NY VIX Channel Trend US Futures Day Trade StrategyNY VIX Channel Trend Strategy

Summary in one paragraph

Session anchored intraday strategy for index futures such as ES and NQ on one to fifteen minute charts. It acts only after the first configurable window of New York Regular Trading Hours and uses a VIX derived daily implied move to form a realistic channel from the session open. Originality comes from using a pure implied volatility yardstick as portable support and resistance, then committing in the direction of the first window close relative to the open. Add it to a clean chart and trade the simple visuals. For conservative alerts use on bar close.

Scope and intent

• Markets. Index futures ES and NQ

• Timeframes. One to thirty minutes

• Default demo. ES1 on five minutes

• Purpose. Provide a portable intraday yardstick for entries and exits without curve fitting

• Limits. This is a strategy. Orders are simulated on standard candles

Originality and usefulness

• Unique concept. A VIX only channel anchored at 09:30 New York plus a single window trend test

• Addresses. False urgency at session open and unrealistic bands from arbitrary multipliers

• Testability. Every input is visible and the channel is plotted so users can audit behavior

• Portable yardstick. Daily implied move equals VIX percent divided by square root of two hundred fifty two

• Protected status. None. Method and use are fully disclosed

Method overview in plain language

Take the daily VIX or VIX9D value, convert it to a daily fraction by dividing by square root of two hundred fifty two, then anchor a symmetric channel at the New York session open. Observe the first N minutes. If that window closes above the open the bias is long. If it closes below the open the bias is short. One trade per session. Exits occur at the channel boundary or at a bracket based on a user selected VIX factor. Positions are closed a set number of minutes before the session ends.

Base measures

Return basis. The daily implied move unit equals VIX percent divided by square root of two hundred fifty two and serves as the distance unit for targets and stops.

Components

• VIX Channel. Top, mid, bottom lines anchored at 09:30 New York. No extra multipliers

• Window Trend. Close of the first N minutes relative to the session open sets direction

• Risk Bracket. Take profit and stop loss equal to VIX unit times user factor

• Session Window. Uses the exchange time of the chart

Fusion rule

Minimum gates count equals one. The trade only arms after the window has elapsed and a direction exists. One entry per session.

Signal rule

• Long when the window close is above the session open and the window has completed

• Short when the window close is below the session open and the window has completed

• Exit on channel touch. Long exits at the top. Short exits at the bottom

• Flat thirty minutes before the session close or at the user setting

Inputs with guidance

Setup

• Use VIX9D. Width source. Typical true for fast tone or false for baseline

• Use daily OPEN. Toggle for sensitivity to overnight changes

Logic

• Window minutes. Five to one hundred twenty. Larger values delay entries and reduce whipsaw

• VIX factor for TP. Zero point five to two. Raising it widens the profit target

• VIX factor for SL. Zero point five to two. Raising it widens the stop

• Exit minutes before close. Fifteen to ninety. Raising it exits earlier

Properties visible in this publication

• Initial capital one hundred thousand USD

• Base currency USD

• request.security uses lookahead off

• Commission cash per contract two point five $ per each contract. Slippage one tick

• Default order size method FIXED with value one contract. Pyramiding zero. Process orders on close ON. Bar magnifier OFF. Recalculate after order is filled OFF. Calc on every tick ON

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategy uses standard candles.

Honest limitations and failure modes

Economic releases and thin liquidity can break the channel. Very quiet regimes can reduce signal contrast. Session windows follow the exchange time of the chart. If both stop and target can be hit within one bar, assume stop first for conservative reading without bar magnifier.

Works best in liquid hours of New York RTH. Very large gaps and surprise news may exceed the implied channel. Always validate on the symbols you trade.

Entries and exits

• Entry logic. After the first window, go long if the window close is above the session open, go short if below

• Exit logic. Long exits at the channel top or at the take profit or stop. Short exits at the channel bottom or at the take profit or stop. Flat before session close by the configured minutes

• Risk model. Initial stop and target based on the VIX unit times user factors. No trail and no break even. No cooldown

• Tie handling. Treat as stop first for conservative interpretation

Position sizing

Fixed size one contract per trade. Target risk per trade should generally remain near one percent of account equity. Risk is based on the daily volatility value, the max loss from the tests for one year duration with 5min chart was 4%, while the avg loss was below <1% of the total capital.

