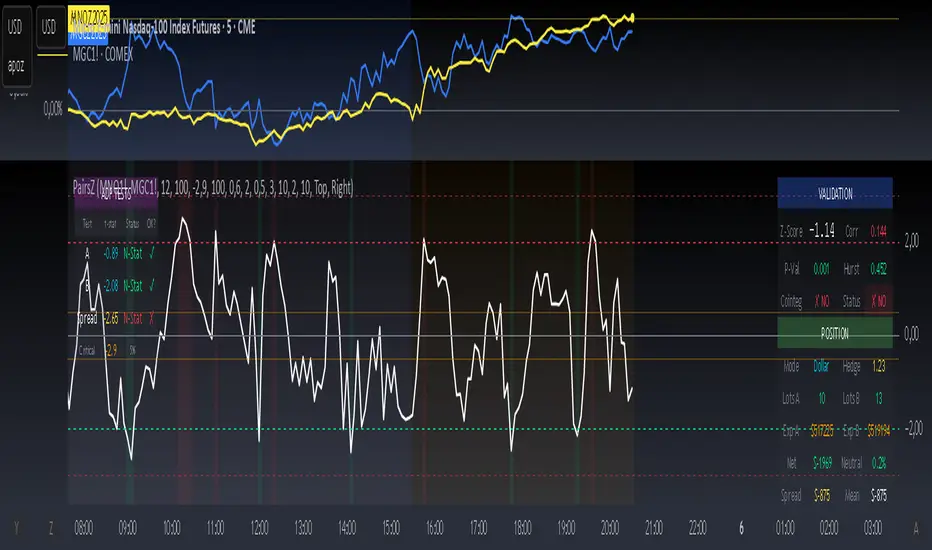

Spread Trading Z-ScoreIndicator: Z-Score Spread Indicator

Description

The "Z-Score Spread Indicator" is a powerful tool for traders employing mean-reversion strategies on the spread between two financial assets (e.g., futures contracts like MNQ and MES). This indicator calculates and plots the Z-score of the price spread, indicating how far the current spread deviates from its historical mean. It features customizable entry and exit thresholds with adjustable offsets, along with an estimated p-value displayed in a table to assess statistical significance.

Key Features

Asset Selection: Allows users to select two asset symbols (e.g., CME_MINI:MNQ1! and CME_MINI:MES1!) via customizable inputs.

Z-Score Calculation: Computes the Z-score based on the spread’s simple moving average and standard deviation over a user-defined lookback period.

Customizable Thresholds with Offset: Offers adjustable base entry and exit thresholds, with an optional offset to fine-tune trading levels, plotted as horizontal lines.

P-Value Estimation: Provides an approximate p-value to evaluate the statistical significance of the Z-score, displayed in a table anchored to the top-left corner.

Visual Representation: Plots the Z-score with a zero line and threshold lines for intuitive interpretation.

Adjustable Parameters

Asset A Symbol: Symbol for Asset A (default: CME_MINI:MNQ1!).

Asset B Symbol: Symbol for Asset B (default: CME_MINI:MES1!).

Z-Score Lookback: Lookback period for Z-score calculation (default: 40, minimum 2).

Base Entry Threshold: Threshold for entry signals (default: 1.8, adjustable with a step of 0.1).

Base Exit Threshold: Threshold for exit signals (default: 0.5, adjustable with a step of 0.1).

Threshold Offset (+/-): Offset to adjust entry and exit thresholds symmetrically (default: 0.0, range -5.0 to 5.0, step 0.1).

Usage

Add the indicator to your chart via the "Indicators" tab.

Customize the parameters based on your preferred assets and trading strategy (lookback period, thresholds, offset).

Observe the Z-score plot and threshold lines (red for short entry, green for long entry, orange dotted for exits) to identify potential trade setups.

Check the p-value table in the top-left corner to assess the statistical significance of the current Z-score.

Use this data to inform mean-reversion trading decisions, ideally in conjunction with other indicators.

Notes

A Z-score above the entry threshold (positive) or below the negative entry threshold suggests a potential short or long entry, respectively. Exits are signaled when the Z-score crosses the exit thresholds.

The p-value is an approximation based on the normal distribution; a value below 0.05 typically indicates statistical significance, but further validation is recommended.

The indicator uses a simple spread (Asset A - Asset B) without volatility adjustments; consider pairing it with a lots calculator for hedging.

Limitations

The p-value is an approximation and may not reflect advanced statistical tests (e.g., ADF) due to Pine Script constraints.

No automatic trading signals are generated; it provides data for manual analysis.

Author

Developed by grogusama, October 15, 2025, 07:29 PM CEST.

Regressions

VBE Pro - Advanced Volatility Bands with Zero Lag & PredictionVBE Pro: Zero-Lag Predictive Bands

A next-gen volatility envelope that blends zero-lag smoothing with forward-looking volatility models (EWMA/GARCH/HAR/ML) to keep bands tight in calm markets, responsive in shocks, and adaptive across regimes.

What it does

Builds volatility from multiple methods (ATR, StDev, Parkinson, Garman-Klass, Rogers-Satchell, Yang-Zhang).

Projects near-term vol with your choice of predictor, then blends it via a weight slider.

Applies zero-lag smoothing (ZLEMA/ZLMA/DEMA/TEMA/HMA/JMA/Ehlers/Kalman/T3) to cut delay without over-shoot.

Auto-adapts band width by regime (high/low/normal) and can expand dynamically with price acceleration.

Optional displacement to align with your execution style.

On-chart

Upper/Lower zero-lag bands with optional fill.

Middle line (ZL-smoothed source).

Regime-tinted background (High/Low).

Displacement marker (if used).

Compact top-right info table: current vs predicted vol, regime, squeeze, multiplier, methods, ZL gain, est. lag reduction.

Signals & Alerts

Break↑ / Break↓ when price crosses the bands.

Vol↑ / Vol↓ expansion/contraction sequences.

“Squeeze” when band width compresses vs its ZL average.

“ZL” marker when significant zero-lag is active.

Prediction divergence ⚠ when projected vol deviates > threshold.

Built-in alertconditions for all of the above.

Quick start

Method: ATR or Hybrid for robustness.

Smoothing: ZLEMA, length 5–8, ZL gain 2–3 (push higher only if you accept more projection).

Bands: Multiplier 2.0, Adaptive on, Dynamic off to start.

