SMA Cross 5/50 with Trend Filter & Risk Management by JuggiDThe basic SMA (5/50) crossover strategy can be enhanced to improve profitability by adding filters and risk management. For example, a long entry is triggered only when the fast SMA (5) crosses above the slow SMA (50) **and** the price is above the SMA (200), ensuring trades align with the major trend. Similarly, a short entry requires the crossover confirmation plus the price staying below the SMA (200). To reduce false signals and protect capital, stop-loss and take-profit levels can be set automatically (e.g., 2% loss, 5% gain), while additional confirmation tools such as volume spikes, RSI above 50, or MACD momentum can be applied to validate stronger signals. This approach helps avoid whipsaws in sideways markets and allows trades to capture larger moves while minimizing downside risk.

Pine Dienstprogramme

Weekly Session BreakThis indicator plots a vertical line at the end of the trading week (Friday) to mark the weekly session break. It is designed to be used on intraday charts (sub-1 hour timeframes).

The line's appearance is fully customizable via the Inputs tab, allowing you to change its color, style (solid, dotted, or dashed), and thickness.

Key Features:

End-of-Week Marker: Accurately draws a vertical line on the last bar of the trading week.

Timeframe Specific: Lines are only visible on intraday charts (1-minute to 59-minute timeframes) to prevent clutter on higher timeframes.

Customizable: Adjust the line's color, style, and thickness from the Inputs menu.

FiniteStateMachine🟩 OVERVIEW

A flexible framework for creating, testing and implementing a Finite State Machine (FSM) in your script. FSMs use rules to control how states change in response to events.

This is the first Finite State Machine library on TradingView and it's quite a different way to think about your script's logic. Advantages of using this vs hardcoding all your logic include:

• Explicit logic : You can see all rules easily side-by-side.

• Validation : Tables show your rules and validation results right on the chart.

• Dual approach : Simple matrix for straightforward transitions; map implementation for concurrent scenarios. You can combine them for complex needs.

• Type safety : Shows how to use enums for robustness while maintaining string compatibility.

• Real-world examples : Includes both conceptual (traffic lights) and practical (trading strategy) demonstrations.

• Priority control : Explicit control over which rules take precedence when multiple conditions are met.

• Wildcard system : Flexible pattern matching for states and events.

The library seems complex, but it's not really. Your conditions, events, and their potential interactions are complex. The FSM makes them all explicit, which is some work. However, like all "good" pain in life, this is front-loaded, and *saves* pain later, in the form of unintended interactions and bugs that are very hard to find and fix.

🟩 SIMPLE FSM (MATRIX-BASED)

The simple FSM uses a matrix to define transition rules with the structure: state > event > state. We look up the current state, check if the event in that row matches, and if it does, output the resulting state.

Each row in the matrix defines one rule, and the first matching row, counting from the top down, is applied.

A limitation of this method is that you can supply only ONE event.

You can design layered rules using widlcards. Use an empty string "" or the special string "ANY" for any state or event wildcard.

The matrix FSM is foruse where you have clear, sequential state transitions triggered by single events. Think traffic lights, or any logic where only one thing can happen at a time.

The demo for this FSM is of traffic lights.

🟩 CONCURRENT FSM (MAP-BASED)

The map FSM uses a more complex structure where each state is a key in the map, and its value is an array of event rules. Each rule maps a named condition to an output (event or next state).

This FSM can handle multiple conditions simultaneously. Rules added first have higher priority.

Adding more rules to existing states combines the entries in the map (if you use the supplied helper function) rather than overwriting them.

This FSM is for more complex scenarios where multiple conditions can be true simultaneously, and you need to control which takes precedence. Like trading strategies, or any system with concurrent conditions.

The demo for this FSM is a trading strategy.

🟩 HOW TO USE

Pine Script libraries contain reusable code for importing into indicators. You do not need to copy any code out of here. Just import the library and call the function you want.

For example, for version 1 of this library, import it like this:

import SimpleCryptoLife/FiniteStateMachine/1

See the EXAMPLE USAGE sections within the library for examples of calling the functions.

For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script User Manual.

🟩 TECHNICAL IMPLEMENTATION

Both FSM implementations support wildcards using blank strings "" or the special string "ANY". Wildcards match in this priority order:

• Exact state + exact event match

• Exact state + empty event (event wildcard)

• Empty state + exact event (state wildcard)

• Empty state + empty event (full wildcard)

When multiple rules match the same state + event combination, the FIRST rule encountered takes priority. In the matrix FSM, this means row order determines priority. In the map FSM, it's the order you add rules to each state.

The library uses user-defined types for the map FSM:

• o_eventRule : Maps a condition name to an output

• o_eventRuleWrapper : Wraps an array of rules (since maps can't contain arrays directly)

Everything uses strings for maximum library compatibility, though the examples show how to use enums for type safety by converting them to strings.

Unlike normal maps where adding a duplicate key overwrites the value, this library's `m_addRuleToEventMap()` method *combines* rules, making it intuitive to build rule sets without breaking them.

🟩 VALIDATION & ERROR HANDLING

The library includes comprehensive validation functions that catch common FSM design errors:

Error detection:

• Empty next states

• Invalid states not in the states array

• Duplicate rules

• Conflicting transitions

• Unreachable states (no entry/exit rules)

Warning detection:

• Redundant wildcards

• Empty states/events (potential unintended wildcards)

• Duplicate conditions within states

You can display validation results in tables on the chart, with tooltips providing detailed explanations. The helper functions to display the tables are exported so you can call them from your own script.

🟩 PRACTICAL EXAMPLES

The library includes four comprehensive demos:

Traffic Light Demo (Simple FSM) : Uses the matrix FSM to cycle through traffic light states (red → red+amber → green → amber → red) with timer events. Includes pseudo-random "break" events and repair logic to demonstrate wildcards and priority handling.

Trading Strategy Demo (Concurrent FSM) : Implements a realistic long-only trading strategy using BOTH FSM types:

• Map FSM converts multiple technical conditions (EMA crosses, gaps, fractals, RSI) into prioritised events

• Matrix FSM handles state transitions (idle → setup → entry → position → exit → re-entry)

• Includes position management, stop losses, and re-entry logic

Error Demonstrations : Both FSM types include error demos with intentionally malformed rules to showcase the validation system's capabilities.

🟩 BRING ON THE FUNCTIONS

f_printFSMMatrix(_mat_rules, _a_states, _tablePosition)

Prints a table of states and rules to the specified position on the chart. Works only with the matrix-based FSM.

Parameters:

_mat_rules (matrix)

_a_states (array)

_tablePosition (simple string)

Returns: The table of states and rules.

method m_loadMatrixRulesFromText(_mat_rules, _rulesText)

Loads rules into a rules matrix from a multiline string where each line is of the form "current state | event | next state" (ignores empty lines and trims whitespace).

This is the most human-readable way to define rules because it's a visually aligned, table-like format.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_rulesText (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_addRuleToMatrix(_mat_rules, _currentState, _event, _nextState)

Adds a single rule to the rules matrix. This can also be quite readble if you use short variable names and careful spacing.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_nextState (string)

Returns: No explicit return. The matrix is modified as a side-effect.

method m_validateRulesMatrix(_mat_rules, _a_states, _showTable, _tablePosition)

Validates a rules matrix and a states array to check that they are well formed. Works only with the matrix-based FSM.

Checks: matrix has exactly 3 columns; no empty next states; all states defined in array; no duplicate states; no duplicate rules; all states have entry/exit rules; no conflicting transitions; no redundant wildcards. To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the rules and states are ready.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_a_states (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the rules and states are valid; `false` if errors or warnings exist.

method m_getStateFromMatrix(_mat_rules, _currentState, _event, _strictInput, _strictTransitions)

Returns the next state based on the current state and event, or `na` if no matching transition is found. Empty (not na) entries are treated as wildcards if `strictInput` is false.

Priority: exact match > event wildcard > state wildcard > full wildcard.

Namespace types: matrix

Parameters:

_mat_rules (matrix)

_currentState (string)

_event (string)

_strictInput (bool)

_strictTransitions (bool)

Returns: The next state or `na`.

method m_addRuleToEventMap(_map_eventRules, _state, _condName, _output)

Adds a single event rule to the event rules map. If the state key already exists, appends the new rule to the existing array (if different). If the state key doesn't exist, creates a new entry.

Namespace types: map

Parameters:

_map_eventRules (map)

_state (string)

_condName (string)

_output (string)

Returns: No explicit return. The map is modified as a side-effect.

method m_addEventRulesToMapFromText(_map_eventRules, _configText)

Loads event rules from a multiline text string into a map structure.

Format: "state | condName > output | condName > output | ..." . Pairs are ordered by priority. You can have multiple rules on the same line for one state.

Supports wildcards: Use an empty string ("") or the special string "ANY" for state or condName to create wildcard rules.

Examples: " | condName > output" (state wildcard), "state | > output" (condition wildcard), " | > output" (full wildcard).

Splits lines by , extracts state as key, creates/appends to array with new o_eventRule(condName, output).

Call once, e.g., on barstate.isfirst for best performance.

Namespace types: map

Parameters:

_map_eventRules (map)

_configText (string)

Returns: No explicit return. The map is modified as a side-effect.

f_printFSMMap(_map_eventRules, _a_states, _tablePosition)

Prints a table of map-based event rules to the specified position on the chart.

