MyLibraryLibrary "MyLibrary"

TODO: add library description here

init(value)

Parameters:

value

set(source, value)

Parameters:

source

value

get(source)

Parameters:

source

Indikatoren und Strategien

Motion▮ FEATURES

Now as library version :)

String-based transition-effects

Performance optimization. Reduced memory consumption up to >90% by kicking the output to the "stdout".

Use marquee- or loader-effect on any possible string location.

Example: UI Price-Ticker

----------------------------------------------------------------------------

Library "Motion"

_getStringMono(_len, _str, _sep)

Parameters:

_len

_str

_sep

marquee(this, _extern, _ws, _subLen, _subStart)

Parameters:

this

_extern

_ws

_subLen

_subStart

transition(this, _subLen, _subStart)

Parameters:

this

_subLen

_subStart

hold(this)

Parameters:

this

keyframe

keyframe A keyframe object.

Fields:

seq

intv

step

length

update_no

frame_no

ltr

hold

Replica of TradingView's Backtesting Engine with ArraysHello everyone,

Here is a perfectly replicated TradingView backtesting engine condensed into a single library function calculated with arrays. It includes TradingView's calculations for Net profit, Total Trades, Percent of Trades Profitable, Profit Factor, Max Drawdown (absolute and percent), and Average Trade (absolute and percent). Here's how TradingView defines each aspect of its backtesting system:

Net Profit: The overall profit or loss achieved.

Total Trades: The total number of closed trades, winning and losing.

Percent Profitable: The percentage of winning trades, the number of winning trades divided by the total number of closed trades.

Profit Factor: The amount of money the strategy made for every unit of money it lost, gross profits divided by gross losses.

Max Drawdown: The greatest loss drawdown, i.e., the greatest possible loss the strategy had compared to its highest profits.

Average Trade: The sum of money gained or lost by the average trade, Net Profit divided by the overall number of closed trades.

Here's how each variable is defined in the library function:

_backtest(bool _enter, bool _exit, float _startQty, float _tradeQty)

bool _enter: When the strategy should enter a trade (entry condition)

bool _exit: When the strategy should exit a trade (exit condition)

float _startQty: The starting capital in the account (for BTCUSD, it is the amount of USD the account starts with)

float _tradeQty: The amount of capital traded (if set to 1000 on BTCUSD, it will trade 1000 USD on each trade)

Currently, this library only works with long strategies, and I've included a commented out section under DEMO STRATEGY where you can replicate my results with TradingView's backtesting engine. There's tons I could do with this beyond what is shown, but this was a project I worked on back in June of 2022 before getting burned out. Feel free to comment with any suggestions or bugs, and I'll try to add or fix them all soon. Here's my list of thing to add to the library currently (may not all be added):

Add commission calculations.

Add support for shorting

Add a graph that resembles TradingView's overview graph.

Clean and optimize code.

Clean up in a way that makes it easy to add other TradingView calculations (such as Sharpe and Sortino ratio).

Separate all variables, so they become accessible outside of calculations (such as gross profit, gross loss, number of winning trades, number of losing trades, etc.).

Thanks for reading,

OztheWoz

Library_SmoothersLibrary "Library_Smoothers"

CorrectedMA(Src, Len)

CorrectedMA The strengths of the corrected Average (CA) is that the current value of the time series must exceed a the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals when the trend is in a weak phase.

Parameters:

Src

Len

Returns: The Corrected source.

EHMA(src, len)

EMA Exponential Moving Average.

Parameters:

src : Source to act upon

len

Returns: EMA of source

FRAMA(src, len, FC, SC)

FRAMA Fractal Adaptive Moving Average

Parameters:

src : Source to act upon

len : Length of moving average

FC : Fast moving average

SC : Slow moving average

Returns: FRAMA of source

Jurik(src, length, phase, power)

Jurik A low lag filter

Parameters:

src : Source

length : Length for smoothing

phase : Phase range is ±100

power : Mathematical power to use. Doesn't need to be whole numbers

Returns: Jurik of source

SMMA(src, len)

SMMA Smoothed moving average. Think of the SMMA as a hybrid of its better-known siblings — the simple moving average (SMA) and the exponential moving average (EMA).

Parameters:

src : Source

len

Returns: SMMA of source

SuperSmoother(src, len)

SuperSmoother

Parameters:

src : Source to smooth

len

Returns: SuperSmoother of the source

TMA(src, len)

TMA Triangular Moving Average

Parameters:

src : Source

len

Returns: TMA of source

TSF(src, len)

TSF Time Series Forecast. Uses linear regression.

Parameters:

src : Source

len

Returns: TSF of source

VIDYA(src, len)

VIDYA Chande's Variable Index Dynamic Average. See www.fxcorporate.com

Parameters:

src : Source

len

Returns: VIDYA of source

VAWMA(src, len, startingWeight, volumeDefault)

VAWMA = VWMA and WMA combined. Simply put, this attempts to determine the average price per share over time weighted heavier for recent values. Uses a triangular algorithm to taper off values in the past (same as WMA does).