Prediction: EWMA, weight 0.25–0.35. Move to GARCH in mean-reverty tapes; HAR-RV for mixed regimes.

Regime lookback: 50.

Liquidity Index with Advanced Statistical NormalizationLiquidity Index with Advanced Statistical Normalization

An open-source TradingView indicator for analyzing global liquidity cycles using robust statistical methods

Overview

This Pine Script indicator combines multiple macroeconomic data sources to construct a composite liquidity index that tracks global financial conditions. It employs advanced statistical techniques typically found in quantitative finance research, adapted for real-time charting.

Key Features

📊 Multi-Source Data Integration

- Federal Reserve Components: Fed Funds Rate, Reverse Repo (RRP), Treasury General Account (TGA)

- PBOC Components: China M2 Money Stock adjusted by CNY/USD exchange rate

- Volatility Index: MOVE Index (bond market volatility)

🔬 Advanced Statistical Methods

1. Theil-Sen Estimator: Robust trend detection resistant to outliers

2. Triple Normalization:

- Z-score normalization

- MAD (Median Absolute Deviation) normalization

- Quantile normalization via inverse normal CDF

3. Multi-Timeframe Analysis: Short (8-bar) and long (34-bar) windows with blended composite

📈 Signal Processing

- Log-transformation for non-linear relationships

- Smoothing via customizable SMA

- Composite signal averaging across normalization methods

Why This Approach?

Traditional liquidity indicators often suffer from:

- Sensitivity to outliers in economic data

- Assumption of normal distributions

- Single-timeframe bias

This script addresses these issues by:

- Using median-based robust statistics (Theil-Sen, MAD)

- Applying multiple normalization techniques

- Blending short and long-term perspectives

Customization Options

short_length // Short window (default: 8)

long_length // Long window (default: 34)

show_short // Display short composite

show_long // Display long composite

show_blended // Display blended signal

smoothing_length // SMA smoothing period (default: 10)

How to Use

1. Liquidity Expansion (positive values): Risk-on environment, favorable for asset prices

2. Liquidity Contraction (negative values): Risk-off environment, potential market stress

3. Divergences: Compare indicator direction vs. price action for early warnings

Potential Improvements

Community members are encouraged to enhance:

- Additional data sources (ECB balance sheet, BOJ operations, etc.)

- Alternative normalization methods (robust scaling, rank transformation)

- Machine learning integration (LSTM forecasting, regime detection)

- Alert conditions for liquidity inflection points

- Volatility-adjusted weighting schemes

Technical Notes

- Uses request.security() for multi-symbol data fetching

- All calculations handle missing data via nz() functions

- Median-based statistics computed via array operations

- Custom inverse CDF approximation (no external libraries required)

Contributing

This is a foundation for liquidity analysis. Potential extensions:

- LLM Integration: Use language models to parse Fed/PBOC meeting minutes and adjust weights dynamically

- Sentiment Layer: Incorporate crypto funding rates or options skew

- Adaptive Parameters: Auto-tune window lengths based on market regime

- Cross-Asset Validation: Backtest signals against BTC, equities, bonds

---

License: Open source - modify and redistribute freelyDisclaimer: For educational purposes only. Not financial advice.

Bitcoin Power Law Corridor + Z-score

This script visualizes the long-term Bitcoin Power Law Corridor, a conceptual model originally discussed by Harold Christopher Burger, and enhances it with a logarithmic Z-Score framework.

The indicator plots Bitcoin’s long-term regression curve together with estimated resistance and support bands based on power-law relationships between price and time since inception.

The added Z-Score expresses the statistical distance between price and the central regression line, using logarithmic scaling:

Z ≈ 0 → price near its long-term fair-value trajectory.

Z ≈ +2 → price near the lower corridor boundary (historically undervalued region).

Z ≈ −2 → price near the upper corridor boundary (historically overheated region).

This indicator is designed for visual and educational purposes only.

It should not be considered financial advice, a predictive model, or a signal provider.

Users should always combine this tool with other forms of technical, fundamental, and sentiment analysis to confirm confluence before making any decision.

EMA+MACD动态0轴主图动态MACD,EMA55作为当前周期动态0轴使用。EMA13作为小4倍周期动态0轴。当前周期DIF线穿越0轴标记+MACD金死叉标记。

The main chart dynamic MACD and EMA55 are used as the dynamic 0-axis for the current cycle. EMA13 is used as the dynamic 0- axis for the smaller 4x cycle. The current cycle's DIF line has crossed the 0-axis, marked with a "+" sign indicating a golden cross on the MACD.

FVG Zones with Signals█ OVERVIEW

"FVG Zones with Signals" is a technical analysis tool that identifies Fair Value Gaps (FVG) on the chart and draws customizable zones in the form of boxes. It is ideal for traders using price action and market structure strategies, helping to identify potential imbalance zones and trading opportunities based on breakout and exit signals. With flexible size filter settings, box styles, and signal options, the indicator ensures clarity and precision on the chart.

█ CONCEPTS

The indicator is designed to identify potential entry points for trades based on FVG breakouts or retests. For chart clarity, a size filter for FVGs is included, based on a multiplier of the average candle size over a specified period.

Why are FVGs important? FVG zones represent areas of market imbalance, often attracting price back to "fill" the gap. Larger gaps (with a higher size multiplier) have a greater chance of being retested, as they indicate deeper imbalances—leaving more unexecuted orders in those zones, which attracts liquidity. Market makers and institutions often return to these levels to "refresh" liquidity before further moves. However, not every large FVG is retested quickly—in strong trends, smaller imbalances may be ignored, and the location (e.g., near swing highs/lows) is critical for retest probability.

█ FEATURES

- FVG Detection: Identifies bullish and bearish FVGs based on size filters (Candle Size Period and FVG Size Multiplier), with automatic initialization of historical gaps up to 500 candles back.

- Customizable Boxes: Draws FVG boxes with adjustable border colors, background gradients, border styles (solid, dashed, dotted), border widths, and transparency for both the background and the 50% FVG midline.

- Breakout and Exit Signals: Generates "Break" signals (green upward triangle for breakouts above bearish FVG, red downward triangle for breakouts below bullish FVG) and "Exit" signals (circles for exiting the zone), with options to select signal types (Break, Exit, or Both). A break signal causes the box to disappear, leaving a triangle as a trace of the breakout, which may serve as a signal to open a position. Exit signals (circles) may also indicate entry opportunities but require additional confirmation, such as alignment with the main trend.