If you have any questions please let me know. Thank you for coming by !

Historical Volatility

HV Spike Strategy (HVP + OR Breakout + Reversal + TP/SL Modes)Here is a script that I tried to make it simple, although it has several parameters, I will try to explain, here we go:

Logic: Open Range Breakout: otherwise knows as First Candle Rule, usually used for the first candle in the opening of a market session, in my strategy there is an option to use it even for Crypto that operate 24/7, how to do that? Simply by detecting Volatility from the HVP (Historical Volatility Percentile). Then the ORB logic kicks in and the first candle with high volatility gives the ranges for the trades. The proper HVP Activation Threshold has to be selected for each currency pair/index/crypto in order to have maximum profit.

Enter a trade: when the price goes 100% above/below the First Candle Rule Range. That way it is filtering fake breakouts. Also if the price reverses back into the range the strategy takes the opposite trade.

Exit a trade: SL/TP By percentage or ATR, selection in the input menu.

My intention is to avoid using lagging indicators or guessing of Price Action, purely Bull/Bear indication by the first candle.

I hope you find this helpful! Wishing all successful Trades!

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Multi-Step Vegas SuperTrend - strategy [presentTrading]Long time no see! I am back : ) Please allow me to gain some warm-up.

█ Introduction and How it is Different

The "Vegas SuperTrend Strategy" is an enhanced trading strategy that leverages both the Vegas Channel and SuperTrend indicators to generate buy and sell signals.

What sets this strategy apart from others is its dynamic adjustment to market volatility and its multi-step take profit mechanism. Unlike traditional single-step profit-taking approaches, this strategy allows traders to systematically scale out of positions at predefined profit levels, thereby optimizing their risk-reward ratio and maximizing potential gains.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The Vegas SuperTrend Strategy combines the strengths of the Vegas Channel and SuperTrend indicators to identify market trends and generate trade signals. The following subsections delve into the details of how each component works and how they are integrated.

🔶 Vegas Channel Calculation

The Vegas Channel is based on a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified period. The channel is defined by upper and lower bounds that are dynamically adjusted based on market volatility.

Simple Moving Average (SMA):

SMA_vegas = (1/N) * Σ(Close_i) for i = 0 to N-1

where N is the length of the Vegas Window.

Standard Deviation (STD):

STD_vegas = sqrt((1/N) * Σ(Close_i - SMA_vegas)^2) for i = 0 to N-1

Vegas Channel Upper and Lower Bounds:

VegasChannelUpper = SMA_vegas + STD_vegas

VegasChannelLower = SMA_vegas - STD_vegas

The details are here:

🔶 Trend Detection and Trade Signals

The strategy determines the current market trend based on the closing price relative to the SuperTrend bounds:

Market Trend:

MarketTrend = 1 if Close > SuperTrendPrevLower

-1 if Close < SuperTrendPrevUpper

Previous Trend otherwise

Trade signals are generated when there is a shift in the market trend:

Bullish Signal: When the market trend shifts from -1 to 1.

Bearish Signal: When the market trend shifts from 1 to -1.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates a multi-step take profit mechanism that allows for partial exits at predefined profit levels. This helps in locking in profits gradually and reducing exposure to market reversals.

Take Profit Levels:

The take profit levels are calculated as percentages of the entry price:

TakeProfitLevel_i = EntryPrice * (1 + TakeProfitPercent_i/100) for long positions

TakeProfitLevel_i = EntryPrice * (1 - TakeProfitPercent_i/100) for short positions

Multi-steps take profit local picture:

█ Trade Direction

The trade direction can be customized based on the user's preference:

Long: The strategy only takes long positions.

Short: The strategy only takes short positions.