Parameters:

_map_eventRules (map)

_a_states (array)

_tablePosition (simple string)

Returns: The table of map-based event rules.

method m_validateEventRulesMap(_map_eventRules, _a_states, _a_validEvents, _showTable, _tablePosition)

Validates an event rules map to check that it's well formed.

Checks: map is not empty; wrappers contain non-empty arrays; no duplicate condition names per state; no empty fields in o_eventRule objects; optionally validates outputs against matrix events.

NOTE: Both "" and "ANY" are treated identically as wildcards for both states and conditions.

To avoid slowing down the script unnecessarily, call this method once (perhaps using `barstate.isfirst`), when the map is ready.

Namespace types: map

Parameters:

_map_eventRules (map)

_a_states (array)

_a_validEvents (array)

_showTable (bool)

_tablePosition (simple string)

Returns: `true` if the event rules map is valid; `false` if errors or warnings exist.

method m_getEventFromConditionsMap(_currentState, _a_activeConditions, _map_eventRules)

Returns a single event or state string based on the current state and active conditions.

Uses a map of event rules where rules are pre-sorted by implicit priority via load order.

Supports wildcards using empty string ("") or "ANY" for flexible rule matching.

Priority: exact match > condition wildcard > state wildcard > full wildcard.

Namespace types: series string, simple string, input string, const string

Parameters:

_currentState (string)

_a_activeConditions (array)

_map_eventRules (map)

Returns: The output string (event or state) for the first matching condition, or na if no match found.

o_eventRule

o_eventRule defines a condition-to-output mapping for the concurrent FSM.

Fields:

condName (series string) : The name of the condition to check.

output (series string) : The output (event or state) when the condition is true.

o_eventRuleWrapper

o_eventRuleWrapper wraps an array of o_eventRule for use as map values (maps cannot contain collections directly).

Fields:

a_rules (array) : Array of o_eventRule objects for a specific state.

Market Order Risk CalculatorObviously the Long/Short Position tool does this, but when you are scalping, 10 - 15 seconds matters. What matters more than that is defined risk, you dont want your losses being scattered, 300 here 145 there, you want consistent risk to have consistent data.

What this does is when you are framing a trade, it provides a hands off tool that tells you exactly how many contracts to enter with, that way if you have bracket orders on, your stop will be exactly where you want it to be without going over your defined risk.

Futures Tick & Point Value [BoredYeti]Futures Tick & Point Value

This utility displays tick size, dollars per tick, and (optionally) a per-point row for the current futures contract.

Features

• Hardcoded $/tick map for common CME/NYMEX/CBOT/COMEX contracts

• Automatic fallback using pointvalue * mintick for any other symbol

• Table settings: adjustable position, text size, customizable colors

• Optional “Per Point” row showing ticks and $/point

Notes

• Contract specs can vary by broker/exchange and may change over time. Always confirm with official specifications.

• Educational tool only; not financial advice.

Intelligent Currency Breakout ChannelIndicator: Intelligent Currency Breakout Channel

This document provides a detailed explanation of the "Intelligent Currency Breakout Channel" indicator for TradingView.

1. Overview

The Intelligent Currency Breakout Channel is an advanced technical analysis tool designed to identify periods of price consolidation and signal potential breakouts. It automatically draws channels around ranging price action and utilizes sophisticated volume analysis to provide deeper insights into market sentiment. The indicator also includes a built-in logarithmic regression screener to help traders align their breakout signals with the broader market trend.

2. Key Features

Automatic Channel Detection: The indicator identifies periods of low volatility and automatically draws a containing channel (box) around the price action.

Breakout Signals: It generates clear visual alerts (▲ for bullish, ▼ for bearish) when the price closes decisively outside of a channel.

In-Depth Volume Analysis: Within each channel, the indicator plots volume as candlestick-like bars, offering three distinct modes: Total Volume, Buy/Sell Comparison, and Volume Delta. This helps traders gauge the strength and conviction behind price movements.

Real-time Sentiment Gauge: When a channel is active, a dynamic color-graded gauge appears on the right side of the chart. It visualizes the current volume delta momentum relative to its recent range, offering an at-a-glance sentiment reading.

Integrated Trend Screener: A secondary analysis tool based on logarithmic regression is included to determine the underlying trend direction (Up, Down, or Neutral), which can be used to filter breakout signals.

Fully Customizable: Users can extensively customize all parameters, from calculation lengths and breakout sensitivity to the visual appearance of every component.

3. How to Use

Channel Formation: Watch for the indicator to draw a new channel. This signifies that the market is in a consolidation or ranging phase. The formation of a channel itself can be an alertable event.

Volume Interpretation: Observe the volume bars inside the channel. An increase in volume as the price approaches the channel's upper or lower boundary can foreshadow a potential breakout. Use the Volume Display Mode to analyze if buying pressure (Comparison, Delta) or selling pressure is building.

Breakout Confirmation: A bullish breakout signal (▲) appears when the price closes above the channel's upper boundary. A bearish breakout signal (▼) appears when the price closes below the lower boundary. For higher-quality signals, enable the Strong Closes Only option.

Trend Confirmation (Screener): Use the screener's plot and background color to confirm the broader trend. For instance, you might choose to only take bullish breakout signals when the screener indicates an uptrend (green background) and bearish signals when it indicates a downtrend (red background).

Sentiment Gauge: The pointer on the gauge indicates current momentum. A pointer in the upper (green) section suggests bullish pressure, while a pointer in the lower (red) section suggests bearish pressure. This can provide additional confluence for a trade decision.

4. Settings and Inputs

Main Settings

Overlap Channels: If enabled, allows multiple channels to be drawn on the chart simultaneously, even if they overlap. When disabled, a new channel will only form if it doesn't intersect with an existing one.

Strong Closes Only: If enabled, a breakout is only triggered if the midpoint of the candle's body (average of open and close) is outside the channel. This helps filter out false signals caused by long wicks. If disabled, any close outside the channel triggers a breakout.

Normalization Length: The lookback period (in bars) used for price normalization. A higher value creates a more stable normalization but may be slower to react to recent price changes.

Box Detection Length: The lookback period used to detect the channel formation pattern. A lower value will result in more frequent channels but may be more sensitive to noise. A higher value will result in fewer, but potentially more significant, channels.

Volume Analysis

Show Volume Analysis: Toggles the visibility of the candlestick-like volume bars inside the channel.

Volume Display Mode:

Volume: Displays total volume as symmetrical bars around the channel's midline.

Comparison: Shows buying volume (green) above the midline and selling volume (red) below it.

Delta: Shows the net difference between buying and selling volume. Positive delta is shown above the midline, and negative delta is shown below.

Volume Delta Timeframe Source: The timeframe from which to source volume data for calculations. Using a lower timeframe can provide a more granular view of volume dynamics.

Volume Scaling: A multiplier that adjusts the vertical size of the volume bars relative to the channel's height.

Appearance

Volume Text Size: Sets the size of the volume data text displayed in the corners of the channel. Options: Tiny, Small, Medium, Large.

Bullish Color: The primary color for all bullish visual elements, including breakout signals and positive volume bars.

Bearish Color: The primary color for all bearish visual elements, including breakout signals and negative volume bars.

Screener Settings

Lookback Period: The number of bars used for the logarithmic regression calculation to determine the trend.

Screener Type:

Log Regression Channel: The signal is based on the slope of the entire regression channel over the lookback period. An upward sloping channel is bullish (1), and a downward sloping one is bearish (-1).

Logarithmic Regression: The signal is based on the most recent value of the regression line compared to its value 3 bars ago. This provides a more responsive measure of the immediate trend.

5. Alerts

You can set up the following alerts through the TradingView alerts panel:

New Channel Formed: Triggers when a new price consolidation channel is detected and drawn on the chart.

Bullish Breakout: Triggers when the price breaks out and closes above the upper boundary of a channel.

Bearish Breakout: Triggers when the price breaks out and closes below the lower boundary of a channel.

Is In Channel: Triggers on every bar that the price is currently trading inside an active channel.

Signal UP: Triggers when the Screener's signal turns bullish (1).

Signal DOWN: Triggers when the Screener's signal turns bearish (-1).

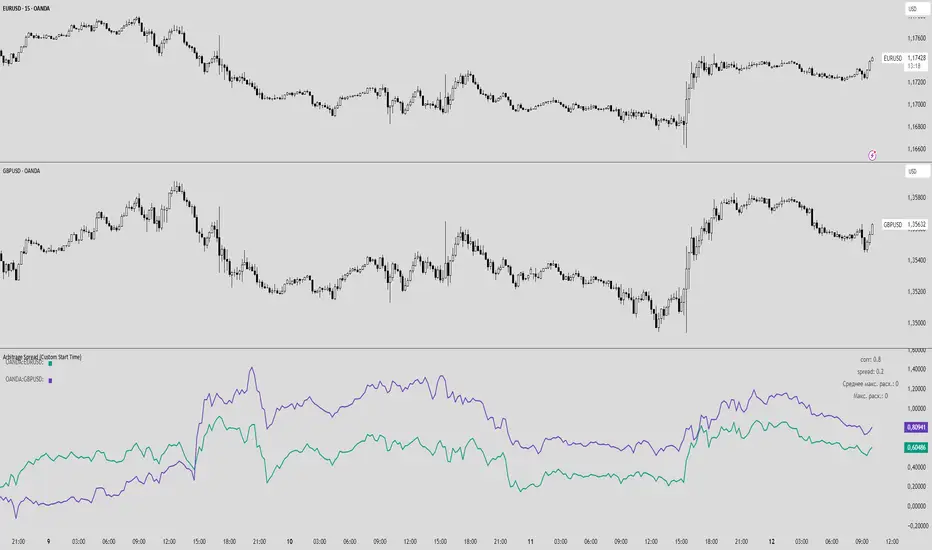

FXSArbitrage Spread (Custom Start Time)

This indicator analyzes the spread and correlation between two selected instruments or currency pairs.