- Midline: Automatically draws a dashed line at the 50% FVG level with adjustable transparency, aiding in assessing price reactions within the zone.

- Box Limitation: Automatically removes old or inactive FVGs after 500 candles to avoid chart clutter.

- Alerts: Built-in alerts for all signal types, including price and FVG type descriptions.

█ HOW TO USE

Add to Chart: Apply the indicator to your TradingView chart via the Pine Editor or Indicators menu.

Configure Settings:

- FVG Settings: Adjust Candle Size Period (default 20) and FVG Size Multiplier (default 1) to filter out small gaps—higher values generate fewer but more significant FVGs.

- Box Settings: Configure colors and styles for bullish (green) and bearish (red) boxes, including background transparency (default 80) and midline transparency.

- Signal Settings: Select signal types (Break, Exit, or Both) in Signal Type. Breakout signals appear after a candle closes outside the zone, while exit signals appear when exiting an FVG without a full breakout.

- Styling: Customize signal colors (green for buy/up, red for sell/down) and shape sizes.

Interpreting Signals:

- Break Up Signal: A green triangle below the bar indicates a breakout above a bearish FVG, suggesting potential continuation of an uptrend.

- Break Down Signal: A red triangle above the bar indicates a breakout below a bullish FVG, suggesting potential continuation of a downtrend.

- Exit Up/Down Signal: A green/red circle indicates an exit from an FVG without a full breakout, which may signal the end of a correction or preparation for a reversal.

- FVG Zones: If the price returns to an FVG and fills the gap, it may indicate equilibrium; an unfilled gap often leads to a retest.

- Use signals in conjunction with other technical analysis tools for confirmation, such as RSI (to identify overbought/oversold conditions) or MACD (to confirm momentum). Analyze FVGs from higher timeframes—these zones act as stronger imbalance levels and carry greater structural significance.

Exit signals (retests without breakouts) tend to be most effective when traded in line with the current trend.

█ APPLICATIONS

- Price Action Trading: Use FVG zones as dynamic support and resistance levels. In an uptrend, look for buying opportunities in bullish FVGs, where price often tests the gap before continuing. Combining with RSI, MACD, or Fibonacci levels enhances the significance of zones.

- Breakout Strategies: Trade based on breakout signals from FVGs. A buy signal after breaking a bearish FVG may indicate a strong upward impulse, especially when supported by a rising MACD or RSI exiting oversold conditions.

Larger FVG gaps (higher multiplier) have a greater chance of retest, as they indicate deeper imbalances.

█ NOTES

- Test the indicator across different timeframes and markets (stocks, forex, crypto) to optimize size filters for your trading style.

- The indicator initializes historical FVGs up to 500 candles back, which may slow loading on longer charts.

- For best results, use on high-liquidity markets where FVGs are more frequently retested.

- In consolidation zones, the indicator may generate more false signals, so additional confirmation is recommended.

Machine Learning Price Predictor: Ridge AR [Bitwardex]🔹Machine Learning Price Predictor: Ridge AR is a research-oriented indicator demonstrating the use of Regularized AutoRegression (Ridge AR) for short-term price forecasting.

The model combines autoregressive structure with Ridge regularization , providing stability under noisy or volatile market conditions.

The latest version introduces Bull and Bear signals , visually representing the current momentum phase and model direction directly on the chart.

Unlike traditional linear regression, Ridge AR minimizes overfitting, stabilizes coefficient dynamics, and enhances predictive consistency in correlated datasets.

The script plots:

Fit Line — in-sample fitted data;

Forecast Line — out-of-sample projection;

Trend Segments — color-coded bullish/bearish sections;

Bull/Bear Labels 🐂🐻 — dynamic visual signals showing directional bias.

Designed for researchers, students, and developers, this tool helps explore regularized time-series forecasting in Pine Script™.

🧩 Ridge AR Settings

Training Window — number of bars used for model training;

Forecast Horizon — forecast length (bars ahead);

AR Order — number of lags used as features;

Ridge Strength (λ) — regularization coefficient;

Damping Factor — exponential trend decay rate;

Trend Length — period for trend/volatility estimation;

Momentum Weight — strength of the recent move;

Mean Reversion — pullback intensity toward the mean.

🧮 Data Processing

Prefilter:

None — raw close price;

EMA — exponential smoothing;

SuperSmoother — Ehlers filter for noise reduction.

EMA Length, SuperSmoother Length — smoothing parameters.

🖥️ Display Settings

Update Mode:

Lock — static model;

Update Once Reached — rebuild after forecast horizon;

Continuous — update every bar.

Forecast Color — projection line color;

Bullish/Bearish Colors — colors for trend segments.

🐂🐻 Bull/Bear Signal System

The Bull/Bear Signal System adds directional visual cues to highlight local momentum shifts and model-based trend confirmation.

Bull (🐂) — appears when upward momentum is confirmed (momentum > 0) .

Displayed below the bar, colored with Bullish Color.

Bear (🐻) — appears when downward momentum is dominant (momentum < 0) .

Displayed above the bar, colored with Bearish Color.

Signals are generated during model recalculations or when the directional bias changes in Continuous mode.

These visual markers are analytical aids , not trading triggers.

🧠 Core Algorithmic Components

Regularized AutoRegression (Ridge AR):

Solves: (X′X+λI)−1X′y

to derive stable regression coefficients.

Matrix and Pseudoinverse Operations — implemented natively in Pine Script™.

Prefiltering (EMA / Ehlers SuperSmoother) — stabilizes noisy data.

Forecast Dynamics — integrates damping, momentum, and mean reversion.

Trend Visualization — color-coded bullish/bearish line segments.

Bull/Bear Signal Engine — visualizes real-time impulse direction.

📊 Applications

Academic and educational purposes;

Demonstration of Ridge Regression and AR models;

Analysis of bull/bear market phase transitions;

Visualization of time-series dependencies.

⚠️ Disclaimer

This script is provided for educational and research purposes only.

It does not provide trading or investment advice.

The author assumes no liability for financial losses resulting from its use.

Use responsibly and at your own risk.

LSVR - Liquidity Sweep & Volume ReversalLSVR condenses a pro workflow into one visual overlay: Higher-Timeframe (HTF) Trend → Liquidity Sweep & Reclaim → Volume Confirmation. A signal only prints when all three gates align at bar close, and the chart shows everything you need—trend context, the sweep “trap” candle, and a projected Entry/SL/TP based on your chosen R multiple.

