickness of the main indicator curve.

✅ Best Use Cases

Identifying if a market is regime-shifting from trending to mean-reverting (or vice versa).

Filtering signals in automated or systematic trading strategies.

Spotting periods of randomness where trading signals should be deprioritized.

Enhancing mean-reversion or trend-following models with regime-awareness.

⚠️ Limitations

Not predictive: Reflects current and recent market state, not future direction.

Sensitive to input parameters—overfitting may occur if settings are changed too frequently.

Smoothing can introduce lag in regime recognition.

May not work optimally in markets with structural breaks or extreme volatility.

💡 What Makes This Unique

Employs advanced statistical market analysis (Hurst exponent) rarely found in standard toolkits.

Offers immediate regime visualization through smart dynamic coloring and zone fills.

🔬 How It Works

Rolling Log Return Calculation:

Each new price creates a log return, forming the basis for robust, non-linear analysis. This ensures all price differences are treated proportionally.

Rescaled Range Analysis:

A rolling window maintains cumulative deviations and computes the statistical “range” (max-min of deviations). This is compared against the standard deviation to estimate “memory”.

Exponent Calculation & Smoothing:

The raw Hurst value is translated from the log of the rescaled range ratio, and then optionally smoothed via EMA to dampen noise and false signals.

Regime Detection Logic:

The smoothed value is checked against 0.5. Values above = trending; below = mean-reverting; near 0.5 = random. These control plot/fill color and zone display.

💡 Note:

Use longer calculation lengths for major market character study, and shorter ones for tactical, short-term adaptation. Smoothing balances noise vs. lag—find a best fit for your trading style. Always combine regime awareness with broader technical/fundamental context for best results.

MACD by Take and TradeImproved version of MACD with asymmetrical BUY and SELL approaches.

This indicator is based on popular MACD one, but with some "tricks" designed to make it more applicable to the rapidly changing crypto market.

Key benefits:

Dynamic auto-adjusted threshold to filter out weak signals

Highlighted BUY/SELL signals with divergence (if a signal is accompanied by divergence, for example, price makes a new high while macd has a second high below the first, this signal is considered stronger and will be highlighted in a darker color)

Boost BUY signals on very slow market in accumulation phase

Not symmetric! It uses 2 different signal lines, which allows to obtain SELL signals earlier comparing to classic MACD approach

Classic concept of MACD

Classic MACD, in its simplest case, consists of two lines - macd line and signal line. Macd line is a difference between so-called "fast" and "slow" EMA lines (there are just a Exponential Moving Average lines with different windows: "12" for fast and "26" for slow). Signal line is just a smoothed "macd" line.

When macd line crosses signal line from bottom to up and intersection point < 0, this is "BUY" signal. And vise versa, when macd line crosses signal line from top to bottom, and intersection point > 0, this is "SELL" signal.

Parameters used in default configuration of classic MACD indicator:

Fast line: EMA-12

Slow line: EMA-26

Signal line: EMA-9

Problem of classic concept

Classic MACD indicator usually gives not bad "BUY" signals, especially if using them not for operational trading but for "investment" strategy. But "SELL" signalls usually generated too late. Simply because the market tends to fall much faster than it rises.

Possible solution (the main feature of our version of MACD)

To make indicator react faster on SELL condition, while still keeping it reliable for BUY signals, we decided to use two signal lines . Faster than default signal line (with window=6) for BUY signals and much faster than default (with window=2) for SELL signals.

This approach allowed us to receive sell signals earlier and exit deals on more favorable prices. Trade off of this change - is the number of SELL signals - there were more of them. However, this does not matter, since we receive the very first sell signal with a "very fast signal line" much earlier than with classic indicator settings.

Parameters we use in our improved MACD indicator:

Fast line: EMA-12

Slow line: EMA-24

Faster signal line: EMA-6

Much faster signal line: EMA-2

Removing noise (false triggerings)

Other drawback of classic MACD - it generates a lot of "weak" (false) signals. This signals are generated when macd crosses signal line much close to zero-line. And usually there are a lot of such intersections.

To remove this kind of noise, we added a trigger threshold, which by default is equal to 2.5% of the average asset price over a long period of time. Due to the link to the average price, this threshold automatically takes a specific value for each trading pair. Threshold 2.5% works perfect for all trading pairs for 1D timeframe. For other timeframes user can (and maybe will want) change it.

Boost weak BUY signals in a prolonged bear market

Signals on bearish stage are usually very weak, because there is no volatility, and no price impulse. And such signals will be filtered out as "noise" - see above. But this time is perfect time to buy! Therefore, we further boost the buy signals in a prolonged bear market so that they can pass through the filter and appear on the chart. Bearish period is the best time to invest!

Developed by Take and Trade. Enjoy using it!

The Echo Forecast [LuxAlgo]This indicator uses a simple time series forecasting method derived from the similarity between recent prices and similar/dissimilar historical prices. We named this method "ECHO".

This method originally assumes that future prices can be estimated from a historical series of observations that are most similar to the most recent price variations. This similarity is quantified using the correlation coefficient. Such an assumption can prove to be relatively effective with the forecasting of a periodic time series. We later introduced the ability to select dissimilar series of observations for further experimentation.