Key Features:

Displays the percentage change of the two instruments in a separate chart (does not overlay the main chart).

Lines show the entire historical price movement of the selected instruments.

Calculates the current spread and correlation from a chosen date and time (default — last Monday 00:00).

Spread and corr values are rounded to two decimal places for convenience.

The top-right table displays:

corr — correlation coefficient between the instruments,

spread — current spread between the pairs,

Average max deviation for the period — manual input,

Maximum deviation for the entire period — manual input.

The top-left table shows the color of each pair for clarity.

Alerts can be set for specific corr and spread values.

Features:

Historical lines allow visual tracking of dynamics over the entire available period.

Current spread is calculated separately from the selected start time, allowing analysis of current conditions without affecting historical visualization.

Fully customizable: line colors, calculation period, start date/time for spread, manual statistical data.

AInfluence Manual Data Input Utility Indicator V101AInfluence (Manual Data Input Utility Indicator) V101

Overview

This utility indicator enables you to plot an external data series directly on your TradingView chart. It is designed for users who want to correlate custom datasets, such as sentiment analysis, economic data, or other external metrics, with price action.

Instructions

1. Add the indicator to your chart.

2. Go into the indicator's "Settings" panel.

3. Paste your pre-formatted data into the text input field.

Data Formatting Rules

The script requires a specific format for each data point, which consists of a numerical value and a timestamp

• Structure: Each data point must be on a new line.

• Limit: You can paste a maximum of 146 records.

Example Data:

93.1562,2025-09-06 00:59:11

94.9062,2025-09-06 01:59:21

93.4062,2025-09-06 02:59:18

95.2188,2025-09-06 03:59:31

93.4062,2025-09-06 04:59:21

91.4583,2025-09-06 05:58:51

93.7812,2025-09-06 06:59:17

The source code for this indicator is open and accessible.

Custom Trade Checklist by [YSFX]# Custom Trade Checklist: Your On-Chart Trading Co-Pilot

## Overview

Ever taken a trade based on impulse, only to realize you forgot a key step in your analysis? The Custom Trade Checklist is a simple yet powerful on-chart utility designed to help you remain disciplined and consistent with your trading strategy.

By externalizing your trading plan into a visible, interactive checklist, you can reduce emotional decision-making and systematically verify your criteria before entering or exiting a trade. This tool acts as your personal co-pilot, ensuring you follow your rules on every single trade.

## Key Features

✅ Fully Customizable Rules: Define up to 10 unique checklist items tailored to your specific trading strategy. Examples include "Market Structure Aligned?", "RSI Oversold?", "News Events Checked?", or "Risk/Reward > 2:1?".

⚪ Dynamic Status Tracking: Use a simple dropdown menu in the settings to mark each rule with intuitive symbols like:

✅ / ✓ - Completed / True

❌ / ✕ - Failed / False

🟡 - Pending / Caution

⚪ - Neutral / Not Checked

And many more for complete flexibility.

📋 Clean & Minimalist Display: The checklist is presented in a clean, unobtrusive table that can be positioned in any corner of your chart, ensuring it provides guidance without cluttering your analysis.

⚙️ Flexible Configuration:

Choose the maximum number of entries to display.

Optionally hide disabled checklist items to keep your view focused on what's active.

Customize the table title to match your strategy (e.g., "Pre-Trade Checklist", "Swing Trade Rules").

🎨 Complete Color Control: Personalize every aspect of the table's appearance. You can independently set the colors for the title, text, background, border, and each individual status symbol to perfectly match your chart's theme.

## How to Use

Add the Indicator to your chart.

Open the Settings Panel by clicking the gear icon (⚙️) on the indicator.

Define Your Rules:

Go through Entry 1 to Entry 10.

For each rule you want to use, check the box to enable it.

In the text field, write your rule (e.g., "Price above 200 EMA").

Update Your Status: Before placing a trade, go back into the settings and update the status dropdown for each rule based on your analysis.

Customize Appearance:

Under the "General" tab, change the table title and position.

Under the "Colors" tab, adjust the colors to your liking.

## Who Is This For?

This tool is perfect for:

Discretionary Traders who need to enforce a consistent set of rules.

New Traders looking to build good habits and internalize their trading plan.

Systematic Traders who want a final pre-flight check before executing a trade.

Anyone working on improving their trading psychology and reducing impulsive actions.

This indicator does not generate signals or trading advice; it is a utility to support the trader's own process and discipline. We hope it helps you achieve greater consistency in your trading journey!

Bar Index & TimeLibrary to convert a bar index to a timestamp and vice versa.

Utilizes runtime memory to store the 𝚝𝚒𝚖𝚎 and 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 values of every bar on the chart (and optional future bars), with the ability of storing additional custom values for every chart bar.

█ PREFACE

This library aims to tackle some problems that pine coders (from beginners to advanced) often come across, such as:

I'm trying to draw an object with a 𝚋𝚊𝚛_𝚒𝚗𝚍𝚎𝚡 that is more than 10,000 bars into the past, but this causes my script to fail. How can I convert the 𝚋𝚊𝚛_𝚒𝚗𝚍𝚎𝚡 to a UNIX time so that I can draw visuals using xloc.bar_time ?

I have a diagonal line drawing and I want to get the "y" value at a specific time, but line.get_price() only accepts a bar index value. How can I convert the timestamp into a bar index value so that I can still use this function?

I want to get a previous 𝚘𝚙𝚎𝚗 value that occurred at a specific timestamp. How can I convert the timestamp into a historical offset so that I can use 𝚘𝚙𝚎𝚗 ?

I want to reference a very old value for a variable. How can I access a previous value that is older than the maximum historical buffer size of 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎 ?

This library can solve the above problems (and many more) with the addition of a few lines of code, rather than requiring the coder to refactor their script to accommodate the limitations.

█ OVERVIEW

The core functionality provided is conversion between xloc.bar_index and xloc.bar_time values.

The main component of the library is the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object, created via the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function which basically stores the 𝚝𝚒𝚖𝚎 and 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 of every bar on the chart, and there are 3 more overloads to this function that allow collecting and storing additional data. Once a 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object is created, use any of the exported methods:

Methods to convert a UNIX timestamp into a bar index or bar offset:

𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚐𝚎𝚝𝙽𝚞𝚖𝚋𝚎𝚛𝙾𝚏𝙱𝚊𝚛𝚜𝙱𝚊𝚌𝚔()

Methods to retrieve the stored data for a bar index:

𝚝𝚒𝚖𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚝𝚒𝚖𝚎𝙲𝚕𝚘𝚜𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚟𝚊𝚕𝚞𝚎𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡(), 𝚐𝚎𝚝𝙰𝚕𝚕𝚅𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜𝙰𝚝𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡()

Methods to retrieve the stored data at a number of bars back (i.e., historical offset):

𝚝𝚒𝚖𝚎(), 𝚝𝚒𝚖𝚎𝙲𝚕𝚘𝚜𝚎(), 𝚟𝚊𝚕𝚞𝚎()

Methods to retrieve all the data points from the earliest bar (or latest bar) stored in memory, which can be useful for debugging purposes:

𝚐𝚎𝚝𝙴𝚊𝚛𝚕𝚒𝚎𝚜𝚝𝚂𝚝𝚘𝚛𝚎𝚍𝙳𝚊𝚝𝚊(), 𝚐𝚎𝚝𝙻𝚊𝚝𝚎𝚜𝚝𝚂𝚝𝚘𝚛𝚎𝚍𝙳𝚊𝚝𝚊()

Note: the library's strong suit is referencing data from very old bars in the past, which is especially useful for scripts that perform its necessary calculations only on the last bar.

█ USAGE

Step 1

Import the library. Replace with the latest available version number for this library.

//@version=6

indicator("Usage")

import n00btraders/ChartData/

Step 2

Create a 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object to collect data on every bar. Do not declare as `var` or `varip`.

chartData = ChartData.collectChartData() // call on every bar to accumulate the necessary data

Step 3

Call any method(s) on the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object. Do not modify its fields directly.

if barstate.islast

int firstBarTime = chartData.timeAtBarIndex(0)

int lastBarTime = chartData.time(0)

log.info("First `time`: " + str.format_time(firstBarTime) + ", Last `time`: " + str.format_time(lastBarTime))

█ EXAMPLES

• Collect Future Times

The overloaded 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() functions that accept a 𝚋𝚊𝚛𝚜𝙵𝚘𝚛𝚠𝚊𝚛𝚍 argument can additionally store time values for up to 500 bars into the future.

//@version=6

indicator("Example `collectChartData(barsForward)`")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData(barsForward = 500)

var rectangle = box.new(na, na, na, na, xloc = xloc.bar_time, force_overlay = true)

if barstate.islast

int futureTime = chartData.timeAtBarIndex(bar_index + 100)

int lastBarTime = time

box.set_lefttop(rectangle, lastBarTime, open)

box.set_rightbottom(rectangle, futureTime, close)

box.set_text(rectangle, "Extending box 100 bars to the right. Time: " + str.format_time(futureTime))

• Collect Custom Data

The overloaded 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() functions that accept a 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜 argument can additionally store custom user-specified values for every bar on the chart.

