Cryptocurrency SentimentOverview

This script focuses on calculating and visualizing the sentiment difference between LONG positions and SHORT positions for a selected cryptocurrency pair on the Bitfinex exchange. It provides a clean and clear visual representation of the sentiment, helping traders analyze market behavior.

Key Features

Dynamic Symbol Selection:

The script automatically detects the cryptocurrency symbol from the chart (syminfo.basecurrency) and dynamically constructs the LONGS and SHORTS ticker symbols.

Works seamlessly for pairs like BTCUSD, ETHUSD, and others available on Bitfinex.

Sentiment Calculation:

The sentiment difference is calculated as:

Sentiment Difference=−1×(100− SHORTS/LONGS ×100)

LONGS : The total number of long positions.

SHORTS : The total number of short positions.

If SHORTS is 0, the value is safely skipped to avoid division errors.

Color Coding:

The script visually highlights the sentiment difference:

Green Line: Indicates that LONG positions are dominant (bullish sentiment).

Red Line: Indicates that SHORT positions are dominant (bearish sentiment).

Zero Reference Line:

A gray horizontal line at 0 helps users quickly identify the transition between bullish (above zero) and bearish (below zero) sentiment.

How It Works

Fetching Data:

The script uses request.security to fetch LONGS and SHORTS data at the current chart timeframe (timeframe.period) for the dynamically generated Bitfinex tickers.

Handling Data:

Missing or invalid data (NaN) is filtered out to prevent errors.

Extreme spikes or irregular values are safely avoided.

Visualization:

The sentiment difference is plotted with dynamic color coding:

Green when LONGS > SHORTS (bullish sentiment).

Red when SHORTS > LONGS (bearish sentiment).

Benefits

Market Sentiment Insight: Helps traders quickly identify if the market is leaning towards bullish or bearish sentiment based on actual LONG and SHORT position data.

Dynamic and Adaptive: Automatically adjusts to the selected cryptocurrency symbol on the chart.

Clean Visualization: Focuses solely on sentiment difference with color-coded signals, making it easy to interpret.

Best Use Cases

Trend Confirmation: Use the sentiment difference to confirm trends during bullish or bearish moves.

Market Reversals: Identify potential reversals when sentiment shifts from positive (green) to negative (red) or vice versa.

Sentiment Monitoring: Monitor the overall market bias for cryptocurrencies like BTC, ETH, XRP, etc., in real-time.

Sample Chart Output

Above Zero → Green Line: Bullish sentiment dominates.

Below Zero → Red Line: Bearish sentiment dominates.

Zero Line → Transition point for shifts in sentiment.

Cryptomarket

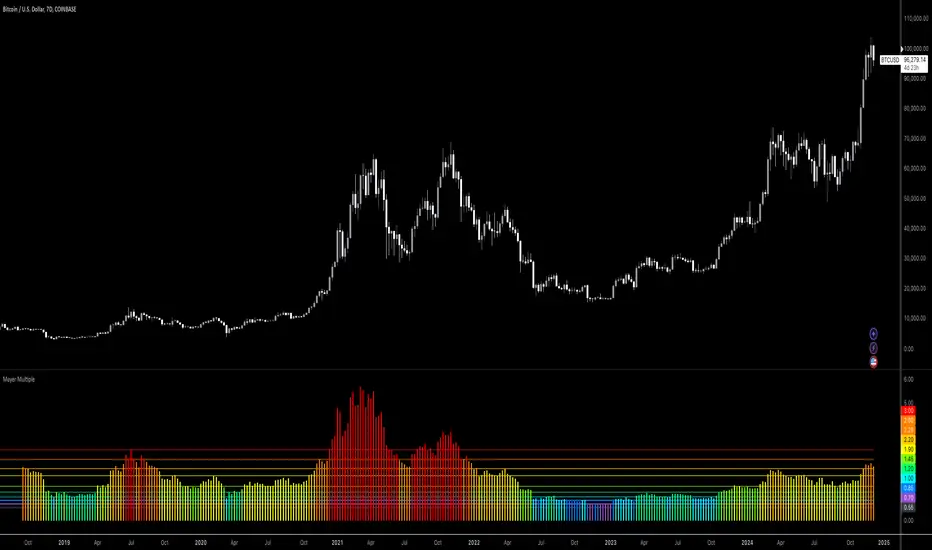

Bitcoin: Mayer MultipleMayer Multiple Indicator

The Mayer Multiple is a powerful tool designed to help traders assess market conditions and identify optimal buying or selling opportunities. It calculates the ratio between the current price and its 200-day simple moving average (SMA), visualizing key thresholds that indicate value zones, caution areas, and overheated markets.

Key Features:

Dynamic Market Zones: Clearly marked levels like "Smash Buy," "Boost DCA," and "Extreme Euphoria" to guide your trading decisions.

Customizable Input: Adjust the SMA length to fit your strategy.

Color-Coded Signals: Intuitive visualization of market sentiment for quick analysis.

Comprehensive Thresholds: Historical insights into price behavior with plotted reference levels based on probabilities.

This indicator is ideal for traders aiming to enhance their long-term strategies and improve decision-making in volatile markets. Use it to gain an edge in identifying potential turning points and managing risk effectively.

DCA Valuation & Unrealized GainsThis Pine Script for TradingView calculates and visualizes the relationship between a Dollar Cost Average (DCA) price and the All-Time High (ATH) price for over 50 different cryptocurrencies. Here's what it does:

1. Inputs for DCA Prices:

- Users can manually input DCA prices for specific cryptocurrencies (e.g., BTC, ETH, BNB).

2. Dynamic ATH Calculation:

- Dynamically calculates the ATH price for the current asset using the highest price in the chart's loaded data and persists this value across bars.

3. Percentage Change from DCA to ATH:

- Computes the percentage gain from the DCA price to the ATH price.

4. Visualizations:

- Draws a line at the DCA price and the ATH price, both extended to the right.

- Adds an arrow pointing from the DCA price to the ATH, offset by 10 bars into the future.

- Displays labels for:

- The percentage gain from DCA to ATH.

- "No DCA Configured" if no valid DCA price is set for the asset.

5. Color Coding:

- Labels and arrows are color-coded to indicate positive or negative percentage changes:

- Green for gains.

- Red for losses.

6. Adaptability:

- The script dynamically adjusts to the current asset based on its ticker and uses the corresponding DCA price.

This functionality provides traders with clear insights into their investment's performance relative to its ATH, aiding in decision-making.

-----

To add a new asset to the script:

1. Define the DCA Input: Add a new input for the asset's DCA price using the `input.float` function. For example:

dcaPriceNEW = input.float(title="NEW DCA Price", defval=0.1, tooltip="Set the DCA price for NEW")

2. Add the Asset Logic: Include a conditional check for the new asset in the ticker matching logic:

if str.contains(currentAsset, "NEW") and dcaPriceNEW != 0

dcaPrice := dcaPriceNEW

Where NEW is the ticker symbol of the asset you're adding.

NOTE: SOLO had to be put before SOL because otherwise the indicator was pulling the DCA price from SOL even on the SOLO chart. If you have a similar issue, try that fix.

Adding an asset requires only these two changes. Once done, the script dynamically incorporates the new asset into its calculations and visualizations.

Cryptocurrency StrengthMulti-Currency Analysis: Monitor up to 19 different currencies simultaneously, including major pairs like USD, EUR, JPY, and GBP, as well as emerging market currencies such as CNY, INR, and BRL.

Customizable Display: Easily toggle the visibility of each currency and personalize their colors to suit your preferences, allowing for a tailored analysis experience.

Real-Time Strength Measurement: The indicator calculates and displays the relative strength of each currency in real-time, helping you identify potential trends and trading opportunities.

Clear Visual Representation: With color-coded lines and a dynamic legend, the indicator presents complex currency relationships in an easy-to-understand format.