This forecasting technique is closely inspired by the analogue method introduced by Lorenz for the prediction of atmospheric data.

1. Settings

Evaluation Window: Window size used for finding historical observations similar/dissimilar to recent observations. The total evaluation window is equal to "Forecast Window" + "Evaluation Window"

Forecast Window: Determines the forecasting horizon.

Forecast Mode: Determines whether to choose historical series similar or dissimilar to the recent price observations.

Forecast Construction: Determines how the forecast is constructed. See "Usage" below.

Src: Source input of the forecast

Other style settings are self-explanatory.

2. Usage

This tool can be used to forecast future trends but also to indicate which historical variations have the highest degree of similarity/dissimilarity between the observations in the orange zone.

The forecasting window determines the prices segment (in orange) to be used as a reference for the search of the most similar/dissimilar historical price segment (in green) within the gray area.

Most forecasting techniques highly benefit from a detrended series. Due to the nature of this method, we highly recommend applying it to a detrended and periodic series.

You can see above the method is applied on a smooth periodic oscillator and a momentum oscillator.

The construction of the forecast is made from the price changes obtained in the green area, denoted as w(t) . Using the "Cumulative" options we construct the forecast from the cumulative sum of w(t) . Finally, we add the most recent price value to this cumulated series.

Using the "Mean" options will add the series w(t) with the mean of the prices within the orange segment.

Finally the "Linreg" will add the series w(t) to an extrapolated linear regression fit to the prices within the orange segment.

PM Range Breaker [CHE] PM Range Breaker — Premarket bias with first-five range breaks, optional SWDEMA regime latch, and simple two-times-range targets

Summary

This indicator sets a once-per-day directional bias during New York premarket and then tracks a strict first-five-minutes range from the session open. After the first five complete, it marks clean breakouts and can project targets at two times the measured range. A second mode latches an EMA-based regime to inform the bias and optional background tinting. A compact panel reports live state, first-five levels, and rolling hit rates of both bias modes using a user-defined midday close for statistics.

Motivation: Why this design?

Intraday traders often get whipsawed by early noise or by fast flips in trend filters. This script commits to a bias at a single premarket minute and then waits for the market to present an objective structure: the first-five range. Breaks after that window are clearer and easier to manage. The alternative SWDEMA regime gives a slower, latched context for users who prefer a trend scaffold rather than a midpoint reference.

What’s different vs. standard approaches?

Baseline: Typical open-range-breakout lines or a single moving-average filter without daily commitment.

Architecture differences:

Bias decision at a fixed New York time using either a midpoint lookback (“Classic”) or a two-EMA regime latch (“SWDEMA”).

Strict five-minute window from session open; breakout shapes print only after that window.

Single-shot breakout direction per session (debounce) and optional two-times-range targets.

On-chart panel with hit rates using a configurable midday close for statistics.

Practical effect: Cleaner visuals, fewer repeated signals, and a traceable daily decision that can be evaluated over time.

How it works (technical)

Time handling uses New York session times for premarket decision, open, first-five end, and a midday statistics checkpoint.

Classic bias: A midpoint is computed from the highest and lowest over a user period; at the premarket minute, the bias is set long when the close is above the midpoint, short otherwise.

SWDEMA bias: Two EMAs define a regime score that requires price and trend agreement; when both agree on a confirmed bar, the regime latches. At the premarket minute, the daily bias is set from the current regime.

The first-five range captures high and low from open until the end minute, then freezes. Breakouts are detected after that window using close-based cross logic.

The script draws range lines and optional targets at two times the frozen range. A session break direction latch prevents duplicate break markers.

Statistics compare daily open and a configurable midday close to record if the chosen bias aligned with the move.

Optional elements include EMA lines, midpoint line, latched-regime background, and regime switch markers.

Data aggregation for day logic and the first-five window is sampled on one-minute data with explicit lookahead off. On charts above one minute, values update intra-bar until the underlying minute closes.

Parameter Guide

Premarket Start (NY) — Minute when the bias is decided — Default: 08:30 — Move earlier for more stability; later for recency.

Market Open (NY) — Session start used for the first-five window — Default: 09:30 — Align to instrument’s RTH if different.

First-5 End (NY) — End of the first-five window — Default: 09:35 — Extend slightly to capture wider opening ranges.

Day End (NY) for Stats — Midday checkpoint for hit rate — Default: 12:00 — Use a later time for a longer evaluation window.

Show First-5 Lines — Draw the frozen range lines — Default: On — Turn off if your chart is crowded.

Show Bias Background (Session) — Tint by daily bias during session — Default: On — Useful for directional context.

Show Break Shapes — Print breakout triangles — Default: On — Disable if you only want lines and alerts.

Show 2R Targets (Optional) — Plot targets at two times the range — Default: On — Switch off if you manage exits differently.

Line Length Right — Extension length of drawn lines — Default: 20 (bars) — Increase for slower timeframes.

High/Low Line Colors — Visual colors for range levels — Defaults: Green/Red — Adjust to your theme.