How it works

HTF Trend Filter: Projects a smoothed KAMA/EMA from a higher timeframe to the chart using a safe, lookahead-off request. Long signals are considered only above the HTF line; shorts only below.

Liquidity Sweep & Reclaim: Finds confirmed swing highs/lows, then detects an ATR-scaled overshoot through that swing followed by a reclaim (close back inside a configurable % of the bar range).

Volume Confirmation: Requires either a volume spike over Volume SMA × multiplier or optional OBV divergence. No participation = no signal.

Score: Each setup is scored: trend (0/1) + overshoot strength (0..1.5) + conviction (0/1). Signals fire only when the score ≥ Min Signal Score.

What you see

HTF Ribbon (subtle green/red backdrop) for bias.

Sweep Box on the signal candle (green = long, red = short).

Signal markers (“L” / “S”) with a small score label.

Projected lines that persist until the next signal: Entry (close), Stop (beyond swept swing), Target (R multiple).

Heatmap that intensifies when the score crosses your threshold.

Dashboard (top-right): HTF direction, Volume×SMA, current Score, gate pass status.

Tooltip on the last bar with quick stats.

Quick start

Apply to any liquid symbol and set HTF to ~3–6× your chart timeframe (e.g., 15m chart → 1H–4H).

Trade with the HTF trend: take L signals above the HTF line and S signals below it.

Entry = signal bar close, SL = beyond the swept swing, TP = your Projected Take-Profit (R).

Tighten or loosen selectivity with Min Signal Score, Reclaim %, Overshoot (ATR×), and Cooldown.

Recommended presets

Choppy/crypto 15m: minScore 1.25, reclaimPct 0.60–0.65, overshootATR 1.0–1.2, useOBVDiv=false, cooldown 8.

FX 5m / session trend: minScore 1.0–1.1, reclaimPct 0.50–0.55, overshootATR 0.8–1.0, useOBVDiv=true, cooldown 5.

Indices 1m (RTH): minScore 1.2, reclaimPct 0.55–0.60, useOBVDiv=false, cooldown 10.

Non-repainting by design

HTF values use lookahead_off with realtime offset.

Swings are confirmed pivots (no “forming” pivots).

Signals print at bar close only.

Notes

OBV divergence can add sensitivity on liquid markets; keep it off for stricter filtering.

Use Cooldown to avoid clustered sweeps.

This is an overlay/analysis tool, not financial advice. Test settings in Replay/Paper Trading before using live.

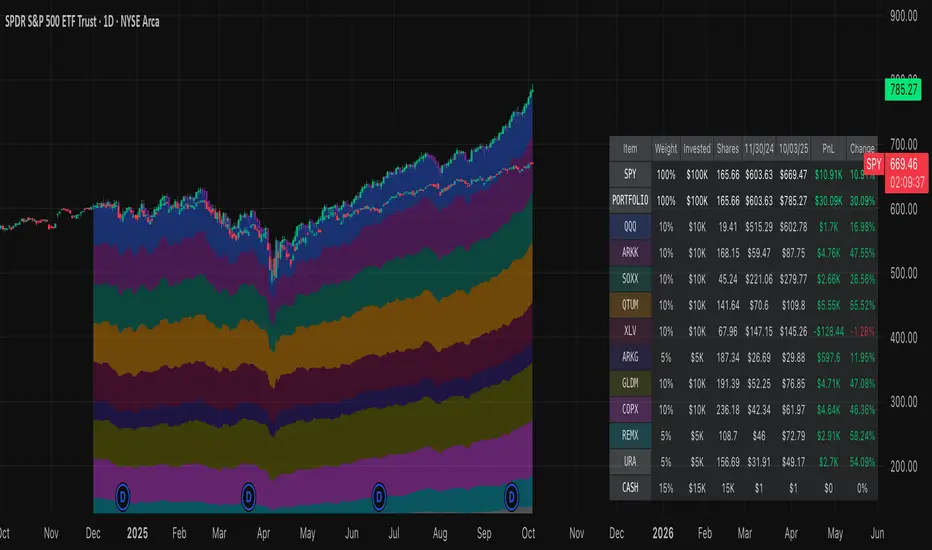

Normalized Portfolio TrackerThis script lets you create, visualize, and track a custom portfolio of up to 15 assets directly on TradingView.

It calculates a synthetic "portfolio index" by combining multiple tickers with user-defined weights, automatically normalizing them so the total allocation always equals 100%.

All assets are scaled to a common starting point, allowing you to compare your portfolio’s performance versus any benchmark like SPY, QQQ, or BTC.

🚀 Goal

This script helps traders and investors:

• Understand the combined performance of their portfolio.

• Normalize diverse assets into a single synthetic chart .

• Make portfolio-level insights without relying on external spreadsheets.

🎯 Use Cases

• Backtest your portfolio allocations directly on the chart.

• Compare your portfolio vs. benchmarks like SPY, QQQ, BTC.

• Track thematic baskets (commodities, EV supply chain, regional ETFs).

• Visualize how each component contributes to overall performance.

📊 Features

• Weighted Portfolio Performance : Combines selected assets into a synthetic value series.

• Base Price Alignment : Each asset is normalized to its starting price at the chosen date.

• Dynamic Portfolio Table : Displays symbols, normalized weights (%), equivalent shares (based on each asset’s start price, sums to 100 shares), and a total row that always sums to 100%.

• Multi-Asset Support : Works with stocks, ETFs, indices, crypto, or any TradingView-compatible symbol.

⚙️ Configuration

Flexible Portfolio Setup

• Add up to 15 assets with custom weight inputs.

• You can enter any arbitrary numbers (e.g. 30, 15, 55).

• The script automatically normalizes all weights so the total allocation always equals 100%.

Start Date Selection

• Choose any custom start date to normalize all assets.

• The portfolio value is then scaled relative to the main chart symbol, so you can directly compare portfolio performance against benchmarks like SPY or QQQ.

Chart Styles

• Candlestick chart

• Heikin Ashi chart

• Line chart

Custom Display

• Adjustable colors and line widths

• Optionally display asset list, normalized weights, and equivalent shares

⚙️ How It Works

• Fetch OHLC data for each asset.

• Normalizes weights internally so totals = 100%.

• Stores each asset’s base price at the selected start date.

• Calculates equivalent “shares” for each allocation.

• Builds a synthetic portfolio value series by summing weighted contributions.