Parameters:

src : Source

len : Length

startingWeight

volumeDefault : The default value to use when a chart has no volume.

Returns: The VAWMA of the source.

WWMA(src, len)

WWMA Welles Wilder Moving Average

Parameters:

src : Source

len

Returns: The WWMA of the source

ZLEMA(src, len)

ZLEMA Zero Lag Expotential Moving Average

Parameters:

src : Source

len

Returns: The ZLEMA of the source

SmootherType(mode, src, len, fastMA, slowMA, offset, phase, power, startingWeight, volumeDefault, Corrected)

Performs the specified moving average

Parameters:

mode : Name of moving average

src : the source to apply the MA type

len

fastMA : FRAMA fast moving average

slowMA : FRAMA slow moving average

offset : Linear regression offset

phase : Jurik phase

power : Jurik power

startingWeight : VAWMA starting weight

volumeDefault : VAWMA default volume

Corrected

Returns: The MA smoothed source

HendrixLIBRARY - utilsLibrary "HendrixLIBRARY"

getVolumeData()

getLTF(customTimeframe, ltf)

Parameters:

customTimeframe

ltf

sumArray(a)

Parameters:

a

arrs2vals(upVolumeArray, downVolumeArray, volArr)

Parameters:

upVolumeArray

downVolumeArray

volArr

getVolumesFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getDeltaFromVolumes(upVolume, downVolume)

Parameters:

upVolume

downVolume

getDeltaFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getUpColor()

getDownColor()

getBlackColor()

getColors()

printTableTR(txt)

Parameters:

txt

printTableBR(txt)

Parameters:

txt

printTableMR(txt)

Parameters:

txt

print(txt, lbl)

Parameters:

txt

lbl

printSyminfo(sym)

Parameters:

sym

Profit EstimateLibrary "profitestimate"

Simple profit Estimatr. Engages when Position != 0

and holds until posittion is na/0...

if position changes sizes, it will update automatically and adjust.

it has an input for comission to estmate exit fees

update_avgprice(_sizewas, _delta, _pricewas, _newprice)

Get a new Average position Price

Parameters:

_sizewas : (float) the position prior

_delta : (float) the order amount

_pricewas : (float) the prior price

_newprice : (float) the price of order

Returns: New Avg Price

amount(_position, _close, _commission, _leverage, _fullqty)

Position Net Profit Net Commission, automatic on/off if position != 0

Parameters:

_position : (float) position size (total or margin size)

_close

_commission : (float) % where (0.1 = 0.1%)

_leverage : (float) optional if leveraged, default 1x

_fullqty : (bool) if position entered is tottal trade size default is margin qty (1/lev)

Returns: quote value of profit

percent(_position, _close, _commission, _leverage, _fullqty)

Position Net Profit, automatic on/off if position != 0

Parameters:

_position : (float) position size (total or margin size)

_close

_commission : (float) % where (0.1 = 0.1%)

_leverage : (float) optional if leveraged, default 1x

_fullqty : (bool) if position entered is tottal trade size, default is margin qty (1/lev)

Returns: percentage profit (1% = 1)

HeikinashiLibrary "Heikinashi"

This library calculates "Heikinashi".

calc(_o, _h, _l, _c, _my_close)

This function calculates "Heikinashi".

Parameters:

_o : open

_h : high

_l : low

_c : close

_my_close : Specify if you want to force only the closing price to a real value.

Returns: TODO: add what function returns

String Extra FunctionsLibrary "string_extras"

Additional String shortcuts, unshift and pop return the string ~without~ the first or last, so in use will still require to extract first or last character prior to overwriting a string with the output.

can be imported "as str" to work side by side with regular pine

last(_string)

last char of a string

Parameters:

_string

Returns: last char of a string

shift(_string)

string without first char

Parameters:

_string

Returns: string without first char

pop(_string)

string without last char

Parameters:

_string

Returns: string without last char

get(_string, _position)

get specific char of a string

Parameters:

_string

_position

Returns: string _string

push(_string, _char)

push to end of a string

Parameters:

_string

_char

Returns: string _string

unshift(_string, _char)

unshift char to prepend string

Parameters:

_string

_char

Returns: string _string

HSupertrendLibrary "HSupertrend"

Supertrend implementation based on harmonic patterns

hsupertrend(zProperties, pProperties, errorPercent, showPatterns, patternColor)

derives supertrend based on harmonic patterns

Parameters:

zProperties : ZigzagProperties containing Zigzag length and source array

pProperties : PatternProperties used for calculation

errorPercent : Error threshold for scanning patterns

showPatterns : Draw identified patterns structure on chart

patternColor : Color of the pattern lines to be drawn

Returns:

ZigzagProperties

ZigzagProperties contains values required for zigzag calculation

Fields:

length : Zigzag length

source : Array containing custom OHLC. If not set, array.from(high, low) is used

PatternProperties

PatternProperties are essential pattern parameters used for calculation of bullish and bearish zones