Advantages

Comprehensive Market View: Gain insights into the broader forex market dynamics by analyzing multiple currencies at once.

Trend Identification: Quickly spot strong and weak currencies, aiding in the identification of potential trending pairs.

Divergence Detection: Use the indicator to identify divergences between currency strength and price action, potentially signaling reversals or continuation patterns.

Flexible Time Frames: Apply the indicator across various time frames to align with your trading strategy, from intraday to long-term analysis.

Enhanced Decision Making: Make more informed trading decisions by understanding the relative strength of currencies involved in your trades.

Unique Qualities

TSI-Based Calculations: Utilizes the True Strength Index for a more nuanced and responsive measure of currency strength compared to simple price-based indicators.

Adaptive Legend: The indicator features a dynamic legend that updates automatically based on the selected currencies, ensuring a clutter-free and relevant display.

Emerging Market Inclusion: Unlike many standard currency strength indicators, this tool includes a wide range of emerging market currencies, providing a truly global perspective.

Whether you're a seasoned forex trader or just starting out, this Currency Strength Indicator offers valuable insights that can complement your existing strategy and potentially improve your trading outcomes. Its combination of comprehensive analysis, customization options, and clear visualization makes it an essential tool for navigating the complex world of currency trading.

RSI Strategy With TP/SL - Lower TFThis Pine Script strategy integrates the Relative Strength Index (RSI) for trade signals with user-defined Take Profit (TP) and Stop Loss (SL) levels. It's designed for flexible application in different market conditions, offering long, short, or dual-direction trading.

Short Description

The strategy uses the RSI to identify overbought and oversold market conditions:

Buy signal: When RSI drops below the specified "Buy Level."

Sell signal: When RSI rises above the "Sell Level."

Additionally, it manages risk and profit targets with:

Take Profit (TP): Exits trades when the price reaches a percentage gain.

Stop Loss (SL): Exits trades to limit losses if the price falls by a certain percentage.

The strategy is versatile and includes options for visualizing performance, monthly profit/loss data, and detailed trade metrics.

How to Use

Set Parameters:

RSI Period: Default is 14. Adjust based on your analysis.

RSI Buy/Sell Levels:

Buy Level: Default is 40. Consider higher levels for conservative entries.

Sell Level: Default is 60. Lower this for earlier exits.

Take Profit (%): Set your profit target (default: 5%).

Stop Loss (%): Set your risk tolerance (default: 2%).

Trade Direction: Choose "Long Only," "Short Only," or "Both."

Interpret Signals:

Buy signals appear when RSI crosses below the buy threshold.

Sell signals appear when RSI crosses above the sell threshold.

Risk Management:

The strategy dynamically calculates TP and SL levels for each trade.

TP/SL is applied using the percentage input based on the entry price.

Monitor Performance:

Review trade statistics in the "Strategy Tester."

Use the monthly performance table to track P/L across months.

Customize Alerts:

Alerts for buy, sell, TP, and SL events can be used to automate notifications.

Key Features

Configurable RSI Settings: Adaptable to various market conditions.

Risk Management: Built-in TP and SL management.

Customizable Trade Direction: Tailored for long-only, short-only, or both directions.

Monthly P/L Table: Visualizes performance trends over time.

Alerts: Notifies when critical trade events occur.

Please do your own research before ase this to your real trading.

SMA Fibonacci Rainbow Waves[FibonacciFlux]SMA Fibonacci Rainbow Waves

Overview

The SMA Fibonacci Rainbow Waves script is designed for traders who seek to blend simplicity with complexity in their trading strategies. By leveraging multiple Simple Moving Averages (SMAs) weighted by Fibonacci numbers, this indicator provides a nuanced view of price action, allowing traders to capture essential market dynamics while filtering out unnecessary noise.

Key Features

1. Multiple Simple Moving Averages (SMA)

- The indicator employs a series of SMAs to represent both short-term and long-term trends, providing a comprehensive view of market sentiment.

- Each SMA helps identify critical price levels that serve as support and resistance, particularly the purple Fibonacci SMA, which can be pivotal for limit entries. Traders positioned at this level can initiate stop-loss hunts at the institutional level, potentially achieving risk-reward ratios exceeding 30.

2. Fibonacci Weighting

- By applying Fibonacci principles to the SMAs, the indicator enhances adaptability to market conditions.

- This unique approach allows traders to pinpoint significant support and resistance levels within Fibonacci layers, enabling them to anticipate market movements effectively.

3. Dynamic Support and Resistance Levels

- The SMA Fibonacci Rainbow Waves indicator identifies key price levels that act as support and resistance based on Fibonacci layers.

- For instance, on the hourly chart, these levels function as reliable zones for traders to watch for potential reversals, while on the 15-minute chart, a consolidation within the rainbow pocket followed by expansion can signal lucrative trading opportunities.

4. Visual Clarity with Color Coding

- Each SMA is assigned a distinct color, making it easy to differentiate between the various levels on the chart.

- Fills between SMAs visually represent zones of confluence, enhancing the analysis of potential trading opportunities.

Signal Generation and Alerts

- The indicator generates buy and sell signals based on the interactions of the SMAs, providing clear entry and exit points.

- Customizable alerts notify traders of significant market changes, allowing for timely reactions to evolving conditions.

Benefits

1. Simplified Trading Approach

- Traders can focus on significant market trends without distraction, enhancing decision-making efficiency and reducing emotional trading.

2. Flexibility Across Timeframes

- The indicator operates effectively across multiple timeframes, allowing traders to apply its principles in various scenarios, from scalping to longer-term strategies.

3. Enhanced Market Insights

- The combination of multiple SMAs and Fibonacci weighting offers a comprehensive view of market trends, helping traders identify lucrative opportunities that may be overlooked.

4. Bridging Simplicity and Complexity

- This indicator elegantly addresses the contradictions in trading psychology, allowing traders to maintain clarity while navigating complex market dynamics.

Conclusion

The SMA Fibonacci Rainbow Waves script is an essential tool for traders seeking to streamline their analysis while effectively capturing market movements. By integrating Fibonacci principles with multiple SMAs, this indicator empowers traders to follow trends confidently. Its design makes it invaluable for both novice and experienced traders, revealing entry points often missed by traditional indicators.

Open Source Collaboration

This script is available as an open-source project on TradingView, inviting contributions from the global trading community to enhance its functionality. Collaboration ensures it remains a valuable resource for market participants.

Important Note

As with any trading tool, thorough analysis and risk management are crucial when using this indicator. Past performance does not guarantee future results, and traders should always prepare for potential market fluctuations.

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.

- Longer periods (e.g., 300 bars): Focuses on longer-term trends, reducing the frequency of trades and focusing only on significant deviations.

🔶 Standard Deviation Multiplier (2.618):

The multiplier controls how wide the Bollinger Bands are around the moving average. By default, the bands are set at 2.618 standard deviations away from the average, ensuring that only significant deviations trigger trades.

- Higher multipliers (e.g., 3.0): Require a more extreme deviation to trigger trades, reducing trade frequency but potentially increasing the accuracy of signals.

- Lower multipliers (e.g., 2.0): Make the bands narrower, increasing the number of trade signals but potentially decreasing their reliability.

🔶 Take-Profit Levels:

The strategy has four take-profit levels to gradually lock in profits:

- Level 1 (3%): 25% of the position is closed at a 3% profit.

- Level 2 (8%): 20% of the position is closed at an 8% profit.

- Level 3 (14%): 15% of the position is closed at a 14% profit.

- Level 4 (21%): 10% of the position is closed at a 21% profit.

Adjusting these take-profit levels affects how quickly profits are realized:

- Lower take-profit levels: Capture gains more quickly, reducing risk but potentially cutting off larger profits.

- Higher take-profit levels: Let trades run longer, aiming for bigger gains but increasing the risk of price reversals before profits are locked in.