• Renders as Candlestick, Heikin Ashi, or Line chart.

• Adds a portfolio info table for clarity.

⚠️ Notes

• This script is for visualization only . It does not place trades or auto-rebalance.

• Weight inputs are automatically normalized, so you don’t need to enter exact percentages.

Regression Channel (ShareScope-style, parallel)What it does

Replicates ShareScope’s Trend of displayed data look: a single straight linear-regression line (dashed) across a chosen window with parallel, constant-width bands above and below, plus optional shading.

Use it to see the overall trend gradient for a period and a statistically sized channel based on the fit’s residual error.

How it works (math, short)

Computes an OLS regression once over the analysis window.

Residual standard error s is derived from SSE and degrees of freedom (n−2).

Band half-width is constant across the window:

Mean CI (narrower): half = z * s / √n

Prediction (wider): half = z * s * √(1 + 1/n)

Three straight, parallel lines are drawn from the regression endpoints; midline is dashed.

This is intentionally not a tapered CI (which widens at the ends). It matches the visual behaviour of ShareScope’s shaded trend line channel.

Inputs

Source – Price series (Close, High, Low, HL2, etc.).

Use last N bars / N (bars) – Rolling window length.

From / To (date mode) – Alternative fixed date window.

Confidence (%) – 90 / 95 / 99 / Custom (uses z≈t).

Custom Z (t) – Override the quantile if desired.

Prediction bands – Use wider prediction envelope instead of mean CI.

Shade region + colors / opacity / line width.

Usage

To mimic ShareScope exactly, pick the same date span (use date mode) and set Confidence 99%.

Choose Prediction OFF for a tighter “confidence” look; ON for a wider, more permissive channel.

If ShareScope used High as source, set Source = High here as well.

Notes & limitations

TradingView does not expose the visible viewport to Pine. The script cannot auto-read “displayed data.” Use last N bars or date range.

Bands are parallel by design. Prices may close outside; the channel does not bend.

Window capped at 5,000 bars for performance. No alerts are emitted.

Differences vs TV’s native tools

Linear Regression (drawing) – manual object; no statistical sizing or shading.

Linear Regression Channel (indicator) – uses price standard deviations around the regression; width is a user stdev multiple.

This script – uses residual error of the OLS fit and a z/t quantile to size a statistically meaningful parallel channel.

Changelog

r3.1 – Guard fix (no return at top level), minor refactor, stable line updates.

r3 – Switched to single-fit OLS with parallel constant-width bands (ShareScope look).

(Earlier experimental builds r1–r2.2 implemented rolling/tapered CI; superseded.)

Disclaimer: Educational use only. Not investment advice.

Linear Regression by Uttamwith Buy Sell Signal with regression channel

with Buy Sell Signal with regression channel

with Buy Sell Signal with regression channel

with Buy Sell Signal with regression channel

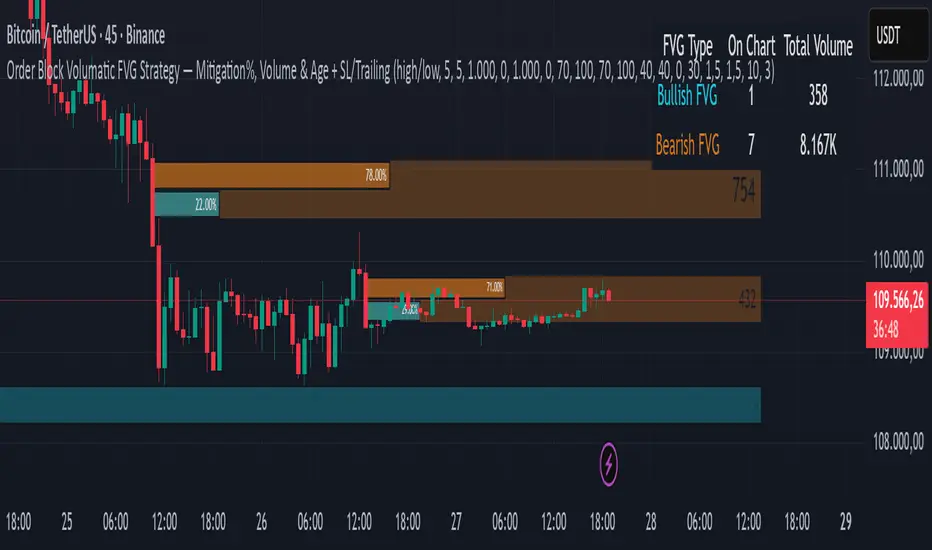

Order Block Volumatic FVG StrategyInspired by: Volumatic Fair Value Gaps —

License: CC BY-NC-SA 4.0 (Creative Commons Attribution–NonCommercial–ShareAlike).

This script is a non-commercial derivative work that credits the original author and keeps the same license.

What this strategy does

This turns BigBeluga’s visual FVG concept into an entry/exit strategy. It scans bullish and bearish FVG boxes, measures how deep price has mitigated into a box (as a percentage), and opens a long/short when your mitigation threshold and filters are satisfied. Risk is managed with a fixed Stop Loss % and a Trailing Stop that activates only after a user-defined profit trigger.

Additions vs. the original indicator

✅ Strategy entries based on % mitigation into FVGs (long/short).

✅ Lower-TF volume split using upticks/downticks; fallback if LTF data is missing (distributes prior bar volume by close’s position in its H–L range) to avoid NaN/0.

✅ Per-FVG total volume filter (min/max) so you can skip weak boxes.

✅ Age filter (min bars since the FVG was created) to avoid fresh/immature boxes.

✅ Bull% / Bear% share filter (the 46%/53% numbers you see inside each FVG).

✅ Optional candle confirmation and cooldown between trades.

✅ Risk management: fixed SL % + Trailing Stop with a profit trigger (doesn’t trail until your trigger is reached).

✅ Pine v6 safety: no unsupported args, no indexof/clamp/when, reverse-index deletes, guards against zero/NaN.

How a trade is decided (logic overview)

Detect FVGs (same rules as the original visual logic).

For each FVG currently intersected by the bar, compute:

Mitigation % (how deep price has entered the box).

Bull%/Bear% split (internal volume share).

Total volume (printed on the box) from LTF aggregation or fallback.

Age (bars) since the box was created.

Apply your filters:

Mitigation ≥ Long/Short threshold.

Volume between your min and max (if enabled).

Age ≥ min bars (if enabled).

Bull% / Bear% within your limits (if enabled).