//@version=6

indicator("Example `collectChartData(variables)`")

import n00btraders/ChartData/1

var map variables = map.new()

variables.put("open", open)

variables.put("close", close)

variables.put("open-close midpoint", (open + close) / 2)

variables.put("boolean", open > close ? 1 : 0)

chartData = ChartData.collectChartData(variables = variables)

var fgColor = chart.fg_color

var table1 = table.new(position.top_right, 2, 9, color(na), fgColor, 1, fgColor, 1, true)

var table2 = table.new(position.bottom_right, 2, 9, color(na), fgColor, 1, fgColor, 1, true)

if barstate.isfirst

table.cell(table1, 0, 0, "ChartData.value()", text_color = fgColor)

table.cell(table2, 0, 0, "open ", text_color = fgColor)

table.merge_cells(table1, 0, 0, 1, 0)

table.merge_cells(table2, 0, 0, 1, 0)

for i = 1 to 8

table.cell(table1, 0, i, text_color = fgColor, text_halign = text.align_left, text_font_family = font.family_monospace)

table.cell(table2, 0, i, text_color = fgColor, text_halign = text.align_left, text_font_family = font.family_monospace)

table.cell(table1, 1, i, text_color = fgColor)

table.cell(table2, 1, i, text_color = fgColor)

if barstate.islast

for i = 1 to 8

float open1 = chartData.value("open", 5000 * i)

float open2 = i < 3 ? open : -1

table.cell_set_text(table1, 0, i, "chartData.value(\"open\", " + str.tostring(5000 * i) + "): ")

table.cell_set_text(table2, 0, i, "open : ")

table.cell_set_text(table1, 1, i, str.tostring(open1))

table.cell_set_text(table2, 1, i, open2 >= 0 ? str.tostring(open2) : "Error")

• xloc.bar_index → xloc.bar_time

The 𝚝𝚒𝚖𝚎 value (or 𝚝𝚒𝚖𝚎_𝚌𝚕𝚘𝚜𝚎 value) can be retrieved for any bar index that is stored in memory by the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object.

//@version=6

indicator("Example `timeAtBarIndex()`")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData()

if barstate.islast

int start = bar_index - 15000

int end = bar_index - 100

// line.new(start, close, end, close) // !ERROR - `start` value is too far from current bar index

start := chartData.timeAtBarIndex(start)

end := chartData.timeAtBarIndex(end)

line.new(start, close, end, close, xloc.bar_time, width = 10)

• xloc.bar_time → xloc.bar_index

Use 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡() to find the bar that a timestamp belongs to.

If the timestamp falls in between the close of one bar and the open of the next bar,

the 𝚜𝚗𝚊𝚙 parameter can be used to determine which bar to choose:

𝚂𝚗𝚊𝚙.𝙻𝙴𝙵𝚃 - prefer to choose the leftmost bar (typically used for closing times)

𝚂𝚗𝚊𝚙.𝚁𝙸𝙶𝙷𝚃 - prefer to choose the rightmost bar (typically used for opening times)

𝚂𝚗𝚊𝚙.𝙳𝙴𝙵𝙰𝚄𝙻𝚃 (or 𝚗𝚊) - copies the same behavior as xloc.bar_time uses for drawing objects

//@version=6

indicator("Example `timestampToBarIndex()`")

import n00btraders/ChartData/1

startTimeInput = input.time(timestamp("01 Aug 2025 08:30 -0500"), "Session Start Time")

endTimeInput = input.time(timestamp("01 Aug 2025 15:15 -0500"), "Session End Time")

chartData = ChartData.collectChartData()

if barstate.islastconfirmedhistory

int startBarIndex = chartData.timestampToBarIndex(startTimeInput, ChartData.Snap.RIGHT)

int endBarIndex = chartData.timestampToBarIndex(endTimeInput, ChartData.Snap.LEFT)

line1 = line.new(startBarIndex, 0, startBarIndex, 1, extend = extend.both, color = color.new(color.green, 60), force_overlay = true)

line2 = line.new(endBarIndex, 0, endBarIndex, 1, extend = extend.both, color = color.new(color.green, 60), force_overlay = true)

linefill.new(line1, line2, color.new(color.green, 90))

// using Snap.DEFAULT to show that it is equivalent to drawing lines using `xloc.bar_time` (i.e., it aligns to the same bars)

startBarIndex := chartData.timestampToBarIndex(startTimeInput)

endBarIndex := chartData.timestampToBarIndex(endTimeInput)

line.new(startBarIndex, 0, startBarIndex, 1, extend = extend.both, color = color.yellow, width = 3)

line.new(endBarIndex, 0, endBarIndex, 1, extend = extend.both, color = color.yellow, width = 3)

line.new(startTimeInput, 0, startTimeInput, 1, xloc.bar_time, extend.both, color.new(color.blue, 85), width = 11)

line.new(endTimeInput, 0, endTimeInput, 1, xloc.bar_time, extend.both, color.new(color.blue, 85), width = 11)

• Get Price of Line at Timestamp

The pine script built-in function line.get_price() requires working with bar index values. To get the price of a line in terms of a timestamp, convert the timestamp into a bar index or offset.

//@version=6

indicator("Example `line.get_price()` at timestamp")

import n00btraders/ChartData/1

lineStartInput = input.time(timestamp("01 Aug 2025 08:30 -0500"), "Line Start")

chartData = ChartData.collectChartData()

var diagonal = line.new(na, na, na, na, force_overlay = true)

if time <= lineStartInput

line.set_xy1(diagonal, bar_index, open)

if barstate.islastconfirmedhistory

line.set_xy2(diagonal, bar_index, close)

if barstate.islast

int timeOneWeekAgo = timenow - (7 * timeframe.in_seconds("1D") * 1000)

// Note: could also use `timetampToBarIndex(timeOneWeekAgo, Snap.DEFAULT)` and pass the value directly to `line.get_price()`

int barsOneWeekAgo = chartData.getNumberOfBarsBack(timeOneWeekAgo)

float price = line.get_price(diagonal, bar_index - barsOneWeekAgo)

string formatString = "Time 1 week ago: {0,number,#} - Equivalent to {1} bars ago 𝚕𝚒𝚗𝚎.𝚐𝚎𝚝_𝚙𝚛𝚒𝚌𝚎(): {2,number,#.##}"

string labelText = str.format(formatString, timeOneWeekAgo, barsOneWeekAgo, price)

label.new(timeOneWeekAgo, price, labelText, xloc.bar_time, style = label.style_label_lower_right, size = 16, textalign = text.align_left, force_overlay = true)

█ RUNTIME ERROR MESSAGES

This library's functions will generate a custom runtime error message in the following cases:

𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() is not called consecutively, or is called more than once on a single bar

Invalid 𝚋𝚊𝚛𝚜𝙵𝚘𝚛𝚠𝚊𝚛𝚍 argument in the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function

Invalid 𝚟𝚊𝚛𝚒𝚊𝚋𝚕𝚎𝚜 argument in the 𝚌𝚘𝚕𝚕𝚎𝚌𝚝𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊() function

Invalid 𝚕𝚎𝚗𝚐𝚝𝚑 argument in any of the functions that accept a number of bars back

Note: there is no runtime error generated for an invalid 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙 or 𝚋𝚊𝚛𝙸𝚗𝚍𝚎𝚡 argument in any of the functions. Instead, the functions will assign 𝚗𝚊 to the returned values.

Any other runtime errors are due to incorrect usage of the library.

█ NOTES

• Function Descriptions

The library source code uses Markdown for the exported functions. Hover over a function/method call in the Pine Editor to display formatted, detailed information about the function/method.

//@version=6

indicator("Demo Function Tooltip")

import n00btraders/ChartData/1

chartData = ChartData.collectChartData()

int barIndex = chartData.timestampToBarIndex(timenow)

log.info(str.tostring(barIndex))

• Historical vs. Realtime Behavior

Under the hood, the data collector for this library is declared as `var`. Because of this, the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object will always reflect the latest available data on realtime updates. Any data that is recorded for historical bars will remain unchanged throughout the execution of a script.

//@version=6

indicator("Demo Realtime Behavior")

import n00btraders/ChartData/1

var map variables = map.new()

variables.put("open", open)

variables.put("close", close)

chartData = ChartData.collectChartData(variables)

if barstate.isrealtime

varip float initialOpen = open

varip float initialClose = close

varip int updateCount = 0

updateCount += 1

float latestOpen = open

float latestClose = close

float recordedOpen = chartData.valueAtBarIndex("open", bar_index)

float recordedClose = chartData.valueAtBarIndex("close", bar_index)

string formatString = "# of updates: {0} 𝚘𝚙𝚎𝚗 at update #1: {1,number,#.##} 𝚌𝚕𝚘𝚜𝚎 at update #1: {2,number,#.##} "

+ "𝚘𝚙𝚎𝚗 at update #{0}: {3,number,#.##} 𝚌𝚕𝚘𝚜𝚎 at update #{0}: {4,number,#.##} "

+ "𝚘𝚙𝚎𝚗 stored in memory: {5,number,#.##} 𝚌𝚕𝚘𝚜𝚎 stored in memory: {6,number,#.##}"

string labelText = str.format(formatString, updateCount, initialOpen, initialClose, latestOpen, latestClose, recordedOpen, recordedClose)

label.new(bar_index, close, labelText, style = label.style_label_left, force_overlay = true)

• Collecting Chart Data for Other Contexts

If your use case requires collecting chart data from another context, avoid directly retrieving the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 object as this may exceed memory limits .