Fields:

base : Base for calculating entry and stop of pattern. Can be CD, minmax or correction. Default is CD

entryPercent : Distance from D in terms of percent of Base in the direction of pattern

stopPercent : Distance from D in terms of percent of Base in the opposite direction of pattern

useClosePrices : When set uses close price for calculation of supertrend breakout

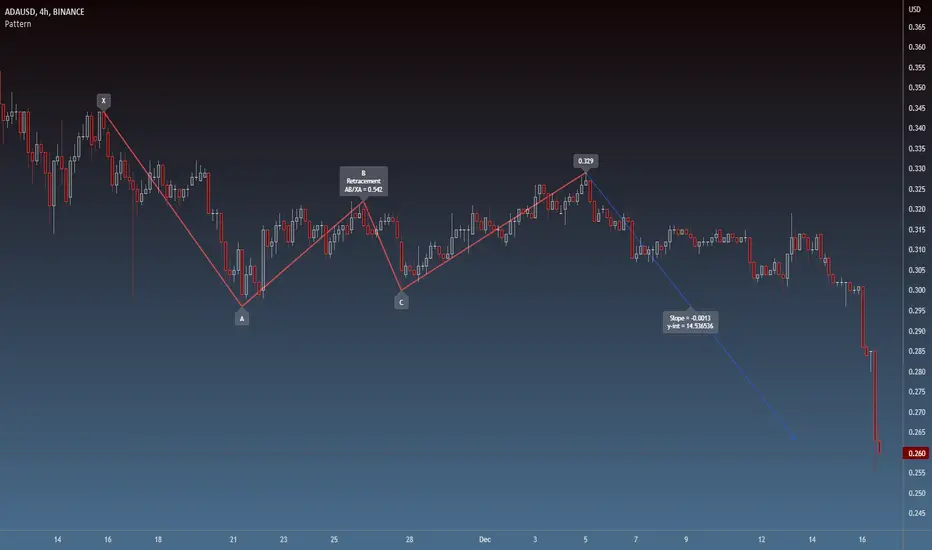

PatternLibrary "Pattern"

Pattern object definitions and functions. Easily draw and keep track of patterns, legs, and points.

Supported pattern types (as of Version 1):

Type Leg validation # legs

"xabcd" Direction 3 or 4 (point D not required)

"zigzag" Direction >= 2

"free" None >= 2

erase_label(this)

Delete the point label

Parameters:

this : Point

Returns: Void

draw_label(this, position, clr, transp, txt_clr, txt, tooltip, size)

Draw the point label

Parameters:

this : Point

position

clr

transp

txt_clr

txt

tooltip

size

Returns: line

leg_init(a, b, prev, next, line)

Initialize a pattern leg

Parameters:

a : Point A (required)

b : Point B (required)

prev : Previous leg

next : Next leg

line : Line

Returns: New instance of leg object

erase(this)

Delete the pattern leg

Parameters:

this : Leg

Returns: Void

erase(this)

Parameters:

this

draw(this, clr, style, transp, width)

Draw the pattern leg

Parameters:

this : Leg

clr : Color

style : Style ("solid", "dotted", "dashed", "arrowleft", "arrowright")

transp : Transparency

width : Width

Returns: line

draw(this, clr, style, transp, width)

Parameters:

this

clr

style

transp

width

leg_getLineTerms(this)

Get the slope and y-intercept of a leg

Parameters:

this : Leg

Returns:

leg_getPrice(this, index)

Get the price (Y) at a given bar index (X) within the leg

Parameters:

this : Leg

index : Bar index

Returns: Price (float)

pattern_init(legs, tp, name, subType, pid)

Initialize a pattern object from a given set of legs

Parameters:

legs : Array of pattern legs (required)

tp : Pattern type ("zigzag", "xabcd", or "free". dft = "free")

name : Pattern name

subType : Pattern subtype

pid : Pattern Identifier string

Returns: New instance of pattern object, if one was successfully created

pattern_init(points, tp, name, subType, pid)

Initialize a pattern object from a given set of points

Parameters:

points

tp : Pattern type ("zigzag", "xabcd", or "free". dft = "free")

name : Pattern name

subType : Pattern subtype

pid : Pattern Identifier string

Returns: New instance of pattern object, if one was successfully created

point

A point on the chart (x,y)

Fields:

x : Bar index (x coordinate)

y

label

leg

A pattern leg (point A to point B)

Fields:

a : Point A

b

deltaX

deltaY

prev

next

retrace

line

pattern

A pattern (set of at least 2 connected legs)

Fields:

legs

type

subType

name

pid

ChasinAlts_LibraryLibrary "ChasinAlts_Library"

rci(_BCgtg, _Tgtg, _close, _smaLen, _bar_index)

Parameters:

_BCgtg

_Tgtg

_close

_smaLen

_bar_index

printedBC(_time, _minPerc, _Tgtg, _lkbk)

Parameters:

_time

_minPerc

_Tgtg

_lkbk

form123(_ppLen, _BCgtg, _Tgtg, _high, _low, _close, _bar_index)

Parameters:

_ppLen

_BCgtg

_Tgtg

_high

_low

_close

_bar_index

obosCnt(_BCgtg, _Tgtg, _rci, _obosMin, _obosMax, _thresh)

Parameters:

_BCgtg

_Tgtg

_rci

_obosMin

_obosMax

_thresh

div(_thresh, _HLestLen, _Tgtg, _BCgtg, _rci, _time, _price, _LSL, _SSL, _LTP, _STP, _colorid, _long, _short)

Parameters:

_thresh

_HLestLen

_Tgtg

_BCgtg

_rci

_time

_price

_LSL

_SSL

_LTP

_STP

_colorid

_long

_short

tradeSim(_SL, _TP, _BCgtg, _Tgtg, _ppLen, _high, _low, _close, _bar_index, _time, _bull_rev, _bear_rev, _bull_obosCnt_gtg, _bear_obosCnt_gtg)

Parameters:

_SL

_TP

_BCgtg

_Tgtg

_ppLen

_high

_low

_close

_bar_index

_time

_bull_rev

_bear_rev

_bull_obosCnt_gtg

_bear_obosCnt_gtg

TrailingStopsLibrary "TrailingStops"

This library contains functions to output trailing stop lines.

f_marketStructureStop(_restartMode, _flipMode, _restartLowIn, _restartHighIn)

Parameters:

_restartMode - Defines how the stop lines persist. Allowed values are:

"Always On" - The stop lines are always present and they just reset when they're crossed.

"Flip" - The stop lines flip when they're crossed.

"Manual" - The stop lines turn off when they're crossed, and turn back on again when _restartLowIn or _restartHighIn are passed into the function as true.

_flipMode - Defines whether the stop lines are broken by wicks or closes. Allowed values are "Wick", and "Close".

_restartLowIn - If _restartMode is "Manual", passing this parameter as true restarts the Low stop line.

_restartHighIn - If _restartMode is "Manual", passing this parameter as true restarts the High stop line.

@returns - floats for the Low and High stop line.

SignalBuilderSignalBuilder

Utility for building a collection of signal values. Provides a default view for displaying signals.

Simplified API for aggregating signal values.

Flexible for use with indicators and strategies.

See the demo section for an example.

MarketStructureLibrary "MarketStructure"

This library contains functions for identifying Lows and Highs in a rule-based way, and deriving useful information from them.

f_simpleLowHigh()

This function finds Local Lows and Highs, but NOT in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

It doesn't have to be "the" high, so don't be confused.

By the rules, Local Lows and Highs must alternate. In this function they do not, so I'm calling them Simple Lows and Highs.

Simple Highs and Lows, by the above definition, can be useful for entries and stops. Because I intend to use them for stops, I want them all, not just the ones that alternate in strict order.

@param - there are no parameters. The function uses the chart OHLC.

@returns boolean values for whether this bar confirms a Simple Low/High, and ints for the bar_index of that Low/High.

f_localLowHigh()

This function finds Local Lows and Highs, in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

By the rules, Local Lows and Highs must alternate, and in this function they do.

@param - there are no parameters. The function uses the chart OHLC.

@returns boolean values for whether this bar confirms a Local Low/High, and ints for the bar_index of that Low/High.

f_enhancedSimpleLowHigh()

This function finds Local Lows and Highs, but NOT in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

By the rules, Local Lows and Highs must alternate. In this function they do not, so I'm calling them Simple Lows and Highs.

Simple Highs and Lows, by the above definition, can be useful for entries and stops. Because I intend to use them for trailing stops, I want them all, not just the ones that alternate in strict order.

The difference between this function and f_simpleLowHigh() is that it also tracks the lowest/highest recent level. This level can be useful for trailing stops.

In effect, these are like more "normal" highs and lows that you would pick by eye, but confirmed faster in many cases than by waiting for the low/high of that particular candle to be taken out on close,

because they are instead confirmed by ANY subsequent candle having its low/high exceeded. Hence, I call these Enhanced Simple Lows/Highs.

The levels are taken from the extreme highs/lows, but the bar indexes are given for the candles that were actually used to confirm the Low/High.

This is by design, because it might be misleading to label the extreme, since we didn't use that candle to confirm the Low/High..

@param - there are no parameters. The function uses the chart OHLC.

@returns - boolean values for whether this bar confirms an Enhanced Simple Low/High

ints for the bar_index of that Low/High

floats for the values of the recent high/low levels

floats for the trailing high/low levels (for debug/post-processing)

bools for market structure bias

f_trueLowHigh()

This function finds True Lows and Highs.

A True High is the candle with the highest recent high, which then has its low taken out on close by a subsequent candle (and vice-versa for True Lows).

The difference between this and an Enhanced High is that confirmation requires not just any Simple High, but confirmation of the very candle that has the highest high.

Because of this, confirmation is often later, and multiple Simple Highs and Lows can develop within ranges formed by a single big candle without any of them being confirmed. This is by design.