Both: The strategy can take both long and short positions based on the market trend.

█ Usage

To use the Vegas SuperTrend Strategy, follow these steps:

Configure Input Settings:

- Set the ATR period, Vegas Window length, SuperTrend Multiplier, and Volatility Adjustment Factor.

- Choose the desired trade direction (Long, Short, Both).

- Enable or disable the take profit mechanism and set the take profit percentages and amounts for each step.

█ Default Settings

The default settings of the strategy are designed to provide a balanced approach to trading. Below is an explanation of each setting and its effect on the strategy's performance:

ATR Period (10): This setting determines the length of the ATR used in the SuperTrend calculation. A longer period smoothens the ATR, making the SuperTrend less sensitive to short-term volatility. A shorter period makes the SuperTrend more responsive to recent price movements.

Vegas Window Length (100): This setting defines the period for the Vegas Channel's moving average. A longer window provides a broader view of the market trend, while a shorter window makes the channel more responsive to recent price changes.

SuperTrend Multiplier (5): This base multiplier adjusts the sensitivity of the SuperTrend to the ATR. A higher multiplier makes the SuperTrend less sensitive, reducing the frequency of trade signals. A lower multiplier increases sensitivity, generating more signals.

Volatility Adjustment Factor (5): This factor dynamically adjusts the SuperTrend multiplier based on the width of the Vegas Channel. A higher factor increases the sensitivity of the SuperTrend to changes in market volatility, while a lower factor reduces it.

Take Profit Percentages (3.0%, 6.0%, 12.0%, 21.0%): These settings define the profit levels at which portions of the trade are exited. They help in locking in profits progressively as the trade moves in favor.

Take Profit Amounts (25%, 20%, 10%, 15%): These settings determine the percentage of the position to exit at each take profit level. They are distributed to ensure that significant portions of the trade are closed as the price reaches the set levels, reducing exposure to reversals.

Adjusting these settings can significantly impact the strategy's performance. For instance, increasing the ATR period or the SuperTrend multiplier can reduce the number of trades, potentially improving the win rate but also missing out on some profitable opportunities. Conversely, lowering these values can increase trade frequency, capturing more short-term movements but also increasing the risk of false signals.

Portfolio Performance - Effects of RebalancingFunction:

- Can be used to evaluate the performance of a portfolio containing 2 assets over a set time interval

- Shows the % return of the portfolio over the time interval defined by the user

- Includes a threshold rebalancing algorithm to show the effects that rebalancing has on the portfolio over the long term

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time assuming that the user would rebalance the portfolio when asset weights crossed a threshold

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. AMEX:SPY

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the initial investment of the portfolio. Default setting is $100,000

- Define the second asset to be included in the portfolio. e.g. BATS:AGG

- The strategy comes pre-populated with a portfolio that has a weight of 80% asset 1 and 20% asset 2. i.e. 80% AMEX:SPY and 20% BATS:AGG if the symbols mentioned above were chosen

- The 7 lines show the weighted % return of each portfolio over the time period defined by the user

- Each line (except the blue) is the return based on a different rebalancing threshold. The default settings are 1%, 2.5%, 5%, 10%, 15%, 20%, 30%

- The blue line is the % return of a portfolio that was made up of 100% asset 1 over the time interval. i.e. 100% AMEX:SPY

- Asset weights and rebalancing thresholds are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

Portfolio Performance - 2 AssetsFunction:

- Can be used to evaluate the performance of portfolios containing 2 assets over a set time interval

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time

- Shows the % return of each portfolio over the time interval defined by the user

- Capable of showing the risk adjusted % return of each portfolio over the time interval defined by the user (setting turned off by default)

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. NASDAQ:BND

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the second asset to be included in the portfolio. e.g. AMEX:VOO

- The strategy comes pre-populated with 6 portfolios with the most common stock/bond weightings (100% stocks/0% bonds, 80% stocks/20% bonds, 60% stocks/40% bonds, et cetera)

- The 6 lines show the weighted % return of each portfolio over the time period defined by the user