🔶 Hold Days (20 bars):

The strategy automatically closes the position after 20 bars if none of the take-profit levels are hit. This feature prevents trades from being held indefinitely, especially if market conditions are stagnant. Adjusting this:

- Shorter hold periods: Reduce the duration of exposure, minimizing risks from market changes but potentially closing trades too early.

- Longer hold periods: Allow trades to stay open longer, increasing the chance for mean reversion but also increasing exposure to unfavorable market conditions.

By understanding how these default settings affect the strategy’s performance, traders can optimize the Bitcoin CME-Spot Bollinger Bands Strategy to their preferences, adapting it to different market environments and risk tolerances.

Multi-Step FlexiSuperTrend - Indicator [presentTrading]This version of the indicator is built upon the foundation of a strategy version published earlier. However, this indicator version focuses on providing visual insights and alerts for traders, rather than executing trades. This one is mostly for @thorcmt.

█ Introduction and How it is Different

The **Multi-Step FlexiSuperTrend Indicator** is a versatile tool designed to provide traders with a highly customizable and flexible approach to trend analysis. Unlike traditional supertrend indicators, which focus on a single factor or threshold, the **FlexiSuperTrend** allows users to define multiple levels of take-profit targets and incorporate different trend normalization methods.

It comes with several advanced customization features, including multi-step take profits, deviation plotting, and trend normalization, making it suitable for both novice and expert traders.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The **Multi-Step FlexiSuperTrend** works by calculating a supertrend based on multiple factors and incorporating oscillations from trend deviations. Here’s a breakdown of how it functions:

🔶 SuperTrend Calculation

At the heart of the indicator is the SuperTrend formula, which dynamically adjusts based on price movements.

🔶 Normalization of Deviations

To enhance accuracy, the **FlexiSuperTrend** calculates multiple deviations from the trend and normalizes them.

🔶 Multi-Step Take Profit Levels

The indicator allows setting up to three take profit levels, which are displayed via price level alerts. lows traders to exit part of their position at various profit intervals.

For more detail, please check the strategy version - Multi-Step-FlexiSuperTrend-Strategy:

and 'FlexiSuperTrend-Strategy'

█ Trade Direction

The **Multi-Step FlexiSuperTrend Indicator** supports both long and short trade directions.

This flexibility allows traders to adapt to trending, volatile, or sideways markets.

█ Usage

To use the **FlexiSuperTrend Indicator**, traders can set up their preferences for the following key features:

- **Trading Direction**: Choose whether to focus on long, short, or both signals.

- **Indicator Source**: The price source to calculate the trend (e.g., close, hl2).

- **Indicator Length**: The number of periods to calculate the ATR and trend (the larger the value, the smoother the trend).

- **Starting and Increment Factor**: These adjust how reactive the trend is to price movements. The starting factor dictates how far the initial trend band is from the price, and the increment factor adjusts subsequent trend deviations.

The indicator then displays buy and sell signals on the chart, along with alerts for each take-profit level.

Local picture

█ Default Settings

The default settings of the **Multi-Step FlexiSuperTrend** are carefully designed to provide an optimal balance between sensitivity and accuracy. Let’s examine these default parameters and their effect on performance:

🔶 Indicator Length (Default: 10)

The **Indicator Length** determines the lookback period for the ATR calculation. A smaller value makes the indicator more reactive to price changes, but may generate more false signals. A longer length smooths the trend and reduces noise but may delay signals.

Effect on performance: Shorter lengths perform better in volatile markets, while longer lengths excel in trending markets.

🔶 Starting Factor (Default: 0.618)

This factor adjusts the starting distance of the SuperTrend from the current price. The smaller the starting factor, the closer the trend is to the price, making it more sensitive. Conversely, a larger factor allows more distance, reducing sensitivity but filtering out false signals.

Effect on performance: A smaller factor provides quicker signals but can lead to frequent false positives. A larger factor generates fewer but more reliable signals.

🔶 Increment Factor (Default: 0.382)

The **Increment Factor** controls how the trend bands adjust as the price moves. It increases the distance of the bands from the price with each iteration.

Effect on performance: A higher increment factor can result in wider stop-loss or trend reversal bands, allowing for longer trends to develop without frequent exits. A lower factor keeps the bands closer to the price and is more suited for shorter-term trades.

🔶 Take Profit Levels (Default: 2%, 8%, 18%)

The default take-profit levels are set at 2%, 8%, and 18%. These values represent the thresholds at which the trader can partially exit their positions. These multi-step levels are highly customizable depending on the trader’s risk tolerance and strategy.

Effect on performance: Lower take-profit levels (e.g., 2%) capture small, quick profits in volatile markets, while higher levels (8%-18%) allow for a more gradual exit in strong trends.

🔶 Normalization Method (Default: None)

The default normalization method is **None**, meaning the deviations are not normalized. However, enabling normalization (e.g., **Max-Min**) can improve the clarity of the indicator’s signals in volatile or choppy markets by smoothing out the noise.

Effect on performance: Using a normalization method can reduce the effect of extreme deviations, making signals more stable and less prone to false positives.

Cumulative Net Money FlowDescription:

Dive into the financial depth of the markets with the "Cumulative Net Money Flow" indicator, designed to provide a comprehensive view of the monetary dynamics in trading. This tool is invaluable for traders and investors seeking to quantify the actual money entering or exiting the market over a specified period.

Features:

Value-Weighted Calculations: This indicator multiplies the trading volume by the price, offering a money flow perspective rather than just counting shares or contracts.

Custom Timeframe Adaptability: Adjust the timeframe to match your trading strategy, whether you are day trading, swing trading, or looking for longer-term trends.

Cumulative Insight: Tracks and accumulates net money flow to highlight overall market sentiment, making it easier to spot trends in capital movement.

Color-Coded Visualization: Displays positive money flow in green and negative money flow in red, providing clear, visual cues about market conditions.

Utility: "Cumulative Net Money Flow" is particularly effective in revealing the strength behind market movements. By understanding whether the money flow is predominantly buying or selling, traders can better align their strategies with market sentiment. This indicator is suited for various asset classes, including stocks, cryptocurrencies, and forex.

DEMA Adaptive DMI [BackQuant]DEMA Adaptive DMI

PLEASE Read the following, knowing what an indicator does at its core before adding it into a system is pivotal. The core concepts can allow you to include it in a logical and sound manner.

Conceptual Foundation and Innovation

The DEMA Adaptive DMI blends the Double Exponential Moving Average (DEMA) with the Directional Movement Index (DMI) to offer a unique approach to trend-following. By applying DEMA to the high and low prices, this indicator refines the traditional DMI calculation, enhancing its responsiveness to price changes. This results in a more adaptive and timely measure of market trends and momentum, providing traders with a more refined tool for capturing directional movements in the market.

Technical Composition and Calculation

At its core, the DEMA Adaptive DMI calculates the DEMA for both the high and low prices over a user-defined period. This dual application of DEMA serves to smooth out price fluctuations while retaining sensitivity to market movements. The DMI is then derived from the changes in these DEMA values, producing a set of plus and minus directional indicators that reflect the prevailing trend. Additionally, an Average Directional Index (ADX) is computed to measure the strength of the trend, with the entire process being dynamically adjusted based on the DEMA calculations.

DEMA Application:

The DEMA is applied to both high and low prices to reduce lag and provide a smoother representation of price action.

Directional Movement Calculation: The DMI is calculated using the smoothed price changes, resulting in plus and minus indicators that accurately reflect market trends.

ADX Calculation:

The ADX is computed to quantify the strength of the trend, offering traders insight into whether the market is trending strongly or is in a phase of consolidation.

Features and User Inputs The DEMA Adaptive DMI offers a range of customizable options to suit different trading styles and market conditions:

DEMA Calculation Period: Users can set the period for the DEMA calculation, allowing for adjustments based on the desired sensitivity.

