Composite Trend Trader Module [BackQuant]Composite Trend Trader Module

Overview and Purpose

The Composite Trend Trader Module (CTM) is an invite-only Pine Script indicator designed to provide traders with a comprehensive tool for trend-following, dip-buying, and market strength assessment. By integrating multiple market data inputs—price momentum, volatility, volume, and statistical baselines—the CTM generates actionable outputs for trend identification, swing trade entries, and dip-buying opportunities. The indicator is intended for traders seeking a systematic approach to market analysis with customizable settings, while maintaining simplicity in its user interface. As a closed-source script, the underlying calculations remain proprietary, but this description outlines its functionality, features, and practical applications in trading.

Visual Components

The CTM provides the following visual elements on the chart:

• Signal Spine – A colored line (default 25-period weighted moving average) that reflects the dominant trend—green for bullish, red for bearish, and grey for neutral or transitional periods.

• Swing Triggers – Unicode markers ("𝕃" for long, "𝕊" for short) appear below or above bars when the trend shifts, signaling potential swing trade entries.

• Dip-Hunter Signals – Green arrows mark dip-buying opportunities, accompanied by faint green background highlights and forward-projecting entry lines for precise entry levels.

• Heat Meter – A horizontal strip at the bottom of the chart, graded from -50 (overheated) to +50 (deep dip), visually indicates the strength of dip conditions using a red-to-green gradient.

Core Features

The CTM comprises several components that work together to deliver a cohesive trading framework. Below is a detailed explanation of each, without disclosing proprietary calculations.

1. Universal Trend Tracking (UTT)

The UTT combines multiple momentum and statistical indicators into a single composite score ranging from -1 to +1. This score is derived from:

• Price-based momentum metrics.

• Volatility-adjusted thresholds.

• Statistical measures of price deviation and market structure.

When the UTT score exceeds +0.2, the market is considered in an actionable uptrend; below -0.2, a downtrend is identified. Values between these thresholds indicate a neutral or choppy market, helping traders avoid low-probability setups during consolidation.

2. Signal Spine

The signal spine is a 25-period weighted moving average of price, colored according to the UTT score (green for bullish, red for bearish, grey for neutral). This line serves as a visual anchor for tracking the prevailing trend and highlights regime changes in real time, enabling traders to align their strategies with market direction.

3. Swing Triggers (𝕃/𝕊)

Swing trade signals are generated when the UTT crosses the zero line, indicating a shift in market regime. A "𝕃" marker appears below the bar for a bullish crossover (potential long entry), and a "𝕊" marker appears above for a bearish crossover (potential short entry). These signals incorporate volatility-adaptive thresholds to minimize false triggers during low-volatility periods, improving reliability compared to traditional moving-average crossovers.

4. Dip-Hunter Engine

The Dip-Hunter subsystem identifies high-probability dip-buying opportunities by evaluating five conditions:

• Dip Magnitude – The price must have fallen by a user-defined percentage (default 2%) from a recent swing high, calculated over a specified lookback period (default 5 bars).

• Volume Burst – Current volume must exceed the average volume over a user-defined lookback (default 65 bars) by a specified multiplier (default 2x).

• Volatility Spike – The intraday range or Average True Range (ATR) must exceed a statistical baseline by a user-defined multiplier (default 1.5x).

• Structural Permission – Price must be below a fast Exponential Moving Average (EMA, default 20 periods), and the market structure must be bearish (fast EMA below slow EMA, default 50 periods).

• Trend Filter (Optional) – When enabled, dip signals are only generated if the UTT indicates a bullish trend, preventing trades against a bearish macro environment.

When these conditions align, the Dip-Hunter plots a green arrow, highlights the candle background, and draws a forward-projecting horizontal line at a user-selected price level (Low, Close, or calculated dip percentage).

5. Strength Score and Heat Meter

Each bar is assigned a strength score (0 to 5, or -50 to +50 when scaled for the heat meter) based on the following criteria:

• +1 for meeting the dip threshold.

• +1 for a volume spike.

• +1 for a volume momentum spike (based on rate-of-change).

• +1 for a confirmed volatility spike.

• +1 if price is below the fast EMA.

• +2 if the macro trend filter is bullish (when enabled).

The heat meter visualizes this score as a pointer on a red-to-green gradient strip, enabling traders to quickly assess the intensity of dip conditions and prioritize high-quality setups.

6. Entry-Line Generator

For each dip signal, the CTM draws a forward-projecting horizontal line to mark potential entry levels. Traders can configure:

• The price level for the line (Low, Close, or exact dip percentage).

• The duration of the line (default 100 bars).

• A minimum gap between signals (default 5 bars) to prevent overlapping lines during clustered events.

These lines serve as visual guides for setting limit orders or stop-loss levels.

7. Alerts

The CTM includes seven pre-configured alert conditions to support automated workflows:

• CTM Long/Short – Triggered on bullish or bearish UTT zero-line crossovers for swing trades.

• Market Overheated – Activates when the strength score falls below -40, indicating potential exhaustion.

• Close to Dip – Signals when the strength score reaches 0.6, suggesting an impending dip opportunity.

• Dip Confirmed – Fires on the first bar meeting all dip conditions.

• Dip Active – Triggers while dip conditions remain valid.

• Dip Fading – Activates when the strength score crosses below 0.5, indicating a weakening dip.

• Trend-Blocked – Alerts when dip conditions are met but blocked by the trend filter.

These alerts can be routed to brokers or trading bots for seamless execution.

"CPM Long Signal {{exchange}}:{{ticker}}")

"CPM Short Signal {{exchange}}:{{ticker}}")

"Market overheated {{ticker}}")

"Close to a dip {{ticker}}")

"Dip confirmed {{ticker}}")

"Dip active {{ticker}}")

"Dip strength fading {{ticker}}")

"Signal blocked by trend filter {{ticker}}")

User Controls

The CTM offers extensive customization to adapt to different trading styles and preferences:

• Signal Settings – Toggle the signal spine, composite score plot, swing triggers, and bar coloring. Adjust line width for visibility.

• Display Settings – Customize bullish, bearish, and neutral colors to match chart templates.

• Dip-Hunter Settings – Configure volume lookback, spike multipliers, EMA periods, volatility thresholds, dip percentage, and lookback bars.

• Trend Filter – Enable or disable the requirement for a bullish UTT before dip signals are generated.

• Strength & Meter – Toggle bar coloring based on the strength score, adjust the number of meter cells (default 60), and select meter position (e.g., bottom-center).

• Entry Settings – Control entry line visibility, length, and price source (Low, Close, or dip percentage).

Trading Applications

The CTM supports multiple trading strategies, each leveraging its outputs for specific market conditions:

• Trend-Ride Mode – Trade in the direction of the signal spine. Enter long positions on the first "𝕃" marker in a green (bullish) regime, and scale out when the UTT returns to grey (neutral). This is ideal for trend-following traders seeking to capture sustained moves, with the first signal in a new trend regime offering high statistical expectancy.

• Forced Dip Entries – Enable the trend filter and focus on dip signals (green arrows). Place limit orders at the entry line, set stops below the line, and target the midpoint of the prior value area (e.g., using support/resistance levels). This suits mean-reversion traders aiming to buy dips in bullish trends, with clear risk management via entry lines.