//@version=6

indicator("Demo Return Calculated Results")

import n00btraders/ChartData/1

timeInput = input.time(timestamp("01 Sep 2025 08:30 -0500"), "Time")

var int oneMinuteBarsAgo = na

// !ERROR - Memory Limits Exceeded

// chartDataArray = request.security_lower_tf(syminfo.tickerid, "1", ChartData.collectChartData())

// oneMinuteBarsAgo := chartDataArray.last().getNumberOfBarsBack(timeInput)

// function that returns calculated results (a single integer value instead of an entire `ChartData` object)

getNumberOfBarsBack() =>

chartData = ChartData.collectChartData()

chartData.getNumberOfBarsBack(timeInput)

calculatedResultsArray = request.security_lower_tf(syminfo.tickerid, "1", getNumberOfBarsBack())

oneMinuteBarsAgo := calculatedResultsArray.size() > 0 ? calculatedResultsArray.last() : na

if barstate.islast

string labelText = str.format("The selected timestamp occurs 1-minute bars ago", oneMinuteBarsAgo)

label.new(bar_index, hl2, labelText, style = label.style_label_left, size = 16, force_overlay = true)

• Memory Usage

The library's convenience and ease of use comes at the cost of increased usage of computational resources. For simple scripts, using this library will likely not cause any issues with exceeding memory limits. But for large and complex scripts, you can reduce memory issues by specifying a lower 𝚌𝚊𝚕𝚌_𝚋𝚊𝚛𝚜_𝚌𝚘𝚞𝚗𝚝 amount in the indicator() or strategy() declaration statement.

//@version=6

// !ERROR - Memory Limits Exceeded using the default number of bars available (~20,000 bars for Premium plans)

//indicator("Demo `calc_bars_count` parameter")

// Reduce number of bars using `calc_bars_count` parameter

indicator("Demo `calc_bars_count` parameter", calc_bars_count = 15000)

import n00btraders/ChartData/1

map variables = map.new()

variables.put("open", open)

variables.put("close", close)

variables.put("weekofyear", weekofyear)

variables.put("dayofmonth", dayofmonth)

variables.put("hour", hour)

variables.put("minute", minute)

variables.put("second", second)

// simulate large memory usage

chartData0 = ChartData.collectChartData(variables)

chartData1 = ChartData.collectChartData(variables)

chartData2 = ChartData.collectChartData(variables)

chartData3 = ChartData.collectChartData(variables)

chartData4 = ChartData.collectChartData(variables)

chartData5 = ChartData.collectChartData(variables)

chartData6 = ChartData.collectChartData(variables)

chartData7 = ChartData.collectChartData(variables)

chartData8 = ChartData.collectChartData(variables)

chartData9 = ChartData.collectChartData(variables)

log.info(str.tostring(chartData0.time(0)))

log.info(str.tostring(chartData1.time(0)))

log.info(str.tostring(chartData2.time(0)))

log.info(str.tostring(chartData3.time(0)))

log.info(str.tostring(chartData4.time(0)))

log.info(str.tostring(chartData5.time(0)))

log.info(str.tostring(chartData6.time(0)))

log.info(str.tostring(chartData7.time(0)))

log.info(str.tostring(chartData8.time(0)))

log.info(str.tostring(chartData9.time(0)))

if barstate.islast

result = table.new(position.middle_right, 1, 1, force_overlay = true)

table.cell(result, 0, 0, "Script Execution Successful ✅", text_size = 40)

█ EXPORTED ENUMS

Snap

Behavior for determining the bar that a timestamp belongs to.

Fields:

LEFT : Snap to the leftmost bar.

RIGHT : Snap to the rightmost bar.

DEFAULT : Default `xloc.bar_time` behavior.

Note: this enum is used for the 𝚜𝚗𝚊𝚙 parameter of 𝚝𝚒𝚖𝚎𝚜𝚝𝚊𝚖𝚙𝚃𝚘𝙱𝚊𝚛𝙸𝚗𝚍𝚎𝚡().

█ EXPORTED TYPES

Note: users of the library do not need to worry about directly accessing the fields of these types; all computations are done through method calls on an object of the 𝙲𝚑𝚊𝚛𝚝𝙳𝚊𝚝𝚊 type.

Variable

Represents a user-specified variable that can be tracked on every chart bar.

Fields:

name (series string) : Unique identifier for the variable.

values (array) : The array of stored values (one value per chart bar).

ChartData

Represents data for all bars on a chart.

Fields:

bars (series int) : Current number of bars on the chart.

timeValues (array) : The `time` values of all chart (and future) bars.

timeCloseValues (array) : The `time_close` values of all chart (and future) bars.

variables (array) : Additional custom values to track on all chart bars.

█ EXPORTED FUNCTIONS

collectChartData()

Collects and tracks the `time` and `time_close` value of every bar on the chart.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(barsForward)

Collects and tracks the `time` and `time_close` value of every bar on the chart as well as a specified number of future bars.

Parameters:

barsForward (simple int) : Number of future bars to collect data for.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(variables)

Collects and tracks the `time` and `time_close` value of every bar on the chart. Additionally, tracks a custom set of variables for every chart bar.

Parameters:

variables (simple map) : Custom values to collect on every chart bar.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

collectChartData(barsForward, variables)

Collects and tracks the `time` and `time_close` value of every bar on the chart as well as a specified number of future bars. Additionally, tracks a custom set of variables for every chart bar.

Parameters:

barsForward (simple int) : Number of future bars to collect data for.

variables (simple map) : Custom values to collect on every chart bar.

Returns: `ChartData` object to convert between `xloc.bar_index` and `xloc.bar_time`.

█ EXPORTED METHODS

method timestampToBarIndex(chartData, timestamp, snap)

Converts a UNIX timestamp to a bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

timestamp (series int) : A UNIX time.

snap (series Snap) : A `Snap` enum value.

Returns: A bar index, or `na` if unable to find the appropriate bar index.

method getNumberOfBarsBack(chartData, timestamp)

Converts a UNIX timestamp to a history-referencing length (i.e., number of bars back).

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

timestamp (series int) : A UNIX time.

Returns: A bar offset, or `na` if unable to find a valid number of bars back.

method timeAtBarIndex(chartData, barIndex)

Retrieves the `time` value for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (int) : The bar index.

Returns: The `time` value, or `na` if there is no `time` stored for the bar index.

method time(chartData, length)

Retrieves the `time` value of the bar that is `length` bars back relative to the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

length (series int) : Number of bars back.

Returns: The `time` value `length` bars ago, or `na` if there is no `time` stored for that bar.

method timeCloseAtBarIndex(chartData, barIndex)

Retrieves the `time_close` value for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (series int) : The bar index.

Returns: The `time_close` value, or `na` if there is no `time_close` stored for the bar index.

method timeClose(chartData, length)

Retrieves the `time_close` value of the bar that is `length` bars back from the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

length (series int) : Number of bars back.

Returns: The `time_close` value `length` bars ago, or `na` if there is none stored.

method valueAtBarIndex(chartData, name, barIndex)

Retrieves the value of a custom variable for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

name (series string) : The variable name.

barIndex (series int) : The bar index.

Returns: The value of the variable, or `na` if that variable is not stored for the bar index.

method value(chartData, name, length)

Retrieves a variable value of the bar that is `length` bars back relative to the latest bar.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

name (series string) : The variable name.

length (series int) : Number of bars back.

Returns: The value `length` bars ago, or `na` if that variable is not stored for the bar index.

method getAllVariablesAtBarIndex(chartData, barIndex)

Retrieves all custom variables for the specified bar index.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

barIndex (series int) : The bar index.

Returns: Map of all custom variables that are stored for the specified bar index.

method getEarliestStoredData(chartData)

Gets all values from the earliest bar data that is currently stored in memory.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

Returns: A tuple:

method getLatestStoredData(chartData, futureData)

Gets all values from the latest bar data that is currently stored in memory.

Namespace types: ChartData

Parameters:

chartData (series ChartData) : The `ChartData` object.

futureData (series bool) : Whether to include the future data that is stored in memory.

