PROTECTED SOURCE SCRIPT

QuantMEX Walk Forward Simulation - RSI

QuantMEX Walk Forward Simulation - RSI

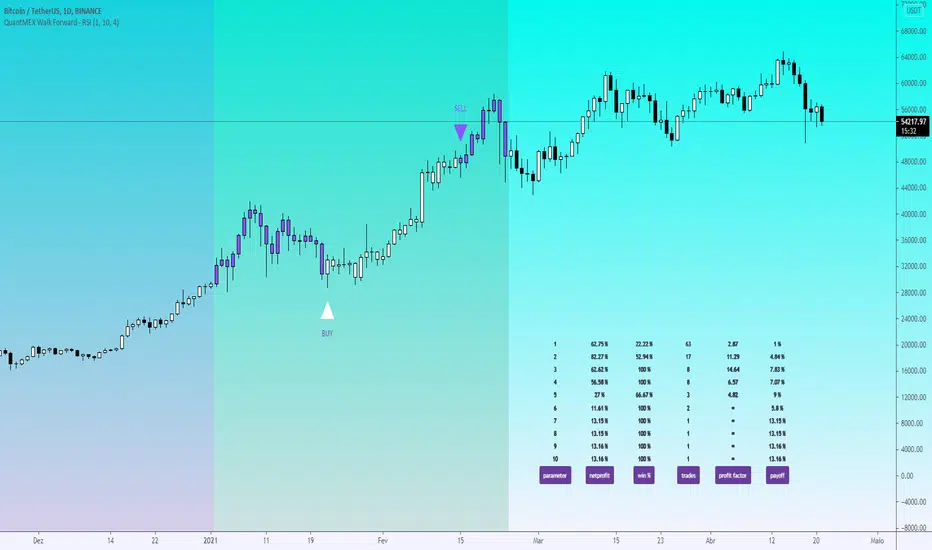

Simulation is one of the most powerful analytical techniques ever created. It is a crucial step in finding effective strategies. The purpose of this indicador is the walf-forward simulation method for the classic Relative Strength Index, adopting a systematic and orderly procedure designed to realistically test a hypothesis based on its functionalities without the need to use the Tradingview backtest. The indicator allows to check the net profit, percentage of winning traders, total trades, profit factor and payoff of several parameters simultaneously.

1) Data segmentation: We divided the historical database with an interval of 8 months. The initial data segments correspond to 75% of the sample and the final data segments correspond to 25% of the sample.

2) Parameters for optimization: Through the oldest data and we found the specific parameters that would have maximized the performance of the risk / return ratio for the RSI. We systematically vary the RSI parameters in order to identify which specific variables would have produced the greatest returns in relation to the risk of loss. Older data segments are known as in-sample data, while newer data segments, not yet used, are known as out-of-sample data.

3) Walk-Forward SIMULATION: The discovered parameters are projected over time for the next and most recent unseen and out-of-sample data segments, which were not included in the research on brute force optimizations carried out in the previous steps.

As a reference, we used the concepts of the classic book "The Evaluation and Optimization of Trading Strategies" by Robert Pardo.

Simulation is one of the most powerful analytical techniques ever created. It is a crucial step in finding effective strategies. The purpose of this indicador is the walf-forward simulation method for the classic Relative Strength Index, adopting a systematic and orderly procedure designed to realistically test a hypothesis based on its functionalities without the need to use the Tradingview backtest. The indicator allows to check the net profit, percentage of winning traders, total trades, profit factor and payoff of several parameters simultaneously.

1) Data segmentation: We divided the historical database with an interval of 8 months. The initial data segments correspond to 75% of the sample and the final data segments correspond to 25% of the sample.

2) Parameters for optimization: Through the oldest data and we found the specific parameters that would have maximized the performance of the risk / return ratio for the RSI. We systematically vary the RSI parameters in order to identify which specific variables would have produced the greatest returns in relation to the risk of loss. Older data segments are known as in-sample data, while newer data segments, not yet used, are known as out-of-sample data.

3) Walk-Forward SIMULATION: The discovered parameters are projected over time for the next and most recent unseen and out-of-sample data segments, which were not included in the research on brute force optimizations carried out in the previous steps.

As a reference, we used the concepts of the classic book "The Evaluation and Optimization of Trading Strategies" by Robert Pardo.

Geschütztes Skript

Dieses Script ist als Closed-Source veröffentlicht. Sie können es kostenlos und ohne Einschränkungen verwenden – erfahren Sie hier mehr.

Haftungsausschluss

Die Informationen und Veröffentlichungen sind nicht als Finanz-, Anlage-, Handels- oder andere Arten von Ratschlägen oder Empfehlungen gedacht, die von TradingView bereitgestellt oder gebilligt werden, und stellen diese nicht dar. Lesen Sie mehr in den Nutzungsbedingungen.

Geschütztes Skript

Dieses Script ist als Closed-Source veröffentlicht. Sie können es kostenlos und ohne Einschränkungen verwenden – erfahren Sie hier mehr.

Haftungsausschluss

Die Informationen und Veröffentlichungen sind nicht als Finanz-, Anlage-, Handels- oder andere Arten von Ratschlägen oder Empfehlungen gedacht, die von TradingView bereitgestellt oder gebilligt werden, und stellen diese nicht dar. Lesen Sie mehr in den Nutzungsbedingungen.