• Scalp Confirmation – Hide the signal spine and use bar coloring to identify short-term momentum. Green bars indicate broad buying pressure, while red bars warn against long scalps in oversold conditions. This is useful for intraday scalpers seeking confirmation of momentum before entering trades.

• Event Guardrails – Avoid trading when the heat meter is below -40 before major economic releases (e.g., FOMC, CPI), as spreads and slippage may widen. This enhances risk management by flagging high-risk periods during macroeconomic events.

• Multi-Timeframe Analysis – Apply the CTM on a daily timeframe in a secondary pane and a lower timeframe (e.g., hourly) on the primary chart. Trade only when both timeframes align (e.g., both in bullish regimes). This increases conviction for swing or position traders by confirming trend alignment across timeframes.

Frequently Asked Questions

• How does the CTM differ from a moving-average ribbon? The CTM integrates multiple momentum, volatility, and statistical indicators, using adaptive thresholds and proprietary calculations to respond faster to structural changes while filtering noise more effectively than traditional dual-EMA systems.

• Can the underlying formulas be accessed? No, the script is closed-source, and calculations are protected to preserve intellectual property. Users receive all outputs, alerts, and customizable parameters.

• Does the indicator repaint? No, all calculations use confirmed historical data without look-ahead bias. Entry lines are static from the signal bar.

• Which markets is it suitable for? The CTM is optimized for equities, futures, and cryptocurrencies. Adjust dip percentage and volume multipliers for low-liquidity markets.

• What about latency? The script uses efficient Pine Script functions and lightweight loops, ensuring minimal performance impact.

Limitations and Best Practices

• Market-Specific Tuning – Thinly traded markets may require adjustments to dip percentage and volume thresholds to avoid excessive signals.

• Complementary Tools – Combine the CTM with price action, support/resistance levels, or order flow analysis to confirm signals and avoid over-reliance on the indicator.

• Event Risk – Be cautious during high-impact news events, as volatility spikes may trigger signals that are quickly reversed.

• Trend Filter Use – Enabling the trend filter reduces false dip signals in bearish markets but may delay entries in rapidly reversing markets.

Conclusion

The Composite Trend Trader Module consolidates trend-following, dip-buying, and strength assessment into a single, customizable indicator. By providing clear visual cues, actionable alerts, and flexible settings, it equips traders with a robust framework for navigating various market conditions. While the proprietary calculations remain protected, the CTM’s outputs enable traders to make informed decisions, align strategies with market regimes, and manage risk effectively. Use it as a strategic tool alongside sound risk management and complementary analysis for optimal results.

Chart

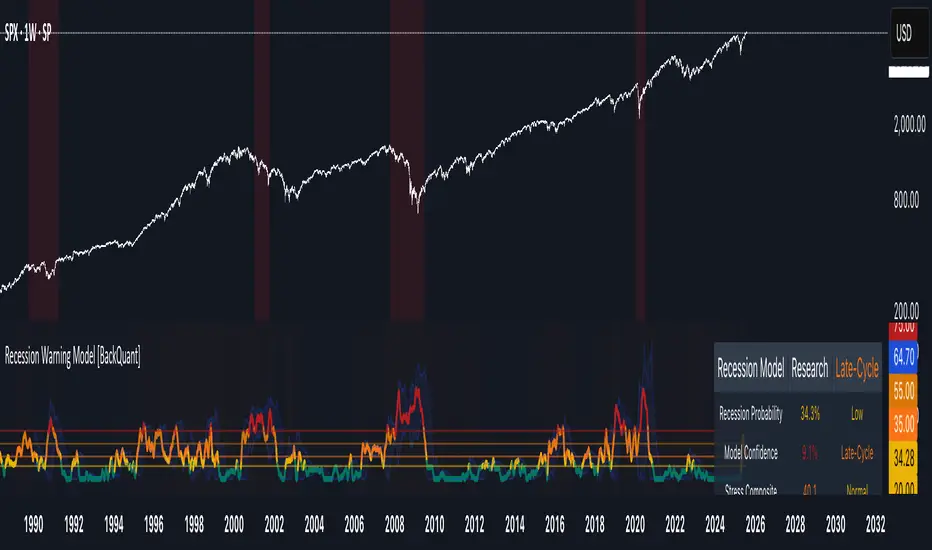

Recession Warning Model [BackQuant]Recession Warning Model

Overview

The Recession Warning Model (RWM) is a Pine Script® indicator designed to estimate the probability of an economic recession by integrating multiple macroeconomic, market sentiment, and labor market indicators. It combines over a dozen data series into a transparent, adaptive, and actionable tool for traders, portfolio managers, and researchers. The model provides customizable complexity levels, display modes, and data processing options to accommodate various analytical requirements while ensuring robustness through dynamic weighting and regime-aware adjustments.

Purpose

The RWM fulfills the need for a concise yet comprehensive tool to monitor recession risk. Unlike approaches relying on a single metric, such as yield-curve inversion, or extensive economic reports, it consolidates multiple data sources into a single probability output. The model identifies active indicators, their confidence levels, and the current economic regime, enabling users to anticipate downturns and adjust strategies accordingly.

Core Features

- Indicator Families : Incorporates 13 indicators across five categories: Yield, Labor, Sentiment, Production, and Financial Stress.

- Dynamic Weighting : Adjusts indicator weights based on recent predictive accuracy, constrained within user-defined boundaries.

- Leading and Coincident Split : Separates early-warning (leading) and confirmatory (coincident) signals, with adjustable weighting (default 60/40 mix).

- Economic Regime Sensitivity : Modulates output sensitivity based on market conditions (Expansion, Late-Cycle, Stress, Crisis), using a composite of VIX, yield-curve, financial conditions, and credit spreads.

- Display Options : Supports four modes—Probability (0-100%), Binary (four risk bins), Lead/Coincident, and Ensemble (blended probability).

- Confidence Intervals : Reflects model stability, widening during high volatility or conflicting signals.

- Alerts : Configurable thresholds (Watch, Caution, Warning, Alert) with persistence filters to minimize false signals.

- Data Export : Enables CSV output for probabilities, signals, and regimes, facilitating external analysis in Python or R.

Model Complexity Levels

Users can select from four tiers to balance simplicity and depth:

1. Essential : Focuses on three core indicators—yield-curve spread, jobless claims, and unemployment change—for minimalistic monitoring.

2. Standard : Expands to nine indicators, adding consumer confidence, PMI, VIX, S&P 500 trend, money supply vs. GDP, and the Sahm Rule.

3. Professional : Includes all 13 indicators, incorporating financial conditions, credit spreads, JOLTS vacancies, and wage growth.

4. Research : Unlocks all indicators plus experimental settings for advanced users.

Key Indicators

Below is a summary of the 13 indicators, their data sources, and economic significance:

- Yield-Curve Spread : Difference between 10-year and 3-month Treasury yields. Negative spreads signal banking sector stress.

- Jobless Claims : Four-week moving average of unemployment claims. Sustained increases indicate rising layoffs.

- Unemployment Change : Three-month change in unemployment rate. Sharp rises often precede recessions.

- Sahm Rule : Triggers when unemployment rises 0.5% above its 12-month low, a reliable recession indicator.