Long/Short Bias Colors — Background tints — Defaults: Green/Red with high transparency — Lower transparency for stronger emphasis.

Show Corner Panel — Enable the info panel — Default: On — Centralizes status and numbers.

Show Hit Rates in Panel — Include success rates — Default: On — Turn off to reduce panel rows.

Panel Position — Anchor on chart — Default: Top right — Move to avoid overlap.

Panel Size — Text size in panel — Default: Small — Increase on high-resolution displays.

Dark Panel — Dark theme for the panel — Default: On — Match your chart background.

Show EMA Lines — Plot blue and red EMAs — Default: Off — Enable for SWDEMA context.

Show Midpoint Line — Plot the midpoint — Default: Off — Useful for Classic mode visualization.

Midpoint Lookback Period — Bars for high-low midpoint — Default: 300 — Larger values stabilize; smaller values respond faster.

Midpoint Line Color — Color for midpoint — Default: Gray — A neutral line works best.

SWDEMA Lengths (Blue/Red) — Periods for the two EMAs — Defaults: 144 and 312 — Longer values reduce flips.

Sources (Blue/Red) — Price sources — Defaults: Close and HLC3 — Adjust if you prefer consistency.

Offsets (Blue/Red) — Pixel offsets for EMA plots — Defaults: zero — Use only for visual shift.

Show Latched Regime Background — Background by SWDEMA regime — Default: Off — Separate from session bias.

Latched Background Transparency — Opacity of regime background — Default: eighty-eight — Lower value for stronger tint.

Show Latch Switch Markers — Plot regime change markers — Default: Off — For auditing regime changes.

Bias Mode — Classic midpoint or SWDEMA latch — Default: Classic — Choose per your style.

Background Mode — Session bias or SWDEMA regime — Default: Session — Decide which background narrative you want.

Reading & Interpretation

Panel: Shows the active bias, first-five high and low, and a state that reads Building during the window, Ready once frozen, and Break arrows when a breakout occurs. Hit rates show the percentage of days where each bias mode aligned with the midday move.

Colors and shapes: Green background implies long bias; red implies short bias. Triangle markers denote the first valid breakout after the first-five window. Optional regime markers flag regime changes.

Lines: First-five high and low form the core structure. Optional targets mark a level at two times the frozen range from the breakout side.

Practical Workflows & Combinations

Trend following: Choose a bias mode. Wait for the first clean breakout after the first-five window in the direction of the bias. Confirm with structure such as higher highs and higher lows or lower highs and lower lows.

Exits and risk: Conservative users can trail behind the opposite side of the first-five range. Aggressive users can scale near the two-times-range target.

Multi-asset and multi-TF: Works well on intraday timeframes from one minute upward. For non-US sessions, adjust the time inputs to the instrument’s regular trading hours.

Behavior, Constraints & Performance

Repaint and confirmation: Bias and regime decisions use confirmed bars. Breakout signals evaluate on bar close at the chart timeframe. On higher timeframes, minute-based sources update within the live bar until the minute closes.

security and HTF: The script samples one-minute data. Lookahead is off. Values stabilize once the source minute closes.

Resources: `max_bars_back` is five thousand. Drawing objects and the panel update efficiently, with position extensions handled on the last bar.

Known limits: Midday statistics use the configured time, not the official daily close. Session logic assumes New York session timing. Targets are simple multiples of the first-five range and do not adapt to volatility beyond that structure.

Sensible Defaults & Quick Tuning

Start with Classic bias, midpoint lookback at three hundred, and all visuals on.

Too many flips in context → switch to SWDEMA mode or increase EMA lengths.

Breakouts feel noisy → extend the first-five end by a minute or two, or wait for a retest by your own rules.

Too sluggish → reduce midpoint lookback or shorten EMA lengths.

Chart cluttered → hide EMA or midpoint lines and keep only range levels and breakout shapes.

What this indicator is—and isn’t

This is a visualization and signal layer for session bias and first-five structure. It does not manage orders, position sizing, or risk. It is not predictive. Use it alongside market structure, execution rules, and independent risk controls.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Many thanks to LonesomeTheBlue

for the original work. I adapted the midpoint calculation for this script. www.tradingview.com

Rolling Midpoint of Price & VWAP with ATR BandsThe Rolling Midpoint of Price & VWAP with ATR Bands indicator is a dual-equilibrium concept that fuses price-range structure and traded-volume flow into one continuously updating hybrid model. Traditional VWAPs reset each session and reflect where trading occurred by volume, while midpoints used here reveal where price has structurally balanced between extremes. This script merges both ideas into a cohesive, dynamic system. The Rolling Price Midpoint (50 % of range) represents the structural fair-value line, calculated as the average of the highest high and lowest low over a selected window. The Rolling VWAP (Volume-Weighted Window) tracks the flow-based fair-value line by weighting each bar’s typical price by its volume. Together, these components form the Hybrid Equilibrium — the adaptive center of gravity that shifts as price and volume evolve. Surrounding this equilibrium, ATR Bands at ± 2.226 ATR and ± 5.382 ATR define volatility envelopes that expand and contract with market energy. The result is a living cloud that breathes with the market: compressing during phases of balance and widening during impulsive movements, offering traders a clear visual framework for understanding equilibrium, volatility, and directional bias in real time.