A True High looks like the intuitive "real high" when you look at the chart. True Lows and Highs must alternate.

@param - there are no parameters. The function uses the chart OHLC.

@returns - boolean values for whether this bar confirms an Enhanced Simple Low/High

ints for the bar_index of that Low/High

floats for the values of the recent high/low levels

floats for the trailing high/low levels (for debug/post-processing)

bools for market structure bias

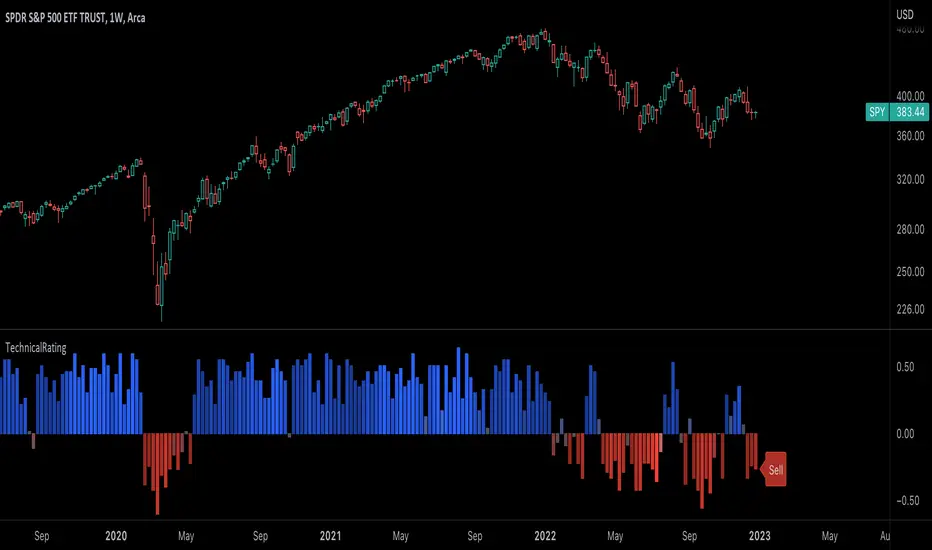

TechnicalRating█ OVERVIEW

This library is a Pine Script™ programmer’s tool for incorporating TradingView's well-known technical ratings within their scripts. The ratings produced by this library are the same as those from the speedometers in the technical analysis summary and the "Rating" indicator in the Screener , which use the aggregate biases of 26 technical indicators to calculate their results.

█ CONCEPTS

Ensemble analysis

Ensemble analysis uses multiple weaker models to produce a potentially stronger one. A common form of ensemble analysis in technical analysis is the usage of aggregate indicators together in hopes of gaining further market insight and reinforcing trading decisions.

Technical ratings

Technical ratings provide a simplified way to analyze financial markets by combining signals from an ensemble of indicators into a singular value, allowing traders to assess market sentiment more quickly and conveniently than analyzing each constituent separately. By consolidating the signals from multiple indicators into a single rating, traders can more intuitively and easily interpret the "technical health" of the market.

Calculating the rating value

Using a variety of built-in TA functions and functions from our ta library, this script calculates technical ratings for moving averages, oscillators, and their overall result within the `calcRatingAll()` function.

The function uses the script's `calcRatingMA()` function to calculate the moving average technical rating from an ensemble of 15 moving averages and filters:

• Six Simple Moving Averages and six Exponential Moving Averages with periods of 10, 20, 30, 50, 100, and 200

• A Hull Moving Average with a period of 9

• A Volume-Weighted Moving Average with a period of 20

• An Ichimoku Cloud with a conversion line length of 9, base length of 26, and leading span B length of 52

The function uses the script's `calcRating()` function to calculate the oscillator technical rating from an ensemble of 11 oscillators:

• RSI with a period of 14

• Stochastic with a %K period of 14, a smoothing period of 3, and a %D period of 3

• CCI with a period of 20

• ADX with a DI length of 14 and an ADX smoothing period of 14

• Awesome Oscillator

• Momentum with a period of 10

• MACD with fast, slow, and signal periods of 12, 26, and 9

• Stochastic RSI with an RSI period of 14, a %K period of 14, a smoothing period of 3, and a %D period of 3

• Williams %R with a period of 14

• Bull Bear Power with a period of 50

• Ultimate Oscillator with fast, middle, and slow lengths of 7, 14, and 28

Each indicator is assigned a value of +1, 0, or -1, representing a bullish, neutral, or bearish rating. The moving average rating is the mean of all ratings that use the `calcRatingMA()` function, and the oscillator rating is the mean of all ratings that use the `calcRating()` function. The overall rating is the mean of the moving average and oscillator ratings, which ranges between +1 and -1. This overall rating, along with the separate MA and oscillator ratings, can be used to gain insight into the technical strength of the market. For a more detailed breakdown of the signals and conditions used to calculate the indicators' ratings, consult our Help Center explanation.