- All asset weights are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

- There are 6 plots that show the risk adjusted returns of each portfolio (setting turned off by default)

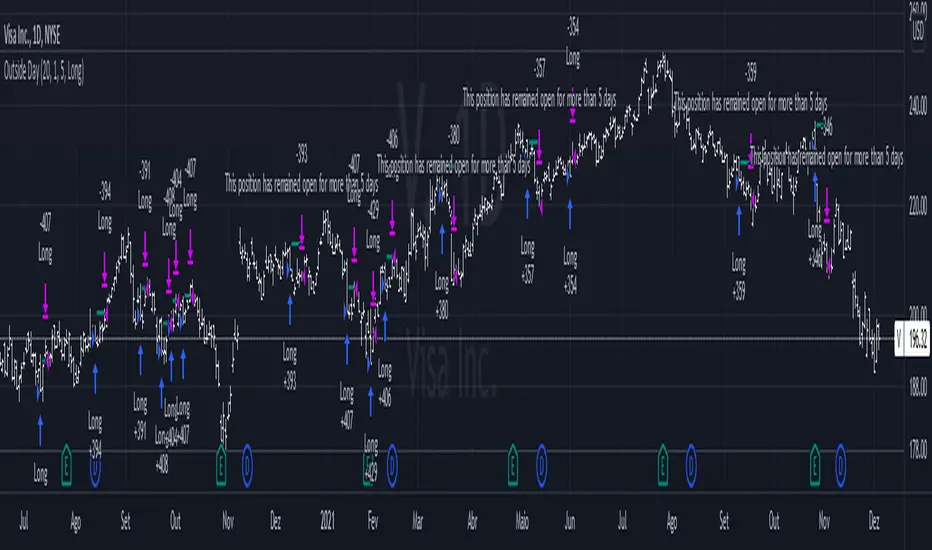

Outside DayThis strategy is taken from Perry Kaufman's book "Trading System and Methods".

You can enter on the direction of the candle, or opposite to it. I find that the opposite tends to yield better results in volatile assets, allowing a better reward to risk ratio. There is no stop loss in this strategy, only a fixed take profit and a time limitation.

Does your trading pass the seasonality test?Are you consistently beating the standard "Buy and Hold" benchmark?

Check your performance against the next most common strategy:

Buy at the start of the holiday season and close in the new year.

By default, the strategy starts with $100,000 and risks 25% of the account on each swing trade.

Commission is set to be 0.5% of each trade.

You can tweak the direction of trades by adjusting the first setting.

Tweak the holding period by changing the Entry and Exit months.

Red plot: Balance of account

Orange plot: Equity of account

2HLA very simple, almost naive strategy, in which you buy on the lowest of the two previous candles and sell at the highest of the two previous candles. You can configure these highest and lowest lenght, in some assets two is too small of a number to make profit. You can also configure to exit the position after X, and I found that 7 (which is a week of working days) is a good number for that.

This is strategy is intended to be used as a swing trade. Your capital needs to be high enough so that it can pay the operaitonal costs, and reach it's target with a reasonable profit.

Since this is a volatility based strategy, assets that are more liquid won't work properly.

Toby Crabel's narrow range with historical volatility1. Find bar with the smallest narrow range for a chosen period. Use hvol for filter.

2. Place stop-order for long position at previous high and stop-order for short at previous low to catch breakout in any direction.

3. Take profit on the next bar.

Historical Volatility Strategy Backtest Strategy buy when HVol above BuyBand and close position when HVol below CloseBand.

Markets oscillate from periods of low volatility to high volatility

and back. The author`s research indicates that after periods of

extremely low volatility, volatility tends to increase and price

may move sharply. This increase in volatility tends to correlate

with the beginning of short- to intermediate-term moves in price.

They have found that we can identify which markets are about to make

such a move by measuring the historical volatility and the application

of pattern recognition.

The indicator is calculating as the standard deviation of day-to-day

logarithmic closing price changes expressed as an annualized percentage.

Please, use it only for learning or paper trading. Do not for real trading.