DMI Length: The length of the DMI calculation can be adjusted, providing flexibility in how trends are measured.

ADX Smoothing Period: The smoothing period for the ADX can be customized to fine-tune the trend strength measurement.

Divergence Detection: Optional divergence detection features allow traders to spot potential reversals based on the DMI and price action.

Visualization options include static high and low levels to mark extreme DMI thresholds, the ability to color bars according to trend direction, and background hues to highlight overbought and oversold conditions.

Practical Applications

The DEMA Adaptive DMI is particularly effective in markets where trend strength and direction are crucial for successful trading. Traders can leverage this indicator to:

Identify Trend Reversals:

Detect potential trend reversals by monitoring the DMI and ADX in conjunction with divergence signals.

Trend Confirmation:

Use the DEMA-based DMI to confirm the strength and direction of a trend, aiding in the timing of entries and exits.

Strategic Positioning:

The indicator's responsiveness allows traders to position themselves effectively in fast-moving markets, reducing the risk of late entries or exits.

Advantages and Strategic Value

By integrating the DEMA with the DMI, this indicator provides a more adaptive and timely measure of market trends. The reduced lag from the DEMA ensures that traders receive signals that are closely aligned with current market conditions, while the dynamic DMI calculation offers a more accurate representation of trend direction and strength. This makes the DEMA Adaptive DMI a valuable tool for traders looking to enhance their trend-following strategies with a focus on precision and adaptability.

Summary and Usage Tips

The DEMA Adaptive DMI is a sophisticated trend-following indicator that combines the benefits of DEMA and DMI into a single, powerful tool. Traders are encouraged to incorporate this indicator into their trading systems for a more nuanced and responsive approach to trend detection and confirmation. Whether used for identifying trend reversals, confirming trend strength, or strategically positioning in the market, the DEMA Adaptive DMI offers a versatile and reliable solution for trend-following strategies.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

Atlantean Bitcoin Weekly Market Condition - Top/Bottom BTC Overview:

The "Atlantean Bitcoin Weekly Market Condition Detector - Top/Bottom BTC" is a specialized TradingView indicator designed to identify significant turning points in the Bitcoin market on a weekly basis. By analyzing long-term and short-term moving averages across two distinct resolutions, this indicator provides traders with valuable insights into potential market bottoms and tops, as well as the initiation of bull markets.

Key Features:

Market Bottom Detection: The script uses a combination of a simple moving average (SMA) and an exponential moving average (EMA) calculated over long and short periods to identify potential market bottoms. When these conditions are met, the script signals a "Market Bottom" label on the chart, indicating a possible buying opportunity.

Bull Market Start Indicator: When the short-term EMA crosses above the long-term SMA, it signals the beginning of a bull market. This is marked by a "Bull Market Start" label on the chart, helping traders to prepare for potential market upswings.

Market Top Detection: The script identifies potential market tops by analyzing the crossunder of long and short-term moving averages. A "Market Top" label is plotted, suggesting a potential selling point.

Customizable Moving Averages Display: Users can choose to display the moving averages used for detecting market tops and bottoms, providing additional insights into market conditions.

How It Works: The indicator operates by monitoring the interactions between the specified moving averages:

Market Bottom: Detected when the long-term SMA (adjusted by a factor of 0.745) crosses over the short-term EMA.

Bull Market Start: Detected when the short-term EMA crosses above the long-term SMA.

Market Top: Detected when the long-term SMA (adjusted by a factor of 2) crosses under the short-term SMA.

These conditions are highlighted on the chart, allowing traders to visualize significant market events and make informed decisions.

Intended Use: This indicator is best used on weekly Bitcoin charts. It’s designed to provide long-term market insights rather than short-term trading signals. Traders can use this tool to identify strategic entry and exit points during major market cycles. The optional display of moving averages can further enhance understanding of market dynamics.

Originality and Utility: Unlike many other indicators, this script not only highlights traditional market tops and bottoms but also identifies the aggressive start of bull markets, offering a comprehensive view of market conditions. The unique combination of adjusted moving averages makes this script a valuable tool for long-term Bitcoin traders.

Disclaimer: The signals provided by this indicator are based on historical data and mathematical calculations. They do not guarantee future market performance. Traders should use this tool as part of a broader trading strategy and consider other factors before making trading decisions. Not financial advice.

Happy Trading!

By Atlantean

Multi-Step FlexiSuperTrend - Strategy [presentTrading]At the heart of this endeavor is a passion for continuous improvement in the art of trading

█ Introduction and How it is Different

The "Multi-Step FlexiSuperTrend - Strategy " is an advanced trading strategy that integrates the well-known SuperTrend indicator with a nuanced and dynamic approach to market trend analysis. Unlike conventional SuperTrend strategies that rely on static thresholds and fixed parameters, this strategy introduces multi-step take profit mechanisms that allow traders to capitalize on varying market conditions in a more controlled and systematic manner.

What sets this strategy apart is its ability to dynamically adjust to market volatility through the use of an incremental factor applied to the SuperTrend calculation. This adjustment ensures that the strategy remains responsive to both minor and major market shifts, providing a more accurate signal for entries and exits. Additionally, the integration of multi-step take profit levels offers traders the flexibility to scale out of positions, locking in profits progressively as the market moves in their favor.

BTC 6hr Long/Short Performance

█ Strategy, How it Works: Detailed Explanation

The Multi-Step FlexiSuperTrend strategy operates on the foundation of the SuperTrend indicator, but with several enhancements that make it more adaptable to varying market conditions. The key components of this strategy include the SuperTrend Polyfactor Oscillator, a dynamic normalization process, and multi-step take profit levels.

🔶 SuperTrend Polyfactor Oscillator

The SuperTrend Polyfactor Oscillator is the heart of this strategy. It is calculated by applying a series of SuperTrend calculations with varying factors, starting from a defined "Starting Factor" and incrementing by a specified "Increment Factor." The indicator length and the chosen price source (e.g., HLC3, HL2) are inputs to the oscillator.

The SuperTrend formula typically calculates an upper and lower band based on the average true range (ATR) and a multiplier (the factor). These bands determine the trend direction. In the FlexiSuperTrend strategy, the oscillator is enhanced by iteratively applying the SuperTrend calculation across different factors. The iterative process allows the strategy to capture both minor and significant trend changes.

For each iteration (indexed by `i`), the following calculations are performed:

1. ATR Calculation: The Average True Range (ATR) is calculated over the specified `indicatorLength`:

ATR_i = ATR(indicatorLength)

2. Upper and Lower Bands Calculation: The upper and lower bands are calculated using the ATR and the current factor:

Upper Band_i = hl2 + (ATR_i * Factor_i)

Lower Band_i = hl2 - (ATR_i * Factor_i)

Here, `Factor_i` starts from `startingFactor` and is incremented by `incrementFactor` in each iteration.

3. Trend Determination: The trend is determined by comparing the indicator source with the upper and lower bands:

Trend_i = 1 (uptrend) if IndicatorSource > Upper Band_i

Trend_i = 0 (downtrend) if IndicatorSource < Lower Band_i

Otherwise, the trend remains unchanged from the previous value.

4. Output Calculation: The output of each iteration is determined based on the trend:

Output_i = Lower Band_i if Trend_i = 1

Output_i = Upper Band_i if Trend_i = 0

This process is repeated for each iteration (from 0 to 19), creating a series of outputs that reflect different levels of trend sensitivity.

Local

🔶 Normalization Process

To make the oscillator values comparable across different market conditions, the deviations between the indicator source and the SuperTrend outputs are normalized. The normalization method can be one of the following:

1. Max-Min Normalization: The deviations are normalized based on the range of the deviations:

Normalized Value_i = (Deviation_i - Min Deviation) / (Max Deviation - Min Deviation)

2. Absolute Sum Normalization: The deviations are normalized based on the sum of absolute deviations:

Normalized Value_i = Deviation_i / Sum of Absolute Deviations

This normalization ensures that the oscillator values are within a consistent range, facilitating more reliable trend analysis.