(Optional) the current candle must be in trade direction (confirm).

If multiple FVGs qualify on the same bar, the strategy uses the most recent one.

Enter long/short (no pyramiding).

Exit with:

Fixed Stop Loss %, and

Trailing Stop that only starts after price reaches your profit trigger %.

Input settings (quick guide)

Mitigation source: close or high/low. Use high/low for intrabar touches; close is stricter.

Mitigation % thresholds: minimal mitigation for Long and Short.

TOTAL Volume filter: skip FVGs with too little/too much total volume (per box).

Bull/Bear share filter: require, e.g., Long only if Bull% ≥ 50; avoid Short when Bull% is high (Short Bull% max).

Age filter (bars): e.g., ≥ 20–30 bars to avoid fresh boxes.

Confirm candle: require candle direction to match the trade.

Cooldown (bars): minimum bars between entries.

Risk:

Stop Loss % (fixed from entry price).

Activate trailing at +% profit (the trigger).

Trailing distance % (the trailing gap once active).

Lower-TF aggregation:

Auto: TF/Divisor → picks 1/3/5m automatically.

Fixed: choose 1/3/5/15m explicitly.

If LTF can’t be fetched, fallback allocates prior bar’s volume by its close position in the bar’s H–L.

Suggested starting presets (you should optimize per market)

Mitigation: 60–80% for both Long/Short.

Bull/Bear share:

Long: Bull% ≥ 50–70, Bear% ≤ 100.

Short: Bull% ≤ 60 (avoid shorting into strong support), Bear% ≥ 0–70 as you prefer.

Age: ≥ 20–30 bars.

Volume: pick a min that filters noise for your symbol/timeframe.

Risk: SL 4–6%, trailing trigger 1–2%, distance 1–2% (crypto example).

Set slippage/fees in Strategy Properties.

Notes, limitations & best practices

Data differences: The LTF split uses request.security_lower_tf. If the exchange/data feed has sparse LTF data, the fallback kicks in (it’s deliberate to avoid NaNs but is a heuristic).

Real-time vs backtest: The current bar can update until close; results on historical bars use closed data. Use “Bar Replay” to understand intrabar effects.

No pyramiding: Only one position at a time. Modify pyramiding in the header if you need scaling.

Assets: For spot/crypto, TradingView “volume” is exchange volume; in some markets it may be tick volume—interpret filters accordingly.

Risk disclosure: Past performance ≠ future results. Use appropriate position sizing and risk controls; this is not financial advice.

Credits

Visual FVG concept and original implementation: BigBeluga.

This derivative strategy adds entry/exit logic, volume/age/share filters, robust LTF handling, and risk management while preserving the original spirit.

License remains CC BY-NC-SA 4.0 (non-commercial, attribution required, share-alike).

EMA Separation (LFZ Scalps) v6 — Early TriggerPlots the percentage distance between a fast and a slow EMA (default 9 & 21) to gauge trend strength and filter out choppy London Flow Zone breakouts.

• Gray – EMAs nearly flat (low momentum, avoid trades)

• Orange – early trend building

• Green/Red – strong directional momentum

Useful for day-traders: wait for the gap to widen beyond your chosen threshold (e.g., 0.25 %) before entering a breakout. Adjustable EMA lengths and alert when the separation exceeds your “strong trend” level.

Nadaraya-Watson Multi-TF DashboardThis script is a Multi-Timeframe Flip State Dashboard based on Nadaraya-Watson: Rational Quadratic Kernel (Non-Repainting) indicator. It visualizes trend "flip" states across up to 8 custom timeframes using a consistent, non-repainting methodology. Built on 1-minute data, each timeframe row in the table updates only after its bar fully closes, ensuring accuracy and eliminating repainting issues.

Key features:

✅ Based on the Nadaraya-Watson Rational Quadratic Kernel, used to estimate trend direction

🧠 Each timeframe uses the same base 1-minute data for consistency across resolutions

🔄 Flip state detection is defined by slope reversals in the kernel regression

🧱 Fully supports non-repainting, close-confirmed states using lookahead=off

🧮 Configurable lookback window, kernel weighting, lag, and timeframes

🎨 Visual dashboard plots each TF’s state as a colored cell (green for bullish, red for bearish)

🛠️ Includes inline plots and debug traces to help visualize regression and flip logic

This dashboard is ideal for traders who want a compact visual overview of confirmed trend shifts across multiple timeframes, all using a mathematically grounded, TF-consistent model.

Alerta de toque de la 200-Week SMACuando el precio toca la MMS de 200 semanas es una posible compra.

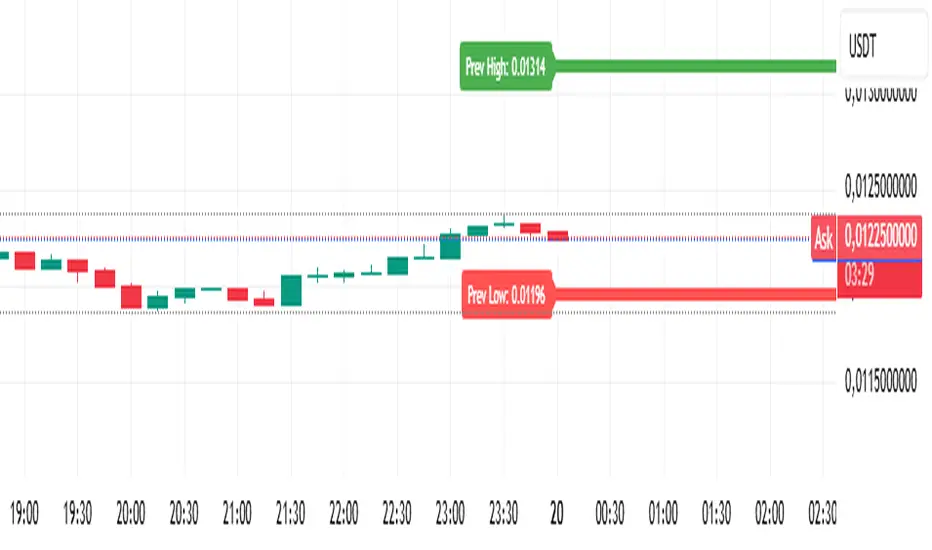

Analitica Trading — Previous Day SR (2 lines + labels) 2.0📊 Analitica Trading — Previous Day SR (Support & Resistance)

This indicator displays the previous day’s key levels on any timeframe:

Prev High → Green horizontal line with label.