➖

⚙️ Auto-Preset System

The Auto-Preset System intelligently adjusts lookback windows for both the Price Midpoint and VWAP calculations according to the active chart timeframe.

This ensures that the indicator automatically adapts to any trading style — from scalping on 1-minute charts to swing trading on daily or weekly charts — without manual tuning.

🔹 How It Works

When Auto-Preset mode is enabled, the script dynamically selects the most effective lookback lengths for each timeframe.

These presets are optimized to balance responsiveness and stability, maintaining consistent real-world coverage (e.g., the same approximate duration of price data) across all intervals.

📊 Preset Mapping Table

| Chart Timeframe | Price Midpoint Lookback | VWAP Lookback |

|:----------------:|:-----------------------:|:--------------:|

| 1–3m | 13 bars | 21 bars

| 5–10m | 21 bars | 34 bars

| 15–30m | 34 bars | 55 bars

| 1–2 hr | 55 bars | 89 bars

| 4 hr-1D | 89 bars | 144 bars

| 1W | 144 bars | 233 bars

| 1M | 233 bars | 377 bars

⚡ Notes & Customization

- Manual Override: Turn off Auto-Preset Mode to specify your own custom lookback lengths.

- Consistency Across Scales: These adaptive values keep the indicator visually coherent when switching between timeframes — avoiding distortions that can occur with static lengths.

- Practical Benefit: Traders can maintain a single chart layout that self-tunes seamlessly, removing the need to manually recalibrate settings when shifting from short-term to long-term analysis.

In short, the Auto-Preset System is designed to make this hybrid equilibrium tool timeframe-aware — automatically scaling its logic so that the cloud behaves consistently, regardless of chart resolution.

➖

🌐 Hybrid Equilibrium Envelope

The core hybrid midpoint acts as the mean of structural (price) and volumetric (VWAP) balance.

ATR-based bands project natural expansion zones:

🔸+2.226 / –2.226 ATR → inner equilibrium (controlled trend)

*🔸+5.382 / –5.382 ATR → outer volatility extension (over-stretch / reversion zones)

Color-coded fills show regime strength:

* 🟧 Upper Outer (+5.382) – strong bullish expansion

* 🟩 Upper Inner (+2.226) – trending equilibrium

* 🔴 Lower Inner (–2.226) – mild bearish control

* 🟣 Lower Outer (–5.382) – volatility exhaustion

➖

🧭 Higher-Timeframe Framework

Two macro anchors — Price length of 144 and VWAP length of 233 — outline higher-timeframe bias zones. These help confirm when local momentum aligns with (or fades against) long-term structure.

Labels on the right show active lookback values for quick readout:

`$(13) V(21)` → current rolling pair

`$144 / V233` → macro anchors

➖

🧩 Chart Examples

**AMD 15m (Equilibrium Expansion)**

Price steadily rides above the hybrid midpoint as teal and orange (bullish) ATR zones widen, confirming a phase of controlled bullish volatility and healthy trend expansion.

BTCUSD 1m (Volatility Compression)

Bitcoin coils tightly inside the teal-to-maroon equilibrium bands before breaking out.

The hybrid midpoint flattens and ATR envelopes contract, signaling a state of balance before volatility expansion.

ETHUSD 15m (Transition from Compression → Impulse)

Ethereum transitions from purple-zone compression into a clear upper-band expansion.

The hybrid midpoint breaks above the macro VWAP 233, confirming the shift from equilibrium to directional momentum.

SOFI 1m (Micro Bias Reversal)

SOFI’s intraday structure flips as price reclaims the hybrid midpoint.

The macro VWAP 233 flattens, signaling a transition from oversold lower bands back toward equilibrium and early trend recovery.

➖

🎯 How to Use

1. Bias Detection – Price > Hybrid Midpoint → bullish; < → bearish.

2. Volatility Gauge – Watch band spacing for compression / expansion cycles.

3. Confluence Checks – Align Hybrid Midpoint with HTF 233 VWAP for strong continuation signals.

4. Mean Reversion Zones – Outer bands highlight areas where probability of snap-back increases.

➖

🔧 Inputs & Customization

Auto Presets toggle

🔸Manual Lookback Overrides** for fine-tuning

🔸Plot Window Length** (show recent vs full history)

🔸ATR Sensitivity & Fill Opacity** controls

🔸Label Padding / Font Size** for cleaner overlay visuals

➖

🧮 Formula Highlights

➖Rolling Midpoint = (highest(high,N) + lowest(low,N)) / 2

➖Rolling VWAP = Σ(Typical Price×Vol) / Σ(Vol)

➖Hybrid = (PriceMid + VWAP) / 2

➖Upper₂ = Hybrid + ATR×2.226

➖Lower₂ = Hybrid − ATR×2.226

➖Upper₅ = Hybrid + ATR×5.382

➖Lower₅ = Hybrid − ATR×5.382

➖

🎯 Ideal For

➡️ Traders who want adaptive fair-value zones that evolve with both price and volume.