Returns: A tuple:

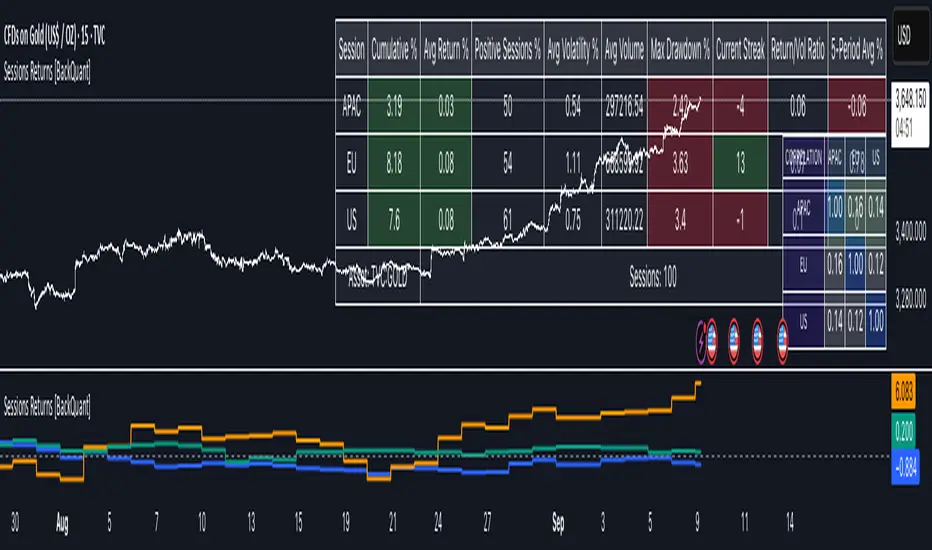

Cumulative Returns by Session [BackQuant]Cumulative Returns by Session

What this is

This tool breaks the trading day into three user-defined sessions and tracks how much each session contributes to return, volatility, and volume. It then aggregates results over a rolling window so you can see which session has been pulling its weight, how streaky each session has been, and how sessions relate to one another through a compact correlation heatmap.

We’ve also given the functionality for the user to use a simplified table, just by switching off all settings they are not interested in.

How it works

1) Session segmentation

You define APAC, EU, and US sessions with explicit hours and time zones. The script detects when each session starts and ends on every intraday bar and records its open, intraday high and low, close, and summed volume.

2) Per-session math

At each session end the script computes:

Return — either Percent: (Close−Open)÷Open×100(Close − Open) ÷ Open × 100(Close−Open)÷Open×100 or Points: (Close−Open)(Close − Open)(Close−Open), based on your selection.

Volatility — either Range: (High−Low)÷Open×100(High − Low) ÷ Open × 100(High−Low)÷Open×100 or ATR scaled by price: ATR÷Open×100ATR ÷ Open × 100ATR÷Open×100.

Volume — total volume transacted during that session.

3) Storage and lookback

Each day’s three session stats are stored as a row. You choose how many recent sessions to keep in memory. The script then:

Builds cumulative returns for APAC, EU, US across the lookback.

Computes averages, win rates, and a Sharpe-like ratio avgreturn÷avgvolatilityavg return ÷ avg volatilityavgreturn÷avgvolatility per session.

Tracks streaks of positive or negative sessions to show momentum.

Tracks drawdowns on cumulative returns to show worst runs from peak.

Computes rolling means over a short window for short-term drift.

4) Correlation heatmap

Using the stored arrays of session returns, the script calculates Pearson correlations between APAC–EU, APAC–US, and EU–US, and colors the matrix by strength and sign so you can spot coupling or decoupling at a glance.

What it plots

Three lines: cumulative return for APAC, EU, US over the chosen lookback.

Zero reference line for orientation.

A statistics table with cumulative %, average %, positive session rate, and optional columns for volatility, average volume, max drawdown, current streak, return-to-vol ratio, and rolling average.

A small correlation heatmap table showing APAC, EU, US cross-session correlations.

How to use it

Pick the asset — leave Custom Instrument empty to use the chart symbol, or point to another symbol for cross-asset studies.

Set your sessions and time zones — defaults approximate APAC, EU, and US hours, but you can align them to exchange times or your workflow.

Choose calculation modes — Percent vs Points for return, Range vs ATR for volatility. Points are convenient for futures and fixed-tick assets, Percent is comparable across symbols.

Decide the lookback — more sessions smooths lines and stats; fewer sessions makes the tool more reactive.

Toggle analytics — add volatility, volume, drawdown, streaks, Sharpe-like ratio, rolling averages, and the correlation table as needed.

Why session attribution helps

Different sessions are driven by different flows. Asia often sets the overnight tone, Europe adds liquidity and direction changes, and the US session can dominate range expansion. Separating contributions by session helps you:

Identify which session has been the main driver of net trend.

Measure whether volatility or volume is concentrated in a specific window.

See if one session’s gains are consistently given back in another.

Adapt tactics: fade during a mean-reverting session, press during a trending session.

Reading the tables

Cumulative % — sum of session returns over the lookback. The sign and slope tell you who is carrying the move.

Avg Return % and Positive Sessions % — direction and hit rate. A low average but high hit rate implies many small moves; the reverse implies occasional big swings.

Avg Volatility % — typical intrabars range for that session. Compare with Avg Return to judge efficiency.

Return/Vol Ratio — return per unit of volatility. Higher is better for stability.

Max Drawdown % — worst cumulative give-back within the lookback. A quick way to spot riskiness by session.

Current Streak — consecutive up or down sessions. Useful for mean-reversion or regime awareness.

Rolling Avg % — short-window drift indicator to catch recent turnarounds.

Correlation matrix — green clusters indicate sessions tending to move together; red indicates offsetting behavior.

Settings overview

Basic

Number of Sessions — how many recent days to include.

Custom Instrument — analyze another ticker while staying on your current chart.

Session Configuration and Times

Enable or hide APAC, EU, US rows.

Set hours per session and the specific time zone for each.

Calculation Methods

Return Calculation — Percent or Points.

Volatility Calculation — Range or ATR; ATR Length when applicable.

Advanced Analytics

Correlation, Drawdown, Momentum, Sharpe-like ratio, Rolling Statistics, Rolling Period.

Display Options and Colors

Show Statistics Table and its position.

Toggle columns for Volatility and Volume.

Pick individual colors for each session line and row accents.

Common applications

Session bias mapping — find which window tends to trend in your market and plan exposure accordingly.

Strategy scheduling — allocate attention or risk to the session with the best return-to-vol ratio.

News and macro awareness — see if correlation rises around central bank cycles or major data releases.

Cross-asset monitoring — set the Custom Instrument to a driver (index future, DXY, yields) to see if your symbol reacts in a particular session.

Notes

This indicator works on intraday charts, since sessions are defined within a day. If you change session clocks or time zones, give the script a few bars to accumulate fresh rows. Percent vs Points and Range vs ATR choices affect comparability across assets, so be consistent when comparing symbols.

Session context is one of the simplest ways to explain a messy tape. By separating the day into three windows and scoring each one on return, volatility, and consistency, this tool shows not just where price ended up but when and how it got there. Use the cumulative lines to spot the steady driver, read the table to judge quality and risk, and glance at the heatmap to learn whether the sessions are amplifying or canceling one another. Adjust the hours to your market and let the data tell you which session deserves your focus.

عكفة الماكد المتقدمة - أبو فارس ©// 🔒 Advanced MACD Curve © 2025

// 💡 Idea & Creativity: Engineer Abu Elias

// 🛠️ Development & Implementation: Abu Fares

// 📜 All intellectual rights reserved - Copying, modifying, or redistributing is not permitted

// 🚫 Any attempt to tamper with this code or violate intellectual property rights is legally prohibited

// 📧 For inquiries and licensing: Please contact the developer, Abu Fares

عكفة الماكد المتقدمة - أبو فارس ©// 🔒 عكفة الماكد المتقدمة © 2025

// 💡 فكرة وإبداع: المهندس أبو الياس

// 🛠️ تطوير وتنفيذ: أبو فارس

// 📜 جميع الحقوق الفكرية محفوظة - لا يُسمح بالنسخ أو التعديل أو إعادة التوزيع

// 🚫 أي محاولة للعبث بهذا الكود أو انتهاك الحقوق الفكرية مرفوضة قانونياً

// 📧 للاستفسارات والتراخيص: يرجى التواصل مع المطور أبو فارس

// 🔒 Advanced MACD Curve © 2025

// 💡 Idea & Creativity: Engineer Abu Elias

// 🛠️ Development & Implementation: Abu Fares

// 📜 All intellectual rights reserved - Copying, modifying, or redistributing is not permitted

// 🚫 Any attempt to tamper with this code or violate intellectual property rights is legally prohibited

// 📧 For inquiries and licensing: Please contact the developer, Abu Fares

SMC Pro (Wellington) v1.4.2This SMC indicator combines BOS/CHoCH, OBs, FVGs, liquidity, and Premium/Discount with confirmation on the 1H (EMA200).

Entries only appear when 3+ confluences align, filtering noise and delivering clear signals.

✅ Ready-to-use alerts (LONG, SHORT, or unified)

✅ Real-time HUD

✅ Strategy tailored for XAUUSD

Retail Sentiment Indicator - Multi-Asset CFD & Fear/Greed IndexRetail Sentiment Indicator - Multi-Asset CFD & Fear/Greed Index

Overview

The Retail Sentiment Indicator provides real-time sentiment data for major financial instruments including stocks, forex, commodities, and cryptocurrencies. This indicator displays retail trader positioning and market sentiment using CFD data and fear/greed indices.

Methodology and Scale Calculation

This indicator operates on a **-50 to +50 scale** with zero representing perfect market equilibrium.

Scale Interpretation:

- **Zero (0)**: Market balance - exactly 50% of investors buying, 50% selling

- **Positive values**: Majority buying pressure

- Example: If 63% of investors are buying, the indicator shows +13 (63 - 50 = +13)

- **Negative values**: Majority selling pressure

- Example: If 92% of investors are selling, the indicator shows -42 (50 - 92 = -42)

BTC Fear & Greed Index Scaling:

The original `BTC FEAR&GREED` index is natively scaled from 0-100 by its creator. In our indicator, this data has been rescaled to also fit the -50 to +50 range for consistency with other sentiment data sources.