For more details:

🔶 Multi-Step Take Profit Mechanism

One of the unique features of this strategy is the multi-step take profit mechanism. This allows traders to lock in profits at multiple levels as the market moves in their favor. The strategy uses three take profit levels, each defined as a percentage increase (for long trades) or decrease (for short trades) from the entry price.

1. First Take Profit Level: Calculated as a percentage increase/decrease from the entry price:

TP_Level1 = Entry Price * (1 + tp_level1 / 100) for long trades

TP_Level1 = Entry Price * (1 - tp_level1 / 100) for short trades

The strategy exits a portion of the position (defined by `tp_percent1`) when this level is reached.

2. Second Take Profit Level: Similar to the first level, but with a higher percentage:

TP_Level2 = Entry Price * (1 + tp_level2 / 100) for long trades

TP_Level2 = Entry Price * (1 - tp_level2 / 100) for short trades

The strategy exits another portion of the position (`tp_percent2`) at this level.

3. Third Take Profit Level: The final take profit level:

TP_Level3 = Entry Price * (1 + tp_level3 / 100) for long trades

TP_Level3 = Entry Price * (1 - tp_level3 / 100) for short trades

The remaining portion of the position (`tp_percent3`) is exited at this level.

This multi-step approach provides a balance between securing profits and allowing the remaining position to benefit from continued favorable market movement.

█ Trade Direction

The strategy allows traders to specify the trade direction through the `tradeDirection` input. The options are:

1. Both: The strategy will take both long and short positions based on the entry signals.

2. Long: The strategy will only take long positions.

3. Short: The strategy will only take short positions.

This flexibility enables traders to tailor the strategy to their market outlook or current trend analysis.

█ Usage

To use the Multi-Step FlexiSuperTrend strategy, traders need to set the input parameters according to their trading style and market conditions. The strategy is designed for versatility, allowing for various market environments, including trending and ranging markets.

Traders can also adjust the multi-step take profit levels and percentages to match their risk management and profit-taking preferences. For example, in highly volatile markets, traders might set wider take profit levels with smaller percentages at each level to capture larger price movements.

The normalization method and the incremental factor can be fine-tuned to adjust the sensitivity of the SuperTrend Polyfactor Oscillator, making the strategy more responsive to minor market shifts or more focused on significant trends.

█ Default Settings

The default settings of the strategy are carefully chosen to provide a balanced approach between risk management and profit potential. Here is a breakdown of the default settings and their effects on performance:

1. Indicator Length (10): This parameter controls the lookback period for the ATR calculation. A shorter length makes the strategy more sensitive to recent price movements, potentially generating more signals. A longer length smooths out the ATR, reducing sensitivity but filtering out noise.

2. Starting Factor (0.618): This is the initial multiplier used in the SuperTrend calculation. A lower starting factor makes the SuperTrend bands closer to the price, generating more frequent trend changes. A higher starting factor places the bands further away, filtering out minor fluctuations.

3. Increment Factor (0.382): This parameter controls how much the factor increases with each iteration of the SuperTrend calculation. A smaller increment factor results in more gradual changes in sensitivity, while a larger increment factor creates a wider range of sensitivity across the iterations.

4. Normalization Method (None): The default is no normalization, meaning the raw deviations are used. Normalization methods like Max-Min or Absolute Sum can make the deviations more consistent across different market conditions, improving the reliability of the oscillator.

5. Take Profit Levels (2%, 8%, 18%): These levels define the thresholds for exiting portions of the position. Lower levels (e.g., 2%) capture smaller profits quickly, while higher levels (e.g., 18%) allow positions to run longer for more significant gains.

6. Take Profit Percentages (30%, 20%, 15%): These percentages determine how much of the position is exited at each take profit level. A higher percentage at the first level locks in more profit early, reducing exposure to market reversals. Lower percentages at higher levels allow for a portion of the position to benefit from extended trends.

Market Structure Based Stop LossMarket Structure Based Dynamic Stop Loss

Introduction

The Market Structure Based Stop Loss indicator is a strategic tool for traders designed to be useful in both rigorous backtesting and live testing, by providing an objective, “guess-free” stop loss level. This indicator dynamically plots suggested stop loss levels based on market structure, and the concepts of “interim lows/highs.”

It provides a robust framework for managing risk in both long and short positions. By leveraging historical price movements and real time market dynamics, this indicator helps traders identify quantitatively consistent risk levels while optimizing trade returns.

Legend

This indicator utilizes various inputs to customize its functionality, including "Stop Loss Sensitivity" and "Wick Depth," which dictate how closely the stop loss levels hug the price's highs and lows. The stop loss levels are plotted as lines on the trading chart, providing clear visual cues for position management. As seen in the chart below, this indicator dynamically plots stop loss levels for both long and short positions at every point in time.

A “Stop Loss Table” is also included, in order to enhance precision trading and increase backtesting accuracy. It is customizable in both size and positioning.

Case Study

Methodology

The methodology behind this indicator focuses on the precision placement of stop losses using market structure as a guide. It calculates stop losses by identifying the "lowest close" and the corresponding "lowest low" for long setups, and inversely for short setups. By adjusting the sensitivity settings, traders can tweak the indicator's responsiveness to price changes, ensuring that the stop losses are set with a balance between tight risk control and enough room to avoid premature exits due to market noise. The indicator's ability to adapt to different trading styles and time frames makes it an essential tool for traders aiming for efficiency and effectiveness in their risk management strategies.

An important point to make is the fact that the stop loss levels are always placed within the wicks. This is important to avoid what can be described as a “floating stop loss”. A stop loss placed outside of a wick is susceptible to an outsized degree of slippage. This is because traders always cluster their stop losses at high/low wicks, and a stop loss placed outside of this level will inevitably be caught in a low liquidity cascade or “wash-out.” When price approaches a cluster of stop losses, it is highly probable that you will be stopped out anyway, so it is prudent to attempt to be the trader who gets stopped out first in order to avoid high slippage, and losses above what you originally intended.

// For long positions: stop-loss is slightly inside the lowest wick

float dynamic_SL_Long = lowestClose - (lowestClose - lowestLow) * (1 - WickDepth)

// For short positions: stop-loss is slightly inside the highest wick

float dynamic_SL_Short = highestClose + (highestHigh - highestClose) * (1 - WickDepth)

The percentage depth of the wick in which the stop loss is placed is customisable with the “Wick Depth” variable, in order to customize stop loss strategies around the liquidity of the market a trader is executing their orders in.

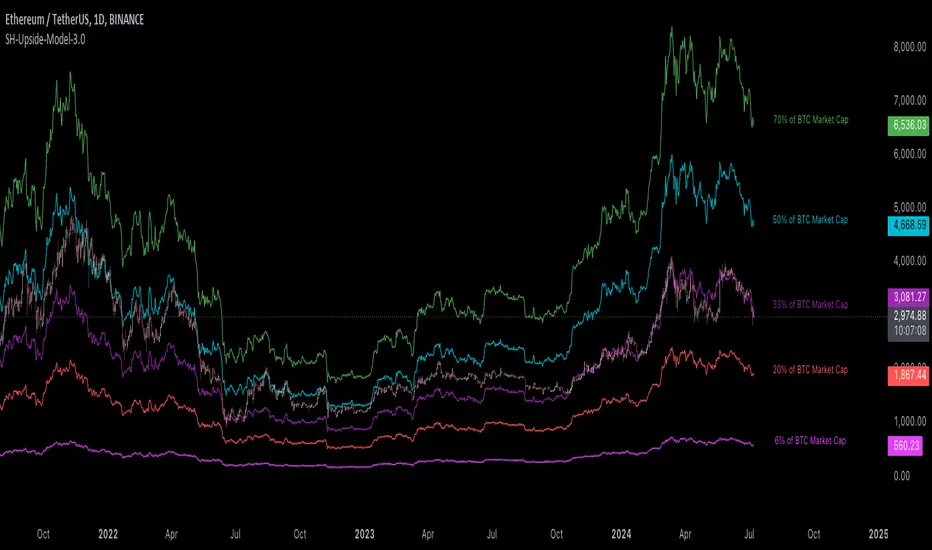

[Suitable Hope] Crypto Upside Model 3.0The "Crypto Upside Model 3.0" indicator dynamically calculates the potential price of any cryptocurrency based on various percentages of Ethereum or Bitcoin's market capitalization.