➡️ Analysts who shift between scalping, swing, and position timeframes, and need a tool that self-adjusts.

➡️ Those who rely on visual structure clarity to confirm setups across changing volatility conditions.

➡️ Anyone seeking a hybrid model that unites structural range logic (midpoint) and flow-based balance (VWAP).

➖

🏁 Final Word

This script is more than a visual overlay — it’s a complete trend and structure framework built to adapt with market rhythm. It helps traders visualize equilibrium, momentum, and volatility as one cohesive system. Whether you’re seeking clean trend alignment, dynamic support/resistance, or early warning signs of reversals, this indicator is tuned to help you react with confidence — not hindsight.

➖

Remember — no single indicator should ever stand alone. For best results, pair it with price action context, higher-timeframe structure, and complementary tools such as moving averages or trendlines. Use it to confirm setups, not define them in isolation.

💡 Turn logic into clarity, structure into trades, and uncertainty into confidence.

Breakouts with timefilter [LuciTech]Here's the updated description with "colors" replaced by "colours" throughout, maintaining the original structure and content:

Breaking Point 2.0

This is a technical analysis overlay indicator designed to identify breakout levels based on pivot highs and lows, with a focus on price action during customizable time windows using London time (UK). It draws horizontal lines at pivot points and plots signals when price breaks above or below these levels, offering traders a tool to monitor potential bullish or bearish movements. The indicator includes options for time filtering and displaying only the most recent breakout.

Features

The Pivot Breakout Lines display horizontal lines at detected pivot highs (bullish) and pivot lows (bearish), coloured green and red by default. These lines extend from the pivot point to the breakout bar and can be set to show only the latest breakout.

The Breakout Signals mark bullish breakouts with an upward triangle below the bar and bearish breakouts with a downward triangle above the bar, using customizable colours.

The Time Filter restricts signals and lines to a specific window (default: 14:30–15:00 UK), which can be toggled on or off. A shaded background highlights this period when enabled.

How It Works

The indicator calculates pivot highs and lows using a user-defined lookback period (default: 5 bars). When price closes above a pivot high, it triggers a bullish signal and draws a line from the pivot to the breakout bar. When price closes below a pivot low, it triggers a bearish signal with a corresponding line.

If the time filter is active, signals and lines only appear within the specified window. Outside this period—or if the filter is disabled—they appear based solely on price action. The indicator maintains up to three recent pivots in memory, removing older ones as new pivots form.

Alerts are available for both bullish and bearish breakouts, triggered when signals occur.

Settings

Length controls the lookback period for pivot detection (default: 5).

Colours Bull/Bear sets the colours for bullish (default: green) and bearish (default: red) lines and signals.

Show Last Breakout toggles whether only the most recent breakout line and signal are displayed (default: false).

Time Filter enables or disables the time restriction (default: true).

Fill Background toggles a shaded area during the time window (default: true), with a customizable colour.

Time Settings define the start hour/minute and end hour/minute for the filter (default: 14:30–15:00).

Interpretation

The Pivot Breakout Lines highlight levels where price has previously reversed, potentially acting as support or resistance. A breakout above a pivot high may suggest bullish momentum, while a breakout below a pivot low may indicate bearish pressure.

The Breakout Signals provide visual cues for these events, useful for timing entries or exits. When "Show Last Breakout" is enabled, the chart focuses on the most recent signal, reducing clutter.

The Time Filter and background shading help traders concentrate on specific trading sessions, such as high-volatility periods. When disabled, the indicator tracks breakouts across all times.

Backtesting & Trading Engine [PineCoders]The PineCoders Backtesting and Trading Engine is a sophisticated framework with hybrid code that can run as a study to generate alerts for automated or discretionary trading while simultaneously providing backtest results. It can also easily be converted to a TradingView strategy in order to run TV backtesting. The Engine comes with many built-in strats for entries, filters, stops and exits, but you can also add you own.

If, like any self-respecting strategy modeler should, you spend a reasonable amount of time constantly researching new strategies and tinkering, our hope is that the Engine will become your inseparable go-to tool to test the validity of your creations, as once your tests are conclusive, you will be able to run this code as a study to generate the alerts required to put it in real-world use, whether for discretionary trading or to interface with an execution bot/app. You may also find the backtesting results the Engine produces in study mode enough for your needs and spend most of your time there, only occasionally converting to strategy mode in order to backtest using TV backtesting.

As you will quickly grasp when you bring up this script’s Settings, this is a complex tool. While you will be able to see results very quickly by just putting it on a chart and using its built-in strategies, in order to reap the full benefits of the PineCoders Engine, you will need to invest the time required to understand the subtleties involved in putting all its potential into play.

Disclaimer: use the Engine at your own risk.

Before we delve in more detail, here’s a bird’s eye view of the Engine’s features:

More than 40 built-in strategies,

Customizable components,

Coupling with your own external indicator,

Simple conversion from Study to Strategy modes,

Post-Exit analysis to search for alternate trade outcomes,

Use of the Data Window to show detailed bar by bar trade information and global statistics, including some not provided by TV backtesting,

Plotting of reminders and generation of alerts on in-trade events.