Prev Low → Red horizontal line with label.

🔹 Stable across timeframes: The levels are calculated from the daily candles and remain fixed, no matter if you switch to 1D, 1H, or 5m.

🔹 Simple & clean: Exactly two lines only (no duplicates).

🔹 Price labels included: Each line has a clear tag showing the exact level.

🔹 Dynamic update: Lines refresh automatically at the start of each new daily session.

🔹 Alerts: Optional alerts trigger when the price breaks above the Prev High or below the Prev Low.

💡 Ideal for support/resistance trading, breakouts, and Smart Money Concepts (SMC) strategies.

Omega ATR Indicator📖 Introduction

The Ω ATR Indicator was created to provide a more complete and professional framework for volatility analysis than the classic Average True Range (ATR).

While the traditional ATR is a useful tool, it has limitations: it delivers a simple rolling average of volatility, but it does not adapt to market regimes, it does not highlight extreme events, and it often leaves the trader with incomplete information about risk.

The Ω ATR takes the same foundation and elevates it into a multi-dimensional volatility dashboard, adding statistical layers, adaptive calculations, and clear visual references that allow traders to interpret volatility in a way that is immediately actionable.

🔎 What makes it different from a standard ATR?

This indicator introduces several features beyond the classic formula:

True Range Core – plots the raw True Range (TR) for each bar, providing a direct, bar-by-bar view of volatility impulses.

Standard & Adjusted ATR – includes both the conventional ATR (smoothed average) and an Adjusted ATR that automatically corrects for extreme conditions by incorporating percentile rescaling.

Percentile Volatility Levels – dynamically calculated extreme thresholds (99.8%, 75%, 50%, 25%), plotted as dotted levels across the chart. These act as reference lines for “normal” vs. “abnormal” volatility, useful for spotting unusual price expansions or contractions.

Linear Regression Volatility Trend – overlays a regression line of volatility, showing whether the market is moving toward expansion (rising vol), contraction (falling vol), or stability.

Monetary Value Translation – the indicator converts volatility into points, ticks, and dollar values (based on the instrument’s point value). This allows futures traders and high-value instruments users to immediately see how much volatility is “worth” in cash terms.

Interactive Table Display – a real-time statistics table is displayed directly on the chart, showing:

SMA of ATR in $ and points

Percentile-based volatility range (VAR) in $ and points

Tick equivalences, for quick position sizing

⚡ How traders can use it

The Ω ATR Indicator is designed to be versatile, fitting both discretionary traders and systematic strategy developers.

Risk Management: ATR-based stop losses and position sizing are significantly improved by using the adjusted ATR and percentile thresholds. Traders can size their positions according to volatility regimes, not just raw averages.

Breakout & Exhaustion Detection: When TR or ATR values spike above the 99.8% or 95% percentile levels, this often corresponds to breakout conditions or volatility exhaustion — useful for breakout strategies, mean-reversion setups, and volatility fades.

Market Regime Identification: The regression line helps distinguish if volatility is rising (trending environment, larger swings expected) or compressing (range-bound environment, lower risk opportunities).

Multi-Asset Flexibility: Works equally well on equities, futures, crypto, and FX. Its point/tick/dollar conversion makes it especially powerful for futures traders who need to quantify risk precisely.

Scalping to Swing Trading: On lower timeframes, it acts as a micro-volatility detector; on higher timeframes, it functions as a strategic risk gauge for position management.

⚙️ Settings and Customization

Length: The ATR lookback period (default = 34).

Shorter lengths (14–21) for intraday traders who want fast response.

Longer lengths (34–55) for swing/position traders who want smoother readings.

AVG / ADJ AVG: Toggle to display the standard ATR or the adjusted ATR.

Volatility Levels: Enable/disable up to 4 percentile-based levels (1st = 25%, 2nd = 50%, 3rd = 75%, 4th = 99.8%). Recommended: keep 3 levels active for clarity.

Color Controls: All plots and levels are fully customizable to match your chart style.

Table Display: Positioned on the chart (default: middle-right) with key values updated in real time.

🧭 Best Practices for Use

Combine with Trend Tools: Volatility readings are most powerful when combined with trend filters or volume analysis. For example, a breakout with both high volatility and trend confirmation is stronger than either alone.

ATR Stops: Use the Adjusted ATR rather than the standard one when trailing stops in highly volatile instruments like crypto or Nasdaq futures, as it adapts to outlier spikes.

Dollar Risk Translation: Use the dollar-value outputs to predefine maximum acceptable risk per trade (e.g., “I only risk $250 per position”). This bridges volatility to portfolio risk management.

Event Monitoring: Around economic events or earnings, expect volatility spikes above higher percentile levels. The indicator makes these moves instantly visible.

📌 Summary

The Ω ATR Indicator is not just “another ATR.” It is a comprehensive volatility framework that transforms volatility from a simple statistic into an actionable trading signal.

By combining:

the classic ATR,

an adjusted ATR,

percentile extremes,

regression-based volatility trends,

and real-time dollar conversions,

…this tool allows traders to precisely understand, visualize, and act on volatility in ways that a standard ATR simply cannot provide.

Whether you are scalping intraday moves, swing trading equities, or managing futures positions, the Ω ATR equips you with a professional-grade volatility dashboard that clarifies risk, highlights opportunity, and adapts across all markets and timeframes.

👉 Designed and developed by OmegaTools for traders who demand precision, clarity, and adaptability in their volatility analysis.

BTCUSD Dual Thrust (1H)BTCUSD Dual Thrust (1H) — Indicator

Overview

The Dual Thrust is a classic breakout-type strategy designed to capture strong directional moves when markets show imbalance between buyers and sellers. This indicator adapts the method specifically for BTCUSD on the 1-Hour timeframe, showing dynamic Buy/Sell trigger levels and live signals.

Origin

The Dual Thrust system was originally introduced by Michael Vitucci and has been widely used in futures and high-volatility markets. It was designed as a day-trading breakout framework, where daily high/low and close data define the range for the next session’s trade triggers.

How it Works

Each new day, the indicator calculates a “breakout range” using daily price data.

Two trigger levels are projected from the daily open:

Buy Trigger: Open + Range × KUp

Sell Trigger: Open - Range × KDn

Range can be built from either:

Classic Dual Thrust formula: max(High - Close , Close - Low) over a lookback period, or

ATR-based range: for volatility-adaptive signals.