Determining rating status

The `ratingStatus()` function produces a string representing the status of a series of ratings. The `strongBound` and `weakBound` parameters, with respective default values of 0.5 and 0.1, define the bounds for "strong" and "weak" ratings.

The rating status is determined as follows:

Rating Value Rating Status

< -strongBound Strong Sell

< -weakBound Sell

-weakBound to weakBound Neutral

> weakBound Buy

> strongBound Strong Buy

By customizing the `strongBound` and `weakBound` values, traders can tailor the `ratingStatus()` function to fit their trading style or strategy, leading to a more personalized approach to evaluating ratings.

Look first. Then leap.

█ FUNCTIONS

This library contains the following functions:

calcRatingAll()

Calculates 3 ratings (ratings total, MA ratings, indicator ratings) using the aggregate biases of 26 different technical indicators.

Returns: A 3-element tuple: ( [(float) ratingTotal, (float) ratingOther, (float) ratingMA ].

countRising(plot)

Calculates the number of times the values in the given series increase in value up to a maximum count of 5.

Parameters:

plot : (series float) The series of values to check for rising values.

Returns: (int) The number of times the values in the series increased in value.

ratingStatus(ratingValue, strongBound, weakBound)

Determines the rating status of a given series based on its values and defined bounds.

Parameters:

ratingValue : (series float) The series of values to determine the rating status for.

strongBound : (series float) The upper bound for a "strong" rating.

weakBound : (series float) The upper bound for a "weak" rating.

Returns: (string) The rating status of the given series ("Strong Buy", "Buy", "Neutral", "Sell", or "Strong Sell").

TurntLibraryLibrary "TurntLibrary"

Collection of functions created for simplification/easy referencing. Includes variations of moving averages, length value oscillators, and a few other simple functions based upon HH/LL values.

ma(source, length, type)

Apply a moving average to a float value

Parameters:

source : Value to be used

length : Number of bars to include in calculation

type : Moving average type to use ("SMA","EMA","RMA","WMA","VWAP","SWMA","LRC")

Returns: Smoothed value of initial float value

curve(src, len, lb1, lb2)

Exaggerates curves of a float value designed for use as an exit signal.

Parameters:

src : Initial value to curve

len : Number of bars to include in calculation

lb1 : (Default = 1) First lookback length

lb2 : (Default = 2) Second lookback length

Returns: Curved Average

fragma(src, len, space, str)

Average of a moving average and the previous value of the moving average

Parameters:

src : Initial float value to use

len : Number of bars to include in calculation

space : Lookback integer for second half of average

str : Moving average type to use ("SMA","EMA","RMA","WMA","VWAP","SWMA","LRC")

Returns: Fragmented Average

maxmin(x, y)

Difference of 2 float values, subtracting the lowest from the highest

Parameters:

x : Value 1

y : Value 2

Returns: The +Difference between 2 float values

oscLen(val, type)

Variable Length using a oscillator value and a corresponding slope shape ("Incline",Decline","Peak","Trough")

Parameters:

val : Oscillator Value to use

type : Slope of length curve ("Incline",Decline","Peak","Trough")

Returns: Variable Length Integer

hlAverage(val, smooth, max, min, type, include)

Average of HH,LL with variable lengths based on the slope shape ("Incline","Decline","Trough") value relative to highest and lowest

Parameters:

val : Source Value to use

smooth

max

min

type

include : Add "val" to the averaging process, instead of more weight to highest or lowest value

Returns: Variable Length Average of Highest Lowest "val"

pct(val)

Convert a positive float / price to a percentage of it's highest value on record

Parameters:

val : Value To convert to a percentage of it's highest value ever

Returns: Percentage

hlrange(x, len)

Difference between Highest High and Lowest Low of float value

Parameters:

x : Value to use in calculation

len : Number of bars to include in calculation

Returns: Difference

midpoint(x, len, smooth)

The average value of the float's Highest High and Lowest Low in a number of bars

Parameters:

x : Value to use in calculation

len

smooth : (Default=na) Optional smoothing type to use ("SMA","EMA","RMA","WMA","VWAP","SWMA","LRC")

Returns: Midpoint

TableBuilderTableBuilder is a library designed to make it easier to create tables in PineScript.

It allows you to more flexibly define the structure of a table before actually building it.

Features:

Style inheritance: styles are inherited from Table, to Column, to Row, and then Cell.

Columns are useful for propagating/reusing style but they are not required.

Add rows with different numbers of cells. The resultant number of columns in the table will be determined by the max number of cells vs the number of defined columns.

Auto text color: Instead of having to set the font color for every cell, the color is automatically determined by the luminosity of the background color.

See the 'Demo' section of the code for an example.

ColorUtility for working with colors.

Get the luminosity of a color and determine the optimal (black or white) foreground color.

ISODateTimeLibrary "ISODateTime"

getDateParts(dateStr)

Get year, month, day from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getTimeParts(dateStr)

Get hour, minute, seconds from date string.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: array of int

getUTCTimezone(dateStr)

Get UTC timezone.