By combining your own strats to the built-in strats supplied with the Engine, and then tuning the numerous options and parameters in the Inputs dialog box, you will be able to play what-if scenarios from an infinite number of permutations.

USE CASES

You have written an indicator that provides an entry strat but it’s missing other components like a filter and a stop strategy. You add a plot in your indicator that respects the Engine’s External Signal Protocol, connect it to the Engine by simply selecting your indicator’s plot name in the Engine’s Settings/Inputs and then run tests on different combinations of entry stops, in-trade stops and profit taking strats to find out which one produces the best results with your entry strat.

You are building a complex strategy that you will want to run as an indicator generating alerts to be sent to a third-party execution bot. You insert your code in the Engine’s modules and leverage its trade management code to quickly move your strategy into production.

You have many different filters and want to explore results using them separately or in combination. Integrate the filter code in the Engine and run through different permutations or hook up your filtering through the external input and control your filter combos from your indicator.

You are tweaking the parameters of your entry, filter or stop strat. You integrate it in the Engine and evaluate its performance using the Engine’s statistics.

You always wondered what results a random entry strat would yield on your markets. You use the Engine’s built-in random entry strat and test it using different combinations of filters, stop and exit strats.

You want to evaluate the impact of fees and slippage on your strategy. You use the Engine’s inputs to play with different values and get immediate feedback in the detailed numbers provided in the Data Window.

You just want to inspect the individual trades your strategy generates. You include it in the Engine and then inspect trades visually on your charts, looking at the numbers in the Data Window as you move your cursor around.

You have never written a production-grade strategy and you want to learn how. Inspect the code in the Engine; you will find essential components typical of what is being used in actual trading systems.

You have run your system for a while and have compiled actual slippage information and your broker/exchange has updated his fees schedule. You enter the information in the Engine and run it on your markets to see the impact this has on your results.

FEATURES

Before going into the detail of the Inputs and the Data Window numbers, here’s a more detailed overview of the Engine’s features.

Built-in strats

The engine comes with more than 40 pre-coded strategies for the following standard system components:

Entries,

Filters,

Entry stops,

2 stage in-trade stops with kick-in rules,

Pyramiding rules,

Hard exits.

While some of the filter and stop strats provided may be useful in production-quality systems, you will not devise crazy profit-generating systems using only the entry strats supplied; that part is still up to you, as will be finding the elusive combination of components that makes winning systems. The Engine will, however, provide you with a solid foundation where all the trade management nitty-gritty is handled for you. By binding your custom strats to the Engine, you will be able to build reliable systems of the best quality currently allowed on the TV platform.

On-chart trade information

As you move over the bars in a trade, you will see trade numbers in the Data Window change at each bar. The engine calculates the P&L at every bar, including slippage and fees that would be incurred were the trade exited at that bar’s close. If the trade includes pyramided entries, those will be taken into account as well, although for those, final fees and slippage are only calculated at the trade’s exit.

You can also see on-chart markers for the entry level, stop positions, in-trade special events and entries/exits (you will want to disable these when using the Engine in strategy mode to see TV backtesting results).

Customization

You can couple your own strats to the Engine in two ways:

1. By inserting your own code in the Engine’s different modules. The modular design should enable you to do so with minimal effort by following the instructions in the code.

2. By linking an external indicator to the engine. After making the proper selections in the engine’s Settings and providing values respecting the engine’s protocol, your external indicator can, when the Engine is used in Indicator mode only:

Tell the engine when to enter long or short trades, but let the engine’s in-trade stop and exit strats manage the exits,

Signal both entries and exits,

Provide an entry stop along with your entry signal,

Filter other entry signals generated by any of the engine’s entry strats.

Conversion from strategy to study

TradingView strategies are required to backtest using the TradingView backtesting feature, but if you want to generate alerts with your script, whether for automated trading or just to trigger alerts that you will use in discretionary trading, your code has to run as a study since, for the time being, strategies can’t generate alerts. From hereon we will use indicator as a synonym for study.

Unless you want to maintain two code bases, you will need hybrid code that easily flips between strategy and indicator modes, and your code will need to restrict its use of strategy() calls and their arguments if it’s going to be able to run both as an indicator and a strategy using the same trade logic. That’s one of the benefits of using this Engine. Once you will have entered your own strats in the Engine, it will be a matter of commenting/uncommenting only four lines of code to flip between indicator and strategy modes in a matter of seconds.

Additionally, even when running in Indicator mode, the Engine will still provide you with precious numbers on your individual trades and global results, some of which are not available with normal TradingView backtesting.

Post-Exit Analysis for alternate outcomes (PEA)

While typical backtesting shows results of trade outcomes, PEA focuses on what could have happened after the exit. The intention is to help traders get an idea of the opportunity/risk in the bars following the trade in order to evaluate if their exit strategies are too aggressive or conservative.