A LONG signal fires when price crosses above the Buy Trigger.

An EXIT signal fires when price crosses below the Sell Trigger.

Buy/Sell lines step forward across each intraday bar until recalculated at the next daily open.

Practical Use

Optimized for BTCUSD 1-Hour charts (crypto’s volatility provides stronger follow-through).

Use the Buy/Sell levels as dynamic breakout lines or as confluence with your own setups.

Alerts are built in, so you can receive notifications when a LONG or EXIT condition triggers.

Designed as an indicator only (not a backtest strategy).

Key Features

✅ Daily Buy/Sell trigger lines auto-calculated and forward-filled

✅ LONG / EXIT labels on signals

✅ Optional ATR mode for volatility regimes

✅ Optional bar coloring for easy visual scanning

✅ Alerts ready for live monitoring

⚡️ Tip: While this indicator highlights breakout opportunities, effectiveness can improve when combined with trend filters (e.g., 200-SMA) or when aligned with higher timeframe supply/demand zones.

APC Companion – Volume Accumulation/DistributionIndicator Description (TradingView – Open Source)

APC Companion – Volume Accumulation/Distribution Filter

(Designed to work standalone or together with the APC Compass)

What this indicator does

The APC Companion measures whether markets are under Accumulation (buying pressure) or Distribution (selling pressure) by combining:

Chaikin A/D slope – volume flow into price moves

On-Balance Volume momentum – confirms trend strength

VWAP spread – price vs. fair value by traded volume

CLV × Volume Z-Score – detects intrabar absorption / selling pressure

VWMA vs. EMA100 – confirms whether weighted volume supports price action

The result is a single Acc/Dist Score (−5 … +5) and a Coherence % showing how many signals agree.

How to interpret

Score ≥ +3 & Coherence ≥ 60% → Accumulation (green) → market supported by buyers

Score ≤ −3 & Coherence ≥ 60% → Distribution (red) → market pressured by sellers

Anything in between = neutral (no strong bias)

Using with APC Compass

Long trades: Only take Compass Long signals when Companion shows Accumulation.

Short trades: Only take Compass Short signals when Companion shows Distribution.

Neutral Companion: Skip or reduce size if there is no confirmation.

This filter greatly reduces false signals and improves trade quality.

Best practice

Swing trading: 4H / 1D charts, lenZ 40–80, lenSlope 14–20

Intraday: 5m–30m charts, lenZ 20–30, lenSlope 10–14

Position sizing: Increase with higher Coherence %, reduce when below 60%

Exits: Reduce or close if Score drops back to neutral or flips opposite

Disclaimer

This script is published open source for educational purposes only.

It is not financial advice. Test thoroughly before using in live trading.

Weekly Fibonacci Pivot Levelsthis indicator in simple ways, draw the weekly fibo zones based on calculations

weekly zones are drawn automatically based on previous week, and are updated once a new week is opened

you can use it the way you like or adapt to your trading strategy

i really use it at extremes and when a divergence is occurring in these zones

Auto Trend Channel with Fibonacci‼️ PLEASE USE WITH LOG CHART

🟠 Overview

This indicator introduces a novel approach to trend channel construction by implementing a touch-based validation system that ensures channels actually function as dynamic support and resistance levels. Unlike traditional linear regression channels that simply fit a mathematical line through price data, this indicator validates channel effectiveness by measuring how frequently price interacts with the boundaries, creating channels that traders can reliably use for entry and exit decisions.

🟠 Core Idea: Touch-Based Channel Validation

The fundamental problem with standard regression channels is that they often create mathematically correct but practically useless boundaries that price rarely respects. This indicator solves this by introducing a dual-scoring optimization system that evaluates each potential channel based on two critical factors:

Trend Correlation (70% weight): Measures how well prices follow the overall trend direction using Pearson correlation coefficient

Boundary Touch Frequency (30% weight): Counts actual instances where price highs touch the upper channel and lows touch the lower channel

This combination ensures the selected channel not only follows the trend but actively serves as support and resistance.

🟠 Trading Applications

Trend Following

Strong Uptrend: Price consistently bounces off lower channel and Fibonacci levels

Strong Downtrend: Price repeatedly fails at upper channel and Fibonacci resistance

Trend Weakening: Price fails to reach channel extremes or breaks through

Entry Strategies

Channel Bounce Entries: Enter long when price touches lower channel with confirmation; short at upper channel touches

Fibonacci Retracement Entries: Use 38.2% or 61.8% levels for pullback entries in trending markets

Breakout Entries: Trade breakouts when price closes beyond channels with increased volume

🟠 Customization Parameters

Automatic/Manual Period: Choose between intelligent auto-detection or fixed lookback period

Touch Sensitivity (0.1%-10%): Defines how close price must be to count as a boundary touch

Minimum Touches (1-10): Filter threshold for channel validation

Adaptive Deviation: Toggle between calculated or manual deviation multipliers

Divergences v2.4 [LTB][SPTG]Open-source credit & license

Original author: LonesomeTheBlue.

This fork by: sirpipthegreat — with attribution to the original work.

License: Open-source, published under the MPL-2.0 (same license header in the code).

I am publishing this open-source in accordance with TradingView’s Open-source reuse rules.

What’s new:

- Fixes & stability (addresses “historical offset beyond buffer” errors)

- Capped and validated all historical indexing with guarded lookbacks (e.g., min(…, 200) style limits) to prevent referencing data beyond the buffer on shorter histories/thin symbols.

- Refactored highest/lowest bars scans to obey the cap and avoid cumulative overflows on long sessions.

- Added per-bar counters with safety clamps to ensure it never exceeds available history.

- Ensured HTF switching doesn’t create invalid offsets when the higher timeframe compresses history.

Modernization & user control:

- Pine v6 upgrade and re-organization of logic for clarity/performance.

- More predictable tops/bottoms detection.

What it does:

- Detects regular (trend-reversal) and optional hidden (trend-continuation) divergences between price swing tops/bottoms and the selected oscillator(s).

- Computes candidate pivots with a light HTF alignment to reduce micro-noise; validates divergence when oscillator and price move in opposite directions across those pivots.

- Plots colored lines/labels on price to highlight bearish (regular & hidden) and bullish (regular & hidden) patterns.

How to use:

- Choose the oscillator set you trust (start with RSI + MACD).

- Consider confluence (S/R, volume, trend filters). This tool only identifies conditions