Parameters:

dateStr : : ISO 8601 format, i.e. "2022-05-04T14:00:00.001000-04:00" or "2022-05-04T14:00:00Z"

Returns: string UTC timezone

Obj_XABCD_HarmonicLibrary "Obj_XABCD_Harmonic"

Harmonic XABCD Pattern object and associated methods. Easily validate, draw, and get information about harmonic patterns. See example code at the end of the script for details.

init_params(pct_error, pct_asym, types, w_e, w_p, w_d)

Create a harmonic parameters object (used by xabcd_harmonic object for pattern validation and scoring).

Parameters:

pct_error : Allowed % error of leg retracement ratio versus the defined harmonic ratio

pct_asym : Allowed leg length/period asymmetry % (a leg is considered invalid if it is this % longer or shorter than the average length of the other legs)

types : Array of pattern types to validate (1=Gartley, 2=Bat, 3=Butterfly, 4=Crab, 5=Shark, 6=Cypher)

w_e : Weight of ratio % error (used in score calculation, dft = 1)

w_p : Weight of PRZ confluence (used in score calculation, dft = 1)

w_d : Weight of Point D / PRZ confluence (used in score calculation, dft = 1)

Returns: harmonic_params object instance. It is recommended to store and reuse this object for multiple xabcd_harmonic objects rather than creating new params objects unnecessarily.

init(xX, xY, aX, aY, bX, bY, cX, cY, dX, dY, params, tp, p)

Initialize an xabcd_harmonic object instance.

If the pattern is valid, an xabcd_harmonic object instance is returned. If you want to specify your

own validation and scoring parameters, you can do so by passing a harmonic_params object (params).

Or, if you prefer to do your own validation, you can explicitly pass the harmonic pattern type (tp)

and validation will be skipped. You can also pass in an existing xabcd_harmonic instance if you wish

to re-initialize it (e.g. for re-validation and/or re-scoring).

Parameters:

xX : Point X bar index

xY : Point X price/level

aX : Point A bar index

aY : Point A price/level

bX : Point B bar index

bY : Point B price/level

cX : Point C bar index

cY : Point C price/level

dX : Point D bar index

dY : Point D price/level

params : harmonic_params used to validate and score the pattern. Validation will be skipped if a type (tp) is explicitly passed in.

tp : Pattern type

p : xabcd_harmonic object instance to initialize (optional, for re-validation/re-scoring)

Returns: xabcd_harmonic object instance if a valid harmonic, else na

get_name(p)

Get the pattern name

Parameters:

p : Instance of xabcd_harmonic object

Returns: Pattern name (string)

get_symbol(p)

Get the pattern symbol

Parameters:

p : Instance of xabcd_harmonic object

Returns: Pattern symbol (1 byte string)

get_pid(p)

Get the Pattern ID. Patterns of the same type with the same coordinates will have the same Pattern ID.

Parameters:

p : Instance of xabcd_harmonic object

Returns: Pattern ID (string)

set_target(p, target, target_lvl, calc_target)

Set value for a target. Use the calc_target parameter to automatically calculate the target for a specific harmonic ratio.

Parameters:

p : Instance of xabcd_harmonic object

target : Target (1 or 2)

target_lvl : Target price/level (required if calc_target is not specified)

calc_target : Target to auto calculate (required if target is not specified)

Options:

Returns: Target price/level (float)

erase_pattern(p)

Erase the pattern

Parameters:

p : Instance of xabcd_harmonic object

Returns: p

draw_pattern(p)

Draw the pattern

Parameters:

p : Instance of xabcd_harmonic object

Returns: Pattern lines

erase_label(p)

Erase the pattern label

Parameters:

p : Instance of xabcd_harmonic object

Returns: p

draw_label(p, txt, tooltip, clr, txt_clr)

Draw the pattern label. Default text is the pattern name.

Parameters:

p : Instance of xabcd_harmonic object

txt : Label text

tooltip : Tooltip text

clr : Label color

txt_clr : Text color

Returns: Label

harmonic_params

Validation and scoring parameters for a Harmonic Pattern object (xabcd_harmonic)

Fields:

pct_error : Allowed % error of leg retracement ratio versus the defined harmonic ratio

pct_asym

types

w_e

w_p

w_d

xabcd_harmonic

Harmonic Pattern object

Fields:

bull : Bullish pattern flag

tp

xX

xY

aX

aY

bX

bY

cX

cY

dX

dY

r_xb

re_xb

r_ac

re_ac

r_bd

re_bd

r_xd

re_xd

score

score_eAvg

score_prz

score_eD

prz_bN

prz_bF

prz_xN

prz_xF

t1Hit : Target 1 flag

t1

t2Hit

t2

sHit : Stop flag

stop : Stop level

entry : Entry level

eHit

eX

eY

pLines

pLabel

pid

params

Signal AnalyzerThis library contains functions that try to analyze trading signals performance.