- Consumer Confidence : University of Michigan survey. Declines reflect household pessimism, impacting spending.

- PMI : Purchasing Managers’ Index. Values below 50 indicate manufacturing contraction.

- VIX : CBOE Volatility Index. Elevated levels suggest market anticipation of economic distress.

- S&P 500 Growth : Weekly moving average trend. Declines reduce wealth effects, curbing consumption.

- M2 + GDP Trend : Monitors money supply and real GDP. Simultaneous declines signal credit contraction.

- NFCI : Chicago Fed’s National Financial Conditions Index. Positive values indicate tighter conditions.

- Credit Spreads : Proxy for corporate bond spreads using 10-year vs. 2-year Treasury yields. Widening spreads reflect stress.

- JOLTS Vacancies : Job openings data. Significant drops precede hiring slowdowns.

- Wage Growth : Year-over-year change in average hourly earnings. Late-cycle spikes often signal economic overheating.

Data Processing

- Rate of Change (ROC) : Optionally applied to capture momentum in data series (default: 21-bar period).

- Z-Score Normalization : Standardizes indicators to a common scale (default: 252-bar lookback).

- Smoothing : Applies a short moving average to final signals (default: 5-bar period) to reduce noise.

- Binary Signals : Generated for each indicator (e.g., yield-curve inverted or PMI below 50) based on thresholds or Z-score deviations.

Probability Calculation

1. Each indicator’s binary signal is weighted according to user settings or dynamic performance.

2. Weights are normalized to sum to 100% across active indicators.

3. Leading and coincident signals are aggregated separately (if split mode is enabled) and combined using the specified mix.

4. The probability is adjusted by a regime multiplier, amplifying risk during Stress or Crisis regimes.

5. Optional smoothing ensures stable outputs.

Display and Visualization

- Probability Mode : Plots a continuous 0-100% recession probability with color gradients and confidence bands.

- Binary Mode : Categorizes risk into four levels (Minimal, Watch, Caution, Alert) for simplified dashboards.

- Lead/Coincident Mode : Displays leading and coincident probabilities separately to track signal divergence.

- Ensemble Mode : Averages traditional and split probabilities for a balanced view.

- Regime Background : Color-coded overlays (green for Expansion, orange for Late-Cycle, amber for Stress, red for Crisis).

- Analytics Table : Optional dashboard showing probability, confidence, regime, and top indicator statuses.

Practical Applications

- Asset Allocation : Adjust equity or bond exposures based on sustained probability increases.

- Risk Management : Hedge portfolios with VIX futures or options during regime shifts to Stress or Crisis.

- Sector Rotation : Shift toward defensive sectors when coincident signals rise above 50%.

- Trading Filters : Disable short-term strategies during high-risk regimes.

- Event Timing : Scale positions ahead of high-impact data releases when probability and VIX are elevated.

Configuration Guidelines

- Enable ROC and Z-score for consistent indicator comparison unless raw data is preferred.

- Use dynamic weighting with at least one economic cycle of data for optimal performance.

- Monitor stress composite scores above 80 alongside probabilities above 70 for critical risk signals.

- Adjust adaptation speed (default: 0.1) to 0.2 during Crisis regimes for faster indicator prioritization.

- Combine RWM with complementary tools (e.g., liquidity metrics) for intraday or short-term trading.

Limitations

- Macro indicators lag intraday market moves, making RWM better suited for strategic rather than tactical trading.

- Historical data availability may constrain dynamic weighting on shorter timeframes.

- Model accuracy depends on the quality and timeliness of economic data feeds.

Final Note

The Recession Warning Model provides a disciplined framework for monitoring economic downturn risks. By integrating diverse indicators with transparent weighting and regime-aware adjustments, it empowers users to make informed decisions in portfolio management, risk hedging, or macroeconomic research. Regular review of model outputs alongside market-specific tools ensures its effective application across varying market conditions.

MP Master VWAP [BackQuant]MP Master VWAP

Overview

MP Master VWAP is an, volume-weighted average price suite. It re-anchors automatically to any time partition you select—Day, Week, Month, Quarter or Year—and builds an adaptive standard-deviation envelope, optional pivot clusters and context-aware candle colouring so you can read balance, imbalance and auction edges in a single glance. We use private methods on calculating key levels, making them adaptive and more responsive. This is not just a plain VWAP.

Key Components

• Anchored VWAP core – The engine resets VWAP the instant a new session for the chosen anchor begins. Separator lines and a live high–low box make those rotations obvious.

• Dynamic sigma bands – Three upper and three lower bands, scaled by real-time standard deviation. 1-σ filters noise, 2-σ marks momentum, 3-σ flags exhaustion.

• Previous-period memory – The prior session’s VWAP and bands stay on-screen in a muted style so you can trade retests of last month’s value without clutter.

• High-precision price labels – VWAP and every active band print their prices on the hard right edge; labels vanish if you want a cleaner chart.

• Pivot package – Choose Traditional, Fibonacci or Camarilla calculations on a Daily, Weekly or Monthly look-back. Levels plot as subtle circles that complement, not compete with, the VWAP map.

• Context candles – Bars tint relative to their location: vivid red above U2, soft red between U1-U2, neutral grey inside value, soft green between L2-L1, vivid green below L2.

Customisation Highlights

Period section

• Anchor reset drop-down

• Toggles for separator lines and period high/low

Band section

• Independent visibility for L1/U1, L2/U2, L3/U3

• Individual multipliers to fit any volatility profile

• Optional real-time price labels

Pivot section

• Three formula choices

• Independent timeframe—mix a Monthly VWAP with Weekly Camarilla for confluence

Visual section

• Separate switches for current vs previous envelopes

• Candle-colour toggle for traders who prefer raw price bars

Colour section

• Full palette selectors to match dark or light themes instantly

Some Potential Ways it can be used:

Mean-reversion fade – Price spikes into U2 or U3 and stalls (especially at a pivot). Fade back toward VWAP; scale out at U1 and VWAP.

Trend continuation – Close above U1 on rising volume; trail a stop behind U1. Mirror setup for shorts under L1.

Breakout validation – Session gaps below previous VWAP but quickly reclaims it. Use the cross-above alert to automate entry and target U1 / U2.

Overnight inventory flush – Globex extremes that tag L2 / U2 often reverse at the cash open; scalp rotations back to VWAP.

Risk framing – Let the gap between VWAP and L2 / U2 dictate position size, keeping reward-to-risk consistent across assets.

Alerts Included

• Cross above / below current VWAP

• Cross first sigma bands (U1 / L1)

• Break above second sigma bands (U2) or below L2

• Touch of third sigma bands (U3 / L3)

• Cross of previous-period VWAP

• New period high or low

Best Practices

• Tighten sigma multipliers on thin-liquidity symbols; widen them on index futures or high-cap crypto.

• Pair the envelope with order-flow or footprint tools to confirm participation at band edges.

• On intraday charts, anchor a higher-timeframe VWAP (e.g., Monthly on a 15-minute) to reveal institutional accumulation.

• Treat the previous period’s VWAP as yesterday’s fair value—gaps that never revisit it often morph into trend days.

Final Notes

MP Master VWAP condenses auction-market theory into one readable overlay: automatic period resets, adaptive deviation bands, historical memory, multi-style pivots and self-explanatory colour coding. You can deploy it on equities, futures, crypto or FX—wherever volume meets time, VWAP remains the benchmark of true price discovery.

Price Widget on ScreenSimple yet useful script, to see the PRICE/CHANGE of the chart you are on. I use it in my 6/8 charts screen, so you can see the graph and the price.

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

Stock Table aiTrendviewProfessional Stock Market Monitoring Table (Pine Script v5)

This indicator is a real-time multi-asset monitoring table designed for professional traders, analysts, and portfolio managers using TradingView. Built with Pine Script v5, it enables users to track up to 10 instruments (stocks, indices, forex pairs, cryptocurrencies, or commodities) in a unified table embedded directly into the chart. It is intended to streamline portfolio monitoring, cross-market analysis, and rapid visual comparison of asset performance.

The core logic of this script involves retrieving live price data through TradingView’s request.security() function for each of the selected symbols. It calculates both absolute price change and percentage price change relative to the previous bar close. This ensures users can see real-time movements in each asset’s price. These calculations are updated at the close of every bar to optimize performance and reduce processing load using the barstate.islast condition.

The display structure is dynamically generated using table.new() and related functions. Internally, the script stores symbol and price data in arrays for efficient processing. Symbols are cleaned to remove exchange prefixes (e.g., "NASDAQ:", "BINANCE:") so only the ticker name is displayed. Based on the selected layout (1 to 5 columns), the table auto-adjusts its row structure to maintain clarity and symmetry. Each cell reflects the ticker symbol, current price, and changes, with conditional formatting applied to indicate price movement direction using green (positive), red (negative), or neutral colors.

Users can customize many visual elements including text size, color themes, transparency, table position, and whether headers are shown. The script includes built-in fallbacks for invalid symbols or empty data, ensuring robustness and uninterrupted performance during live market hours.

Use cases include:

Intraday traders monitoring multiple instruments simultaneously.

Swing traders assessing relative strength and correlation.

Portfolio managers scanning asset performance without switching charts.

Analysts preparing multi-asset presentations or watchlists.

To use the tool:

Paste the Pine Script into the Pine Editor.

Add the script to the chart.

Enter your desired symbols via the input fields.

Customize table position, layout, size, and color to suit your workspace.

This script does not provide trade signals or financial advice. It is purely a market visualization and data presentation tool. All calculations are based on live chart data and are synchronized with the chart’s timeframe.

Disclaimer from aiTrendview:

This script is a visual tool developed for market awareness and comparative observation. It does not constitute financial advice or guarantee trading results. aiTrendview and its affiliates are not responsible for any losses arising from decisions made based on this tool. All trading involves risk, and past performance is not indicative of future results. Always consult with a qualified financial advisor before making trading decisions.

Price Exhaustion Envelope [BackQuant]Price Exhaustion Envelope

Visual preview of the bands:

What it is

The Price Exhaustion Envelope (PEE) is a multi‑factor overextension detector wrapped inside a dynamic envelope framework. It measures how “tired” a move is by blending price stretch, volume surges, momentum and acceleration, plus optional RSI divergence. The result is a composite exhaustion score that drives both on‑chart signals and the adaptive width of three optional envelope bands around a smoothed baseline. When the score spikes above or below your chosen threshold, the script can flag exhaustion, paint candles, tint the background and fire alerts.

How it works under the hood

Exhaustion score

Price component: distance of close from its mean in standard deviation units.

Volume component: normalized volume pressure that highlights unusual participation.

Momentum component: rate of change and acceleration of price, scaled by their own volatility.

RSI divergence (optional): bullish and bearish divergences gently push the score lower or higher.

Mode control: choose Price, Volume, Momentum or Composite. Composite averages the main pieces for a balanced view.

Energy scale (0 to 100)

The composite score is pushed through a logistic transform to create an “energy” value. High energy (above 70 to 80) signals a move that may be running hot, while very low energy (below 20 to 30) points to exhaustion on the downside.

Envelope engine

Baseline: EMA of price over the main lookback length.

Width: base width is standard deviation times a multiplier.

Type selector:

• Static keeps the width fixed.

• Dynamic expands width in proportion to the absolute exhaustion score.

• Adaptive links width to the energy reading so bands breathe with market “heat.”

Smoothing: a short EMA on the width reduces jitter and keeps bands pleasant to trade around.

Band architecture

You can toggle up to three symmetric bands on each side of the baseline. They default to 1.0, 1.6 and 2.2 multiples of the smoothed width. Soft transparent fills create a layered thermograph of extension. The outermost band often maps to true blow‑off extremes.

On‑chart elements

Baseline line that flips color in real time depending on where price sits.

Up to three upper and lower bands with progressive opacity.

Triangle markers at fresh exhaustion triggers.

Tiny warning glyphs at extreme upper or lower breaches.

Optional bar coloring to visually tag exhausted candles.

Background halo when energy > 80 or < 20 for instant context.

A compact info table showing State, Score, Energy, Momentum score and where price sits inside the envelope (percent).

How to use it in trading

Mean reversion plays

When price pierces the outer band and an exhaustion marker prints, look for reversal candles or lower‑timeframe confirmation to fade the move back toward the baseline.

For conservative entries, wait for the composite score to roll back under the threshold or for energy to drop from extreme to neutral.

Set stops just beyond the extreme levels (use extreme_upper and extreme_lower as natural invalidation points). Targets can be the baseline or the opposite inner band.

Trend continuation with smart pullbacks

In strong trends, the first tag of Band 1 or Band 2 against the dominant direction often offers low‑risk continuation entries. Use energy readings: if energy is low on a pullback during an uptrend, a bounce is more likely.

Combine with RSI divergence: hidden bullish divergence near a lower band in an uptrend can be a powerful confirmation.

Breakout filtering

A breakout that occurs while the composite score is still moderate (not exhausted) has a higher chance of follow‑through. Skip signals when energy is already above 80 and price is punching the outer band, as the move may be late.

Watch env_position (Envelope %) in the table. Breakouts near 40 to 60 percent of the envelope are “healthy,” while those at 95 percent are stretched.

Scaling out and risk control

Use exhaustion alerts to trim positions into strength or weakness.

Trail stops just outside Band 2 or Band 3 to stay in trends while letting the envelope expand in volatile phases.

Multi‑timeframe confluence

Run the script on a higher timeframe to locate exhaustion context, then drill down to a lower timeframe for entries.

Opposite signals across timeframes (daily exhaustion vs. 5‑minute breakout) warn you to reduce size or tighten management.

Key inputs to experiment with

Lookback Period: larger values smooth the score and envelope, ideal for swing trading. Shorter values make it reactive for scalps.

Exhaustion Threshold: raise above 2.0 in choppy assets to cut noise, drop to 1.5 for smooth FX pairs.

Envelope Type: Dynamic is great for crypto spikes, Adaptive shines in stocks where volume and volatility wave together.

RSI Divergence: turn off if you prefer a pure price/volume model or if divergence floods the score in your asset.

Alert set included

Fresh upper exhaustion

Fresh lower exhaustion

Extreme upper breach

Extreme lower breach

RSI bearish divergence

RSI bullish divergence

Hook these to TradingView notifications so you get pinged the moment a move hits exhaustion.

Best practices

Always pair exhaustion signals with structure. Support and resistance, liquidity pools and session opens matter.

Avoid blindly shorting every upper signal in a roaring bull market. Let the envelope type help you filter.

Use the table to sanity‑check: a very high score but mid‑range env_position means the band may still be wide enough to absorb more movement.

Backtest threshold combinations on your instrument. Different tickers carry different volatility fingerprints.

Final note

Price Exhaustion Envelope is a flexible framework, not a turnkey system. It excels as a context layer that tells you when the crowd is pressing too hard or when a move still has fuel. Combine it with sound execution tactics, risk limits and market awareness. Trade safe and let the envelope breathe with the market.

Momentum Reversal StrategyBEST USE IN 15MIN TIME FRAME EURUSD / XAUSUD

1. Strategy Overview

This strategy hunts short-term momentum reversals at key levels during high-liquidity sessions.

Timeframes: 5-minute for entries; 15-minute for trend context

Sessions: London for EUR/USD & GBP/USD; New York for XAU/USD

Pairs: EUR/USD, GBP/USD, XAU/USD

Indicators (3 max):

EMA(20) and EMA(50) (close)

MACD (12, 26, 9) histogram

Optional: RSI(14) (for divergence filter)

2. Entry Rules

Trend Filter (15 min):

Long only if EMA20 > EMA50; short only if EMA20 < EMA50.

Price-Action Zone (5 min):

Identify recent swing high/low within past 20 bars.

Draw horizontal support (for longs) or resistance (for shorts).

Indicator Alignment (5 min):

MACD histogram crossing from negative to positive for longs, positive to negative for shorts.

Candle close beyond EMA20 in direction of trade.

Candle Confirmation:

Bullish engulfing or hammer at support for longs; bearish engulfing or shooting star at resistance for shorts.

Entry Execution:

Place market order on candle close that meets all above.

3. Exit Rules

Stop-Loss (SL):

Long: 1.5× ATR(14) below entry candle low.

Short: 1.5× ATR(14) above entry candle high.

Take-Profit (TP):

Set at 2× SL distance (RR 1:2).

Trailing SL:

After price moves 1× SL in profit, trail SL to breakeven.

Partial Booking:

Close 50% at 1× SL (50% of TP), move SL to entry.

Close remaining at full TP.

4. Trade Management

False Signal Filter: Skip trades when RSI(14) > 70 for longs or < 30 for shorts (avoids overbought/oversold extremes).

One Trade at a Time: No multiple positions on same pair.

Session Cutoff: Close any open trade 15 minutes before session end.

5. Risk Parameters

Risk per Trade: 1% of account equity.

Reward Target: ≥2% (1:2 RR) per trade.

Win-Rate Expectancy: ≥75% based on indicator confluence and price-action confirmation.

Elite Display# 😎 Elite Display - Simple Chart Info with Style

**Never lose track of what you're looking at!**

A clean, fun way to display your asset name, timeframe, and daily performance directly on your chart. Created by ** ** for traders who like their charts both informative and stylish.

## 📊 **What it shows:**

- Asset name (BTCUSDT) or description (Bitcoin/TetherUS)

- Current timeframe (1H, 4H, 1D, etc.)

- Daily % change with green/red colors

**Example:** `BTCUSDT | 1H | +2.45%`

## 🎨 **Make it yours:**

- **60+ separator styles** - From classic `|` to fun emojis 🚀💎⚡

- **Mood mode** - Separators react to your performance (😄 for gains, 😢 for losses)

- **Position anywhere** - 9 spots on your chart

- **Custom styling** - Colors, fonts, sizes, bold/italic

## 🎯 **Perfect for:**

- Multi-timeframe analysis (never forget which TF you're on!)

- Taking clean screenshots for social media

- Avoiding "wait, what symbol is this?" moments

- Adding a bit of personality to your workspace

## ⚙️ **Super simple setup:**

1. Add to chart

2. Pick what to show (asset/timeframe/both)

3. Choose your style (classic, fun, or reactive mood)

4. Position it wherever you want

5. Done!

**It's just chart info... but way more fun!** 😊

*Works on all markets: Stocks, Crypto, Forex, Commodities*# 📊 TradingHUD - Your Smart Chart Companion

**Transform your charts with the ultimate context display!** Never lose track of your symbol, timeframe, and performance again. This highly customizable indicator brings personality and clarity to your trading workspace.

## 🚀 **Key Features:**

✅ **5 Display Modes:**

- Asset Name (ticker only)

- Full Description (complete name)

- Both combined

- Timeframe Only

- Daily Variation Only

✅ **60+ Separator Styles in 3 Categories:**

- 🎨 **Classic** (15): Professional symbols (|, •, →, ★, etc.)

- 🎉 **Fun** (20): Colorful objects (🚀, 💎, ⚡, 🎯, 💰, etc.)

- 🎭 **Mood** (40+): Reactive yellow faces!

- 😄 **Happy** (21): 😀😊🥰😎🥳 (for green gains)

- 😢 **Sad** (23): 😢😭🥺😞😩 (for red losses)

✅ **Intelligent Variation Display:**

- Daily % change with smart color coding

- Green/red performance tracking

- Only appears on relevant timeframes (intraday + daily)

- Automatically hidden on weekly/monthly

✅ **Ultimate Customization:**

- 9 positioning options anywhere on chart

- Font families: Default or Monospace

- Bold/italic text formatting

- Custom colors and sizes

- Flexible element ordering

## 🎭 **Mood Mode Magic:**

Watch your separators celebrate wins with 😄🤑🚀 or empathize with losses using 😢😭💸. Toggle this emotional feature on/off anytime!

## 💡 **Perfect For:**

- Multi-timeframe analysis

- Screenshot documentation with context

- Avoiding symbol confusion

- Real-time performance tracking

- Adding personality to professional charts

- Social media trading posts

## ⚙️ **Quick Setup:**

1. Add TradingHUD to your chart

2. Select display mode (Asset/Description/Both/etc.)

3. Choose separator style (Classic/Fun/Mood)

4. Position anywhere you want

5. Customize colors, fonts, and formatting

6. Trade with confidence and style!

## 🎯 **Live Examples:**

- **Classic**: `BTCUSDT | 1H | +2.45%`

- **Fun**: `AAPL 🚀 4H 🚀 -1.23%`

- **Happy Mood**: `Gold 😄 1D 😄 +3.67%`

- **Sad Mood**: `BTC 😢 15min 😢 -5.12%`

**Professional meets personality. Context meets creativity. This is TradingHUD.** 📈✨

*Compatible with all markets: Stocks, Crypto, Forex, Commodities, Indices*

Fibonacci Sequence Moving Average [BackQuant]Fibonacci Sequence Moving Average with Adaptive Oscillator

1. Overview

The Fibonacci Sequence Moving Average indicator is a two‑part trading framework that combines a custom moving average built from the famous Fibonacci number set with a fully featured oscillator, normalisation engine and divergence suite. The moving average half delivers an adaptive trend line that respects natural market rhythms, while the oscillator half translates that trend information into a bounded momentum stream that is easy to read, easy to compare across assets and rich in confluence signals. Everything from weighting logic to colour palettes can be customised, so the tool comfortably fits scalpers zooming into one‑minute candles as well as position traders running multi‑month trend following campaigns.

2. Core Calculation

Fibonacci periods – The default length array is 5, 8, 13, 21, 34. A single multiplier input lets you scale the whole family up or down without breaking the golden‑ratio spacing. For example a multiplier of 3 yields 15, 24, 39, 63, 102.

Component averages – Each period is passed through Simple Moving Average logic to produce five baseline curves (ma1 through ma5).

Weighting methods – You decide how those five values are blended:

• Equal weighting treats every curve the same.

• Linear weighting applies factors 1‑to‑5 so the slowest curve counts five times as much as the fastest.

• Exponential weighting doubles each step for a fast‑reacting yet still smooth line.

• Fibonacci weighting multiplies each curve by its own period value, honouring the spirit of ratio mathematics.

Smoothing engine – The blended average is then smoothed a second time with your choice of SMA, EMA, DEMA, TEMA, RMA, WMA or HMA. A short smoothing length keeps the result lively, while longer lengths create institution‑grade glide paths that act like dynamic support and resistance.

3. Oscillator Construction

Once the smoothed Fib MA is in place, the script generates a raw oscillator value in one of three flavours:

• Distance – Percentage distance between price and the average. Great for mean‑reversion.

• Momentum – Percentage change of the average itself. Ideal for trend acceleration studies.

• Relative – Distance divided by Average True Range for volatility‑aware scaling.

That raw series is pushed through a look‑back normaliser that rescales every reading into a fixed −100 to +100 window. The normalisation window defaults to 100 bars but can be tightened for fast markets or expanded to capture long regimes.

4. Visual Layer

The oscillator line is gradient‑coloured from deep red through sky blue into bright green, so you can spot subtle momentum shifts with peripheral vision alone. There are four horizontal guide lines: Extreme Bear at −50, Bear Threshold at −20, Bull Threshold at +20 and Extreme Bull at +50. Soft fills above and below the thresholds reinforce the zones without cluttering the chart.

The smoothed Fib MA can be plotted directly on price for immediate trend context, and each of the five component averages can be revealed for educational or research purposes. Optional bar‑painting mirrors oscillator polarity, tinting candles green when momentum is bullish and red when momentum is bearish.

5. Divergence Detection

The script automatically looks for four classes of divergences between price pivots and oscillator pivots:

Regular Bullish, signalling a possible bottom when price prints a lower low but the oscillator prints a higher low.

Hidden Bullish, often a trend‑continuation cue when price makes a higher low while the oscillator slips to a lower low.

Regular Bearish, marking potential tops when price carves a higher high yet the oscillator steps down.

Hidden Bearish, hinting at ongoing downside when price posts a lower high while the oscillator pushes to a higher high.

Each event is tagged with an ℝ or ℍ label at the oscillator pivot, colour‑coded for clarity. Look‑back distances for left and right pivots are fully adjustable so you can fine‑tune sensitivity.

6. Alerts

Five ready‑to‑use alert conditions are included:

• Bullish when the oscillator crosses above +20.

• Bearish when it crosses below −20.

• Extreme Bullish when it pops above +50.

• Extreme Bearish when it dives below −50.

• Zero Cross for momentum inflection.

Attach any of these to TradingView notifications and stay updated without staring at charts.

7. Practical Applications

Swing trading trend filter – Plot the smoothed Fib MA on daily candles and only trade in its direction. Enter on oscillator retracements to the 0 line.

Intraday reversal scouting – On short‑term charts let Distance mode highlight overshoots beyond ±40, then fade those moves back to mean.

Volatility breakout timing – Use Relative mode during earnings season or crypto news cycles to spot momentum surges that adjust for changing ATR.

Divergence confirmation – Layer the oscillator beneath price structure to validate double bottoms, double tops and head‑and‑shoulders patterns.

8. Input Summary

• Source, Fibonacci multiplier, weighting method, smoothing length and type

• Oscillator calculation mode and normalisation look‑back

• Divergence look‑back settings and signal length

• Show or hide options for every visual element

• Full colour and line width customisation

9. Best Practices

Avoid using tiny multipliers on illiquid assets where the shortest Fibonacci window may drop under three bars. In strong trends reduce divergence sensitivity or you may see false counter‑trend flags. For portfolio scanning set oscillator to Momentum mode, hide thresholds and colour bars only, which turns the indicator into a heat‑map that quickly highlights leaders and laggards.

10. Final Notes

The Fibonacci Sequence Moving Average indicator seeks to fuse the mathematical elegance of the golden ratio with modern signal‑processing techniques. It is not a standalone trading system, rather a multi‑purpose information layer that shines when combined with market structure, volume analysis and disciplined risk management. Always test parameters on historical data, be mindful of slippage and remember that past performance is never a guarantee of future results. Trade wisely and enjoy the harmony of Fibonacci mathematics in your technical toolkit.

Weighted Multi-Mode Oscillator [BackQuant]Weighted Multi‑Mode Oscillator

1. What Is It?

The Weighted Multi‑Mode Oscillator (WMMO) is a next‑generation momentum tool that turns a dynamically‑weighted moving average into a 0‑100 bounded oscillator.

It lets you decide how each bar is weighted (by volume, volatility, momentum or a hybrid blend) and how the result is normalised (Percentile, Z‑Score or Min‑Max).

The outcome is a self‑adapting gauge that delivers crystal‑clear overbought / oversold zones, divergence clues and regime shifts on any market or timeframe.

2. How It Works

• Dynamic Weight Engine

▪ Volume – emphasises bars with exceptional participation.

▪ Volatility – inverse ATR weighting filters noisy spikes.

▪ Momentum – amplifies strong directional ROC bursts.

▪ Hybrid – equal‑weight blend of the three dimensions.

• Multi‑Mode Smoothing

Choose from 8 MA types (EMA, DEMA, HMA, LINREG, TEMA, RMA, SMA, WMA) plus a secondary smoothing factor to fine‑tune lag vs. responsiveness.

• Normalization Suite

▪ Percentile – rank vs. recent history (context aware).

▪ Z‑Score – standard deviations from mean (statistical extremes).

▪ Min‑Max – scale between rolling high/low (trend friendly).

3. Reading the Oscillator

Zone Default Level Interpretation

Bull > 80 Acceleration; momentum buyers in control

Neutral 20 – 80 Consolidation / no edge

Bear < 20 Exhaustion; sellers dominate

Gradient line/area automatically shades from bright green (strong bull) to deep red (strong bear).

Optional bar‑painting colours price bars the same way for rapid chart scanning.

4. Typical Use‑Cases

Trend Confirmation – Set Weight = Hybrid, Smoothing = EMA. Enter pullbacks only when WMMO > 50 and rising.

Mean Reversion – Weight = Volatility, reduce upper / lower bands to 70 / 30 and fade extremes.

Volume Pulse – Intraday futures: Weight = Volume to catch participation surges before breakout candles.

Divergence Spotting – Compare price highs/lows to WMMO peaks for early reversal clues.

5. Inputs & Styling

Calculation: Source, MA Length, MA Type, Smoothing

Weighting: Volume period & factor, Volatility length, Momentum period

Normalisation: Method, Look‑back, Upper / Lower thresholds

Display: Gradient fills, Threshold lines, Bar‑colouring toggle, Line width & colours

All thresholds, colours and fills are fully customisable inside the settings panel.

6. Built‑In Alerts

WMMO Long – oscillator crosses up through upper threshold.

WMMO Short – oscillator crosses down through lower threshold.

Attach them once and receive push / e‑mail notifications the moment momentum flips.

7. Best Practices

Percentile mode is self‑adaptive and works well across assets; Z‑Score excels in ranges; Min‑Max shines in persistent trends.

Very short MA lengths (< 10) may produce jitter; compensate with higher “Smoothing” or longer look‑backs.

Pair WMMO with structure‑based tools (S/R, trend lines) for higher‑probability trade confluence.

Disclaimer

This script is provided for educational purposes only. It is not financial advice. Always back‑test thoroughly and manage risk before trading live capital.

Custom Portfolio [BackQuant]Custom Portfolio {BackQuant]

Overview

This script turns TradingView into a lightweight portfolio optimizer with institutional-grade analytics and real-time position management capabilities.

Rank up to 15 tickers every bar using a pair-wise relative-strength "league table" that compares each asset against all others through your choice of 12 technical indicators.

Auto-allocate 100% of capital to the single strongest asset and optionally apply dynamic leverage when the aggregate market is trending, with full position tracking and rebalancing logic.

Track performance against a custom buy-and-hold benchmark while watching a fully fledged stats dashboard update in real time, including 15 professional risk metrics.

How it works

Relative-strength engine – Each asset is compared against every other asset with a user-selectable indicator (default: 9/21 EMA cross). The system generates a complete comparison matrix where Asset A vs Asset B, Asset A vs Asset C, and so on, creating strength scores. The summed scores crown a weekly/daily/hourly "winner" that receives the full allocation.

Regime filter – A second indicator applied to TOTAL crypto-market cap (or any symbol you choose) classifies the environment as trending or mean-reverting . Leverage activates only in trending regimes, protecting capital during choppy or declining markets. Choose from indicators like Universal Trend Model, Relative Strength Overlay, Momentum Velocity, or Custom RSI for regime detection.

Capital & position logic – Equity grows linearly when flat and multiplicatively while invested. The system tracks entry prices, calculates returns including leverage adjustments, and handles position transitions seamlessly. Optional intra-trade leverage rebalancing keeps exposure in sync with market conditions, recalculating position sizes as regime conditions change.

Risk & performance analytics – Every confirmed bar records return, drawdown, VaR/CVaR, Sharpe, Sortino, alpha/beta vs your benchmark, gain-to-pain, Calmar, win-rate, Omega ratio, portfolio variance, skewness, and annualized statistics. All metrics render in a professional table for instant inspection with proper annualization based on your selected trading days (252 for traditional markets, 365 for crypto).

Key inputs

Backtest window – Hard-code a start date or let the script run from series' inception with full date range validation.

Asset list (15 slots) – Works with spot, futures, indices, even synthetic spreads (e.g., BYBIT:BTCUSDT.P). The script automatically cleans ticker symbols for display.

Indicator universe – Switch the comparative metric to DEMA, BBPCT, LSMAz adaptive scores, Volatility WMA, DEMA ATR, Median Supertrend, and more proprietary indicators.

With more always being added!

Leverage settings – Max leverage from 1x to any multiple, auto-rebalancing toggle, trend/reversion thresholds with precision controls.

Visual toggles – Show/hide equity curve, rolling drawdown heat-map, daily PnL spikes, position label, advanced metrics table, buy-and-hold comparison equity.

Risk-free rate input – Customize the risk-free rate for accurate Sharpe ratio calculations, supporting both percentage and decimal inputs.

On-chart visuals

Color-coded equity curve with "shadow" offset for depth perception that changes from green (profitable) to red (losing) based on recent performance momentum.

Rolling drawdown strip that fades from light to deep red as losses widen, with customizable maximum drawdown scaling for visual clarity.

Optional daily-return histogram line and zero reference for understanding day-to-day volatility patterns.

Bottom-center table prints the current winning ticker in real time with clean formatting.

Top-right metrics grid updates every bar with 15 key performance indicators formatted to three decimal places for precision.

Benchmark overlay showing buy-and-hold performance of your selected index (default: SPX) for relative performance comparison.

Typical workflow

Add the indicator on a blank chart (overlay off).

Populate ticker slots with the assets you actually trade from your broker's symbol list.

Pick your momentum or mean-reversion metric and a regime filter that matches your market hypothesis.

Set max leverage (1 = spot only) and decide if you want dynamic rebalancing.

Press the little " L " on the price axis to view the equity curve in log scale for better long-term visualization.

Enable the metrics table to monitor Sharpe, Sortino, and drawdown in real time.

Iterate through different asset combinations and indicator settings; compare performance vs buy-and-hold; refine until you find robust parameters.

Who is it for?

Systematic crypto traders looking for a one-click, cross-sectional rotation model with professional risk management.

Portfolio quants who need rapid prototyping without leaving TradingView or exporting to Python/R.

Swing traders wanting an at-a-glance health check of their multi-coin basket with instant position signals.

Fund managers requiring detailed performance attribution and risk metrics for client reporting.

Researchers backtesting momentum and mean-reversion strategies across multiple assets simultaneously.

Important notes & tips

Set Trading Days in a Year to 252 for traditional markets; 365 for 24/7 crypto to ensure accurate annualization.

CAGR and Sharpe assume the backtest start date you choose—short windows can inflate stats, so test across multiple market cycles.

Leverage is theoretical; always confirm your broker's margin rules and account for funding costs not modeled here.

The script is computationally heavy at 15 assets due to the N×N comparison matrix—reduce the list or lengthen the timeframe if you hit execution limits.

Best results often come from mixing assets with different volatility profiles rather than highly correlated instruments.

The regime filter symbol can be changed from CRYPTOCAP:TOTAL to any broad market index that represents your asset universe.

Kase Convergence Divergence [BackQuant]Kase Convergence Divergence

The Kase Convergence Divergence is a sophisticated oscillator designed to measure directional market strength through the lens of volatility-adjusted log return structures. Inspired by Cynthia Kase’s work on statistical momentum and price projection ranges, this unique indicator offers a hybrid framework that merges signal processing, multi-length sweep logic, and adaptive smoothing techniques.

Unlike traditional momentum oscillators like MACD or RSI, which rely on static moving average differences, KCD introduces a dual-process system combining:

Kase-style statistical range projection (via log returns and volatility),

A sweeping loop of lookback lengths for robustness,

First and second derivative modes to capture both velocity and acceleration of price movement.

Core Logic & Computation

The KCD calculation is centered on two volatility-normalized transforms:

KSDI Up: Measures how far the current high has moved relative to a past low, normalized by return volatility.

KSDI Down: Measures how far the current low has moved relative to a past high, also normalized.

For every length in a user-defined sweep range (e.g., 25–35), both KSDI_up and KSDI_dn are computed, and their maximum values across the loop are retained. The difference between these two max values produces the raw signal:

KPO (Kase Projection Oscillator): Measures directional skew.

KCD (Kase Convergence Divergence): Defined as KPO – MA(KPO) — similar in spirit to MACD but structurally different.

Users can choose to visualize either the first derivative (KPO) , or the second derivative (KCD) , depending on market conditions or strategy style.

Key Features

✅ Multi-Length Sweep Logic: Improves signal reliability by aggregating statistical range projections across a set of lookbacks.

✅ Advanced Smoothing Modes: Supports DEMA, HMA, TEMA, LINREG, WMA and more for dynamic adaptation.

✅ Dual Derivative Modes: Choose between speed (first derivative) or smoothness (second derivative) to fit your trading regime.

✅ Color-Encoded Signal Bands: Heatmap-style oscillator coloring enhances visual feedback on trend strength.

✅ Candlestick Painting: Optional bar coloring makes it easy to spot trend shifts on the main chart.

✅ Adaptive Fill Zones: Green and red fills between the oscillator and zero line help distinguish bullish and bearish regimes at a glance.

Practical Applications

📈 Trend Confirmation: Use KCD as a secondary confirmation layer after breakout or pullback entries.

📉 Momentum Shifts: Crossover and crossunder of the zero line highlight potential regime changes.

📊 Strategy Filters: Incorporate into algos to avoid trendless or mean-reverting environments.

🧪 Derivative Switching: Flip between KPO and KCD modes depending on whether you want to measure acceleration or deceleration of price flow.

Alerts & Signals

Two built-in alerts help you catch regime shifts in real time:

Long Signal: Triggered when the selected oscillator crosses above zero.

Short Signal: Triggered when it crosses below zero.

These events can be used to generate entries, exits, or trend validation cues in multi-layer systems.

Conclusion

The Kase Convergence Divergence goes beyond traditional oscillators by offering a volatility-normalized, derivative-aware signal engine with enhanced visual dynamics. Its sweeping architecture and dynamic fill logic make it especially powerful for identifying trending environments, filtering chop, and adding statistical rigor to your trading toolkit.

Whether you’re a discretionary trader seeking precision, or a quant looking to model more robust return structures, KCD offers a creative yet analytically grounded solution.

Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

Bilateral Filter For Loop [BackQuant]Bilateral Filter For Loop

The Bilateral Filter For Loop is an advanced technical indicator designed to filter out market noise and smooth out price data, thus improving the identification of underlying market trends. It employs a bilateral filter, which is a sophisticated non-linear filter commonly used in image processing and price time series analysis. By considering both spatial and range differences between price points, this filter is highly effective at preserving significant trends while reducing random fluctuations, ultimately making it suitable for dynamic trend-following strategies.

Please take the time to read the following:

Key Features

1. Bilateral Filter Calculation:

The bilateral filter is the core of this indicator and works by applying a weight to each data point based on two factors: spatial distance and price range difference. This dual weighting process allows the filter to preserve important price movements while reducing the impact of less relevant fluctuations. The filter uses two primary parameters:

Spatial Sigma (σ_d): This parameter adjusts the weight applied based on the distance of each price point from the current price. A larger spatial sigma means more smoothing, as further away values will contribute more heavily to the result.

Range Sigma (σ_r): This parameter controls how much weight is applied based on the difference in price values. Larger price differences result in smaller weights, while similar price values result in larger weights, thereby preserving the trend while filtering out noise.

The output of this filter is a smoothed version of the original price series, which eliminates short-term fluctuations, helping traders focus on longer-term trends. The bilateral filter is applied over a rolling window, adjusting the level of smoothing dynamically based on both the distance between values and their relative price movements.

2. For Loop Calculation for Trend Scoring:

A for-loop is used to calculate the trend score based on the filtered price data. The loop compares the current value to previous values within the specified window, scoring the trend as follows:

+1 for upward movement (when the filtered value is greater than the previous value).

-1 for downward movement (when the filtered value is less than the previous value).

The cumulative result of this loop gives a continuous trend score, which serves as a directional indicator for the market's momentum. By summing the scores over the window period, the loop provides an aggregate value that reflects the overall trend strength. This score helps determine whether the market is experiencing a strong uptrend, downtrend, or sideways movement.

3. Long and Short Conditions:

Once the trend score has been calculated, it is compared against predefined threshold levels:

A long signal is generated when the trend score exceeds the upper threshold, indicating that the market is in a strong uptrend.

A short signal is generated when the trend score crosses below the lower threshold, signaling a potential downtrend or trend reversal.

These conditions provide clear signals for potential entry points, and the color-coding helps traders quickly identify market direction:

Long signals are displayed in green.

Short signals are displayed in red.

These signals are designed to provide high-confidence entries for trend-following strategies, helping traders capture profitable movements in the market.

4. Trend Background and Bar Coloring:

The script offers customizable visual settings to enhance the clarity of the trend signals. Traders can choose to:

Color the bars based on the trend direction: Bars are colored green for long signals and red for short signals.

Change the background color to provide additional context: The background will be shaded green for a bullish trend and red for a bearish trend. This visual feedback helps traders to stay aligned with the prevailing market sentiment.

These features offer a quick visual reference for understanding the market's direction, making it easier for traders to identify when to enter or exit positions.

5. Threshold Lines for Visual Feedback:

Threshold lines are plotted on the chart to represent the predefined long and short levels. These lines act as clear markers for when the market reaches a critical threshold, triggering a potential buy (long) or sell (short) signal. By showing these threshold lines on the chart, traders can quickly gauge the strength of the market and assess whether the trend is strong enough to warrant action.

These thresholds can be adjusted based on the trader's preferences, allowing them to fine-tune the indicator for different market conditions or asset behaviors.

6. Customizable Parameters for Flexibility:

The indicator offers several parameters that can be adjusted to suit individual trading preferences:

Window Period (Bilateral Filter): The window size determines how many past price values are used to calculate the bilateral filter. A larger window increases smoothing, while a smaller window results in more responsive, but noisier, data.

Spatial Sigma (σ_d) and Range Sigma (σ_r): These values control how sensitive the filter is to price changes and the distance between data points. Fine-tuning these parameters allows traders to adjust the degree of noise reduction applied to the price series.

Threshold Levels: The upper and lower thresholds determine when the trend score crosses into long or short territory. These levels can be customized to better match the trader's risk tolerance or asset characteristics.

Visual Settings: Traders can customize the appearance of the chart, including the line width of trend signals, bar colors, and background shading, to make the indicator more readable and aligned with their charting style.

7. Alerts for Trend Reversals:

The indicator includes alert conditions for real-time notifications when the market crosses the defined thresholds. Traders can set alerts to be notified when:

The trend score crosses the long threshold, signaling an uptrend.

The trend score crosses the short threshold, signaling a downtrend.

These alerts provide timely information, allowing traders to take immediate action when the market shows a significant change in direction.

Final Thoughts

The Bilateral Filter For Loop indicator is a robust tool for trend-following traders who wish to reduce market noise and focus on the underlying trend. By applying the bilateral filter and calculating trend scores, this indicator helps traders identify strong uptrends and downtrends, providing reliable entry signals with minimal market noise. The customizable parameters, visual feedback, and alerting system make it a versatile tool for traders seeking to improve their timing and capture profitable market movements.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

CRYPTO:SOLUSD

Wavelet Filter with Adaptive Upsampling [BackQuant]Wavelet Filter with Adaptive Upsampling