After a trade is exited, the Engine’s PEA module continues analyzing outcomes for a user-defined quantity of bars. It identifies the maximum opportunity and risk available in that space, and calculates the drawdown required to reach the highest opportunity level post-exit, while recording the number of bars to that point.

Typically, if you can’t find opportunity greater than 1X past your trade using a few different reasonable lengths of PEA, your strategy is doing pretty good at capturing opportunity. Remember that 100% of opportunity is never capturable. If, however, PEA was finding post-trade maximum opportunity of 3 or 4X with average drawdowns of 0.3 to those areas, this could be a clue revealing your system is exiting trades prematurely. To analyze PEA numbers, you can uncomment complete sets of plots in the Plot module to reveal detailed global and individual PEA numbers.

Statistics

The Engine provides stats on your trades that TV backtesting does not provide, such as:

Average Profitability Per Trade (APPT), aka statistical expectancy, a crucial value.

APPT per bar,

Average stop size,

Traded volume .

It also shows you on a trade-by-trade basis, on-going individual trade results and data.

In-trade events

In-trade events can plot reminders and trigger alerts when they occur. The built-in events are:

Price approaching stop,

Possible tops/bottoms,

Large stop movement (for discretionary trading where stop is moved manually),

Large price movements.

Slippage and Fees

Even when running in indicator mode, the Engine allows for slippage and fees to be included in the logic and test results.

Alerts

The alert creation mechanism allows you to configure alerts on any combination of the normal or pyramided entries, exits and in-trade events.

Backtesting results

A few words on the numbers calculated in the Engine. Priority is given to numbers not shown in TV backtesting, as you can readily convert the script to a strategy if you need them.

We have chosen to focus on numbers expressing results relative to X (the trade’s risk) rather than in absolute currency numbers or in other more conventional but less useful ways. For example, most of the individual trade results are not shown in percentages, as this unit of measure is often less meaningful than those expressed in units of risk (X). A trade that closes with a +25% result, for example, is a poor outcome if it was entered with a -50% stop. Expressed in X, this trade’s P&L becomes 0.5, which provides much better insight into the trade’s outcome. A trade that closes with a P&L of +2X has earned twice the risk incurred upon entry, which would represent a pre-trade risk:reward ratio of 2.

The way to go about it when you think in X’s and that you adopt the sound risk management policy to risk a fixed percentage of your account on each trade is to equate a currency value to a unit of X. E.g. your account is 10K USD and you decide you will risk a maximum of 1% of it on each trade. That means your unit of X for each trade is worth 100 USD. If your APPT is 2X, this means every time you risk 100 USD in a trade, you can expect to make, on average, 200 USD.

By presenting results this way, we hope that the Engine’s statistics will appeal to those cognisant of sound risk management strategies, while gently leading traders who aren’t, towards them.

We trade to turn in tangible profits of course, so at some point currency must come into play. Accordingly, some values such as equity, P&L, slippage and fees are expressed in currency.

Many of the usual numbers shown in TV backtests are nonetheless available, but they have been commented out in the Engine’s Plot module.

Position sizing and risk management

All good system designers understand that optimal risk management is at the very heart of all winning strategies. The risk in a trade is defined by the fraction of current equity represented by the amplitude of the stop, so in order to manage risk optimally on each trade, position size should adjust to the stop’s amplitude. Systems that enter trades with a fixed stop amplitude can get away with calculating position size as a fixed percentage of current equity. In the context of a test run where equity varies, what represents a fixed amount of risk translates into different currency values.

Dynamically adjusting position size throughout a system’s life is optimal in many ways. First, as position sizing will vary with current equity, it reproduces a behavioral pattern common to experienced traders, who will dial down risk when confronted to poor performance and increase it when performance improves. Second, limiting risk confers more predictability to statistical test results. Third, position sizing isn’t just about managing risk, it’s also about maximizing opportunity. By using the maximum leverage (no reference to trading on margin here) into the trade that your risk management strategy allows, a dynamic position size allows you to capture maximal opportunity.

To calculate position sizes using the fixed risk method, we use the following formula: Position = Account * MaxRisk% / Stop% [, which calculates a position size taking into account the trade’s entry stop so that if the trade is stopped out, 100 USD will be lost. For someone who manages risk this way, common instructions to invest a certain percentage of your account in a position are simply worthless, as they do not take into account the risk incurred in the trade.

The Engine lets you select either the fixed risk or fixed percentage of equity position sizing methods. The closest thing to dynamic position sizing that can currently be done with alerts is to use a bot that allows syntax to specify position size as a percentage of equity which, while being dynamic in the sense that it will adapt to current equity when the trade is entered, does not allow us to modulate position size using the stop’s amplitude. Changes to alerts are on the way which should solve this problem.

In order for you to simulate performance with the constraint of fixed position sizing, the Engine also offers a third, less preferable option, where position size is defined as a fixed percentage of initial capital so that it is constant throughout the test and will thus represent a varying proportion of current equity.