Like the % of average returns after a long or short signal is provided or the number of times that signal was correct, in the inmediate 2 candles after the signal.

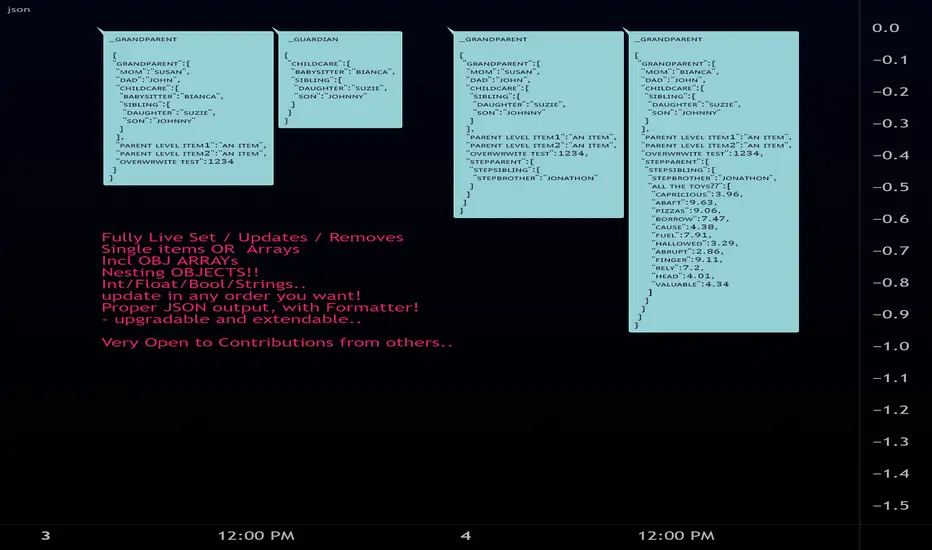

jsonLibrary "json"

JSON Easy Object Create/stringiffy

Functions to add/write JSON

new (name , kind) -> object

set (_item , _obj , _key ) -> key index for parent object's array

add (_obj , _key , _item ) -> key index for parent object's array

write (object , kind ) -> stringified object // (enter kind to cut off key )

============================================

obj

obj Object storage container/item

Fields:

key : (string ) item name

kind : (string ) item's type(for writing)

item : (string ) item (converted to string)

keys : (string ) keys of all sub-items and objects

items : (obj ) nested obj off individual subitems (for later...)

============================================

new(_name, _kind)

create multitype object

Parameters:

_name : (string) Name off object

_kind : (string) Preset Type (_OBJECT if a container item)

Returns: object container/item 2-in-1

============================================

add(_item, _obj, _key)

Set item to object obj item (same as set, prep for future Pine methods)

Parameters:

_item : ( int / float / bool / string )

_obj : (obj multi-type-item object)

_key : ( string )

set(_item, _obj, _key)

Set item to object obj item (same as add, prep for future Pine methods)

Parameters:

_item : ( int / float / bool / string )

_obj : (obj multi-type-item object)

_key : ( string )

addstore(_parent, _child)

Add a object as a subobject to storage (Future upgrade to write/edit)

Parameters:

_parent : to insert obj into

_child : to be inserted

setstore(_child, _parent)

Add a object as a subobject to storage (Future upgrade to write/edit)

Parameters:

_child : to be inserted

_parent : to insert obj into

add(_parent, _child)

Add a object as a string rendered item

Parameters:

_parent : to insert obj into

_child : to be inserted

set(_child, _parent)

Add a object as a string rendered item

Parameters:

_child : to be inserted

_parent : to insert obj into

============================================

write(_object, _key, _itemname)

Write object to string Object

Parameters:

_object : (obj)

_key : (array<(string/int)> )/(string)

_itemname : (string)

Returns: stringified flattened object.

clean_output(_str)

Clean JSON final output

Parameters:

_str : string json item

Returns: cleaned string

WelcomeUDT█ OVERVIEW

This is a simplest example of user-defined types (UDT) or objects , which simplify as alternative to hello world.

█ CREDITS

Tradingview

█ USAGE

These are the types used during initializations, commonly variables.

export type Settings

int bar

float price

string phrase

...

Example of library function to print out label.

export printLabel(Settings setup) =>

if setup.variable

var label lab = na

label.delete(lab)

lab := label.new(setup.bar, setup.price, setup.phrase, color = setup.bg)

else

label.new(setup.bar, setup.price, setup.phrase, color = setup.bg)

Usage of types

Settings setup = Settings.new(bar_index , priceInput, phraseInput, colorInput, variableInput)

Alternative way to write types

Settings setup = Settings.new(

bar = bar_index ,

price = priceInput,

phrase = phraseInput,

variable = variableInput)

Usage of types into custom function / library function.

printLabel(setup)

printLabel(Settings)

Print out label

Parameters:

Settings : types

Returns: Label object

Settings

Initialize type values

Fields:

bar : X position for label

price : Y position for label

phrase : Text for label

bg : Color for label

variable : Boolean for enable new line and delete line