By fetching and analyzing marketcap data from TradingView sources, it allows traders to visualize potential price targets if their chosen cryptocurrency reaches specific market dominance levels. This tool is designed for daily timeframe analysis and can be used to set informed price expectations and strategic investment goals, providing valuable insights for long-term investment planning.

Why using the Crypto Upside Model 3.0?

Strategic Planning: Helps traders and investors set realistic price targets and investment goals by visualizing potential market cap scenarios.

Informed Decision-Making: Provides a data-driven approach to understanding how a cryptocurrency might perform relative to major assets like Bitcoin and Ethereum.

Customizable Analysis: Allows users to choose different comparison assets (ETH or BTC) and visualize various market cap dominance percentages, offering tailored insights.

Daily Timeframe Focus: Ideal for swing traders and long-term investors who operate on a daily analysis timeframe, providing relevant and actionable data.

Bull Markets: Identify potential price targets if your cryptocurrency's market cap increases significantly.

Bear Markets: Assess how much value could be retained relative to major cryptocurrencies.

Strategic Entry/Exit Points: Use the visualized targets to plan entry or exit points in your trading strategy.

Comparative Advantage

Dynamic Adaptation: Unlike fixed indicators, this tool adapts to any active chart, making it versatile for multiple cryptocurrencies.

Market Cap Insights: Provides a unique perspective by linking price targets to market cap dominance, a critical factor in the crypto market.

User Instructions

Setup: Add the " Upside Model 3.0" indicator to your TradingView chart.

Configuration: Use the input settings to select the comparison cryptocurrency (ETH or BTC) and enable the desired market cap percentage plots.

Analysis: The indicator will display potential price targets based on the selected market cap percentages, providing a visual guide for setting price expectations.

Limitations

Marketcap Data Availability: The indicator relies on marketcap data from TradingView, which may not be available for all cryptocurrencies. If the data is unavailable, the indicator will not function for that asset. This tool is more likely to work with older, established cryptocurrencies, as marketcap data for newer cryptocurrencies may not yet be available.

Daily Timeframe Restriction: The indicator is designed to work exclusively on the daily timeframe, limiting its applicability for intraday trading.

Assumptions of Market Dynamics: The calculations assume a direct correlation between market dominance and price, which may not account for other market dynamics and external factors influencing prices.

Data Accuracy: The accuracy of the indicator depends on the reliability of the data provided by TradingView, which may sometimes experience delays or inaccuracies.

Currently available cryptocurrencies: Bitcoin, Ethereum, Solana, Binance Coin, Cardano, Ripple, Polkadot, Avalanche, Chainlink, Litecoin, Dogecoin, Terra, Uniswap, VeChain, Stellar, Internet Computer, Hedera, Filecoin, Monero, Aave, TRON, NEAR Protocol, Compound, Maker,... For all compatible cryptocurrencies, please consult CRYPTOCAP's documentation.

Final notes

Although various sources ask a payment or user data for similar kind of private indicators, this one is entirely free and open source. "Uncanny" isn't it? I hope this indicator will provide you value. Feel free to leave a message if you have any questions or constructive feedback.

Examples of how I use this indicator

When using ETH's historical price as a reference compared to Bitcoin's marketcap, we can notice that price generally has been held between the +-30% and 50% lines of BTC's marketcap. If history is repeating again, we can expect major resistances around the 50% looking ahead into the future. This for me would be a great area to potentially reduce my ETH spot position.

When using SOL's historical price action, we can notice that the 15% line of ETH's marketcap has been a top in the previous cycle. Today SOL (July 2024), is back at this level. Could this be a top again or could price break this 15% level and head perhaps towards 30% which currently sits around $260? Time will tell.

These are 2 simple example of how I interpret the data. I'm keen to hear what other findings with other pairs you can find.

CryptoLibrary "Crypto"

This Library includes functions related to crytocurrencies and their blockchain

btcBlockReward(t)

Delivers the BTC block reward for a specific date/time

Parameters:

t (int) : Time of the current candle

Returns: blockRewardBtc

ATH/ATL Tracker [LuxAlgo]The ATH/ATL Tracker effectively displays changes made between new All-Time Highs (ATH)/All-Time Lows (ATL) and their previous respective values, over the entire history of available data.

The indicator shows a histogram of the change between a new ATH/ATL and its respective preceding ATH/ATL. A tooltip showing the price made during a new ATH/ATL alongside its date is included.

🔶 USAGE

By tracking the change between new ATHs/ATLs and older ATHs/ATLs, traders can gain insight into market sentiment, breadth, and rotation.

If many stocks are consistently setting new ATHs and the number of new ATHs is increasing relative to old ATHs, it could indicate broad market participation in a rally. If only a few stocks are reaching new ATHs or the number is declining, it might signal that the market's upward momentum is decreasing.

A significant increase in new ATHs suggests optimism and willingness among investors to buy at higher prices, which could be considered a positive sentiment. On the other hand, a decrease or lack of new ATHs might indicate caution or pessimism.

By observing the sectors where stocks are consistently setting new ATHs, users can identify which sectors are leading the market. Sectors with few or no new ATHs may be losing momentum and could be identified as lagging behind the overall market sentiment.

🔶 DETAILS

The indicator's main display is a histogram-style readout that displays the change in price from older ATH/ATLs to Newer/Current ATH/ATLs. This change is determined by the distance that the current values have overtaken the previous values, resulting in the displayed data.

The largest changes in ATH/ATLs from the ticker's history will appear as the largest bars in the display.

The most recent bars (depending on the selected display setting) will always represent the current ATH or ATL values.

When determining ATH & ATL values, it is important to filter out insignificant highs and lows that may happen constantly when exploring higher and lower prices. To combat this, the indicator looks to a higher timeframe than your chart's timeframe in order to determine these more significant ATHs & ATLs.

For Example: If a user was on a 1-minute chart and 5 highs-new highs occur across 5 adjacent bars, this has the potential to show up as 5 new ATHs. When looking at a higher timeframe, 5 minutes, only the highest of the 5 bars will indicate a new ATH. To assist with this, the indicator will display warnings in the dashboard when a suboptimal timeframe is selected as input.

🔹 Dashboard

The dashboard displays averages from the ATH/ATL data to aid in the anticipation and expectations for new ATH/ATLs.

The average duration is an average of the time between each new ATH/ATL, in this indicator it is calculated in "Days" to provide a more comprehensive understanding.

The average change is the average of all change data displayed in the histogram.

🔶 SETTINGS

Duration: The designated higher timeframe to use for filtering out insignificant ATHs & ATLs.

Order: The display order for the ATH/ATL Bars, Options are to display in chronological (oldest to newest) or reverse chronological order (newest to oldest).

Bar Width: Sets the width for each ATH/ATL bar.

Bar Spacing: Sets the # of empty bars in between each ATH/ATL bar.

Dashboard Settings: Parameters for the dashboard's size and location on the chart.

Cosine Kernel Regressions [QuantraSystems]Cosine Kernel Regressions

Introduction

The Cosine Kernel Regressions indicator (CKR) uses mathematical concepts to offer a unique approach to market analysis. This indicator employs Kernel Regressions using bespoke tunable Cosine functions in order to smoothly interpret a variety of market data, providing traders with incredibly clean insights into market trends.