This unified scaling approach allows for direct comparison across all instruments and data sources within the indicator.

-Important Data Source Selection-

Bitcoin (BTC) Data Sources

When viewing Bitcoin charts, the indicator offers **two different data sources**:

1. **Default Auto-Mode**: `BTCUSD Retail CFD` - Retail CFD traders sentiment data (automatically loaded).

2. **Manual Selection**: `BTC FEAR&GREED` - Fear & Greed Index from website: alternative dot me

**To access BTC Fear & Greed Index**: Input settings -> disable checkbox "Auto-load Sentiment Data" -> manually select "BTC FEAR&GREED" from the dropdown menu.

US Stock Market Data Sources

For US stocks and indices (S&P 500, NASDAQ, Dow Jones), there are **two data source options**:

1. **Default Auto-Mode**: Individual retail CFD sentiment data for each instrument

2. **Manual Selection**: `SNN FEAR&GREED` - SNN's Fear & Greed Index covering the overall US market sentiment. SNN was used as the name to avoid any potential trademark infringement.

**To access SNN Fear & Greed Index**: When viewing US market charts, disable in input settings checkbox "Auto-load Sentiment Data" and manually select "SNN FEAR&GREED" from the dropdown menu.

This distinction allows traders to choose between **instrument-specific retail sentiment** (auto-mode) or **broader market sentiment indices** (manual selection).

Features

- **Auto-Detection**: Automatically loads sentiment data based on the current chart symbol

- **Manual Selection**: Choose from 40+ supported instruments when auto-detection is unavailable

- **Multiple Data Sources**: Combines retail CFD sentiment with Fear & Greed indices

- **Visual Zones**: Clear greed/fear zones with color-coded backgrounds

- **Real-time Updates**: Live sentiment data from merged data sources

Supported Instruments

Major Indices

- S&P 500, NASDAQ, Dow Jones 30, DAX

Forex Pairs

- Major pairs: EURUSD, GBPUSD, USDJPY, USDCHF, USDCAD

- Cross pairs: EURJPY, GBPJPY, AUDUSD, NZDUSD, and 20+ others

Commodities

- Precious metals: Gold (XAUUSD), Silver (XAGUSD)

- Energy: WTI Oil

- Agricultural: Wheat, Coffee

- Industrial: Copper

Cryptocurrencies

- Bitcoin (BTC) sentiment data

- BTC & SNN Fear & Greed indices

How to Use

1. **Auto Mode** (Default): Enable "Auto-load Sentiment Data" to automatically display sentiment for the current chart symbol

2. **Manual Mode**: Disable auto-load and select from the dropdown menu for specific instruments

3. **Interpretation**:

- Values above 0 (green) indicate retail greed/bullish sentiment

- Values below 0 (red) indicate retail fear/bearish sentiment

- Fear & Greed indices use 0-100 scale (50 is neutral)

Data Sources

This indicator uses curated sentiment data from retail CFD providers and established fear/greed indices. Data is updated regularly and sourced from reputable financial data providers.

Trading Strategy & Market Philosophy

Contrarian Trading Approach

The primary purpose of this indicator is based on the fundamental market principle that **the majority of retail investors are often wrong**, and markets typically move opposite to the positions held by the majority of market participants.

Key Strategy Guidelines:

- **Contrarian Signal**: When the majority of users are positioned on one side of the market, there is statistically greater market advantage in taking positions in the opposite direction

- **Trend Exhaustion Signal**: An interesting observed phenomenon occurs when, during a long-lasting trend where the majority of investors have consistently been on the wrong side, the Sentiment indicator suddenly shows that the majority has flipped and opened positions in the direction of that long-running trend. This is often a signal of fuel exhaustion for further movement in that direction

Interpretation Examples

- High greed readings (majority bullish) → Consider bearish opportunities

- High fear readings (majority bearish) → Consider bullish opportunities

- Sudden sentiment flip during established trends → Potential trend reversal signal

Technical Notes

- Built with PineScript v6

- Dynamic symbol detection with fallback options

- Optimized for performance with minimal resource usage

- Color-coded visualization with customizable zones

Data Sources & Expansion

Acknowledgments

We extend our gratitude to **TradingView** for enabling the use of custom data feeds based on GitHub repositories, making this comprehensive sentiment analysis possible.

Data Expansion Opportunities

As the operator of this indicator, I am **open to suggestions for new data sources** that could be integrated and published. If you have ideas for additional instruments or sentiment data:

How to Submit Suggestions:

1. Send a **private message** with your proposal

2. Include: **instrument/data type**, **source**, and **brief description**

3. If technically feasible, we will work to import and publish the data

Data Infrastructure Status

Current Data Upload Process:

Please note that sentiment data uploads may occasionally experience minor interruptions. However, this should not pose significant issues as sentiment data typically changes gradually rather than rapidly.

Infrastructure Development:

We are actively working on establishing permanent cloud-based infrastructure to ensure continuous, automated data collection and upload processes. This will provide more reliable and consistent data availability in the future.

Disclaimer

This indicator is for educational and informational purposes only. Sentiment data should be used as part of a comprehensive trading strategy and not as the sole basis for trading decisions. Past performance does not guarantee future results. The contrarian approach described is a market theory and may not always produce profitable results.

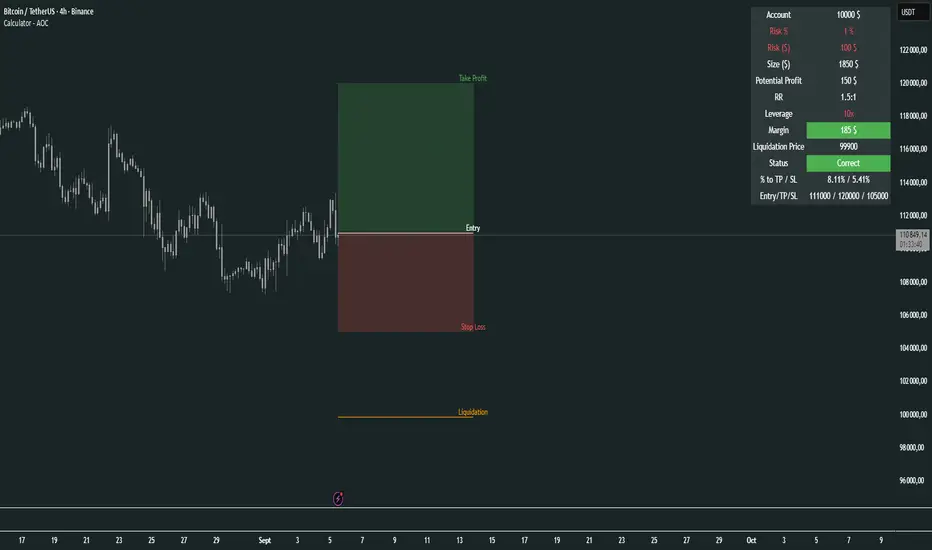

Calculator - AOC📊 Calculator - AOC Indicator 🚀

The Calculator - AOC indicator is a powerful and user-friendly tool designed for TradingView to help traders plan and visualize trades with precision. It calculates key trade metrics, displays entry, take-profit (TP), stop-loss (SL), and liquidation levels, and provides a clear overview of risk management and potential profits. Perfect for both novice and experienced traders! 💡

✨ Features

📈 Trade Planning: Input your Entry Price, Take Profit (TP), Stop Loss (SL), and Trade Direction (Long/Short) to visualize your trade setup on the chart.

💰 Risk Management: Set your Initial Capital and Risk per Trade (%) to calculate the optimal Position Size and Risk Amount for each trade.

⚖️ Leverage Support: Define your Leverage to compute the Required Margin and Liquidation Price, ensuring you stay aware of potential risks.

📊 Risk/Reward Ratio: Automatically calculates the Risk-to-Reward Ratio to evaluate trade profitability.

🎨 Visuals: Displays Entry, TP, SL, and Liquidation levels as lines and boxes on the chart, with customizable Line Width, Line Style, and Label Size.

✅ Trade Validation: Checks if your trade setup is valid (e.g., correct TP/SL placement) and highlights issues like potential liquidation risks with color-coded statuses (Correct ✅, Incorrect ❌, or Liquidation ⚠️).

📋 Summary Table: A clean, top-right table summarizes key metrics: Capital, Risk %, Risk Amount, Position Size, Potential Profit, Risk/Reward, Margin, Liquidation Price, Trade Status, and % to TP/SL.

🖌️ Customization: Adjust Line Extension (Bars) for how far lines extend, and choose from Solid, Dashed, or Dotted line styles for a personalized chart experience.

🛠️ How to Use

Add to Chart: Apply the indicator to your TradingView chart.

Configure Inputs:

Accountability: Set your Initial Capital and Risk per Trade (%).

Target: Enter Entry Price, TP, and SL prices.

Leverage: Specify your leverage (e.g., 10x).

Direction: Choose Long or Short.

Display Settings: Customize Line Width, Line Style, Label Size, and Line Extension.

Analyze: The indicator plots Entry, TP, SL, and Liquidation levels on the chart and displays a table with all trade metrics.

Validate: Check the Trade Status in the table to ensure your setup is valid or if adjustments are needed.

🎯 Why Use It?

Plan Smarter: Visualize your trade setup and understand your risk/reward profile instantly.