Let’s recap. The three position sizing methods the Engine offers are:

1. By specifying the maximum percentage of risk to incur on your remaining equity, so the Engine will dynamically adjust position size for each trade so that, combining the stop’s amplitude with position size will yield a fixed percentage of risk incurred on current equity,

2. By specifying a fixed percentage of remaining equity. Note that unless your system has a fixed stop at entry, this method will not provide maximal risk control, as risk will vary with the amplitude of the stop for every trade. This method, as the first, does however have the advantage of automatically adjusting position size to equity. It is the Engine’s default method because it has an equivalent in TV backtesting, so when flipping between indicator and strategy mode, test results will more or less correspond.

3. By specifying a fixed percentage of the Initial Capital. While this is the least preferable method, it nonetheless reflects the reality confronted by most system designers on TradingView today. In this case, risk varies both because the fixed position size in initial capital currency represents a varying percentage of remaining equity, and because the trade’s stop amplitude may vary, adding another variability vector to risk.

Note that the Engine cannot display equity results for strategies entering trades for a fixed amount of shares/contracts at a variable price.

SETTINGS/INPUTS

Because the initial text first published with a script cannot be edited later and because there are just too many options, the Engine’s Inputs will not be covered in minute detail, as they will most certainly evolve. We will go over them with broad strokes; you should be able to figure the rest out. If you have questions, just ask them here or in the PineCoders Telegram group.

Display

The display header’s checkbox does nothing.

For the moment, only one exit strategy uses a take profit level, so only that one will show information when checking “Show Take Profit Level”.

Entries

You can activate two simultaneous entry strats, each selected from the same set of strats contained in the Engine. If you select two and they fire simultaneously, the main strat’s signal will be used.

The random strat in each list uses a different seed, so you will get different results from each.

The “Filter transitions” and “Filter states” strats delegate signal generation to the selected filter(s). “Filter transitions” signals will only fire when the filter transitions into bull/bear state, so after a trade is stopped out, the next entry may take some time to trigger if the filter’s state does not change quickly. When you choose “Filter states”, then a new trade will be entered immediately after an exit in the direction the filter allows.

If you select “External Indicator”, your indicator will need to generate a +2/-2 (or a positive/negative stop value) to enter a long/short position, providing the selected filters allow for it. If you wish to use the Engine’s capacity to also derive the entry stop level from your indicator’s signal, then you must explicitly choose this option in the Entry Stops section.

Filters

You can activate as many filters as you wish; they are additive. The “Maximum stop allowed on entry” is an important component of proper risk management. If your system has an average 3% stop size and you need to trade using fixed position sizes because of alert/execution bot limitations, you must use this filter because if your system was to enter a trade with a 15% stop, that trade would incur 5 times the normal risk, and its result would account for an abnormally high proportion in your system’s performance.

Remember that any filter can also be used as an entry signal, either when it changes states, or whenever no trade is active and the filter is in a bull or bear mode.

Entry Stops

An entry stop must be selected in the Engine, as it requires a stop level before the in-trade stop is calculated. Until the selected in-trade stop strat generates a stop that comes closer to price than the entry stop (or respects another one of the in-trade stops kick in strats), the entry stop level is used.

It is here that you must select “External Indicator” if your indicator supplies a +price/-price value to be used as the entry stop. A +price is expected for a long entry and a -price value will enter a short with a stop at price. Note that the price is the absolute price, not an offset to the current price level.

In-Trade Stops

The Engine comes with many built-in in-trade stop strats. Note that some of them share the “Length” and “Multiple” field, so when you swap between them, be sure that the length and multiple in use correspond to what you want for that stop strat. Suggested defaults appear with the name of each strat in the dropdown.

In addition to the strat you wish to use, you must also determine when it kicks in to replace the initial entry’s stop, which is determined using different strats. For strats where you can define a positive or negative multiple of X, percentage or fixed value for a kick-in strat, a positive value is above the trade’s entry fill and a negative one below. A value of zero represents breakeven.

Pyramiding

What you specify in this section are the rules that allow pyramiding to happen. By themselves, these rules will not generate pyramiding entries. For those to happen, entry signals must be issued by one of the active entry strats, and conform to the pyramiding rules which act as a filter for them. The “Filter must allow entry” selection must be chosen if you want the usual system’s filters to act as additional filtering criteria for your pyramided entries.

Hard Exits

You can choose from a variety of hard exit strats. Hard exits are exit strategies which signal trade exits on specific events, as opposed to price breaching a stop level in In-Trade Stops strategies. They are self-explanatory. The last one labelled When Take Profit Level (multiple of X) is reached is the only one that uses a level, but contrary to stops, it is above price and while it is relative because it is expressed as a multiple of X, it does not move during the trade. This is the level called Take Profit that is show when the “Show Take Profit Level” checkbox is checked in the Display section.

While stops focus on managing risk, hard exit strategies try to put the emphasis on capturing opportunity.

Slippage

You can define it as a percentage or a fixed value, with different settings for entries and exits. The entry and exit markers on the chart show the impact of slippage on the entry price (the fill).

Fees

Fees, whether expressed as a percentage of position size in and out of the trade or as a fixed value per in and out, are in the same units of currency as the capital defined in the Position Sizing section. Fees being deducted from your Capital, they do not have an impact on the chart marker positions.