The CKR is particularly useful for traders looking to understand underlying trends without the 'noise' typical in raw price movements. It can serve as a standalone trend analysis tool or be combined with other indicators for more robust trading strategies.

Legend

Fast Trend Signal Line - This is the foreground oscillator, it is colored upon the earliest confirmation of a change in trend direction.

Slow Trend Signal Line - This oscillator is calculated in a similar manner. However, it utilizes a lower frequency within the cosine tuning function, allowing it to capture longer and broader trends in one signal. This allows for tactical trading; the user can trade smaller moves without losing sight of the broader trend.

Case Study

In this case study, the CKR was used alongside the Triple Confirmation Kernel Regression Oscillator (KRO)

Initially, the KRO indicated an oversold condition, which could be interpreted as a signal to enter a long position in anticipation of a price rebound. However, the CKR’s fast trend signal line had not yet confirmed a positive trend direction - suggesting that entering a trade too early and without confirmation could be a mistake.

Waiting for a confirmed positive trend from the CKR proved beneficial for this trade. A few candles after the oversold signal, the CKR's fast trend signal line shifted upwards, indicating a strong upward momentum. This was the optimal entry point suggested by the CKR, occurring after the confirmation of the trend change, which significantly reduced the likelihood of entering during a false recovery or continuation of the downtrend.

This is one of the many uses of the CKR - by timing entries using the fast signal line , traders could avoid unnecessary losses by preventing premature entries.

Methodology

The methodology behind CKR is a multi-layered approach and utilizes many ‘base’ indicators.

Relative Strength Index

Stochastic Oscillator

Bollinger Band Percent

Chande Momentum Oscillator

Commodity Channel Index

Fisher Transform

Volume Zone Oscillator

The calculated output from each indicator is standardized and scaled before being averaged. This prevents any single indicator from overpowering the resulting signal.

// ╔════════════════════════════════╗ //

// ║ Scaling/Range Adjustment ║ //

// ╚════════════════════════════════╝ //

RSI_ReScale (_res ) => ( _res - 50 ) * 2.8

STOCH_ReScale (_stoch ) => ( _stoch - 50 ) * 2

BBPCT_ReScale (_bbpct ) => ( _bbpct - 0.5 ) * 120

CMO_ReScale (_chandeMO ) => ( _chandeMO * 1.15 )

CCI_ReScale (_cci ) => ( _cci / 2 )

FISH_ReScale (_fish1 ) => ( _fish1 * 30 )

VZO_ReScale (_VP, _TV ) => (_VP / _TV) * 110

These outputs are then fed into a customized cosine kernel regression function, which smooths the data, and combines all inputs into a single coherent output.

// ╔════════════════════════════════╗ //

// ║ COSINE KERNEL REGRESSIONS ║ //

// ╚════════════════════════════════╝ //

// Define a function to compute the cosine of an input scaled by a frequency tuner

cosine(x, z) =>

// Where x = source input

// y = function output

// z = frequency tuner

var y = 0.

y := math.cos(z * x)

Y

// Define a kernel that utilizes the cosine function

kernel(x, z) =>

var y = 0.

y := cosine(x, z)

math.abs(x) <= math.pi/(2 * z) ? math.abs(y) : 0. // cos(zx) = 0

// The above restricts the wave to positive values // when x = π / 2z

The tuning of the regression is adjustable, allowing users to fine-tune the sensitivity and responsiveness of the indicator to match specific trading strategies or market conditions. This robust methodology ensures that CKR provides a reliable and adaptable tool for market analysis.

Bitcoin Futures vs. Spot Tri-Frame - Strategy [presentTrading]Prove idea with a backtest is always true for trading.

I developed and open-sourced it as an educational material for crypto traders to understand that the futures and spot spread may be effective but not be as effective as they might think. It serves as an indicator of sentiment rather than a reliable predictor of market trends over certain periods. It is better suited for specific trading environments, which require further research.

█ Introduction and How it is Different

The "Bitcoin Futures vs. Spot Tri-Frame Strategy" utilizes three different timeframes to calculate the Z-Score of the spread between BTC futures and spot prices on Binance and OKX exchanges. The strategy executes long or short trades based on composite Z-Score conditions across the three timeframes.

The spread refers to the difference in price between BTC futures and BTC spot prices, calculated by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges.

BTCUSD 1D L/S Performance

█ Strategy, How It Works: Detailed Explanation

🔶 Calculation of the Spread

The spread is the difference in price between BTC futures and BTC spot prices. The strategy calculates the spread by taking a weighted average of futures prices from multiple exchanges (Binance and OKX) and subtracting a weighted average of spot prices from the same exchanges. This spread serves as the primary metric for identifying trading opportunities.

Spread = Weighted Average Futures Price - Weighted Average Spot Price

🔶 Z-Score Calculation

The Z-Score measures how many standard deviations the current spread is from its historical mean. This is calculated for each timeframe as follows:

Spread Mean_tf = SMA(Spread_tf, longTermSMA)

Spread StdDev_tf = STDEV(Spread_tf, longTermSMA)

Z-Score_tf = (Spread_tf - Spread Mean_tf) / Spread StdDev_tf

Local performance

🔶 Composite Entry Conditions

The strategy triggers long and short entries based on composite Z-Score conditions across all three timeframes:

- Long Condition: All three Z-Scores must be greater than the long entry threshold.

Long Condition = (Z-Score_tf1 > zScoreLongEntryThreshold) and (Z-Score_tf2 > zScoreLongEntryThreshold) and (Z-Score_tf3 > zScoreLongEntryThreshold)

- Short Condition: All three Z-Scores must be less than the short entry threshold.

Short Condition = (Z-Score_tf1 < zScoreShortEntryThreshold) and (Z-Score_tf2 < zScoreShortEntryThreshold) and (Z-Score_tf3 < zScoreShortEntryThreshold)

█ Trade Direction

The strategy allows the user to specify the trading direction:

- Long: Only long trades are executed.

- Short: Only short trades are executed.

- Both: Both long and short trades are executed based on the Z-Score conditions.

█ Usage

The strategy can be applied to BTC or Crypto trading on major exchanges like Binance and OKX. By leveraging discrepancies between futures and spot prices, traders can exploit market inefficiencies. This strategy is suitable for traders who prefer a statistical approach and want to diversify their timeframes to validate signals.

█ Default Settings

- Input TF 1 (60 minutes): Sets the first timeframe for Z-Score calculation.

- Input TF 2 (120 minutes): Sets the second timeframe for Z-Score calculation.

- Input TF 3 (180 minutes): Sets the third timeframe for Z-Score calculation.

- Long Entry Z-Score Threshold (3): Defines the threshold above which a long trade is triggered.

- Short Entry Z-Score Threshold (-3): Defines the threshold below which a short trade is triggered.

- Long-Term SMA Period (100): The period used to calculate the simple moving average for the spread.

- Use Hold Days (true): Enables holding trades for a specified number of days.

- Hold Days (5): Number of days to hold the trade before exiting.

- TPSL Condition (None): Defines the conditions for taking profit and stop loss.

- Take Profit (%) (30.0): The percentage at which the trade will take profit.

- Stop Loss (%) (20.0): The percentage at which the trade will stop loss.

By fine-tuning these settings, traders can optimize the strategy to suit their risk tolerance and trading style, enhancing overall performance.

Crypto Realized Profits/Losses Extremes [AlgoAlpha]🌟🚀 Introducing the Crypto Realized Profits/Losses Extremes Indicator by AlgoAlpha 🚀🌟

Unlock the potential of cryptocurrency markets with our cutting-edge On-Chain Pine Script™ indicator, designed to highlight extreme realized profit and loss zones! 🎯📈

Key Features:

✨ Realized Profits/Losses Calculation: Uses real-time data from the blockchain to monitor profit and loss realization events.

📊 Multi-Crypto Compatibility: The Indicator is compatible on other Crypto tickers besides Bitcoin.

⚙️ Customizable Sensitivity: Adjust the look-back period, normalization period, and deviation thresholds to tailor the indicator to your trading style.

🎨 Visual Enhancements: Choose from a variety of colors for up and down trends, and toggle extreme profit/loss overlay for easy viewing.

🔔 Integrated Alerts: Set up alerts for high and extreme profit or loss conditions, helping you stay ahead of significant market movements.

🔍 How to Use:

🛠 Add the Indicator: Add the indicator to favorites. Customize settings like period lengths and deviation thresholds according to your needs.

📊 Market Analysis: Monitor the main oscillator and the bands to understand current profit and loss extremes in the market. When the oscillator is at the upper band, this means that the market is doing really well and traders/investors will be likely to take profit and cause a reversal. The opposite is true when the oscillator reaches the lower band. The main oscillator can also be used for trend analysis.

🔔 Set Alerts: Configure alerts to notify you when the market enters a zone of high profit or loss, or during trend changes, enabling timely decisions without constant monitoring.

How It Works:

The indicator calculates a normalized area under the RSI curve applied on on-chain data regarding the number of wallets in profit. It employs a custom "src" variable that aggregates data from the blockchain about profit and loss addresses, adapting to intraday or longer timeframes as needed. The main oscillator plots this normalized area, while the upper and lower bands are plotted based on a deviation metric to identify extreme conditions. Colored fills between these bands visually denote these zones. For interaction, the indicator plots bubbles for extreme profits or losses and provides optional bar coloring to reflect the current market trend.

🚀💹 Enjoy a comprehensive, customizable, and visually engaging tool that helps you stay ahead in the fast-paced crypto market!

Crypto Liquidation Heatmap [LuxAlgo]The Crypto Liquidation Heatmap tool offers real-time insights into the liquidations of the top cryptocurrencies by market capitalization, presenting the current state of the market in a visually accessible format. Assets are sorted in descending order, with those experiencing the highest liquidation values placed at the top of the heatmap.

Additional details, such as the breakdown of long and short liquidation values and the current price of each asset, can be accessed by hovering over individual boxes.

🔶 USAGE

The crypto liquidation heatmap tool provides real-time insights into liquidations across all timeframes for the top 29 cryptocurrencies by market capitalization. The assets are visually represented in descending order, prioritizing assets with the highest liquidation values at the top of the heatmap.

Different colors are used to indicate whether long or short liquidations are dominant for each asset. Green boxes indicate that long liquidations surpass short liquidations, while red boxes indicate the opposite, with short liquidations exceeding long liquidations.

Hovering over each box provides additional details, such as the current price of the asset, the breakdown of long and short liquidation values, and the duration for the calculated liquidation values.

🔶 DETAILS

🔹Crypto Liquidation

Crypto liquidation refers to the process of forcibly closing a trader's positions in the cryptocurrency market. It occurs when a trader's margin account can no longer support their open positions due to significant losses or a lack of sufficient margin to meet the maintenance requirements. Liquidations can be categorized as either a long liquidation or a short liquidation.

A long liquidation occurs when long positions are being liquidated, typically due to a sudden drop in the price of the asset being traded. Traders who were bullish on the asset and had opened long positions will face losses as the market moves against them.

On the other hand, a short liquidation occurs when short positions are being liquidated, often triggered by a sudden spike in the price of the asset. Traders who were bearish on the asset and had opened short positions will face losses as the market moves against them.

🔹Liquidation Data

It's worth noting that liquidation data is not readily available on TradingView. However, we recognize the close correlation between liquidation data, trading volumes, and asset price movements. Therefore, this script analyzes accessible data sources, extracts necessary information, and offers an educated estimation of liquidation data. It's important to emphasize that the presented data doesn't reflect precise quantitative values of liquidations. Traders and analysts should instead focus on observing changes over time and identifying correlations between liquidation data and price movements.

🔶 SETTINGS

🔹Cryptocurrency Asset List

It is highly recommended to select instruments from the same exchange with the same currency to maintain proportional integrity among the chosen assets, as different exchanges may have varying trading volumes.

Supported currencies include USD, USDT, USDC, USDP, and USDD. Remember to use the same currency when selecting assets.

List of Crypto Assets: The default options feature the top 29 cryptocurrencies by market capitalization, currently listed on the Binance Exchange. Please note that only crypto assets are supported; any other asset type will not be processed or displayed. To maximize the utility of this tool, it is crucial to heed the warning message displayed above.

🔹Liquidation Heatmap Settings

Position: Specifies the placement of the liquidation heatmap on the chart.

Size: Determines the size of the liquidation heatmap displayed on the chart.

🔶 RELATED SCRIPTS

Liquidations-Meter

Liquidation-Estimates

Liquidation-Levels

Trend Regression Kernel [IkkeOmar]Kernel by @jdehorty huge shoutout to him! This is only an idea for how I use it when trading

All credit for the kernel goes to him, I did not make the kernel! I don't know how to make it more clear.

I use this to assist with top-down analysis.

timeframe I want to trade : timeframe to analyse with white noise and kernel:

1m : 1H

5m : 2H

15m : 4H

1H : 1D

In the chart you see that I have the 1H open, I use the white noise at a "lower setting length" (55 in this case), I change the source of to be the kernel on the higher timeframe. When a new trend is detected by the White noise I wait for price to retest the kernel before building a position. Another case described below:

Here i use the adaptive MCVF (I have made this free for everyone on TradingView) to buy when price is below the kernel while the trend for the white noise is bullish .

Notice that the Kernel is set on the 4H timeframe! The source of the white noise is the kernel!

Here is an example in a bearish trend:

Notice, I am on the 5m chart, kernel uses the 2H chart and the source of the white noise is the kernel.

I use the adaptive MCVF to help me get entries AFTER the first touch of the kernel.

Mandatory code explanation, with respect to the house rules:

Input settings:

Input Settings:

The script provides various input parameters to customize the indicator:

src: The source of price data, defaulted to closing prices.

h, r, x_0: Parameters for Kernel 1.

h2, r2, x_2: Parameters for Kernel 2.

Kernel Regression Functions:

Two functions kernel_regression1 and kernel_regression2 are defined to perform kernel regression calculations.

These functions estimate the trend using the Nadaraya-Watson kernel non-parametric regression method.

They take the source data (_src), the size of the data series (_size), and the lookback window (_h) as inputs.

They iterate over the data series and calculate the weighted sum of the values based on the specified kernel parameters.

The result is divided by the cumulative weight to obtain the estimated value.

Estimations:

The kernel_regression1 and kernel_regression2 functions are called with the respective parameters to estimate trends (yhat1 and yhat2).

Buy and Sell Signals:

Buy and sell signals are generated based on crossover and crossunder conditions between the two trend estimates (yhat1 and yhat2).

buySignal is true when yhat1 crosses above yhat2.

SellSignal is true when yhat1 crosses below yhat2.

Plotting:

The average of the two trend estimates (yhat1 and yhat2) is calculated and plotted.

The color of the plot is determined based on whether yhat1 is greater than yhat2, less than yhat2, or equal to yhat2.

Buy and sell signals are plotted using triangle shapes below and above bars, respectively.

Alerts:

Alert conditions are set based on buy and sell signals. Alerts are triggered when a crossover (long signal) or crossunder (short signal) occurs.

The alerts include information about the signal type, symbol, and price.

It's important to mention that the buy and sell signals from the indicator is very discretionary, I rarely use them, and if I do it's if they are in confluence with a correction i am biased towards or if it has confluence with some of my other systems.

The adaptive MCVF and White noise is free for everyone on TradingView, linked below:)

Huge shoutout to @jdehorty, original kernel below:

Bitcoin Leverage Sentiment - Strategy [presentTrading]█ Introduction and How it is Different