Stay Disciplined: Precise position sizing and risk calculations help you stick to your trading plan.

Avoid Mistakes: Clear validation warnings prevent costly errors like incorrect TP/SL placement or liquidation risks.

User-Friendly: Intuitive visuals and a summary table make trade analysis quick and easy.

📝 Notes

Ensure Entry, TP, and SL prices align with your trade direction to avoid "Incorrect" or "Liquidation" statuses.

The indicator updates dynamically on the latest bar, ensuring real-time visuals.

Best used with proper risk management to maximize trading success! 💪

Happy trading! 🚀📈

VWAP + EMA50 + EMA200 (with optional Anchored VWAP)VWAP + EMA50 + EMA200 (with optional Anchored VWAP)

均线趋势过滤器 (MA_trend Signal/Noise Filter)双语简介

中文:

这款指标是一个基于“信噪比”思想的终极趋势过滤器。它通过比较快速和慢速EMA均线之间的差值(即信号)与ATR(平均真实波幅,代表噪音)来判断市场趋势。只有当信号的强度超过噪音的指定倍数时,才会确认趋势的有效性。该指标可帮助交易者过滤掉噪音,精确捕捉强势趋势,避免误操作。

English:

This indicator is the Ultimate Trend Filter based on the Signal-to-Noise ratio concept. It compares the difference between the fast and slow EMA (Signal) to the ATR (Noise) to determine market trends. A trend is confirmed only when the signal strength exceeds the noise by a specified multiplier. This indicator helps traders filter out noise and accurately capture strong trends, avoiding false signals.

FX Sessions (DTS)FX Sessions (DST-Safe)

This indicator highlights the four main Forex trading sessions — Sydney, Tokyo, London, and New York — using the local timezone of each market.

• DST handled automatically: Sessions shift correctly when London or New York move clocks forward/back.

• Clear visualization: Light background shading for each session, with the London–New York overlap emphasized for peak liquidity.

• Customizable: Toggle individual sessions, labels, and the on-chart legend table.

• Intraday focus: Works best on lower timeframes (1m–1h) for identifying active trading hours and volatility windows.

Use this tool to instantly spot when liquidity and volatility are likely to increase, so you know where to focus your trading.

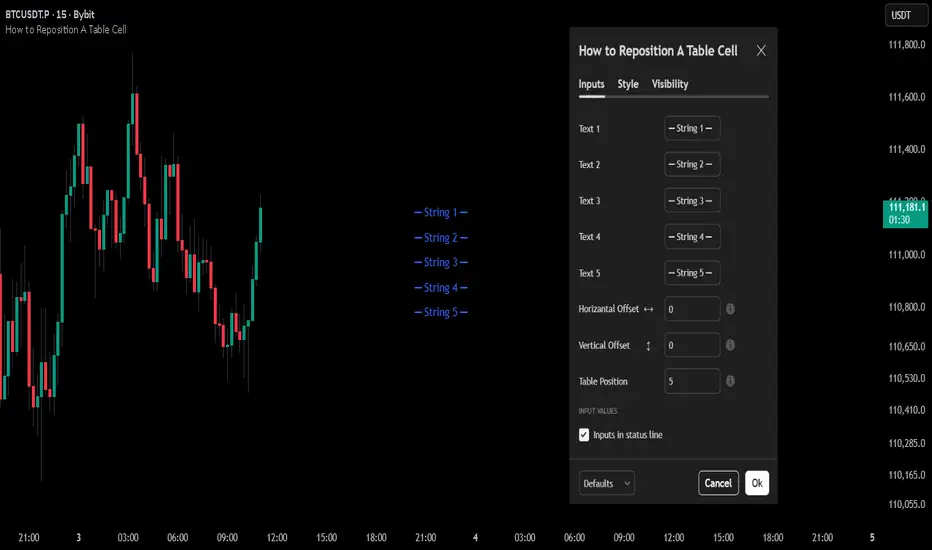

How to Reposition A Table CellOVERVIEW

Using table functions in Pine Script is one of the most effective methods for reporting and interpreting data in a readable manner. However, the built-in capabilities for dynamically repositioning table location are limited. To extend these limitations, a small intervention to the script may be required. This indicator exemplifies how such intervention can be modeled.

CONCEPTS

This indicator provides comprehensive control over table positioning through several user-defined parameters that work together to create flexible display options.

Text Parameters : These five string inputs allow users to define the content displayed in the table. Each parameter accepts custom text that will be displayed as separate rows within the table cell. (The relevant parameters are designed as examples. When implementing the code into your own scripts, you can use series string variables instead of the those inputs.)

Horizontal Offset : This integer parameter controls the horizontal positioning of the table content. Negative values shift the table content to the left, while positive values move it to the right. The offset is multiplied by a spacing factor (currently set to 4) to provide more noticeable movement. This parameter is particularly useful when you need to avoid overlapping with other chart elements or align multiple indicators.

Vertical Offset : This integer parameter manages the vertical positioning by adding line breaks above or below the content. Negative values push the content downward by adding line breaks at the beginning, while positive values elevate the content by adding line breaks at the end. This creates effective vertical spacing without affecting the table's base position.

Table Position : This parameter accepts values from 1 to 9, corresponding to the standard TradingView table positions arranged in a 3x3 grid format (1-3: top row, 4-6: middle row, 7-9: bottom row). This serves as the base positioning before any offset adjustments are applied, providing users with familiar reference points for initial placement.

FUNCTION

The core functionality centers on the custom f_position() function, which processes text positioning based on horizontal and vertical offset values. For vertical positioning, it adds line breaks before or after content depending on the offset direction. For horizontal positioning, it splits the text by rows and adds calculated spaces to each row, maintaining proper alignment across multi-line content. The spacing uses a fixed multiplier of 4, providing good balance between precision and visible movement.

ORIGINALITY & NOTES

Tihs indicator,

introduces a novel approach to table positioning that goes beyond TradingView's standard 9-position limitation by implementing custom offset calculations that allow pixel-level control over table placement.

serves as an educational resource, demonstrating advanced Pine Script techniques for UI manipulation that can be adapted for various custom indicator developments.

is particularly valuable for developers creating complex dashboard layouts or educational materials where precise positioning is crucial. The modular design of the positioning function makes it easily adaptable for other projects requiring similar functionality.

I hope it helps everyone, Always combine with risk management principles and market context awareness. I hope it helps everyone. Trade as safely as possible. Best of luck!

Market Spiralyst [Hapharmonic]Hello, traders and creators! 👋

Market Spiralyst: Let's change the way we look at analysis, shall we? I've got to admit, I scratched my head on this for weeks, Haha :). What you're seeing is an exploration of what's possible when code meets art on financial charts. I wanted to try blending art with trading, to do something new and break away from the same old boring perspectives. The goal was to create a visual experience that's not just analytical, but also relaxing and aesthetically pleasing.

This work is intended as a guide and a design example for all developers, born from the spirit of learning and a deep love for understanding the Pine Script™ language. I hope it inspires you as much as it challenged me!

🧐 Core Concept: How It Works

Spiralyst is built on two distinct but interconnected engines:

The Generative Art Engine: At its core, this indicator uses a wide range of mathematical formulas—from simple polygons to exotic curves like Torus Knots and Spirographs—to draw beautiful, intricate shapes directly onto your chart. This provides a unique and dynamic visual backdrop for your analysis.

The Market Pulse Engine: This is where analysis meets art. The engine takes real-time data from standard technical indicators (RSI and MACD in this version) and translates their states into a simple, powerful "Pulse Score." This score directly influences the appearance of the "Scatter Points" orbiting the main shape, turning the entire artwork into a living, breathing representation of market momentum.

🎨 Unleash Your Creativity! This Is Your Playground

We've included 25 preset shapes for you... but that's just the starting point !

The real magic happens when you start tweaking the settings yourself. A tiny adjustment can make a familiar shape come alive and transform in ways you never expected.

I'm genuinely excited to see what your imagination can conjure up! If you create a shape you're particularly proud of or one that looks completely unique, I would love to see it. Please feel free to share a screenshot in the comments below. I can't wait to see what you discover! :)

Here's the default shape to get you started:

The Dynamic Scatter Points: Reading the Pulse

This is where the magic happens! The small points scattered around the main shape are not just decorative; they are the visual representation of the Market Pulse Score.

The points have two forms:

A small asterisk (`*`): Represents a low or neutral market pulse.

A larger, more prominent circle (`o`): Represents a high, strong market pulse.

Here’s how to read them:

The indicator calculates the Pulse Strength as a percentage (from 0% to 100%) based on the total score from the active indicators (RSI and MACD). This percentage determines the ratio of circles to asterisks.

High Pulse Strength (e.g., 80-100%): Most of the scatter points will transform into large circles (`o`). This indicates that the underlying momentum is strong and It could be an uptrend. It's a visual cue that the market is gaining strength and might be worth paying closer attention to.

Low Pulse Strength (e.g., 0-20%): Most or all of the scatter points will remain as small asterisks (`*`). This suggests weak, neutral, or bearish momentum.

The key takeaway: The more circles you see, the stronger the bullish momentum is according to the active indicators. Watch the artwork "breathe" as the circles appear and disappear with the market's rhythm!

And don't worry about the shape you choose; the scatter points will intelligently adapt and always follow the outer boundary of whatever beautiful form you've selected.

How to Use

Getting started with Spiralyst is simple: